Accounting Assignment 2019: AASB, Financial Reporting, and Solutions

VerifiedAdded on 2022/11/07

|13

|2037

|453

Homework Assignment

AI Summary

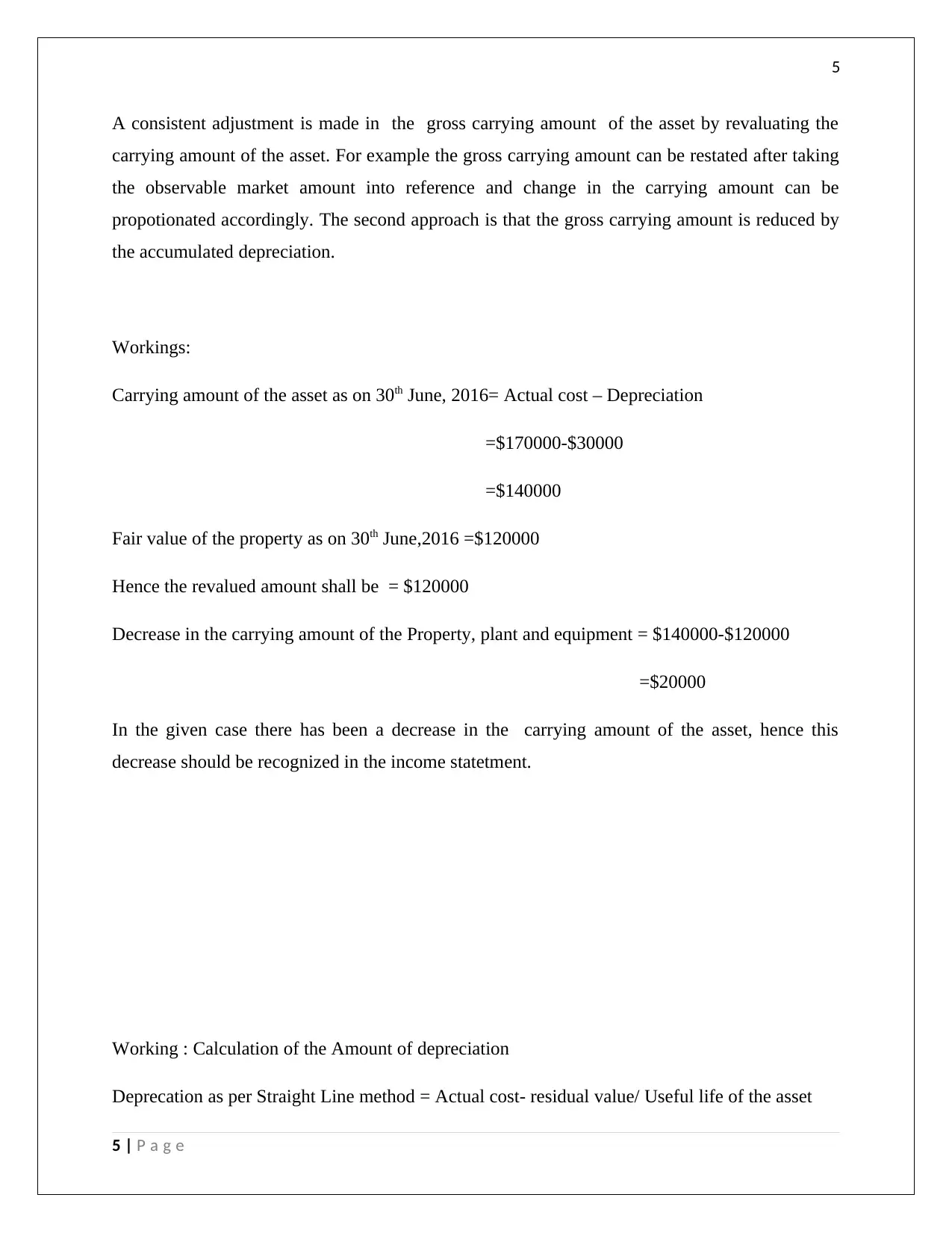

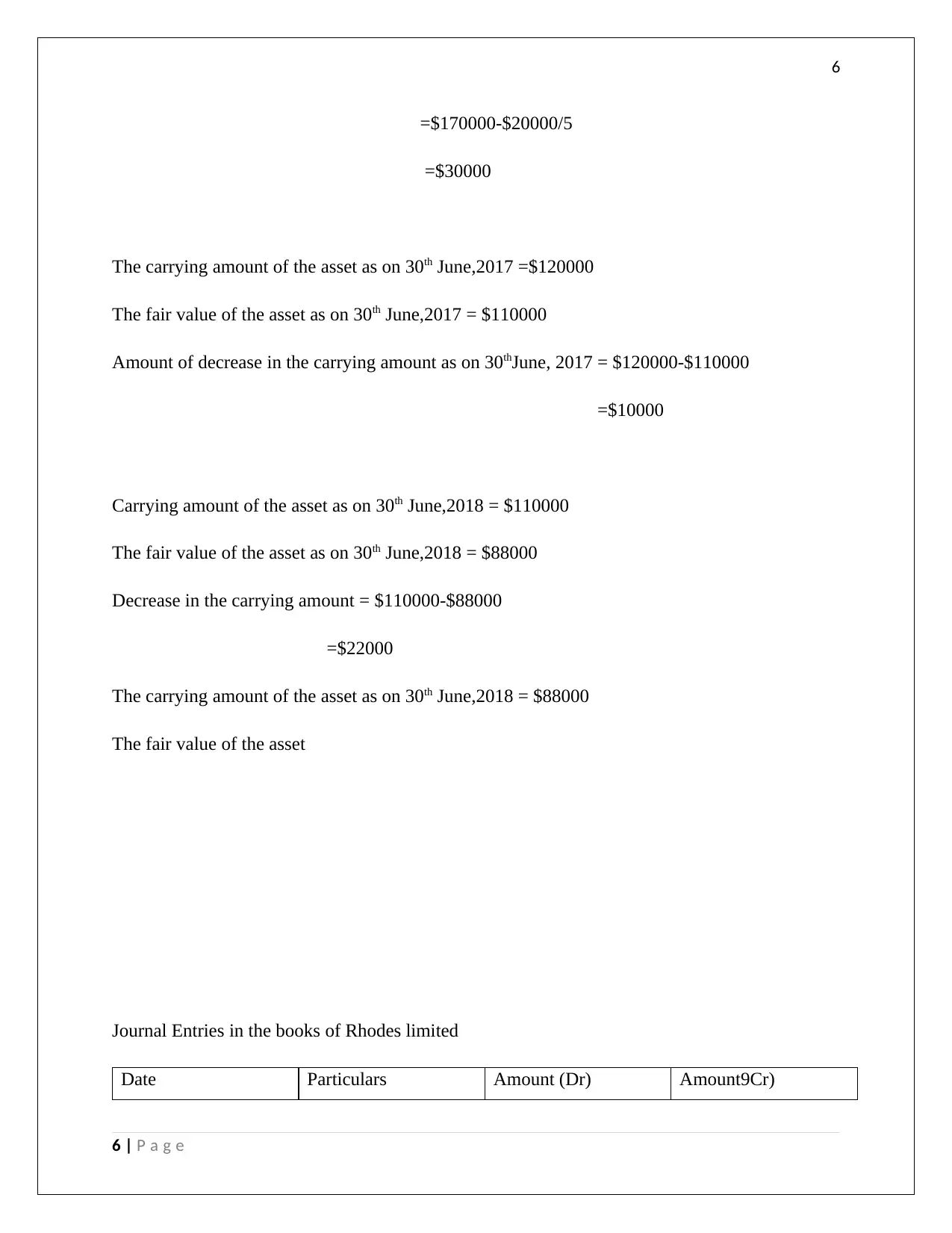

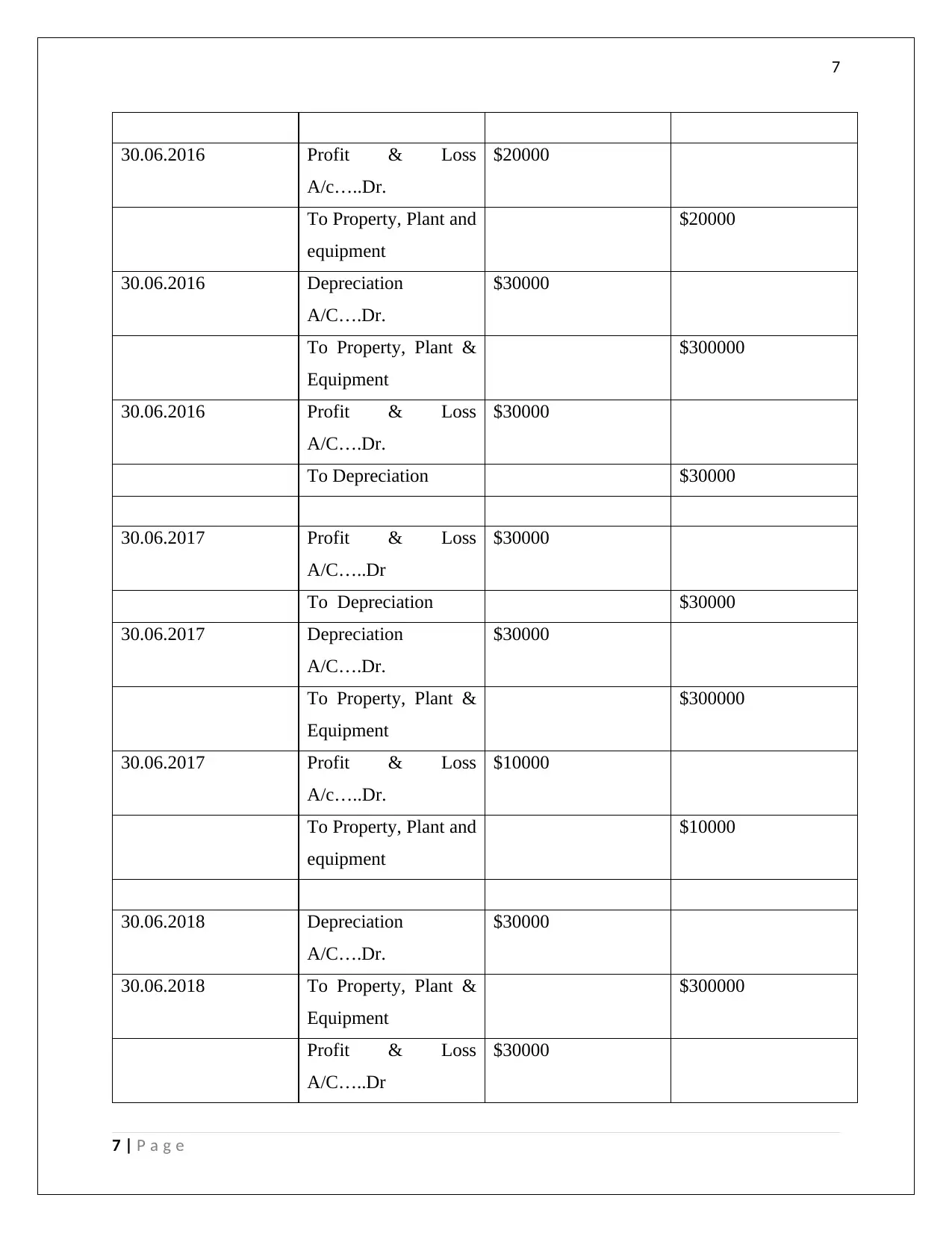

This accounting assignment solution provides a comprehensive analysis of financial reporting concepts and the application of Australian Accounting Standards Board (AASB) standards. The solution addresses three key questions: the revaluation model for property, plant, and equipment (AASB 116), including journal entries and depreciation calculations; the recognition and measurement of provisions (AASB 137) with a focus on determining the amount of provision to be recognized; and the treatment of intangible assets, specifically bitcoins, according to AASB guidelines. The solution includes detailed workings, calculations, and journal entries, demonstrating a strong understanding of accounting principles and the ability to apply them to practical scenarios. The assignment also includes an executive summary, conclusion, and references, providing a well-structured and informative response to the assignment brief.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.