FIN510 - Corporate Finance: Investment and Risk Analysis Assignment

VerifiedAdded on 2022/12/27

|11

|3015

|25

Homework Assignment

AI Summary

This assignment solution for FIN510, a Corporate Finance course, analyzes monthly returns, average returns, and volatility of five selected companies and a market index (ASX200). It calculates standard deviations, betas, and provides a risk evaluation report for clients, including recommendations for investment strategies and portfolio development. The solution includes detailed calculations of monthly returns, average returns, variance, standard deviation, and beta for each company, along with portfolio analysis. The report assesses risk, analyzes whether shares are over or underpriced, and suggests investment recommendations. The assignment covers key concepts in corporate finance such as portfolio management, risk assessment, and investment strategy, and the solution is presented in an organized, easy-to-understand format, including relevant formulas, and excel outputs.

1

FIN510Aspects of Corporate Finance

Written Assignment

FIN510Aspects of Corporate Finance

Written Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Solution to Part 1: Monthly and average returns of shares and portfolio........................................3

Sub-Section A: Estimation of average of monthly returns on the basis of monthly returns

computed above in respect of each share and market index ASX200.............................................5

Sub-Section B: Calculation of average return of the portfolio (Portfolio is made of equal weight

of each of five shares)......................................................................................................................5

Solution to Part 2: Volatility............................................................................................................6

Sub Section A: Standard deviation of returns of five companies....................................................6

Sub Section B: Standard Deviation of Portfolio and its comparison with each of individual share

.........................................................................................................................................................7

Sub Section C: Standard Deviation of ASX200 and its comparison...............................................7

Solution to Part 3: Beta Calculation................................................................................................8

Sub Section A: Beta of each company (Share)................................................................................8

Sub Section B: Analysis of beta for each company.........................................................................8

Solution to Part 4: Forecast & Investment strategy.........................................................................9

Sub Section A: Report presented to the clients of Tri-Star Management........................................9

Part a: Risk evaluation of each company.....................................................................................9

Part b: Analysis of whether shares are overpriced, underpriced, or correctly price during the

forecasted period..........................................................................................................................9

Part c: Recommendation for investment in each of the investment...........................................10

Sub Section B: Recommendation to invest in portfolio................................................................10

Contents

Solution to Part 1: Monthly and average returns of shares and portfolio........................................3

Sub-Section A: Estimation of average of monthly returns on the basis of monthly returns

computed above in respect of each share and market index ASX200.............................................5

Sub-Section B: Calculation of average return of the portfolio (Portfolio is made of equal weight

of each of five shares)......................................................................................................................5

Solution to Part 2: Volatility............................................................................................................6

Sub Section A: Standard deviation of returns of five companies....................................................6

Sub Section B: Standard Deviation of Portfolio and its comparison with each of individual share

.........................................................................................................................................................7

Sub Section C: Standard Deviation of ASX200 and its comparison...............................................7

Solution to Part 3: Beta Calculation................................................................................................8

Sub Section A: Beta of each company (Share)................................................................................8

Sub Section B: Analysis of beta for each company.........................................................................8

Solution to Part 4: Forecast & Investment strategy.........................................................................9

Sub Section A: Report presented to the clients of Tri-Star Management........................................9

Part a: Risk evaluation of each company.....................................................................................9

Part b: Analysis of whether shares are overpriced, underpriced, or correctly price during the

forecasted period..........................................................................................................................9

Part c: Recommendation for investment in each of the investment...........................................10

Sub Section B: Recommendation to invest in portfolio................................................................10

3

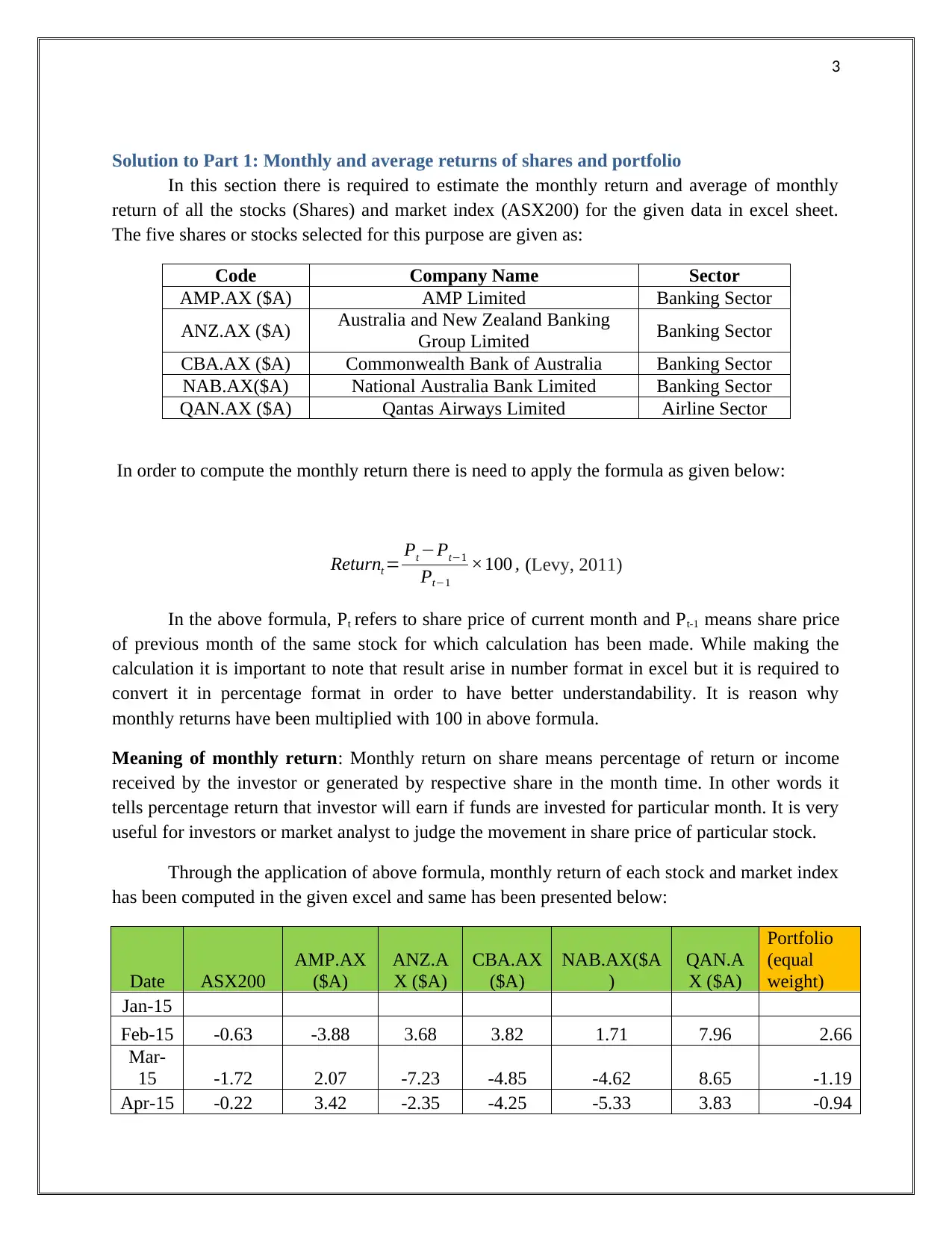

Solution to Part 1: Monthly and average returns of shares and portfolio

In this section there is required to estimate the monthly return and average of monthly

return of all the stocks (Shares) and market index (ASX200) for the given data in excel sheet.

The five shares or stocks selected for this purpose are given as:

Code Company Name Sector

AMP.AX ($A) AMP Limited Banking Sector

ANZ.AX ($A) Australia and New Zealand Banking

Group Limited Banking Sector

CBA.AX ($A) Commonwealth Bank of Australia Banking Sector

NAB.AX($A) National Australia Bank Limited Banking Sector

QAN.AX ($A) Qantas Airways Limited Airline Sector

In order to compute the monthly return there is need to apply the formula as given below:

Returnt = Pt −Pt−1

Pt−1

×100 , (Levy, 2011)

In the above formula, Pt refers to share price of current month and Pt-1 means share price

of previous month of the same stock for which calculation has been made. While making the

calculation it is important to note that result arise in number format in excel but it is required to

convert it in percentage format in order to have better understandability. It is reason why

monthly returns have been multiplied with 100 in above formula.

Meaning of monthly return: Monthly return on share means percentage of return or income

received by the investor or generated by respective share in the month time. In other words it

tells percentage return that investor will earn if funds are invested for particular month. It is very

useful for investors or market analyst to judge the movement in share price of particular stock.

Through the application of above formula, monthly return of each stock and market index

has been computed in the given excel and same has been presented below:

Date ASX200

AMP.AX

($A)

ANZ.A

X ($A)

CBA.AX

($A)

NAB.AX($A

)

QAN.A

X ($A)

Portfolio

(equal

weight)

Jan-15

Feb-15 -0.63 -3.88 3.68 3.82 1.71 7.96 2.66

Mar-

15 -1.72 2.07 -7.23 -4.85 -4.62 8.65 -1.19

Apr-15 -0.22 3.42 -2.35 -4.25 -5.33 3.83 -0.94

Solution to Part 1: Monthly and average returns of shares and portfolio

In this section there is required to estimate the monthly return and average of monthly

return of all the stocks (Shares) and market index (ASX200) for the given data in excel sheet.

The five shares or stocks selected for this purpose are given as:

Code Company Name Sector

AMP.AX ($A) AMP Limited Banking Sector

ANZ.AX ($A) Australia and New Zealand Banking

Group Limited Banking Sector

CBA.AX ($A) Commonwealth Bank of Australia Banking Sector

NAB.AX($A) National Australia Bank Limited Banking Sector

QAN.AX ($A) Qantas Airways Limited Airline Sector

In order to compute the monthly return there is need to apply the formula as given below:

Returnt = Pt −Pt−1

Pt−1

×100 , (Levy, 2011)

In the above formula, Pt refers to share price of current month and Pt-1 means share price

of previous month of the same stock for which calculation has been made. While making the

calculation it is important to note that result arise in number format in excel but it is required to

convert it in percentage format in order to have better understandability. It is reason why

monthly returns have been multiplied with 100 in above formula.

Meaning of monthly return: Monthly return on share means percentage of return or income

received by the investor or generated by respective share in the month time. In other words it

tells percentage return that investor will earn if funds are invested for particular month. It is very

useful for investors or market analyst to judge the movement in share price of particular stock.

Through the application of above formula, monthly return of each stock and market index

has been computed in the given excel and same has been presented below:

Date ASX200

AMP.AX

($A)

ANZ.A

X ($A)

CBA.AX

($A)

NAB.AX($A

)

QAN.A

X ($A)

Portfolio

(equal

weight)

Jan-15

Feb-15 -0.63 -3.88 3.68 3.82 1.71 7.96 2.66

Mar-

15 -1.72 2.07 -7.23 -4.85 -4.62 8.65 -1.19

Apr-15 -0.22 3.42 -2.35 -4.25 -5.33 3.83 -0.94

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

May-

15 -5.51 -9.61 -0.39 0.05 -0.05 -10.23 -4.05

Jun-15 4.40 9.80 1.49 2.85 4.38 18.67 7.44

Jul-15 -8.64 -9.98 -14.53 -12.32 -10.35 -10.40 -11.52

Aug-

15

-3.56 -6.55 -3.04 -2.09 -3.82 10.71 -0.96

Sep-15 4.34 5.54 0.48 5.51 0.57 -0.29 2.36

Oct-15 -1.39 1.40 -0.22 3.52 -2.52 -7.85 -1.13

Nov-

15

2.50 0.34 6.68 7.68 6.41 12.36 6.69

Dec-15 -5.48 -7.89 -13.43 -8.02 -8.41 -5.13 -8.58

Jan-16 -2.49 -0.93 -7.36 -10.84 -9.36 -0.52 -5.80

Feb-16 4.14 8.83 4.73 9.74 8.47 5.44 7.44

Mar-

16 3.33 4.30 3.45 -1.37 3.62 -20.88 -2.18

Apr-16 2.41 -4.08 4.99 4.79 -0.15 -4.35 0.24

May-

16 -2.70 -8.51 -2.23 -3.95 -3.03 -8.44 -5.23

Jun-16 6.28 12.60 7.13 4.01 4.36 12.06 8.03

Jul-16 -2.32 -9.47 4.10 -7.16 3.01 2.53 -1.40

Aug-

16 0.05 3.04 2.71 3.86 1.94 -3.70 1.57

Sep-16 -2.17 -13.45 0.80 1.37 0.47 0.14 -2.13

Oct-16 2.31 2.84 2.01 7.17 3.32 7.84 4.64

Nov-

16 4.14 7.23 10.19 4.78 6.49 0.91 5.92

Dec-16 -0.79 -0.79 -3.71 -0.91 2.12 2.40 -0.18

Jan-17 1.62 -2.40 5.50 0.81 5.47 9.97 3.87

Feb-17 2.67 9.16 2.98 6.83 4.22 3.73 5.38

Mar-

17 1.01 3.47 2.95 1.73 1.98 11.07 4.24

Apr-17 -3.37 -5.78 -14.50 -8.87 -11.41 18.16 -4.48

May-

17 -0.05 2.77 5.28 3.97 1.31 14.17 5.50

Jun-17 -0.02 3.85 3.17 1.11 1.22 -6.99 0.47

Jul-17 -0.11 -5.38 -0.78 -9.47 0.83 7.52 -1.45

Aug-

17 -0.58 -2.53 0.68 2.17 4.30 1.92 1.31

Sep-17 4.00 2.90 1.08 3.16 3.68 6.81 3.53

Oct-17 1.03 2.82 -4.88 2.32 -9.40 -7.80 -3.39

Nov-

17 1.59 1.57 3.72 1.15 3.16 -11.11 -0.30

Dec-17 -0.45 1.16 -0.56 -1.83 -1.49 4.56 0.37

May-

15 -5.51 -9.61 -0.39 0.05 -0.05 -10.23 -4.05

Jun-15 4.40 9.80 1.49 2.85 4.38 18.67 7.44

Jul-15 -8.64 -9.98 -14.53 -12.32 -10.35 -10.40 -11.52

Aug-

15

-3.56 -6.55 -3.04 -2.09 -3.82 10.71 -0.96

Sep-15 4.34 5.54 0.48 5.51 0.57 -0.29 2.36

Oct-15 -1.39 1.40 -0.22 3.52 -2.52 -7.85 -1.13

Nov-

15

2.50 0.34 6.68 7.68 6.41 12.36 6.69

Dec-15 -5.48 -7.89 -13.43 -8.02 -8.41 -5.13 -8.58

Jan-16 -2.49 -0.93 -7.36 -10.84 -9.36 -0.52 -5.80

Feb-16 4.14 8.83 4.73 9.74 8.47 5.44 7.44

Mar-

16 3.33 4.30 3.45 -1.37 3.62 -20.88 -2.18

Apr-16 2.41 -4.08 4.99 4.79 -0.15 -4.35 0.24

May-

16 -2.70 -8.51 -2.23 -3.95 -3.03 -8.44 -5.23

Jun-16 6.28 12.60 7.13 4.01 4.36 12.06 8.03

Jul-16 -2.32 -9.47 4.10 -7.16 3.01 2.53 -1.40

Aug-

16 0.05 3.04 2.71 3.86 1.94 -3.70 1.57

Sep-16 -2.17 -13.45 0.80 1.37 0.47 0.14 -2.13

Oct-16 2.31 2.84 2.01 7.17 3.32 7.84 4.64

Nov-

16 4.14 7.23 10.19 4.78 6.49 0.91 5.92

Dec-16 -0.79 -0.79 -3.71 -0.91 2.12 2.40 -0.18

Jan-17 1.62 -2.40 5.50 0.81 5.47 9.97 3.87

Feb-17 2.67 9.16 2.98 6.83 4.22 3.73 5.38

Mar-

17 1.01 3.47 2.95 1.73 1.98 11.07 4.24

Apr-17 -3.37 -5.78 -14.50 -8.87 -11.41 18.16 -4.48

May-

17 -0.05 2.77 5.28 3.97 1.31 14.17 5.50

Jun-17 -0.02 3.85 3.17 1.11 1.22 -6.99 0.47

Jul-17 -0.11 -5.38 -0.78 -9.47 0.83 7.52 -1.45

Aug-

17 -0.58 -2.53 0.68 2.17 4.30 1.92 1.31

Sep-17 4.00 2.90 1.08 3.16 3.68 6.81 3.53

Oct-17 1.03 2.82 -4.88 2.32 -9.40 -7.80 -3.39

Nov-

17 1.59 1.57 3.72 1.15 3.16 -11.11 -0.30

Dec-17 -0.45 1.16 -0.56 -1.83 -1.49 4.56 0.37

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

In the above table, monthly returns of all five shares and ASX200 have been shown form

Feb-15 to Dec-17. It is not possible to calculate the monthly return for month Jan-15 due to share

price of previous month has not been provided.

Sub-Section A: Estimation of average of monthly returns on the basis of monthly returns

computed above in respect of each share and market index ASX200

In order to estimate the average of monthly return it is required to divide the sum of

monthly returns with number of months. Same can be computed through using the excel formula

known as “Average” (Madura, 2014).

Average of monthly returns of each share and market index has been computed through

using the excel formula and answer derived has been presented below:

Particulars ASX200 AMP.AX

($A)

ANZ.AX

($A)

CBA.AX

($A) NAB.AX($A) QAN.AX

($A)

Average

Monthly

return or

Mean

0.10 -0.06 0.07 0.18 0.09 2.11

The average return means return earned on the particular share by the investor if money

has been invested for particular months and return has been made out monthly basis. Returns are

first calculated on monthly basis and then their average is made to predict the average monthly

return.

On comparison of average monthly return of each stock with the market index ASX200 it

has been found that AMP Limited, NAB Bank & ANZ Bank have average return below the

average monthly return of market index ASX200 and average monthly return of Qantas Airways

& Commonwealth Bank were greater than market index ASX200. It means Qantas Airways and

Commonwealth Bank have performed well with respect to the market as they have earned higher

return as compared to market return. But it is highly important to analyse the stock with their risk

factor (Volatility) in order to judge the performance of each stock with respect to their market.

Sub-Section B: Calculation of average return of the portfolio (Portfolio is made of equal

weight of each of five shares)

It is important to understand what is meant by portfolio. Portfolio represents group of

financial assets such as stocks, commodities, bonds, currencies and cash equivalents. The

purpose of portfolio is to lower the risk of investment in the stocks and increase the overall

return. Portfolio is for those investors who are risk adverse but want reasonable return on their

investment.

In the above table, monthly returns of all five shares and ASX200 have been shown form

Feb-15 to Dec-17. It is not possible to calculate the monthly return for month Jan-15 due to share

price of previous month has not been provided.

Sub-Section A: Estimation of average of monthly returns on the basis of monthly returns

computed above in respect of each share and market index ASX200

In order to estimate the average of monthly return it is required to divide the sum of

monthly returns with number of months. Same can be computed through using the excel formula

known as “Average” (Madura, 2014).

Average of monthly returns of each share and market index has been computed through

using the excel formula and answer derived has been presented below:

Particulars ASX200 AMP.AX

($A)

ANZ.AX

($A)

CBA.AX

($A) NAB.AX($A) QAN.AX

($A)

Average

Monthly

return or

Mean

0.10 -0.06 0.07 0.18 0.09 2.11

The average return means return earned on the particular share by the investor if money

has been invested for particular months and return has been made out monthly basis. Returns are

first calculated on monthly basis and then their average is made to predict the average monthly

return.

On comparison of average monthly return of each stock with the market index ASX200 it

has been found that AMP Limited, NAB Bank & ANZ Bank have average return below the

average monthly return of market index ASX200 and average monthly return of Qantas Airways

& Commonwealth Bank were greater than market index ASX200. It means Qantas Airways and

Commonwealth Bank have performed well with respect to the market as they have earned higher

return as compared to market return. But it is highly important to analyse the stock with their risk

factor (Volatility) in order to judge the performance of each stock with respect to their market.

Sub-Section B: Calculation of average return of the portfolio (Portfolio is made of equal

weight of each of five shares)

It is important to understand what is meant by portfolio. Portfolio represents group of

financial assets such as stocks, commodities, bonds, currencies and cash equivalents. The

purpose of portfolio is to lower the risk of investment in the stocks and increase the overall

return. Portfolio is for those investors who are risk adverse but want reasonable return on their

investment.

6

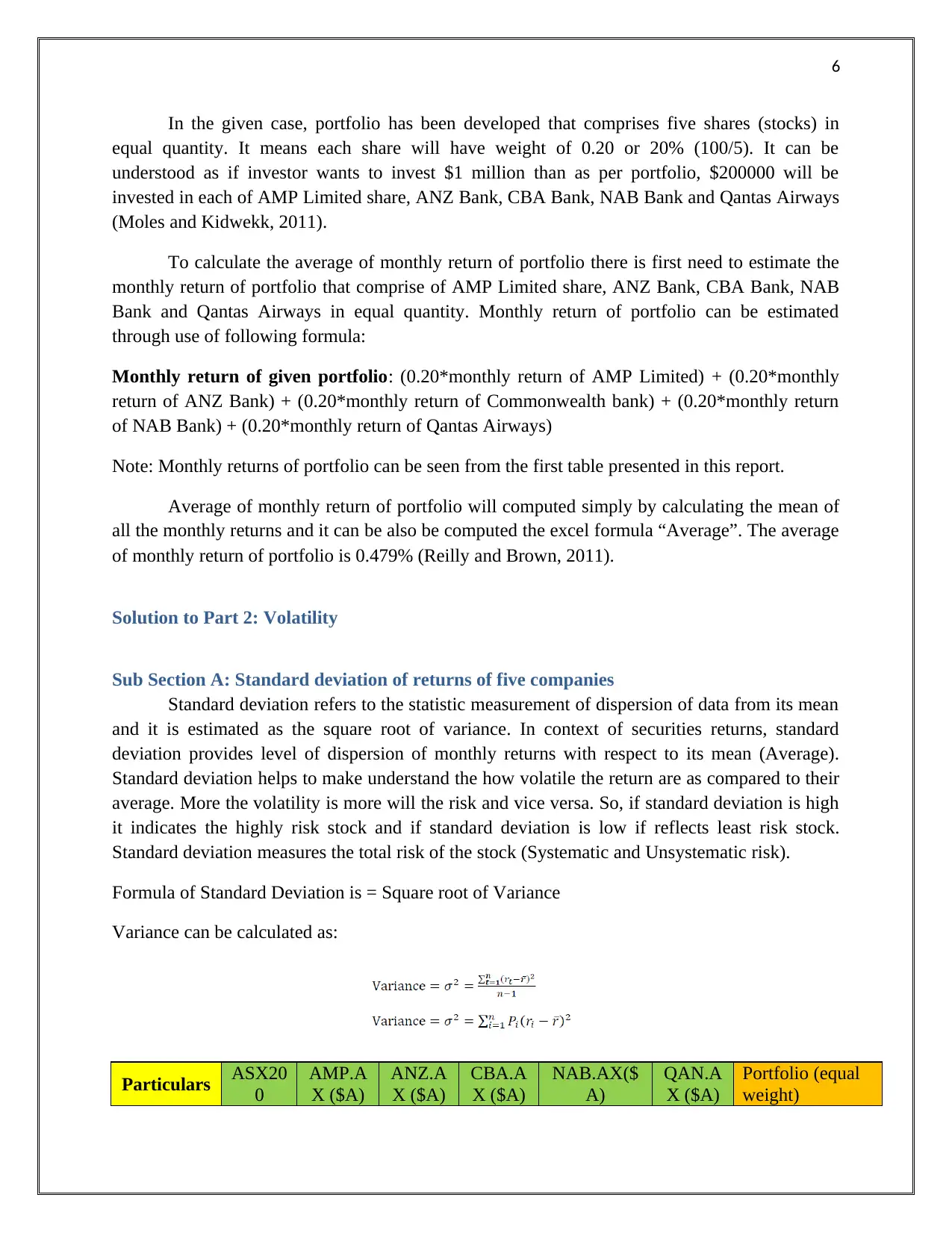

In the given case, portfolio has been developed that comprises five shares (stocks) in

equal quantity. It means each share will have weight of 0.20 or 20% (100/5). It can be

understood as if investor wants to invest $1 million than as per portfolio, $200000 will be

invested in each of AMP Limited share, ANZ Bank, CBA Bank, NAB Bank and Qantas Airways

(Moles and Kidwekk, 2011).

To calculate the average of monthly return of portfolio there is first need to estimate the

monthly return of portfolio that comprise of AMP Limited share, ANZ Bank, CBA Bank, NAB

Bank and Qantas Airways in equal quantity. Monthly return of portfolio can be estimated

through use of following formula:

Monthly return of given portfolio: (0.20*monthly return of AMP Limited) + (0.20*monthly

return of ANZ Bank) + (0.20*monthly return of Commonwealth bank) + (0.20*monthly return

of NAB Bank) + (0.20*monthly return of Qantas Airways)

Note: Monthly returns of portfolio can be seen from the first table presented in this report.

Average of monthly return of portfolio will computed simply by calculating the mean of

all the monthly returns and it can be also be computed the excel formula “Average”. The average

of monthly return of portfolio is 0.479% (Reilly and Brown, 2011).

Solution to Part 2: Volatility

Sub Section A: Standard deviation of returns of five companies

Standard deviation refers to the statistic measurement of dispersion of data from its mean

and it is estimated as the square root of variance. In context of securities returns, standard

deviation provides level of dispersion of monthly returns with respect to its mean (Average).

Standard deviation helps to make understand the how volatile the return are as compared to their

average. More the volatility is more will the risk and vice versa. So, if standard deviation is high

it indicates the highly risk stock and if standard deviation is low if reflects least risk stock.

Standard deviation measures the total risk of the stock (Systematic and Unsystematic risk).

Formula of Standard Deviation is = Square root of Variance

Variance can be calculated as:

Particulars ASX20

0

AMP.A

X ($A)

ANZ.A

X ($A)

CBA.A

X ($A)

NAB.AX($

A)

QAN.A

X ($A)

Portfolio (equal

weight)

In the given case, portfolio has been developed that comprises five shares (stocks) in

equal quantity. It means each share will have weight of 0.20 or 20% (100/5). It can be

understood as if investor wants to invest $1 million than as per portfolio, $200000 will be

invested in each of AMP Limited share, ANZ Bank, CBA Bank, NAB Bank and Qantas Airways

(Moles and Kidwekk, 2011).

To calculate the average of monthly return of portfolio there is first need to estimate the

monthly return of portfolio that comprise of AMP Limited share, ANZ Bank, CBA Bank, NAB

Bank and Qantas Airways in equal quantity. Monthly return of portfolio can be estimated

through use of following formula:

Monthly return of given portfolio: (0.20*monthly return of AMP Limited) + (0.20*monthly

return of ANZ Bank) + (0.20*monthly return of Commonwealth bank) + (0.20*monthly return

of NAB Bank) + (0.20*monthly return of Qantas Airways)

Note: Monthly returns of portfolio can be seen from the first table presented in this report.

Average of monthly return of portfolio will computed simply by calculating the mean of

all the monthly returns and it can be also be computed the excel formula “Average”. The average

of monthly return of portfolio is 0.479% (Reilly and Brown, 2011).

Solution to Part 2: Volatility

Sub Section A: Standard deviation of returns of five companies

Standard deviation refers to the statistic measurement of dispersion of data from its mean

and it is estimated as the square root of variance. In context of securities returns, standard

deviation provides level of dispersion of monthly returns with respect to its mean (Average).

Standard deviation helps to make understand the how volatile the return are as compared to their

average. More the volatility is more will the risk and vice versa. So, if standard deviation is high

it indicates the highly risk stock and if standard deviation is low if reflects least risk stock.

Standard deviation measures the total risk of the stock (Systematic and Unsystematic risk).

Formula of Standard Deviation is = Square root of Variance

Variance can be calculated as:

Particulars ASX20

0

AMP.A

X ($A)

ANZ.A

X ($A)

CBA.A

X ($A)

NAB.AX($

A)

QAN.A

X ($A)

Portfolio (equal

weight)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

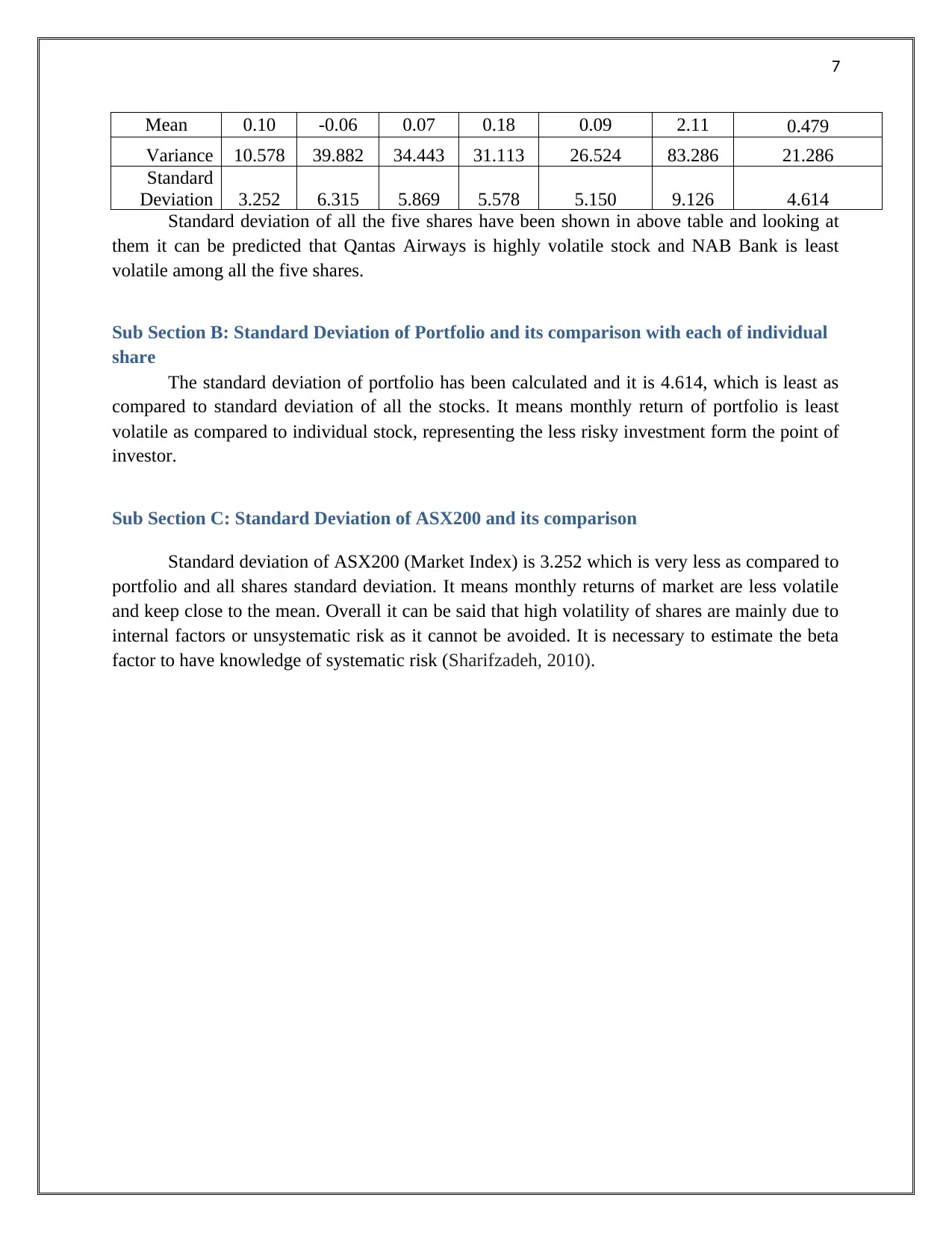

Mean 0.10 -0.06 0.07 0.18 0.09 2.11 0.479

Variance 10.578 39.882 34.443 31.113 26.524 83.286 21.286

Standard

Deviation 3.252 6.315 5.869 5.578 5.150 9.126 4.614

Standard deviation of all the five shares have been shown in above table and looking at

them it can be predicted that Qantas Airways is highly volatile stock and NAB Bank is least

volatile among all the five shares.

Sub Section B: Standard Deviation of Portfolio and its comparison with each of individual

share

The standard deviation of portfolio has been calculated and it is 4.614, which is least as

compared to standard deviation of all the stocks. It means monthly return of portfolio is least

volatile as compared to individual stock, representing the less risky investment form the point of

investor.

Sub Section C: Standard Deviation of ASX200 and its comparison

Standard deviation of ASX200 (Market Index) is 3.252 which is very less as compared to

portfolio and all shares standard deviation. It means monthly returns of market are less volatile

and keep close to the mean. Overall it can be said that high volatility of shares are mainly due to

internal factors or unsystematic risk as it cannot be avoided. It is necessary to estimate the beta

factor to have knowledge of systematic risk (Sharifzadeh, 2010).

Mean 0.10 -0.06 0.07 0.18 0.09 2.11 0.479

Variance 10.578 39.882 34.443 31.113 26.524 83.286 21.286

Standard

Deviation 3.252 6.315 5.869 5.578 5.150 9.126 4.614

Standard deviation of all the five shares have been shown in above table and looking at

them it can be predicted that Qantas Airways is highly volatile stock and NAB Bank is least

volatile among all the five shares.

Sub Section B: Standard Deviation of Portfolio and its comparison with each of individual

share

The standard deviation of portfolio has been calculated and it is 4.614, which is least as

compared to standard deviation of all the stocks. It means monthly return of portfolio is least

volatile as compared to individual stock, representing the less risky investment form the point of

investor.

Sub Section C: Standard Deviation of ASX200 and its comparison

Standard deviation of ASX200 (Market Index) is 3.252 which is very less as compared to

portfolio and all shares standard deviation. It means monthly returns of market are less volatile

and keep close to the mean. Overall it can be said that high volatility of shares are mainly due to

internal factors or unsystematic risk as it cannot be avoided. It is necessary to estimate the beta

factor to have knowledge of systematic risk (Sharifzadeh, 2010).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

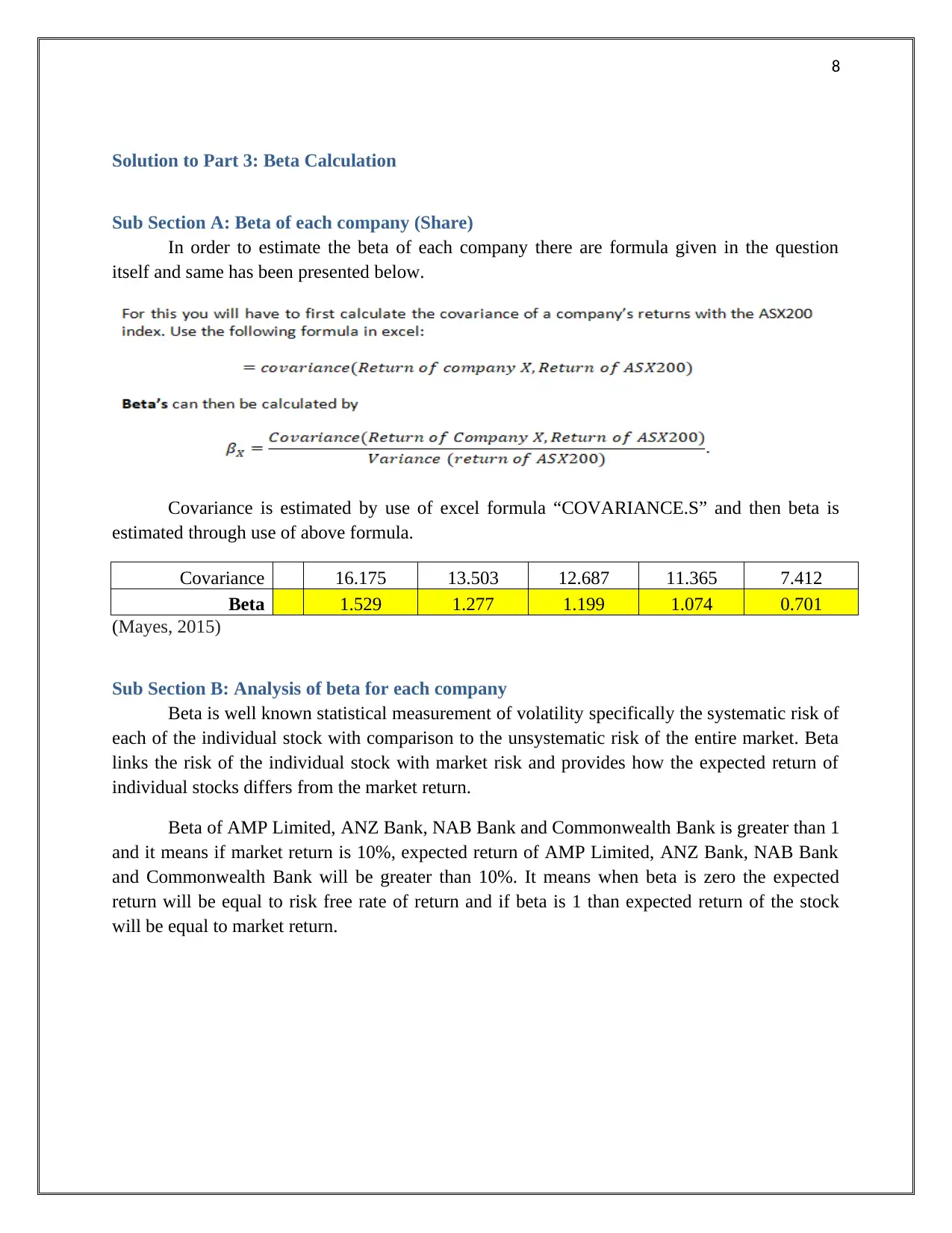

Solution to Part 3: Beta Calculation

Sub Section A: Beta of each company (Share)

In order to estimate the beta of each company there are formula given in the question

itself and same has been presented below.

Covariance is estimated by use of excel formula “COVARIANCE.S” and then beta is

estimated through use of above formula.

Covariance 16.175 13.503 12.687 11.365 7.412

Beta 1.529 1.277 1.199 1.074 0.701

(Mayes, 2015)

Sub Section B: Analysis of beta for each company

Beta is well known statistical measurement of volatility specifically the systematic risk of

each of the individual stock with comparison to the unsystematic risk of the entire market. Beta

links the risk of the individual stock with market risk and provides how the expected return of

individual stocks differs from the market return.

Beta of AMP Limited, ANZ Bank, NAB Bank and Commonwealth Bank is greater than 1

and it means if market return is 10%, expected return of AMP Limited, ANZ Bank, NAB Bank

and Commonwealth Bank will be greater than 10%. It means when beta is zero the expected

return will be equal to risk free rate of return and if beta is 1 than expected return of the stock

will be equal to market return.

Solution to Part 3: Beta Calculation

Sub Section A: Beta of each company (Share)

In order to estimate the beta of each company there are formula given in the question

itself and same has been presented below.

Covariance is estimated by use of excel formula “COVARIANCE.S” and then beta is

estimated through use of above formula.

Covariance 16.175 13.503 12.687 11.365 7.412

Beta 1.529 1.277 1.199 1.074 0.701

(Mayes, 2015)

Sub Section B: Analysis of beta for each company

Beta is well known statistical measurement of volatility specifically the systematic risk of

each of the individual stock with comparison to the unsystematic risk of the entire market. Beta

links the risk of the individual stock with market risk and provides how the expected return of

individual stocks differs from the market return.

Beta of AMP Limited, ANZ Bank, NAB Bank and Commonwealth Bank is greater than 1

and it means if market return is 10%, expected return of AMP Limited, ANZ Bank, NAB Bank

and Commonwealth Bank will be greater than 10%. It means when beta is zero the expected

return will be equal to risk free rate of return and if beta is 1 than expected return of the stock

will be equal to market return.

9

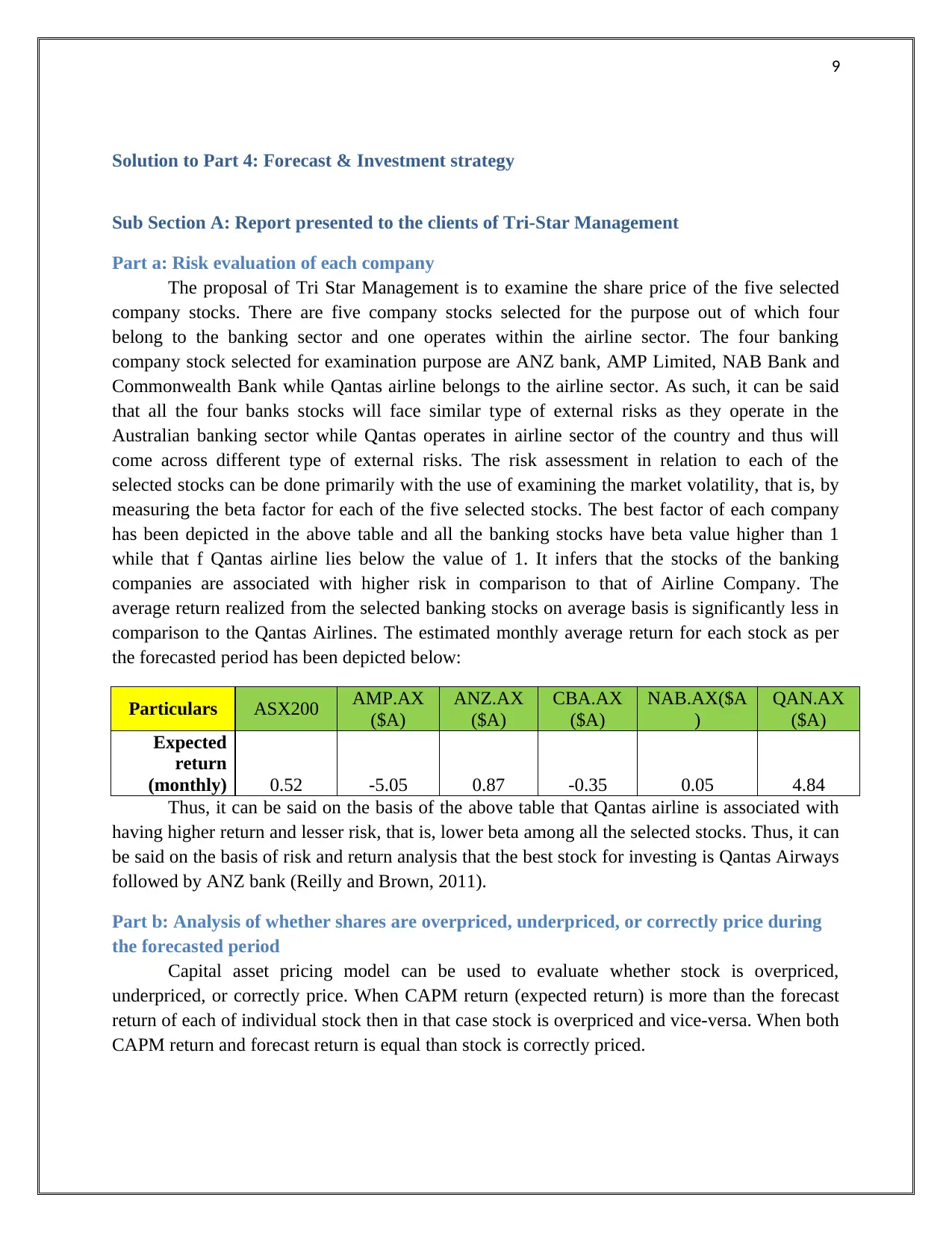

Solution to Part 4: Forecast & Investment strategy

Sub Section A: Report presented to the clients of Tri-Star Management

Part a: Risk evaluation of each company

The proposal of Tri Star Management is to examine the share price of the five selected

company stocks. There are five company stocks selected for the purpose out of which four

belong to the banking sector and one operates within the airline sector. The four banking

company stock selected for examination purpose are ANZ bank, AMP Limited, NAB Bank and

Commonwealth Bank while Qantas airline belongs to the airline sector. As such, it can be said

that all the four banks stocks will face similar type of external risks as they operate in the

Australian banking sector while Qantas operates in airline sector of the country and thus will

come across different type of external risks. The risk assessment in relation to each of the

selected stocks can be done primarily with the use of examining the market volatility, that is, by

measuring the beta factor for each of the five selected stocks. The best factor of each company

has been depicted in the above table and all the banking stocks have beta value higher than 1

while that f Qantas airline lies below the value of 1. It infers that the stocks of the banking

companies are associated with higher risk in comparison to that of Airline Company. The

average return realized from the selected banking stocks on average basis is significantly less in

comparison to the Qantas Airlines. The estimated monthly average return for each stock as per

the forecasted period has been depicted below:

Particulars ASX200 AMP.AX

($A)

ANZ.AX

($A)

CBA.AX

($A)

NAB.AX($A

)

QAN.AX

($A)

Expected

return

(monthly) 0.52 -5.05 0.87 -0.35 0.05 4.84

Thus, it can be said on the basis of the above table that Qantas airline is associated with

having higher return and lesser risk, that is, lower beta among all the selected stocks. Thus, it can

be said on the basis of risk and return analysis that the best stock for investing is Qantas Airways

followed by ANZ bank (Reilly and Brown, 2011).

Part b: Analysis of whether shares are overpriced, underpriced, or correctly price during

the forecasted period

Capital asset pricing model can be used to evaluate whether stock is overpriced,

underpriced, or correctly price. When CAPM return (expected return) is more than the forecast

return of each of individual stock then in that case stock is overpriced and vice-versa. When both

CAPM return and forecast return is equal than stock is correctly priced.

Solution to Part 4: Forecast & Investment strategy

Sub Section A: Report presented to the clients of Tri-Star Management

Part a: Risk evaluation of each company

The proposal of Tri Star Management is to examine the share price of the five selected

company stocks. There are five company stocks selected for the purpose out of which four

belong to the banking sector and one operates within the airline sector. The four banking

company stock selected for examination purpose are ANZ bank, AMP Limited, NAB Bank and

Commonwealth Bank while Qantas airline belongs to the airline sector. As such, it can be said

that all the four banks stocks will face similar type of external risks as they operate in the

Australian banking sector while Qantas operates in airline sector of the country and thus will

come across different type of external risks. The risk assessment in relation to each of the

selected stocks can be done primarily with the use of examining the market volatility, that is, by

measuring the beta factor for each of the five selected stocks. The best factor of each company

has been depicted in the above table and all the banking stocks have beta value higher than 1

while that f Qantas airline lies below the value of 1. It infers that the stocks of the banking

companies are associated with higher risk in comparison to that of Airline Company. The

average return realized from the selected banking stocks on average basis is significantly less in

comparison to the Qantas Airlines. The estimated monthly average return for each stock as per

the forecasted period has been depicted below:

Particulars ASX200 AMP.AX

($A)

ANZ.AX

($A)

CBA.AX

($A)

NAB.AX($A

)

QAN.AX

($A)

Expected

return

(monthly) 0.52 -5.05 0.87 -0.35 0.05 4.84

Thus, it can be said on the basis of the above table that Qantas airline is associated with

having higher return and lesser risk, that is, lower beta among all the selected stocks. Thus, it can

be said on the basis of risk and return analysis that the best stock for investing is Qantas Airways

followed by ANZ bank (Reilly and Brown, 2011).

Part b: Analysis of whether shares are overpriced, underpriced, or correctly price during

the forecasted period

Capital asset pricing model can be used to evaluate whether stock is overpriced,

underpriced, or correctly price. When CAPM return (expected return) is more than the forecast

return of each of individual stock then in that case stock is overpriced and vice-versa. When both

CAPM return and forecast return is equal than stock is correctly priced.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

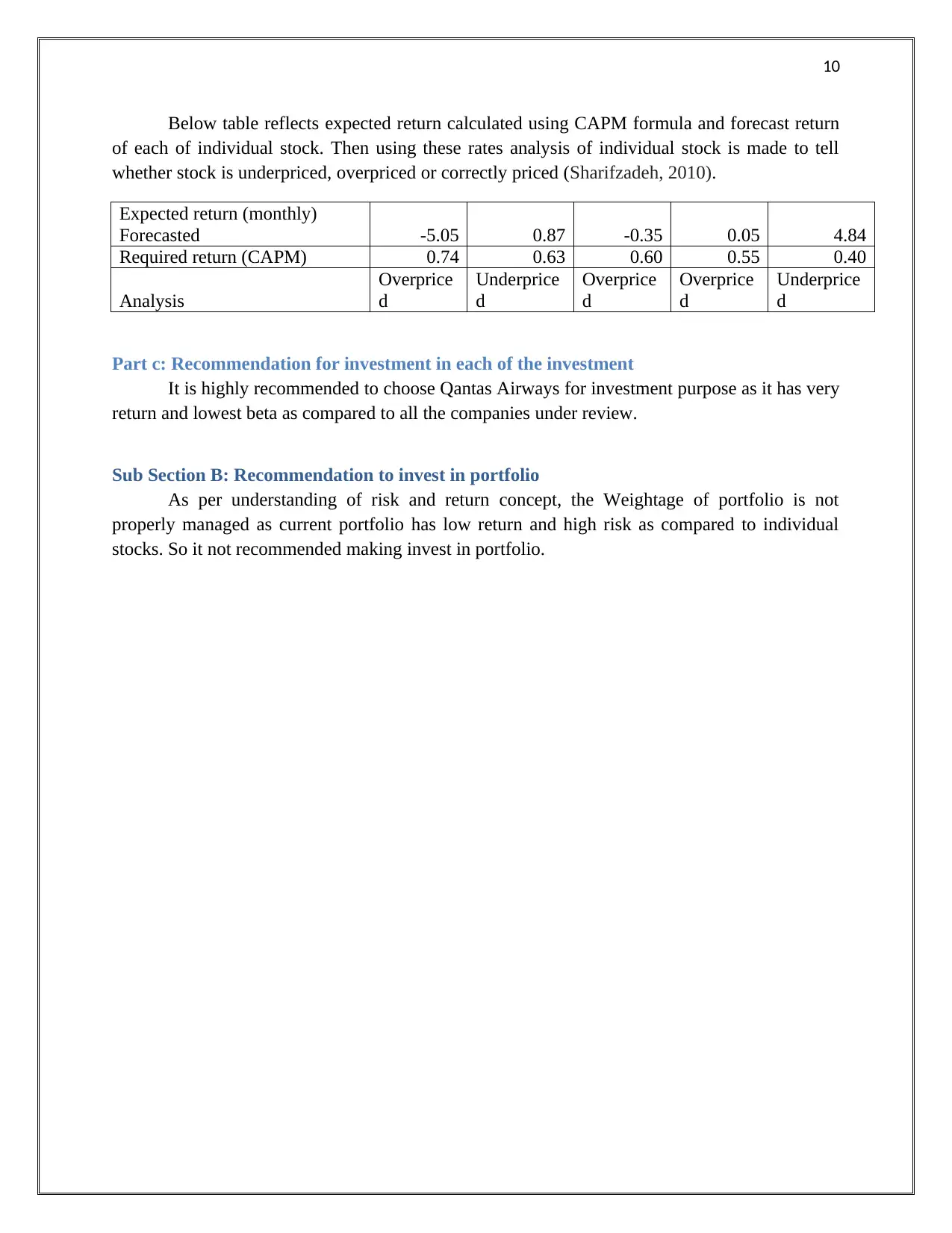

Below table reflects expected return calculated using CAPM formula and forecast return

of each of individual stock. Then using these rates analysis of individual stock is made to tell

whether stock is underpriced, overpriced or correctly priced (Sharifzadeh, 2010).

Expected return (monthly)

Forecasted -5.05 0.87 -0.35 0.05 4.84

Required return (CAPM) 0.74 0.63 0.60 0.55 0.40

Analysis

Overprice

d

Underprice

d

Overprice

d

Overprice

d

Underprice

d

Part c: Recommendation for investment in each of the investment

It is highly recommended to choose Qantas Airways for investment purpose as it has very

return and lowest beta as compared to all the companies under review.

Sub Section B: Recommendation to invest in portfolio

As per understanding of risk and return concept, the Weightage of portfolio is not

properly managed as current portfolio has low return and high risk as compared to individual

stocks. So it not recommended making invest in portfolio.

Below table reflects expected return calculated using CAPM formula and forecast return

of each of individual stock. Then using these rates analysis of individual stock is made to tell

whether stock is underpriced, overpriced or correctly priced (Sharifzadeh, 2010).

Expected return (monthly)

Forecasted -5.05 0.87 -0.35 0.05 4.84

Required return (CAPM) 0.74 0.63 0.60 0.55 0.40

Analysis

Overprice

d

Underprice

d

Overprice

d

Overprice

d

Underprice

d

Part c: Recommendation for investment in each of the investment

It is highly recommended to choose Qantas Airways for investment purpose as it has very

return and lowest beta as compared to all the companies under review.

Sub Section B: Recommendation to invest in portfolio

As per understanding of risk and return concept, the Weightage of portfolio is not

properly managed as current portfolio has low return and high risk as compared to individual

stocks. So it not recommended making invest in portfolio.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

References

Levy, H. 2011. The Capital Asset Pricing Model in the 21st Century: Analytical, Empirical, and

Behavioral Perspectives. USA: Cambridge University Press.

Madura, J. 2014. Financial Markets and Institutions. Germany: Cengage Learning.

Mayes, TR 2015, Financial Analysis with Microsoft Excel. Boston: Cengage Learning.

Moles, P. and Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Reilly.F.K. and Brown.K.C. 2011. Investment analysis & portfolio management. Australia:

South western Cengage learning.

Sharifzadeh, M. 2010. An Empirical and Theoretical Analysis of Capital Asset Pricing Model.

USA: John Wiley &sons.

References

Levy, H. 2011. The Capital Asset Pricing Model in the 21st Century: Analytical, Empirical, and

Behavioral Perspectives. USA: Cambridge University Press.

Madura, J. 2014. Financial Markets and Institutions. Germany: Cengage Learning.

Mayes, TR 2015, Financial Analysis with Microsoft Excel. Boston: Cengage Learning.

Moles, P. and Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Reilly.F.K. and Brown.K.C. 2011. Investment analysis & portfolio management. Australia:

South western Cengage learning.

Sharifzadeh, M. 2010. An Empirical and Theoretical Analysis of Capital Asset Pricing Model.

USA: John Wiley &sons.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.