Budgeting in Organizations: Process, Purpose, and Types

VerifiedAdded on 2022/12/14

|13

|3415

|157

AI Summary

This report contains an introduction to budgeting in organizations, the process of budgeting as well as the purpose of the process to a firm, country and an institution. Further the report outlines the traditional budgetary process and its application to the current world. The report further defines three different kinds of budgets which are, zero-based, activity based and the rolling budget. Finally this report concludes with recommends the best budget which the Snappy Drinks could have used.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

Running head: BUSINESS FINANCE

Business Finance

Student’s Name

Affiliate Institution

Date

Running head: BUSINESS FINANCE

Business Finance

Student’s Name

Affiliate Institution

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

BUSINESS FINANCE

Executive summary

This report contains an introduction to budgeting in organizations, the process of budgeting as

well as the purpose of the process to a firm, country and an institution. Further the report outlines

the traditional budgetary process and its application to the current world. The report further

defines three different kinds of budgets which are, zero-based, activity based and the rolling

budget. Finally this report concludes with recommends the best budget which the Snappy Drinks

could have used.

{1}

The budgeting process

Budgeting refers to the process of designing, implementation and operation an

organization operation in a single budget. Budgeting g can also be said to be the planning

process, preparation, the control procedure and any other activity or procedure involved in this

whole process of preparing a budget (Clark, 2011 pp 576-593). This process represents the

highest accounting level which is used for future reference as it does not only contain reporting

information but also a particular cause of action is provided. Budgeting is part of the

management policies, long-range financial planning, capital expenditure, project management,

and cash flow. A budget is an economic and operating plan spelling out the management target

which they aim at attaining on a forecast basis. A budget is a specific target that Snappy Drinks

is supposed to puts forward and works to achieve it through all available means.

Objectives and the purpose of preparing a budget

BUSINESS FINANCE

Executive summary

This report contains an introduction to budgeting in organizations, the process of budgeting as

well as the purpose of the process to a firm, country and an institution. Further the report outlines

the traditional budgetary process and its application to the current world. The report further

defines three different kinds of budgets which are, zero-based, activity based and the rolling

budget. Finally this report concludes with recommends the best budget which the Snappy Drinks

could have used.

{1}

The budgeting process

Budgeting refers to the process of designing, implementation and operation an

organization operation in a single budget. Budgeting g can also be said to be the planning

process, preparation, the control procedure and any other activity or procedure involved in this

whole process of preparing a budget (Clark, 2011 pp 576-593). This process represents the

highest accounting level which is used for future reference as it does not only contain reporting

information but also a particular cause of action is provided. Budgeting is part of the

management policies, long-range financial planning, capital expenditure, project management,

and cash flow. A budget is an economic and operating plan spelling out the management target

which they aim at attaining on a forecast basis. A budget is a specific target that Snappy Drinks

is supposed to puts forward and works to achieve it through all available means.

Objectives and the purpose of preparing a budget

3

BUSINESS FINANCE

The primary and overall goal of a budget is to help an organization nation or even an

institution to plan the different operational phases in a business, a government or an institution,

coordination of various activities in the available departments of the firm, nation or of the

institution to ensure that adequate control is achieved. For the above purpose to be accomplished

a budget has to aim at attaining several objectives as follows;

Acceleration of departments or divisions efficiency and the firms, nation or institutions

cost centers.

Deciding in the capitalization composition to ensure that funds are available at a

reasonable cost.

Coordination of departmental efforts in the organization towards achieving a common

objective.

The anticipation of the future financial conditions of a firm as well as the needs for

money to be used in the business to keep it in a solvent form.

Prognosticate the future sales of a firm, costs of production and other firm expenses;

this is for the firm to earn income amount and minimization of the business losses as

desired.

Fixing responsibility to departmental heads.

Ensuring productive firms cash and inventory control.

Budget preparation process in Snappy Drinks is supposed to kicks off after managers

have received marketing objectives and forecasts from the top management for the coming year

which is accompanied with a calendar of events stating hen the budget should be complete.

Marketing objectives from senior management and financial forecasts provide a guideline for

departmental budgeting preparation. The initial stage of budget preparation is sales estimate

BUSINESS FINANCE

The primary and overall goal of a budget is to help an organization nation or even an

institution to plan the different operational phases in a business, a government or an institution,

coordination of various activities in the available departments of the firm, nation or of the

institution to ensure that adequate control is achieved. For the above purpose to be accomplished

a budget has to aim at attaining several objectives as follows;

Acceleration of departments or divisions efficiency and the firms, nation or institutions

cost centers.

Deciding in the capitalization composition to ensure that funds are available at a

reasonable cost.

Coordination of departmental efforts in the organization towards achieving a common

objective.

The anticipation of the future financial conditions of a firm as well as the needs for

money to be used in the business to keep it in a solvent form.

Prognosticate the future sales of a firm, costs of production and other firm expenses;

this is for the firm to earn income amount and minimization of the business losses as

desired.

Fixing responsibility to departmental heads.

Ensuring productive firms cash and inventory control.

Budget preparation process in Snappy Drinks is supposed to kicks off after managers

have received marketing objectives and forecasts from the top management for the coming year

which is accompanied with a calendar of events stating hen the budget should be complete.

Marketing objectives from senior management and financial forecasts provide a guideline for

departmental budgeting preparation. The initial stage of budget preparation is sales estimate

4

BUSINESS FINANCE

preparation (Abalos, Smith, Grant, Drury, MacKell & Wagner-Riddle, 2016 p76). This estimate

requires intensive market research and the current situation of the market. After the research

individual projection of what the market would be for the period of operation of the prepared

budget is recorded. This process takes several factors into consideration including both the

external and internal. The sale department is the one responsible for the preparation and

recommending the sale budget. The sale budget goes hand in hand with another budget which

includes all the expenses for sailing and distributing. The two combined budgets for Snappy

Drinks will provide the net revenue on sales which are forecasted for the coming year.

After the sales budget is prepared for Snappy Drinks, the firm’s production budget will

also be developed. This budget relies on the sales budget to consider the amount of the expected

goods; minimum and maximum stock the firm is expected to hold in raw material form and

finished products. Furthermore, this budget will rely on the capacity of the Snappy Drinks

equipment and machines as well s other production factors in the industry (Fauré and Rouleau,

2011 pp167-182). After the preparation of this budget, it can now be converted to a production

cost budget. This budget comprises of material cost, labor cost, and overhead budgets. After this

capital budget is prepared this outlines the estimate of payment to be received on capital account

in comparison to revenue account. After capital account budget a cash budget is prepared which

shows the amount and individually received on revenue account. Once all the budgets are ready,

the master budget is then made. And this is achieved by combining all the other prepared

budgets.

Budgeting is one of the most critical tools in operations of Snappy Drinks. This process is

associated with several advantages to the firm as follows; it helps an organization to remain

focused; it forms the basis of motivation to employees as they work towards sustaining the set

BUSINESS FINANCE

preparation (Abalos, Smith, Grant, Drury, MacKell & Wagner-Riddle, 2016 p76). This estimate

requires intensive market research and the current situation of the market. After the research

individual projection of what the market would be for the period of operation of the prepared

budget is recorded. This process takes several factors into consideration including both the

external and internal. The sale department is the one responsible for the preparation and

recommending the sale budget. The sale budget goes hand in hand with another budget which

includes all the expenses for sailing and distributing. The two combined budgets for Snappy

Drinks will provide the net revenue on sales which are forecasted for the coming year.

After the sales budget is prepared for Snappy Drinks, the firm’s production budget will

also be developed. This budget relies on the sales budget to consider the amount of the expected

goods; minimum and maximum stock the firm is expected to hold in raw material form and

finished products. Furthermore, this budget will rely on the capacity of the Snappy Drinks

equipment and machines as well s other production factors in the industry (Fauré and Rouleau,

2011 pp167-182). After the preparation of this budget, it can now be converted to a production

cost budget. This budget comprises of material cost, labor cost, and overhead budgets. After this

capital budget is prepared this outlines the estimate of payment to be received on capital account

in comparison to revenue account. After capital account budget a cash budget is prepared which

shows the amount and individually received on revenue account. Once all the budgets are ready,

the master budget is then made. And this is achieved by combining all the other prepared

budgets.

Budgeting is one of the most critical tools in operations of Snappy Drinks. This process is

associated with several advantages to the firm as follows; it helps an organization to remain

focused; it forms the basis of motivation to employees as they work towards sustaining the set

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

BUSINESS FINANCE

budget. On the other hand, budgeting simplifies managers’ work while helping them to offer

services more effectively and efficiently. Through budgeting, Snappy Drinks will be able to

achieve their long and short term set goals more perfectly (Fauré and Rouleau, 2011 pp167-182).

{2}

Traditional budgeting refers to a method of preparing a budget whereby the ended year

budget is taken into consideration and acts as the base. The upcoming year budget is prepared

through the introduction of several changes in the lasts year’s budget. This is done through

adjusting several changes such as expenses after considering the inflation rate of the market, the

users demand in the market, the situation of the market currently and many other considerations

such an s government policies. Revenues and costs of previous years form a very crucial part of

the current year’s budget drafting (Mao and Humphrey, 2013 pp67-78). This budgetary process

will have several advantages to Snappy Drinks which includes; it is not complicated to

implement, it provides stability factor in the firm as few things only change, this budgetary

process promotes decentralization where every branch is independent like in the case of most

banks. Furthermore, this method of budgeting provides an opportunity for s firm to consolidate

several projects of the firm to a significant major project. Finally, traditional budgeting is easy to

prepare, and it requires less time to get it done; hence it is not complicated.

Snappy Drinks Plc incidental budget would have appeared as;

BUSINESS FINANCE

budget. On the other hand, budgeting simplifies managers’ work while helping them to offer

services more effectively and efficiently. Through budgeting, Snappy Drinks will be able to

achieve their long and short term set goals more perfectly (Fauré and Rouleau, 2011 pp167-182).

{2}

Traditional budgeting refers to a method of preparing a budget whereby the ended year

budget is taken into consideration and acts as the base. The upcoming year budget is prepared

through the introduction of several changes in the lasts year’s budget. This is done through

adjusting several changes such as expenses after considering the inflation rate of the market, the

users demand in the market, the situation of the market currently and many other considerations

such an s government policies. Revenues and costs of previous years form a very crucial part of

the current year’s budget drafting (Mao and Humphrey, 2013 pp67-78). This budgetary process

will have several advantages to Snappy Drinks which includes; it is not complicated to

implement, it provides stability factor in the firm as few things only change, this budgetary

process promotes decentralization where every branch is independent like in the case of most

banks. Furthermore, this method of budgeting provides an opportunity for s firm to consolidate

several projects of the firm to a significant major project. Finally, traditional budgeting is easy to

prepare, and it requires less time to get it done; hence it is not complicated.

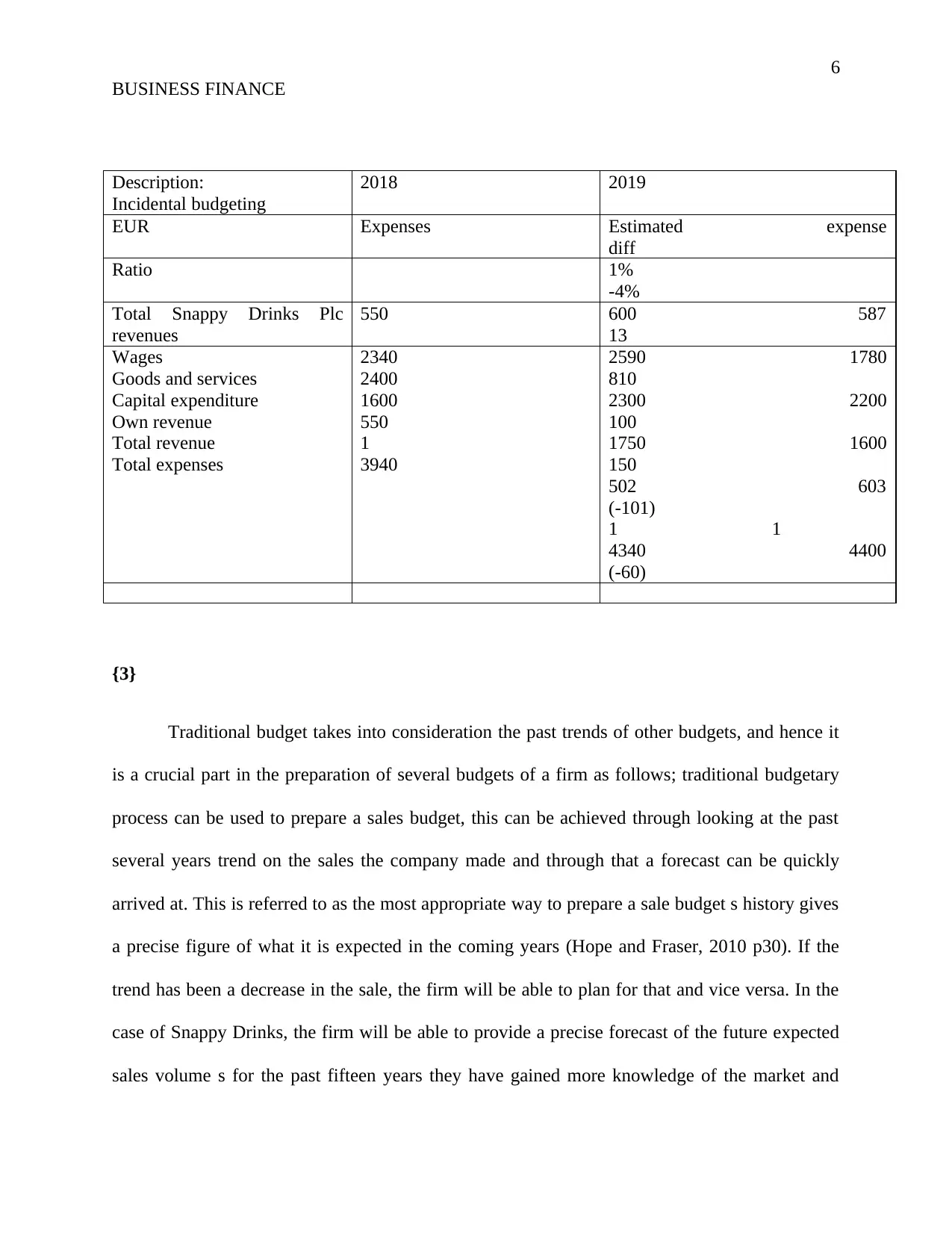

Snappy Drinks Plc incidental budget would have appeared as;

6

BUSINESS FINANCE

Description:

Incidental budgeting

2018 2019

EUR Expenses Estimated expense

diff

Ratio 1%

-4%

Total Snappy Drinks Plc

revenues

550 600 587

13

Wages

Goods and services

Capital expenditure

Own revenue

Total revenue

Total expenses

2340

2400

1600

550

1

3940

2590 1780

810

2300 2200

100

1750 1600

150

502 603

(-101)

1 1

4340 4400

(-60)

{3}

Traditional budget takes into consideration the past trends of other budgets, and hence it

is a crucial part in the preparation of several budgets of a firm as follows; traditional budgetary

process can be used to prepare a sales budget, this can be achieved through looking at the past

several years trend on the sales the company made and through that a forecast can be quickly

arrived at. This is referred to as the most appropriate way to prepare a sale budget s history gives

a precise figure of what it is expected in the coming years (Hope and Fraser, 2010 p30). If the

trend has been a decrease in the sale, the firm will be able to plan for that and vice versa. In the

case of Snappy Drinks, the firm will be able to provide a precise forecast of the future expected

sales volume s for the past fifteen years they have gained more knowledge of the market and

BUSINESS FINANCE

Description:

Incidental budgeting

2018 2019

EUR Expenses Estimated expense

diff

Ratio 1%

-4%

Total Snappy Drinks Plc

revenues

550 600 587

13

Wages

Goods and services

Capital expenditure

Own revenue

Total revenue

Total expenses

2340

2400

1600

550

1

3940

2590 1780

810

2300 2200

100

1750 1600

150

502 603

(-101)

1 1

4340 4400

(-60)

{3}

Traditional budget takes into consideration the past trends of other budgets, and hence it

is a crucial part in the preparation of several budgets of a firm as follows; traditional budgetary

process can be used to prepare a sales budget, this can be achieved through looking at the past

several years trend on the sales the company made and through that a forecast can be quickly

arrived at. This is referred to as the most appropriate way to prepare a sale budget s history gives

a precise figure of what it is expected in the coming years (Hope and Fraser, 2010 p30). If the

trend has been a decrease in the sale, the firm will be able to plan for that and vice versa. In the

case of Snappy Drinks, the firm will be able to provide a precise forecast of the future expected

sales volume s for the past fifteen years they have gained more knowledge of the market and

7

BUSINESS FINANCE

referring to the trend of the past fifteen years the company will be able to draft a better sales

budget.

Moreover, traditional budgeting is also crucial in the preparation of the production

budget; this is a similar case to the sale budget as the production budget heavily depends on the

sale budget. Through the use of past data on the production volumes and inventory holding

capacity of the firm a clear and appropriate production budget will be quickly arrived at. The

future forecast mostly depends on history and other factors to help in forecasting (Atrill,

McLaney and McLaney, 2015 p89). Referring to the past several year's of operation of Snappy

Drinks, traditional budgets will help a firm in the realization of the correct target or objective to

set. Trough referring to the preceding year’s budget the firm can be able to make decisions on

whether to employ more workers or retrench (Ibrahim and Proctor, 2012). For the case of

Snappy Drinks, more workers need to be added the company has planned to add on to its

production budget. This is as a result of the increase in market sale both domestically and

internationally.

{4}

A rolling budget refers to a revised financial plan sets for the future accounting period.

This method is used to replace the previous year in a continuous budgeting system. This is a new

and updated budget that replaces one another after the period of service expires. Rolling budget

tries to simplify the incremental budget through setting budgets on a quarterly or monthly basis

every year (Zeller and Metzger, 2013 pp299-310). After every quarter a budgeting process is

undertaken. It presents budgeting as a continuous process. This kind of budgeting is mostly used

BUSINESS FINANCE

referring to the trend of the past fifteen years the company will be able to draft a better sales

budget.

Moreover, traditional budgeting is also crucial in the preparation of the production

budget; this is a similar case to the sale budget as the production budget heavily depends on the

sale budget. Through the use of past data on the production volumes and inventory holding

capacity of the firm a clear and appropriate production budget will be quickly arrived at. The

future forecast mostly depends on history and other factors to help in forecasting (Atrill,

McLaney and McLaney, 2015 p89). Referring to the past several year's of operation of Snappy

Drinks, traditional budgets will help a firm in the realization of the correct target or objective to

set. Trough referring to the preceding year’s budget the firm can be able to make decisions on

whether to employ more workers or retrench (Ibrahim and Proctor, 2012). For the case of

Snappy Drinks, more workers need to be added the company has planned to add on to its

production budget. This is as a result of the increase in market sale both domestically and

internationally.

{4}

A rolling budget refers to a revised financial plan sets for the future accounting period.

This method is used to replace the previous year in a continuous budgeting system. This is a new

and updated budget that replaces one another after the period of service expires. Rolling budget

tries to simplify the incremental budget through setting budgets on a quarterly or monthly basis

every year (Zeller and Metzger, 2013 pp299-310). After every quarter a budgeting process is

undertaken. It presents budgeting as a continuous process. This kind of budgeting is mostly used

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

BUSINESS FINANCE

by service companies who develop more than three budgets in a whole year. This budget will

help Snappy Drinks in reducing any long term risk that a firm can face by making a complex

yearly budget which will be hard to subject to changes.

Zero-based budgeting is a budgeting process which starts at zero every time a new budget

is being drafted each budget for every department is expected to be justifiable in zero-based

budgeting. Zero-based budgets require in-depth research and look on every transaction as well as

departmental needs (Weetman, P. 2010 pp76-80). This budgetary process will help Snappy

Drinks in tracking every purchase and preventing wasteful spending. This has brought several

reforms to incremental budgeting, as through additional budgeting employees’ takes advantage

and makes unnecessary and wasteful spending leading to losses (Hansen, 2011 pp289-319). Most

of the businesses today are encouraging the application of this budgetary process as it presents

itself to be more accurate as well as cost-saving budget to a company in making future forecasts.

The fiscal process improves the incremental budget through the introduction of zero starts and

hence every department has to track and justify all the listed needs in the budget and their

recommendation on it is required centrally to the incremental budget.

Activity-based budgeting is a process of budgeting which researches, records and makes

the analysis of the activities that leads to business expenses. This process is considered more than

just minor adjustment of the previously available budgets as in the case of incremental

budgeting. In Activity-based budgeting, research is conducted to look for business operation

efficiencies, and a budget is developed from the evidence gathered of similar activities (Pyhrr,

2012 pp677-696). Contrary to incremental budgeting activity-based budget advocates for

intensive market research on all the activities which brings forth cost to a firm and considers

them. Progressive budget, on the other hand, advocates for adjusting of cost values of the past

BUSINESS FINANCE

by service companies who develop more than three budgets in a whole year. This budget will

help Snappy Drinks in reducing any long term risk that a firm can face by making a complex

yearly budget which will be hard to subject to changes.

Zero-based budgeting is a budgeting process which starts at zero every time a new budget

is being drafted each budget for every department is expected to be justifiable in zero-based

budgeting. Zero-based budgets require in-depth research and look on every transaction as well as

departmental needs (Weetman, P. 2010 pp76-80). This budgetary process will help Snappy

Drinks in tracking every purchase and preventing wasteful spending. This has brought several

reforms to incremental budgeting, as through additional budgeting employees’ takes advantage

and makes unnecessary and wasteful spending leading to losses (Hansen, 2011 pp289-319). Most

of the businesses today are encouraging the application of this budgetary process as it presents

itself to be more accurate as well as cost-saving budget to a company in making future forecasts.

The fiscal process improves the incremental budget through the introduction of zero starts and

hence every department has to track and justify all the listed needs in the budget and their

recommendation on it is required centrally to the incremental budget.

Activity-based budgeting is a process of budgeting which researches, records and makes

the analysis of the activities that leads to business expenses. This process is considered more than

just minor adjustment of the previously available budgets as in the case of incremental

budgeting. In Activity-based budgeting, research is conducted to look for business operation

efficiencies, and a budget is developed from the evidence gathered of similar activities (Pyhrr,

2012 pp677-696). Contrary to incremental budgeting activity-based budget advocates for

intensive market research on all the activities which brings forth cost to a firm and considers

them. Progressive budget, on the other hand, advocates for adjusting of cost values of the past

9

BUSINESS FINANCE

events recorded on the previous budget in consideration ton inflation and other issues in the

market.

Recommendations

{5}

The budgeting process has five main elements which all are and can potentially be

applied to Snappy Drinks to improve the business model and also the market performance both

the domestically and internationally. The first element of budgeting is; be comprehensive. This

means that the individuals who are responsible for planning and coming up with the budget

should be prepared to spend a lot of time to research and come out with a satisfying budget. For a

successful budget to be produced comprehensiveness plays a significant role in categorising

expenses and incomes and including every aspect in the list (Schick, 2010 pp1-15). The Finance

Director, Hayley, and Donna and other individuals in the company should be prepared to spend a

lot of time to come out with the best budget which will support all the set expansion mission and

objective of the company.

The second element of budgeting is the capability to be able to understand one's capacity.

Having survived for more than fifteen years, the company should at now be able to classify her

need and priorities and hence to list off non-necessities in the budget (Schick, 2010 pp1-15). As

the company has already done, it has clearly defined her goals on adding other products in her

production proceed. In budgeting, a firm is first required to list down all the set goals and then

start planning on how the budgeting process will help in attaining the goals. Snappy Drinks has

already succeeded in this stage, and hence more strategies need to be looked at and to identify

how the budget to be released will enable the company to achieve her set goals.

BUSINESS FINANCE

events recorded on the previous budget in consideration ton inflation and other issues in the

market.

Recommendations

{5}

The budgeting process has five main elements which all are and can potentially be

applied to Snappy Drinks to improve the business model and also the market performance both

the domestically and internationally. The first element of budgeting is; be comprehensive. This

means that the individuals who are responsible for planning and coming up with the budget

should be prepared to spend a lot of time to research and come out with a satisfying budget. For a

successful budget to be produced comprehensiveness plays a significant role in categorising

expenses and incomes and including every aspect in the list (Schick, 2010 pp1-15). The Finance

Director, Hayley, and Donna and other individuals in the company should be prepared to spend a

lot of time to come out with the best budget which will support all the set expansion mission and

objective of the company.

The second element of budgeting is the capability to be able to understand one's capacity.

Having survived for more than fifteen years, the company should at now be able to classify her

need and priorities and hence to list off non-necessities in the budget (Schick, 2010 pp1-15). As

the company has already done, it has clearly defined her goals on adding other products in her

production proceed. In budgeting, a firm is first required to list down all the set goals and then

start planning on how the budgeting process will help in attaining the goals. Snappy Drinks has

already succeeded in this stage, and hence more strategies need to be looked at and to identify

how the budget to be released will enable the company to achieve her set goals.

10

BUSINESS FINANCE

{6}

Having been in operation for more than fifteen years, Snappy Drinks can be able to use

the activity-based budgeting in drafting the next operational year’s budget and notices a big

difference. Through the application of this budget process, the company will not only update the

past years budget but also the company will be able to eliminate wasteful spending by her

departments and also track all the transactions of an activity involved in the budget to make

better forecasts in the future (Clark, 2011 pp576-593). Moreover, the company can also use a

rolling budget. Through this, the company will have evaded from budget risks that may be

associated with the yearly budget. More so the company will be able to learn the market ell as

compared to budgeting for the whole financial year.

Through the use of activity-based budget, Snappy Drinks will be able to write off some

expenses included in the past financial year’s budget which may have been the root cause of

reduced income enjoyed by the company. Tracking and introducing integrity in every process as

activity-based budget advocates will hold in coming up with the best budget for Snappy Drinks

to the next year. More so the company can combine both rolling and activity-based budgeting to

have the best-desired result after every quarter or after every budget service period (Zezhong

Xiao, Weetman and Sun, 2014 pp76-90). A combination of the two budgeting process will help

the company to generate more revenue and have a better market share as compared to those firms

using incremental budgeting process.

BUSINESS FINANCE

{6}

Having been in operation for more than fifteen years, Snappy Drinks can be able to use

the activity-based budgeting in drafting the next operational year’s budget and notices a big

difference. Through the application of this budget process, the company will not only update the

past years budget but also the company will be able to eliminate wasteful spending by her

departments and also track all the transactions of an activity involved in the budget to make

better forecasts in the future (Clark, 2011 pp576-593). Moreover, the company can also use a

rolling budget. Through this, the company will have evaded from budget risks that may be

associated with the yearly budget. More so the company will be able to learn the market ell as

compared to budgeting for the whole financial year.

Through the use of activity-based budget, Snappy Drinks will be able to write off some

expenses included in the past financial year’s budget which may have been the root cause of

reduced income enjoyed by the company. Tracking and introducing integrity in every process as

activity-based budget advocates will hold in coming up with the best budget for Snappy Drinks

to the next year. More so the company can combine both rolling and activity-based budgeting to

have the best-desired result after every quarter or after every budget service period (Zezhong

Xiao, Weetman and Sun, 2014 pp76-90). A combination of the two budgeting process will help

the company to generate more revenue and have a better market share as compared to those firms

using incremental budgeting process.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

BUSINESS FINANCE

Conclusion

Budgeting refers to the planning process, preparation, the control procedure and any other

activity or procedure involved in this whole process of preparing a budget. The primary and

overall purpose of a budget is to help an organization nation or even an institution to plan the

different operational phases in a business, a country or an institution, coordination of various

activities in the available departments of the firm, nation or of the institution to ensure that

adequate control is achieved. The initial stage of budget preparation in Snappy Drinks will be

sales estimate preparation. After the sales budget is prepared, the firms’ production budget is also

developed. Once all the budgets are ready, the master budget is then made.

Traditional budgeting refers to a method of preparing a budget whereby the ended year

budget is taken into consideration and acts as the base. A rolling budget is used to replace the

previous year in a continuous budgeting system. On the other hand, activity-based budgeting is a

process of budgeting which researches, records and makes the analysis of the activities that leads

to business expenses (Drury, C. 2005 p98). Finally, Zero-based budgeting is a budgeting process

which starts at zero every time a new budget is being drafted each budget for every department is

expected to be justifiable in zero-based budgeting.

BUSINESS FINANCE

Conclusion

Budgeting refers to the planning process, preparation, the control procedure and any other

activity or procedure involved in this whole process of preparing a budget. The primary and

overall purpose of a budget is to help an organization nation or even an institution to plan the

different operational phases in a business, a country or an institution, coordination of various

activities in the available departments of the firm, nation or of the institution to ensure that

adequate control is achieved. The initial stage of budget preparation in Snappy Drinks will be

sales estimate preparation. After the sales budget is prepared, the firms’ production budget is also

developed. Once all the budgets are ready, the master budget is then made.

Traditional budgeting refers to a method of preparing a budget whereby the ended year

budget is taken into consideration and acts as the base. A rolling budget is used to replace the

previous year in a continuous budgeting system. On the other hand, activity-based budgeting is a

process of budgeting which researches, records and makes the analysis of the activities that leads

to business expenses (Drury, C. 2005 p98). Finally, Zero-based budgeting is a budgeting process

which starts at zero every time a new budget is being drafted each budget for every department is

expected to be justifiable in zero-based budgeting.

12

BUSINESS FINANCE

References

Abalos, D., Smith, W. N., Grant, B. B., Drury, C. F., MacKell, S., & Wagner-Riddle, C. 2016. Scenario

analysis of fertilizer management practices for N2O mitigation from corn systems in Canada.

Science of the Total Environment, 573, 356-365.

Atrill, P., McLaney, E. J., & McLaney, E. 2015. Management Accounting for Decision Makers.

Clark, T.N., 2011. Community structure, decision-making, budget expenditures, and urban renewal in 51

American communities. American Sociological Review, pp.576-593.

Drury, C. 2005. Management Accounting for Business. Andover, England: Cengage Learning EMEA.

Fauré, B. and Rouleau, L., 2011. The strategic competence of accountants and middle managers in

budget making. Accounting, Organizations and Society, 36(3), pp.167-182.

Hansen, S.C., 2011. A theoretical analysis of the impact of adopting rolling budgets, activity-based

budgeting and beyond budgeting. European Accounting Review, 20(2), pp.289-319.

Hope, J. and Fraser, R., 2010. Beyond budgeting. Strategic Finance, 82(4), p.30.

Ibrahim, M.M. and Proctor, R.A., 2012. Incremental budgeting in local authorities. International

Journal of Public Sector Management, 5(5).

Mao, M. and Humphrey, M., 2013, May. Scaling and scheduling to maximize application performance

within budget constraints in cloud workflows. In 2013 IEEE 27th International Symposium on

Parallel and Distributed Processing (pp. 67-78). IEEE.

Pyhrr, P.A., 2012. Zero‐Based Budgeting. Handbook of Budgeting, pp.677-696.

Schick, A., 2010. Crisis budgeting. OECD Journal on Budgeting, 9(3), pp.1-14.

Weetman, P. 2010. Management Accounting. Upper Saddle River, NJ: FT Press.

Zeller, T.L. and Metzger, L.M., 2013. Good Bye Traditional Budgeting, Hello Rolling Forecast: Has the

Time Come?. American Journal of Business Education, 6(3), pp.299-310.

BUSINESS FINANCE

References

Abalos, D., Smith, W. N., Grant, B. B., Drury, C. F., MacKell, S., & Wagner-Riddle, C. 2016. Scenario

analysis of fertilizer management practices for N2O mitigation from corn systems in Canada.

Science of the Total Environment, 573, 356-365.

Atrill, P., McLaney, E. J., & McLaney, E. 2015. Management Accounting for Decision Makers.

Clark, T.N., 2011. Community structure, decision-making, budget expenditures, and urban renewal in 51

American communities. American Sociological Review, pp.576-593.

Drury, C. 2005. Management Accounting for Business. Andover, England: Cengage Learning EMEA.

Fauré, B. and Rouleau, L., 2011. The strategic competence of accountants and middle managers in

budget making. Accounting, Organizations and Society, 36(3), pp.167-182.

Hansen, S.C., 2011. A theoretical analysis of the impact of adopting rolling budgets, activity-based

budgeting and beyond budgeting. European Accounting Review, 20(2), pp.289-319.

Hope, J. and Fraser, R., 2010. Beyond budgeting. Strategic Finance, 82(4), p.30.

Ibrahim, M.M. and Proctor, R.A., 2012. Incremental budgeting in local authorities. International

Journal of Public Sector Management, 5(5).

Mao, M. and Humphrey, M., 2013, May. Scaling and scheduling to maximize application performance

within budget constraints in cloud workflows. In 2013 IEEE 27th International Symposium on

Parallel and Distributed Processing (pp. 67-78). IEEE.

Pyhrr, P.A., 2012. Zero‐Based Budgeting. Handbook of Budgeting, pp.677-696.

Schick, A., 2010. Crisis budgeting. OECD Journal on Budgeting, 9(3), pp.1-14.

Weetman, P. 2010. Management Accounting. Upper Saddle River, NJ: FT Press.

Zeller, T.L. and Metzger, L.M., 2013. Good Bye Traditional Budgeting, Hello Rolling Forecast: Has the

Time Come?. American Journal of Business Education, 6(3), pp.299-310.

13

BUSINESS FINANCE

Zezhong Xiao, J., Weetman, P., & Sun, M. 2014. Political influence and coexistence of a uniform

accounting system and accounting standards: recent developments in China. Abacus, 40(2), 193-

218.

BUSINESS FINANCE

Zezhong Xiao, J., Weetman, P., & Sun, M. 2014. Political influence and coexistence of a uniform

accounting system and accounting standards: recent developments in China. Abacus, 40(2), 193-

218.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.