Financial Analysis Report: Woodside Petroleum Performance (FBL5030)

VerifiedAdded on 2023/02/01

|23

|6043

|95

Report

AI Summary

This report presents a financial performance analysis of Woodside Petroleum from 2014 to 2018, focusing on profitability, liquidity, and solvency. The analysis employs financial ratio analysis, comparing Woodside's performance with its competitor Santos Limited and industry averages. The report includes an executive summary, introduction, and detailed sections on profitability (operating profit margin, return on equity, net profit margin), liquidity (current ratio, days receivable ratio, acid test ratio), and solvency (debt ratio, equity ratio, interest coverage ratio). The methodology involves gathering financial data from various sources, calculating relevant ratios, and interpreting the results to evaluate Woodside's financial health and growth prospects. The findings suggest that Woodside generally outperforms its competitor and the industry average in key financial metrics, indicating strong operational efficiency and financial stability. The report concludes with a summary of the company's financial performance and potential for future growth, providing valuable insights for investors and stakeholders. The financial data used in the report includes operating profit, net profit, total revenue, shareholder's equity, current assets, and liabilities, among other items.

1

FBL5030

FUNDAMENTALS OF VALUE CREATION IN BUSINESS

Semester 191

ASSIGNMENT - ACCOUNTING

FBL5030

FUNDAMENTALS OF VALUE CREATION IN BUSINESS

Semester 191

ASSIGNMENT - ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive Summary

The present report is developed for analyzing the financial performance of Woodside

Petroleum over the selected financial period of 2014-2018. It focuses on evaluation and

examination of key ratios in relation to profitability, liquidity and solvency position of the

company.

Methodology

The report has adopted the use of financial ratio analysis technique to examine the

financial performance of the selected company. The results obtained are compared with a

selected competitor company, that is, Santos Limited and with the industry average for

facilitating the decision-making of the investors.

Results

The results of the ratio analysis have indicated that its financial performance assessed in

terms of profitability, liquidity and solvency is better as compared with the competitor company

and the overall industry average.

Executive Summary

The present report is developed for analyzing the financial performance of Woodside

Petroleum over the selected financial period of 2014-2018. It focuses on evaluation and

examination of key ratios in relation to profitability, liquidity and solvency position of the

company.

Methodology

The report has adopted the use of financial ratio analysis technique to examine the

financial performance of the selected company. The results obtained are compared with a

selected competitor company, that is, Santos Limited and with the industry average for

facilitating the decision-making of the investors.

Results

The results of the ratio analysis have indicated that its financial performance assessed in

terms of profitability, liquidity and solvency is better as compared with the competitor company

and the overall industry average.

3

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Evaluation of financial performance of Woodside Petroleum with respect to its competitor and

industry average for last five years..................................................................................................4

Profitability Analysis.......................................................................................................................6

Operating Profit Margin (OPM)..................................................................................................6

Return on Equity (ROE)..............................................................................................................7

Net Profit Margin.........................................................................................................................9

Liquidity Analysis.........................................................................................................................10

Current Ratio..............................................................................................................................10

Days Receivable Ratio (DRR)...................................................................................................11

Acid Test Ratio..........................................................................................................................12

Solvency Analysis.........................................................................................................................14

Debt Ratio..................................................................................................................................14

Equity Ratio...............................................................................................................................15

Interest Coverage ratio...............................................................................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................19

Appendix........................................................................................................................................22

Contents

Executive Summary.........................................................................................................................2

Introduction......................................................................................................................................4

Evaluation of financial performance of Woodside Petroleum with respect to its competitor and

industry average for last five years..................................................................................................4

Profitability Analysis.......................................................................................................................6

Operating Profit Margin (OPM)..................................................................................................6

Return on Equity (ROE)..............................................................................................................7

Net Profit Margin.........................................................................................................................9

Liquidity Analysis.........................................................................................................................10

Current Ratio..............................................................................................................................10

Days Receivable Ratio (DRR)...................................................................................................11

Acid Test Ratio..........................................................................................................................12

Solvency Analysis.........................................................................................................................14

Debt Ratio..................................................................................................................................14

Equity Ratio...............................................................................................................................15

Interest Coverage ratio...............................................................................................................16

Conclusion.....................................................................................................................................17

References......................................................................................................................................19

Appendix........................................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

Woodside Petroleum is a recognized company of Australia that is involved in exploring

and developing of petroleum products. The company is recognized to be the largest operator of

oil and gas within Australia and as such is attributed to be the most renowned independent

dedicated oil and gas company. The company is listed on ASX and is headquartered within

Australia. The company has the presence of about 3300 employees for carrying out its

operational activities. It conducts its operations through its different subsidiaries such as

Woodside Finance Limited, Woodside Natural Gas Inc., Woodside Eastern Energy Pty Ltd,

Woodside Energy and others. It has a global presence and is recognized all over the world for its

expertise and capabilities (Woodside Annual Report, 2014). It is an explorer, developer,

producer and supplier of energy that has an international presence and has achieved a leadership

position within the energy sector of Australia owing to the use of its world class capabilities and

expertise. The company conducts its activities with the use of three operational segments that are

liquefied natural gas, oil and liquefied petroleum gas.

This report has undertaken a comparative analysis of the financial performances of the

five year period from 2013-2017. This has been done for examining the financial strategies of the

company by carrying out an evaluation of its financial performance and analyzing its future

growth prospects. The analysis of the financial performance of the company has been undertaken

with the use of ratio analysis technique. The technique of ratio analysis involves evaluating the

financial statements of a company for examining its profitability, liquidity, solvency or market

performance. The report is made of distinct sections for presenting the financial results obtained

with the use of ratio analysis technique. The financial analysis of the company with the use of

ratio analysis has been carried out by examining its profitability, liquidity and solvency position.

The report is structured in the sections consisting of profitability, liquidity and solvency that

have examined the key ratios that provide an insight into its financial performance over the

selected period. Financial performance of Woodside Petroleum has been compared with its

competitor Santos Limited and also with the industry average. Lastly, the conclusion section has

provided a brief summary regarding the financial performance of the company and examining its

future growth prospects (Arnold, 2013).

Evaluation of financial performance of Woodside Petroleum with respect to its competitor

and industry average for last five years

Financial performance of Woodside Petroleum has been evaluated through using the ratio

analysis as the important financial tool. Ratio analysis provides the best medium to evaluate the

financial performance of any company and also allows comparing the performance with past

years as well as from its competitors. Ratio analysis has certain limitations that must be

considered before making any recommendations. Before making the calculation of ratios it is

important to gather relevant data from the prescribed sources (DatAnalysis-Morning Star) so that

Introduction

Woodside Petroleum is a recognized company of Australia that is involved in exploring

and developing of petroleum products. The company is recognized to be the largest operator of

oil and gas within Australia and as such is attributed to be the most renowned independent

dedicated oil and gas company. The company is listed on ASX and is headquartered within

Australia. The company has the presence of about 3300 employees for carrying out its

operational activities. It conducts its operations through its different subsidiaries such as

Woodside Finance Limited, Woodside Natural Gas Inc., Woodside Eastern Energy Pty Ltd,

Woodside Energy and others. It has a global presence and is recognized all over the world for its

expertise and capabilities (Woodside Annual Report, 2014). It is an explorer, developer,

producer and supplier of energy that has an international presence and has achieved a leadership

position within the energy sector of Australia owing to the use of its world class capabilities and

expertise. The company conducts its activities with the use of three operational segments that are

liquefied natural gas, oil and liquefied petroleum gas.

This report has undertaken a comparative analysis of the financial performances of the

five year period from 2013-2017. This has been done for examining the financial strategies of the

company by carrying out an evaluation of its financial performance and analyzing its future

growth prospects. The analysis of the financial performance of the company has been undertaken

with the use of ratio analysis technique. The technique of ratio analysis involves evaluating the

financial statements of a company for examining its profitability, liquidity, solvency or market

performance. The report is made of distinct sections for presenting the financial results obtained

with the use of ratio analysis technique. The financial analysis of the company with the use of

ratio analysis has been carried out by examining its profitability, liquidity and solvency position.

The report is structured in the sections consisting of profitability, liquidity and solvency that

have examined the key ratios that provide an insight into its financial performance over the

selected period. Financial performance of Woodside Petroleum has been compared with its

competitor Santos Limited and also with the industry average. Lastly, the conclusion section has

provided a brief summary regarding the financial performance of the company and examining its

future growth prospects (Arnold, 2013).

Evaluation of financial performance of Woodside Petroleum with respect to its competitor

and industry average for last five years

Financial performance of Woodside Petroleum has been evaluated through using the ratio

analysis as the important financial tool. Ratio analysis provides the best medium to evaluate the

financial performance of any company and also allows comparing the performance with past

years as well as from its competitors. Ratio analysis has certain limitations that must be

considered before making any recommendations. Before making the calculation of ratios it is

important to gather relevant data from the prescribed sources (DatAnalysis-Morning Star) so that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

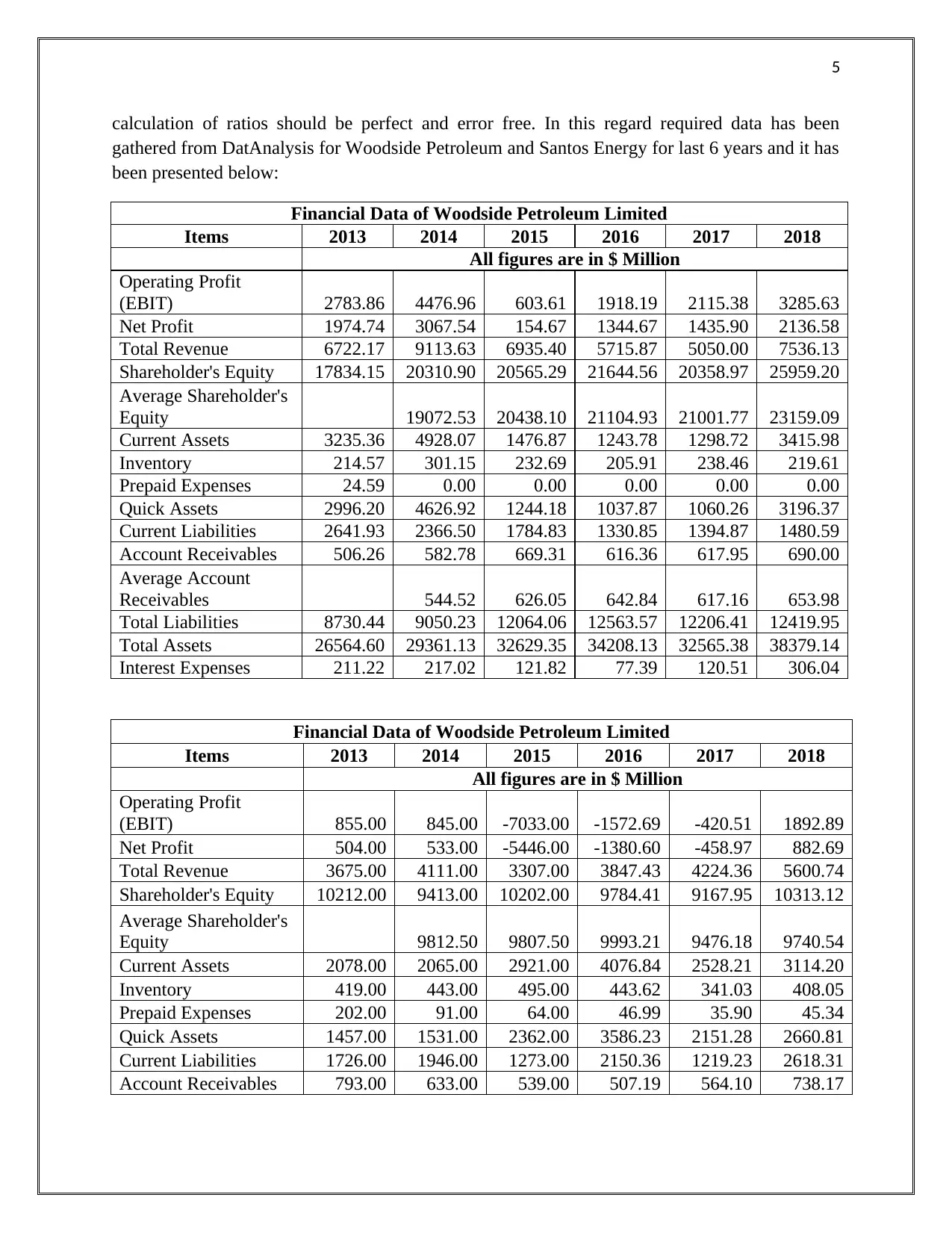

calculation of ratios should be perfect and error free. In this regard required data has been

gathered from DatAnalysis for Woodside Petroleum and Santos Energy for last 6 years and it has

been presented below:

Financial Data of Woodside Petroleum Limited

Items 2013 2014 2015 2016 2017 2018

All figures are in $ Million

Operating Profit

(EBIT) 2783.86 4476.96 603.61 1918.19 2115.38 3285.63

Net Profit 1974.74 3067.54 154.67 1344.67 1435.90 2136.58

Total Revenue 6722.17 9113.63 6935.40 5715.87 5050.00 7536.13

Shareholder's Equity 17834.15 20310.90 20565.29 21644.56 20358.97 25959.20

Average Shareholder's

Equity 19072.53 20438.10 21104.93 21001.77 23159.09

Current Assets 3235.36 4928.07 1476.87 1243.78 1298.72 3415.98

Inventory 214.57 301.15 232.69 205.91 238.46 219.61

Prepaid Expenses 24.59 0.00 0.00 0.00 0.00 0.00

Quick Assets 2996.20 4626.92 1244.18 1037.87 1060.26 3196.37

Current Liabilities 2641.93 2366.50 1784.83 1330.85 1394.87 1480.59

Account Receivables 506.26 582.78 669.31 616.36 617.95 690.00

Average Account

Receivables 544.52 626.05 642.84 617.16 653.98

Total Liabilities 8730.44 9050.23 12064.06 12563.57 12206.41 12419.95

Total Assets 26564.60 29361.13 32629.35 34208.13 32565.38 38379.14

Interest Expenses 211.22 217.02 121.82 77.39 120.51 306.04

Financial Data of Woodside Petroleum Limited

Items 2013 2014 2015 2016 2017 2018

All figures are in $ Million

Operating Profit

(EBIT) 855.00 845.00 -7033.00 -1572.69 -420.51 1892.89

Net Profit 504.00 533.00 -5446.00 -1380.60 -458.97 882.69

Total Revenue 3675.00 4111.00 3307.00 3847.43 4224.36 5600.74

Shareholder's Equity 10212.00 9413.00 10202.00 9784.41 9167.95 10313.12

Average Shareholder's

Equity 9812.50 9807.50 9993.21 9476.18 9740.54

Current Assets 2078.00 2065.00 2921.00 4076.84 2528.21 3114.20

Inventory 419.00 443.00 495.00 443.62 341.03 408.05

Prepaid Expenses 202.00 91.00 64.00 46.99 35.90 45.34

Quick Assets 1457.00 1531.00 2362.00 3586.23 2151.28 2660.81

Current Liabilities 1726.00 1946.00 1273.00 2150.36 1219.23 2618.31

Account Receivables 793.00 633.00 539.00 507.19 564.10 738.17

calculation of ratios should be perfect and error free. In this regard required data has been

gathered from DatAnalysis for Woodside Petroleum and Santos Energy for last 6 years and it has

been presented below:

Financial Data of Woodside Petroleum Limited

Items 2013 2014 2015 2016 2017 2018

All figures are in $ Million

Operating Profit

(EBIT) 2783.86 4476.96 603.61 1918.19 2115.38 3285.63

Net Profit 1974.74 3067.54 154.67 1344.67 1435.90 2136.58

Total Revenue 6722.17 9113.63 6935.40 5715.87 5050.00 7536.13

Shareholder's Equity 17834.15 20310.90 20565.29 21644.56 20358.97 25959.20

Average Shareholder's

Equity 19072.53 20438.10 21104.93 21001.77 23159.09

Current Assets 3235.36 4928.07 1476.87 1243.78 1298.72 3415.98

Inventory 214.57 301.15 232.69 205.91 238.46 219.61

Prepaid Expenses 24.59 0.00 0.00 0.00 0.00 0.00

Quick Assets 2996.20 4626.92 1244.18 1037.87 1060.26 3196.37

Current Liabilities 2641.93 2366.50 1784.83 1330.85 1394.87 1480.59

Account Receivables 506.26 582.78 669.31 616.36 617.95 690.00

Average Account

Receivables 544.52 626.05 642.84 617.16 653.98

Total Liabilities 8730.44 9050.23 12064.06 12563.57 12206.41 12419.95

Total Assets 26564.60 29361.13 32629.35 34208.13 32565.38 38379.14

Interest Expenses 211.22 217.02 121.82 77.39 120.51 306.04

Financial Data of Woodside Petroleum Limited

Items 2013 2014 2015 2016 2017 2018

All figures are in $ Million

Operating Profit

(EBIT) 855.00 845.00 -7033.00 -1572.69 -420.51 1892.89

Net Profit 504.00 533.00 -5446.00 -1380.60 -458.97 882.69

Total Revenue 3675.00 4111.00 3307.00 3847.43 4224.36 5600.74

Shareholder's Equity 10212.00 9413.00 10202.00 9784.41 9167.95 10313.12

Average Shareholder's

Equity 9812.50 9807.50 9993.21 9476.18 9740.54

Current Assets 2078.00 2065.00 2921.00 4076.84 2528.21 3114.20

Inventory 419.00 443.00 495.00 443.62 341.03 408.05

Prepaid Expenses 202.00 91.00 64.00 46.99 35.90 45.34

Quick Assets 1457.00 1531.00 2362.00 3586.23 2151.28 2660.81

Current Liabilities 1726.00 1946.00 1273.00 2150.36 1219.23 2618.31

Account Receivables 793.00 633.00 539.00 507.19 564.10 738.17

6

Average Account

Receivables 713.00 586.00 523.10 535.65 651.14

Total Liabilities 10397.00 12932.00 11724.00 11307.35 8403.85 13962.88

Total Assets 20609.00 22345.00 21926.00 21091.76 17571.79 24276.00

Interest Expenses 62.00 116.00 297.00 409.07 376.92 365.54

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

Note 1: Details of ratio calculation has been shown in appendix for further review.

Note 2: Industry average has been taken from CSI Market (Web-link:

https://csimarket.com/Industry/industry_Financial_Strength_Ratios.php?ind=603)

Profitability Analysis

The profitability analysis is carried out for developing an understanding of the ability of a

company to generate profits from its operational activities. The analysis is useful to examine the

profit generating capacity of a company in relation to other companies operating within the same

industry. The analysis has been carried by calculation of the following ratios and comparing the

results obtained within the competitor data obtained from the financial statements of Santos

Limited, a competitor company of Woodside Energy Ltd.

Operating Profit Margin (OPM)

The operating profit margin ratio is used for examining the effectiveness of a company in

managing its operational costs. The analysis of the operating profit margin is very essential for

the companies operating within the energy sector such as Woodside Petroleum as they have to

consistently modify their production levels due to fluctuations in exchange rates and other

factors which have a large impact on the cost of their operations.

The ratio can be calculated with the use of following formula:

Formula: Earnings before interest and tax (EBIT)/ Total Revenue (Brigham & Michael, 2013)

The evaluation of the operating profit margin ration would help in examining the

potential of a company for realizing future growth. It analyzes the financial position of a

company by evaluating its ability to meet its fixed costs and interest’s obligations. The

companies having higher operating profit margins indicates having a control over their

operational costs and thus realizing higher profits.

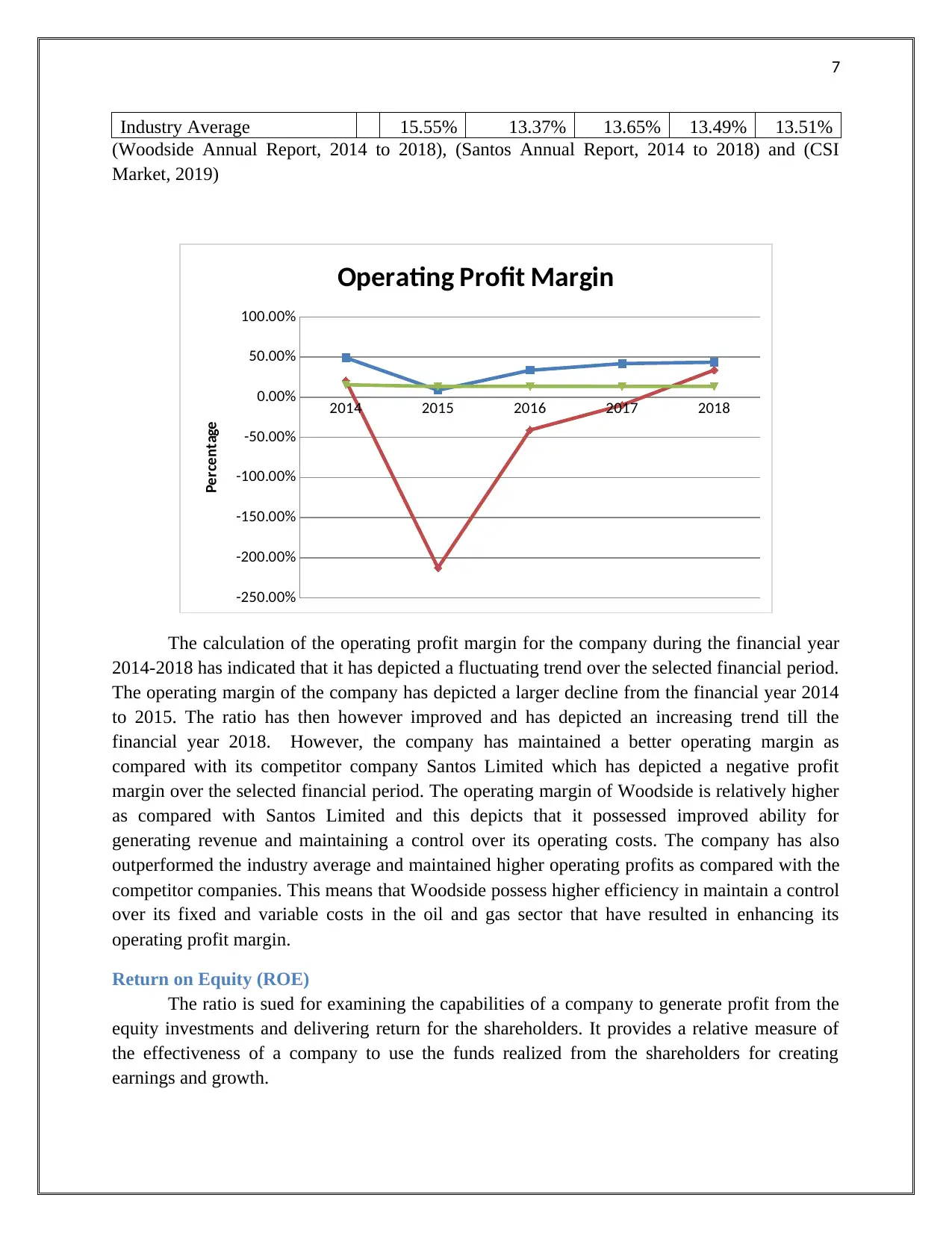

Operating Profit Margin

Ratios 2014 2015 2016 2017 2018

Woodside Petroleum 49.12% 8.70% 33.56% 41.89% 43.60%

Santos Limited 20.55% -212.67% -40.88% -9.95% 33.80%

Average Account

Receivables 713.00 586.00 523.10 535.65 651.14

Total Liabilities 10397.00 12932.00 11724.00 11307.35 8403.85 13962.88

Total Assets 20609.00 22345.00 21926.00 21091.76 17571.79 24276.00

Interest Expenses 62.00 116.00 297.00 409.07 376.92 365.54

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

Note 1: Details of ratio calculation has been shown in appendix for further review.

Note 2: Industry average has been taken from CSI Market (Web-link:

https://csimarket.com/Industry/industry_Financial_Strength_Ratios.php?ind=603)

Profitability Analysis

The profitability analysis is carried out for developing an understanding of the ability of a

company to generate profits from its operational activities. The analysis is useful to examine the

profit generating capacity of a company in relation to other companies operating within the same

industry. The analysis has been carried by calculation of the following ratios and comparing the

results obtained within the competitor data obtained from the financial statements of Santos

Limited, a competitor company of Woodside Energy Ltd.

Operating Profit Margin (OPM)

The operating profit margin ratio is used for examining the effectiveness of a company in

managing its operational costs. The analysis of the operating profit margin is very essential for

the companies operating within the energy sector such as Woodside Petroleum as they have to

consistently modify their production levels due to fluctuations in exchange rates and other

factors which have a large impact on the cost of their operations.

The ratio can be calculated with the use of following formula:

Formula: Earnings before interest and tax (EBIT)/ Total Revenue (Brigham & Michael, 2013)

The evaluation of the operating profit margin ration would help in examining the

potential of a company for realizing future growth. It analyzes the financial position of a

company by evaluating its ability to meet its fixed costs and interest’s obligations. The

companies having higher operating profit margins indicates having a control over their

operational costs and thus realizing higher profits.

Operating Profit Margin

Ratios 2014 2015 2016 2017 2018

Woodside Petroleum 49.12% 8.70% 33.56% 41.89% 43.60%

Santos Limited 20.55% -212.67% -40.88% -9.95% 33.80%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Industry Average 15.55% 13.37% 13.65% 13.49% 13.51%

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

2014 2015 2016 2017 2018

-250.00%

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

Operating Profit Margin

Percentage

The calculation of the operating profit margin for the company during the financial year

2014-2018 has indicated that it has depicted a fluctuating trend over the selected financial period.

The operating margin of the company has depicted a larger decline from the financial year 2014

to 2015. The ratio has then however improved and has depicted an increasing trend till the

financial year 2018. However, the company has maintained a better operating margin as

compared with its competitor company Santos Limited which has depicted a negative profit

margin over the selected financial period. The operating margin of Woodside is relatively higher

as compared with Santos Limited and this depicts that it possessed improved ability for

generating revenue and maintaining a control over its operating costs. The company has also

outperformed the industry average and maintained higher operating profits as compared with the

competitor companies. This means that Woodside possess higher efficiency in maintain a control

over its fixed and variable costs in the oil and gas sector that have resulted in enhancing its

operating profit margin.

Return on Equity (ROE)

The ratio is sued for examining the capabilities of a company to generate profit from the

equity investments and delivering return for the shareholders. It provides a relative measure of

the effectiveness of a company to use the funds realized from the shareholders for creating

earnings and growth.

Industry Average 15.55% 13.37% 13.65% 13.49% 13.51%

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

2014 2015 2016 2017 2018

-250.00%

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

100.00%

Operating Profit Margin

Percentage

The calculation of the operating profit margin for the company during the financial year

2014-2018 has indicated that it has depicted a fluctuating trend over the selected financial period.

The operating margin of the company has depicted a larger decline from the financial year 2014

to 2015. The ratio has then however improved and has depicted an increasing trend till the

financial year 2018. However, the company has maintained a better operating margin as

compared with its competitor company Santos Limited which has depicted a negative profit

margin over the selected financial period. The operating margin of Woodside is relatively higher

as compared with Santos Limited and this depicts that it possessed improved ability for

generating revenue and maintaining a control over its operating costs. The company has also

outperformed the industry average and maintained higher operating profits as compared with the

competitor companies. This means that Woodside possess higher efficiency in maintain a control

over its fixed and variable costs in the oil and gas sector that have resulted in enhancing its

operating profit margin.

Return on Equity (ROE)

The ratio is sued for examining the capabilities of a company to generate profit from the

equity investments and delivering return for the shareholders. It provides a relative measure of

the effectiveness of a company to use the funds realized from the shareholders for creating

earnings and growth.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

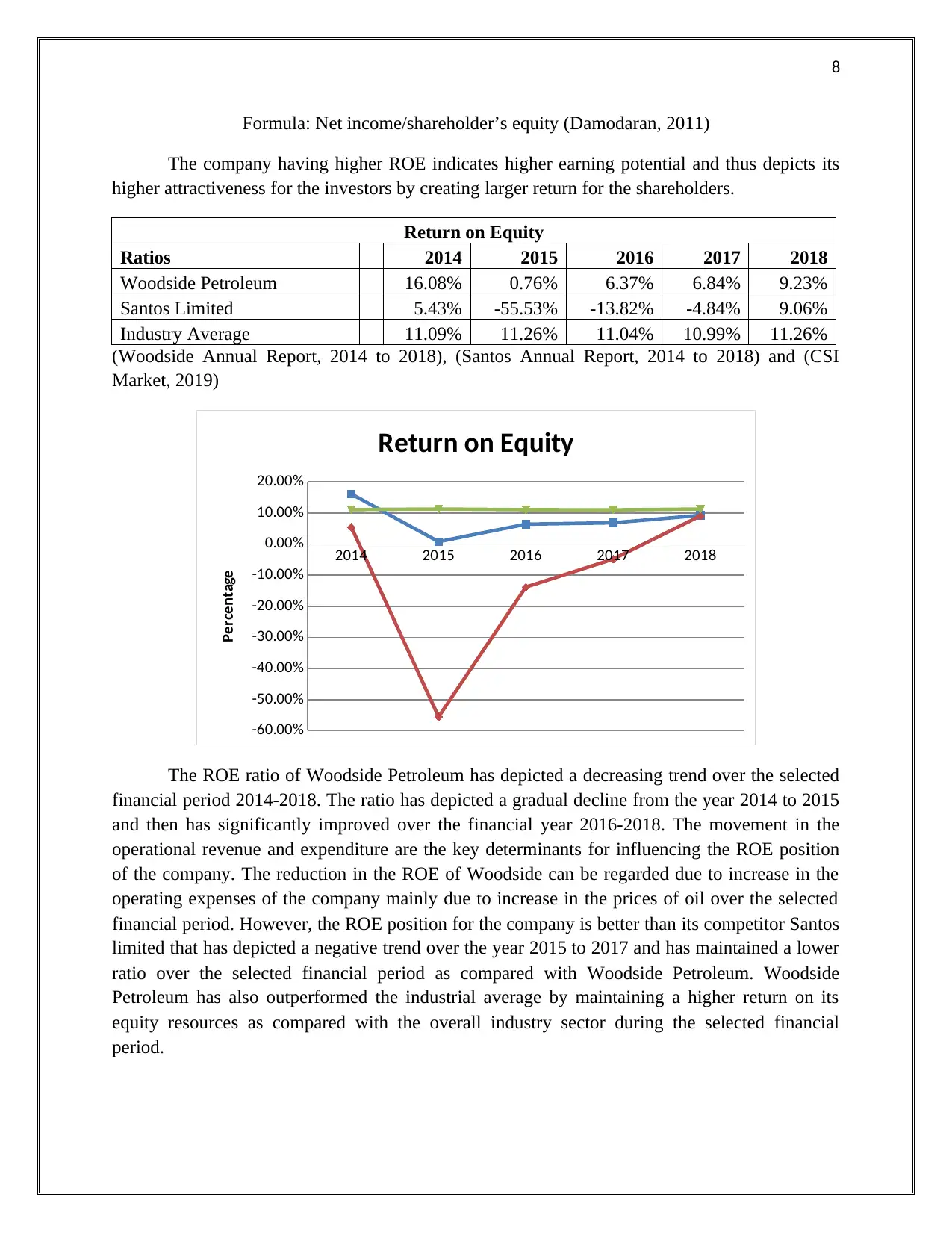

Formula: Net income/shareholder’s equity (Damodaran, 2011)

The company having higher ROE indicates higher earning potential and thus depicts its

higher attractiveness for the investors by creating larger return for the shareholders.

Return on Equity

Ratios 2014 2015 2016 2017 2018

Woodside Petroleum 16.08% 0.76% 6.37% 6.84% 9.23%

Santos Limited 5.43% -55.53% -13.82% -4.84% 9.06%

Industry Average 11.09% 11.26% 11.04% 10.99% 11.26%

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

2014 2015 2016 2017 2018

-60.00%

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

Return on Equity

Percentage

The ROE ratio of Woodside Petroleum has depicted a decreasing trend over the selected

financial period 2014-2018. The ratio has depicted a gradual decline from the year 2014 to 2015

and then has significantly improved over the financial year 2016-2018. The movement in the

operational revenue and expenditure are the key determinants for influencing the ROE position

of the company. The reduction in the ROE of Woodside can be regarded due to increase in the

operating expenses of the company mainly due to increase in the prices of oil over the selected

financial period. However, the ROE position for the company is better than its competitor Santos

limited that has depicted a negative trend over the year 2015 to 2017 and has maintained a lower

ratio over the selected financial period as compared with Woodside Petroleum. Woodside

Petroleum has also outperformed the industrial average by maintaining a higher return on its

equity resources as compared with the overall industry sector during the selected financial

period.

Formula: Net income/shareholder’s equity (Damodaran, 2011)

The company having higher ROE indicates higher earning potential and thus depicts its

higher attractiveness for the investors by creating larger return for the shareholders.

Return on Equity

Ratios 2014 2015 2016 2017 2018

Woodside Petroleum 16.08% 0.76% 6.37% 6.84% 9.23%

Santos Limited 5.43% -55.53% -13.82% -4.84% 9.06%

Industry Average 11.09% 11.26% 11.04% 10.99% 11.26%

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

2014 2015 2016 2017 2018

-60.00%

-50.00%

-40.00%

-30.00%

-20.00%

-10.00%

0.00%

10.00%

20.00%

Return on Equity

Percentage

The ROE ratio of Woodside Petroleum has depicted a decreasing trend over the selected

financial period 2014-2018. The ratio has depicted a gradual decline from the year 2014 to 2015

and then has significantly improved over the financial year 2016-2018. The movement in the

operational revenue and expenditure are the key determinants for influencing the ROE position

of the company. The reduction in the ROE of Woodside can be regarded due to increase in the

operating expenses of the company mainly due to increase in the prices of oil over the selected

financial period. However, the ROE position for the company is better than its competitor Santos

limited that has depicted a negative trend over the year 2015 to 2017 and has maintained a lower

ratio over the selected financial period as compared with Woodside Petroleum. Woodside

Petroleum has also outperformed the industrial average by maintaining a higher return on its

equity resources as compared with the overall industry sector during the selected financial

period.

9

Net Profit Margin

The ratio is used for assessing the ability of a company to realize net income or profit as a

percentage of revenue. The ratio can be used for examining the proportion of revenue retained by

a company as income after meeting all the operational expenses. The ratio is highly significant

for determining the profitability position of utility companies such as Woodside Petroleum as it

helps in determining the profits retained after meeting all the operational expenses of interest,

taxes and dividends. Thus, it helps in assessing the financial risk present within a company by

examining whether it is able to generate sufficient amount of revenue to meet its plans of future

growth and development.

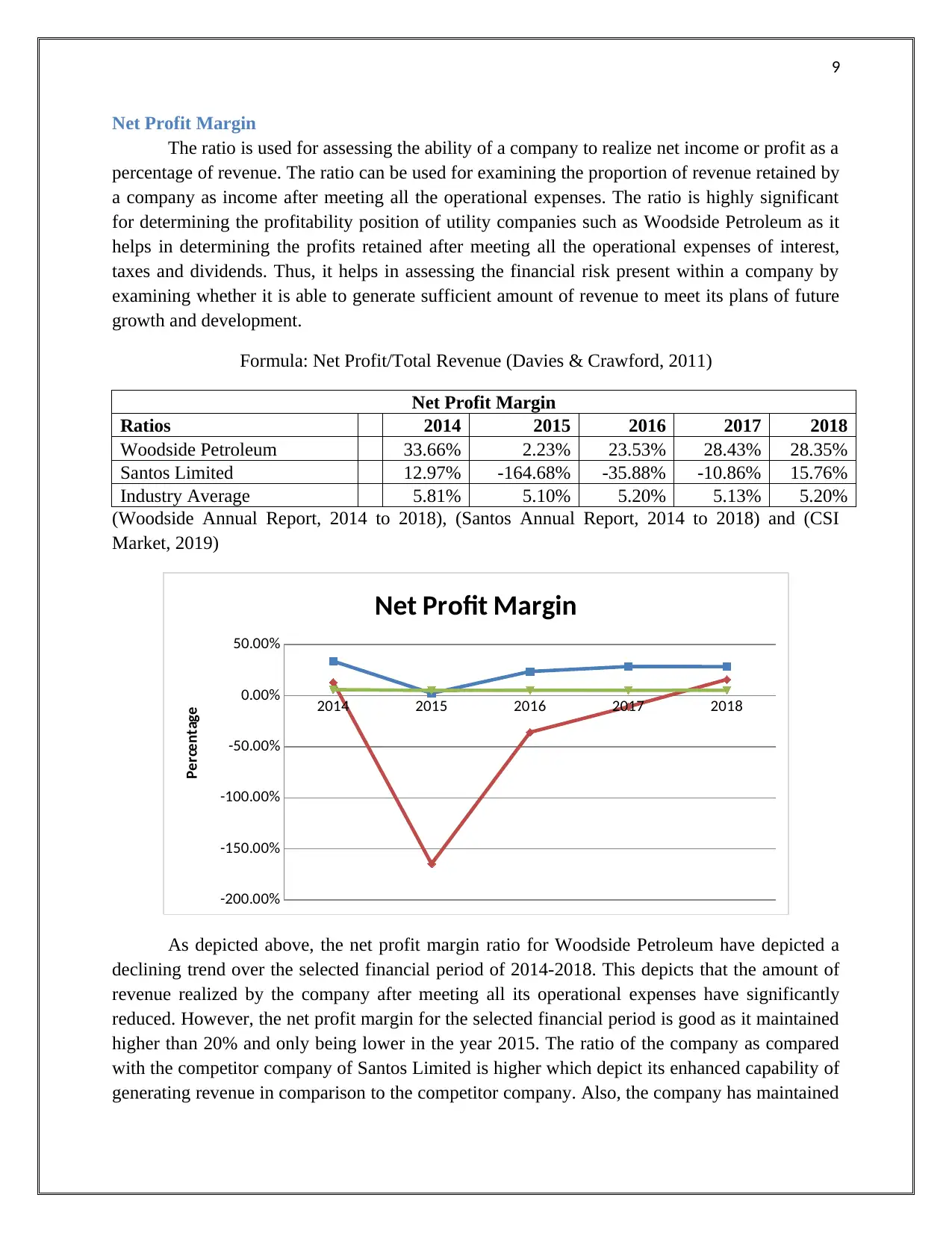

Formula: Net Profit/Total Revenue (Davies & Crawford, 2011)

Net Profit Margin

Ratios 2014 2015 2016 2017 2018

Woodside Petroleum 33.66% 2.23% 23.53% 28.43% 28.35%

Santos Limited 12.97% -164.68% -35.88% -10.86% 15.76%

Industry Average 5.81% 5.10% 5.20% 5.13% 5.20%

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

2014 2015 2016 2017 2018

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

Net Profit Margin

Percentage

As depicted above, the net profit margin ratio for Woodside Petroleum have depicted a

declining trend over the selected financial period of 2014-2018. This depicts that the amount of

revenue realized by the company after meeting all its operational expenses have significantly

reduced. However, the net profit margin for the selected financial period is good as it maintained

higher than 20% and only being lower in the year 2015. The ratio of the company as compared

with the competitor company of Santos Limited is higher which depict its enhanced capability of

generating revenue in comparison to the competitor company. Also, the company has maintained

Net Profit Margin

The ratio is used for assessing the ability of a company to realize net income or profit as a

percentage of revenue. The ratio can be used for examining the proportion of revenue retained by

a company as income after meeting all the operational expenses. The ratio is highly significant

for determining the profitability position of utility companies such as Woodside Petroleum as it

helps in determining the profits retained after meeting all the operational expenses of interest,

taxes and dividends. Thus, it helps in assessing the financial risk present within a company by

examining whether it is able to generate sufficient amount of revenue to meet its plans of future

growth and development.

Formula: Net Profit/Total Revenue (Davies & Crawford, 2011)

Net Profit Margin

Ratios 2014 2015 2016 2017 2018

Woodside Petroleum 33.66% 2.23% 23.53% 28.43% 28.35%

Santos Limited 12.97% -164.68% -35.88% -10.86% 15.76%

Industry Average 5.81% 5.10% 5.20% 5.13% 5.20%

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

2014 2015 2016 2017 2018

-200.00%

-150.00%

-100.00%

-50.00%

0.00%

50.00%

Net Profit Margin

Percentage

As depicted above, the net profit margin ratio for Woodside Petroleum have depicted a

declining trend over the selected financial period of 2014-2018. This depicts that the amount of

revenue realized by the company after meeting all its operational expenses have significantly

reduced. However, the net profit margin for the selected financial period is good as it maintained

higher than 20% and only being lower in the year 2015. The ratio of the company as compared

with the competitor company of Santos Limited is higher which depict its enhanced capability of

generating revenue in comparison to the competitor company. Also, the company has maintained

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

a higher net profit margin in comparison to the industry average which signifies its superior

position within the oil and gas sector of Australia.

Overall Profitability performance: It can be concluded that overall profitability performance

of Woodside Petroleum was far better than its competitor Santos Limited and also with the

industry average. It means Woodside rank amongst the top companies when it comes to

profitability in its sector as well as in whole industry.

Liquidity Analysis

The analysis is carried out determining the ability of a company for meeting its financial

obligations as they become due in a timely manner. The analysis is very significant for lenders

and creditors to develop an insight into the financial position of a company to meet its credit

obligations. The liquidity position of Woodside Petroleum can be evaluated with the use of

following ratios:

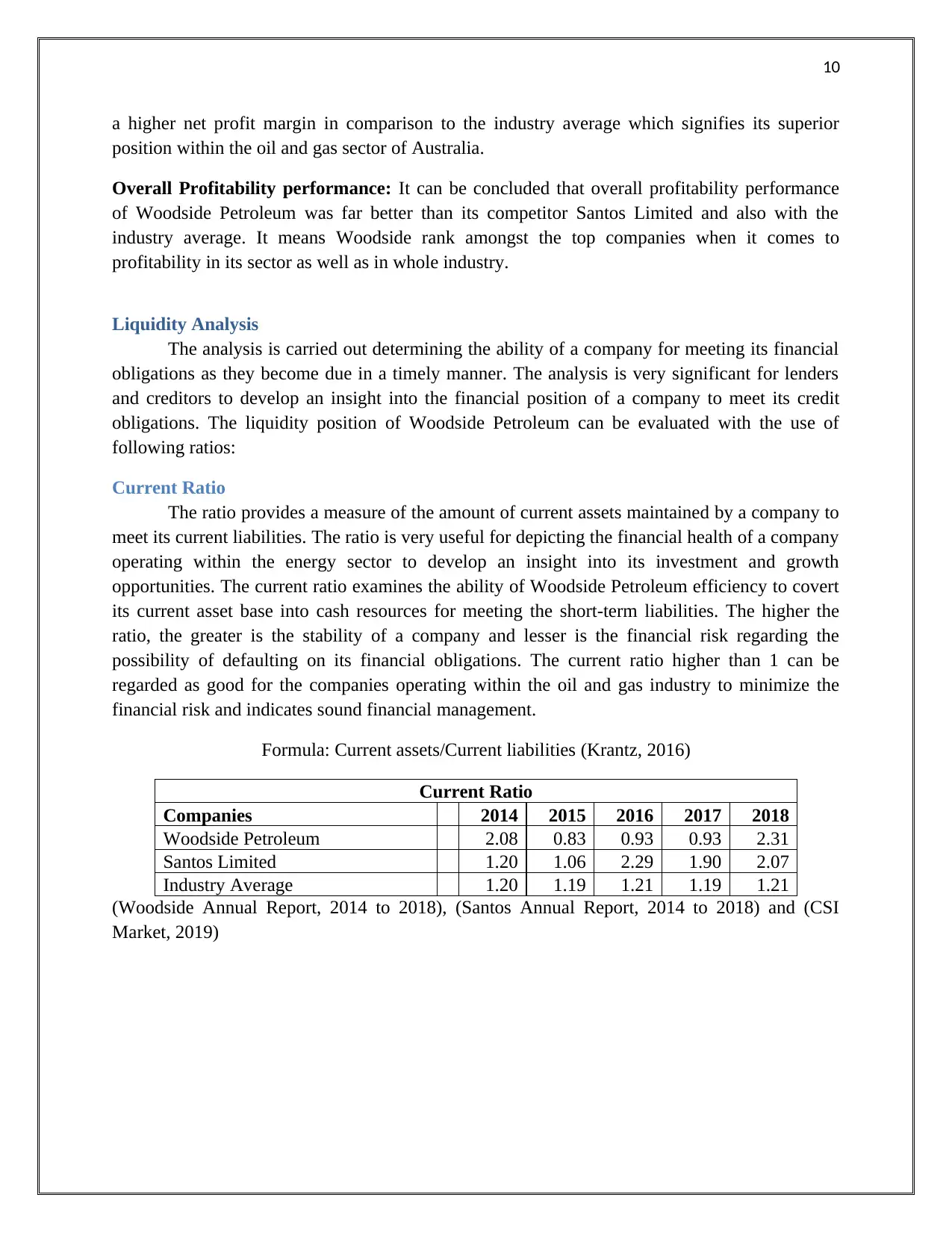

Current Ratio

The ratio provides a measure of the amount of current assets maintained by a company to

meet its current liabilities. The ratio is very useful for depicting the financial health of a company

operating within the energy sector to develop an insight into its investment and growth

opportunities. The current ratio examines the ability of Woodside Petroleum efficiency to covert

its current asset base into cash resources for meeting the short-term liabilities. The higher the

ratio, the greater is the stability of a company and lesser is the financial risk regarding the

possibility of defaulting on its financial obligations. The current ratio higher than 1 can be

regarded as good for the companies operating within the oil and gas industry to minimize the

financial risk and indicates sound financial management.

Formula: Current assets/Current liabilities (Krantz, 2016)

Current Ratio

Companies 2014 2015 2016 2017 2018

Woodside Petroleum 2.08 0.83 0.93 0.93 2.31

Santos Limited 1.20 1.06 2.29 1.90 2.07

Industry Average 1.20 1.19 1.21 1.19 1.21

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

a higher net profit margin in comparison to the industry average which signifies its superior

position within the oil and gas sector of Australia.

Overall Profitability performance: It can be concluded that overall profitability performance

of Woodside Petroleum was far better than its competitor Santos Limited and also with the

industry average. It means Woodside rank amongst the top companies when it comes to

profitability in its sector as well as in whole industry.

Liquidity Analysis

The analysis is carried out determining the ability of a company for meeting its financial

obligations as they become due in a timely manner. The analysis is very significant for lenders

and creditors to develop an insight into the financial position of a company to meet its credit

obligations. The liquidity position of Woodside Petroleum can be evaluated with the use of

following ratios:

Current Ratio

The ratio provides a measure of the amount of current assets maintained by a company to

meet its current liabilities. The ratio is very useful for depicting the financial health of a company

operating within the energy sector to develop an insight into its investment and growth

opportunities. The current ratio examines the ability of Woodside Petroleum efficiency to covert

its current asset base into cash resources for meeting the short-term liabilities. The higher the

ratio, the greater is the stability of a company and lesser is the financial risk regarding the

possibility of defaulting on its financial obligations. The current ratio higher than 1 can be

regarded as good for the companies operating within the oil and gas industry to minimize the

financial risk and indicates sound financial management.

Formula: Current assets/Current liabilities (Krantz, 2016)

Current Ratio

Companies 2014 2015 2016 2017 2018

Woodside Petroleum 2.08 0.83 0.93 0.93 2.31

Santos Limited 1.20 1.06 2.29 1.90 2.07

Industry Average 1.20 1.19 1.21 1.19 1.21

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

2014 2015 2016 2017 2018

0.00

0.50

1.00

1.50

2.00

2.50

Current Ratio

Times

The current ratio for Woodside has depicted a slight increase over the selected financial

period of 2014-2018. However, the ratio for the financial period 2015-2017 is less than 1 which

indicates its weak liquidity position and decrease in the current asset base as compared with the

current liabilities position. This indicates a point of concern for the company due to the presence

of financial risk of not able to meet its short-term liabilities in the coming period of time. The oil

and gas companies need to maintain a higher current ratio of above 1 for ensuring sound

financial management and ensuring the presence of enough liquid resources to ensure the

availability of cash for conducting its daily operational activities. The liquidity position of Santos

limited between the years 2015-2017 is higher than Woodside Petroleum and the company has

also maintained a current ratio of higher than 1 for all the selected financial period. The current

ratio for the company is also significantly lower as compared with the industry average between

the financial years 2015-2017 which means that it needs to place measures for improving its

current asset position to reduce the financial risk of not able to meet its financial obligations on

time. The increase in the cash equivalents by the company will significantly lead to improving

the financial stability of the company and thus ensuring its continued growth by carrying out

effectively its investment activities (Gibson, 2011).

Days Receivable Ratio (DRR)

The ratio indicates the effectiveness of a company to convert its sales into cash for

meeting the daily operational needs of a business. The presence of adequate cash is essential for

a company to conduct the business operations and therefore the ratio helps in predicting the days

that is required for collecting the cash from its debtors. The lower the ratio the better it is for the

company as less the number of days required to access the cash the larger is the availability of

cash resources for making any relevant investment decisions. The enhanced cash flow will help

in maximizing the operational efficiency of a company by giving them an advantage in

maintaining cash holdings.

2014 2015 2016 2017 2018

0.00

0.50

1.00

1.50

2.00

2.50

Current Ratio

Times

The current ratio for Woodside has depicted a slight increase over the selected financial

period of 2014-2018. However, the ratio for the financial period 2015-2017 is less than 1 which

indicates its weak liquidity position and decrease in the current asset base as compared with the

current liabilities position. This indicates a point of concern for the company due to the presence

of financial risk of not able to meet its short-term liabilities in the coming period of time. The oil

and gas companies need to maintain a higher current ratio of above 1 for ensuring sound

financial management and ensuring the presence of enough liquid resources to ensure the

availability of cash for conducting its daily operational activities. The liquidity position of Santos

limited between the years 2015-2017 is higher than Woodside Petroleum and the company has

also maintained a current ratio of higher than 1 for all the selected financial period. The current

ratio for the company is also significantly lower as compared with the industry average between

the financial years 2015-2017 which means that it needs to place measures for improving its

current asset position to reduce the financial risk of not able to meet its financial obligations on

time. The increase in the cash equivalents by the company will significantly lead to improving

the financial stability of the company and thus ensuring its continued growth by carrying out

effectively its investment activities (Gibson, 2011).

Days Receivable Ratio (DRR)

The ratio indicates the effectiveness of a company to convert its sales into cash for

meeting the daily operational needs of a business. The presence of adequate cash is essential for

a company to conduct the business operations and therefore the ratio helps in predicting the days

that is required for collecting the cash from its debtors. The lower the ratio the better it is for the

company as less the number of days required to access the cash the larger is the availability of

cash resources for making any relevant investment decisions. The enhanced cash flow will help

in maximizing the operational efficiency of a company by giving them an advantage in

maintaining cash holdings.

12

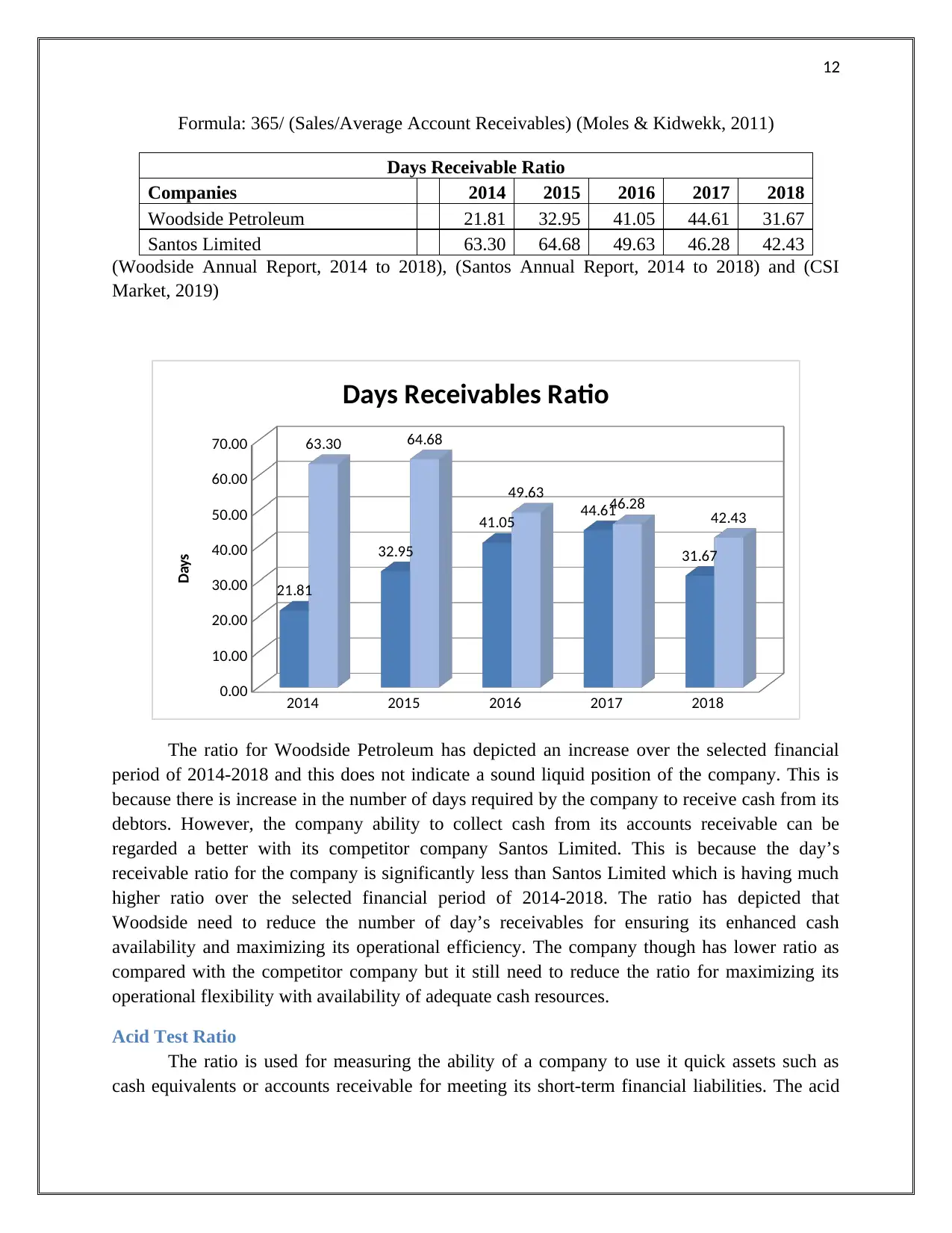

Formula: 365/ (Sales/Average Account Receivables) (Moles & Kidwekk, 2011)

Days Receivable Ratio

Companies 2014 2015 2016 2017 2018

Woodside Petroleum 21.81 32.95 41.05 44.61 31.67

Santos Limited 63.30 64.68 49.63 46.28 42.43

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

2014 2015 2016 2017 2018

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

21.81

32.95

41.05 44.61

31.67

63.30 64.68

49.63 46.28 42.43

Days Receivables Ratio

Days

The ratio for Woodside Petroleum has depicted an increase over the selected financial

period of 2014-2018 and this does not indicate a sound liquid position of the company. This is

because there is increase in the number of days required by the company to receive cash from its

debtors. However, the company ability to collect cash from its accounts receivable can be

regarded a better with its competitor company Santos Limited. This is because the day’s

receivable ratio for the company is significantly less than Santos Limited which is having much

higher ratio over the selected financial period of 2014-2018. The ratio has depicted that

Woodside need to reduce the number of day’s receivables for ensuring its enhanced cash

availability and maximizing its operational efficiency. The company though has lower ratio as

compared with the competitor company but it still need to reduce the ratio for maximizing its

operational flexibility with availability of adequate cash resources.

Acid Test Ratio

The ratio is used for measuring the ability of a company to use it quick assets such as

cash equivalents or accounts receivable for meeting its short-term financial liabilities. The acid

Formula: 365/ (Sales/Average Account Receivables) (Moles & Kidwekk, 2011)

Days Receivable Ratio

Companies 2014 2015 2016 2017 2018

Woodside Petroleum 21.81 32.95 41.05 44.61 31.67

Santos Limited 63.30 64.68 49.63 46.28 42.43

(Woodside Annual Report, 2014 to 2018), (Santos Annual Report, 2014 to 2018) and (CSI

Market, 2019)

2014 2015 2016 2017 2018

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

21.81

32.95

41.05 44.61

31.67

63.30 64.68

49.63 46.28 42.43

Days Receivables Ratio

Days

The ratio for Woodside Petroleum has depicted an increase over the selected financial

period of 2014-2018 and this does not indicate a sound liquid position of the company. This is

because there is increase in the number of days required by the company to receive cash from its

debtors. However, the company ability to collect cash from its accounts receivable can be

regarded a better with its competitor company Santos Limited. This is because the day’s

receivable ratio for the company is significantly less than Santos Limited which is having much

higher ratio over the selected financial period of 2014-2018. The ratio has depicted that

Woodside need to reduce the number of day’s receivables for ensuring its enhanced cash

availability and maximizing its operational efficiency. The company though has lower ratio as

compared with the competitor company but it still need to reduce the ratio for maximizing its

operational flexibility with availability of adequate cash resources.

Acid Test Ratio

The ratio is used for measuring the ability of a company to use it quick assets such as

cash equivalents or accounts receivable for meeting its short-term financial liabilities. The acid

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.