Financial Analysis of Caltex Australia

VerifiedAdded on 2023/04/03

|22

|4550

|450

AI Summary

This report evaluates the financial performance of Caltex Australia and provides recommendations to potential investors. It includes ratio analysis, cash management, sensitivity analysis, and dividend payout ratio.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

1

Unit Code: HI5002

Unit Title: Finance for Business

Group Assignment

Unit Code: HI5002

Unit Title: Finance for Business

Group Assignment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2

Abstract

The report has evaluated the financial performance of Caltex Australia for proving

recommendation to a potential investors regarding investment within the company. The financial

performance has been analyzed with the use of ratio analysis, cash management, and sensitivity

analysis and dividend payout ratio. It is recommended to an investor to hold back the share and

not to invest within the company due to its weak financial position as depicted with ratio

analysis.

Abstract

The report has evaluated the financial performance of Caltex Australia for proving

recommendation to a potential investors regarding investment within the company. The financial

performance has been analyzed with the use of ratio analysis, cash management, and sensitivity

analysis and dividend payout ratio. It is recommended to an investor to hold back the share and

not to invest within the company due to its weak financial position as depicted with ratio

analysis.

3

Contents

Abstract............................................................................................................................................2

Section I: Introduction.....................................................................................................................4

Section II: Detailed financial analysis of Caltex Australia..............................................................4

Section 2.1: Brief description of Caltex Australia...........................................................................4

Section 2.2: Use of ratios to evaluate the performance of Caltex Australia....................................4

Profitability Ratios of Caltex Australia........................................................................................4

Operating Efficiency Ratio..........................................................................................................7

Section 2.3: Use of marketable securities for cash management.....................................................9

Section 2.4: Sensitivity Analysis through using the given data.....................................................10

Section 2.5: Identification and discussion on systematic risk and Unsystematic risk that impacts

the performance of Caltex Australia..............................................................................................16

Systematic Risks associated with Caltex Australia....................................................................16

Unsystematic Risks associated with the Caltex Australia.........................................................16

Section 2.6: Calculation of dividend payout of Caltex Australia for last three years and

interpretation of dividend policy used by Caltex...........................................................................17

Dividend Payout Ratio of Caltex Australia................................................................................17

Section III: Letter of Recommendation to the client.....................................................................19

Section IV: Conclusion..................................................................................................................19

References......................................................................................................................................20

Contents

Abstract............................................................................................................................................2

Section I: Introduction.....................................................................................................................4

Section II: Detailed financial analysis of Caltex Australia..............................................................4

Section 2.1: Brief description of Caltex Australia...........................................................................4

Section 2.2: Use of ratios to evaluate the performance of Caltex Australia....................................4

Profitability Ratios of Caltex Australia........................................................................................4

Operating Efficiency Ratio..........................................................................................................7

Section 2.3: Use of marketable securities for cash management.....................................................9

Section 2.4: Sensitivity Analysis through using the given data.....................................................10

Section 2.5: Identification and discussion on systematic risk and Unsystematic risk that impacts

the performance of Caltex Australia..............................................................................................16

Systematic Risks associated with Caltex Australia....................................................................16

Unsystematic Risks associated with the Caltex Australia.........................................................16

Section 2.6: Calculation of dividend payout of Caltex Australia for last three years and

interpretation of dividend policy used by Caltex...........................................................................17

Dividend Payout Ratio of Caltex Australia................................................................................17

Section III: Letter of Recommendation to the client.....................................................................19

Section IV: Conclusion..................................................................................................................19

References......................................................................................................................................20

4

Section I: Introduction

The purpose of the assignment is to provide recommendation to an institutional investor

aiming to invest within Australian market by undertaking an analysis of the financial

performance of an ASX listed entity. The ASX listed entity selected for the purpose of

conducting financial evaluation is Caltex Australia, a supplier of transport fuel and convenience

retailing products. The financial evaluation of the selected company has been done by analysis of

its performance ratios such as profitability and operational efficiency. This is followed by

analyzing its cash management and performing sensitivity analysis on the data provided. Also, it

has outlined the systematic and unsystematic risks related with the company and also evaluated

its dividend policy. Lastly, it provides recommendation to a potential investor regarding the

financial health of the company to support the investment decisions on the basis of overall

evaluation carried out. It also includes a conclusions section in the last to summarize the overall

findings generated through the report.

Section II: Detailed financial analysis of Caltex Australia

Section 2.1: Brief description of Caltex Australia

Caltex Australia is a publicly listed ASX company involved in supplying of transport fuel

and also operates as a convenient retailer within Australian market. The core segments of the

company includes purchasing, refining,, distributing and marketing of petroleum based products

and also having its own convenience stores in the country. It has established in period of 1990s

and is regarded to be only fuel based company of Australia that is listed on the ASX. It has

presently attained a distinctive position within the oil and gas sector of the country owing to its

leading position in transporting fuels. It is known to supply about one third of transport fuel

needs within Australian market. The leading position has been attained by the company owning

to its agile supply chain that enables it in providing safe and high quality fuel based products to

its diverse customers such as retail, mining, aviation, agriculture, automotive sector and the

government. It has developed its unique position among all the refiner and marketers in Australia

by conducting its operations in an independent manner and all the decisions are taken by the

management and Board members as it is only publicly listed company. It has the presence of

about 3,500 employees working across the country and is known to be one of the biggest

companies developing attractive job opportunities and supporting the development of

employment sector within the country (Caltex Australia: Our Company, 2018).

Section 2.2: Use of ratios to evaluate the performance of Caltex Australia

Profitability Ratios of Caltex Australia

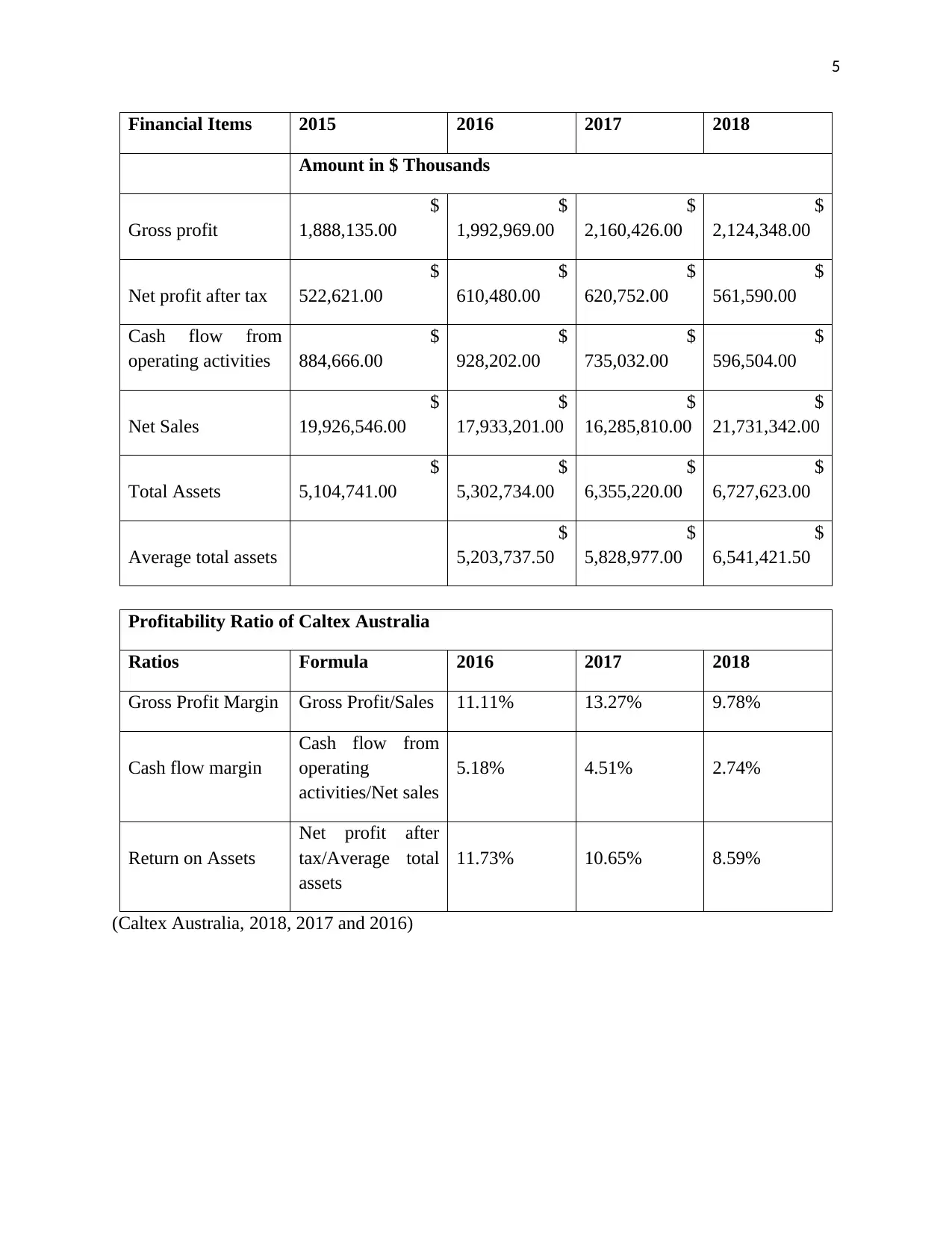

Financial Data of Caltex Australia for calculation of Profitability Ratio

Section I: Introduction

The purpose of the assignment is to provide recommendation to an institutional investor

aiming to invest within Australian market by undertaking an analysis of the financial

performance of an ASX listed entity. The ASX listed entity selected for the purpose of

conducting financial evaluation is Caltex Australia, a supplier of transport fuel and convenience

retailing products. The financial evaluation of the selected company has been done by analysis of

its performance ratios such as profitability and operational efficiency. This is followed by

analyzing its cash management and performing sensitivity analysis on the data provided. Also, it

has outlined the systematic and unsystematic risks related with the company and also evaluated

its dividend policy. Lastly, it provides recommendation to a potential investor regarding the

financial health of the company to support the investment decisions on the basis of overall

evaluation carried out. It also includes a conclusions section in the last to summarize the overall

findings generated through the report.

Section II: Detailed financial analysis of Caltex Australia

Section 2.1: Brief description of Caltex Australia

Caltex Australia is a publicly listed ASX company involved in supplying of transport fuel

and also operates as a convenient retailer within Australian market. The core segments of the

company includes purchasing, refining,, distributing and marketing of petroleum based products

and also having its own convenience stores in the country. It has established in period of 1990s

and is regarded to be only fuel based company of Australia that is listed on the ASX. It has

presently attained a distinctive position within the oil and gas sector of the country owing to its

leading position in transporting fuels. It is known to supply about one third of transport fuel

needs within Australian market. The leading position has been attained by the company owning

to its agile supply chain that enables it in providing safe and high quality fuel based products to

its diverse customers such as retail, mining, aviation, agriculture, automotive sector and the

government. It has developed its unique position among all the refiner and marketers in Australia

by conducting its operations in an independent manner and all the decisions are taken by the

management and Board members as it is only publicly listed company. It has the presence of

about 3,500 employees working across the country and is known to be one of the biggest

companies developing attractive job opportunities and supporting the development of

employment sector within the country (Caltex Australia: Our Company, 2018).

Section 2.2: Use of ratios to evaluate the performance of Caltex Australia

Profitability Ratios of Caltex Australia

Financial Data of Caltex Australia for calculation of Profitability Ratio

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Gross profit

$

1,888,135.00

$

1,992,969.00

$

2,160,426.00

$

2,124,348.00

Net profit after tax

$

522,621.00

$

610,480.00

$

620,752.00

$

561,590.00

Cash flow from

operating activities

$

884,666.00

$

928,202.00

$

735,032.00

$

596,504.00

Net Sales

$

19,926,546.00

$

17,933,201.00

$

16,285,810.00

$

21,731,342.00

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Profitability Ratio of Caltex Australia

Ratios Formula 2016 2017 2018

Gross Profit Margin Gross Profit/Sales 11.11% 13.27% 9.78%

Cash flow margin

Cash flow from

operating

activities/Net sales

5.18% 4.51% 2.74%

Return on Assets

Net profit after

tax/Average total

assets

11.73% 10.65% 8.59%

(Caltex Australia, 2018, 2017 and 2016)

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Gross profit

$

1,888,135.00

$

1,992,969.00

$

2,160,426.00

$

2,124,348.00

Net profit after tax

$

522,621.00

$

610,480.00

$

620,752.00

$

561,590.00

Cash flow from

operating activities

$

884,666.00

$

928,202.00

$

735,032.00

$

596,504.00

Net Sales

$

19,926,546.00

$

17,933,201.00

$

16,285,810.00

$

21,731,342.00

Total Assets

$

5,104,741.00

$

5,302,734.00

$

6,355,220.00

$

6,727,623.00

Average total assets

$

5,203,737.50

$

5,828,977.00

$

6,541,421.50

Profitability Ratio of Caltex Australia

Ratios Formula 2016 2017 2018

Gross Profit Margin Gross Profit/Sales 11.11% 13.27% 9.78%

Cash flow margin

Cash flow from

operating

activities/Net sales

5.18% 4.51% 2.74%

Return on Assets

Net profit after

tax/Average total

assets

11.73% 10.65% 8.59%

(Caltex Australia, 2018, 2017 and 2016)

6

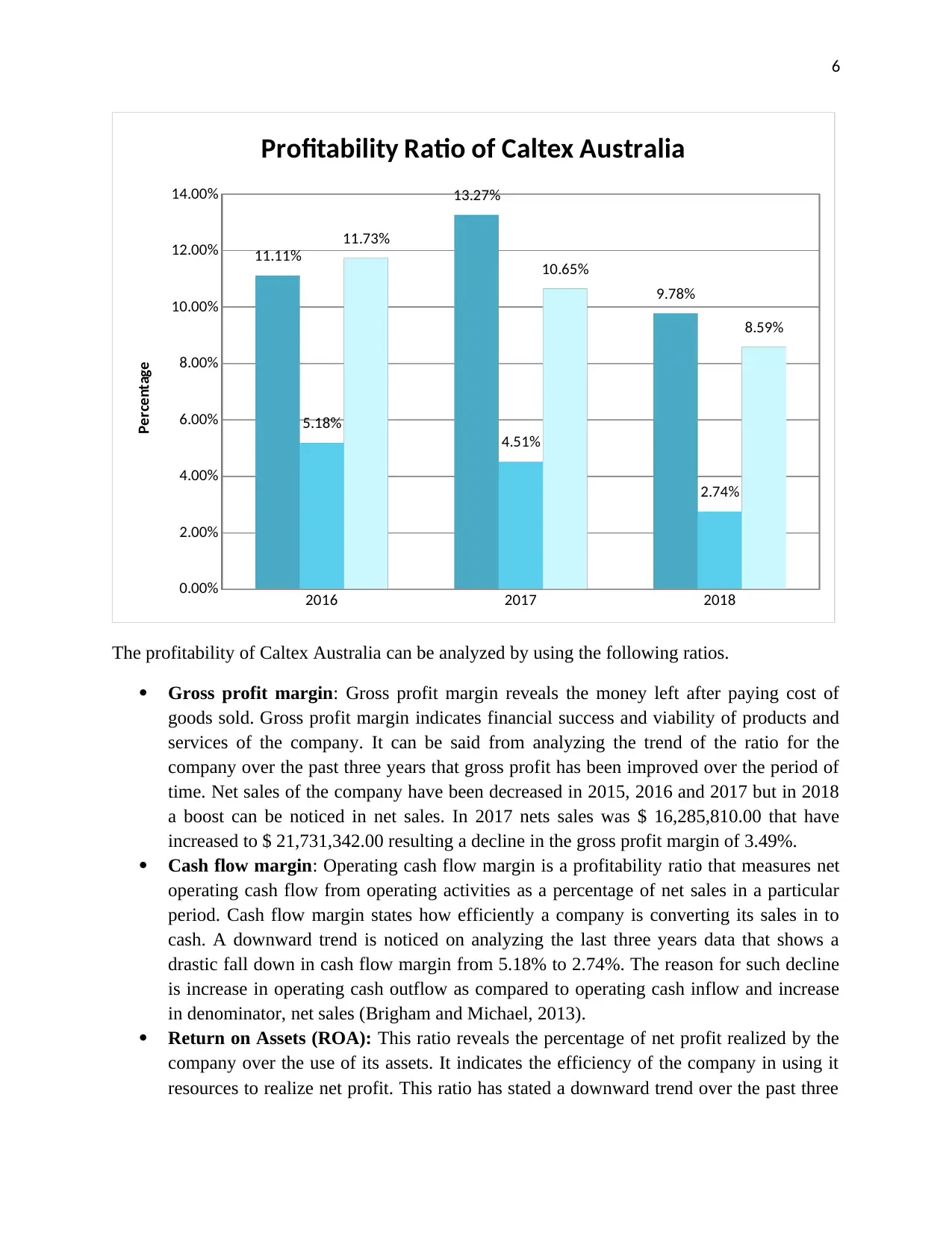

2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

11.11%

13.27%

9.78%

5.18%

4.51%

2.74%

11.73%

10.65%

8.59%

Profitability Ratio of Caltex Australia

Percentage

The profitability of Caltex Australia can be analyzed by using the following ratios.

Gross profit margin: Gross profit margin reveals the money left after paying cost of

goods sold. Gross profit margin indicates financial success and viability of products and

services of the company. It can be said from analyzing the trend of the ratio for the

company over the past three years that gross profit has been improved over the period of

time. Net sales of the company have been decreased in 2015, 2016 and 2017 but in 2018

a boost can be noticed in net sales. In 2017 nets sales was $ 16,285,810.00 that have

increased to $ 21,731,342.00 resulting a decline in the gross profit margin of 3.49%.

Cash flow margin: Operating cash flow margin is a profitability ratio that measures net

operating cash flow from operating activities as a percentage of net sales in a particular

period. Cash flow margin states how efficiently a company is converting its sales in to

cash. A downward trend is noticed on analyzing the last three years data that shows a

drastic fall down in cash flow margin from 5.18% to 2.74%. The reason for such decline

is increase in operating cash outflow as compared to operating cash inflow and increase

in denominator, net sales (Brigham and Michael, 2013).

Return on Assets (ROA): This ratio reveals the percentage of net profit realized by the

company over the use of its assets. It indicates the efficiency of the company in using it

resources to realize net profit. This ratio has stated a downward trend over the past three

2016 2017 2018

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

11.11%

13.27%

9.78%

5.18%

4.51%

2.74%

11.73%

10.65%

8.59%

Profitability Ratio of Caltex Australia

Percentage

The profitability of Caltex Australia can be analyzed by using the following ratios.

Gross profit margin: Gross profit margin reveals the money left after paying cost of

goods sold. Gross profit margin indicates financial success and viability of products and

services of the company. It can be said from analyzing the trend of the ratio for the

company over the past three years that gross profit has been improved over the period of

time. Net sales of the company have been decreased in 2015, 2016 and 2017 but in 2018

a boost can be noticed in net sales. In 2017 nets sales was $ 16,285,810.00 that have

increased to $ 21,731,342.00 resulting a decline in the gross profit margin of 3.49%.

Cash flow margin: Operating cash flow margin is a profitability ratio that measures net

operating cash flow from operating activities as a percentage of net sales in a particular

period. Cash flow margin states how efficiently a company is converting its sales in to

cash. A downward trend is noticed on analyzing the last three years data that shows a

drastic fall down in cash flow margin from 5.18% to 2.74%. The reason for such decline

is increase in operating cash outflow as compared to operating cash inflow and increase

in denominator, net sales (Brigham and Michael, 2013).

Return on Assets (ROA): This ratio reveals the percentage of net profit realized by the

company over the use of its assets. It indicates the efficiency of the company in using it

resources to realize net profit. This ratio has stated a downward trend over the past three

7

years. Return on assets has been declined from 11.73% to 8.59% that shows company has

not been able to use it resources properly. The reason for the same is decreasing profit

and an increase in net sales in the year 2018 (Damodaran, 2011).

Operating Efficiency Ratio

Financial Data of Caltex Australia for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales $ 19,926,546.00

$

17,933,201.00

$

16,285,810.0

0

$

21,731,342.00

Account payables $ 966,806.00

$

1,079,389.00

$

1,735,254.00

$

1,827,169.00

Average account

payable

$

1,023,097.50

$

1,407,321.50

$

1,781,211.50

Account

Receivables $ 681,542.00

$

747,585.00

$

922,420.00

$

1,184,025.00

Average Account

receivables

$

714,563.50

$

835,002.50

$

1,053,222.50

Cost of Goods Sold $ 12,903,682.00

$

11,154,208.00

$

14,125,384.0

0

$

19,606,994.00

Opening Inventory

$

969,885.00

$

1,080,920.00

$

1,694,915.00

Closing Inventory $ 969,885.00

$

1,080,920.00

$

1,694,915.00

$

1,616,125.00

Average Inventory

$

1,025,402.50

$

1,387,917.50

$

1,655,520.00

Net purchases

$

11,265,243.00

$

14,739,379.0

0

$

19,528,204.00

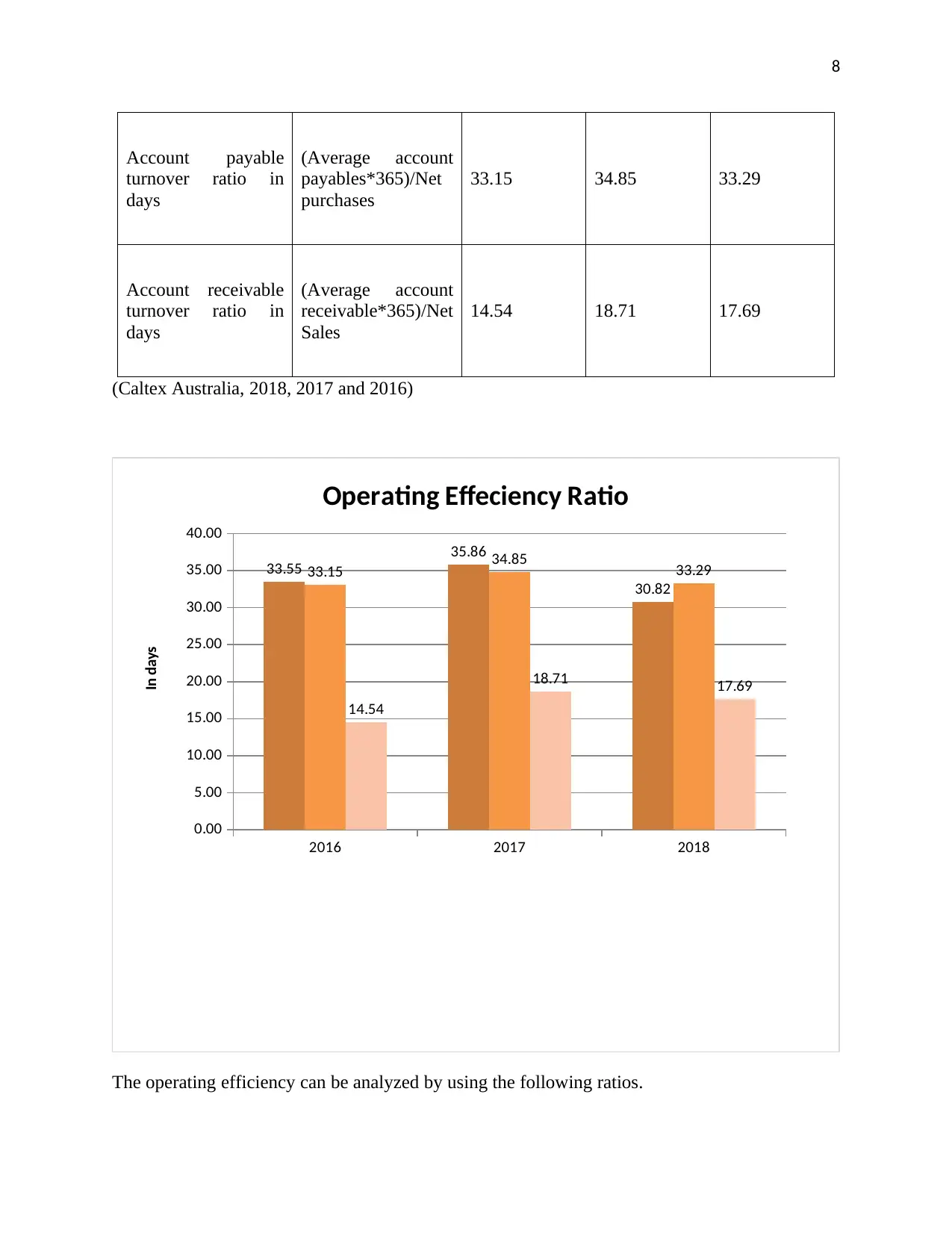

Operating Efficiency Ratios of Caltex Australia

Ratios Formula 2016 2017 2018

Day's sales in

inventory

(Average

inventory*365)/

Cost of goods sold

33.55 35.86 30.82

years. Return on assets has been declined from 11.73% to 8.59% that shows company has

not been able to use it resources properly. The reason for the same is decreasing profit

and an increase in net sales in the year 2018 (Damodaran, 2011).

Operating Efficiency Ratio

Financial Data of Caltex Australia for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales $ 19,926,546.00

$

17,933,201.00

$

16,285,810.0

0

$

21,731,342.00

Account payables $ 966,806.00

$

1,079,389.00

$

1,735,254.00

$

1,827,169.00

Average account

payable

$

1,023,097.50

$

1,407,321.50

$

1,781,211.50

Account

Receivables $ 681,542.00

$

747,585.00

$

922,420.00

$

1,184,025.00

Average Account

receivables

$

714,563.50

$

835,002.50

$

1,053,222.50

Cost of Goods Sold $ 12,903,682.00

$

11,154,208.00

$

14,125,384.0

0

$

19,606,994.00

Opening Inventory

$

969,885.00

$

1,080,920.00

$

1,694,915.00

Closing Inventory $ 969,885.00

$

1,080,920.00

$

1,694,915.00

$

1,616,125.00

Average Inventory

$

1,025,402.50

$

1,387,917.50

$

1,655,520.00

Net purchases

$

11,265,243.00

$

14,739,379.0

0

$

19,528,204.00

Operating Efficiency Ratios of Caltex Australia

Ratios Formula 2016 2017 2018

Day's sales in

inventory

(Average

inventory*365)/

Cost of goods sold

33.55 35.86 30.82

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Account payable

turnover ratio in

days

(Average account

payables*365)/Net

purchases

33.15 34.85 33.29

Account receivable

turnover ratio in

days

(Average account

receivable*365)/Net

Sales

14.54 18.71 17.69

(Caltex Australia, 2018, 2017 and 2016)

2016 2017 2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

33.55

35.86

30.82

33.15 34.85 33.29

14.54

18.71 17.69

Operating Effeciency Ratio

In days

The operating efficiency can be analyzed by using the following ratios.

Account payable

turnover ratio in

days

(Average account

payables*365)/Net

purchases

33.15 34.85 33.29

Account receivable

turnover ratio in

days

(Average account

receivable*365)/Net

Sales

14.54 18.71 17.69

(Caltex Australia, 2018, 2017 and 2016)

2016 2017 2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

33.55

35.86

30.82

33.15 34.85 33.29

14.54

18.71 17.69

Operating Effeciency Ratio

In days

The operating efficiency can be analyzed by using the following ratios.

9

Day’s sales in inventory: This financial ratio depicts the average number of days a

company took to sell its inventory in an accounting year. The less the number of days,

better the ratio is. It shows company is efficiently selling its inventory. The past three

years data of Caltex Australia shows that company has worked upon its efficiency and

made it. Caltex has successfully decreased the number of days to convert its inventory

into sales. In 2016 the ratio was 33.55 days that has decreased to 30.82 days despite

increase in average inventory and net sales.

Account payable turnover ratio in days: This ratio states company’s efficiency in

paying off its creditors for outstanding invoices measured in number of days. Account

payable turnover ratio of Caltex Australia stated a stable trend over the past three years.

Company has taken approx. 33 days to pay off its payables. Company has taken 34.85

days in 2017 to pay off its creditors but in 2018 it covered it up (Davies and Crawford,

2011).

Account receivables turnover ratio in days: This ratio states the number of days a

company took to collect its debtors in an accounting year. The shorter the number of

days, better the ratio is. In the past three years Caltex Australia has not efficiently

collecting its debtors. Caltex Australia has taken 14.54 days in 2016 to collect its debtors

and in 2018 it took 17.69 days to collect the debtors. This is not a good sign for the

company as it is not able to liquidate its credit sales in cash easily (Krantz, 2016).

Section 2.3: Use of marketable securities for cash management

Marketable securities refer to the securities or investments that have been made by the

company to have enough cash and cash equivalents within the year. These investments are used

with the purpose to receive the company within one year. Marketable securities are being listed

under heading the current assets section of the balance sheet and it is valued at current fair value.

On looking at the balance sheet and notes to accounts of Caltex Australia, it has been

found that company has used only cash and cash equivalents and accounts receivables as

marketable securities to have enough cash resources to pay the current liabilities (Caltex

Australia. 2018).

Day’s sales in inventory: This financial ratio depicts the average number of days a

company took to sell its inventory in an accounting year. The less the number of days,

better the ratio is. It shows company is efficiently selling its inventory. The past three

years data of Caltex Australia shows that company has worked upon its efficiency and

made it. Caltex has successfully decreased the number of days to convert its inventory

into sales. In 2016 the ratio was 33.55 days that has decreased to 30.82 days despite

increase in average inventory and net sales.

Account payable turnover ratio in days: This ratio states company’s efficiency in

paying off its creditors for outstanding invoices measured in number of days. Account

payable turnover ratio of Caltex Australia stated a stable trend over the past three years.

Company has taken approx. 33 days to pay off its payables. Company has taken 34.85

days in 2017 to pay off its creditors but in 2018 it covered it up (Davies and Crawford,

2011).

Account receivables turnover ratio in days: This ratio states the number of days a

company took to collect its debtors in an accounting year. The shorter the number of

days, better the ratio is. In the past three years Caltex Australia has not efficiently

collecting its debtors. Caltex Australia has taken 14.54 days in 2016 to collect its debtors

and in 2018 it took 17.69 days to collect the debtors. This is not a good sign for the

company as it is not able to liquidate its credit sales in cash easily (Krantz, 2016).

Section 2.3: Use of marketable securities for cash management

Marketable securities refer to the securities or investments that have been made by the

company to have enough cash and cash equivalents within the year. These investments are used

with the purpose to receive the company within one year. Marketable securities are being listed

under heading the current assets section of the balance sheet and it is valued at current fair value.

On looking at the balance sheet and notes to accounts of Caltex Australia, it has been

found that company has used only cash and cash equivalents and accounts receivables as

marketable securities to have enough cash resources to pay the current liabilities (Caltex

Australia. 2018).

10

Section 2.4: Sensitivity Analysis through using the given data

Life of project consider by the company 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per year 450,000.00$

Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Information given in the question

Section 2.4: Sensitivity Analysis through using the given data

Life of project consider by the company 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per year 450,000.00$

Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Information given in the question

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11

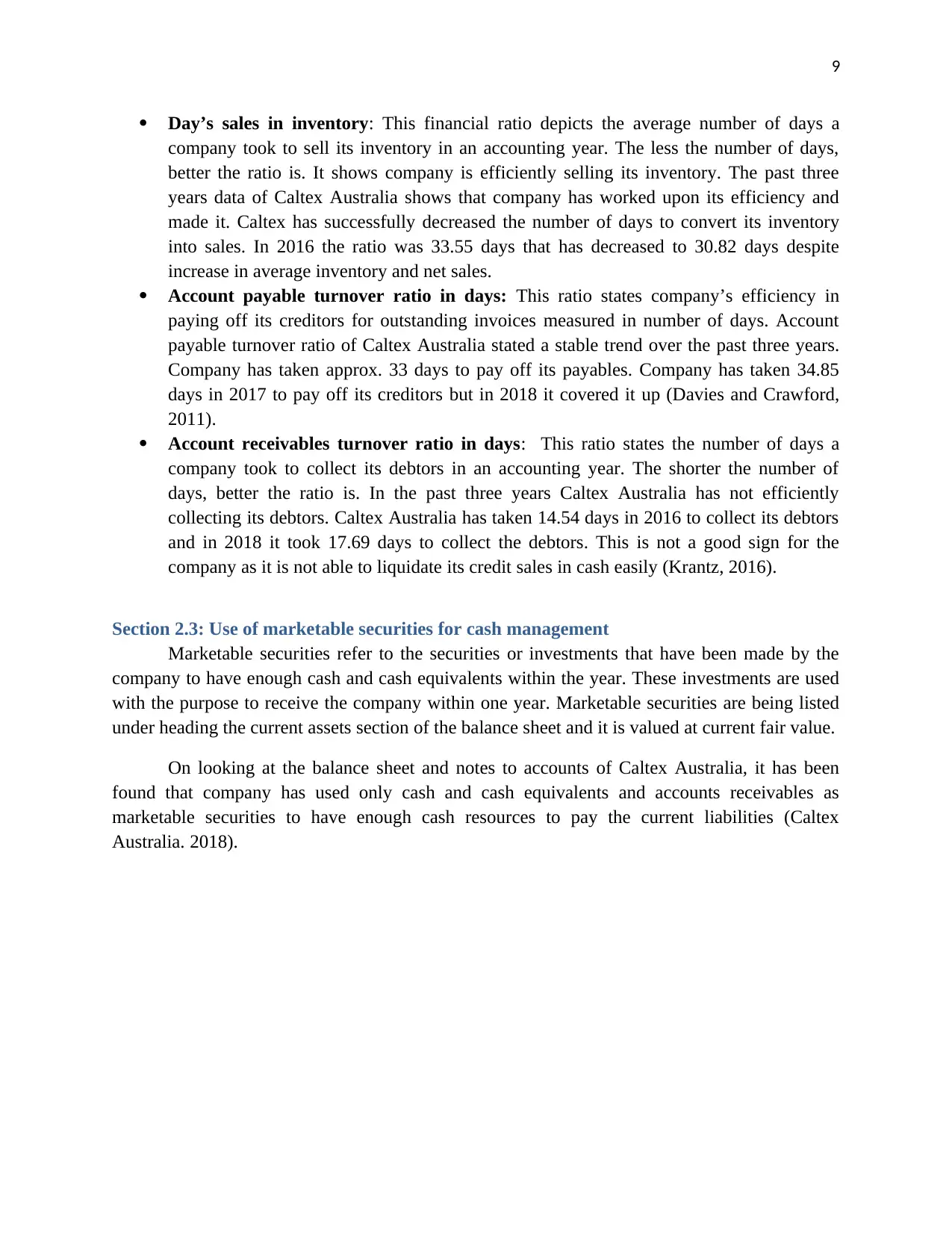

0 1 2 3 4

Cash Inflows

Units sold 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,459,090.91$ 1,326,446.28$ 1,205,860.26$ 1,642,647.36$

Net Present Value 3,034,044.81$

Cash Flows during the life of the project in normal Case

Years

Particulars

(Reilly and Brown, 2011)

0 1 2 3 4

Cash Inflows

Units sold 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,459,090.91$ 1,326,446.28$ 1,205,860.26$ 1,642,647.36$

Net Present Value 3,034,044.81$

Cash Flows during the life of the project in normal Case

Years

Particulars

(Reilly and Brown, 2011)

12

0 1 2 3 4

Cash Inflows

Selling Units 270000 270000 270000 270000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,240,000.00$ 3,240,000.00$ 3,240,000.00$ 3,240,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 3,990,000.00$ 3,990,000.00$ 3,990,000.00$ 3,990,000.00$

Cash flows before tax 1,410,000.00$ 1,410,000.00$ 1,410,000.00$ 1,410,000.00$

Less: Tax @ 30% 423,000.00$ 423,000.00$ 423,000.00$ 423,000.00$

Cash Flows after tax 987,000.00$ 987,000.00$ 987,000.00$ 987,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 2,237,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,306,363.64$ 1,187,603.31$ 1,079,639.37$ 1,527,901.10$

Net Present Value 2,501,507.41$

Particulars Years

Statement of Cash flows when Unit sales decrease by 10%

(Schlichting, 2013)

0 1 2 3 4

Cash Inflows

Selling Units 270000 270000 270000 270000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,240,000.00$ 3,240,000.00$ 3,240,000.00$ 3,240,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 3,990,000.00$ 3,990,000.00$ 3,990,000.00$ 3,990,000.00$

Cash flows before tax 1,410,000.00$ 1,410,000.00$ 1,410,000.00$ 1,410,000.00$

Less: Tax @ 30% 423,000.00$ 423,000.00$ 423,000.00$ 423,000.00$

Cash Flows after tax 987,000.00$ 987,000.00$ 987,000.00$ 987,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,437,000.00$ 1,437,000.00$ 1,437,000.00$ 2,237,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,306,363.64$ 1,187,603.31$ 1,079,639.37$ 1,527,901.10$

Net Present Value 2,501,507.41$

Particulars Years

Statement of Cash flows when Unit sales decrease by 10%

(Schlichting, 2013)

13

0 1 2 3 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,050,000.00$ 1,050,000.00$ 1,050,000.00$ 1,050,000.00$

Less: Tax @ 30% 315,000.00$ 315,000.00$ 315,000.00$ 315,000.00$

Cash Flows after tax 735,000.00$ 735,000.00$ 735,000.00$ 735,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 1,185,000.00$ 1,185,000.00$ 1,185,000.00$ 1,185,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,185,000.00$ 1,185,000.00$ 1,185,000.00$ 1,985,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,077,272.73$ 979,338.84$ 890,308.04$ 1,355,781.71$

Net Present Value 1,702,701.32$

Particulars Years

Statement of Cash flows when Price per unit decreases by 10%

0 1 2 3 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,050,000.00$ 1,050,000.00$ 1,050,000.00$ 1,050,000.00$

Less: Tax @ 30% 315,000.00$ 315,000.00$ 315,000.00$ 315,000.00$

Cash Flows after tax 735,000.00$ 735,000.00$ 735,000.00$ 735,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 1,185,000.00$ 1,185,000.00$ 1,185,000.00$ 1,185,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,185,000.00$ 1,185,000.00$ 1,185,000.00$ 1,985,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 1,077,272.73$ 979,338.84$ 890,308.04$ 1,355,781.71$

Net Present Value 1,702,701.32$

Particulars Years

Statement of Cash flows when Price per unit decreases by 10%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

14

0 1 2 3 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,960,000.00$ 3,960,000.00$ 3,960,000.00$ 3,960,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,710,000.00$ 4,710,000.00$ 4,710,000.00$ 4,710,000.00$

Cash flows before tax 690,000.00$ 690,000.00$ 690,000.00$ 690,000.00$

Less: Tax @ 30% 207,000.00$ 207,000.00$ 207,000.00$ 207,000.00$

Cash Flows after tax 483,000.00$ 483,000.00$ 483,000.00$ 483,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 933,000.00$ 933,000.00$ 933,000.00$ 933,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 933,000.00$ 933,000.00$ 933,000.00$ 1,733,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 848,181.82$ 771,074.38$ 700,976.71$ 1,183,662.32$

Net Present Value 903,895.23$

Particulars Years

Statement of Cash flows when Variable cost per unit increases 10%

0 1 2 3 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,960,000.00$ 3,960,000.00$ 3,960,000.00$ 3,960,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,710,000.00$ 4,710,000.00$ 4,710,000.00$ 4,710,000.00$

Cash flows before tax 690,000.00$ 690,000.00$ 690,000.00$ 690,000.00$

Less: Tax @ 30% 207,000.00$ 207,000.00$ 207,000.00$ 207,000.00$

Cash Flows after tax 483,000.00$ 483,000.00$ 483,000.00$ 483,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 933,000.00$ 933,000.00$ 933,000.00$ 933,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 933,000.00$ 933,000.00$ 933,000.00$ 1,733,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 848,181.82$ 771,074.38$ 700,976.71$ 1,183,662.32$

Net Present Value 903,895.23$

Particulars Years

Statement of Cash flows when Variable cost per unit increases 10%

15

0 1 2 3 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,960,000.00$ 3,960,000.00$ 3,960,000.00$ 3,960,000.00$

Fixed Cost 330,000.00$ 330,000.00$ 330,000.00$ 330,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,740,000.00$ 4,740,000.00$ 4,740,000.00$ 4,740,000.00$

Cash flows before tax 660,000.00$ 660,000.00$ 660,000.00$ 660,000.00$

Less: Tax @ 30% 198,000.00$ 198,000.00$ 198,000.00$ 198,000.00$

Cash Flows after tax 462,000.00$ 462,000.00$ 462,000.00$ 462,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 912,000.00$ 912,000.00$ 912,000.00$ 912,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 912,000.00$ 912,000.00$ 912,000.00$ 1,712,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 829,090.91$ 753,719.01$ 685,199.10$ 1,169,319.04$

Net Present Value 837,328.05$

Particulars Years

Statement of Cash flows when Cash fixed cost per year increases by 10%

Cases NPV (Normal

Case)

NPV (Special

Case) Increase/Decrease

Unit sales decrease by 10% $ 3,034,044.81 $ 2,501,507.41 $ (532,537.39)

Price per unit decreases by 10% $ 3,034,044.81 $ 1,702,701.32 $ (1,331,343.49)

Variable cost per unit increases

10% $ 3,034,044.81 $ 903,895.23 $ (2,130,149.58)

Cash fixed cost per year increases

by 10% $ 3,034,044.81 $ 837,328.05 $ (2,196,716.75)

(Zimmerman and Yahya-Zadeh, 2011)

0 1 2 3 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 18.00$ 18.00$ 18.00$ 18.00$

Net Cash Inflows 5,400,000.00$ 5,400,000.00$ 5,400,000.00$ 5,400,000.00$

Cash Outflows

Variable Cost 3,960,000.00$ 3,960,000.00$ 3,960,000.00$ 3,960,000.00$

Fixed Cost 330,000.00$ 330,000.00$ 330,000.00$ 330,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,740,000.00$ 4,740,000.00$ 4,740,000.00$ 4,740,000.00$

Cash flows before tax 660,000.00$ 660,000.00$ 660,000.00$ 660,000.00$

Less: Tax @ 30% 198,000.00$ 198,000.00$ 198,000.00$ 198,000.00$

Cash Flows after tax 462,000.00$ 462,000.00$ 462,000.00$ 462,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after 912,000.00$ 912,000.00$ 912,000.00$ 912,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 912,000.00$ 912,000.00$ 912,000.00$ 1,712,000.00$

PVF @ 10% 1.000 0.909 0.826 0.751 0.683

(2,600,000.00)$ 829,090.91$ 753,719.01$ 685,199.10$ 1,169,319.04$

Net Present Value 837,328.05$

Particulars Years

Statement of Cash flows when Cash fixed cost per year increases by 10%

Cases NPV (Normal

Case)

NPV (Special

Case) Increase/Decrease

Unit sales decrease by 10% $ 3,034,044.81 $ 2,501,507.41 $ (532,537.39)

Price per unit decreases by 10% $ 3,034,044.81 $ 1,702,701.32 $ (1,331,343.49)

Variable cost per unit increases

10% $ 3,034,044.81 $ 903,895.23 $ (2,130,149.58)

Cash fixed cost per year increases

by 10% $ 3,034,044.81 $ 837,328.05 $ (2,196,716.75)

(Zimmerman and Yahya-Zadeh, 2011)

16

Section 2.5: Identification and discussion on systematic risk and Unsystematic risk that

impacts the performance of Caltex Australia

Systematic Risks associated with Caltex Australia

Systematic risks are the risk that is associated with the company due to fluctuations in the

overall market segment. It is not possible to be diversified as it impacts the entire market

segment not only just a particular company. The systematic risks associated with Caltex

Australia can be categorized as follows:

Commodity Price Risk

The company performance can be significantly impacted by the fluctuations in the prices

of crude oil by influencing its sales and purchase financial transactions. The changes in the price

of crude oil can have a large effect on the earning potential and cash flows of the company. The

company intends to manage this risk by the use of derivative contracts in relation to both crude

and finished products (Caltex Australia, 2018).

Foreign Exchange Risk

The fluctuations in the foreign currencies also have a major impact on the financial

performance the company. This is because it tends to purchase crude products in the US dollar

and sells it in the Australian dollar. Therefore, the changes in the exchange rate between the US

and Australian dollar leads to influencing the earning potential of the company. Caltex Australia

has adopted the use of foreign exchange contracts such as forwards or swaps for mitigating the

exposure for foreign currency (Caltex Australia, 2018).

Interest Rate Risk

The company incorporates the use of debt in its capital structure and therefore is

associated with the risk of not able to meet its interest obligations on its long-term loans. This is

because fluctuations in the market can results in causing changes in the interest rates and thus it

may result for the company to not able to meet its interest obligations in a regular manner. The

company manages the exposure to interest rate risk by the use of derivative instruments (Caltex

Australia: Annual Report, 2018).

Unsystematic Risks associated with the Caltex Australia

On the other hand, the unsystematic risks associated with Caltex Australia are

categorized as follows:

Operational Risk

The nature of business operations of Caltex Australia are associated with high risk of

causing injury to people or property and also leading to incurring financial loss for the company.

As such, the company has implemented in place and adequate system of management to prevent

Section 2.5: Identification and discussion on systematic risk and Unsystematic risk that

impacts the performance of Caltex Australia

Systematic Risks associated with Caltex Australia

Systematic risks are the risk that is associated with the company due to fluctuations in the

overall market segment. It is not possible to be diversified as it impacts the entire market

segment not only just a particular company. The systematic risks associated with Caltex

Australia can be categorized as follows:

Commodity Price Risk

The company performance can be significantly impacted by the fluctuations in the prices

of crude oil by influencing its sales and purchase financial transactions. The changes in the price

of crude oil can have a large effect on the earning potential and cash flows of the company. The

company intends to manage this risk by the use of derivative contracts in relation to both crude

and finished products (Caltex Australia, 2018).

Foreign Exchange Risk

The fluctuations in the foreign currencies also have a major impact on the financial

performance the company. This is because it tends to purchase crude products in the US dollar

and sells it in the Australian dollar. Therefore, the changes in the exchange rate between the US

and Australian dollar leads to influencing the earning potential of the company. Caltex Australia

has adopted the use of foreign exchange contracts such as forwards or swaps for mitigating the

exposure for foreign currency (Caltex Australia, 2018).

Interest Rate Risk

The company incorporates the use of debt in its capital structure and therefore is

associated with the risk of not able to meet its interest obligations on its long-term loans. This is

because fluctuations in the market can results in causing changes in the interest rates and thus it

may result for the company to not able to meet its interest obligations in a regular manner. The

company manages the exposure to interest rate risk by the use of derivative instruments (Caltex

Australia: Annual Report, 2018).

Unsystematic Risks associated with the Caltex Australia

On the other hand, the unsystematic risks associated with Caltex Australia are

categorized as follows:

Operational Risk

The nature of business operations of Caltex Australia are associated with high risk of

causing injury to people or property and also leading to incurring financial loss for the company.

As such, the company has implemented in place and adequate system of management to prevent

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

17

the occurrence of risks related to safety or health. The senior management of the company

regularly reviews the business operations for identifying any type of operational risk and

mitigating the risks in advance (Caltex Australia, 2018).

Competitive Risk

Caltex Australia conducts its operations in a highly competitive market of Australia and

therefore its future growth can be largely impacted by the increasing competition which can lead

to reduction in its sales figures. As such, the company has integrated the use of business

strategies such as reduction in cost and enhancing the operational efficiency for promoting its

sustainable performance.

Environmental Risks

The major operations of the company consist of importing; storing, transporting and

selling petroleum based products and thus is highly exposed to the environmental risk associated

with spillovers. The occurrence of such type of incidents can results in disrupting the

performance of the company in the long-term. The company manages exposure to this risk by

implementation of strict operating standards and policies that ensures its compliance with the

environmental laws and regulations (Caltex Australia, 2018).

Credit Risk

The company is also associated with the risk of incurring financial losses due to failure of its

counterparties to meet their financial obligations. As such, it has implemented a credit policy for

managing its credit risk through regularly reviewing the credit quality of its customers. It

conducts its financial transactions with large number of customers for reducing the cruet risk.

Regulatory Risk

The company conducts its business activities in a highly regulated environment and

therefore it is very essential for complying with all the relevant laws in an effective manner to

minimize the material impact on its operations due to non-complying with adequate laws and

government policies. It proactively manages its regulatory risks through promoting its

engagement with regulatory bodies and also ensuring it’s complying with all the legal laws and

standards (Caltex Australia: Annual Report, 2018).

Section 2.6: Calculation of dividend payout of Caltex Australia for last three years and

interpretation of dividend policy used by Caltex

Dividend Payout Ratio of Caltex Australia

Dividend payout ratio of Caltex Australia for last three years

Items 2016 2017 2018

the occurrence of risks related to safety or health. The senior management of the company

regularly reviews the business operations for identifying any type of operational risk and

mitigating the risks in advance (Caltex Australia, 2018).

Competitive Risk

Caltex Australia conducts its operations in a highly competitive market of Australia and

therefore its future growth can be largely impacted by the increasing competition which can lead

to reduction in its sales figures. As such, the company has integrated the use of business

strategies such as reduction in cost and enhancing the operational efficiency for promoting its

sustainable performance.

Environmental Risks

The major operations of the company consist of importing; storing, transporting and

selling petroleum based products and thus is highly exposed to the environmental risk associated

with spillovers. The occurrence of such type of incidents can results in disrupting the

performance of the company in the long-term. The company manages exposure to this risk by

implementation of strict operating standards and policies that ensures its compliance with the

environmental laws and regulations (Caltex Australia, 2018).

Credit Risk

The company is also associated with the risk of incurring financial losses due to failure of its

counterparties to meet their financial obligations. As such, it has implemented a credit policy for

managing its credit risk through regularly reviewing the credit quality of its customers. It

conducts its financial transactions with large number of customers for reducing the cruet risk.

Regulatory Risk

The company conducts its business activities in a highly regulated environment and

therefore it is very essential for complying with all the relevant laws in an effective manner to

minimize the material impact on its operations due to non-complying with adequate laws and

government policies. It proactively manages its regulatory risks through promoting its

engagement with regulatory bodies and also ensuring it’s complying with all the legal laws and

standards (Caltex Australia: Annual Report, 2018).

Section 2.6: Calculation of dividend payout of Caltex Australia for last three years and

interpretation of dividend policy used by Caltex

Dividend Payout Ratio of Caltex Australia

Dividend payout ratio of Caltex Australia for last three years

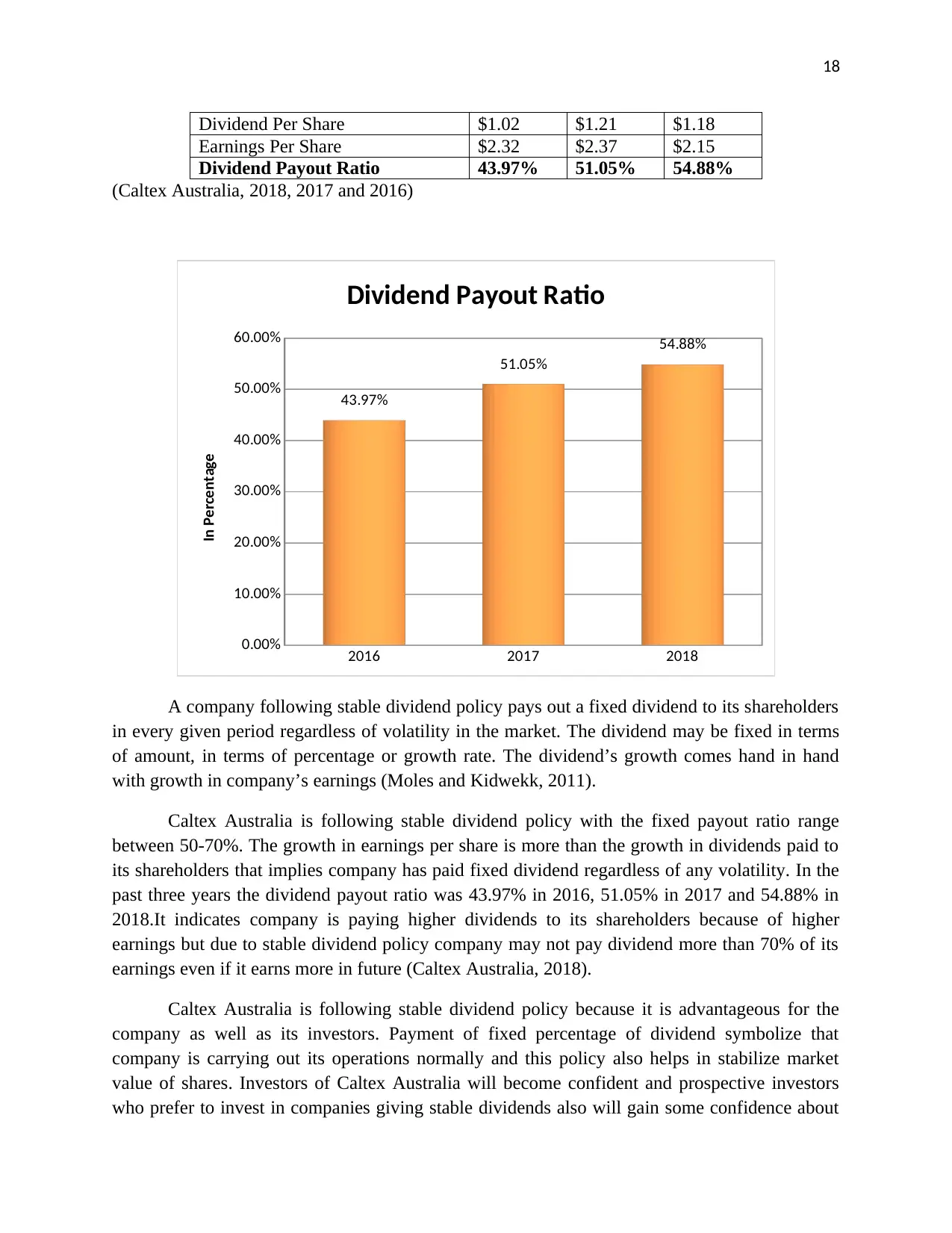

Items 2016 2017 2018

18

Dividend Per Share $1.02 $1.21 $1.18

Earnings Per Share $2.32 $2.37 $2.15

Dividend Payout Ratio 43.97% 51.05% 54.88%

(Caltex Australia, 2018, 2017 and 2016)

2016 2017 2018

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

43.97%

51.05%

54.88%

Dividend Payout Ratio

In Percentage

A company following stable dividend policy pays out a fixed dividend to its shareholders

in every given period regardless of volatility in the market. The dividend may be fixed in terms

of amount, in terms of percentage or growth rate. The dividend’s growth comes hand in hand

with growth in company’s earnings (Moles and Kidwekk, 2011).

Caltex Australia is following stable dividend policy with the fixed payout ratio range

between 50-70%. The growth in earnings per share is more than the growth in dividends paid to

its shareholders that implies company has paid fixed dividend regardless of any volatility. In the

past three years the dividend payout ratio was 43.97% in 2016, 51.05% in 2017 and 54.88% in

2018.It indicates company is paying higher dividends to its shareholders because of higher

earnings but due to stable dividend policy company may not pay dividend more than 70% of its

earnings even if it earns more in future (Caltex Australia, 2018).

Caltex Australia is following stable dividend policy because it is advantageous for the

company as well as its investors. Payment of fixed percentage of dividend symbolize that

company is carrying out its operations normally and this policy also helps in stabilize market

value of shares. Investors of Caltex Australia will become confident and prospective investors

who prefer to invest in companies giving stable dividends also will gain some confidence about

Dividend Per Share $1.02 $1.21 $1.18

Earnings Per Share $2.32 $2.37 $2.15

Dividend Payout Ratio 43.97% 51.05% 54.88%

(Caltex Australia, 2018, 2017 and 2016)

2016 2017 2018

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

43.97%

51.05%

54.88%

Dividend Payout Ratio

In Percentage

A company following stable dividend policy pays out a fixed dividend to its shareholders

in every given period regardless of volatility in the market. The dividend may be fixed in terms

of amount, in terms of percentage or growth rate. The dividend’s growth comes hand in hand

with growth in company’s earnings (Moles and Kidwekk, 2011).

Caltex Australia is following stable dividend policy with the fixed payout ratio range

between 50-70%. The growth in earnings per share is more than the growth in dividends paid to

its shareholders that implies company has paid fixed dividend regardless of any volatility. In the

past three years the dividend payout ratio was 43.97% in 2016, 51.05% in 2017 and 54.88% in

2018.It indicates company is paying higher dividends to its shareholders because of higher

earnings but due to stable dividend policy company may not pay dividend more than 70% of its

earnings even if it earns more in future (Caltex Australia, 2018).

Caltex Australia is following stable dividend policy because it is advantageous for the

company as well as its investors. Payment of fixed percentage of dividend symbolize that

company is carrying out its operations normally and this policy also helps in stabilize market

value of shares. Investors of Caltex Australia will become confident and prospective investors

who prefer to invest in companies giving stable dividends also will gain some confidence about

19

the company. The stable dividend becomes source of income to meet daily expenses for the

investors who invested in Caltex Australia to earn. Stable dividend policy will help Caltex

Australia in improving its credit standing and make financing easy for it (Moles and Kidwekk,

2011).

Section III: Letter of Recommendation to the client

To

Institutional investor (Name)

On the basis of examination of the company performance during the three years from

2016 to 2018, it is highly recommended not to make the investment in Caltex Australia. Caltex

Australia is well company that deals in supply for petroleum products and other related products

to the retailers and wholesalers of Australia. Caltex Australia is facing many global and

economic issues to rapidly increasing fuel prices and demand in Australia and other countries in

which Caltex provide its services. Due to increase in price there is very impact on the

performance of the company during the three years of operations. The financial performance of

Caltex Australia has been judged through calculating and interpreting profitability and

operational efficiency of the company. Profitability ratios such as gross profit ratio; return on

assets, and cash flow margin have been used to depict the profitability performance. It has been

interpreted from the calculation that there has been decreasing trend in profitability ratios that

signifies poor performance of the company. Similarly efficiency ratios such as day’s sales in

inventory, day’s accounts receivable outstanding and day’s account payable outstanding have

been used to evaluate the management operation efficiency during the last three years. It has

been noted that management at Caltex has not shown any major efforts to improve the

operational performance and despite management has taken more days in current year to collect

receivables as compare to previous years. The only reason that supports the company

performance was its stable dividend policy and continuously increasing dividend payout ratio

during the last three years. So, decision to make investment is completely dependent upon the

future management action that helps to increase the profitability performance. In case actions

taken by the management helps to increase the profitability in one or two quarter than investors

will think to make the investment in this company.

From

Name of group of investment analysts

Section IV: Conclusion

The overall performance report of Caltex Australia is not satisfactory during the last three

years. The two groups of financial ratios used to evaluate the performance include profitability

ratios and operating efficiency. There was decreasing trend in all the calculated profitability

the company. The stable dividend becomes source of income to meet daily expenses for the

investors who invested in Caltex Australia to earn. Stable dividend policy will help Caltex

Australia in improving its credit standing and make financing easy for it (Moles and Kidwekk,

2011).

Section III: Letter of Recommendation to the client

To

Institutional investor (Name)

On the basis of examination of the company performance during the three years from

2016 to 2018, it is highly recommended not to make the investment in Caltex Australia. Caltex

Australia is well company that deals in supply for petroleum products and other related products

to the retailers and wholesalers of Australia. Caltex Australia is facing many global and

economic issues to rapidly increasing fuel prices and demand in Australia and other countries in

which Caltex provide its services. Due to increase in price there is very impact on the

performance of the company during the three years of operations. The financial performance of

Caltex Australia has been judged through calculating and interpreting profitability and

operational efficiency of the company. Profitability ratios such as gross profit ratio; return on

assets, and cash flow margin have been used to depict the profitability performance. It has been

interpreted from the calculation that there has been decreasing trend in profitability ratios that

signifies poor performance of the company. Similarly efficiency ratios such as day’s sales in

inventory, day’s accounts receivable outstanding and day’s account payable outstanding have

been used to evaluate the management operation efficiency during the last three years. It has

been noted that management at Caltex has not shown any major efforts to improve the

operational performance and despite management has taken more days in current year to collect

receivables as compare to previous years. The only reason that supports the company

performance was its stable dividend policy and continuously increasing dividend payout ratio

during the last three years. So, decision to make investment is completely dependent upon the

future management action that helps to increase the profitability performance. In case actions

taken by the management helps to increase the profitability in one or two quarter than investors

will think to make the investment in this company.

From

Name of group of investment analysts

Section IV: Conclusion

The overall performance report of Caltex Australia is not satisfactory during the last three

years. The two groups of financial ratios used to evaluate the performance include profitability

ratios and operating efficiency. There was decreasing trend in all the calculated profitability

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

20

ratios during the last three years that signifies that company has failed to keep up the expectation

of the investors despite increase in sales in year 2018. It is highly expected from the company

that its performance will improve in next year due to economic condition of Australia and

demand of petroleum products in Australia.

ratios during the last three years that signifies that company has failed to keep up the expectation

of the investors despite increase in sales in year 2018. It is highly expected from the company

that its performance will improve in next year due to economic condition of Australia and

demand of petroleum products in Australia.

21

References

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Caltex Australia. 2016. Annual Report. [Online]. Available at: https://www.caltex.com.au/our-

company/investor-centre/annual-reports-and-reviews [Accessed on: 31 May 2019].

Caltex Australia. 2017. Annual Report. [Online]. Available at: https://www.caltex.com.au/our-

company/investor-centre/annual-reports-and-reviews [Accessed on: 31 May 2019].

Caltex Australia. 2018. Annual Report. [Online]. Available at:

https://www.caltex.com.au/annual-report-2018 [Accessed on: 31 May 2019].

Caltex Australia. 2018. Our Company. [Online]. Available at: https://www.caltex.com.au/our-

company [Accessed on: 31 May 2019].

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. USA: Pearson.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. and Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Reilly.F.K. and Brown.K.C. 2011. Investment analysis & portfolio management. UK: South

western Cengage learning.

Schlichting, T. 2013. Fundamental Analysis, Behavioral Finance and Technical Analysis on the

Stock Market. Australia: GRIN Verlag.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

References

Brigham, F., and Michael C. 2013. Financial management: Theory & practice. Canada: Cengage

Learning.

Caltex Australia. 2016. Annual Report. [Online]. Available at: https://www.caltex.com.au/our-

company/investor-centre/annual-reports-and-reviews [Accessed on: 31 May 2019].

Caltex Australia. 2017. Annual Report. [Online]. Available at: https://www.caltex.com.au/our-

company/investor-centre/annual-reports-and-reviews [Accessed on: 31 May 2019].

Caltex Australia. 2018. Annual Report. [Online]. Available at:

https://www.caltex.com.au/annual-report-2018 [Accessed on: 31 May 2019].

Caltex Australia. 2018. Our Company. [Online]. Available at: https://www.caltex.com.au/our-

company [Accessed on: 31 May 2019].

Damodaran, A, 2011. Applied corporate finance. USA: John Wiley & sons.

Davies, T. and Crawford, I., 2011. Business accounting and finance. USA: Pearson.

Krantz, M. 2016. Fundamental Analysis for Dummies. USA: John Wiley & Sons.

Moles, P. and Kidwekk, D. 2011. Corporate finance. USA: John Wiley &sons.

Reilly.F.K. and Brown.K.C. 2011. Investment analysis & portfolio management. UK: South

western Cengage learning.

Schlichting, T. 2013. Fundamental Analysis, Behavioral Finance and Technical Analysis on the

Stock Market. Australia: GRIN Verlag.

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and

control. Issues in Accounting Education, 26(1), pp.258-259.

22

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.