Management Accounting: Income Statement, Activity-Based Costing, Variances, and Budgeting

VerifiedAdded on 2022/11/01

|10

|1883

|160

AI Summary

This report covers various aspects of management accounting, including income statement preparation, activity-based costing, variance calculation, and budgeting. It includes a case study of Barbeque and Balloons, and discusses issues related to profit distribution and subjective performance evaluation.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

Table of Contents

Introduction......................................................................................................................................2

Question 1........................................................................................................................................2

Question 2........................................................................................................................................2

a)...................................................................................................................................................2

b)..................................................................................................................................................3

c)...................................................................................................................................................3

Question 3........................................................................................................................................3

a)...................................................................................................................................................3

b)..................................................................................................................................................4

Question 4........................................................................................................................................4

a)...................................................................................................................................................4

b)..................................................................................................................................................5

c)...................................................................................................................................................5

Question 5........................................................................................................................................5

a)...................................................................................................................................................5

b)..................................................................................................................................................6

c)...................................................................................................................................................6

Question 6........................................................................................................................................7

a)...................................................................................................................................................7

b)..................................................................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

Question 1........................................................................................................................................2

Question 2........................................................................................................................................2

a)...................................................................................................................................................2

b)..................................................................................................................................................3

c)...................................................................................................................................................3

Question 3........................................................................................................................................3

a)...................................................................................................................................................3

b)..................................................................................................................................................4

Question 4........................................................................................................................................4

a)...................................................................................................................................................4

b)..................................................................................................................................................5

c)...................................................................................................................................................5

Question 5........................................................................................................................................5

a)...................................................................................................................................................5

b)..................................................................................................................................................6

c)...................................................................................................................................................6

Question 6........................................................................................................................................7

a)...................................................................................................................................................7

b)..................................................................................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

2

Introduction

The business is required to be managed in an effective manner and for that, there is the need to

perform various tasks by which the profits can be maximized. There are various policies and

strategies which are used in this respect and for that evaluation are to be made. In this report

several such aspects will be undertaken with reference to the BBQ and balloons. In this the

income statement will be prepared and after that activity-based techniques will be taken into

consideration. There will also be the calculation of the variances by which the evaluation will be

made in an effective manner. The performance of the business will be evaluated with the help of

this and it will be helpful in managing the business in the coming period.

Question 1

Income Statement of Barbeque and Balloons

Particulars Amount

Revenue from Barbecue $ 4,000.00

Revenue from Balloon $ 1,000.00

Total Revenue $ 5,000.00

Cost of Barbecue $ 500.00

Cost of Balloon $ 30.00

Total Cost of Goods sold $ 530.00

Gross Profit $ 4,470.00

Expenses:

Salary $ 1,600.00

Production expenses $ 250.00

Sales and administration

expenses

$ 300.00

Total Expenses $ 2,150.00

Net Profit $ 2,320.00

Question 2

a)

Operating

BBQ

Inflating

Balloons

Cashier Greetin

g

Custom

ers

Total

Introduction

The business is required to be managed in an effective manner and for that, there is the need to

perform various tasks by which the profits can be maximized. There are various policies and

strategies which are used in this respect and for that evaluation are to be made. In this report

several such aspects will be undertaken with reference to the BBQ and balloons. In this the

income statement will be prepared and after that activity-based techniques will be taken into

consideration. There will also be the calculation of the variances by which the evaluation will be

made in an effective manner. The performance of the business will be evaluated with the help of

this and it will be helpful in managing the business in the coming period.

Question 1

Income Statement of Barbeque and Balloons

Particulars Amount

Revenue from Barbecue $ 4,000.00

Revenue from Balloon $ 1,000.00

Total Revenue $ 5,000.00

Cost of Barbecue $ 500.00

Cost of Balloon $ 30.00

Total Cost of Goods sold $ 530.00

Gross Profit $ 4,470.00

Expenses:

Salary $ 1,600.00

Production expenses $ 250.00

Sales and administration

expenses

$ 300.00

Total Expenses $ 2,150.00

Net Profit $ 2,320.00

Question 2

a)

Operating

BBQ

Inflating

Balloons

Cashier Greetin

g

Custom

ers

Total

3

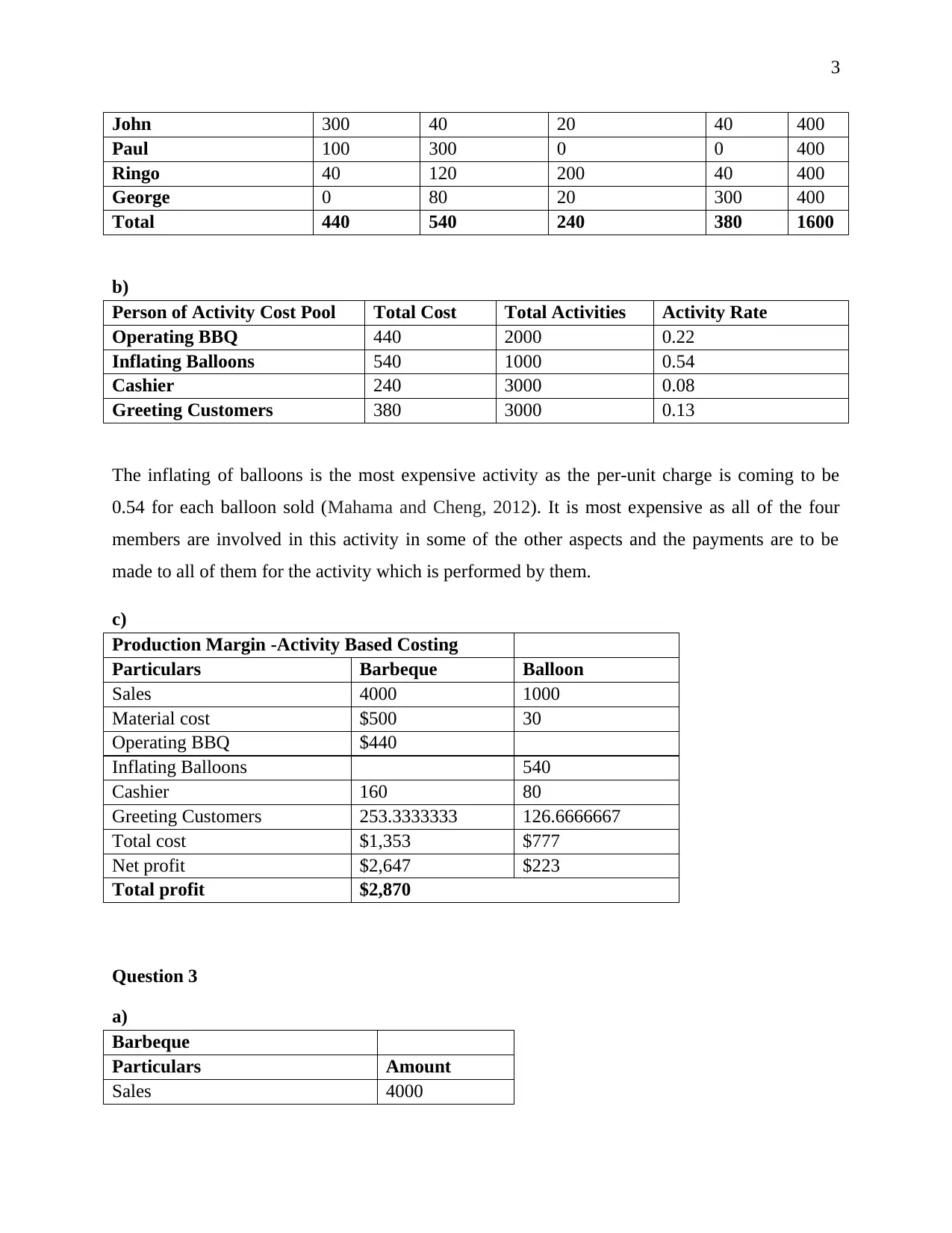

John 300 40 20 40 400

Paul 100 300 0 0 400

Ringo 40 120 200 40 400

George 0 80 20 300 400

Total 440 540 240 380 1600

b)

Person of Activity Cost Pool Total Cost Total Activities Activity Rate

Operating BBQ 440 2000 0.22

Inflating Balloons 540 1000 0.54

Cashier 240 3000 0.08

Greeting Customers 380 3000 0.13

The inflating of balloons is the most expensive activity as the per-unit charge is coming to be

0.54 for each balloon sold (Mahama and Cheng, 2012). It is most expensive as all of the four

members are involved in this activity in some of the other aspects and the payments are to be

made to all of them for the activity which is performed by them.

c)

Production Margin -Activity Based Costing

Particulars Barbeque Balloon

Sales 4000 1000

Material cost $500 30

Operating BBQ $440

Inflating Balloons 540

Cashier 160 80

Greeting Customers 253.3333333 126.6666667

Total cost $1,353 $777

Net profit $2,647 $223

Total profit $2,870

Question 3

a)

Barbeque

Particulars Amount

Sales 4000

John 300 40 20 40 400

Paul 100 300 0 0 400

Ringo 40 120 200 40 400

George 0 80 20 300 400

Total 440 540 240 380 1600

b)

Person of Activity Cost Pool Total Cost Total Activities Activity Rate

Operating BBQ 440 2000 0.22

Inflating Balloons 540 1000 0.54

Cashier 240 3000 0.08

Greeting Customers 380 3000 0.13

The inflating of balloons is the most expensive activity as the per-unit charge is coming to be

0.54 for each balloon sold (Mahama and Cheng, 2012). It is most expensive as all of the four

members are involved in this activity in some of the other aspects and the payments are to be

made to all of them for the activity which is performed by them.

c)

Production Margin -Activity Based Costing

Particulars Barbeque Balloon

Sales 4000 1000

Material cost $500 30

Operating BBQ $440

Inflating Balloons 540

Cashier 160 80

Greeting Customers 253.3333333 126.6666667

Total cost $1,353 $777

Net profit $2,647 $223

Total profit $2,870

Question 3

a)

Barbeque

Particulars Amount

Sales 4000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

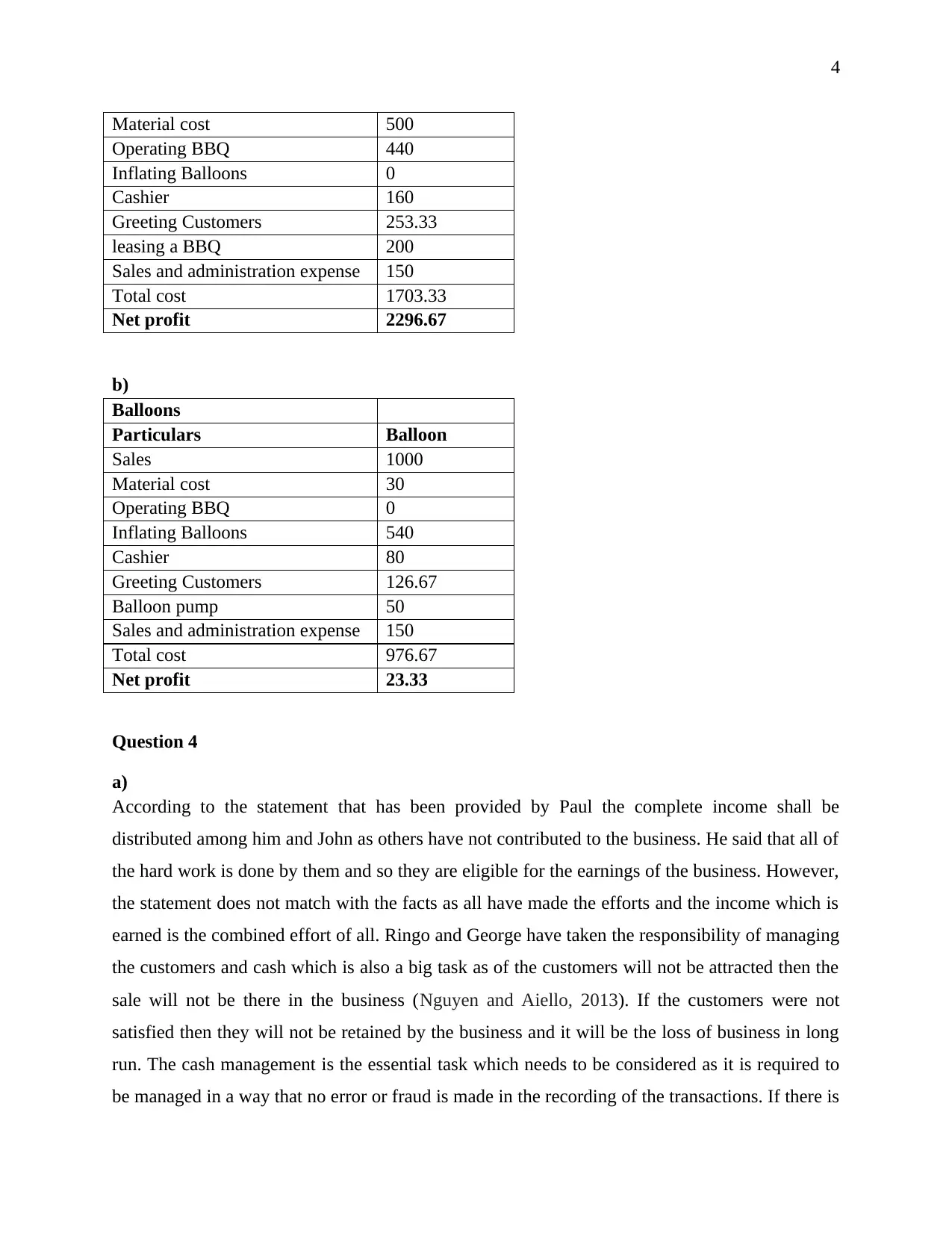

Material cost 500

Operating BBQ 440

Inflating Balloons 0

Cashier 160

Greeting Customers 253.33

leasing a BBQ 200

Sales and administration expense 150

Total cost 1703.33

Net profit 2296.67

b)

Balloons

Particulars Balloon

Sales 1000

Material cost 30

Operating BBQ 0

Inflating Balloons 540

Cashier 80

Greeting Customers 126.67

Balloon pump 50

Sales and administration expense 150

Total cost 976.67

Net profit 23.33

Question 4

a)

According to the statement that has been provided by Paul the complete income shall be

distributed among him and John as others have not contributed to the business. He said that all of

the hard work is done by them and so they are eligible for the earnings of the business. However,

the statement does not match with the facts as all have made the efforts and the income which is

earned is the combined effort of all. Ringo and George have taken the responsibility of managing

the customers and cash which is also a big task as of the customers will not be attracted then the

sale will not be there in the business (Nguyen and Aiello, 2013). If the customers were not

satisfied then they will not be retained by the business and it will be the loss of business in long

run. The cash management is the essential task which needs to be considered as it is required to

be managed in a way that no error or fraud is made in the recording of the transactions. If there is

Material cost 500

Operating BBQ 440

Inflating Balloons 0

Cashier 160

Greeting Customers 253.33

leasing a BBQ 200

Sales and administration expense 150

Total cost 1703.33

Net profit 2296.67

b)

Balloons

Particulars Balloon

Sales 1000

Material cost 30

Operating BBQ 0

Inflating Balloons 540

Cashier 80

Greeting Customers 126.67

Balloon pump 50

Sales and administration expense 150

Total cost 976.67

Net profit 23.33

Question 4

a)

According to the statement that has been provided by Paul the complete income shall be

distributed among him and John as others have not contributed to the business. He said that all of

the hard work is done by them and so they are eligible for the earnings of the business. However,

the statement does not match with the facts as all have made the efforts and the income which is

earned is the combined effort of all. Ringo and George have taken the responsibility of managing

the customers and cash which is also a big task as of the customers will not be attracted then the

sale will not be there in the business (Nguyen and Aiello, 2013). If the customers were not

satisfied then they will not be retained by the business and it will be the loss of business in long

run. The cash management is the essential task which needs to be considered as it is required to

be managed in a way that no error or fraud is made in the recording of the transactions. If there is

5

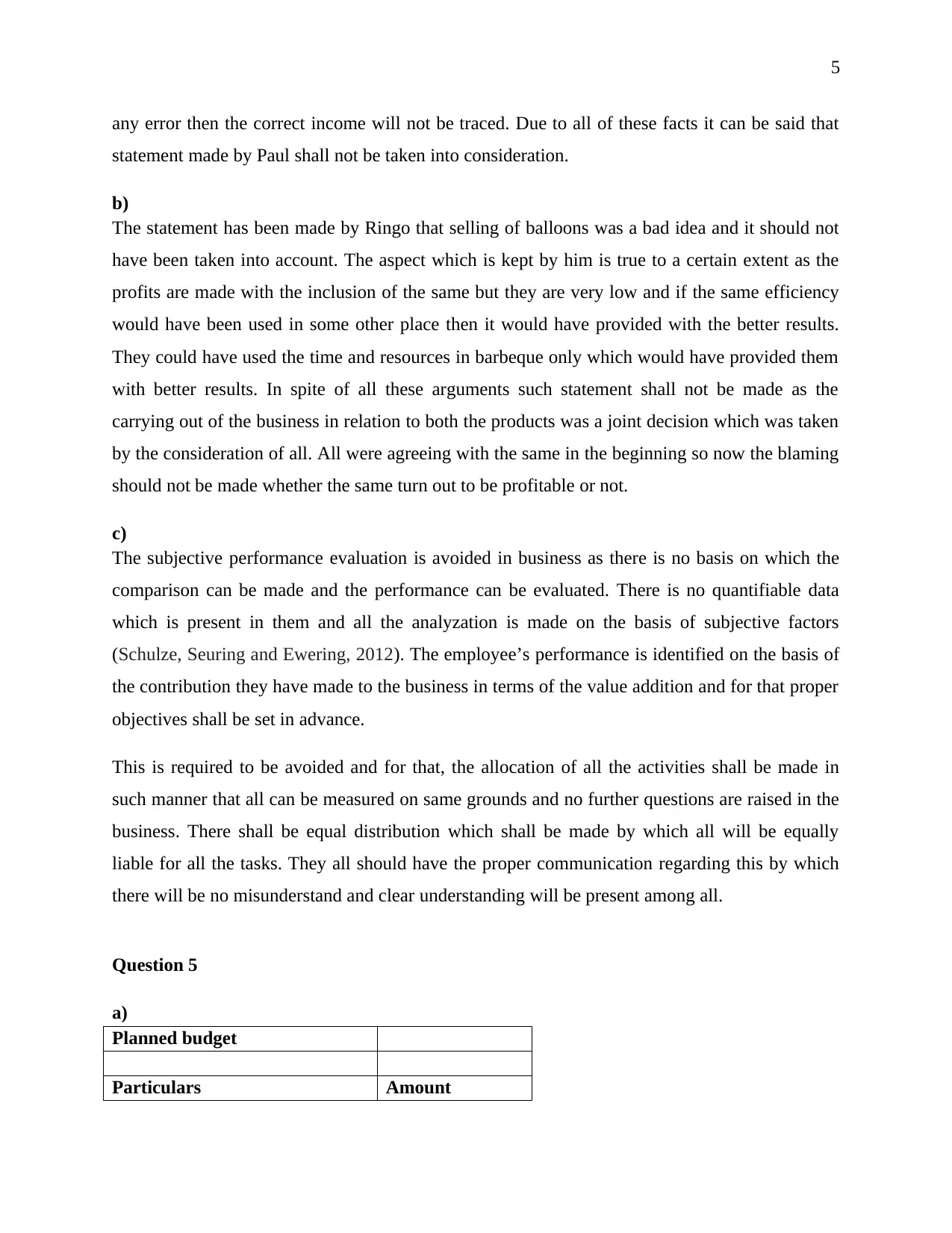

any error then the correct income will not be traced. Due to all of these facts it can be said that

statement made by Paul shall not be taken into consideration.

b)

The statement has been made by Ringo that selling of balloons was a bad idea and it should not

have been taken into account. The aspect which is kept by him is true to a certain extent as the

profits are made with the inclusion of the same but they are very low and if the same efficiency

would have been used in some other place then it would have provided with the better results.

They could have used the time and resources in barbeque only which would have provided them

with better results. In spite of all these arguments such statement shall not be made as the

carrying out of the business in relation to both the products was a joint decision which was taken

by the consideration of all. All were agreeing with the same in the beginning so now the blaming

should not be made whether the same turn out to be profitable or not.

c)

The subjective performance evaluation is avoided in business as there is no basis on which the

comparison can be made and the performance can be evaluated. There is no quantifiable data

which is present in them and all the analyzation is made on the basis of subjective factors

(Schulze, Seuring and Ewering, 2012). The employee’s performance is identified on the basis of

the contribution they have made to the business in terms of the value addition and for that proper

objectives shall be set in advance.

This is required to be avoided and for that, the allocation of all the activities shall be made in

such manner that all can be measured on same grounds and no further questions are raised in the

business. There shall be equal distribution which shall be made by which all will be equally

liable for all the tasks. They all should have the proper communication regarding this by which

there will be no misunderstand and clear understanding will be present among all.

Question 5

a)

Planned budget

Particulars Amount

any error then the correct income will not be traced. Due to all of these facts it can be said that

statement made by Paul shall not be taken into consideration.

b)

The statement has been made by Ringo that selling of balloons was a bad idea and it should not

have been taken into account. The aspect which is kept by him is true to a certain extent as the

profits are made with the inclusion of the same but they are very low and if the same efficiency

would have been used in some other place then it would have provided with the better results.

They could have used the time and resources in barbeque only which would have provided them

with better results. In spite of all these arguments such statement shall not be made as the

carrying out of the business in relation to both the products was a joint decision which was taken

by the consideration of all. All were agreeing with the same in the beginning so now the blaming

should not be made whether the same turn out to be profitable or not.

c)

The subjective performance evaluation is avoided in business as there is no basis on which the

comparison can be made and the performance can be evaluated. There is no quantifiable data

which is present in them and all the analyzation is made on the basis of subjective factors

(Schulze, Seuring and Ewering, 2012). The employee’s performance is identified on the basis of

the contribution they have made to the business in terms of the value addition and for that proper

objectives shall be set in advance.

This is required to be avoided and for that, the allocation of all the activities shall be made in

such manner that all can be measured on same grounds and no further questions are raised in the

business. There shall be equal distribution which shall be made by which all will be equally

liable for all the tasks. They all should have the proper communication regarding this by which

there will be no misunderstand and clear understanding will be present among all.

Question 5

a)

Planned budget

Particulars Amount

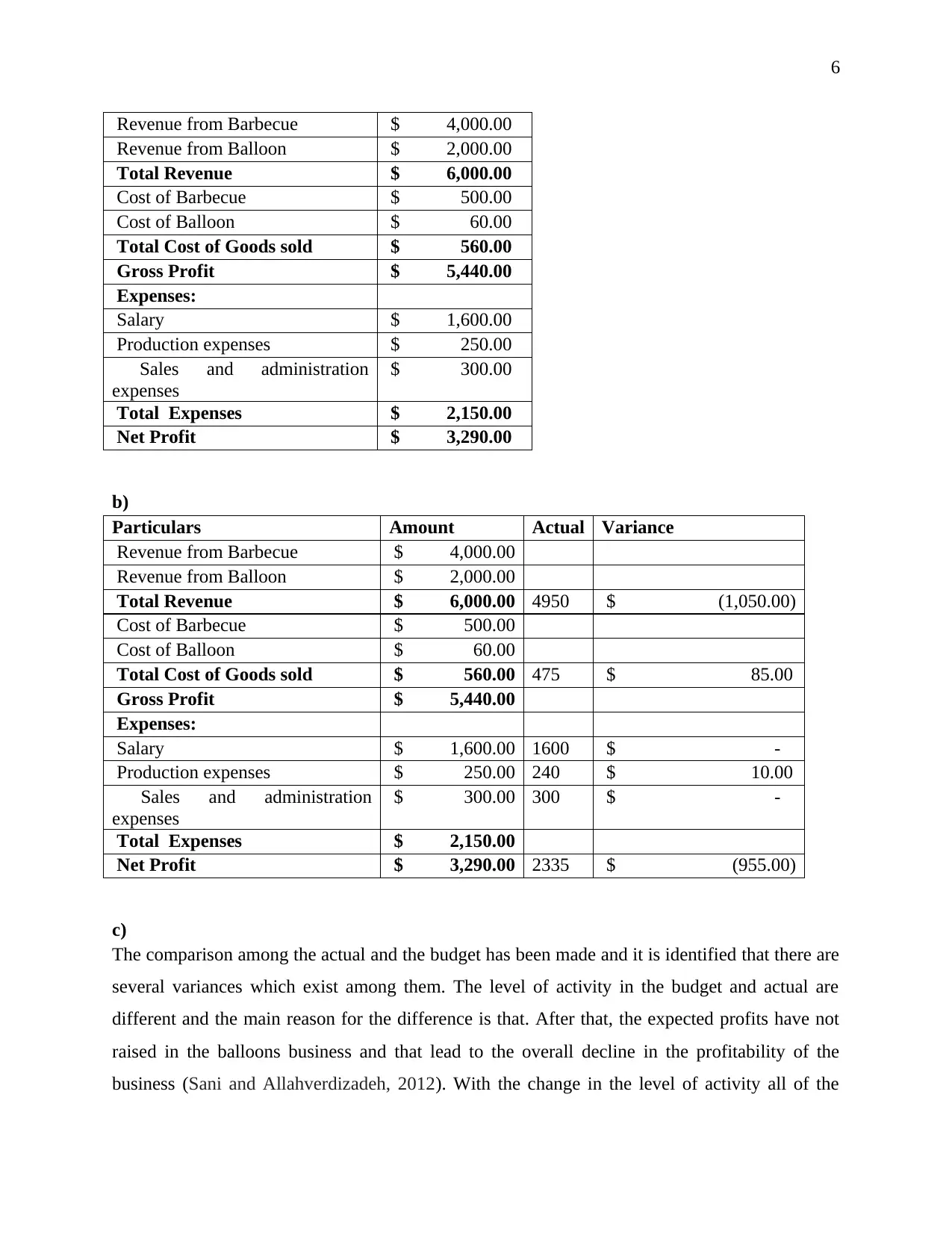

6

Revenue from Barbecue $ 4,000.00

Revenue from Balloon $ 2,000.00

Total Revenue $ 6,000.00

Cost of Barbecue $ 500.00

Cost of Balloon $ 60.00

Total Cost of Goods sold $ 560.00

Gross Profit $ 5,440.00

Expenses:

Salary $ 1,600.00

Production expenses $ 250.00

Sales and administration

expenses

$ 300.00

Total Expenses $ 2,150.00

Net Profit $ 3,290.00

b)

Particulars Amount Actual Variance

Revenue from Barbecue $ 4,000.00

Revenue from Balloon $ 2,000.00

Total Revenue $ 6,000.00 4950 $ (1,050.00)

Cost of Barbecue $ 500.00

Cost of Balloon $ 60.00

Total Cost of Goods sold $ 560.00 475 $ 85.00

Gross Profit $ 5,440.00

Expenses:

Salary $ 1,600.00 1600 $ -

Production expenses $ 250.00 240 $ 10.00

Sales and administration

expenses

$ 300.00 300 $ -

Total Expenses $ 2,150.00

Net Profit $ 3,290.00 2335 $ (955.00)

c)

The comparison among the actual and the budget has been made and it is identified that there are

several variances which exist among them. The level of activity in the budget and actual are

different and the main reason for the difference is that. After that, the expected profits have not

raised in the balloons business and that lead to the overall decline in the profitability of the

business (Sani and Allahverdizadeh, 2012). With the change in the level of activity all of the

Revenue from Barbecue $ 4,000.00

Revenue from Balloon $ 2,000.00

Total Revenue $ 6,000.00

Cost of Barbecue $ 500.00

Cost of Balloon $ 60.00

Total Cost of Goods sold $ 560.00

Gross Profit $ 5,440.00

Expenses:

Salary $ 1,600.00

Production expenses $ 250.00

Sales and administration

expenses

$ 300.00

Total Expenses $ 2,150.00

Net Profit $ 3,290.00

b)

Particulars Amount Actual Variance

Revenue from Barbecue $ 4,000.00

Revenue from Balloon $ 2,000.00

Total Revenue $ 6,000.00 4950 $ (1,050.00)

Cost of Barbecue $ 500.00

Cost of Balloon $ 60.00

Total Cost of Goods sold $ 560.00 475 $ 85.00

Gross Profit $ 5,440.00

Expenses:

Salary $ 1,600.00 1600 $ -

Production expenses $ 250.00 240 $ 10.00

Sales and administration

expenses

$ 300.00 300 $ -

Total Expenses $ 2,150.00

Net Profit $ 3,290.00 2335 $ (955.00)

c)

The comparison among the actual and the budget has been made and it is identified that there are

several variances which exist among them. The level of activity in the budget and actual are

different and the main reason for the difference is that. After that, the expected profits have not

raised in the balloons business and that lead to the overall decline in the profitability of the

business (Sani and Allahverdizadeh, 2012). With the change in the level of activity all of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

costs and income which are there in relation to them also gets affected. Due to those deviations

the variances are identified and the business is to bear the impact of the same. The efforts which

were made for the balloon business are much more than that of the planned ones. There is lot of

time which is consumed in the same but the results for that have not been achieved to that level

(Beynon, Jones and Pickernell, 2016). In order to eliminate the deviations which are identified

there is the need to consider all of the reasons which are involved for the variances and then the

changes in the system shall be incorporated accordingly by which the further position and

performance of the business will be improved.

Question 6

a)

Calculation of variance for barbeque

Particulars Amounts

Actual quantity 2075

Standard quantity 2000

Actual price 450

Standard price 0.25 per unit

Standard price 518.75

Material price variance 68.75 Favorable

Quantity variance -75 Adverse

Total material variance -6.25

b)

Calculation of variance for balloons

Particulars Amounts

Actual quantity 1050

Standard quantity 1000

Actual price 25

Standard price 0.03

Standard price 31.5

Material price variance 6.5 Favorable

Quantity variance -50 Adverse

Total material variance -43.5

costs and income which are there in relation to them also gets affected. Due to those deviations

the variances are identified and the business is to bear the impact of the same. The efforts which

were made for the balloon business are much more than that of the planned ones. There is lot of

time which is consumed in the same but the results for that have not been achieved to that level

(Beynon, Jones and Pickernell, 2016). In order to eliminate the deviations which are identified

there is the need to consider all of the reasons which are involved for the variances and then the

changes in the system shall be incorporated accordingly by which the further position and

performance of the business will be improved.

Question 6

a)

Calculation of variance for barbeque

Particulars Amounts

Actual quantity 2075

Standard quantity 2000

Actual price 450

Standard price 0.25 per unit

Standard price 518.75

Material price variance 68.75 Favorable

Quantity variance -75 Adverse

Total material variance -6.25

b)

Calculation of variance for balloons

Particulars Amounts

Actual quantity 1050

Standard quantity 1000

Actual price 25

Standard price 0.03

Standard price 31.5

Material price variance 6.5 Favorable

Quantity variance -50 Adverse

Total material variance -43.5

8

Conclusion

The report has been made on the new business which has been started and the proper analyzation

of all the aspects in this respect has been made. There is a calculation of the profits which will be

made with the business. The activities which will be involved have been determined and with the

help of appropriate cost drivers there is the calculation of the rate of all the activities. Various

issues have been raised by the partners in relation to the profit distribution and they have been

considered in an appropriate manner. The profitability of both the products has been calculated

and also the comparison has been made between the planned and budgeted amounts. The

variances have been determined for better evaluation.

Conclusion

The report has been made on the new business which has been started and the proper analyzation

of all the aspects in this respect has been made. There is a calculation of the profits which will be

made with the business. The activities which will be involved have been determined and with the

help of appropriate cost drivers there is the calculation of the rate of all the activities. Various

issues have been raised by the partners in relation to the profit distribution and they have been

considered in an appropriate manner. The profitability of both the products has been calculated

and also the comparison has been made between the planned and budgeted amounts. The

variances have been determined for better evaluation.

9

References

Beynon, M.J., Jones, P. and Pickernell, D. (2016) Country-based comparison analysis using

fsQCA investigating entrepreneurial attitudes and activity. Journal of Business Research, 69(4),

pp.1271-1276.

Mahama, H. and Cheng, M.M. (2012) The effect of managers' enabling perceptions on costing

system use, psychological empowerment, and task performance. Behavioral Research in

Accounting, 25(1), pp.89-114.

Nguyen, T.A. and Aiello, M. (2013) Energy intelligent buildings based on user activity: A

survey. Energy and buildings, 56, pp.244-257.

Sani, A.A. and Allahverdizadeh, M. (2012) Target and Kaizen costing. World academy of

science, engineering and Technology, 6(2), pp.40-46.

Schulze, M., Seuring, S. and Ewering, C. (2012) Applying activity-based costing in a supply

chain environment. International Journal of Production Economics, 135(2), pp.716-725.

References

Beynon, M.J., Jones, P. and Pickernell, D. (2016) Country-based comparison analysis using

fsQCA investigating entrepreneurial attitudes and activity. Journal of Business Research, 69(4),

pp.1271-1276.

Mahama, H. and Cheng, M.M. (2012) The effect of managers' enabling perceptions on costing

system use, psychological empowerment, and task performance. Behavioral Research in

Accounting, 25(1), pp.89-114.

Nguyen, T.A. and Aiello, M. (2013) Energy intelligent buildings based on user activity: A

survey. Energy and buildings, 56, pp.244-257.

Sani, A.A. and Allahverdizadeh, M. (2012) Target and Kaizen costing. World academy of

science, engineering and Technology, 6(2), pp.40-46.

Schulze, M., Seuring, S. and Ewering, C. (2012) Applying activity-based costing in a supply

chain environment. International Journal of Production Economics, 135(2), pp.716-725.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.