ACC 203 Financial Accounting For Provision And Contingent Liability - DOC

Added on 2020-05-28

4 Pages981 Words105 Views

718 Geelong Street,Melbourne, VIC 30002 January 2018Christopher SampsonManaging Director, Beachlife LtdLevel 7, 927 William Street,Brisbane QLD-4000Dear Christopher SampsonThe email send on 13 November 2017 was acknowledged by me, where accounting issues had been highlighted that needed adequate advice. Amendments or advice on two different type of entries had been required by you. I whole heartedly assure you that my accounting team has all the adequate experience, which is needed for addressing the issues. Moreover, allthe relevant adjustments that needs to be presented to the board are depicted in the letter, which could help in adjusting all the entries and display correct financial condition of your company. I thank you for providing our organisation with the opportunity to help you with your accounting issues and we have provided all the relevant source with the advice, which could help in nullifying the accounting issues.Being a public limited company Beachlife Ltd needs to be comply with all the regulations and acts imposed by regulators such as Corporation Act 2001. In addition, it also needs to comply with Section 296, Section 334 and Section 292, which directly states the preparation of Financial report with all the accounting standard and regulations (Aasb.gov.au 2018). The company also needs to be comply with the AASB standard in drafting the financial report, which has standards and paragraph in addressing different issues of accounting. Hence, the advice needed for the accounting issues will comply with AASB standard and regulation. Moreover, the letter addressed problems regarding warranty expenses and losses, which will incur in immediate future.Identifying the methods in which infringement claim can be recorded in annual report:The infringement claim is mainly identified to have different chance of occurrence in next fiscal year, which could be recoded in form of contingency liability in the current annual report. This infringement claim is mainly a future expenses, which will be conducted by the company due to actions taken in past. According to AASB 137 paragraph 10, accommodationof contingency liability can be conducted by companies in their annual report in grounds of futures expenses (Aasb.gov.au 2018). In paragraph 10, adequate assumption of the expenses is mainly listed, which needs to be conducted by the company in their annual report.

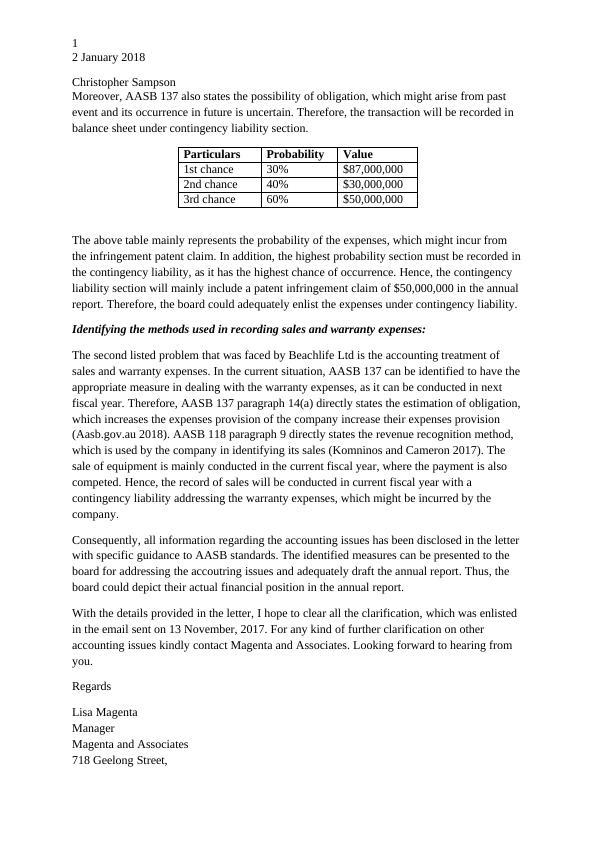

12 January 2018Christopher SampsonMoreover, AASB 137 also states the possibility of obligation, which might arise from past event and its occurrence in future is uncertain. Therefore, the transaction will be recorded in balance sheet under contingency liability section.ParticularsProbabilityValue1st chance30%$87,000,000 2nd chance40%$30,000,000 3rd chance60%$50,000,000 The above table mainly represents the probability of the expenses, which might incur from the infringement patent claim. In addition, the highest probability section must be recorded inthe contingency liability, as it has the highest chance of occurrence. Hence, the contingency liability section will mainly include a patent infringement claim of $50,000,000 in the annual report. Therefore, the board could adequately enlist the expenses under contingency liability.Identifying the methods used in recording sales and warranty expenses:The second listed problem that was faced by Beachlife Ltd is the accounting treatment of sales and warranty expenses. In the current situation, AASB 137 can be identified to have the appropriate measure in dealing with the warranty expenses, as it can be conducted in next fiscal year. Therefore, AASB 137 paragraph 14(a) directly states the estimation of obligation,which increases the expenses provision of the company increase their expenses provision (Aasb.gov.au 2018). AASB 118 paragraph 9 directly states the revenue recognition method, which is used by the company in identifying its sales (Komninos and Cameron 2017). The sale of equipment is mainly conducted in the current fiscal year, where the payment is also competed. Hence, the record of sales will be conducted in current fiscal year with a contingency liability addressing the warranty expenses, which might be incurred by the company.Consequently, all information regarding the accounting issues has been disclosed in the letter with specific guidance to AASB standards. The identified measures can be presented to the board for addressing the accoutring issues and adequately draft the annual report. Thus, the board could depict their actual financial position in the annual report.With the details provided in the letter, I hope to clear all the clarification, which was enlisted in the email sent on 13 November, 2017. For any kind of further clarification on other accounting issues kindly contact Magenta and Associates. Looking forward to hearing from you.RegardsLisa MagentaManagerMagenta and Associates718 Geelong Street,

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Reply to the email correspondence from Magenta and Associates regarding the accoutring issueslg...

|4

|1442

|345

ACC 203 Christopher Sampson Financial Accountinglg...

|5

|1698

|70

Advanced Financial Accounting (AFA) - Assignmentlg...

|7

|1555

|95

ACC 203 Corporations Act 2001 Assignment: Accounting Treatmentslg...

|4

|1124

|71

The Implication of Accounting Treatmentlg...

|6

|1355

|189

Financial Accounting Name of the University Authorlg...

|7

|1405

|37