Accounting and Finance: Business Budgeting and Investment Decisions

VerifiedAdded on 2023/03/31

|7

|884

|259

Homework Assignment

AI Summary

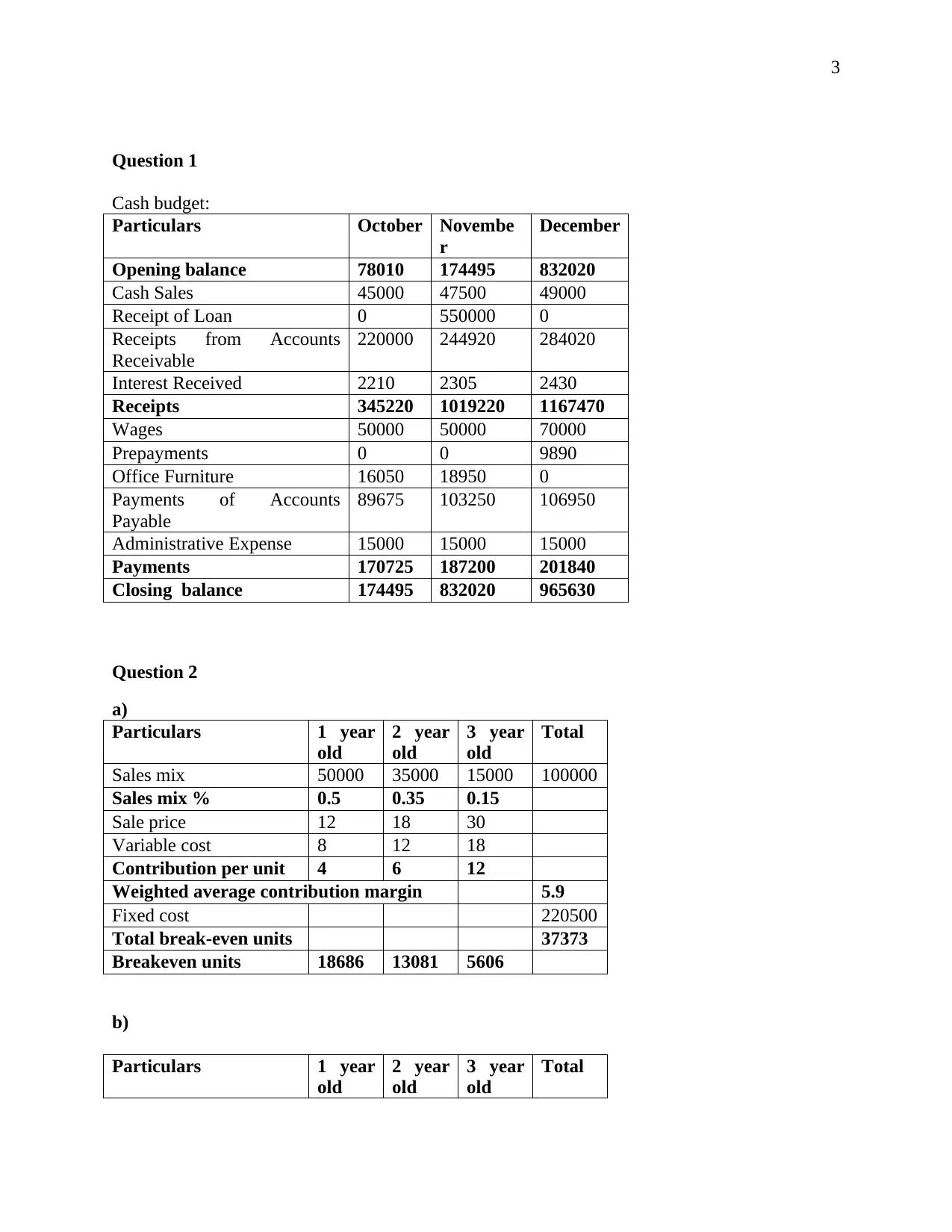

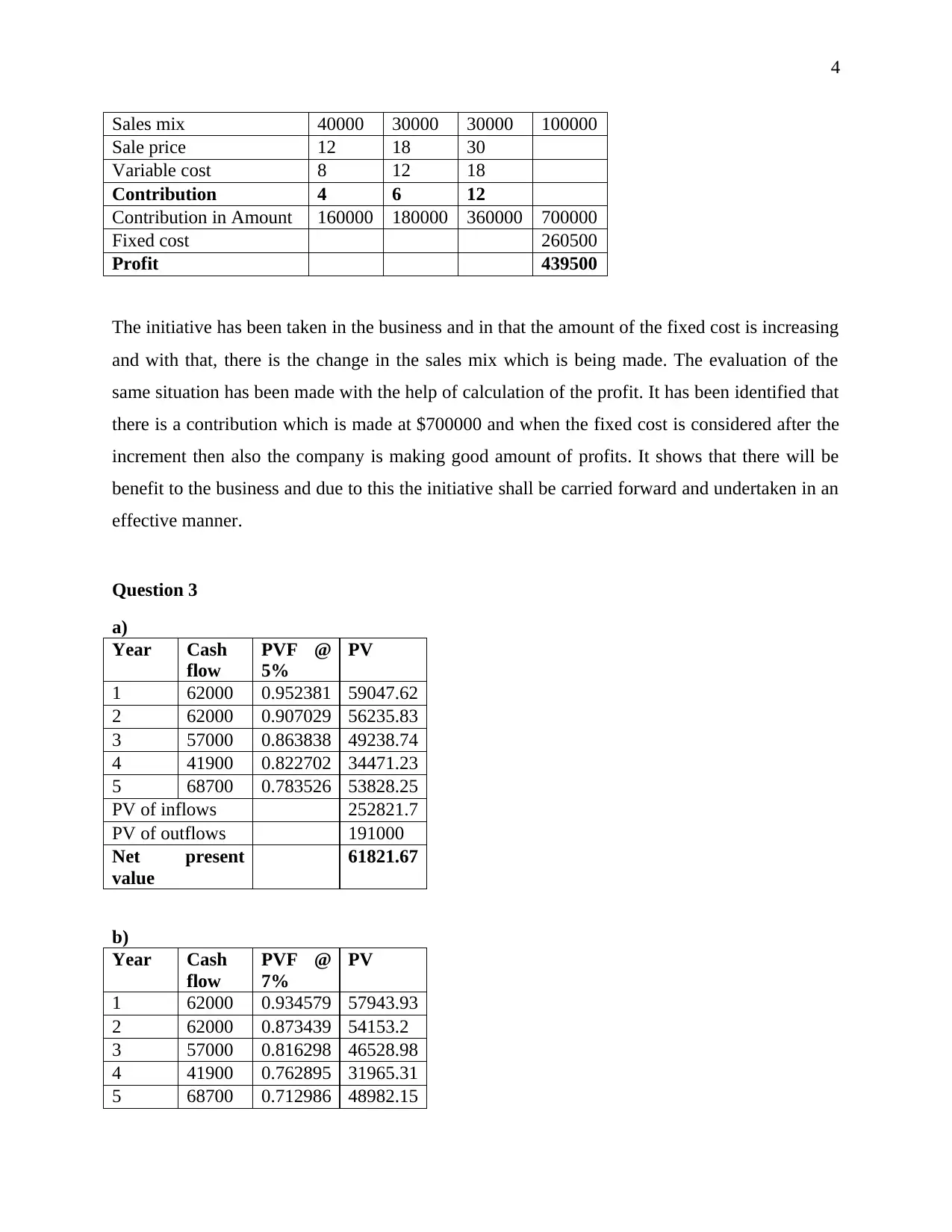

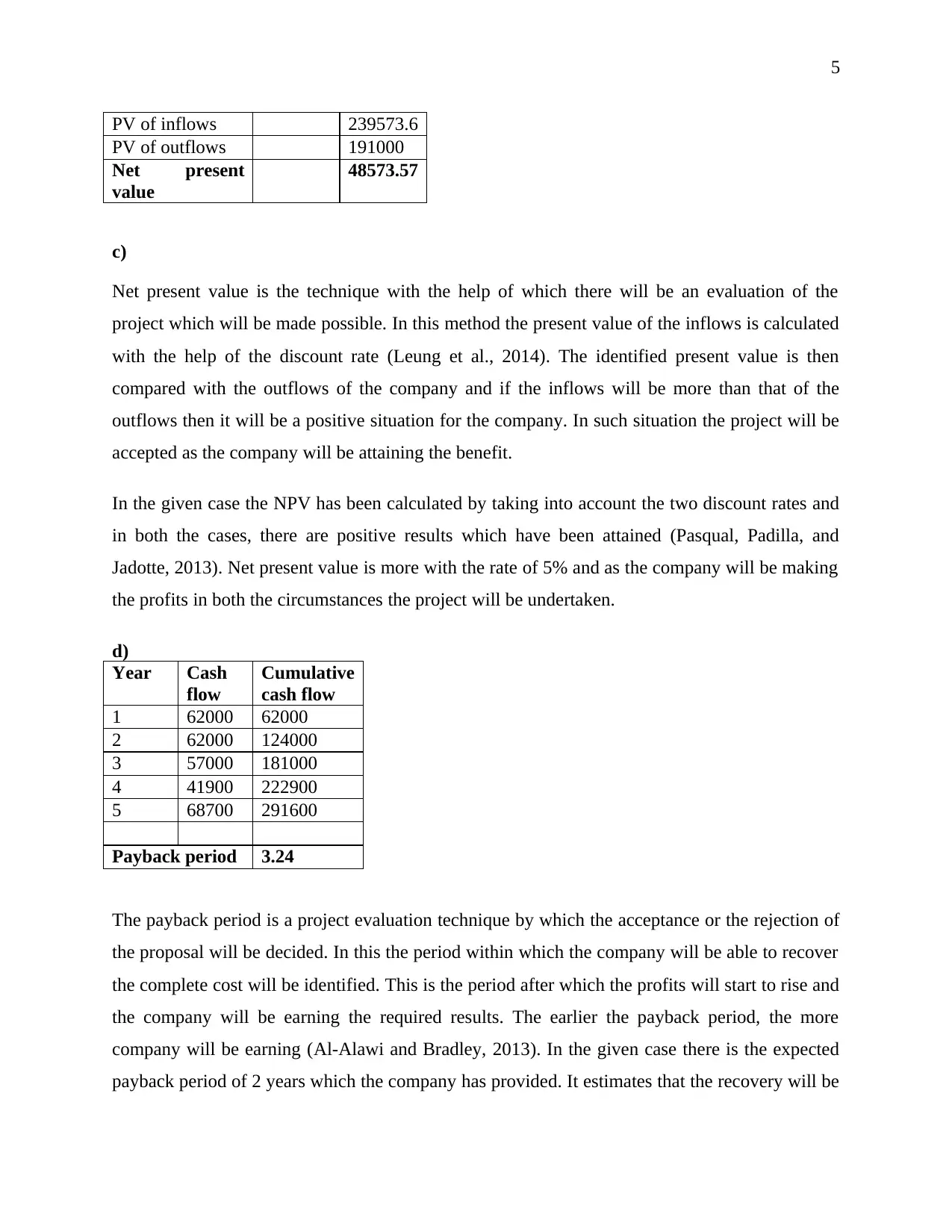

This assignment provides solutions to questions related to accounting and finance for business. It includes a cash budget analysis, break-even point calculation, and an investment appraisal using Net Present Value (NPV) and payback period methods. The cash budget projects cash inflows and outflows over three months (October, November, December). The break-even analysis calculates the break-even units for different product sales mixes. The investment appraisal evaluates a project's viability using NPV at discount rates of 5% and 7%, and determines the payback period. The assignment concludes that based on the calculated payback period being longer than expected, the project may not be undertaken.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.