Phillips Curve: Importance & Vulnerabilities in Keynesian Theory

VerifiedAdded on 2023/04/21

|13

|3802

|285

Essay

AI Summary

This essay examines the importance of the Phillips Curve within the framework of Orthodox Keynesianism, exploring its role in addressing the 'missing equation' problem related to wage determination. It discusses Lipsey's theoretical account of the Phillips Curve and how it established a relationship between aggregate demand and money wages, effectively 'closing' the Keynesian system. The essay further analyzes the theoretical assault on the Phillips Curve, focusing on the expectations-augmented Phillips Curve and Friedman's argument about its verticality in the long run. It also addresses the curve's inability to accommodate the stagflationary conditions of the 1970s, highlighting the damaging impact on Orthodox Keynesianism. Finally, the essay considers the structural conditions in both the UK and international markets during the 1970s that eroded the foundations of Keynesianism.

1

Importance of Phillips curve in Orthodox Keynesianism

Importance of Phillips curve in Orthodox Keynesianism

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Introduction......................................................................................................................................3

Importance of Phillips curve to the orthodox Keynesianism...........................................................3

Expectations augmented Phillips curve...........................................................................................5

Effect of 1970s structural conditions in the UK market..................................................................8

Effect of 1970s structural conditions in the international market place......................................9

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................3

Importance of Phillips curve to the orthodox Keynesianism...........................................................3

Expectations augmented Phillips curve...........................................................................................5

Effect of 1970s structural conditions in the UK market..................................................................8

Effect of 1970s structural conditions in the international market place......................................9

Conclusion.....................................................................................................................................10

Reference.......................................................................................................................................11

3

Introduction

A Phillips curve shows the inverse relationship between the unemployment rate and the rate of

inflation in an economy. According to Colander (1995), it can make an association between the

nominal variables such as the price level, the wage rate, the inflation rate and between the other

components of the real economy. More specifically, it can be stated that the Phillips curve can

derive the changes of nominal income and how it would decompose the changing of quantities as

well as the price level of the goods. Therefore, in terms of economics, the nature of Phillips

curve can determine the reflection of the interaction of demand and supply on the economy and

how it would affect the real and the nominal variables of the economy, so that the policymakers

would also be affected. Before discussing the importance of Phillips in the orthodox economy, it

is necessary to describe the discovery behind its origin.

Importance of Phillips curve to the orthodox Keynesianism

In the opinion of Forder (2010), A. W. Phillips, the economist of the London School of

Economics, had discovered the concept of this curve in the year 1950, while he was engaging

with the Keynesian analytical framework. As per the Keynesian theory, during the period of

recession, the inflationary pressure is much lower. However, if the output of the economy would

start to push the potential GDP, then the economy would face greater challenges. During this

period, Phillips found that the inflation rate of a country is inversely related with the rate of

unemployment of the country. In this context, he collected 60 years information of the UK and

hence, his propounded theory is referred as Phillips curve and has started to describe in the

Keynesian economy.

Introduction

A Phillips curve shows the inverse relationship between the unemployment rate and the rate of

inflation in an economy. According to Colander (1995), it can make an association between the

nominal variables such as the price level, the wage rate, the inflation rate and between the other

components of the real economy. More specifically, it can be stated that the Phillips curve can

derive the changes of nominal income and how it would decompose the changing of quantities as

well as the price level of the goods. Therefore, in terms of economics, the nature of Phillips

curve can determine the reflection of the interaction of demand and supply on the economy and

how it would affect the real and the nominal variables of the economy, so that the policymakers

would also be affected. Before discussing the importance of Phillips in the orthodox economy, it

is necessary to describe the discovery behind its origin.

Importance of Phillips curve to the orthodox Keynesianism

In the opinion of Forder (2010), A. W. Phillips, the economist of the London School of

Economics, had discovered the concept of this curve in the year 1950, while he was engaging

with the Keynesian analytical framework. As per the Keynesian theory, during the period of

recession, the inflationary pressure is much lower. However, if the output of the economy would

start to push the potential GDP, then the economy would face greater challenges. During this

period, Phillips found that the inflation rate of a country is inversely related with the rate of

unemployment of the country. In this context, he collected 60 years information of the UK and

hence, his propounded theory is referred as Phillips curve and has started to describe in the

Keynesian economy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

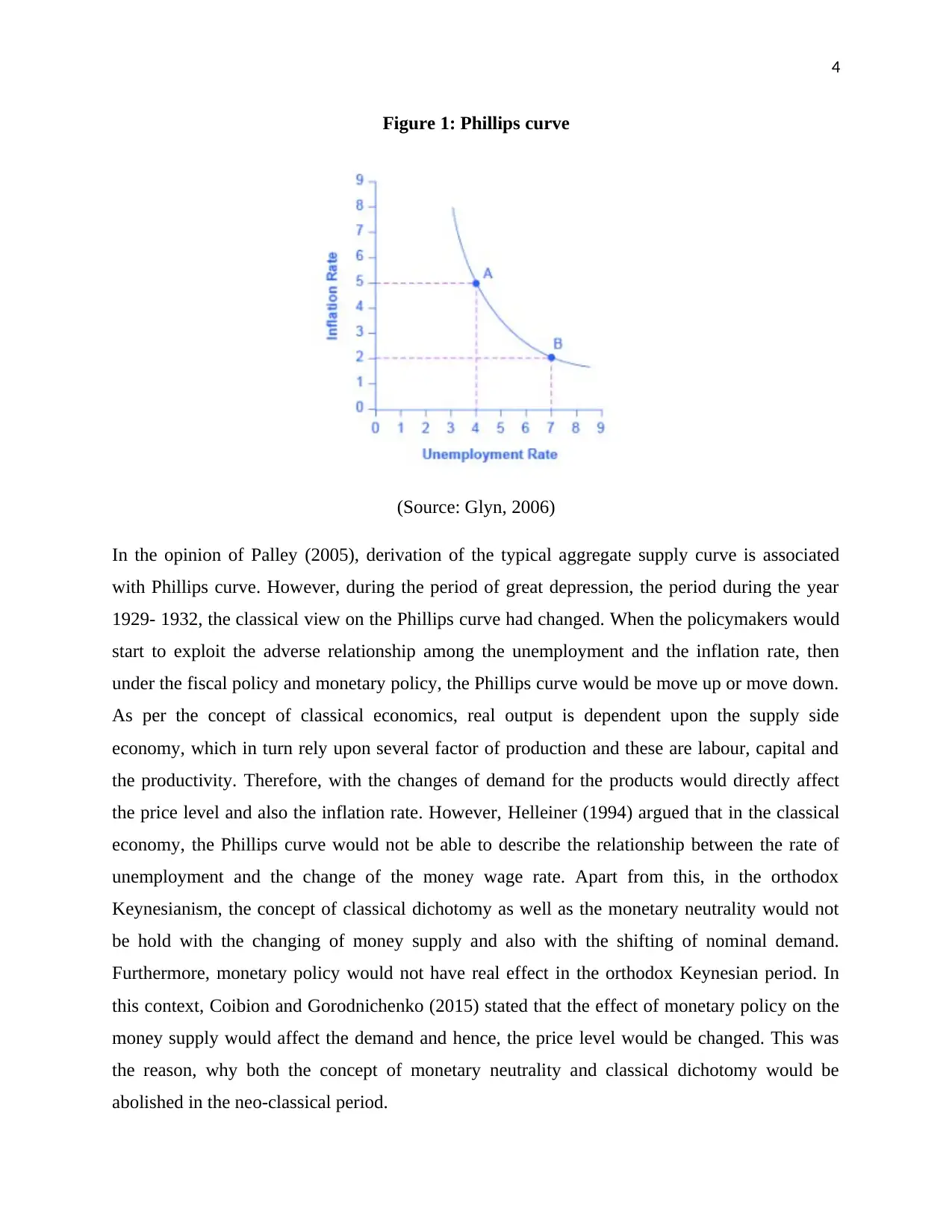

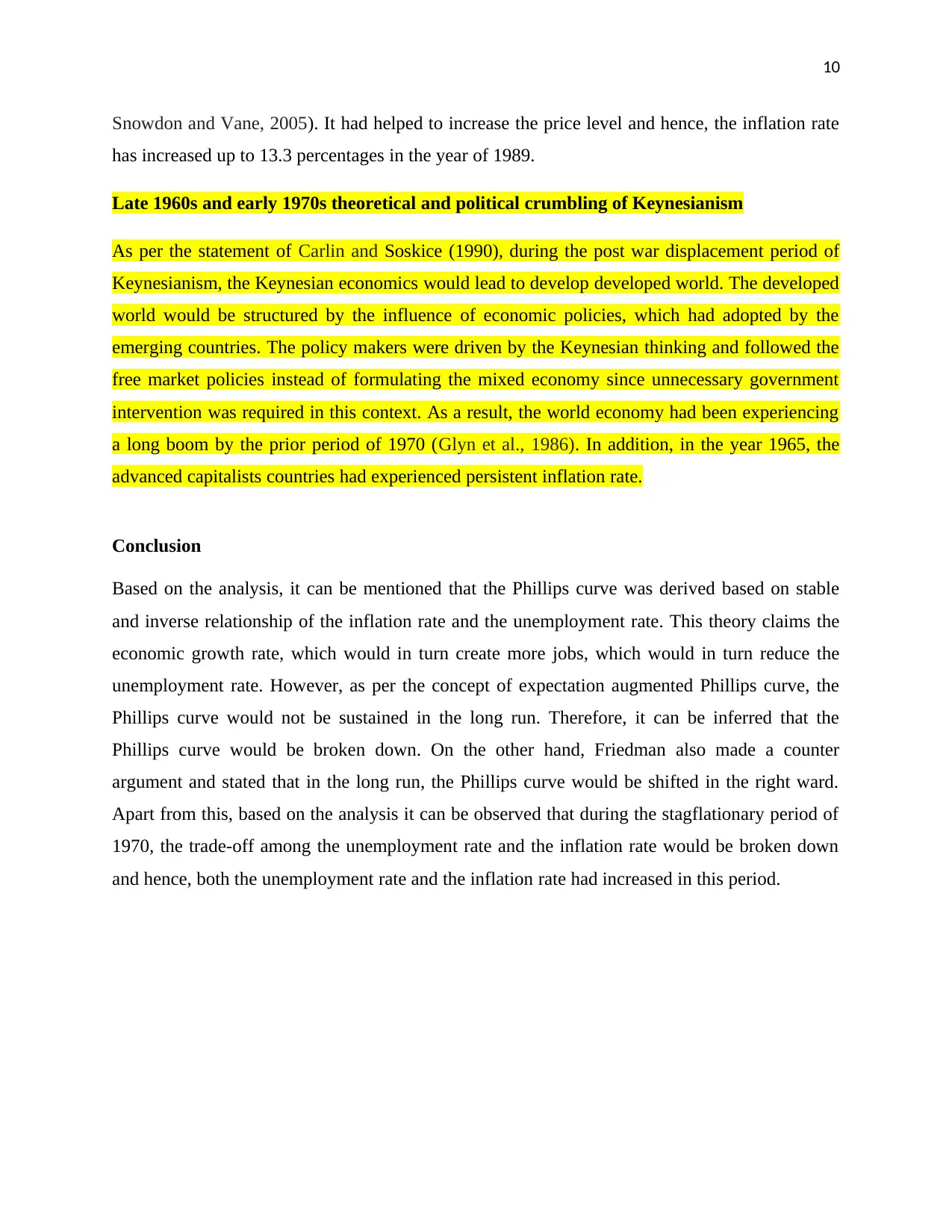

Figure 1: Phillips curve

(Source: Glyn, 2006)

In the opinion of Palley (2005), derivation of the typical aggregate supply curve is associated

with Phillips curve. However, during the period of great depression, the period during the year

1929- 1932, the classical view on the Phillips curve had changed. When the policymakers would

start to exploit the adverse relationship among the unemployment and the inflation rate, then

under the fiscal policy and monetary policy, the Phillips curve would be move up or move down.

As per the concept of classical economics, real output is dependent upon the supply side

economy, which in turn rely upon several factor of production and these are labour, capital and

the productivity. Therefore, with the changes of demand for the products would directly affect

the price level and also the inflation rate. However, Helleiner (1994) argued that in the classical

economy, the Phillips curve would not be able to describe the relationship between the rate of

unemployment and the change of the money wage rate. Apart from this, in the orthodox

Keynesianism, the concept of classical dichotomy as well as the monetary neutrality would not

be hold with the changing of money supply and also with the shifting of nominal demand.

Furthermore, monetary policy would not have real effect in the orthodox Keynesian period. In

this context, Coibion and Gorodnichenko (2015) stated that the effect of monetary policy on the

money supply would affect the demand and hence, the price level would be changed. This was

the reason, why both the concept of monetary neutrality and classical dichotomy would be

abolished in the neo-classical period.

Figure 1: Phillips curve

(Source: Glyn, 2006)

In the opinion of Palley (2005), derivation of the typical aggregate supply curve is associated

with Phillips curve. However, during the period of great depression, the period during the year

1929- 1932, the classical view on the Phillips curve had changed. When the policymakers would

start to exploit the adverse relationship among the unemployment and the inflation rate, then

under the fiscal policy and monetary policy, the Phillips curve would be move up or move down.

As per the concept of classical economics, real output is dependent upon the supply side

economy, which in turn rely upon several factor of production and these are labour, capital and

the productivity. Therefore, with the changes of demand for the products would directly affect

the price level and also the inflation rate. However, Helleiner (1994) argued that in the classical

economy, the Phillips curve would not be able to describe the relationship between the rate of

unemployment and the change of the money wage rate. Apart from this, in the orthodox

Keynesianism, the concept of classical dichotomy as well as the monetary neutrality would not

be hold with the changing of money supply and also with the shifting of nominal demand.

Furthermore, monetary policy would not have real effect in the orthodox Keynesian period. In

this context, Coibion and Gorodnichenko (2015) stated that the effect of monetary policy on the

money supply would affect the demand and hence, the price level would be changed. This was

the reason, why both the concept of monetary neutrality and classical dichotomy would be

abolished in the neo-classical period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

In the neo-classical synthesis, it can be mentioned that the Phillips curve can establish the

relationship between the rates of inflation with the changing of the real economic activities.

However, this concept was against the concept of Phillips curve, which was found in the year

1958. In the orthodox Keynesian, the Phillips curve would formulate the statistical relationship

between the percentage changes in the nominal wage rate and the rate of unemployment. More

specifically, Phillips curve would derive an inverse association between the wage inflation and

the unemployment rate as the proxy of the relationship of price inflation and the real output of

the classical period. Therefore, aggregate supply (AS) curve has positive and finite slope, which

would be related with the negatively sloping Phillips curve. It would in turn develop a positive

relationship between the output level and the rate of inflation. In case of equilibrium position of

the labour market, then the nominal wage rate would not be changed. With the rise of aggregate

demand, it would increase the labour demand and hence, the rate of unemployment would be

declined below the level of equilibrium. Consequently, the nominal wage rate of the employees

and the price level would be increased. Therefore, Galí (2011) cited that the negative slope of the

Phillips curve is the reflection of the excess demand of labour and the lowering unemployment

rate. On the other hand, the wage inflation would also be increased. From this point, it can be

stated that the neoclassical synthesis is the effect of pre-Keynesian neoclassical theory as well as

the Keynesian macroeconomics. This theory was criticised by Richard Lipsey (1960) and stated

that the neoclassical micro theory was converted into the macroeconomics and was referred as

demand pull theories. He also stated that under the labour market disequilibrium position, wage

inflation is dependent upon the distinction among the labour demand and the supply of labour

(Gordon, 2011).

Expectations augmented Phillips curve

The expectations augmented Phillips curve has initiated adaptive expectations in the Phillips

curve. In the opinion of Correa and Minella (2010), the expectations augmented Phillips curve

was initially used for explaining the monetarist view. The expectations augmented model would

lead to the shift of government ability to act. Moreover, under the Keynesian money illusion, the

changes of nominal variables such as the price level and the wage rate as well as the purchasing

power would be stable. As a result, if the government would decide to rely on the expansionary

monetary policy, then the unemployment rate would be declined and the inflation rate would be

In the neo-classical synthesis, it can be mentioned that the Phillips curve can establish the

relationship between the rates of inflation with the changing of the real economic activities.

However, this concept was against the concept of Phillips curve, which was found in the year

1958. In the orthodox Keynesian, the Phillips curve would formulate the statistical relationship

between the percentage changes in the nominal wage rate and the rate of unemployment. More

specifically, Phillips curve would derive an inverse association between the wage inflation and

the unemployment rate as the proxy of the relationship of price inflation and the real output of

the classical period. Therefore, aggregate supply (AS) curve has positive and finite slope, which

would be related with the negatively sloping Phillips curve. It would in turn develop a positive

relationship between the output level and the rate of inflation. In case of equilibrium position of

the labour market, then the nominal wage rate would not be changed. With the rise of aggregate

demand, it would increase the labour demand and hence, the rate of unemployment would be

declined below the level of equilibrium. Consequently, the nominal wage rate of the employees

and the price level would be increased. Therefore, Galí (2011) cited that the negative slope of the

Phillips curve is the reflection of the excess demand of labour and the lowering unemployment

rate. On the other hand, the wage inflation would also be increased. From this point, it can be

stated that the neoclassical synthesis is the effect of pre-Keynesian neoclassical theory as well as

the Keynesian macroeconomics. This theory was criticised by Richard Lipsey (1960) and stated

that the neoclassical micro theory was converted into the macroeconomics and was referred as

demand pull theories. He also stated that under the labour market disequilibrium position, wage

inflation is dependent upon the distinction among the labour demand and the supply of labour

(Gordon, 2011).

Expectations augmented Phillips curve

The expectations augmented Phillips curve has initiated adaptive expectations in the Phillips

curve. In the opinion of Correa and Minella (2010), the expectations augmented Phillips curve

was initially used for explaining the monetarist view. The expectations augmented model would

lead to the shift of government ability to act. Moreover, under the Keynesian money illusion, the

changes of nominal variables such as the price level and the wage rate as well as the purchasing

power would be stable. As a result, if the government would decide to rely on the expansionary

monetary policy, then the unemployment rate would be declined and the inflation rate would be

6

increased. On the other hand, both Phelps and Friedman had argued that the government would

not trade at the high rate of unemployment for lowering down the unemployment rate. Both the

economists mentioned that the real wage rate is constant. In this context, the government would

use both the fiscal or monetary policy in order to lowering down the rate of unemployment under

the natural rate. As a result, increase in demand would increase the price level compared to the

anticipation rate of the employees. For instance, in case of higher revenues, the organisations

would like to employ more employees at the similar wage rate. In case of rising of money wage

rate, the organisations would stop to supply more labours. This is the reason, why the rate of

unemployment would be declined. Furthermore, the purchasing power would be decreased with

the reduction of purchasing power. On the contrary, Daly and Hobijn (2014) argued that with the

passage of time, and in case of higher price inflation, the organisations would like to supply less

labour and would create pressure to maximise the wage rate in order to align with the inflation

rate. Therefore, it can be inferred that both the presence of price inflation and wage inflation

would sustain expansionary fiscal policies at the higher rate.

Both the economists, Phelps and Friedman, also highlighted the diversification among the long

run and short run Phillips curve. As per the concept of Phillips curve of 1960s, the average

inflation rate would be constant, where the inflation rate and the rate of unemployment are

inversely associated. However, with the changes of average inflation rate, the policymakers

would continuously try to push down the rate of unemployment below the natural rate (Correa

and Minella, 2010). Therefore, if the perception of the workers would be similar with the real

values, then the natural unemployment rate would be compatible with the inflation rate.

Therefore, the long run Phillips curve would be vertical and it would be above the natural rate.

Nonetheless, in the transitional phase, it can be observed that the average rate of inflation would

be shifted persistently (Mavroeidis, Plagborg-Møller and Stock, 2014). More specifically, it can

be stated that both the long run as well as short run is the combination of expectations augmented

Phillips curve. The unemployment rate would be returned to its natural rate when the expectation

of the workers towards the price inflation would adapt the changes of actual inflation rate.

On the contrary, Mavroeidis, Plagborg-Møller and Stock (2014) argued that the trade-off among

the unemployment rate and the inflation rate, which would be explained with the help of Phillips

curve, had broken down during the stagflationary period of 1970. During this period, both the

increased. On the other hand, both Phelps and Friedman had argued that the government would

not trade at the high rate of unemployment for lowering down the unemployment rate. Both the

economists mentioned that the real wage rate is constant. In this context, the government would

use both the fiscal or monetary policy in order to lowering down the rate of unemployment under

the natural rate. As a result, increase in demand would increase the price level compared to the

anticipation rate of the employees. For instance, in case of higher revenues, the organisations

would like to employ more employees at the similar wage rate. In case of rising of money wage

rate, the organisations would stop to supply more labours. This is the reason, why the rate of

unemployment would be declined. Furthermore, the purchasing power would be decreased with

the reduction of purchasing power. On the contrary, Daly and Hobijn (2014) argued that with the

passage of time, and in case of higher price inflation, the organisations would like to supply less

labour and would create pressure to maximise the wage rate in order to align with the inflation

rate. Therefore, it can be inferred that both the presence of price inflation and wage inflation

would sustain expansionary fiscal policies at the higher rate.

Both the economists, Phelps and Friedman, also highlighted the diversification among the long

run and short run Phillips curve. As per the concept of Phillips curve of 1960s, the average

inflation rate would be constant, where the inflation rate and the rate of unemployment are

inversely associated. However, with the changes of average inflation rate, the policymakers

would continuously try to push down the rate of unemployment below the natural rate (Correa

and Minella, 2010). Therefore, if the perception of the workers would be similar with the real

values, then the natural unemployment rate would be compatible with the inflation rate.

Therefore, the long run Phillips curve would be vertical and it would be above the natural rate.

Nonetheless, in the transitional phase, it can be observed that the average rate of inflation would

be shifted persistently (Mavroeidis, Plagborg-Møller and Stock, 2014). More specifically, it can

be stated that both the long run as well as short run is the combination of expectations augmented

Phillips curve. The unemployment rate would be returned to its natural rate when the expectation

of the workers towards the price inflation would adapt the changes of actual inflation rate.

On the contrary, Mavroeidis, Plagborg-Møller and Stock (2014) argued that the trade-off among

the unemployment rate and the inflation rate, which would be explained with the help of Phillips

curve, had broken down during the stagflationary period of 1970. During this period, both the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

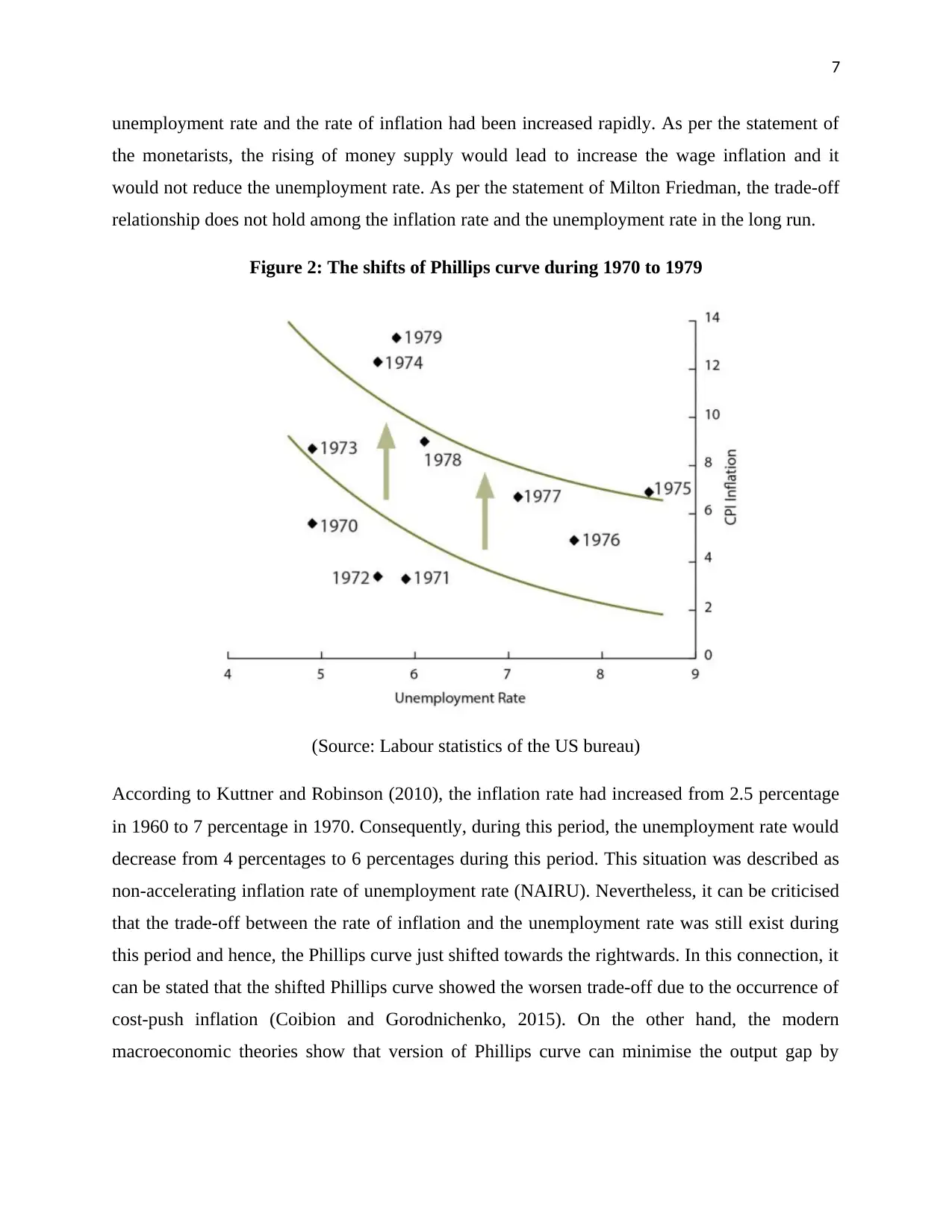

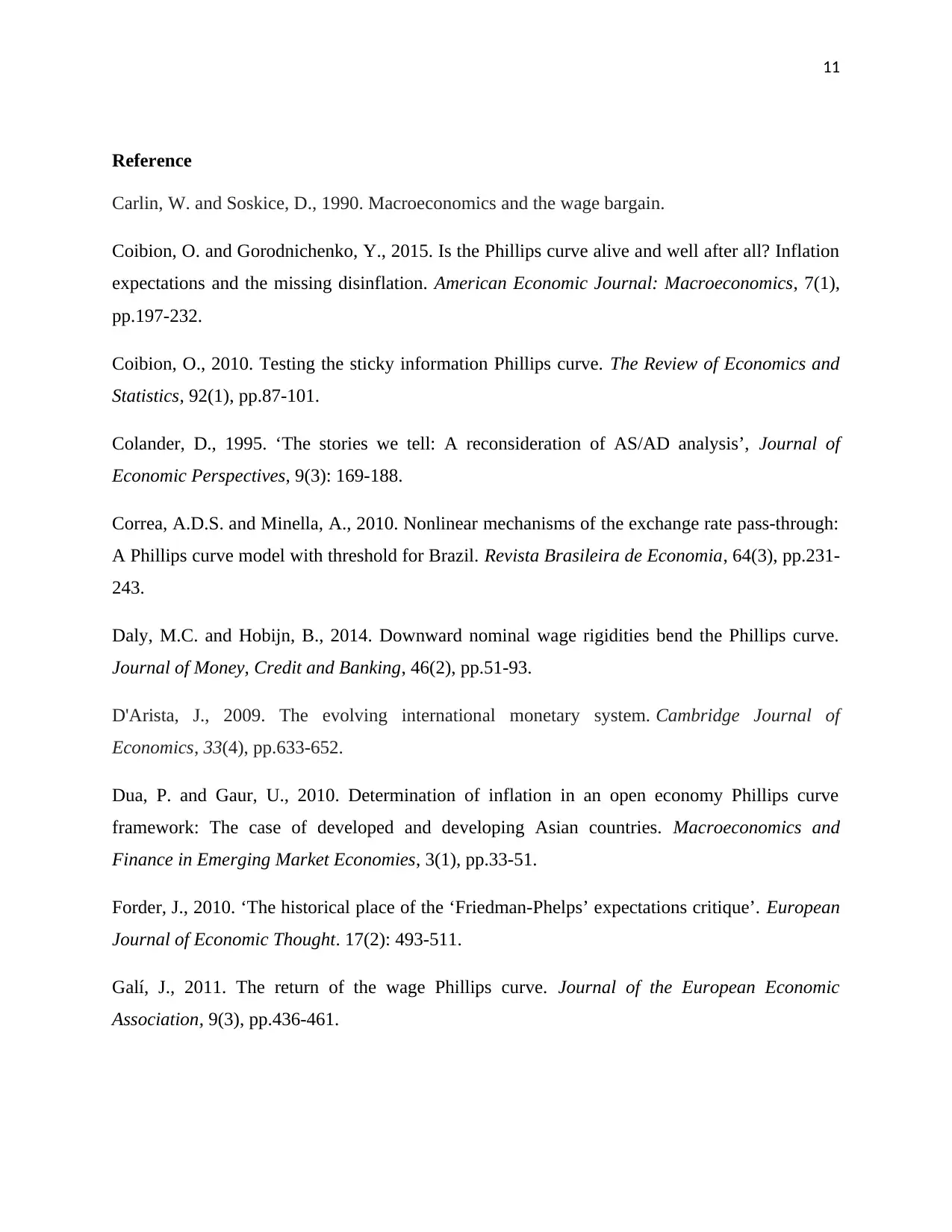

unemployment rate and the rate of inflation had been increased rapidly. As per the statement of

the monetarists, the rising of money supply would lead to increase the wage inflation and it

would not reduce the unemployment rate. As per the statement of Milton Friedman, the trade-off

relationship does not hold among the inflation rate and the unemployment rate in the long run.

Figure 2: The shifts of Phillips curve during 1970 to 1979

(Source: Labour statistics of the US bureau)

According to Kuttner and Robinson (2010), the inflation rate had increased from 2.5 percentage

in 1960 to 7 percentage in 1970. Consequently, during this period, the unemployment rate would

decrease from 4 percentages to 6 percentages during this period. This situation was described as

non-accelerating inflation rate of unemployment rate (NAIRU). Nevertheless, it can be criticised

that the trade-off between the rate of inflation and the unemployment rate was still exist during

this period and hence, the Phillips curve just shifted towards the rightwards. In this connection, it

can be stated that the shifted Phillips curve showed the worsen trade-off due to the occurrence of

cost-push inflation (Coibion and Gorodnichenko, 2015). On the other hand, the modern

macroeconomic theories show that version of Phillips curve can minimise the output gap by

unemployment rate and the rate of inflation had been increased rapidly. As per the statement of

the monetarists, the rising of money supply would lead to increase the wage inflation and it

would not reduce the unemployment rate. As per the statement of Milton Friedman, the trade-off

relationship does not hold among the inflation rate and the unemployment rate in the long run.

Figure 2: The shifts of Phillips curve during 1970 to 1979

(Source: Labour statistics of the US bureau)

According to Kuttner and Robinson (2010), the inflation rate had increased from 2.5 percentage

in 1960 to 7 percentage in 1970. Consequently, during this period, the unemployment rate would

decrease from 4 percentages to 6 percentages during this period. This situation was described as

non-accelerating inflation rate of unemployment rate (NAIRU). Nevertheless, it can be criticised

that the trade-off between the rate of inflation and the unemployment rate was still exist during

this period and hence, the Phillips curve just shifted towards the rightwards. In this connection, it

can be stated that the shifted Phillips curve showed the worsen trade-off due to the occurrence of

cost-push inflation (Coibion and Gorodnichenko, 2015). On the other hand, the modern

macroeconomic theories show that version of Phillips curve can minimise the output gap by

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

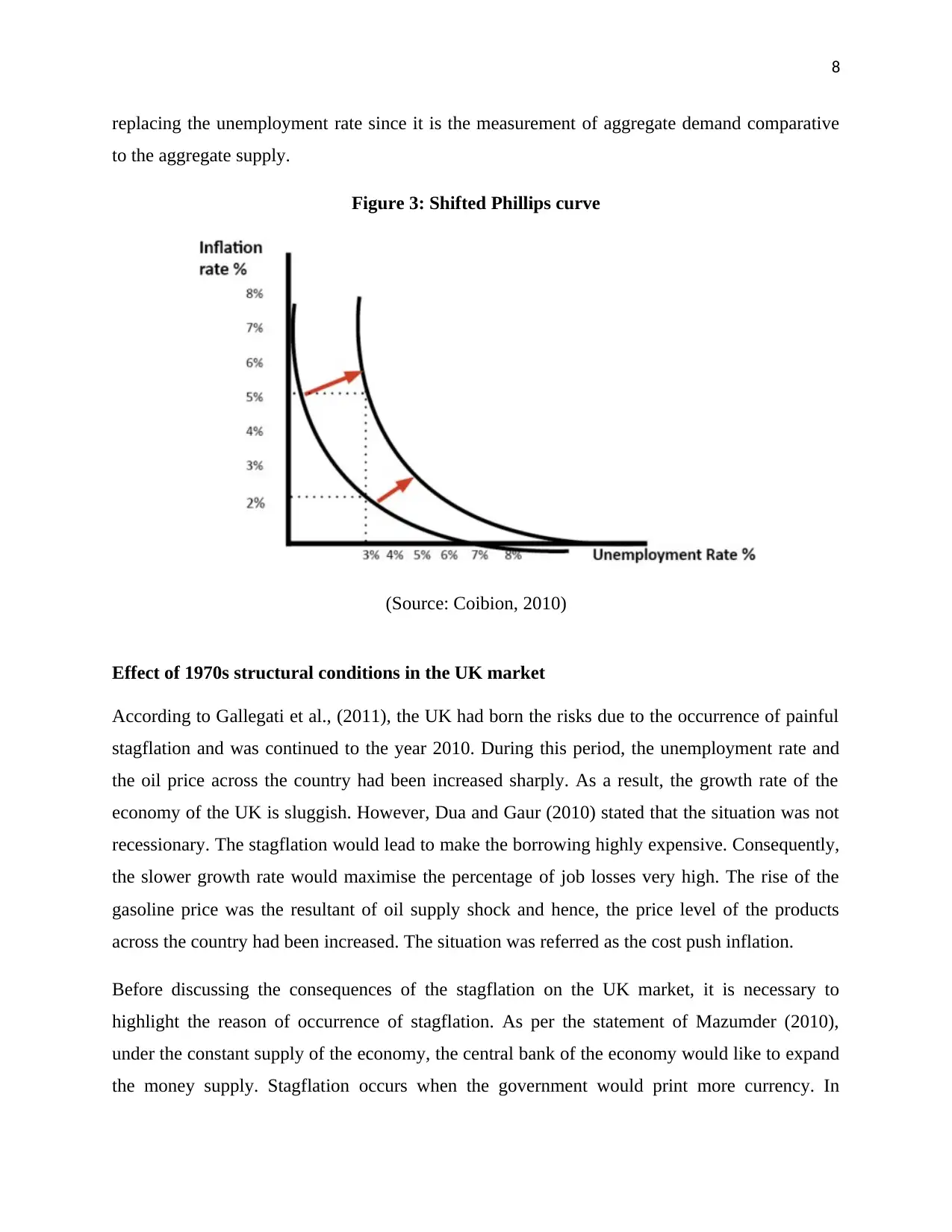

replacing the unemployment rate since it is the measurement of aggregate demand comparative

to the aggregate supply.

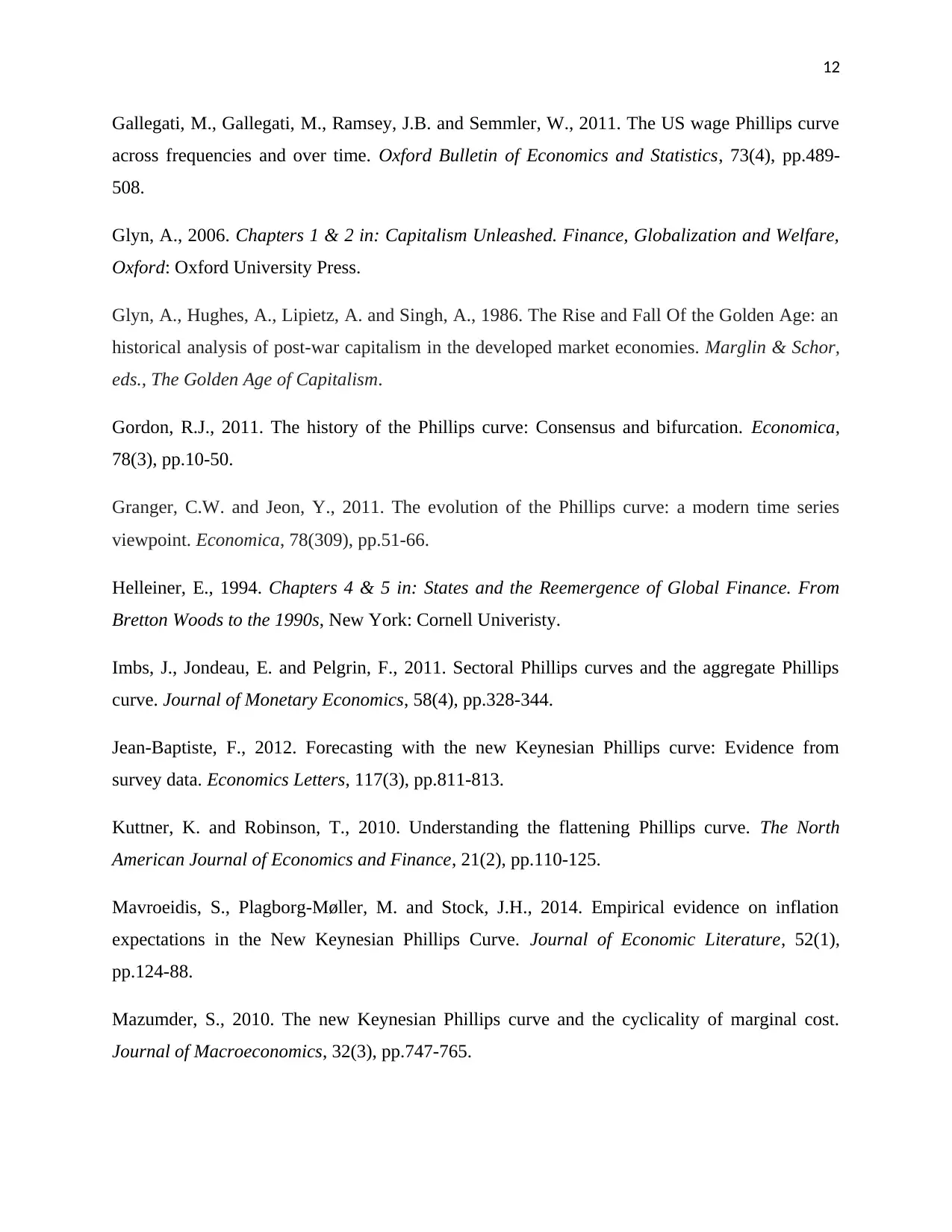

Figure 3: Shifted Phillips curve

(Source: Coibion, 2010)

Effect of 1970s structural conditions in the UK market

According to Gallegati et al., (2011), the UK had born the risks due to the occurrence of painful

stagflation and was continued to the year 2010. During this period, the unemployment rate and

the oil price across the country had been increased sharply. As a result, the growth rate of the

economy of the UK is sluggish. However, Dua and Gaur (2010) stated that the situation was not

recessionary. The stagflation would lead to make the borrowing highly expensive. Consequently,

the slower growth rate would maximise the percentage of job losses very high. The rise of the

gasoline price was the resultant of oil supply shock and hence, the price level of the products

across the country had been increased. The situation was referred as the cost push inflation.

Before discussing the consequences of the stagflation on the UK market, it is necessary to

highlight the reason of occurrence of stagflation. As per the statement of Mazumder (2010),

under the constant supply of the economy, the central bank of the economy would like to expand

the money supply. Stagflation occurs when the government would print more currency. In

replacing the unemployment rate since it is the measurement of aggregate demand comparative

to the aggregate supply.

Figure 3: Shifted Phillips curve

(Source: Coibion, 2010)

Effect of 1970s structural conditions in the UK market

According to Gallegati et al., (2011), the UK had born the risks due to the occurrence of painful

stagflation and was continued to the year 2010. During this period, the unemployment rate and

the oil price across the country had been increased sharply. As a result, the growth rate of the

economy of the UK is sluggish. However, Dua and Gaur (2010) stated that the situation was not

recessionary. The stagflation would lead to make the borrowing highly expensive. Consequently,

the slower growth rate would maximise the percentage of job losses very high. The rise of the

gasoline price was the resultant of oil supply shock and hence, the price level of the products

across the country had been increased. The situation was referred as the cost push inflation.

Before discussing the consequences of the stagflation on the UK market, it is necessary to

highlight the reason of occurrence of stagflation. As per the statement of Mazumder (2010),

under the constant supply of the economy, the central bank of the economy would like to expand

the money supply. Stagflation occurs when the government would print more currency. In

9

addition, the central banks would aim to create more credit. Consequently, the money supply and

the money supply would be increased.

As per the concept of the Keynesian theories, the inflation rate is inversely related with the

unemployment rate as well as is positively related with the growth of the economy. In 1970, the

rising price level and the rising unemployment rate would be the resultant of cost push inflation

and hence, the oil price would be increased (Granger and Jeon, 2011). The monetary policy was

also expensive in this period. Apart from the monetary policy, the export and the import

behaviour of the country had been affected due to the stagflationary situation.

Effect of 1970s structural conditions in the international market place

It is known that stagflation occurs due to the higher inflation and the higher unemployment rate.

It prevents the growth rate of the economy. In the opinion of Jean-Baptiste (2012), after the

occurrence of the stagflation in 1970, the federal government had started to manipulate the

currency in order to spur the growth rate of the economy. The stagflation during the period of

1973 to 1975 was referred as the situation of recession. In the global economy, the

unemployment rate had reached to the highest peak in the year 1975 and was stuck at 9

percentages. The inflation rate also reached to 9.6 per cent from 3.4 per cent in 1973 (Rumler

and Valderrama, 2010; D'Arista, 2009). Apart from this, the global GDP was negative since last

three quarters of 1970.

During the stagflationary period, the US government had implemented three fiscal policies.

Firstly, Nixon, the US president of that period, had frozen the wage level and the price rate for

90 days. After that the price commission and pay board had developed for increasing the wage

and price after 90 days. This was beneficial to control the price level after the year of 1972. This

was the effective approach of controlling the global inflation rate. Secondly, Nixon had planned

to impose 10 percentage of tariff on the imports. He aimed at lowering down the balance of trade

for protecting the domestic firms. In addition, he increased the price of the importable. Thirdly,

Nixon had removed the system of gold standard. It would help to keep the value of dollar at the

fixed rate since the year 1944. In order to worsen the stagflation, the fed government had

increase the funds rate between the period of 1971to 1978 (Imbs, Jondeau and Pelgrin, 2011;

addition, the central banks would aim to create more credit. Consequently, the money supply and

the money supply would be increased.

As per the concept of the Keynesian theories, the inflation rate is inversely related with the

unemployment rate as well as is positively related with the growth of the economy. In 1970, the

rising price level and the rising unemployment rate would be the resultant of cost push inflation

and hence, the oil price would be increased (Granger and Jeon, 2011). The monetary policy was

also expensive in this period. Apart from the monetary policy, the export and the import

behaviour of the country had been affected due to the stagflationary situation.

Effect of 1970s structural conditions in the international market place

It is known that stagflation occurs due to the higher inflation and the higher unemployment rate.

It prevents the growth rate of the economy. In the opinion of Jean-Baptiste (2012), after the

occurrence of the stagflation in 1970, the federal government had started to manipulate the

currency in order to spur the growth rate of the economy. The stagflation during the period of

1973 to 1975 was referred as the situation of recession. In the global economy, the

unemployment rate had reached to the highest peak in the year 1975 and was stuck at 9

percentages. The inflation rate also reached to 9.6 per cent from 3.4 per cent in 1973 (Rumler

and Valderrama, 2010; D'Arista, 2009). Apart from this, the global GDP was negative since last

three quarters of 1970.

During the stagflationary period, the US government had implemented three fiscal policies.

Firstly, Nixon, the US president of that period, had frozen the wage level and the price rate for

90 days. After that the price commission and pay board had developed for increasing the wage

and price after 90 days. This was beneficial to control the price level after the year of 1972. This

was the effective approach of controlling the global inflation rate. Secondly, Nixon had planned

to impose 10 percentage of tariff on the imports. He aimed at lowering down the balance of trade

for protecting the domestic firms. In addition, he increased the price of the importable. Thirdly,

Nixon had removed the system of gold standard. It would help to keep the value of dollar at the

fixed rate since the year 1944. In order to worsen the stagflation, the fed government had

increase the funds rate between the period of 1971to 1978 (Imbs, Jondeau and Pelgrin, 2011;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Snowdon and Vane, 2005). It had helped to increase the price level and hence, the inflation rate

has increased up to 13.3 percentages in the year of 1989.

Late 1960s and early 1970s theoretical and political crumbling of Keynesianism

As per the statement of Carlin and Soskice (1990), during the post war displacement period of

Keynesianism, the Keynesian economics would lead to develop developed world. The developed

world would be structured by the influence of economic policies, which had adopted by the

emerging countries. The policy makers were driven by the Keynesian thinking and followed the

free market policies instead of formulating the mixed economy since unnecessary government

intervention was required in this context. As a result, the world economy had been experiencing

a long boom by the prior period of 1970 (Glyn et al., 1986). In addition, in the year 1965, the

advanced capitalists countries had experienced persistent inflation rate.

Conclusion

Based on the analysis, it can be mentioned that the Phillips curve was derived based on stable

and inverse relationship of the inflation rate and the unemployment rate. This theory claims the

economic growth rate, which would in turn create more jobs, which would in turn reduce the

unemployment rate. However, as per the concept of expectation augmented Phillips curve, the

Phillips curve would not be sustained in the long run. Therefore, it can be inferred that the

Phillips curve would be broken down. On the other hand, Friedman also made a counter

argument and stated that in the long run, the Phillips curve would be shifted in the right ward.

Apart from this, based on the analysis it can be observed that during the stagflationary period of

1970, the trade-off among the unemployment rate and the inflation rate would be broken down

and hence, both the unemployment rate and the inflation rate had increased in this period.

Snowdon and Vane, 2005). It had helped to increase the price level and hence, the inflation rate

has increased up to 13.3 percentages in the year of 1989.

Late 1960s and early 1970s theoretical and political crumbling of Keynesianism

As per the statement of Carlin and Soskice (1990), during the post war displacement period of

Keynesianism, the Keynesian economics would lead to develop developed world. The developed

world would be structured by the influence of economic policies, which had adopted by the

emerging countries. The policy makers were driven by the Keynesian thinking and followed the

free market policies instead of formulating the mixed economy since unnecessary government

intervention was required in this context. As a result, the world economy had been experiencing

a long boom by the prior period of 1970 (Glyn et al., 1986). In addition, in the year 1965, the

advanced capitalists countries had experienced persistent inflation rate.

Conclusion

Based on the analysis, it can be mentioned that the Phillips curve was derived based on stable

and inverse relationship of the inflation rate and the unemployment rate. This theory claims the

economic growth rate, which would in turn create more jobs, which would in turn reduce the

unemployment rate. However, as per the concept of expectation augmented Phillips curve, the

Phillips curve would not be sustained in the long run. Therefore, it can be inferred that the

Phillips curve would be broken down. On the other hand, Friedman also made a counter

argument and stated that in the long run, the Phillips curve would be shifted in the right ward.

Apart from this, based on the analysis it can be observed that during the stagflationary period of

1970, the trade-off among the unemployment rate and the inflation rate would be broken down

and hence, both the unemployment rate and the inflation rate had increased in this period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Reference

Carlin, W. and Soskice, D., 1990. Macroeconomics and the wage bargain.

Coibion, O. and Gorodnichenko, Y., 2015. Is the Phillips curve alive and well after all? Inflation

expectations and the missing disinflation. American Economic Journal: Macroeconomics, 7(1),

pp.197-232.

Coibion, O., 2010. Testing the sticky information Phillips curve. The Review of Economics and

Statistics, 92(1), pp.87-101.

Colander, D., 1995. ‘The stories we tell: A reconsideration of AS/AD analysis’, Journal of

Economic Perspectives, 9(3): 169-188.

Correa, A.D.S. and Minella, A., 2010. Nonlinear mechanisms of the exchange rate pass-through:

A Phillips curve model with threshold for Brazil. Revista Brasileira de Economia, 64(3), pp.231-

243.

Daly, M.C. and Hobijn, B., 2014. Downward nominal wage rigidities bend the Phillips curve.

Journal of Money, Credit and Banking, 46(2), pp.51-93.

D'Arista, J., 2009. The evolving international monetary system. Cambridge Journal of

Economics, 33(4), pp.633-652.

Dua, P. and Gaur, U., 2010. Determination of inflation in an open economy Phillips curve

framework: The case of developed and developing Asian countries. Macroeconomics and

Finance in Emerging Market Economies, 3(1), pp.33-51.

Forder, J., 2010. ‘The historical place of the ‘Friedman-Phelps’ expectations critique’. European

Journal of Economic Thought. 17(2): 493-511.

Galí, J., 2011. The return of the wage Phillips curve. Journal of the European Economic

Association, 9(3), pp.436-461.

Reference

Carlin, W. and Soskice, D., 1990. Macroeconomics and the wage bargain.

Coibion, O. and Gorodnichenko, Y., 2015. Is the Phillips curve alive and well after all? Inflation

expectations and the missing disinflation. American Economic Journal: Macroeconomics, 7(1),

pp.197-232.

Coibion, O., 2010. Testing the sticky information Phillips curve. The Review of Economics and

Statistics, 92(1), pp.87-101.

Colander, D., 1995. ‘The stories we tell: A reconsideration of AS/AD analysis’, Journal of

Economic Perspectives, 9(3): 169-188.

Correa, A.D.S. and Minella, A., 2010. Nonlinear mechanisms of the exchange rate pass-through:

A Phillips curve model with threshold for Brazil. Revista Brasileira de Economia, 64(3), pp.231-

243.

Daly, M.C. and Hobijn, B., 2014. Downward nominal wage rigidities bend the Phillips curve.

Journal of Money, Credit and Banking, 46(2), pp.51-93.

D'Arista, J., 2009. The evolving international monetary system. Cambridge Journal of

Economics, 33(4), pp.633-652.

Dua, P. and Gaur, U., 2010. Determination of inflation in an open economy Phillips curve

framework: The case of developed and developing Asian countries. Macroeconomics and

Finance in Emerging Market Economies, 3(1), pp.33-51.

Forder, J., 2010. ‘The historical place of the ‘Friedman-Phelps’ expectations critique’. European

Journal of Economic Thought. 17(2): 493-511.

Galí, J., 2011. The return of the wage Phillips curve. Journal of the European Economic

Association, 9(3), pp.436-461.

12

Gallegati, M., Gallegati, M., Ramsey, J.B. and Semmler, W., 2011. The US wage Phillips curve

across frequencies and over time. Oxford Bulletin of Economics and Statistics, 73(4), pp.489-

508.

Glyn, A., 2006. Chapters 1 & 2 in: Capitalism Unleashed. Finance, Globalization and Welfare,

Oxford: Oxford University Press.

Glyn, A., Hughes, A., Lipietz, A. and Singh, A., 1986. The Rise and Fall Of the Golden Age: an

historical analysis of post-war capitalism in the developed market economies. Marglin & Schor,

eds., The Golden Age of Capitalism.

Gordon, R.J., 2011. The history of the Phillips curve: Consensus and bifurcation. Economica,

78(3), pp.10-50.

Granger, C.W. and Jeon, Y., 2011. The evolution of the Phillips curve: a modern time series

viewpoint. Economica, 78(309), pp.51-66.

Helleiner, E., 1994. Chapters 4 & 5 in: States and the Reemergence of Global Finance. From

Bretton Woods to the 1990s, New York: Cornell Univeristy.

Imbs, J., Jondeau, E. and Pelgrin, F., 2011. Sectoral Phillips curves and the aggregate Phillips

curve. Journal of Monetary Economics, 58(4), pp.328-344.

Jean-Baptiste, F., 2012. Forecasting with the new Keynesian Phillips curve: Evidence from

survey data. Economics Letters, 117(3), pp.811-813.

Kuttner, K. and Robinson, T., 2010. Understanding the flattening Phillips curve. The North

American Journal of Economics and Finance, 21(2), pp.110-125.

Mavroeidis, S., Plagborg-Møller, M. and Stock, J.H., 2014. Empirical evidence on inflation

expectations in the New Keynesian Phillips Curve. Journal of Economic Literature, 52(1),

pp.124-88.

Mazumder, S., 2010. The new Keynesian Phillips curve and the cyclicality of marginal cost.

Journal of Macroeconomics, 32(3), pp.747-765.

Gallegati, M., Gallegati, M., Ramsey, J.B. and Semmler, W., 2011. The US wage Phillips curve

across frequencies and over time. Oxford Bulletin of Economics and Statistics, 73(4), pp.489-

508.

Glyn, A., 2006. Chapters 1 & 2 in: Capitalism Unleashed. Finance, Globalization and Welfare,

Oxford: Oxford University Press.

Glyn, A., Hughes, A., Lipietz, A. and Singh, A., 1986. The Rise and Fall Of the Golden Age: an

historical analysis of post-war capitalism in the developed market economies. Marglin & Schor,

eds., The Golden Age of Capitalism.

Gordon, R.J., 2011. The history of the Phillips curve: Consensus and bifurcation. Economica,

78(3), pp.10-50.

Granger, C.W. and Jeon, Y., 2011. The evolution of the Phillips curve: a modern time series

viewpoint. Economica, 78(309), pp.51-66.

Helleiner, E., 1994. Chapters 4 & 5 in: States and the Reemergence of Global Finance. From

Bretton Woods to the 1990s, New York: Cornell Univeristy.

Imbs, J., Jondeau, E. and Pelgrin, F., 2011. Sectoral Phillips curves and the aggregate Phillips

curve. Journal of Monetary Economics, 58(4), pp.328-344.

Jean-Baptiste, F., 2012. Forecasting with the new Keynesian Phillips curve: Evidence from

survey data. Economics Letters, 117(3), pp.811-813.

Kuttner, K. and Robinson, T., 2010. Understanding the flattening Phillips curve. The North

American Journal of Economics and Finance, 21(2), pp.110-125.

Mavroeidis, S., Plagborg-Møller, M. and Stock, J.H., 2014. Empirical evidence on inflation

expectations in the New Keynesian Phillips Curve. Journal of Economic Literature, 52(1),

pp.124-88.

Mazumder, S., 2010. The new Keynesian Phillips curve and the cyclicality of marginal cost.

Journal of Macroeconomics, 32(3), pp.747-765.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.