Cost Accounting Project

VerifiedAdded on 2019/10/08

|12

|1389

|495

Project

AI Summary

This project provides solutions to various cost accounting problems. It covers topics such as budgeting (including income statements and break-even analysis), variance analysis, contribution margin calculations, and different overhead allocation methods (traditional costing and activity-based c...

1

Project

Student Name

College

Project

Student Name

College

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Answer 1..........................................................................................................................................3

Part A...........................................................................................................................................3

Part B...........................................................................................................................................3

Part C...........................................................................................................................................4

Part D...........................................................................................................................................4

Part E...........................................................................................................................................4

Part F............................................................................................................................................5

Answer 2..........................................................................................................................................6

Section 1......................................................................................................................................6

Part A.......................................................................................................................................6

Part B.......................................................................................................................................6

Section 2......................................................................................................................................7

Section 3......................................................................................................................................7

Section 4......................................................................................................................................8

Part A.......................................................................................................................................8

Part B.......................................................................................................................................8

Answer 3..........................................................................................................................................9

Part A...........................................................................................................................................9

Part B...........................................................................................................................................9

Table of Contents

Answer 1..........................................................................................................................................3

Part A...........................................................................................................................................3

Part B...........................................................................................................................................3

Part C...........................................................................................................................................4

Part D...........................................................................................................................................4

Part E...........................................................................................................................................4

Part F............................................................................................................................................5

Answer 2..........................................................................................................................................6

Section 1......................................................................................................................................6

Part A.......................................................................................................................................6

Part B.......................................................................................................................................6

Section 2......................................................................................................................................7

Section 3......................................................................................................................................7

Section 4......................................................................................................................................8

Part A.......................................................................................................................................8

Part B.......................................................................................................................................8

Answer 3..........................................................................................................................................9

Part A...........................................................................................................................................9

Part B...........................................................................................................................................9

3

Part C...........................................................................................................................................9

Part D.........................................................................................................................................10

Part 4..............................................................................................................................................11

Part C...........................................................................................................................................9

Part D.........................................................................................................................................10

Part 4..............................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

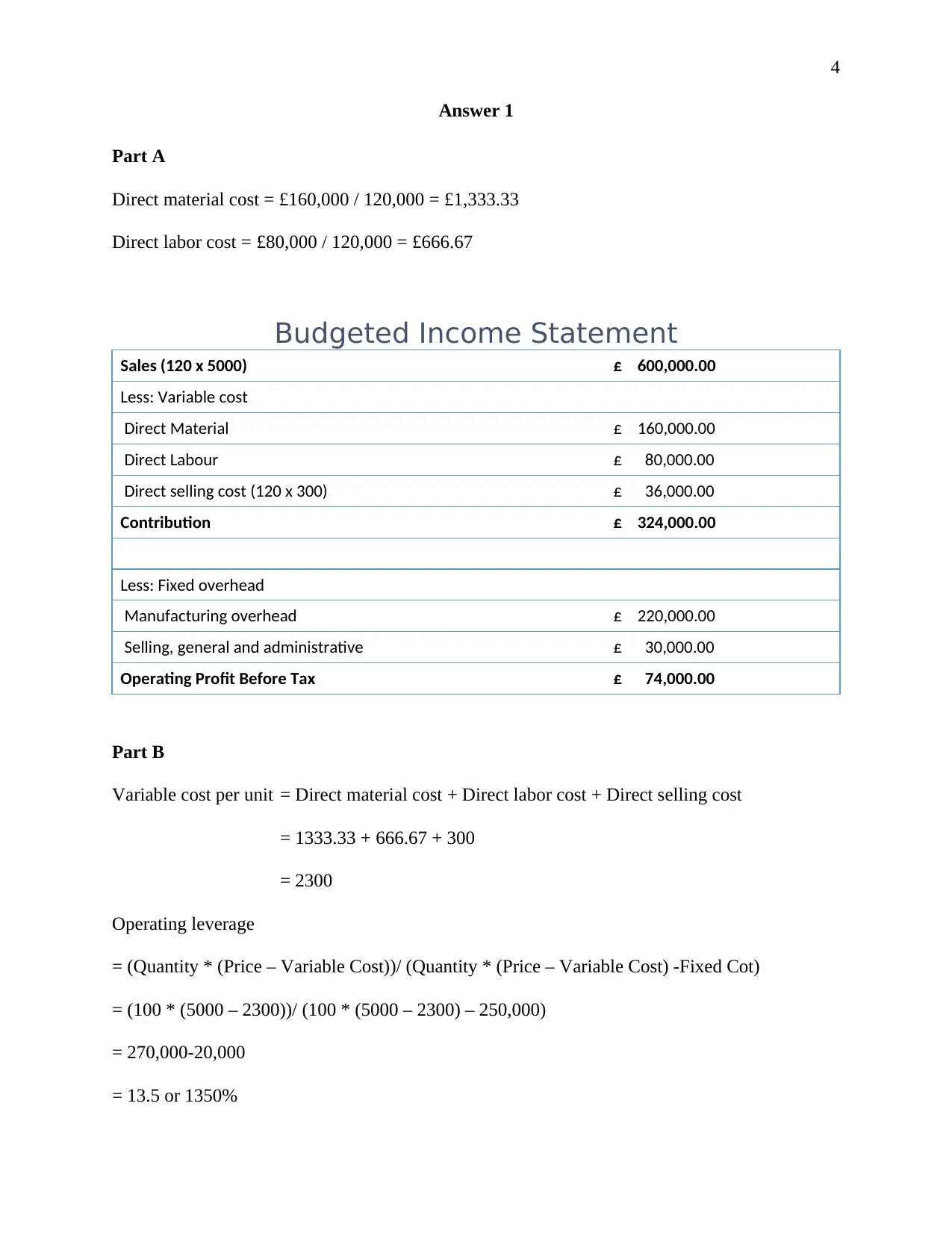

Answer 1

Part A

Direct material cost = £160,000 / 120,000 = £1,333.33

Direct labor cost = £80,000 / 120,000 = £666.67

Budgeted Income Statement

Sales (120 x 5000) £ 600,000.00

Less: Variable cost

Direct Material £ 160,000.00

Direct Labour £ 80,000.00

Direct selling cost (120 x 300) £ 36,000.00

Contribution £ 324,000.00

Less: Fixed overhead

Manufacturing overhead £ 220,000.00

Selling, general and administrative £ 30,000.00

Operating Profit Before Tax £ 74,000.00

Part B

Variable cost per unit = Direct material cost + Direct labor cost + Direct selling cost

= 1333.33 + 666.67 + 300

= 2300

Operating leverage

= (Quantity * (Price – Variable Cost))/ (Quantity * (Price – Variable Cost) -Fixed Cot)

= (100 * (5000 – 2300))/ (100 * (5000 – 2300) – 250,000)

= 270,000-20,000

= 13.5 or 1350%

Answer 1

Part A

Direct material cost = £160,000 / 120,000 = £1,333.33

Direct labor cost = £80,000 / 120,000 = £666.67

Budgeted Income Statement

Sales (120 x 5000) £ 600,000.00

Less: Variable cost

Direct Material £ 160,000.00

Direct Labour £ 80,000.00

Direct selling cost (120 x 300) £ 36,000.00

Contribution £ 324,000.00

Less: Fixed overhead

Manufacturing overhead £ 220,000.00

Selling, general and administrative £ 30,000.00

Operating Profit Before Tax £ 74,000.00

Part B

Variable cost per unit = Direct material cost + Direct labor cost + Direct selling cost

= 1333.33 + 666.67 + 300

= 2300

Operating leverage

= (Quantity * (Price – Variable Cost))/ (Quantity * (Price – Variable Cost) -Fixed Cot)

= (100 * (5000 – 2300))/ (100 * (5000 – 2300) – 250,000)

= 270,000-20,000

= 13.5 or 1350%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

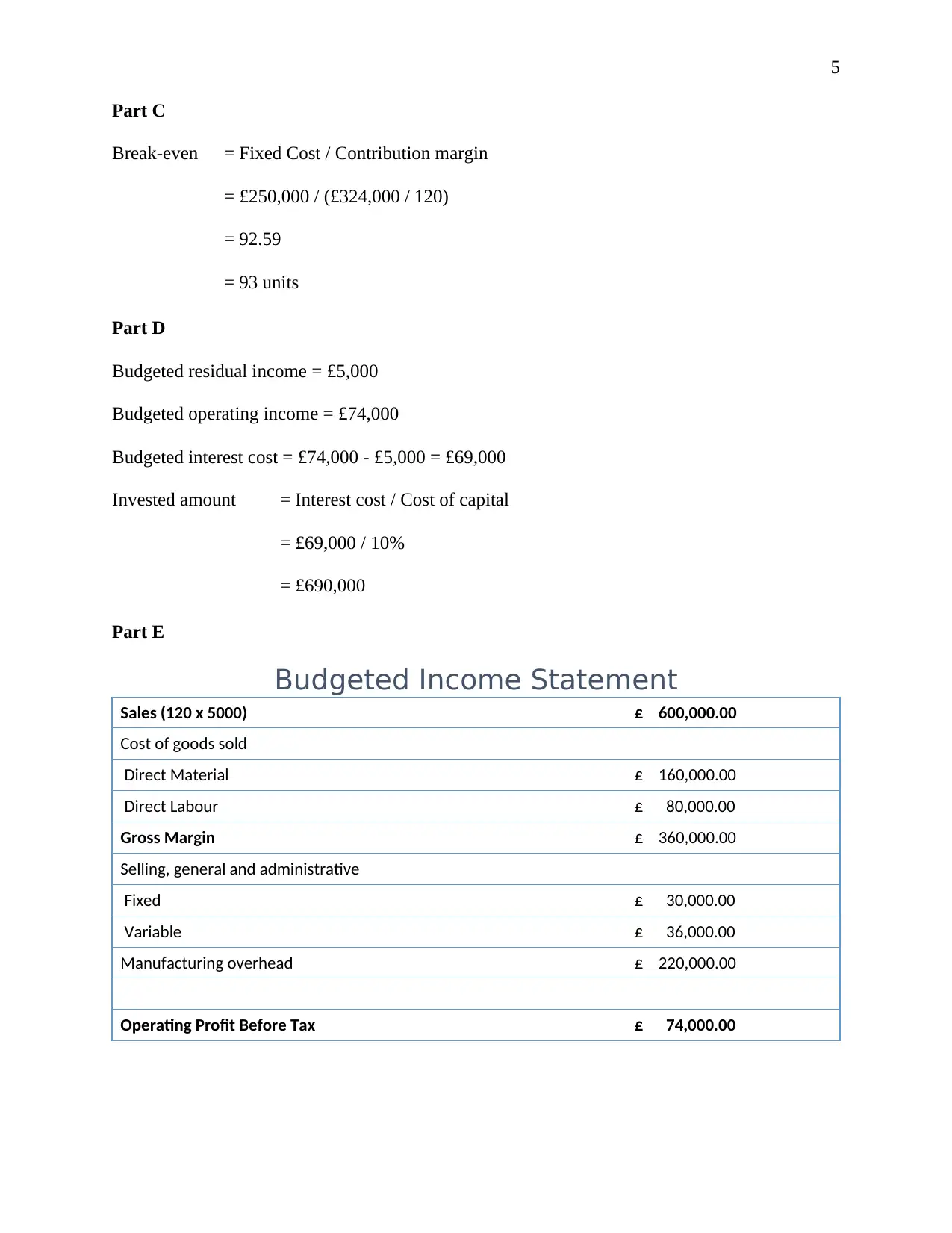

Part C

Break-even = Fixed Cost / Contribution margin

= £250,000 / (£324,000 / 120)

= 92.59

= 93 units

Part D

Budgeted residual income = £5,000

Budgeted operating income = £74,000

Budgeted interest cost = £74,000 - £5,000 = £69,000

Invested amount = Interest cost / Cost of capital

= £69,000 / 10%

= £690,000

Part E

Budgeted Income Statement

Sales (120 x 5000) £ 600,000.00

Cost of goods sold

Direct Material £ 160,000.00

Direct Labour £ 80,000.00

Gross Margin £ 360,000.00

Selling, general and administrative

Fixed £ 30,000.00

Variable £ 36,000.00

Manufacturing overhead £ 220,000.00

Operating Profit Before Tax £ 74,000.00

Part C

Break-even = Fixed Cost / Contribution margin

= £250,000 / (£324,000 / 120)

= 92.59

= 93 units

Part D

Budgeted residual income = £5,000

Budgeted operating income = £74,000

Budgeted interest cost = £74,000 - £5,000 = £69,000

Invested amount = Interest cost / Cost of capital

= £69,000 / 10%

= £690,000

Part E

Budgeted Income Statement

Sales (120 x 5000) £ 600,000.00

Cost of goods sold

Direct Material £ 160,000.00

Direct Labour £ 80,000.00

Gross Margin £ 360,000.00

Selling, general and administrative

Fixed £ 30,000.00

Variable £ 36,000.00

Manufacturing overhead £ 220,000.00

Operating Profit Before Tax £ 74,000.00

6

Part F

Bonus would go up as unsold inventory would bring down the budgeted profit and

above all it will incur inventory cost.

Part F

Bonus would go up as unsold inventory would bring down the budgeted profit and

above all it will incur inventory cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Answer 2

Section 1

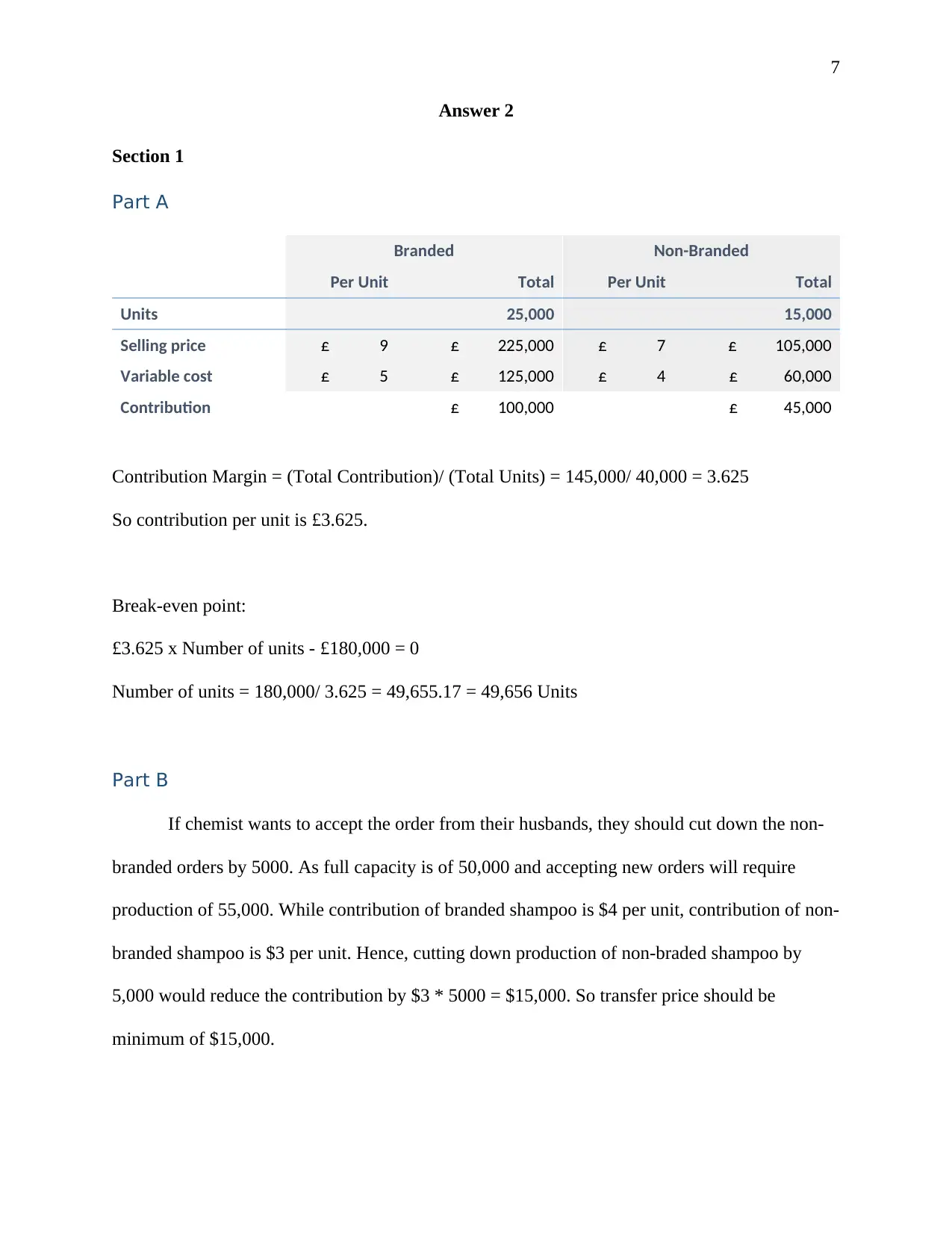

Part A

Branded Non-Branded

Per Unit Total Per Unit Total

Units 25,000 15,000

Selling price £ 9 £ 225,000 £ 7 £ 105,000

Variable cost £ 5 £ 125,000 £ 4 £ 60,000

Contribution £ 100,000 £ 45,000

Contribution Margin = (Total Contribution)/ (Total Units) = 145,000/ 40,000 = 3.625

So contribution per unit is £3.625.

Break-even point:

£3.625 x Number of units - £180,000 = 0

Number of units = 180,000/ 3.625 = 49,655.17 = 49,656 Units

Part B

If chemist wants to accept the order from their husbands, they should cut down the non-

branded orders by 5000. As full capacity is of 50,000 and accepting new orders will require

production of 55,000. While contribution of branded shampoo is $4 per unit, contribution of non-

branded shampoo is $3 per unit. Hence, cutting down production of non-braded shampoo by

5,000 would reduce the contribution by $3 * 5000 = $15,000. So transfer price should be

minimum of $15,000.

Answer 2

Section 1

Part A

Branded Non-Branded

Per Unit Total Per Unit Total

Units 25,000 15,000

Selling price £ 9 £ 225,000 £ 7 £ 105,000

Variable cost £ 5 £ 125,000 £ 4 £ 60,000

Contribution £ 100,000 £ 45,000

Contribution Margin = (Total Contribution)/ (Total Units) = 145,000/ 40,000 = 3.625

So contribution per unit is £3.625.

Break-even point:

£3.625 x Number of units - £180,000 = 0

Number of units = 180,000/ 3.625 = 49,655.17 = 49,656 Units

Part B

If chemist wants to accept the order from their husbands, they should cut down the non-

branded orders by 5000. As full capacity is of 50,000 and accepting new orders will require

production of 55,000. While contribution of branded shampoo is $4 per unit, contribution of non-

branded shampoo is $3 per unit. Hence, cutting down production of non-braded shampoo by

5,000 would reduce the contribution by $3 * 5000 = $15,000. So transfer price should be

minimum of $15,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

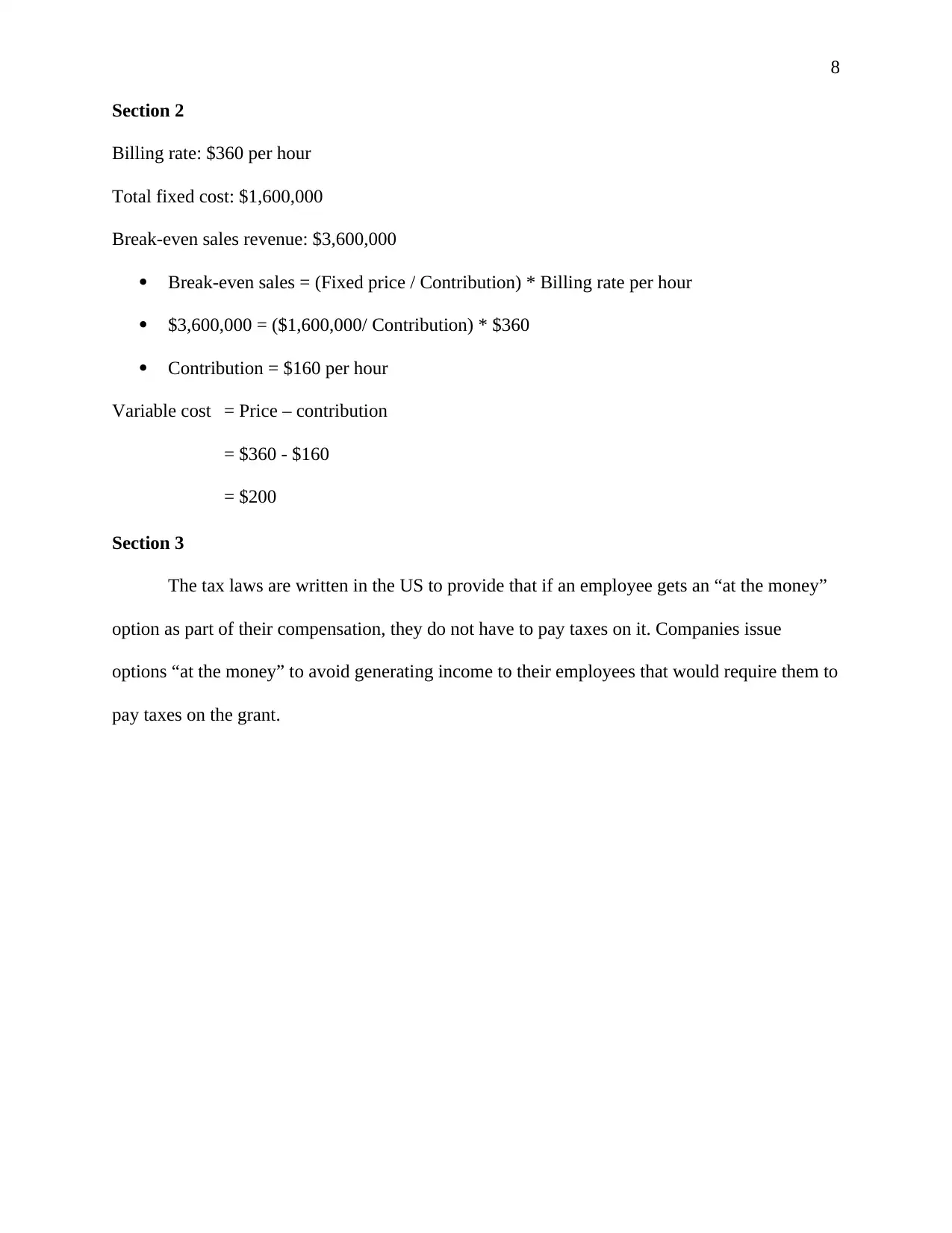

Section 2

Billing rate: $360 per hour

Total fixed cost: $1,600,000

Break-even sales revenue: $3,600,000

Break-even sales = (Fixed price / Contribution) * Billing rate per hour

$3,600,000 = ($1,600,000/ Contribution) * $360

Contribution = $160 per hour

Variable cost = Price – contribution

= $360 - $160

= $200

Section 3

The tax laws are written in the US to provide that if an employee gets an “at the money”

option as part of their compensation, they do not have to pay taxes on it. Companies issue

options “at the money” to avoid generating income to their employees that would require them to

pay taxes on the grant.

Section 2

Billing rate: $360 per hour

Total fixed cost: $1,600,000

Break-even sales revenue: $3,600,000

Break-even sales = (Fixed price / Contribution) * Billing rate per hour

$3,600,000 = ($1,600,000/ Contribution) * $360

Contribution = $160 per hour

Variable cost = Price – contribution

= $360 - $160

= $200

Section 3

The tax laws are written in the US to provide that if an employee gets an “at the money”

option as part of their compensation, they do not have to pay taxes on it. Companies issue

options “at the money” to avoid generating income to their employees that would require them to

pay taxes on the grant.

9

Section 4

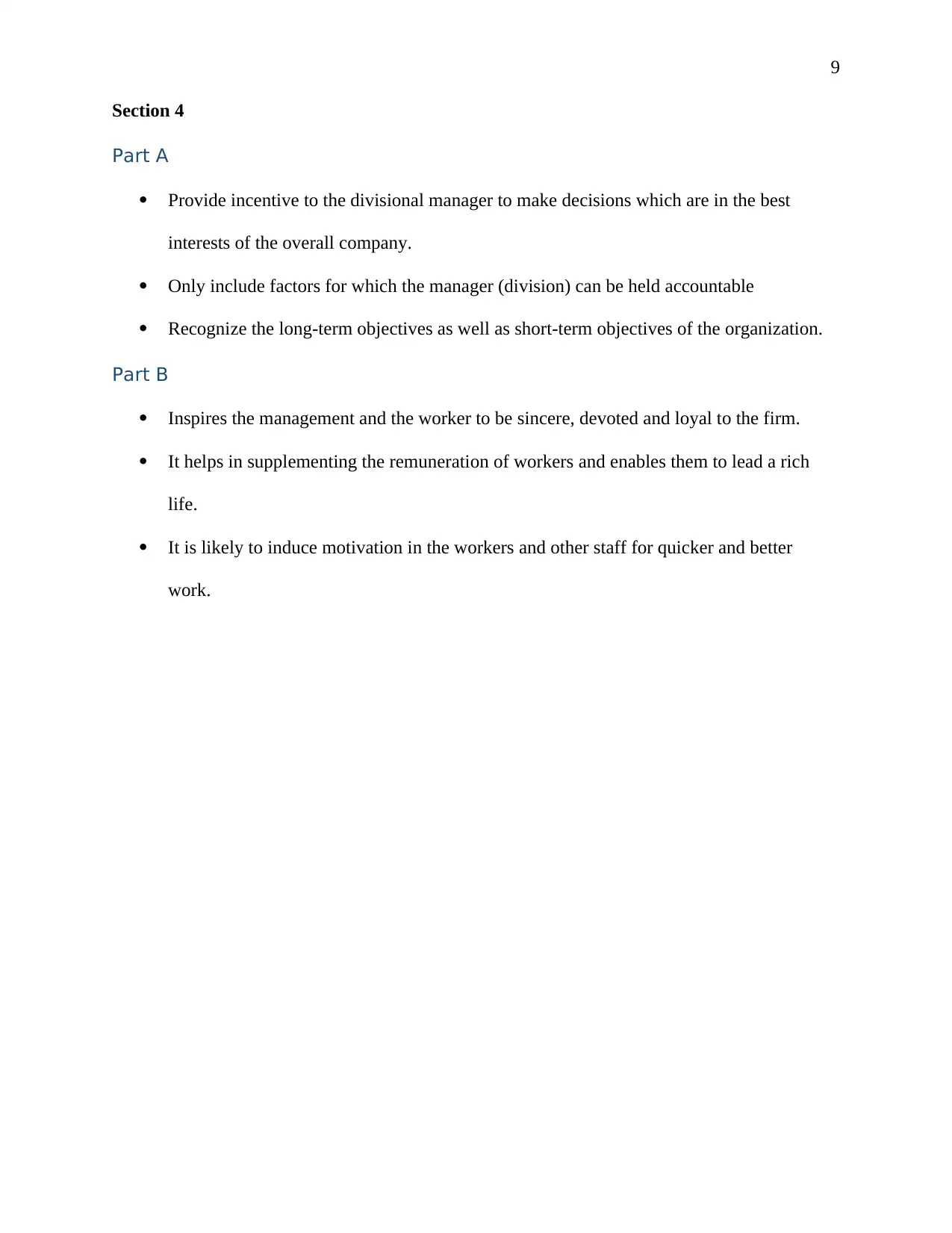

Part A

Provide incentive to the divisional manager to make decisions which are in the best

interests of the overall company.

Only include factors for which the manager (division) can be held accountable

Recognize the long-term objectives as well as short-term objectives of the organization.

Part B

Inspires the management and the worker to be sincere, devoted and loyal to the firm.

It helps in supplementing the remuneration of workers and enables them to lead a rich

life.

It is likely to induce motivation in the workers and other staff for quicker and better

work.

Section 4

Part A

Provide incentive to the divisional manager to make decisions which are in the best

interests of the overall company.

Only include factors for which the manager (division) can be held accountable

Recognize the long-term objectives as well as short-term objectives of the organization.

Part B

Inspires the management and the worker to be sincere, devoted and loyal to the firm.

It helps in supplementing the remuneration of workers and enables them to lead a rich

life.

It is likely to induce motivation in the workers and other staff for quicker and better

work.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

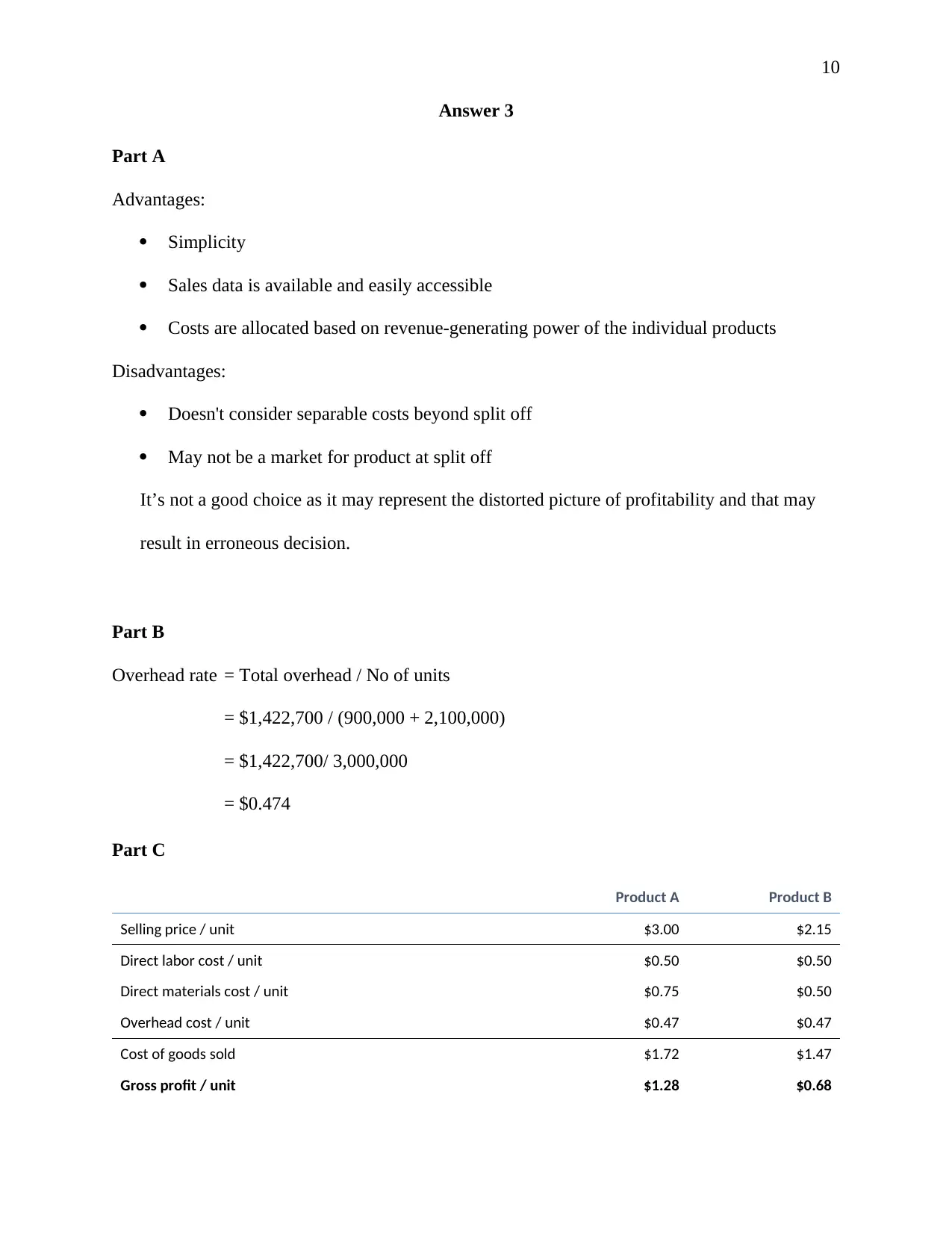

Answer 3

Part A

Advantages:

Simplicity

Sales data is available and easily accessible

Costs are allocated based on revenue-generating power of the individual products

Disadvantages:

Doesn't consider separable costs beyond split off

May not be a market for product at split off

It’s not a good choice as it may represent the distorted picture of profitability and that may

result in erroneous decision.

Part B

Overhead rate = Total overhead / No of units

= $1,422,700 / (900,000 + 2,100,000)

= $1,422,700/ 3,000,000

= $0.474

Part C

Product A Product B

Selling price / unit $3.00 $2.15

Direct labor cost / unit $0.50 $0.50

Direct materials cost / unit $0.75 $0.50

Overhead cost / unit $0.47 $0.47

Cost of goods sold $1.72 $1.47

Gross profit / unit $1.28 $0.68

Answer 3

Part A

Advantages:

Simplicity

Sales data is available and easily accessible

Costs are allocated based on revenue-generating power of the individual products

Disadvantages:

Doesn't consider separable costs beyond split off

May not be a market for product at split off

It’s not a good choice as it may represent the distorted picture of profitability and that may

result in erroneous decision.

Part B

Overhead rate = Total overhead / No of units

= $1,422,700 / (900,000 + 2,100,000)

= $1,422,700/ 3,000,000

= $0.474

Part C

Product A Product B

Selling price / unit $3.00 $2.15

Direct labor cost / unit $0.50 $0.50

Direct materials cost / unit $0.75 $0.50

Overhead cost / unit $0.47 $0.47

Cost of goods sold $1.72 $1.47

Gross profit / unit $1.28 $0.68

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

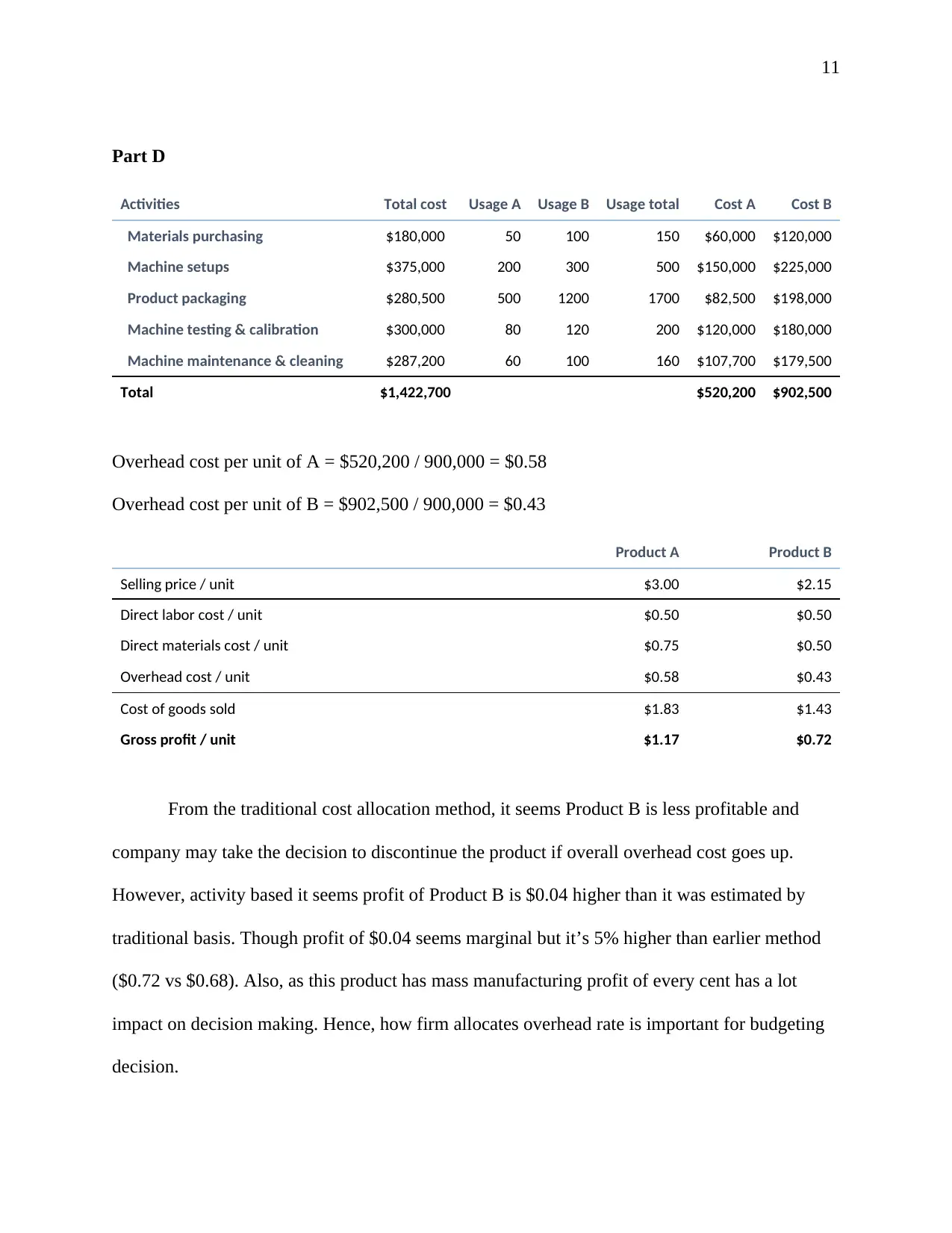

Part D

Activities Total cost Usage A Usage B Usage total Cost A Cost B

Materials purchasing $180,000 50 100 150 $60,000 $120,000

Machine setups $375,000 200 300 500 $150,000 $225,000

Product packaging $280,500 500 1200 1700 $82,500 $198,000

Machine testing & calibration $300,000 80 120 200 $120,000 $180,000

Machine maintenance & cleaning $287,200 60 100 160 $107,700 $179,500

Total $1,422,700 $520,200 $902,500

Overhead cost per unit of A = $520,200 / 900,000 = $0.58

Overhead cost per unit of B = $902,500 / 900,000 = $0.43

Product A Product B

Selling price / unit $3.00 $2.15

Direct labor cost / unit $0.50 $0.50

Direct materials cost / unit $0.75 $0.50

Overhead cost / unit $0.58 $0.43

Cost of goods sold $1.83 $1.43

Gross profit / unit $1.17 $0.72

From the traditional cost allocation method, it seems Product B is less profitable and

company may take the decision to discontinue the product if overall overhead cost goes up.

However, activity based it seems profit of Product B is $0.04 higher than it was estimated by

traditional basis. Though profit of $0.04 seems marginal but it’s 5% higher than earlier method

($0.72 vs $0.68). Also, as this product has mass manufacturing profit of every cent has a lot

impact on decision making. Hence, how firm allocates overhead rate is important for budgeting

decision.

Part D

Activities Total cost Usage A Usage B Usage total Cost A Cost B

Materials purchasing $180,000 50 100 150 $60,000 $120,000

Machine setups $375,000 200 300 500 $150,000 $225,000

Product packaging $280,500 500 1200 1700 $82,500 $198,000

Machine testing & calibration $300,000 80 120 200 $120,000 $180,000

Machine maintenance & cleaning $287,200 60 100 160 $107,700 $179,500

Total $1,422,700 $520,200 $902,500

Overhead cost per unit of A = $520,200 / 900,000 = $0.58

Overhead cost per unit of B = $902,500 / 900,000 = $0.43

Product A Product B

Selling price / unit $3.00 $2.15

Direct labor cost / unit $0.50 $0.50

Direct materials cost / unit $0.75 $0.50

Overhead cost / unit $0.58 $0.43

Cost of goods sold $1.83 $1.43

Gross profit / unit $1.17 $0.72

From the traditional cost allocation method, it seems Product B is less profitable and

company may take the decision to discontinue the product if overall overhead cost goes up.

However, activity based it seems profit of Product B is $0.04 higher than it was estimated by

traditional basis. Though profit of $0.04 seems marginal but it’s 5% higher than earlier method

($0.72 vs $0.68). Also, as this product has mass manufacturing profit of every cent has a lot

impact on decision making. Hence, how firm allocates overhead rate is important for budgeting

decision.

12

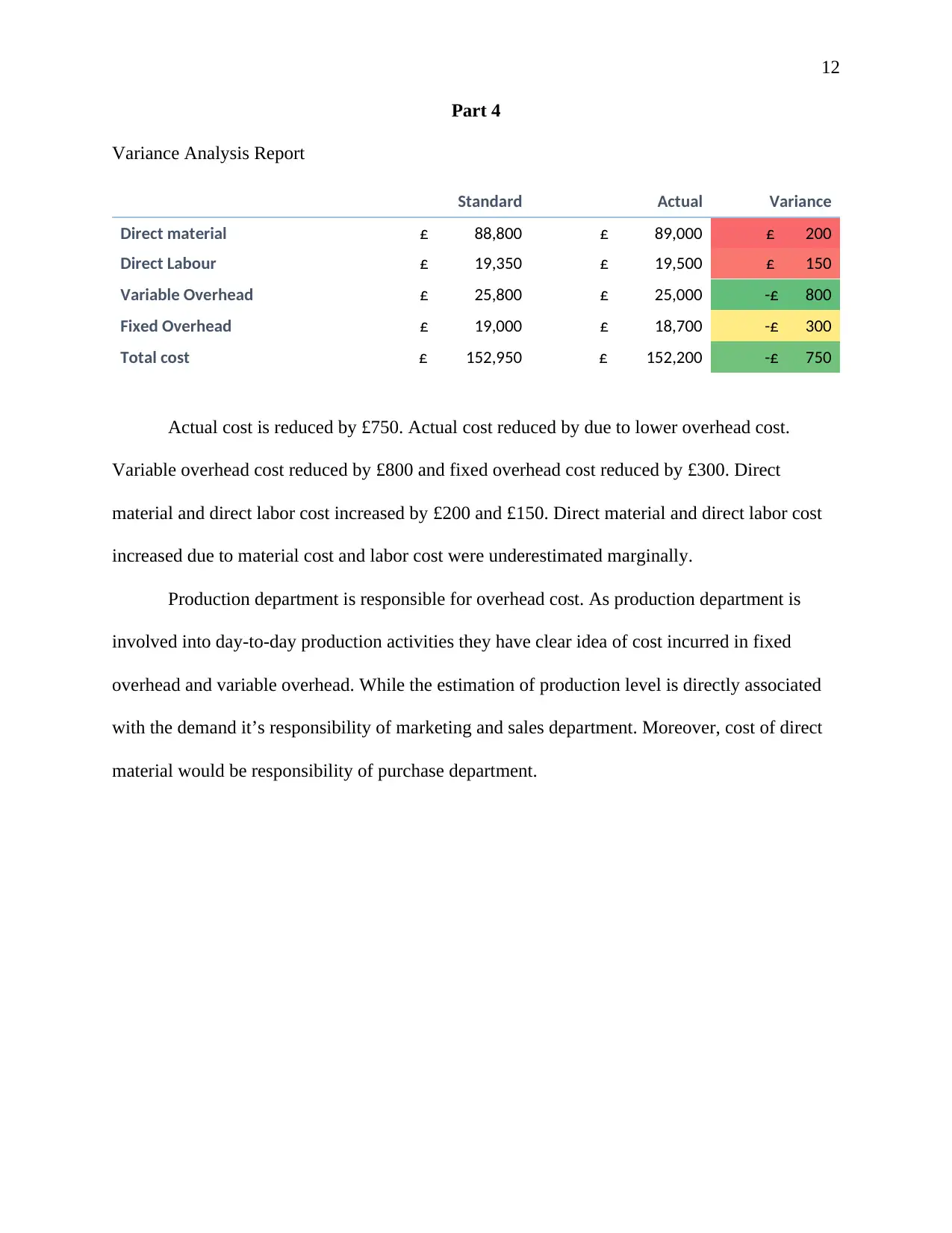

Part 4

Variance Analysis Report

Standard Actual Variance

Direct material £ 88,800 £ 89,000 £ 200

Direct Labour £ 19,350 £ 19,500 £ 150

Variable Overhead £ 25,800 £ 25,000 -£ 800

Fixed Overhead £ 19,000 £ 18,700 -£ 300

Total cost £ 152,950 £ 152,200 -£ 750

Actual cost is reduced by £750. Actual cost reduced by due to lower overhead cost.

Variable overhead cost reduced by £800 and fixed overhead cost reduced by £300. Direct

material and direct labor cost increased by £200 and £150. Direct material and direct labor cost

increased due to material cost and labor cost were underestimated marginally.

Production department is responsible for overhead cost. As production department is

involved into day-to-day production activities they have clear idea of cost incurred in fixed

overhead and variable overhead. While the estimation of production level is directly associated

with the demand it’s responsibility of marketing and sales department. Moreover, cost of direct

material would be responsibility of purchase department.

Part 4

Variance Analysis Report

Standard Actual Variance

Direct material £ 88,800 £ 89,000 £ 200

Direct Labour £ 19,350 £ 19,500 £ 150

Variable Overhead £ 25,800 £ 25,000 -£ 800

Fixed Overhead £ 19,000 £ 18,700 -£ 300

Total cost £ 152,950 £ 152,200 -£ 750

Actual cost is reduced by £750. Actual cost reduced by due to lower overhead cost.

Variable overhead cost reduced by £800 and fixed overhead cost reduced by £300. Direct

material and direct labor cost increased by £200 and £150. Direct material and direct labor cost

increased due to material cost and labor cost were underestimated marginally.

Production department is responsible for overhead cost. As production department is

involved into day-to-day production activities they have clear idea of cost incurred in fixed

overhead and variable overhead. While the estimation of production level is directly associated

with the demand it’s responsibility of marketing and sales department. Moreover, cost of direct

material would be responsibility of purchase department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.