Accounting Concepts, Measurement Issues and Qualitative Criteria of Conceptual Framework: Analysis of an ASX Listed Entity

Added on 2022-10-31

14 Pages3413 Words494 Views

1

HA3011

Advanced Financial Accounting

HA3011

Advanced Financial Accounting

2

Contents

Introduction......................................................................................................................................3

Part 1: Description on accounting concepts and application of same by the selected company.....3

Part 2: Discussion of Measurement Issues in Accounting in reference to Conceptual Framework

and by Using Examples from Selected Company...........................................................................6

Part 3: Analysis of Significance of Relevance and Faithful Representation Qualitative Principles

of Conceptual Framework with Reference to Examples from selected company...........................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Contents

Introduction......................................................................................................................................3

Part 1: Description on accounting concepts and application of same by the selected company.....3

Part 2: Discussion of Measurement Issues in Accounting in reference to Conceptual Framework

and by Using Examples from Selected Company...........................................................................6

Part 3: Analysis of Significance of Relevance and Faithful Representation Qualitative Principles

of Conceptual Framework with Reference to Examples from selected company...........................9

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

3

Introduction

The conceptual framework is being developed by the IASB for enhancing the quality of

financial reports and ensuring that it is able to meet the varying interests of end-users in an

effective manner. As such, the framework has emphasized on using the measurement basis for

reporting the value of assets and liabilities that is able to improve the qualitative characteristics

of relevancy and reliability of financial reporting. The impact on relevance and reliability that are

the two fundamental qualitative characteristics of financial reporting provided by conceptual

framework must be considered before the selection of a measurement basis for valuing the assets

and liabilities. In this context, the report has examined the accounting concepts, measurement

issues and qualitative criteria of conceptual framework by analysis of the annual report of a

selected ASX listed entity of CHTR H LWR FP Units Stapled Securities.

Part 1: Description on accounting concepts and application of same by the selected

company

Accounting concepts is most important concepts that act as the basic assumptions,

accounting principles and rules while performing the recording of business transactions and

drafting the financial statements of the company. The complete accounting process is based on

the accounting concepts and it is also mandatory for the business entities to follow the

accounting concepts. All the major accounting concepts have been discussed below and their

practical applications by Charter Hall Long WALE REIT have also been provided.

Business Entity Concept

The main objective of including this accounting concept is to make the business process

separate from the individual (Owner) so that it helps to perform proper accounting and allow

entity to have separate name, identity and presence. In simple words, this accounting concept

provides that business entity and business owners are two distinct persons and have distinct

identities. For example, if there is contract made with business entity than it implies that such

contract is binding on entity not on the business owner (Damodaran, 2011).

Introduction

The conceptual framework is being developed by the IASB for enhancing the quality of

financial reports and ensuring that it is able to meet the varying interests of end-users in an

effective manner. As such, the framework has emphasized on using the measurement basis for

reporting the value of assets and liabilities that is able to improve the qualitative characteristics

of relevancy and reliability of financial reporting. The impact on relevance and reliability that are

the two fundamental qualitative characteristics of financial reporting provided by conceptual

framework must be considered before the selection of a measurement basis for valuing the assets

and liabilities. In this context, the report has examined the accounting concepts, measurement

issues and qualitative criteria of conceptual framework by analysis of the annual report of a

selected ASX listed entity of CHTR H LWR FP Units Stapled Securities.

Part 1: Description on accounting concepts and application of same by the selected

company

Accounting concepts is most important concepts that act as the basic assumptions,

accounting principles and rules while performing the recording of business transactions and

drafting the financial statements of the company. The complete accounting process is based on

the accounting concepts and it is also mandatory for the business entities to follow the

accounting concepts. All the major accounting concepts have been discussed below and their

practical applications by Charter Hall Long WALE REIT have also been provided.

Business Entity Concept

The main objective of including this accounting concept is to make the business process

separate from the individual (Owner) so that it helps to perform proper accounting and allow

entity to have separate name, identity and presence. In simple words, this accounting concept

provides that business entity and business owners are two distinct persons and have distinct

identities. For example, if there is contract made with business entity than it implies that such

contract is binding on entity not on the business owner (Damodaran, 2011).

4

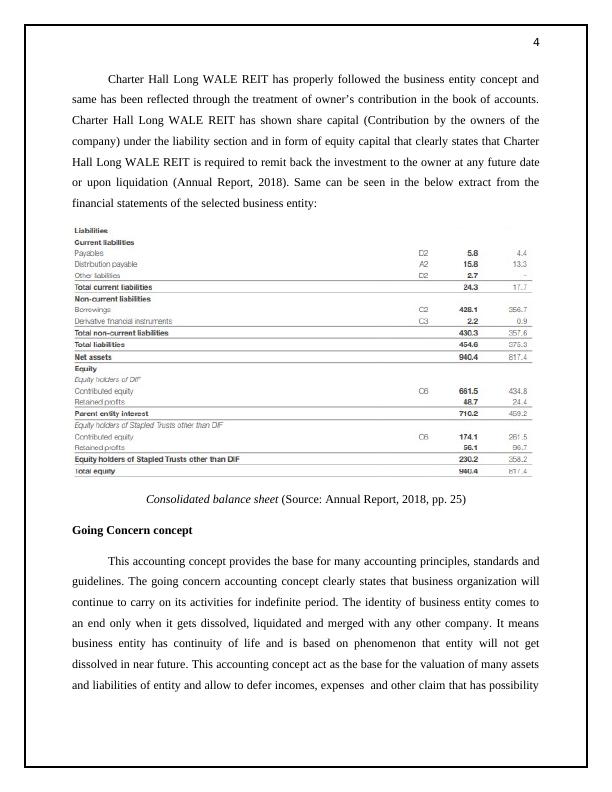

Charter Hall Long WALE REIT has properly followed the business entity concept and

same has been reflected through the treatment of owner’s contribution in the book of accounts.

Charter Hall Long WALE REIT has shown share capital (Contribution by the owners of the

company) under the liability section and in form of equity capital that clearly states that Charter

Hall Long WALE REIT is required to remit back the investment to the owner at any future date

or upon liquidation (Annual Report, 2018). Same can be seen in the below extract from the

financial statements of the selected business entity:

Consolidated balance sheet (Source: Annual Report, 2018, pp. 25)

Going Concern concept

This accounting concept provides the base for many accounting principles, standards and

guidelines. The going concern accounting concept clearly states that business organization will

continue to carry on its activities for indefinite period. The identity of business entity comes to

an end only when it gets dissolved, liquidated and merged with any other company. It means

business entity has continuity of life and is based on phenomenon that entity will not get

dissolved in near future. This accounting concept act as the base for the valuation of many assets

and liabilities of entity and allow to defer incomes, expenses and other claim that has possibility

Charter Hall Long WALE REIT has properly followed the business entity concept and

same has been reflected through the treatment of owner’s contribution in the book of accounts.

Charter Hall Long WALE REIT has shown share capital (Contribution by the owners of the

company) under the liability section and in form of equity capital that clearly states that Charter

Hall Long WALE REIT is required to remit back the investment to the owner at any future date

or upon liquidation (Annual Report, 2018). Same can be seen in the below extract from the

financial statements of the selected business entity:

Consolidated balance sheet (Source: Annual Report, 2018, pp. 25)

Going Concern concept

This accounting concept provides the base for many accounting principles, standards and

guidelines. The going concern accounting concept clearly states that business organization will

continue to carry on its activities for indefinite period. The identity of business entity comes to

an end only when it gets dissolved, liquidated and merged with any other company. It means

business entity has continuity of life and is based on phenomenon that entity will not get

dissolved in near future. This accounting concept act as the base for the valuation of many assets

and liabilities of entity and allow to defer incomes, expenses and other claim that has possibility

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Contemporary Accounting Theorylg...

|16

|4106

|251

Advanced Financial Accounting.lg...

|11

|3030

|4

Contemporary Issues in Accounting Assignment (Doc)lg...

|16

|2265

|258

Accounting Concepts and Measurement in Super Retail Grouplg...

|16

|3343

|59

Assignment (Doc) | Contemporary Accounting Theorylg...

|19

|4598

|16

Accounting Concepts and Framework: National Storage REITlg...

|13

|2239

|369