KPMG Australia: AASB 15 New Revenue Disclosures for Half Year Accounts

VerifiedAdded on 2023/01/18

|8

|1155

|86

Report

AI Summary

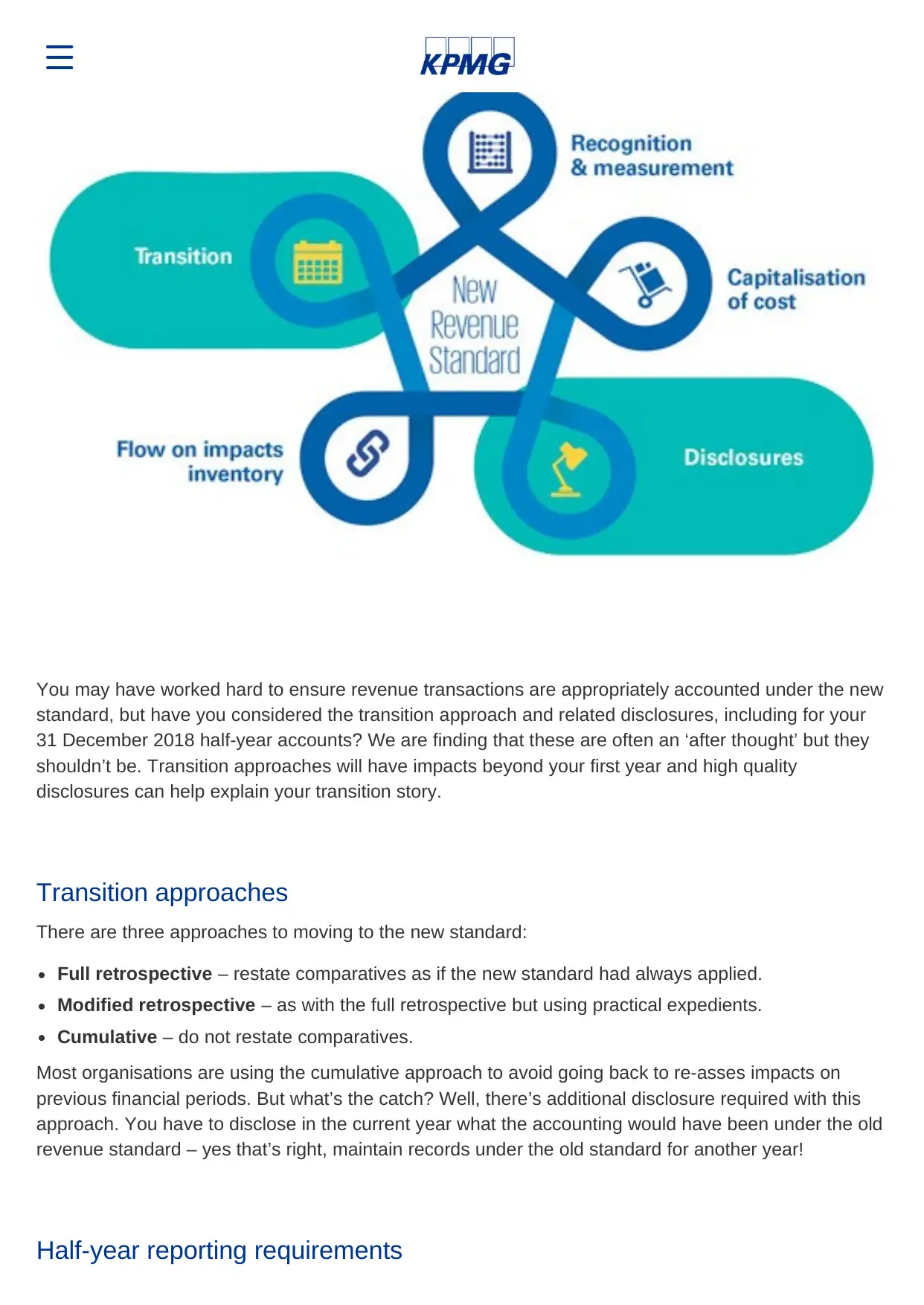

This report, sourced from KPMG Australia, provides a detailed analysis of AASB 15, the new revenue standard, focusing on its implications for financial reporting, particularly for half-year accounts. The report examines various aspects of the standard, including revenue recognition and measurement, capitalization of costs, and the crucial area of disclosures. It highlights the importance of considering transition approaches, such as full retrospective, modified retrospective, and cumulative methods, and their impact on financial statements. The report emphasizes the significance of high-quality disclosures in explaining the transition story to users, especially in the context of half-year reporting requirements. It provides insights into the key areas that should be discussed in half-year accounts, including transition impacts, selected transition approaches, new accounting policies, and meaningful disaggregation of revenue. The report also offers guidance on where to find resources, such as example financial statements, and highlights the role of regulatory bodies like ASIC in monitoring these disclosures.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.