Financial Resources Management: Decisions & Implications at Raddison

VerifiedAdded on 2023/04/11

|17

|4419

|112

Report

AI Summary

This report provides an in-depth analysis of managing financial resources within business organizations, with a specific focus on Raddison Plc and its expansion perspectives. It examines various internal and external sources of finance, including retained profits, sale of fixed assets, equity share...

Managing Financial

Resources

1

Resources

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ...............................................................................................................................3

TASK 1 ................................................................................................................................................3

1.1....................................................................................................................................................3

External Sources of Finance ..................................................................................................4

1.2 ...................................................................................................................................................4

1.3....................................................................................................................................................6

TASK 2 ................................................................................................................................................6

2.1....................................................................................................................................................6

2.2 ...................................................................................................................................................7

2.3 ...................................................................................................................................................7

2.4 ...................................................................................................................................................8

TASK 3 ................................................................................................................................................8

3.1....................................................................................................................................................8

3.2 ...................................................................................................................................................9

3.3..................................................................................................................................................10

TASK 4...............................................................................................................................................11

4.1..................................................................................................................................................11

4.2..................................................................................................................................................12

4.3 .................................................................................................................................................13

Interpretation of financial statements of Raddison and ITS rivalry firm.......................................13

CONCLUSION ...............................................................................................................................14

REFERENCES...................................................................................................................................15

2

INTRODUCTION ...............................................................................................................................3

TASK 1 ................................................................................................................................................3

1.1....................................................................................................................................................3

External Sources of Finance ..................................................................................................4

1.2 ...................................................................................................................................................4

1.3....................................................................................................................................................6

TASK 2 ................................................................................................................................................6

2.1....................................................................................................................................................6

2.2 ...................................................................................................................................................7

2.3 ...................................................................................................................................................7

2.4 ...................................................................................................................................................8

TASK 3 ................................................................................................................................................8

3.1....................................................................................................................................................8

3.2 ...................................................................................................................................................9

3.3..................................................................................................................................................10

TASK 4...............................................................................................................................................11

4.1..................................................................................................................................................11

4.2..................................................................................................................................................12

4.3 .................................................................................................................................................13

Interpretation of financial statements of Raddison and ITS rivalry firm.......................................13

CONCLUSION ...............................................................................................................................14

REFERENCES...................................................................................................................................15

2

INTRODUCTION

Finance is fuel for the business. Any business or trading organizations always deals with

managing financial resources and decision making aspects. For this there must be a basic

understanding of the sources of finances available for funding in order to minimize the costs of

finance and thereby increase profitability. In the present assignment the entire discussion will focus

on the types of financial decisions taken by the organizations, the basis on which these decisions are

taken, and the effects of these decisions on the long term profitability and goals of the company.

This report is based on the software developer company named Raddison Plc which is focusing on

it expansion perspectives (The Basics of Fiancial Management, 2016).

TASK 1

1.1

Sources of finance available

Business can raise funds from various external and internal sources of Finance available.

Following are some of the internal and external sources of finance from where business can raise

funds for its operations as well as expansion.

Internal Sources of Finance:

Internal sources of finance are the finance which can be generated by business itself

internally and need not depend on external sources of finance for the same. Internal sources of

finance are:

Retained Profits: Retained profits are that part of profits which are not distributed to

shareholders as dividends rather retained into business for further expansion. This process is

known as 'Ploughing back of profits'. These are long term source of finance and most

effective as no conditions for repayment is attached to it. Radisson Plc can use this

effectively if business has earned sufficient profits in previous years it can retain part of

profits and use it for expansion (Petty, and et.al, 2015).

Sale of Fixed Assets: Sale of fixed assets such as sale of land or building or investments for

generating cash for further usage is a good option to generate funds internally and

expansion. In case Radisson Plc has some unused land and buildings investments it can sell

them off and generate cash to be utilised for business expansion (Sources of Finance, 2016).

Reduction of Working capital: Cutting down the stock levels or reducing the operating

cycle will generate cash and acts as a very good source of finance. This comes from

effective working capital management.

3

Finance is fuel for the business. Any business or trading organizations always deals with

managing financial resources and decision making aspects. For this there must be a basic

understanding of the sources of finances available for funding in order to minimize the costs of

finance and thereby increase profitability. In the present assignment the entire discussion will focus

on the types of financial decisions taken by the organizations, the basis on which these decisions are

taken, and the effects of these decisions on the long term profitability and goals of the company.

This report is based on the software developer company named Raddison Plc which is focusing on

it expansion perspectives (The Basics of Fiancial Management, 2016).

TASK 1

1.1

Sources of finance available

Business can raise funds from various external and internal sources of Finance available.

Following are some of the internal and external sources of finance from where business can raise

funds for its operations as well as expansion.

Internal Sources of Finance:

Internal sources of finance are the finance which can be generated by business itself

internally and need not depend on external sources of finance for the same. Internal sources of

finance are:

Retained Profits: Retained profits are that part of profits which are not distributed to

shareholders as dividends rather retained into business for further expansion. This process is

known as 'Ploughing back of profits'. These are long term source of finance and most

effective as no conditions for repayment is attached to it. Radisson Plc can use this

effectively if business has earned sufficient profits in previous years it can retain part of

profits and use it for expansion (Petty, and et.al, 2015).

Sale of Fixed Assets: Sale of fixed assets such as sale of land or building or investments for

generating cash for further usage is a good option to generate funds internally and

expansion. In case Radisson Plc has some unused land and buildings investments it can sell

them off and generate cash to be utilised for business expansion (Sources of Finance, 2016).

Reduction of Working capital: Cutting down the stock levels or reducing the operating

cycle will generate cash and acts as a very good source of finance. This comes from

effective working capital management.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

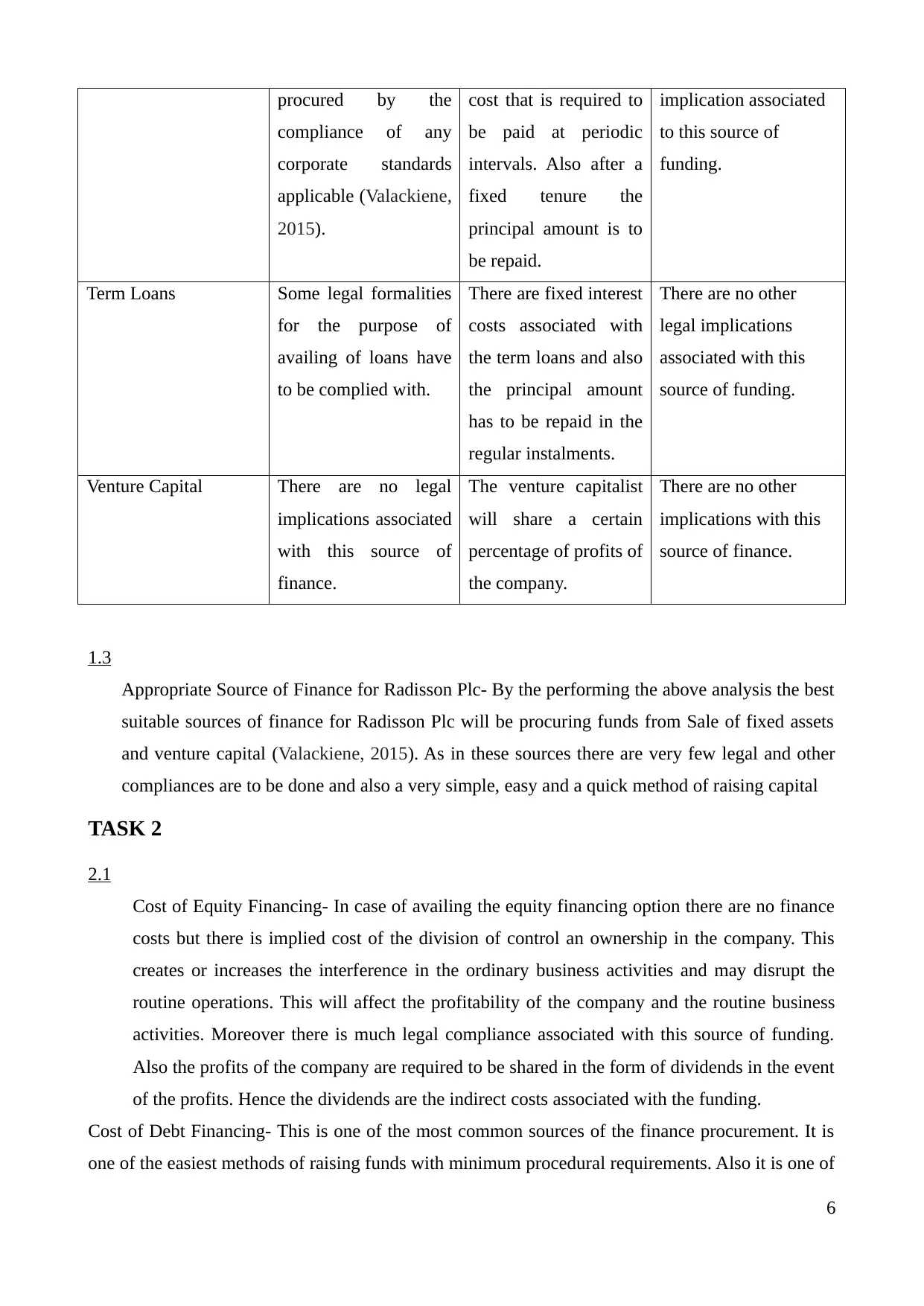

External Sources of Finance

External sources of finance are those finance which are raised from outside the business.

These are the sources of finance which are externally acquired unlike retained earnings which are

internally generated and utilised.

Equity Share Capital: Radisson Plc can raise funds through issuing equity shares. Equity

shares are common sources of funds but are governed by lots of regulations attached to it

therefore complex and involve floatation and underwriting cost. Equity share gives the

owners the ownership rights of the company.

Long term Borrowings: Long term debts are good source of finance with low cost as

compared to equity. Financial instruments such as bonds or debentures can be issued as

acknowledging the debt towards the company and is offered to common public and has

many terms and conditions attached to it (Valackiene, 2015).

Term Loans- Organization can avail term loans from banks and financial institutions which

can be either on fixed or floating rate of interest. A fixed sum as interest and a fixed amount

of the principle portion is required to be paid in the regular intervals. Hence this source is

the simplest way of finance procurement. However the bank keeps with itself a security of

the borrower as collateral. This security is liquidated in the event of failure to repay the

instalments.

Venture Capital: This is modern concept of raising funds from the venture capitalist who

are the group or individuals interested in investing amount into new start ups or business

and exit once they get a good value for their investment (Sources of Finance, 2016).

1.2

Implications of Different Sources of Finance

All the sources of finances have certain implications on the company. Below is a brief

discussion of the implications of the above stated sources of finances in a tabular form.

Sources of Finances Legal Implications Financial

Implications

Others

Retained Profits Since retained profits

are from the internal

funding there are

barely any legal

compliances (Petty,

Since there is always

the concept of

opportunity cost

associated with the

retained earnings. The

If the retained earnings

are ploughed back into

the expansion of the

business the concept of

internal rate of return

4

External sources of finance are those finance which are raised from outside the business.

These are the sources of finance which are externally acquired unlike retained earnings which are

internally generated and utilised.

Equity Share Capital: Radisson Plc can raise funds through issuing equity shares. Equity

shares are common sources of funds but are governed by lots of regulations attached to it

therefore complex and involve floatation and underwriting cost. Equity share gives the

owners the ownership rights of the company.

Long term Borrowings: Long term debts are good source of finance with low cost as

compared to equity. Financial instruments such as bonds or debentures can be issued as

acknowledging the debt towards the company and is offered to common public and has

many terms and conditions attached to it (Valackiene, 2015).

Term Loans- Organization can avail term loans from banks and financial institutions which

can be either on fixed or floating rate of interest. A fixed sum as interest and a fixed amount

of the principle portion is required to be paid in the regular intervals. Hence this source is

the simplest way of finance procurement. However the bank keeps with itself a security of

the borrower as collateral. This security is liquidated in the event of failure to repay the

instalments.

Venture Capital: This is modern concept of raising funds from the venture capitalist who

are the group or individuals interested in investing amount into new start ups or business

and exit once they get a good value for their investment (Sources of Finance, 2016).

1.2

Implications of Different Sources of Finance

All the sources of finances have certain implications on the company. Below is a brief

discussion of the implications of the above stated sources of finances in a tabular form.

Sources of Finances Legal Implications Financial

Implications

Others

Retained Profits Since retained profits

are from the internal

funding there are

barely any legal

compliances (Petty,

Since there is always

the concept of

opportunity cost

associated with the

retained earnings. The

If the retained earnings

are ploughed back into

the expansion of the

business the concept of

internal rate of return

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and et.al, 2015). cost of using the

retained funds is the

return from the next

best alternative

available.

becomes applicable.

Sale of Fixed Assets If the tax cover has

been availed in the

earlier periods than at

the point of sale also

the profit and loss on

the fixed assets is

required to be

calculated and the

necessary legal

obligations has to be

complied.

There is going to be

divestment of the

assets and there is no

finance cost associated

with this method of

funding (Kaplan and

Atkinson, 2015).

.

However substantial

the sale of fixed assets

of the business may

have a negative impact

of the financial

statements of the

organization.

Reduction of Working

Capital

There are no legal

implications attached

with this source of

finance.

It has a considerable

impact on the working

capital of the company

and therefore should

be used only if there is

excess working capital

available.

This method of funds

procurement affects the

liquidity position of

any concern and

therefore is not

advisable.

Share Capital In order to procure

funds from this source

the laws of the

company’s Act and

other stock exchanges

as may be applicable

are required to be

complied with.

Although there is no

fixed periodic costs

associated with the

issue of share capital

but it leads to the

sharing of profits and

ownership. Also in the

event of profits

dividends are required

to be distributed.

There is division of

control and ownership

which may affect the

efficiency of the

various activities in the

company.

External Borrowings These funds are to be There is fixed interest There is no other

5

retained funds is the

return from the next

best alternative

available.

becomes applicable.

Sale of Fixed Assets If the tax cover has

been availed in the

earlier periods than at

the point of sale also

the profit and loss on

the fixed assets is

required to be

calculated and the

necessary legal

obligations has to be

complied.

There is going to be

divestment of the

assets and there is no

finance cost associated

with this method of

funding (Kaplan and

Atkinson, 2015).

.

However substantial

the sale of fixed assets

of the business may

have a negative impact

of the financial

statements of the

organization.

Reduction of Working

Capital

There are no legal

implications attached

with this source of

finance.

It has a considerable

impact on the working

capital of the company

and therefore should

be used only if there is

excess working capital

available.

This method of funds

procurement affects the

liquidity position of

any concern and

therefore is not

advisable.

Share Capital In order to procure

funds from this source

the laws of the

company’s Act and

other stock exchanges

as may be applicable

are required to be

complied with.

Although there is no

fixed periodic costs

associated with the

issue of share capital

but it leads to the

sharing of profits and

ownership. Also in the

event of profits

dividends are required

to be distributed.

There is division of

control and ownership

which may affect the

efficiency of the

various activities in the

company.

External Borrowings These funds are to be There is fixed interest There is no other

5

procured by the

compliance of any

corporate standards

applicable (Valackiene,

2015).

cost that is required to

be paid at periodic

intervals. Also after a

fixed tenure the

principal amount is to

be repaid.

implication associated

to this source of

funding.

Term Loans Some legal formalities

for the purpose of

availing of loans have

to be complied with.

There are fixed interest

costs associated with

the term loans and also

the principal amount

has to be repaid in the

regular instalments.

There are no other

legal implications

associated with this

source of funding.

Venture Capital There are no legal

implications associated

with this source of

finance.

The venture capitalist

will share a certain

percentage of profits of

the company.

There are no other

implications with this

source of finance.

1.3

Appropriate Source of Finance for Radisson Plc- By the performing the above analysis the best

suitable sources of finance for Radisson Plc will be procuring funds from Sale of fixed assets

and venture capital (Valackiene, 2015). As in these sources there are very few legal and other

compliances are to be done and also a very simple, easy and a quick method of raising capital

TASK 2

2.1

Cost of Equity Financing- In case of availing the equity financing option there are no finance

costs but there is implied cost of the division of control an ownership in the company. This

creates or increases the interference in the ordinary business activities and may disrupt the

routine operations. This will affect the profitability of the company and the routine business

activities. Moreover there is much legal compliance associated with this source of funding.

Also the profits of the company are required to be shared in the form of dividends in the event

of the profits. Hence the dividends are the indirect costs associated with the funding.

Cost of Debt Financing- This is one of the most common sources of the finance procurement. It is

one of the easiest methods of raising funds with minimum procedural requirements. Also it is one of

6

compliance of any

corporate standards

applicable (Valackiene,

2015).

cost that is required to

be paid at periodic

intervals. Also after a

fixed tenure the

principal amount is to

be repaid.

implication associated

to this source of

funding.

Term Loans Some legal formalities

for the purpose of

availing of loans have

to be complied with.

There are fixed interest

costs associated with

the term loans and also

the principal amount

has to be repaid in the

regular instalments.

There are no other

legal implications

associated with this

source of funding.

Venture Capital There are no legal

implications associated

with this source of

finance.

The venture capitalist

will share a certain

percentage of profits of

the company.

There are no other

implications with this

source of finance.

1.3

Appropriate Source of Finance for Radisson Plc- By the performing the above analysis the best

suitable sources of finance for Radisson Plc will be procuring funds from Sale of fixed assets

and venture capital (Valackiene, 2015). As in these sources there are very few legal and other

compliances are to be done and also a very simple, easy and a quick method of raising capital

TASK 2

2.1

Cost of Equity Financing- In case of availing the equity financing option there are no finance

costs but there is implied cost of the division of control an ownership in the company. This

creates or increases the interference in the ordinary business activities and may disrupt the

routine operations. This will affect the profitability of the company and the routine business

activities. Moreover there is much legal compliance associated with this source of funding.

Also the profits of the company are required to be shared in the form of dividends in the event

of the profits. Hence the dividends are the indirect costs associated with the funding.

Cost of Debt Financing- This is one of the most common sources of the finance procurement. It is

one of the easiest methods of raising funds with minimum procedural requirements. Also it is one of

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the quickest means of raising finance. The finance cost is the interest charged on the amount of

borrowings made. Hence the only costs associated with this means of finance are the interest costs.

Also the fund providers do not interfere in the ordinarily course of business which leads to the

continuance of the business activities without any disruption. Hence it is one of the most suitable

forms of finance available and is on the top priorities of the fund procurers (Kaplan and Atkinson,

2015).

2.2

Importance of Financial Planning

The process of planning the different sources of finances and making the funds available for the

various business activities by simultaneous reduction in the finance costs which leads to the

increase in the overall profitability of the organization. Hence in order to survive in the competitive

market financial planning is very a very important tool. There are various other benefits in different

areas which are derived through financial planning. They are described in the following points.

Cash Flows- Through effective financial planning companies are able to predict the future

cash inflows and plan the expenditure in that manner. Hence the prediction of the cash flows

derived can be accurately made and various other dependent activities are planned.

Income- Through financial planning it is possible to increase the income by planned cutting

in the wasteful expenditures (Valackiene, 2015). The reduction in expenditures will

automatically have a positive impact on the increase in the incomes of the companies.

Investments- Through financial planning the investments can be planned as per the fund

requirements of the businesses.

2.3

Informational Needs of Decision Makers

For the purpose of sustainable development requires the various indicators to be developed for

promoting better decision making and increase in profitability of an organization (Epstein,

Buhovac, and Yuthas, 2015). The following information is very important for an effective decision

making-

User Identification- By appropriate identification of the users and relevant data collection helps in

addressing their needs in a better way. Other important information is the economic environment of

the country and also of international level. By the assessing the various data such as GDP of the

country etc, one is able to analyze the changes in the economic environment and effectively address

them. In order to facilitate the relevant use of the information it has to be available in the

understandable manner and on time.

7

borrowings made. Hence the only costs associated with this means of finance are the interest costs.

Also the fund providers do not interfere in the ordinarily course of business which leads to the

continuance of the business activities without any disruption. Hence it is one of the most suitable

forms of finance available and is on the top priorities of the fund procurers (Kaplan and Atkinson,

2015).

2.2

Importance of Financial Planning

The process of planning the different sources of finances and making the funds available for the

various business activities by simultaneous reduction in the finance costs which leads to the

increase in the overall profitability of the organization. Hence in order to survive in the competitive

market financial planning is very a very important tool. There are various other benefits in different

areas which are derived through financial planning. They are described in the following points.

Cash Flows- Through effective financial planning companies are able to predict the future

cash inflows and plan the expenditure in that manner. Hence the prediction of the cash flows

derived can be accurately made and various other dependent activities are planned.

Income- Through financial planning it is possible to increase the income by planned cutting

in the wasteful expenditures (Valackiene, 2015). The reduction in expenditures will

automatically have a positive impact on the increase in the incomes of the companies.

Investments- Through financial planning the investments can be planned as per the fund

requirements of the businesses.

2.3

Informational Needs of Decision Makers

For the purpose of sustainable development requires the various indicators to be developed for

promoting better decision making and increase in profitability of an organization (Epstein,

Buhovac, and Yuthas, 2015). The following information is very important for an effective decision

making-

User Identification- By appropriate identification of the users and relevant data collection helps in

addressing their needs in a better way. Other important information is the economic environment of

the country and also of international level. By the assessing the various data such as GDP of the

country etc, one is able to analyze the changes in the economic environment and effectively address

them. In order to facilitate the relevant use of the information it has to be available in the

understandable manner and on time.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sale of fixed assets: Decision makers of Radisson plc are looking for selling fixed assets such as

factories, warehouses and other fixed assets. It is useful for adequate fund but remains risky for

further business operations. There will be lack of fund regarding future plans to be implemented.

Thus, selling of fixed assets is effective option for gaining high level of fund. In accordance to this,

decision makers should analyse proper sourcing and investing of money.

Venture capital: It is an approach for taking help of venture capitalist. Under this process,

other businesses can support Raddison plc. In this regard, it is required for entity to recognize all

business performances and activities of venture capitalists. Thus, decision makers of firm should

focus on market position of supportive companies.

Share Capital: It is related to dividend and support of shareholders of Raddison plc. Through

this approach, organization can take help from shareholders by encouraging them for better

investments and highly effective business performance to systematic management of entity.

2.4

Balance Sheet- From raising funds from the venture capital and sale of fixed assets it will

impact the financial position of the company. In the balance sheet the asset side will be reduced

by those sold and a simultaneous credit will be there in the bank account or cash account.

Venture capital funds will be shown as the part of permanent capital of the company or long

term funds depending on the terms and conditions (Petty, and et.al, 2015).

Profit & Loss Statement- There is going to be no impact on this statement by the sale of fixed

assets unless there is profit or loss on such sale. If there is any profit and loss on the sale the

same will be booked in the P & L in the same year. Also by procuring funds through venture

capital there are only procedural formalities to be charged from P & L. Otherwise there is no

fixed costs.

TASK 3

3.1

Importance of Budgets in making Financial Decisions

Budgets helps in making many important financial decisions such as whether to hold or continue

with the particular project or not, or taking various outsourcing decisions. Budgets help in analyzing

and planning the incomes and expenditures of the company and by simultaneously reducing the

variances. Hence the profitability and long term goals can be easily accomplished by using

budgeting technique (Sources of Finance, 2016).

Below is the illustration of the cash budget which helps in assessing the cash available at the

particular period of time. Hence it is useful in planning the cash inflows and outflows.

8

factories, warehouses and other fixed assets. It is useful for adequate fund but remains risky for

further business operations. There will be lack of fund regarding future plans to be implemented.

Thus, selling of fixed assets is effective option for gaining high level of fund. In accordance to this,

decision makers should analyse proper sourcing and investing of money.

Venture capital: It is an approach for taking help of venture capitalist. Under this process,

other businesses can support Raddison plc. In this regard, it is required for entity to recognize all

business performances and activities of venture capitalists. Thus, decision makers of firm should

focus on market position of supportive companies.

Share Capital: It is related to dividend and support of shareholders of Raddison plc. Through

this approach, organization can take help from shareholders by encouraging them for better

investments and highly effective business performance to systematic management of entity.

2.4

Balance Sheet- From raising funds from the venture capital and sale of fixed assets it will

impact the financial position of the company. In the balance sheet the asset side will be reduced

by those sold and a simultaneous credit will be there in the bank account or cash account.

Venture capital funds will be shown as the part of permanent capital of the company or long

term funds depending on the terms and conditions (Petty, and et.al, 2015).

Profit & Loss Statement- There is going to be no impact on this statement by the sale of fixed

assets unless there is profit or loss on such sale. If there is any profit and loss on the sale the

same will be booked in the P & L in the same year. Also by procuring funds through venture

capital there are only procedural formalities to be charged from P & L. Otherwise there is no

fixed costs.

TASK 3

3.1

Importance of Budgets in making Financial Decisions

Budgets helps in making many important financial decisions such as whether to hold or continue

with the particular project or not, or taking various outsourcing decisions. Budgets help in analyzing

and planning the incomes and expenditures of the company and by simultaneously reducing the

variances. Hence the profitability and long term goals can be easily accomplished by using

budgeting technique (Sources of Finance, 2016).

Below is the illustration of the cash budget which helps in assessing the cash available at the

particular period of time. Hence it is useful in planning the cash inflows and outflows.

8

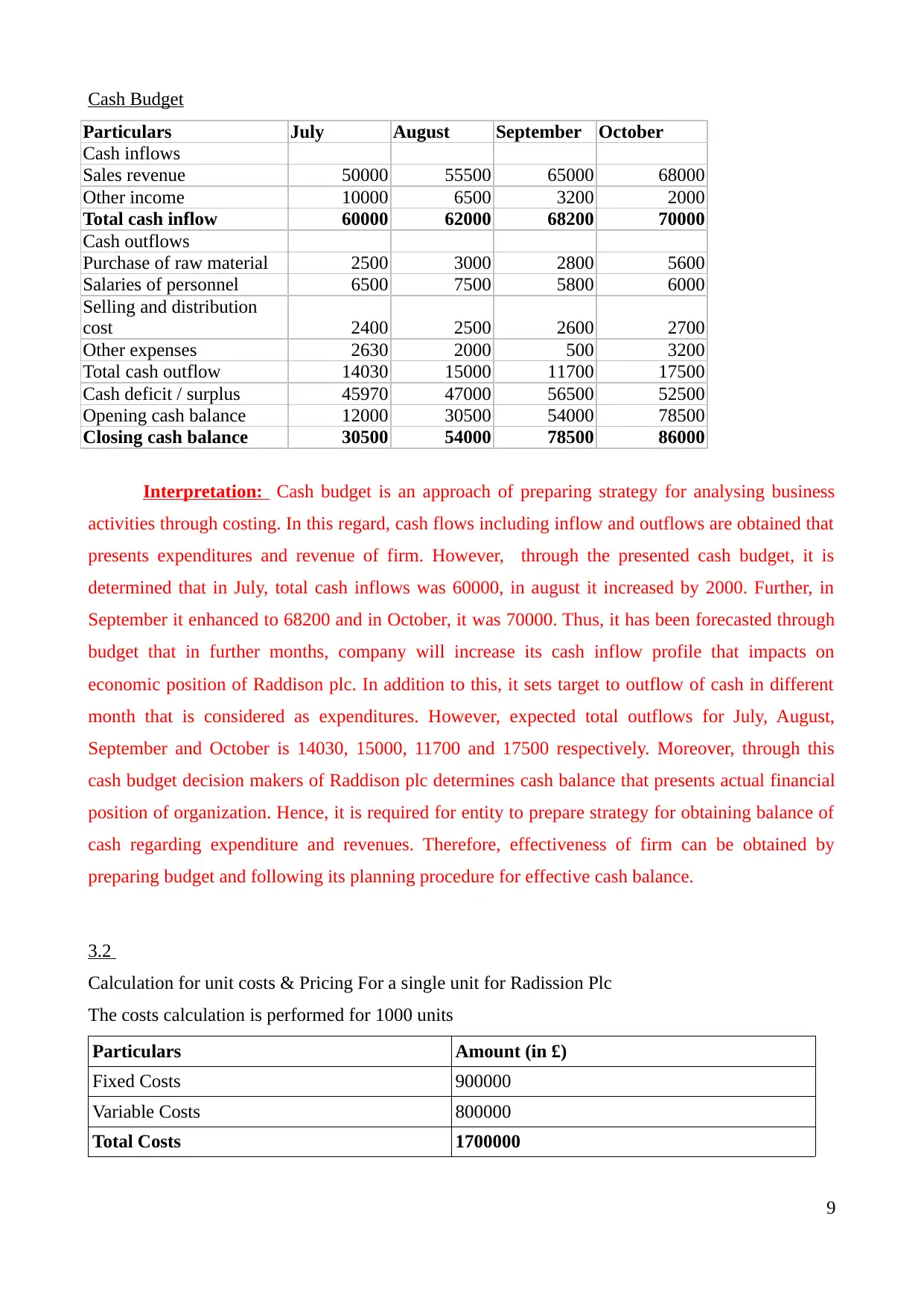

Cash Budget

Particulars July August September October

Cash inflows

Sales revenue 50000 55500 65000 68000

Other income 10000 6500 3200 2000

Total cash inflow 60000 62000 68200 70000

Cash outflows

Purchase of raw material 2500 3000 2800 5600

Salaries of personnel 6500 7500 5800 6000

Selling and distribution

cost 2400 2500 2600 2700

Other expenses 2630 2000 500 3200

Total cash outflow 14030 15000 11700 17500

Cash deficit / surplus 45970 47000 56500 52500

Opening cash balance 12000 30500 54000 78500

Closing cash balance 30500 54000 78500 86000

Interpretation: Cash budget is an approach of preparing strategy for analysing business

activities through costing. In this regard, cash flows including inflow and outflows are obtained that

presents expenditures and revenue of firm. However, through the presented cash budget, it is

determined that in July, total cash inflows was 60000, in august it increased by 2000. Further, in

September it enhanced to 68200 and in October, it was 70000. Thus, it has been forecasted through

budget that in further months, company will increase its cash inflow profile that impacts on

economic position of Raddison plc. In addition to this, it sets target to outflow of cash in different

month that is considered as expenditures. However, expected total outflows for July, August,

September and October is 14030, 15000, 11700 and 17500 respectively. Moreover, through this

cash budget decision makers of Raddison plc determines cash balance that presents actual financial

position of organization. Hence, it is required for entity to prepare strategy for obtaining balance of

cash regarding expenditure and revenues. Therefore, effectiveness of firm can be obtained by

preparing budget and following its planning procedure for effective cash balance.

3.2

Calculation for unit costs & Pricing For a single unit for Radission Plc

The costs calculation is performed for 1000 units

Particulars Amount (in £)

Fixed Costs 900000

Variable Costs 800000

Total Costs 1700000

9

Particulars July August September October

Cash inflows

Sales revenue 50000 55500 65000 68000

Other income 10000 6500 3200 2000

Total cash inflow 60000 62000 68200 70000

Cash outflows

Purchase of raw material 2500 3000 2800 5600

Salaries of personnel 6500 7500 5800 6000

Selling and distribution

cost 2400 2500 2600 2700

Other expenses 2630 2000 500 3200

Total cash outflow 14030 15000 11700 17500

Cash deficit / surplus 45970 47000 56500 52500

Opening cash balance 12000 30500 54000 78500

Closing cash balance 30500 54000 78500 86000

Interpretation: Cash budget is an approach of preparing strategy for analysing business

activities through costing. In this regard, cash flows including inflow and outflows are obtained that

presents expenditures and revenue of firm. However, through the presented cash budget, it is

determined that in July, total cash inflows was 60000, in august it increased by 2000. Further, in

September it enhanced to 68200 and in October, it was 70000. Thus, it has been forecasted through

budget that in further months, company will increase its cash inflow profile that impacts on

economic position of Raddison plc. In addition to this, it sets target to outflow of cash in different

month that is considered as expenditures. However, expected total outflows for July, August,

September and October is 14030, 15000, 11700 and 17500 respectively. Moreover, through this

cash budget decision makers of Raddison plc determines cash balance that presents actual financial

position of organization. Hence, it is required for entity to prepare strategy for obtaining balance of

cash regarding expenditure and revenues. Therefore, effectiveness of firm can be obtained by

preparing budget and following its planning procedure for effective cash balance.

3.2

Calculation for unit costs & Pricing For a single unit for Radission Plc

The costs calculation is performed for 1000 units

Particulars Amount (in £)

Fixed Costs 900000

Variable Costs 800000

Total Costs 1700000

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

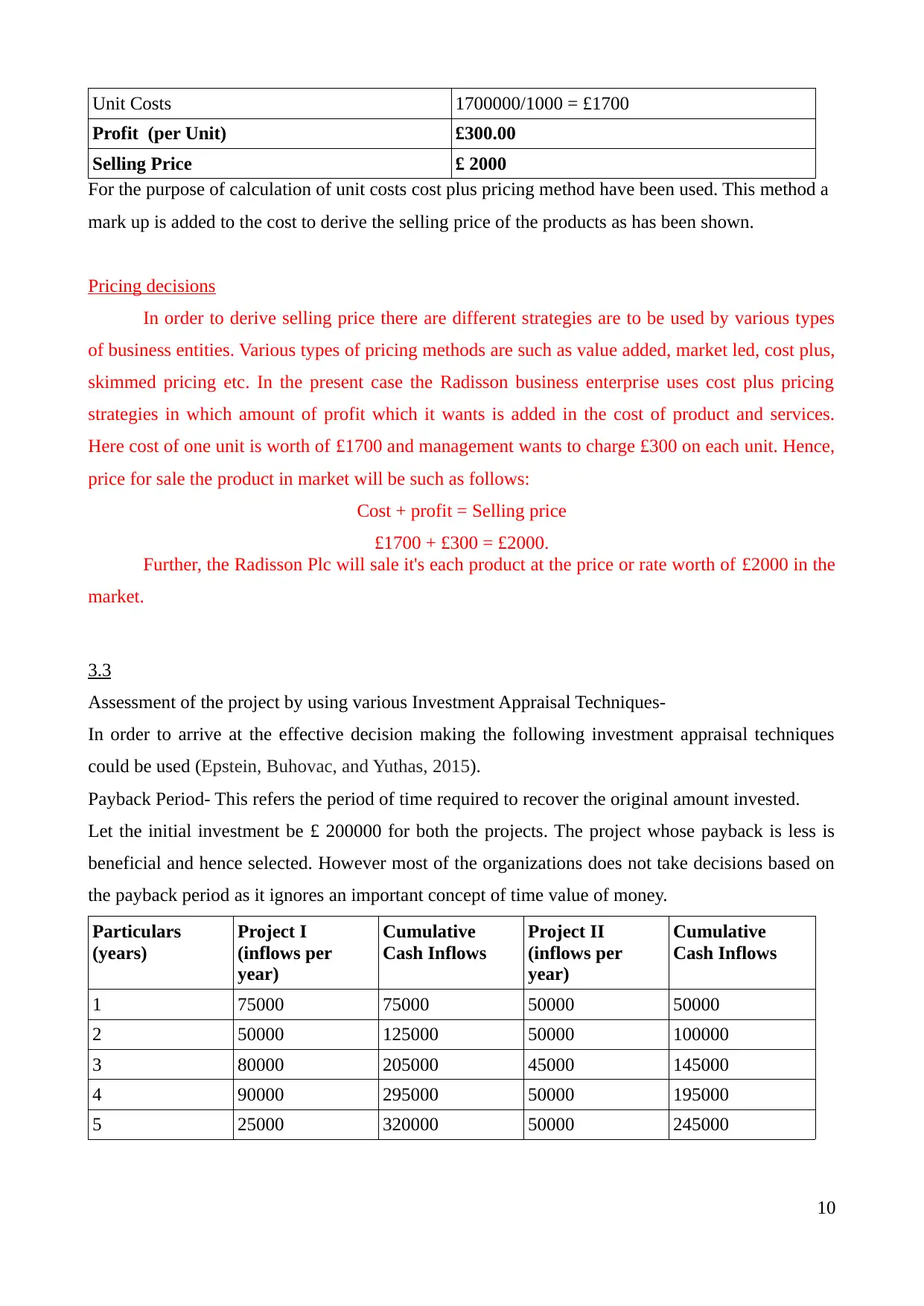

Unit Costs 1700000/1000 = £1700

Profit (per Unit) £300.00

Selling Price £ 2000

For the purpose of calculation of unit costs cost plus pricing method have been used. This method a

mark up is added to the cost to derive the selling price of the products as has been shown.

Pricing decisions

In order to derive selling price there are different strategies are to be used by various types

of business entities. Various types of pricing methods are such as value added, market led, cost plus,

skimmed pricing etc. In the present case the Radisson business enterprise uses cost plus pricing

strategies in which amount of profit which it wants is added in the cost of product and services.

Here cost of one unit is worth of £1700 and management wants to charge £300 on each unit. Hence,

price for sale the product in market will be such as follows:

Cost + profit = Selling price

£1700 + £300 = £2000.

Further, the Radisson Plc will sale it's each product at the price or rate worth of £2000 in the

market.

3.3

Assessment of the project by using various Investment Appraisal Techniques-

In order to arrive at the effective decision making the following investment appraisal techniques

could be used (Epstein, Buhovac, and Yuthas, 2015).

Payback Period- This refers the period of time required to recover the original amount invested.

Let the initial investment be £ 200000 for both the projects. The project whose payback is less is

beneficial and hence selected. However most of the organizations does not take decisions based on

the payback period as it ignores an important concept of time value of money.

Particulars

(years)

Project I

(inflows per

year)

Cumulative

Cash Inflows

Project II

(inflows per

year)

Cumulative

Cash Inflows

1 75000 75000 50000 50000

2 50000 125000 50000 100000

3 80000 205000 45000 145000

4 90000 295000 50000 195000

5 25000 320000 50000 245000

10

Profit (per Unit) £300.00

Selling Price £ 2000

For the purpose of calculation of unit costs cost plus pricing method have been used. This method a

mark up is added to the cost to derive the selling price of the products as has been shown.

Pricing decisions

In order to derive selling price there are different strategies are to be used by various types

of business entities. Various types of pricing methods are such as value added, market led, cost plus,

skimmed pricing etc. In the present case the Radisson business enterprise uses cost plus pricing

strategies in which amount of profit which it wants is added in the cost of product and services.

Here cost of one unit is worth of £1700 and management wants to charge £300 on each unit. Hence,

price for sale the product in market will be such as follows:

Cost + profit = Selling price

£1700 + £300 = £2000.

Further, the Radisson Plc will sale it's each product at the price or rate worth of £2000 in the

market.

3.3

Assessment of the project by using various Investment Appraisal Techniques-

In order to arrive at the effective decision making the following investment appraisal techniques

could be used (Epstein, Buhovac, and Yuthas, 2015).

Payback Period- This refers the period of time required to recover the original amount invested.

Let the initial investment be £ 200000 for both the projects. The project whose payback is less is

beneficial and hence selected. However most of the organizations does not take decisions based on

the payback period as it ignores an important concept of time value of money.

Particulars

(years)

Project I

(inflows per

year)

Cumulative

Cash Inflows

Project II

(inflows per

year)

Cumulative

Cash Inflows

1 75000 75000 50000 50000

2 50000 125000 50000 100000

3 80000 205000 45000 145000

4 90000 295000 50000 195000

5 25000 320000 50000 245000

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

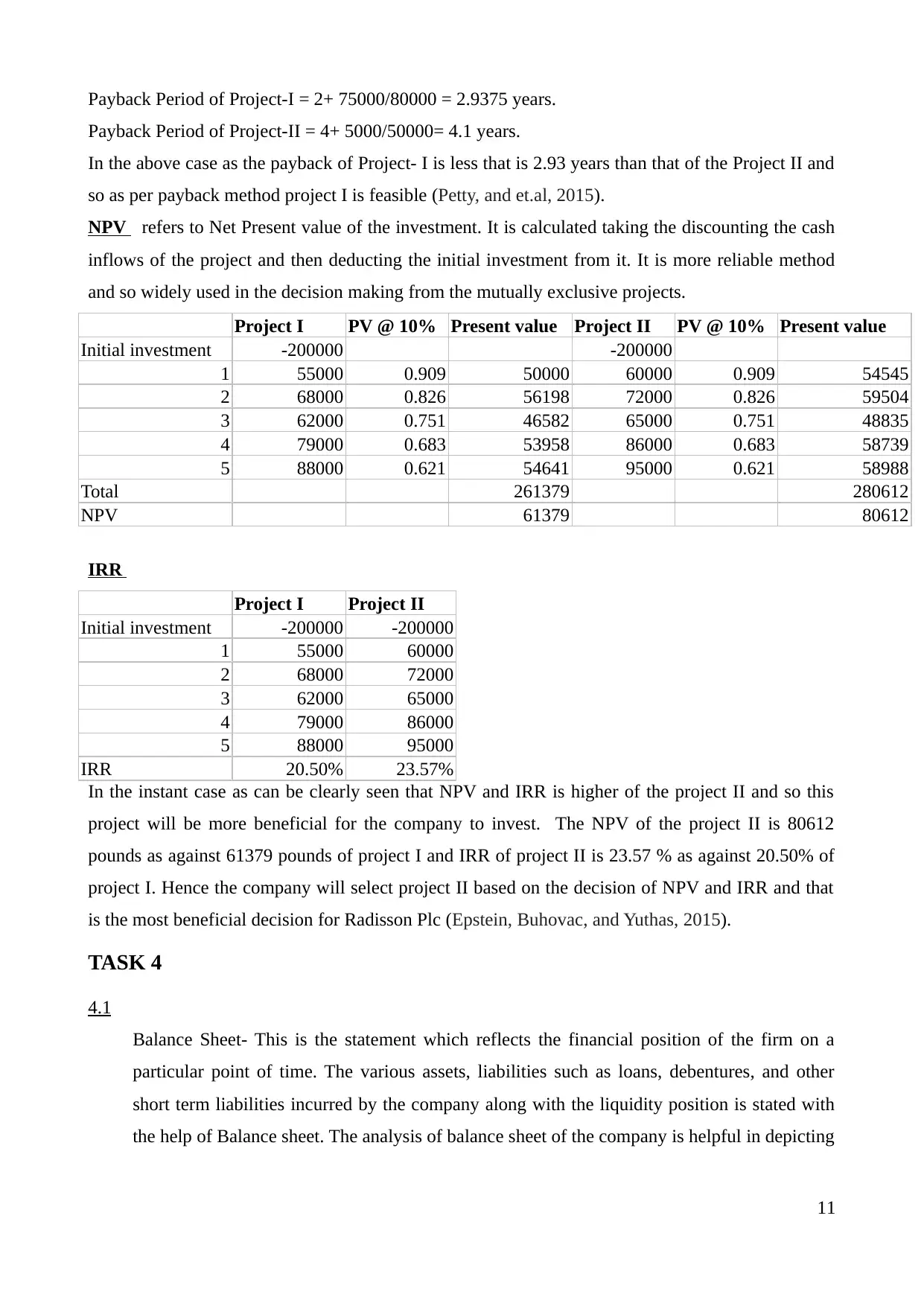

Payback Period of Project-I = 2+ 75000/80000 = 2.9375 years.

Payback Period of Project-II = 4+ 5000/50000= 4.1 years.

In the above case as the payback of Project- I is less that is 2.93 years than that of the Project II and

so as per payback method project I is feasible (Petty, and et.al, 2015).

NPV refers to Net Present value of the investment. It is calculated taking the discounting the cash

inflows of the project and then deducting the initial investment from it. It is more reliable method

and so widely used in the decision making from the mutually exclusive projects.

Project I PV @ 10% Present value Project II PV @ 10% Present value

Initial investment -200000 -200000

1 55000 0.909 50000 60000 0.909 54545

2 68000 0.826 56198 72000 0.826 59504

3 62000 0.751 46582 65000 0.751 48835

4 79000 0.683 53958 86000 0.683 58739

5 88000 0.621 54641 95000 0.621 58988

Total 261379 280612

NPV 61379 80612

IRR

Project I Project II

Initial investment -200000 -200000

1 55000 60000

2 68000 72000

3 62000 65000

4 79000 86000

5 88000 95000

IRR 20.50% 23.57%

In the instant case as can be clearly seen that NPV and IRR is higher of the project II and so this

project will be more beneficial for the company to invest. The NPV of the project II is 80612

pounds as against 61379 pounds of project I and IRR of project II is 23.57 % as against 20.50% of

project I. Hence the company will select project II based on the decision of NPV and IRR and that

is the most beneficial decision for Radisson Plc (Epstein, Buhovac, and Yuthas, 2015).

TASK 4

4.1

Balance Sheet- This is the statement which reflects the financial position of the firm on a

particular point of time. The various assets, liabilities such as loans, debentures, and other

short term liabilities incurred by the company along with the liquidity position is stated with

the help of Balance sheet. The analysis of balance sheet of the company is helpful in depicting

11

Payback Period of Project-II = 4+ 5000/50000= 4.1 years.

In the above case as the payback of Project- I is less that is 2.93 years than that of the Project II and

so as per payback method project I is feasible (Petty, and et.al, 2015).

NPV refers to Net Present value of the investment. It is calculated taking the discounting the cash

inflows of the project and then deducting the initial investment from it. It is more reliable method

and so widely used in the decision making from the mutually exclusive projects.

Project I PV @ 10% Present value Project II PV @ 10% Present value

Initial investment -200000 -200000

1 55000 0.909 50000 60000 0.909 54545

2 68000 0.826 56198 72000 0.826 59504

3 62000 0.751 46582 65000 0.751 48835

4 79000 0.683 53958 86000 0.683 58739

5 88000 0.621 54641 95000 0.621 58988

Total 261379 280612

NPV 61379 80612

IRR

Project I Project II

Initial investment -200000 -200000

1 55000 60000

2 68000 72000

3 62000 65000

4 79000 86000

5 88000 95000

IRR 20.50% 23.57%

In the instant case as can be clearly seen that NPV and IRR is higher of the project II and so this

project will be more beneficial for the company to invest. The NPV of the project II is 80612

pounds as against 61379 pounds of project I and IRR of project II is 23.57 % as against 20.50% of

project I. Hence the company will select project II based on the decision of NPV and IRR and that

is the most beneficial decision for Radisson Plc (Epstein, Buhovac, and Yuthas, 2015).

TASK 4

4.1

Balance Sheet- This is the statement which reflects the financial position of the firm on a

particular point of time. The various assets, liabilities such as loans, debentures, and other

short term liabilities incurred by the company along with the liquidity position is stated with

the help of Balance sheet. The analysis of balance sheet of the company is helpful in depicting

11

the financial status of the company. Hence in order to analyze the company’s standing

Balance sheet is extremely important.

Profit & Loss Statement- This statement presents the revenues earned by the company in the

particular period. It also depicts the revenues from other income generated from those

activities that are not the normal course of activities. This statement also states the various

expenditures incurred by the company for earning the revenues. Hence this statement is

extremely important for the purpose of analyzing the various expenditures whether direct or

indirect. Thus matching of the revenues can be made with the respective incomes and several

controls can be implemented for controlling the expenses (The Basics of Fiancial

Management, 2016).

Cash Flows Statement- This statement shows the movement of cash flows in various activities

that are operating, financing and investing activities. By the analysis of cash flow statement

one is able to view the movement of cash in the various activities and implement effective

controls for reduction of wasteful expenses. Also the cash inflows are analyzed and overall

liquidity position of the company can be predicted.

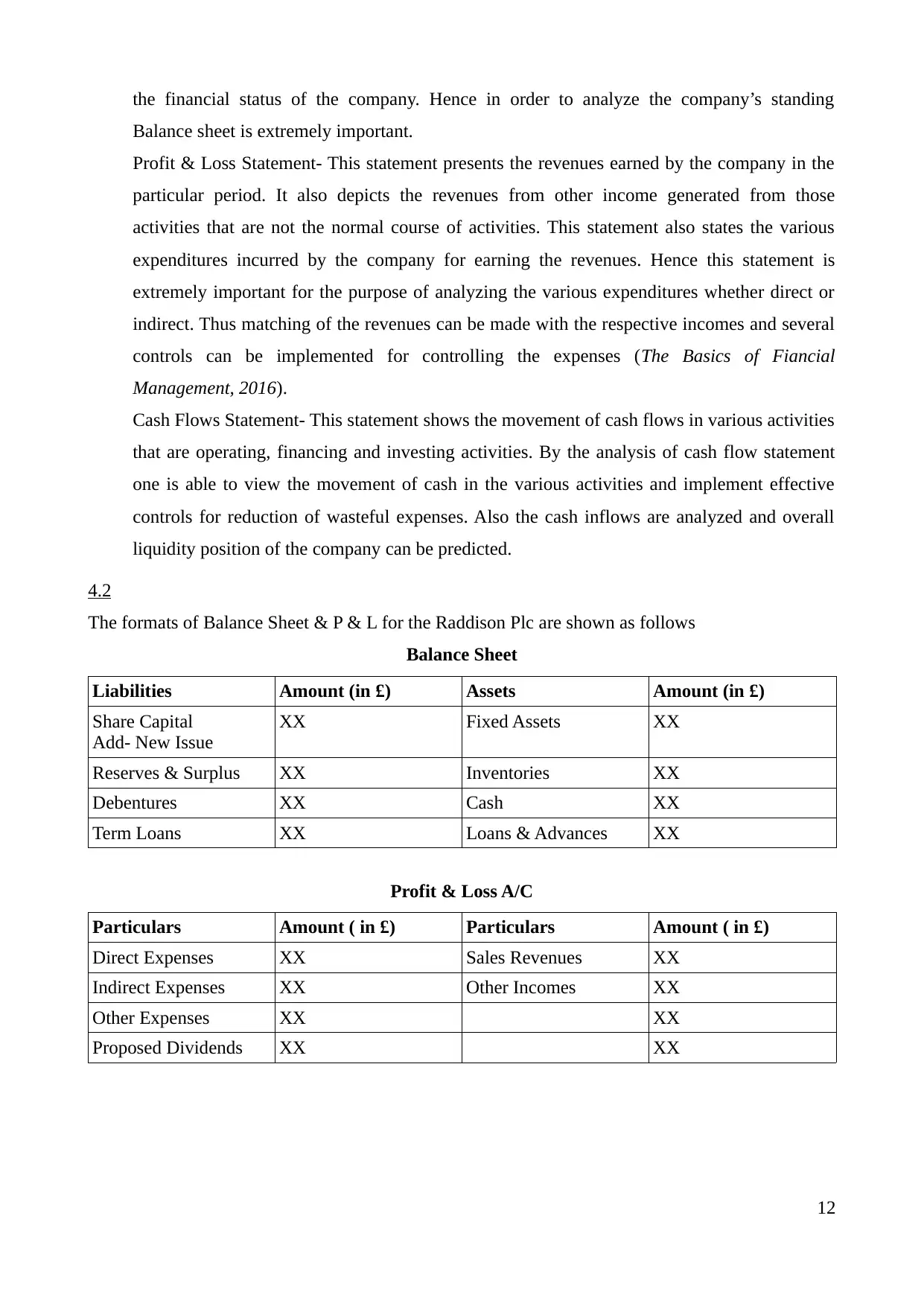

4.2

The formats of Balance Sheet & P & L for the Raddison Plc are shown as follows

Balance Sheet

Liabilities Amount (in £) Assets Amount (in £)

Share Capital

Add- New Issue

XX Fixed Assets XX

Reserves & Surplus XX Inventories XX

Debentures XX Cash XX

Term Loans XX Loans & Advances XX

Profit & Loss A/C

Particulars Amount ( in £) Particulars Amount ( in £)

Direct Expenses XX Sales Revenues XX

Indirect Expenses XX Other Incomes XX

Other Expenses XX XX

Proposed Dividends XX XX

12

Balance sheet is extremely important.

Profit & Loss Statement- This statement presents the revenues earned by the company in the

particular period. It also depicts the revenues from other income generated from those

activities that are not the normal course of activities. This statement also states the various

expenditures incurred by the company for earning the revenues. Hence this statement is

extremely important for the purpose of analyzing the various expenditures whether direct or

indirect. Thus matching of the revenues can be made with the respective incomes and several

controls can be implemented for controlling the expenses (The Basics of Fiancial

Management, 2016).

Cash Flows Statement- This statement shows the movement of cash flows in various activities

that are operating, financing and investing activities. By the analysis of cash flow statement

one is able to view the movement of cash in the various activities and implement effective

controls for reduction of wasteful expenses. Also the cash inflows are analyzed and overall

liquidity position of the company can be predicted.

4.2

The formats of Balance Sheet & P & L for the Raddison Plc are shown as follows

Balance Sheet

Liabilities Amount (in £) Assets Amount (in £)

Share Capital

Add- New Issue

XX Fixed Assets XX

Reserves & Surplus XX Inventories XX

Debentures XX Cash XX

Term Loans XX Loans & Advances XX

Profit & Loss A/C

Particulars Amount ( in £) Particulars Amount ( in £)

Direct Expenses XX Sales Revenues XX

Indirect Expenses XX Other Incomes XX

Other Expenses XX XX

Proposed Dividends XX XX

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Companies- In case of companies they are required to prepare Balance Sheet, Profit & Loss

Statement for the period, Cash Flow Statement, and statement of Equity along with the

explanatory notes as required by the governing legislature that is Companies Act 2006.

Hence the companies are mandatorily required to maintain and present such financial

statements to its stakeholders as are required by the Act applicable (Petty, and et.al, 2015).

Sole Proprietorships- There is no mandatory requirement to be complied by the sole traders.

That is they can maintain such financial statement as they may consider necessary to assess

their income and losses properly. However there is no such mandatory requirement to

maintain any of the financial statement by the governing legislation (Kaplan and Atkinson,

2015).

Partnerships- The partnerships concerns are required to follow the Partnerships Act and

prepare those financial statements as are necessary to assess the income and losses, and

which are required to be maintained by the Partnership Act.

4.3

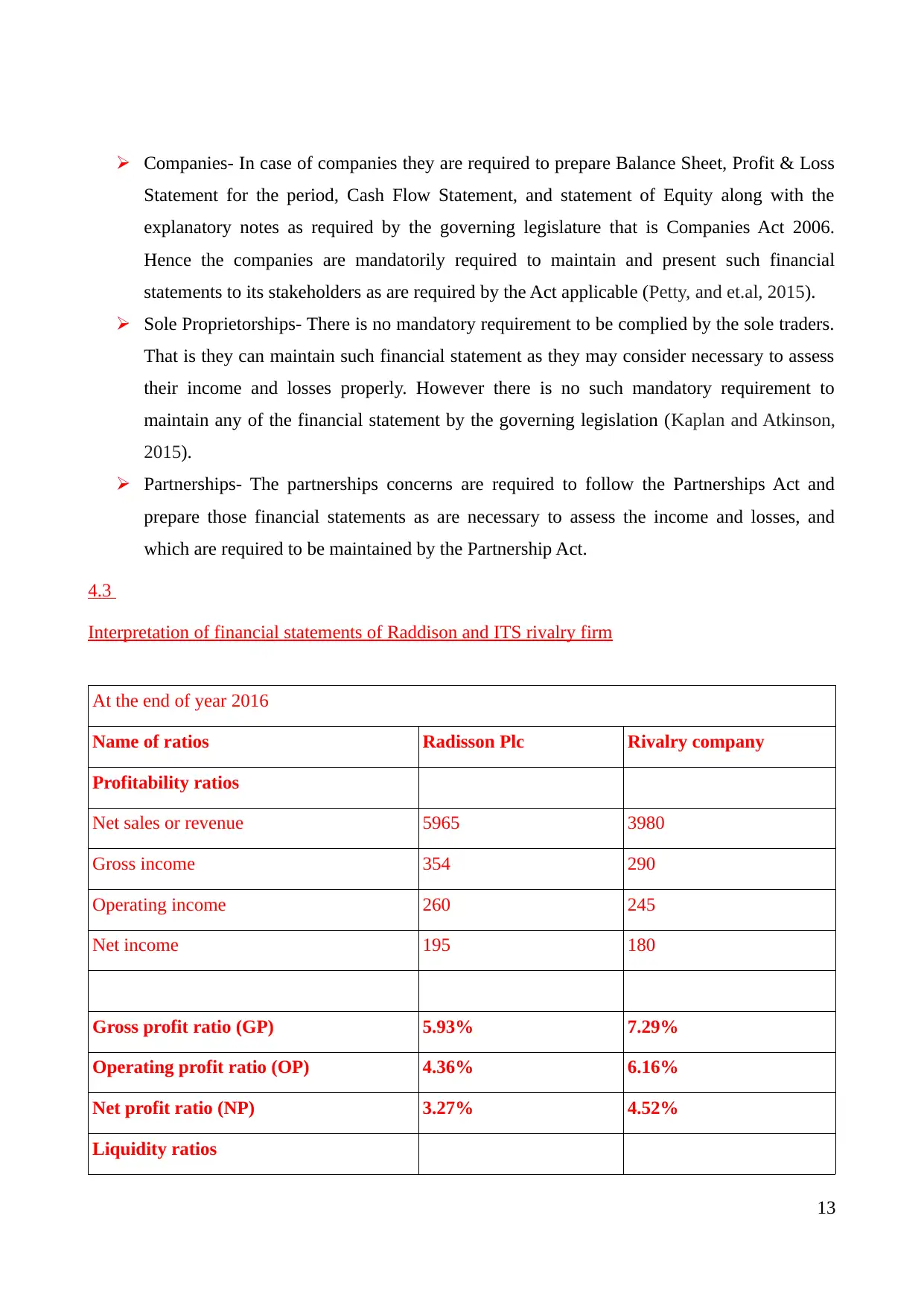

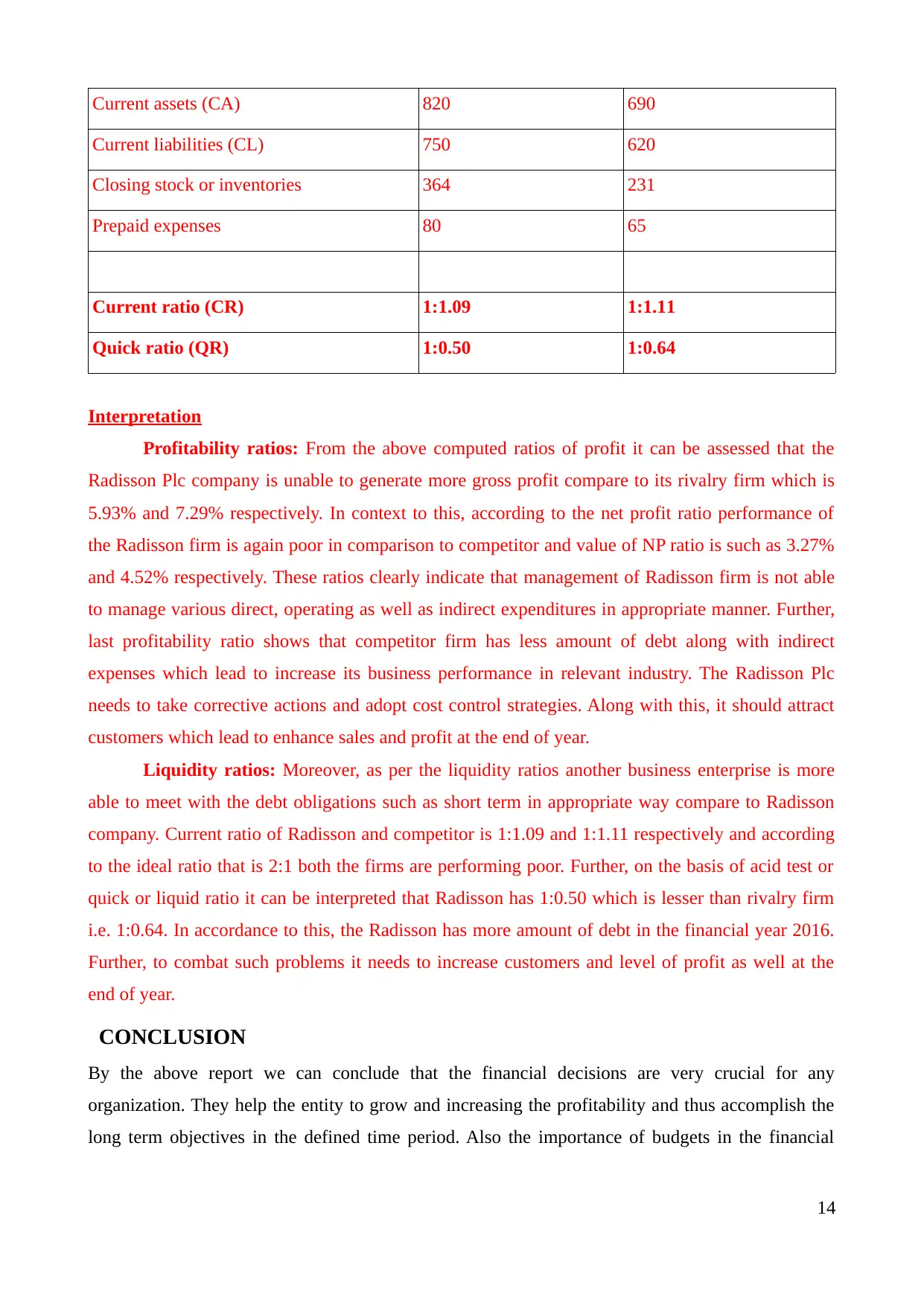

Interpretation of financial statements of Raddison and ITS rivalry firm

At the end of year 2016

Name of ratios Radisson Plc Rivalry company

Profitability ratios

Net sales or revenue 5965 3980

Gross income 354 290

Operating income 260 245

Net income 195 180

Gross profit ratio (GP) 5.93% 7.29%

Operating profit ratio (OP) 4.36% 6.16%

Net profit ratio (NP) 3.27% 4.52%

Liquidity ratios

13

Statement for the period, Cash Flow Statement, and statement of Equity along with the

explanatory notes as required by the governing legislature that is Companies Act 2006.

Hence the companies are mandatorily required to maintain and present such financial

statements to its stakeholders as are required by the Act applicable (Petty, and et.al, 2015).

Sole Proprietorships- There is no mandatory requirement to be complied by the sole traders.

That is they can maintain such financial statement as they may consider necessary to assess

their income and losses properly. However there is no such mandatory requirement to

maintain any of the financial statement by the governing legislation (Kaplan and Atkinson,

2015).

Partnerships- The partnerships concerns are required to follow the Partnerships Act and

prepare those financial statements as are necessary to assess the income and losses, and

which are required to be maintained by the Partnership Act.

4.3

Interpretation of financial statements of Raddison and ITS rivalry firm

At the end of year 2016

Name of ratios Radisson Plc Rivalry company

Profitability ratios

Net sales or revenue 5965 3980

Gross income 354 290

Operating income 260 245

Net income 195 180

Gross profit ratio (GP) 5.93% 7.29%

Operating profit ratio (OP) 4.36% 6.16%

Net profit ratio (NP) 3.27% 4.52%

Liquidity ratios

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Current assets (CA) 820 690

Current liabilities (CL) 750 620

Closing stock or inventories 364 231

Prepaid expenses 80 65

Current ratio (CR) 1:1.09 1:1.11

Quick ratio (QR) 1:0.50 1:0.64

Interpretation

Profitability ratios: From the above computed ratios of profit it can be assessed that the

Radisson Plc company is unable to generate more gross profit compare to its rivalry firm which is

5.93% and 7.29% respectively. In context to this, according to the net profit ratio performance of

the Radisson firm is again poor in comparison to competitor and value of NP ratio is such as 3.27%

and 4.52% respectively. These ratios clearly indicate that management of Radisson firm is not able

to manage various direct, operating as well as indirect expenditures in appropriate manner. Further,

last profitability ratio shows that competitor firm has less amount of debt along with indirect

expenses which lead to increase its business performance in relevant industry. The Radisson Plc

needs to take corrective actions and adopt cost control strategies. Along with this, it should attract

customers which lead to enhance sales and profit at the end of year.

Liquidity ratios: Moreover, as per the liquidity ratios another business enterprise is more

able to meet with the debt obligations such as short term in appropriate way compare to Radisson

company. Current ratio of Radisson and competitor is 1:1.09 and 1:1.11 respectively and according

to the ideal ratio that is 2:1 both the firms are performing poor. Further, on the basis of acid test or

quick or liquid ratio it can be interpreted that Radisson has 1:0.50 which is lesser than rivalry firm

i.e. 1:0.64. In accordance to this, the Radisson has more amount of debt in the financial year 2016.

Further, to combat such problems it needs to increase customers and level of profit as well at the

end of year.

CONCLUSION

By the above report we can conclude that the financial decisions are very crucial for any

organization. They help the entity to grow and increasing the profitability and thus accomplish the

long term objectives in the defined time period. Also the importance of budgets in the financial

14

Current liabilities (CL) 750 620

Closing stock or inventories 364 231

Prepaid expenses 80 65

Current ratio (CR) 1:1.09 1:1.11

Quick ratio (QR) 1:0.50 1:0.64

Interpretation

Profitability ratios: From the above computed ratios of profit it can be assessed that the

Radisson Plc company is unable to generate more gross profit compare to its rivalry firm which is

5.93% and 7.29% respectively. In context to this, according to the net profit ratio performance of

the Radisson firm is again poor in comparison to competitor and value of NP ratio is such as 3.27%

and 4.52% respectively. These ratios clearly indicate that management of Radisson firm is not able

to manage various direct, operating as well as indirect expenditures in appropriate manner. Further,

last profitability ratio shows that competitor firm has less amount of debt along with indirect

expenses which lead to increase its business performance in relevant industry. The Radisson Plc

needs to take corrective actions and adopt cost control strategies. Along with this, it should attract

customers which lead to enhance sales and profit at the end of year.

Liquidity ratios: Moreover, as per the liquidity ratios another business enterprise is more

able to meet with the debt obligations such as short term in appropriate way compare to Radisson

company. Current ratio of Radisson and competitor is 1:1.09 and 1:1.11 respectively and according

to the ideal ratio that is 2:1 both the firms are performing poor. Further, on the basis of acid test or

quick or liquid ratio it can be interpreted that Radisson has 1:0.50 which is lesser than rivalry firm

i.e. 1:0.64. In accordance to this, the Radisson has more amount of debt in the financial year 2016.

Further, to combat such problems it needs to increase customers and level of profit as well at the

end of year.

CONCLUSION

By the above report we can conclude that the financial decisions are very crucial for any

organization. They help the entity to grow and increasing the profitability and thus accomplish the

long term objectives in the defined time period. Also the importance of budgets in the financial

14

planning is realized. Moreover the financial statements required to be prepared by the various

concerns are analyzed and described along with their importance.

15

concerns are analyzed and described along with their importance.

15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Finkler, S. A. and et. al., 2016. Financial management for public, health, and not-for-profit

organizations. CQ Press.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Post, C. and Byron, K., 2015. Women on boards and firm financial performance: A meta-

analysis. Academy of Management Journal, 58(5), pp.1546-1571.

McKinney, J.B., 2015. Effective financial management in public and nonprofit agencies. ABC-CLIO.

Brush, C.G., Edelman, L.F. and Manolova, T., 2015. The impact of resources on small firm

internationalization. Journal of Small Business Strategy, 13(1), pp.1-17.

Valackiene, A., 2015. Theoretical Model of Employee Social Identification in Organization Managing

Crisis Situations. Engineering Economics, 64(4).

Maxwell, S.L., Rhodes, J.R., Runge, M.C., Possingham, H.P., Ng, C.F. and McDonald‐Madden, E.,

2015. How much is new information worth? Evaluating the financial benefit of resolving

management uncertainty. Journal of Applied Ecology, 52(1), pp.12-20.

Petty, J.W, and et.al, 2015. Financial management: Principles and applications. Pearson Higher

Education AU.

Epstein, M.J., Buhovac, A.R. and Yuthas, K., 2015. Managing social, environmental and financial

performance simultaneously. Long Range Planning, 48(1), pp.35-45.

Mayo, A., 2016. Human resources or human capital?: managing people as assets. Routledge.

Johnston, M.W. and Marshall, G.W., 2016. Sales force management: Leadership, innovation,

technology. Routledge.

Monczka, R.M., Handfield, R.B., Giunipero, L.C. and Patterson, J.L., 2015. Purchasing and supply

chain management. Cengage Learning.

Savino, M.M. and Batbaatar, E., 2015. Investigating the resources for Integrated Management

Systems within resource-based and contingency perspective in manufacturing firms. Journal of

Cleaner Production, 104, pp.392-402.

Yuan, L., Qian, X. and Pangarkar, N., 2016. Market Timing and Internationalization Decisions: A

Contingency Perspective. Journal of Management Studies.

Li. P.Y, 2016. The impact of the top management teams’ knowledge and experience on strategic

decisions and performance. Journal of Management & Organization, pp.1-20.

[Online]

Sources of Finance, 2016. [Online]. Available through: <http://www.mbaskool.com/business-

concepts/finance-accounting-economics-terms/7392-sources-of-finance.html>. [Accessed on

14th December 2016].

16

Books and Journals

Finkler, S. A. and et. al., 2016. Financial management for public, health, and not-for-profit

organizations. CQ Press.

Kaplan, R. S. and Atkinson, A. A., 2015. Advanced management accounting. PHI Learning.

Post, C. and Byron, K., 2015. Women on boards and firm financial performance: A meta-

analysis. Academy of Management Journal, 58(5), pp.1546-1571.

McKinney, J.B., 2015. Effective financial management in public and nonprofit agencies. ABC-CLIO.

Brush, C.G., Edelman, L.F. and Manolova, T., 2015. The impact of resources on small firm

internationalization. Journal of Small Business Strategy, 13(1), pp.1-17.

Valackiene, A., 2015. Theoretical Model of Employee Social Identification in Organization Managing

Crisis Situations. Engineering Economics, 64(4).

Maxwell, S.L., Rhodes, J.R., Runge, M.C., Possingham, H.P., Ng, C.F. and McDonald‐Madden, E.,

2015. How much is new information worth? Evaluating the financial benefit of resolving

management uncertainty. Journal of Applied Ecology, 52(1), pp.12-20.

Petty, J.W, and et.al, 2015. Financial management: Principles and applications. Pearson Higher

Education AU.

Epstein, M.J., Buhovac, A.R. and Yuthas, K., 2015. Managing social, environmental and financial

performance simultaneously. Long Range Planning, 48(1), pp.35-45.

Mayo, A., 2016. Human resources or human capital?: managing people as assets. Routledge.

Johnston, M.W. and Marshall, G.W., 2016. Sales force management: Leadership, innovation,

technology. Routledge.

Monczka, R.M., Handfield, R.B., Giunipero, L.C. and Patterson, J.L., 2015. Purchasing and supply

chain management. Cengage Learning.

Savino, M.M. and Batbaatar, E., 2015. Investigating the resources for Integrated Management

Systems within resource-based and contingency perspective in manufacturing firms. Journal of

Cleaner Production, 104, pp.392-402.

Yuan, L., Qian, X. and Pangarkar, N., 2016. Market Timing and Internationalization Decisions: A

Contingency Perspective. Journal of Management Studies.

Li. P.Y, 2016. The impact of the top management teams’ knowledge and experience on strategic

decisions and performance. Journal of Management & Organization, pp.1-20.

[Online]

Sources of Finance, 2016. [Online]. Available through: <http://www.mbaskool.com/business-

concepts/finance-accounting-economics-terms/7392-sources-of-finance.html>. [Accessed on

14th December 2016].

16

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The Basics of Fiancial Management, 2016. [ONLINE]. Available

through:<https://knowhownonprofit.org/organisation/operations/financial-management/

management>. [Accessed on 14th December 2016].

17

through:<https://knowhownonprofit.org/organisation/operations/financial-management/

management>. [Accessed on 14th December 2016].

17

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.