Construction Economics Report: Investment, Alliances, and Cost Control

VerifiedAdded on 2021/04/24

|18

|6167

|47

Report

AI Summary

This report delves into the core aspects of construction economics, examining key developmental conditions that influence investment decisions, such as risk tolerance, return on investment, tax exposure, market trends, and investment horizons. It outlines the key assumptions, constraints, and conditions inherent in cost-benefit analysis (CBA) within the construction industry, including detailed analyses of costs, benefits, payback periods, internal rate of return, net present value, sensitivity analysis, and risk assessment. Furthermore, the report explores project alliancing, discussing its advantages, disadvantages, feasibility, success factors, and challenges. Finally, it investigates various cost control and reduction strategies, including cost leadership, differentiation, and focused approaches, providing a comprehensive overview of financial management and strategic planning in construction projects.

1

Construction Economics

Construction Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

A. Key Developmental Conditions............................................................................................4

Risk Tolerance or Appetite....................................................................................................4

Return or Profits.....................................................................................................................5

Tax Exposure.........................................................................................................................5

Market Trends........................................................................................................................5

Investment Horizons..............................................................................................................6

B. Key assumptions, constraints and conditions of CBA..........................................................6

Assumptions...........................................................................................................................6

Constraints..............................................................................................................................6

Conditions..............................................................................................................................7

CBA Analysis.........................................................................................................................7

Costs...................................................................................................................................7

Benefits..............................................................................................................................9

Payback Period.................................................................................................................10

Internal Rate of Return.........................................................................................................10

Net Present Value.................................................................................................................11

Sensitivity Analysis..............................................................................................................11

Risk Assessment...................................................................................................................11

C. Project Alliancing................................................................................................................12

Project Alliance for the Development Company.................................................................12

Advantages of Project Alliance............................................................................................12

Disadvantages of Project Alliance.......................................................................................13

Suggestions..........................................................................................................................13

Feasibility of adopting Project Alliancing...........................................................................13

Success factors.....................................................................................................................13

Challenges............................................................................................................................14

Table of Contents

A. Key Developmental Conditions............................................................................................4

Risk Tolerance or Appetite....................................................................................................4

Return or Profits.....................................................................................................................5

Tax Exposure.........................................................................................................................5

Market Trends........................................................................................................................5

Investment Horizons..............................................................................................................6

B. Key assumptions, constraints and conditions of CBA..........................................................6

Assumptions...........................................................................................................................6

Constraints..............................................................................................................................6

Conditions..............................................................................................................................7

CBA Analysis.........................................................................................................................7

Costs...................................................................................................................................7

Benefits..............................................................................................................................9

Payback Period.................................................................................................................10

Internal Rate of Return.........................................................................................................10

Net Present Value.................................................................................................................11

Sensitivity Analysis..............................................................................................................11

Risk Assessment...................................................................................................................11

C. Project Alliancing................................................................................................................12

Project Alliance for the Development Company.................................................................12

Advantages of Project Alliance............................................................................................12

Disadvantages of Project Alliance.......................................................................................13

Suggestions..........................................................................................................................13

Feasibility of adopting Project Alliancing...........................................................................13

Success factors.....................................................................................................................13

Challenges............................................................................................................................14

3

D. Cost Control and Reduction Strategies...............................................................................14

Cost Leadership....................................................................................................................14

Differentiation......................................................................................................................15

Focussed Low Cost..............................................................................................................15

Focussed Differentiation......................................................................................................16

Integrated Low Cost.............................................................................................................16

Reference List..........................................................................................................................17

D. Cost Control and Reduction Strategies...............................................................................14

Cost Leadership....................................................................................................................14

Differentiation......................................................................................................................15

Focussed Low Cost..............................................................................................................15

Focussed Differentiation......................................................................................................16

Integrated Low Cost.............................................................................................................16

Reference List..........................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

A. Key Developmental Conditions

Investment decisions refer to those decisions that the investors and top-level managers

undertake related to the amount of funds that are contributed in a particular investment

opportunity (Brealey, Myers & Marcus, 2012). These further determine the amount of capital

that will be spent and the debt acquired for making a profit. Thus, an investment decision is

carried out between an investor and investment advisors. Investments can include either

purchase of financial instruments and assets for gaining profitable income or appreciation of

the value of the investment made (Fabozzi, 2018). Some of the major factors that are

considered by the financier before making an investment decision include risk tolerance or

appetite, return or profits, tax exposure, market trends and investment horizon.

Risk Tolerance or Appetite

Risk tolerance refers to the variability in the returns of an investment that an investor is able

to endure (Frank & Hesse, 2009). It is one of the principle conditions of an investment

decision. A financier must have clear understanding about his or her ability and willingness

of risk appetite before making any investment decision to withstand the large swings in the

value of the investment. Investors carry out risk-related surveys and questionnaires for

analysing the risk associated with a particular investment opportunity. Furthermore, he or she

can also review the worst-case scenarios of returns in different asset classes to retrieve an

idea about the potential loss that might occur during bad years of investment. In addition,

various other factors related to risk tolerance include time horizon of investment, future

earning capacity, home pension and social security (Roszkowski & Davey, 2010). All these

factors influence the risk appetite of an investor largely. Risk tolerance can be of three types,

namely, aggressive risk tolerance, moderate risk tolerance and conservative risk tolerance.

Aggressive risk tolerant investors are likely to be market-savvy and possess an in-depth

understanding of different asset classes and securities (Frijns, Gilbert, Lehnert & Tourani-

Rad, 2013). This enables them to purchase highly volatile instruments of small company

stocks or option contracts having no worth in the market. Moderate investors undertake a

balanced approach for tolerating risk with a time horizon ranging between five to ten years

(Frank & Hesse, 2009). They tend to invest in large company mutual funds possessing less

volatile bonds and riskless securities. Finally, the conservative investors are risk averse and

are not willing to accept any volatility in their investment portfolios.

A. Key Developmental Conditions

Investment decisions refer to those decisions that the investors and top-level managers

undertake related to the amount of funds that are contributed in a particular investment

opportunity (Brealey, Myers & Marcus, 2012). These further determine the amount of capital

that will be spent and the debt acquired for making a profit. Thus, an investment decision is

carried out between an investor and investment advisors. Investments can include either

purchase of financial instruments and assets for gaining profitable income or appreciation of

the value of the investment made (Fabozzi, 2018). Some of the major factors that are

considered by the financier before making an investment decision include risk tolerance or

appetite, return or profits, tax exposure, market trends and investment horizon.

Risk Tolerance or Appetite

Risk tolerance refers to the variability in the returns of an investment that an investor is able

to endure (Frank & Hesse, 2009). It is one of the principle conditions of an investment

decision. A financier must have clear understanding about his or her ability and willingness

of risk appetite before making any investment decision to withstand the large swings in the

value of the investment. Investors carry out risk-related surveys and questionnaires for

analysing the risk associated with a particular investment opportunity. Furthermore, he or she

can also review the worst-case scenarios of returns in different asset classes to retrieve an

idea about the potential loss that might occur during bad years of investment. In addition,

various other factors related to risk tolerance include time horizon of investment, future

earning capacity, home pension and social security (Roszkowski & Davey, 2010). All these

factors influence the risk appetite of an investor largely. Risk tolerance can be of three types,

namely, aggressive risk tolerance, moderate risk tolerance and conservative risk tolerance.

Aggressive risk tolerant investors are likely to be market-savvy and possess an in-depth

understanding of different asset classes and securities (Frijns, Gilbert, Lehnert & Tourani-

Rad, 2013). This enables them to purchase highly volatile instruments of small company

stocks or option contracts having no worth in the market. Moderate investors undertake a

balanced approach for tolerating risk with a time horizon ranging between five to ten years

(Frank & Hesse, 2009). They tend to invest in large company mutual funds possessing less

volatile bonds and riskless securities. Finally, the conservative investors are risk averse and

are not willing to accept any volatility in their investment portfolios.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Return or Profits

The primary reason for investing in an opportunity is to acquire returns of profits from it.

This return can be analysed from the amount of net profit from an investment in comparison

to the total funds or capital invested in it (Phillips, 2012). Thus, return on investment is an

important factor for financiers to evaluate the attractiveness of an investment opportunity.

Many new investors lose their money because they pursue investments in various bonds,

stocks, mutual funds or real asset that have unrealistic rates of returns (Phillips, 2012). Thus,

it essential for the investors to effectively evaluate the return on investment of a project,

company or opportunity by identifying the expected net profits for the past few years.

Tax Exposure

It is essential for the investors to gain tax efficiency for maximizing their returns from the

investments. Tax efficiency measures the returns left after paying off the taxes (Damodaran,

2012). Depending on investment incomes rather than price volatility for generating returns

makes an investor less tax efficient. The structure of accounts under the law affects the tax

efficient investing of the investors. These structures can be of three types, namely taxable, tax

deferred and tax exempt (Gaertner, 2014). Taxable accounts consist of joint investment and

individual accounts, money market mutual funds and bank accounts. For these accounts,

investors are liable to pay taxes on the income received. Furthermore, tax deferred accounts

cover the investment income from various taxes until they remain in some specified accounts

(Doerrenberg, Duncan & Zeppenfeld, 2015). On the other hand, in case of tax-exempt

accounts, investors are free from paying any taxes even at the time of withdrawal (Elton, et

al., 2009).

Market Trends

The movements in the overall economy affect the financial markets and consumer trends

largely (Damodaran, 2012). This in turn encourages the investors and financiers to analyse

the trend in the market for assuming corporate growth and investment attractiveness. Without

interpreting the fundamental trends in the market, volatility in the prices of commodities and

assets can increase, which consequently leads to faulty prediction of risks and returns of the

investments (Damodaran, 2012). The major market forces in the economy that influences the

investing decisions of the financiers include government intervention, international

transactions, speculation and expectation and supply and demand. The fiscal and monetary

policies that the government and central bank control have an impact on the financial markets

(Damodaran, 2012).

Return or Profits

The primary reason for investing in an opportunity is to acquire returns of profits from it.

This return can be analysed from the amount of net profit from an investment in comparison

to the total funds or capital invested in it (Phillips, 2012). Thus, return on investment is an

important factor for financiers to evaluate the attractiveness of an investment opportunity.

Many new investors lose their money because they pursue investments in various bonds,

stocks, mutual funds or real asset that have unrealistic rates of returns (Phillips, 2012). Thus,

it essential for the investors to effectively evaluate the return on investment of a project,

company or opportunity by identifying the expected net profits for the past few years.

Tax Exposure

It is essential for the investors to gain tax efficiency for maximizing their returns from the

investments. Tax efficiency measures the returns left after paying off the taxes (Damodaran,

2012). Depending on investment incomes rather than price volatility for generating returns

makes an investor less tax efficient. The structure of accounts under the law affects the tax

efficient investing of the investors. These structures can be of three types, namely taxable, tax

deferred and tax exempt (Gaertner, 2014). Taxable accounts consist of joint investment and

individual accounts, money market mutual funds and bank accounts. For these accounts,

investors are liable to pay taxes on the income received. Furthermore, tax deferred accounts

cover the investment income from various taxes until they remain in some specified accounts

(Doerrenberg, Duncan & Zeppenfeld, 2015). On the other hand, in case of tax-exempt

accounts, investors are free from paying any taxes even at the time of withdrawal (Elton, et

al., 2009).

Market Trends

The movements in the overall economy affect the financial markets and consumer trends

largely (Damodaran, 2012). This in turn encourages the investors and financiers to analyse

the trend in the market for assuming corporate growth and investment attractiveness. Without

interpreting the fundamental trends in the market, volatility in the prices of commodities and

assets can increase, which consequently leads to faulty prediction of risks and returns of the

investments (Damodaran, 2012). The major market forces in the economy that influences the

investing decisions of the financiers include government intervention, international

transactions, speculation and expectation and supply and demand. The fiscal and monetary

policies that the government and central bank control have an impact on the financial markets

(Damodaran, 2012).

6

Investment Horizons

Investment horizon refers to the total time period during which the investor holds a portfolio

or security (Elton, et al., 2009). It ranges from short-terms of few days to longer-terms of

spanning decades. This length of the investment horizon recognizes the risk associated with

an investment opportunity and consequently, determines the income needs of an investor.

Thus, investors with low risk appetite engage in opportunities that have shorter investment

horizon (Elton, et al., 2009). Furthermore, it can be said that forming an investment horizon is

the first step of the investor while constructing an investment portfolio. Investors having

longer investment horizons prefer to take on more risky projects for investment as the market

then possess a longer duration of recovery in case of any downturn (Elton, et al., 2009).

B. Key assumptions, constraints and conditions of CBA

In order to reach a consensus by the senior management while approving a business project, it

is important to outline the assumptions and constraints of the business (Frew, 2010). The

success of the project could be undermined if these assumptions of the project and related

constraints are not identified. The expected costs and the potential benefits of project could

be altered or changed if there are any sorts of changes in the project’s assumptions,

constraints and conditions.

Assumptions

The analysis of a project is based on the present and the future environment which are

described by Assumptions (Frew,2010). These could include, the data and information about

the expected costs, important statistics, potential benefit values, etc. which are used in a

project analysis and are assumed to be correct, valid and reliable; Change in the outcomes of

the analysis due to inaccurate and invalid data; Expected life of the project.

For this project, the budget proposed by the senior management is $20 million. The costs, that

is the overall expenditure which the business and responsible management of the project

would incur, would be analysed and discussed in the project ahead. Finally, the benefits

which would be gained out of developing the project would be discussed as well.

Constraints

A project development as a whole or performance data availability from current systems can

be limited by certain external factors known as Constraints (Quah & Haldane, 2007). The

constraints would include factors such as the latest technology which is used, should be

implemented in such a way that the minimum business requirements of the project are met.

Investment Horizons

Investment horizon refers to the total time period during which the investor holds a portfolio

or security (Elton, et al., 2009). It ranges from short-terms of few days to longer-terms of

spanning decades. This length of the investment horizon recognizes the risk associated with

an investment opportunity and consequently, determines the income needs of an investor.

Thus, investors with low risk appetite engage in opportunities that have shorter investment

horizon (Elton, et al., 2009). Furthermore, it can be said that forming an investment horizon is

the first step of the investor while constructing an investment portfolio. Investors having

longer investment horizons prefer to take on more risky projects for investment as the market

then possess a longer duration of recovery in case of any downturn (Elton, et al., 2009).

B. Key assumptions, constraints and conditions of CBA

In order to reach a consensus by the senior management while approving a business project, it

is important to outline the assumptions and constraints of the business (Frew, 2010). The

success of the project could be undermined if these assumptions of the project and related

constraints are not identified. The expected costs and the potential benefits of project could

be altered or changed if there are any sorts of changes in the project’s assumptions,

constraints and conditions.

Assumptions

The analysis of a project is based on the present and the future environment which are

described by Assumptions (Frew,2010). These could include, the data and information about

the expected costs, important statistics, potential benefit values, etc. which are used in a

project analysis and are assumed to be correct, valid and reliable; Change in the outcomes of

the analysis due to inaccurate and invalid data; Expected life of the project.

For this project, the budget proposed by the senior management is $20 million. The costs, that

is the overall expenditure which the business and responsible management of the project

would incur, would be analysed and discussed in the project ahead. Finally, the benefits

which would be gained out of developing the project would be discussed as well.

Constraints

A project development as a whole or performance data availability from current systems can

be limited by certain external factors known as Constraints (Quah & Haldane, 2007). The

constraints would include factors such as the latest technology which is used, should be

implemented in such a way that the minimum business requirements of the project are met.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

The investments and certain programs might also be considered which have the possibilities

of becoming cost ineffective at a later point of time.

For this project, the latest technology would be used in the infrastructure building process, so

that the physical platform of the business is setup in the earliest of time that would in turn

enable the onset of the retail businesses of the shops.

Conditions

The factors of the operating environment of any project that can impact the system processes

are known as Conditions (Boardman, Greenberg, Vining & Weimer,2017.). The conditions

for this project can include the technologies which are used for supporting the coordination

into the proposed or existing environments. If duplicate production platforms, systems and

process are used, Redundant investment should be included in the conditions. Finally, the

technical standards of the organisation should be adhered by all the systems.

CBA Analysis

A systematic approach which is used in determining and comparing the costs and the

potential benefits of a project, business or any course of action within a given period of time,

is known as a Cost-Benefit Analysis (Nas, 2016).

Costs

The value of goods and services that are used in the production and operation of a project are

known as Costs, which can also be referred as Inputs (Turner, 2014). The costs that would be

needed for the designing, installing, developing, operating, maintaining, consumables and

disposal for the system that is purposed, would be represented in the cost analysis section. All

the costs that would be needed for developing and operating each alternative, including the

recurring as well as the one-time costs, would be included here.

The construction project of shopping malls is different from that of other single retail store

projects since there is a huge size difference, the configurations and techniques of

construction are different and difficult site conditions causes a great deal of variation.

Architects and architectural firms are needed for the infrastructure planning, designing and

development of shopping malls. Additionally, contractors, subcontractors and cooperative

developers would be needed for getting the job done within a short period of time.

In the project, the infrastructure size should be estimated around 56,212 square feet and

should be double floored. In order to keep bonding and insurance prices low, certain

The investments and certain programs might also be considered which have the possibilities

of becoming cost ineffective at a later point of time.

For this project, the latest technology would be used in the infrastructure building process, so

that the physical platform of the business is setup in the earliest of time that would in turn

enable the onset of the retail businesses of the shops.

Conditions

The factors of the operating environment of any project that can impact the system processes

are known as Conditions (Boardman, Greenberg, Vining & Weimer,2017.). The conditions

for this project can include the technologies which are used for supporting the coordination

into the proposed or existing environments. If duplicate production platforms, systems and

process are used, Redundant investment should be included in the conditions. Finally, the

technical standards of the organisation should be adhered by all the systems.

CBA Analysis

A systematic approach which is used in determining and comparing the costs and the

potential benefits of a project, business or any course of action within a given period of time,

is known as a Cost-Benefit Analysis (Nas, 2016).

Costs

The value of goods and services that are used in the production and operation of a project are

known as Costs, which can also be referred as Inputs (Turner, 2014). The costs that would be

needed for the designing, installing, developing, operating, maintaining, consumables and

disposal for the system that is purposed, would be represented in the cost analysis section. All

the costs that would be needed for developing and operating each alternative, including the

recurring as well as the one-time costs, would be included here.

The construction project of shopping malls is different from that of other single retail store

projects since there is a huge size difference, the configurations and techniques of

construction are different and difficult site conditions causes a great deal of variation.

Architects and architectural firms are needed for the infrastructure planning, designing and

development of shopping malls. Additionally, contractors, subcontractors and cooperative

developers would be needed for getting the job done within a short period of time.

In the project, the infrastructure size should be estimated around 56,212 square feet and

should be double floored. In order to keep bonding and insurance prices low, certain

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

materials and techniques of the best classifications are used by the project developer of

shopping malls. In this project, an average of $20 million would be required for its

completion. The raw materials and equipment that would be needed would cost around $10

million, the cost of labour would be $8 million. Finally, the cost of the machineries would

stand at around $1 million.

If the overall costs are broken down, the following considerations should be taken into

account:- Reinforced concrete foundation; Carpet floors and sheet vinyl; Interior walls, Steel

beam walls; Acoustic ceiling; Fluorescent lighting; Exterior wall designs; Plumbing; Display

fronts (including float glass doors for entrances); Colling and heating systems; Security

systems (including heat or fire detectors); Communication systems; Elevators, Escalators and

stairwells; Services of carpenter, electricals, painting, masonry, etc.; Mezzanines and office

space; Doors, partitions and other property improvements.

The architects and the contracts are relied upon by project owners. Approximately 17 % of

the total building budget will be required by the architect. The architectural team or the

architect would help in determining the overall scope of the project and in establishment of a

preliminary budget. They would draft a list of the budget, work and plan outline that is

proposed. Schematic design would be created and floor plans would be drafted which would

further be verified by planning agencies. The construction documents would be completed

and administered by them. Eth architect of the project is entitled for receiving $3 million for

the services provided.

The contractors would require 14% of the total budget of the project which would entitle

them to receive an amount of $2.5 million. The materials and the services that would be

required for the job would be provided by the contractors, the subcontractors would be hired;

plans and ideas of architecture would be suggested; Final clean-up would be delivered, etc.

Table 1: Costs

Costs Amount ($, in millions)

Development Costs 3

Operational Costs 5

Non-recurring costs 4.4

Recurring Costs 3.6

Total 16

materials and techniques of the best classifications are used by the project developer of

shopping malls. In this project, an average of $20 million would be required for its

completion. The raw materials and equipment that would be needed would cost around $10

million, the cost of labour would be $8 million. Finally, the cost of the machineries would

stand at around $1 million.

If the overall costs are broken down, the following considerations should be taken into

account:- Reinforced concrete foundation; Carpet floors and sheet vinyl; Interior walls, Steel

beam walls; Acoustic ceiling; Fluorescent lighting; Exterior wall designs; Plumbing; Display

fronts (including float glass doors for entrances); Colling and heating systems; Security

systems (including heat or fire detectors); Communication systems; Elevators, Escalators and

stairwells; Services of carpenter, electricals, painting, masonry, etc.; Mezzanines and office

space; Doors, partitions and other property improvements.

The architects and the contracts are relied upon by project owners. Approximately 17 % of

the total building budget will be required by the architect. The architectural team or the

architect would help in determining the overall scope of the project and in establishment of a

preliminary budget. They would draft a list of the budget, work and plan outline that is

proposed. Schematic design would be created and floor plans would be drafted which would

further be verified by planning agencies. The construction documents would be completed

and administered by them. Eth architect of the project is entitled for receiving $3 million for

the services provided.

The contractors would require 14% of the total budget of the project which would entitle

them to receive an amount of $2.5 million. The materials and the services that would be

required for the job would be provided by the contractors, the subcontractors would be hired;

plans and ideas of architecture would be suggested; Final clean-up would be delivered, etc.

Table 1: Costs

Costs Amount ($, in millions)

Development Costs 3

Operational Costs 5

Non-recurring costs 4.4

Recurring Costs 3.6

Total 16

9

The development costs would include the costs for equipment, personnel, training and

development of workers, software packages and licenses. The major categories of costs that

would be included in the operational section would be costs for commercial software,

personnel, contractors, facilities, infrastructure and raw materials and supplies. The non-

recurring costs are associated to the designing, developing, installing, operating, maintaining

and disposal of the system. They are comprised of capital investment and other non-recurring

costs. The capital investment costs would include costs for the procurement, development and

installation of – Air conditioning devices, communication tools, database, equipment of

privacy and security, facilities, software and licenses, vehicles and supplies. The other non-

recurring costs would include costs for the purposes of research, preparation of database,

procurement, conversion of data and software, training, etc. Finally, the recurring costs of the

operations and maintenance would include costs for - Rental, lease and maintenance of data

communications, equipment & software, overhead expenses, wages of workers, utilities and

supplies, etc.

Benefits

The value of the services that are provided by the completion of a project are known as the

benefits (Kerzner and Kerzner, 2017). These can also be referred as the outputs of the project.

Following is table that shows the benefits of development of the project.

Table 2: Benefits

Benefits Amount ($, in millions)

Tangible benefits 24

Intangible benefits 19

Total 43

The tangible benefits would include the sales that would be generated and contributed by all

retail stores of the mall, streamlined production, increased revenue and the saved money and

time, which would derive $24 million annually. The intangible benefits would include

improvements in performance, decision-making, enhancement in the reliability

ofinformation, etc., which would generate an estimate of $19 million for the year.

The development costs would include the costs for equipment, personnel, training and

development of workers, software packages and licenses. The major categories of costs that

would be included in the operational section would be costs for commercial software,

personnel, contractors, facilities, infrastructure and raw materials and supplies. The non-

recurring costs are associated to the designing, developing, installing, operating, maintaining

and disposal of the system. They are comprised of capital investment and other non-recurring

costs. The capital investment costs would include costs for the procurement, development and

installation of – Air conditioning devices, communication tools, database, equipment of

privacy and security, facilities, software and licenses, vehicles and supplies. The other non-

recurring costs would include costs for the purposes of research, preparation of database,

procurement, conversion of data and software, training, etc. Finally, the recurring costs of the

operations and maintenance would include costs for - Rental, lease and maintenance of data

communications, equipment & software, overhead expenses, wages of workers, utilities and

supplies, etc.

Benefits

The value of the services that are provided by the completion of a project are known as the

benefits (Kerzner and Kerzner, 2017). These can also be referred as the outputs of the project.

Following is table that shows the benefits of development of the project.

Table 2: Benefits

Benefits Amount ($, in millions)

Tangible benefits 24

Intangible benefits 19

Total 43

The tangible benefits would include the sales that would be generated and contributed by all

retail stores of the mall, streamlined production, increased revenue and the saved money and

time, which would derive $24 million annually. The intangible benefits would include

improvements in performance, decision-making, enhancement in the reliability

ofinformation, etc., which would generate an estimate of $19 million for the year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

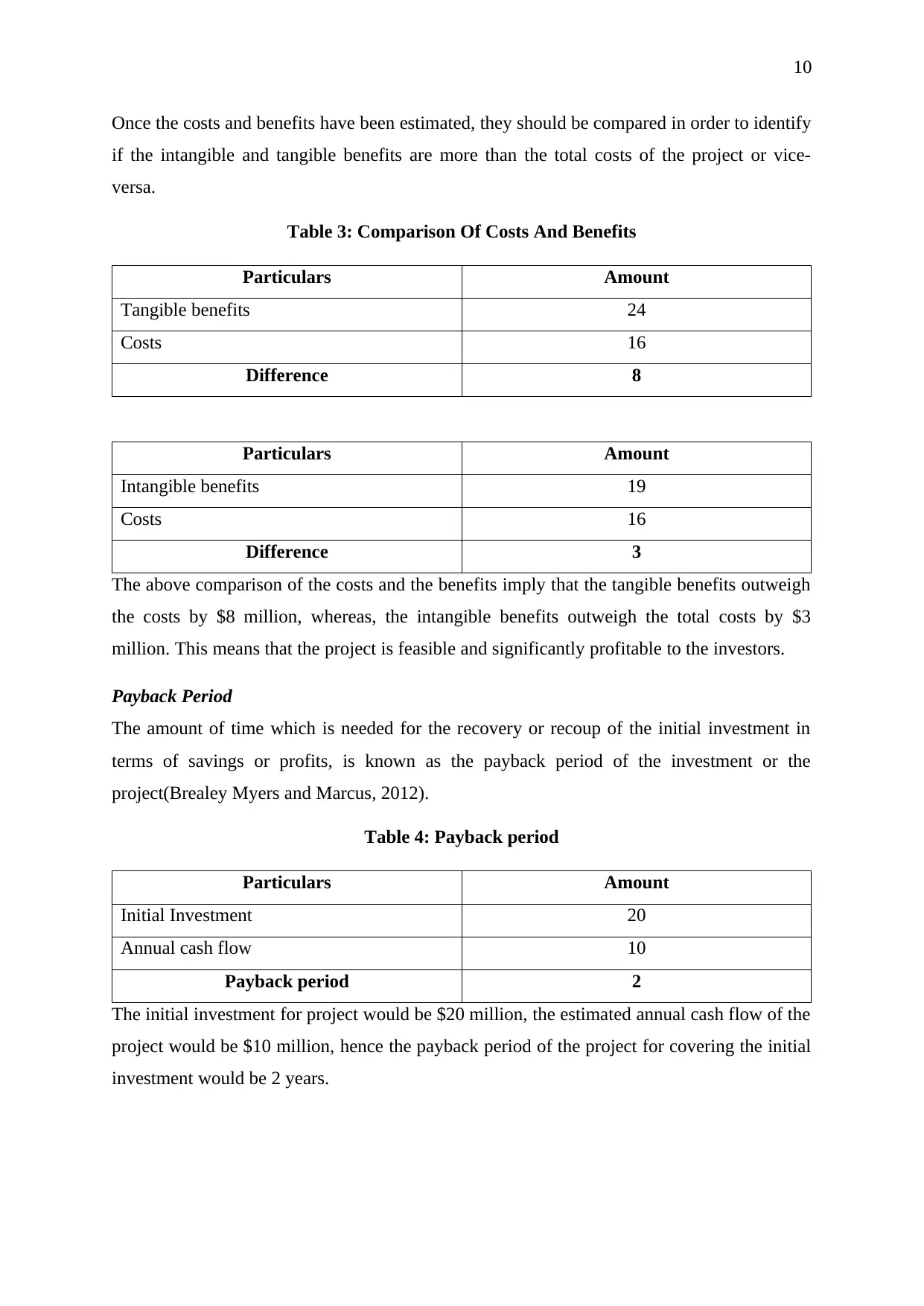

Once the costs and benefits have been estimated, they should be compared in order to identify

if the intangible and tangible benefits are more than the total costs of the project or vice-

versa.

Table 3: Comparison Of Costs And Benefits

Particulars Amount

Tangible benefits 24

Costs 16

Difference 8

Particulars Amount

Intangible benefits 19

Costs 16

Difference 3

The above comparison of the costs and the benefits imply that the tangible benefits outweigh

the costs by $8 million, whereas, the intangible benefits outweigh the total costs by $3

million. This means that the project is feasible and significantly profitable to the investors.

Payback Period

The amount of time which is needed for the recovery or recoup of the initial investment in

terms of savings or profits, is known as the payback period of the investment or the

project(Brealey Myers and Marcus, 2012).

Table 4: Payback period

Particulars Amount

Initial Investment 20

Annual cash flow 10

Payback period 2

The initial investment for project would be $20 million, the estimated annual cash flow of the

project would be $10 million, hence the payback period of the project for covering the initial

investment would be 2 years.

Once the costs and benefits have been estimated, they should be compared in order to identify

if the intangible and tangible benefits are more than the total costs of the project or vice-

versa.

Table 3: Comparison Of Costs And Benefits

Particulars Amount

Tangible benefits 24

Costs 16

Difference 8

Particulars Amount

Intangible benefits 19

Costs 16

Difference 3

The above comparison of the costs and the benefits imply that the tangible benefits outweigh

the costs by $8 million, whereas, the intangible benefits outweigh the total costs by $3

million. This means that the project is feasible and significantly profitable to the investors.

Payback Period

The amount of time which is needed for the recovery or recoup of the initial investment in

terms of savings or profits, is known as the payback period of the investment or the

project(Brealey Myers and Marcus, 2012).

Table 4: Payback period

Particulars Amount

Initial Investment 20

Annual cash flow 10

Payback period 2

The initial investment for project would be $20 million, the estimated annual cash flow of the

project would be $10 million, hence the payback period of the project for covering the initial

investment would be 2 years.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

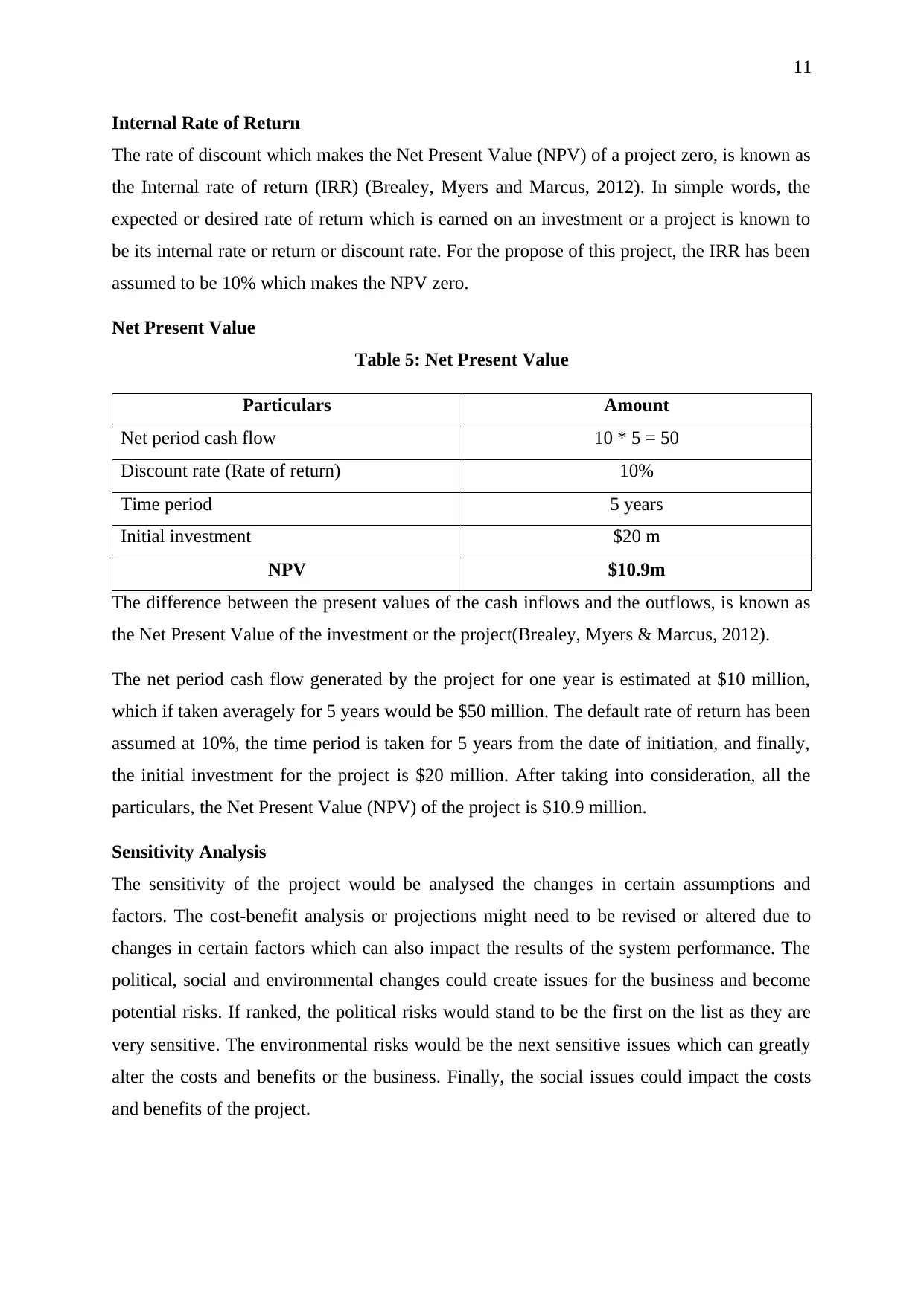

Internal Rate of Return

The rate of discount which makes the Net Present Value (NPV) of a project zero, is known as

the Internal rate of return (IRR) (Brealey, Myers and Marcus, 2012). In simple words, the

expected or desired rate of return which is earned on an investment or a project is known to

be its internal rate or return or discount rate. For the propose of this project, the IRR has been

assumed to be 10% which makes the NPV zero.

Net Present Value

Table 5: Net Present Value

Particulars Amount

Net period cash flow 10 * 5 = 50

Discount rate (Rate of return) 10%

Time period 5 years

Initial investment $20 m

NPV $10.9m

The difference between the present values of the cash inflows and the outflows, is known as

the Net Present Value of the investment or the project(Brealey, Myers & Marcus, 2012).

The net period cash flow generated by the project for one year is estimated at $10 million,

which if taken averagely for 5 years would be $50 million. The default rate of return has been

assumed at 10%, the time period is taken for 5 years from the date of initiation, and finally,

the initial investment for the project is $20 million. After taking into consideration, all the

particulars, the Net Present Value (NPV) of the project is $10.9 million.

Sensitivity Analysis

The sensitivity of the project would be analysed the changes in certain assumptions and

factors. The cost-benefit analysis or projections might need to be revised or altered due to

changes in certain factors which can also impact the results of the system performance. The

political, social and environmental changes could create issues for the business and become

potential risks. If ranked, the political risks would stand to be the first on the list as they are

very sensitive. The environmental risks would be the next sensitive issues which can greatly

alter the costs and benefits or the business. Finally, the social issues could impact the costs

and benefits of the project.

Internal Rate of Return

The rate of discount which makes the Net Present Value (NPV) of a project zero, is known as

the Internal rate of return (IRR) (Brealey, Myers and Marcus, 2012). In simple words, the

expected or desired rate of return which is earned on an investment or a project is known to

be its internal rate or return or discount rate. For the propose of this project, the IRR has been

assumed to be 10% which makes the NPV zero.

Net Present Value

Table 5: Net Present Value

Particulars Amount

Net period cash flow 10 * 5 = 50

Discount rate (Rate of return) 10%

Time period 5 years

Initial investment $20 m

NPV $10.9m

The difference between the present values of the cash inflows and the outflows, is known as

the Net Present Value of the investment or the project(Brealey, Myers & Marcus, 2012).

The net period cash flow generated by the project for one year is estimated at $10 million,

which if taken averagely for 5 years would be $50 million. The default rate of return has been

assumed at 10%, the time period is taken for 5 years from the date of initiation, and finally,

the initial investment for the project is $20 million. After taking into consideration, all the

particulars, the Net Present Value (NPV) of the project is $10.9 million.

Sensitivity Analysis

The sensitivity of the project would be analysed the changes in certain assumptions and

factors. The cost-benefit analysis or projections might need to be revised or altered due to

changes in certain factors which can also impact the results of the system performance. The

political, social and environmental changes could create issues for the business and become

potential risks. If ranked, the political risks would stand to be the first on the list as they are

very sensitive. The environmental risks would be the next sensitive issues which can greatly

alter the costs and benefits or the business. Finally, the social issues could impact the costs

and benefits of the project.

12

Risk Assessment

In order to safeguard a project or business against certain risks, risk identification and

assessment is a must. When there is a possibility of the capital investment unable to achieve

the expected outcomes or benefits due to certain difficulties, it is called investment risk.

Development of a shopping mall involves a high amount of investment risk;therefore, it is

necessary to frame a detailed risk evaluation and analysis. There are several types of risks

associated to the project of shopping mall. These are risk or operations and management,

financial risk, risk of construction period, sale price risk, risk of construction quality,

designing risk, risk of checking and completion. Other risks can be political risks, such as

change in policies and regulations of trade and business by the government, unfavourable

political environment, etc.; Social risks such as change in taste and preferences of consumers,

change in fashion trends, change in lifestyle and habits of people, etc. Environmental risks,

such as wastes generated by a retail store could hamper the environment, due to which its

operations can be stopped.

C. Project Alliancing

It is an important method for delivering of project. A joint contract is made between two

parties where both the parties agree to take joint responsibility for carrying out the project. In

case of project alliancing both the parties should be equally responsible for both the negative

and positive risk involved in the project. Alliancing is generally done to reduce the negative

impacts of the traditional system (Young, Hosseini & Lædre, 2016). One of the important

characteristics of Project Alliancing is contract between multiple parties with equal liability.

The first project alliancing was introduced in Australia (Fernandes, Costa & Lahdenperä,

2017) Various projects like railway, road and other infrastructural projects use this approach.

It is very important for the sub-contractors to take part when the project alliance is going on.

Project Alliance for the Development Company

The company, which is based in wellington and mainly operating in various parts of New

Zealand, can go through the concept of project alliance to increase the effectiveness of the

production. A company, which is mainly in to the development business, focuses on

construction of buildings, roads and other infrastructure related projects. To enhance the

business in a positive way the alliance or the agreement can be made with any designing

company widely operating in New Zealand. A company, which is mainly in to designing, is

chosen because a development company, which is mainly involved in the construction of a

building, can easily synchronize with the designing company. A client who has given money

Risk Assessment

In order to safeguard a project or business against certain risks, risk identification and

assessment is a must. When there is a possibility of the capital investment unable to achieve

the expected outcomes or benefits due to certain difficulties, it is called investment risk.

Development of a shopping mall involves a high amount of investment risk;therefore, it is

necessary to frame a detailed risk evaluation and analysis. There are several types of risks

associated to the project of shopping mall. These are risk or operations and management,

financial risk, risk of construction period, sale price risk, risk of construction quality,

designing risk, risk of checking and completion. Other risks can be political risks, such as

change in policies and regulations of trade and business by the government, unfavourable

political environment, etc.; Social risks such as change in taste and preferences of consumers,

change in fashion trends, change in lifestyle and habits of people, etc. Environmental risks,

such as wastes generated by a retail store could hamper the environment, due to which its

operations can be stopped.

C. Project Alliancing

It is an important method for delivering of project. A joint contract is made between two

parties where both the parties agree to take joint responsibility for carrying out the project. In

case of project alliancing both the parties should be equally responsible for both the negative

and positive risk involved in the project. Alliancing is generally done to reduce the negative

impacts of the traditional system (Young, Hosseini & Lædre, 2016). One of the important

characteristics of Project Alliancing is contract between multiple parties with equal liability.

The first project alliancing was introduced in Australia (Fernandes, Costa & Lahdenperä,

2017) Various projects like railway, road and other infrastructural projects use this approach.

It is very important for the sub-contractors to take part when the project alliance is going on.

Project Alliance for the Development Company

The company, which is based in wellington and mainly operating in various parts of New

Zealand, can go through the concept of project alliance to increase the effectiveness of the

production. A company, which is mainly in to the development business, focuses on

construction of buildings, roads and other infrastructure related projects. To enhance the

business in a positive way the alliance or the agreement can be made with any designing

company widely operating in New Zealand. A company, which is mainly in to designing, is

chosen because a development company, which is mainly involved in the construction of a

building, can easily synchronize with the designing company. A client who has given money

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18