Company Financial Analysis and Capital Structure

VerifiedAdded on 2020/04/15

|16

|2454

|41

AI Summary

This assignment requires a detailed analysis of a company's financial health, focusing on its cash flow, profitability, and the appropriate balance of debt and equity in its capital structure. The report delves into key financial metrics, evaluates the company's competitive position, and suggests strategies for maximizing returns through investment decisions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

By student name

Professor

University

Date: 16 November 2017.

1 | P a g e

By student name

Professor

University

Date: 16 November 2017.

1 | P a g e

2

Executive Summary

In the given project, a hypothetical company has been chosen to show how the financial planning

can be done using the balance sheet analysis, the profit and loss statement, the cash flow

statement and through the use of optimum capital structure, low interest rates and correct

proportion of debt in the capital structure. In the give case study, the person has just graduated

from the college and has ventured into the business. Further analysis has been done using the

past and future estimated data a bout how a change in the single variable can bring about a

change in other factors.

2 | P a g e

Executive Summary

In the given project, a hypothetical company has been chosen to show how the financial planning

can be done using the balance sheet analysis, the profit and loss statement, the cash flow

statement and through the use of optimum capital structure, low interest rates and correct

proportion of debt in the capital structure. In the give case study, the person has just graduated

from the college and has ventured into the business. Further analysis has been done using the

past and future estimated data a bout how a change in the single variable can bring about a

change in other factors.

2 | P a g e

3

Contents

Executive Summary.………………………………………………………………………………….......2

Introduction..…………………………………………………………………………………………….......4

Net Worth Statement & its analysis ..…………………………………………………..............5

Cash Flow Statement, its analysis ………………………………………………………..............7

Debt reduction Goal............………………………………………………………………..............9

Savings Goal…….…….............………………………………………………………………..............10

Personal motivation of the client………………………………………………………..............11

Time Value of Money...........………………………………………………………………..............11

Recommendations...............………………………………………………………………..............13

Conclusion…………….............………………………………………………………………...............14

Refrences.....……………………………………………………………….......................................15

3 | P a g e

Contents

Executive Summary.………………………………………………………………………………….......2

Introduction..…………………………………………………………………………………………….......4

Net Worth Statement & its analysis ..…………………………………………………..............5

Cash Flow Statement, its analysis ………………………………………………………..............7

Debt reduction Goal............………………………………………………………………..............9

Savings Goal…….…….............………………………………………………………………..............10

Personal motivation of the client………………………………………………………..............11

Time Value of Money...........………………………………………………………………..............11

Recommendations...............………………………………………………………………..............13

Conclusion…………….............………………………………………………………………...............14

Refrences.....……………………………………………………………….......................................15

3 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

Introduction

The company chosen would be one of the telecom company and listed on Stock Exchange

named XYZ company limited. The debt break up and the share valuation has also been covered

to give the in depth view of the company using the financial performance analysis (Alexander,

2016). It deals in voice, video, internet, network, media products and other such services.

4 | P a g e

Introduction

The company chosen would be one of the telecom company and listed on Stock Exchange

named XYZ company limited. The debt break up and the share valuation has also been covered

to give the in depth view of the company using the financial performance analysis (Alexander,

2016). It deals in voice, video, internet, network, media products and other such services.

4 | P a g e

5

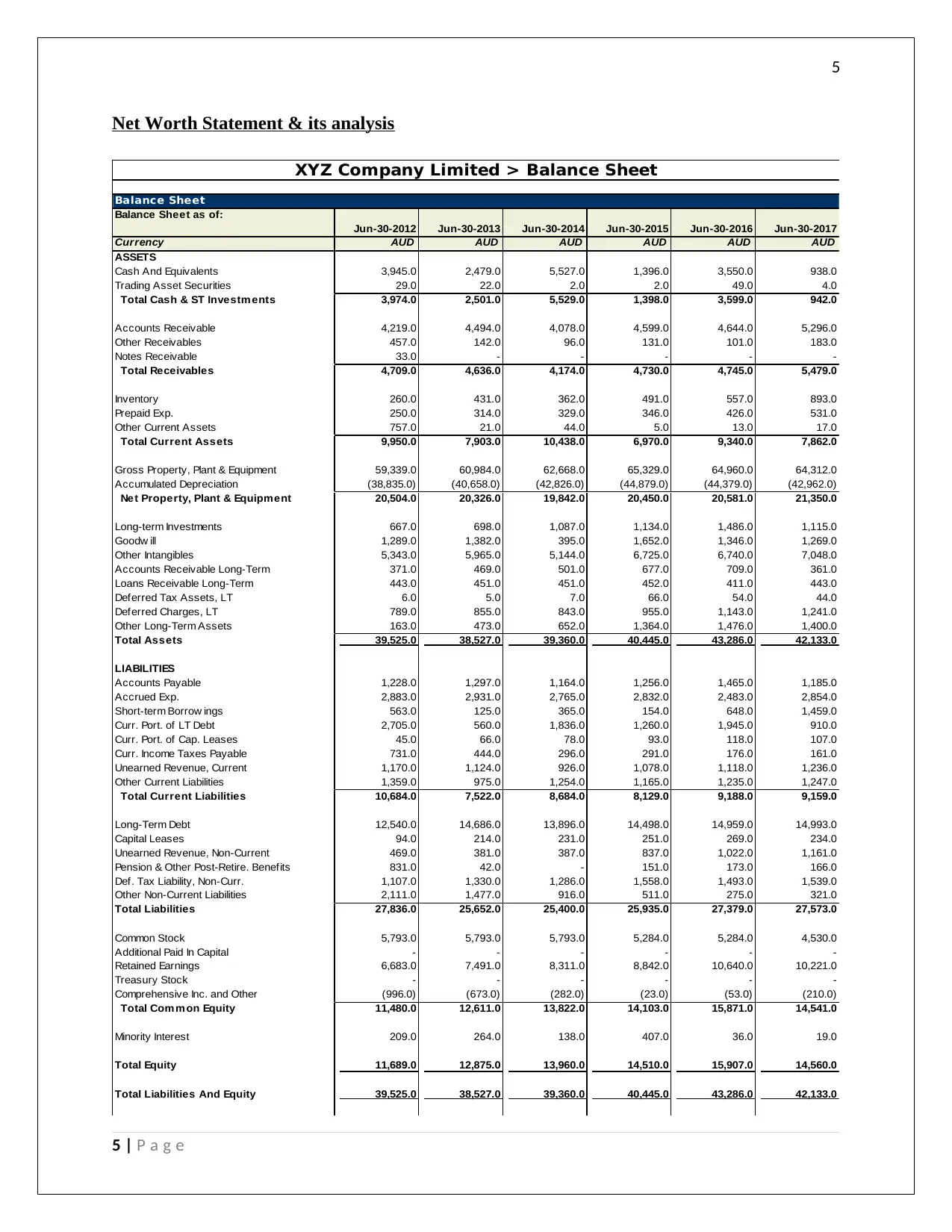

Net Worth Statement & its analysis

Balance Sheet

Balance Sheet as of:

Jun-30-2012 Jun-30-2013 Jun-30-2014 Jun-30-2015 Jun-30-2016 Jun-30-2017

Currency AUD AUD AUD AUD AUD AUD

ASSETS

Cash And Equivalents 3,945.0 2,479.0 5,527.0 1,396.0 3,550.0 938.0

Trading Asset Securities 29.0 22.0 2.0 2.0 49.0 4.0

Total Cash & ST Investm ents 3,974.0 2,501.0 5,529.0 1,398.0 3,599.0 942.0

Accounts Receivable 4,219.0 4,494.0 4,078.0 4,599.0 4,644.0 5,296.0

Other Receivables 457.0 142.0 96.0 131.0 101.0 183.0

Notes Receivable 33.0 - - - - -

Total Receivables 4,709.0 4,636.0 4,174.0 4,730.0 4,745.0 5,479.0

Inventory 260.0 431.0 362.0 491.0 557.0 893.0

Prepaid Exp. 250.0 314.0 329.0 346.0 426.0 531.0

Other Current Assets 757.0 21.0 44.0 5.0 13.0 17.0

Total Current Assets 9,950.0 7,903.0 10,438.0 6,970.0 9,340.0 7,862.0

Gross Property, Plant & Equipment 59,339.0 60,984.0 62,668.0 65,329.0 64,960.0 64,312.0

Accumulated Depreciation (38,835.0) (40,658.0) (42,826.0) (44,879.0) (44,379.0) (42,962.0)

Net Property, Plant & Equipment 20,504.0 20,326.0 19,842.0 20,450.0 20,581.0 21,350.0

Long-term Investments 667.0 698.0 1,087.0 1,134.0 1,486.0 1,115.0

Goodw ill 1,289.0 1,382.0 395.0 1,652.0 1,346.0 1,269.0

Other Intangibles 5,343.0 5,965.0 5,144.0 6,725.0 6,740.0 7,048.0

Accounts Receivable Long-Term 371.0 469.0 501.0 677.0 709.0 361.0

Loans Receivable Long-Term 443.0 451.0 451.0 452.0 411.0 443.0

Deferred Tax Assets, LT 6.0 5.0 7.0 66.0 54.0 44.0

Deferred Charges, LT 789.0 855.0 843.0 955.0 1,143.0 1,241.0

Other Long-Term Assets 163.0 473.0 652.0 1,364.0 1,476.0 1,400.0

Total Assets 39,525.0 38,527.0 39,360.0 40,445.0 43,286.0 42,133.0

LIABILITIES

Accounts Payable 1,228.0 1,297.0 1,164.0 1,256.0 1,465.0 1,185.0

Accrued Exp. 2,883.0 2,931.0 2,765.0 2,832.0 2,483.0 2,854.0

Short-term Borrow ings 563.0 125.0 365.0 154.0 648.0 1,459.0

Curr. Port. of LT Debt 2,705.0 560.0 1,836.0 1,260.0 1,945.0 910.0

Curr. Port. of Cap. Leases 45.0 66.0 78.0 93.0 118.0 107.0

Curr. Income Taxes Payable 731.0 444.0 296.0 291.0 176.0 161.0

Unearned Revenue, Current 1,170.0 1,124.0 926.0 1,078.0 1,118.0 1,236.0

Other Current Liabilities 1,359.0 975.0 1,254.0 1,165.0 1,235.0 1,247.0

Total Current Liabilities 10,684.0 7,522.0 8,684.0 8,129.0 9,188.0 9,159.0

Long-Term Debt 12,540.0 14,686.0 13,896.0 14,498.0 14,959.0 14,993.0

Capital Leases 94.0 214.0 231.0 251.0 269.0 234.0

Unearned Revenue, Non-Current 469.0 381.0 387.0 837.0 1,022.0 1,161.0

Pension & Other Post-Retire. Benefits 831.0 42.0 - 151.0 173.0 166.0

Def. Tax Liability, Non-Curr. 1,107.0 1,330.0 1,286.0 1,558.0 1,493.0 1,539.0

Other Non-Current Liabilities 2,111.0 1,477.0 916.0 511.0 275.0 321.0

Total Liabilities 27,836.0 25,652.0 25,400.0 25,935.0 27,379.0 27,573.0

Common Stock 5,793.0 5,793.0 5,793.0 5,284.0 5,284.0 4,530.0

Additional Paid In Capital - - - - - -

Retained Earnings 6,683.0 7,491.0 8,311.0 8,842.0 10,640.0 10,221.0

Treasury Stock - - - - - -

Comprehensive Inc. and Other (996.0) (673.0) (282.0) (23.0) (53.0) (210.0)

Total Com m on Equity 11,480.0 12,611.0 13,822.0 14,103.0 15,871.0 14,541.0

Minority Interest 209.0 264.0 138.0 407.0 36.0 19.0

Total Equity 11,689.0 12,875.0 13,960.0 14,510.0 15,907.0 14,560.0

Total Liabilities And Equity 39,525.0 38,527.0 39,360.0 40,445.0 43,286.0 42,133.0

XYZ Company Limited > Balance Sheet

5 | P a g e

Net Worth Statement & its analysis

Balance Sheet

Balance Sheet as of:

Jun-30-2012 Jun-30-2013 Jun-30-2014 Jun-30-2015 Jun-30-2016 Jun-30-2017

Currency AUD AUD AUD AUD AUD AUD

ASSETS

Cash And Equivalents 3,945.0 2,479.0 5,527.0 1,396.0 3,550.0 938.0

Trading Asset Securities 29.0 22.0 2.0 2.0 49.0 4.0

Total Cash & ST Investm ents 3,974.0 2,501.0 5,529.0 1,398.0 3,599.0 942.0

Accounts Receivable 4,219.0 4,494.0 4,078.0 4,599.0 4,644.0 5,296.0

Other Receivables 457.0 142.0 96.0 131.0 101.0 183.0

Notes Receivable 33.0 - - - - -

Total Receivables 4,709.0 4,636.0 4,174.0 4,730.0 4,745.0 5,479.0

Inventory 260.0 431.0 362.0 491.0 557.0 893.0

Prepaid Exp. 250.0 314.0 329.0 346.0 426.0 531.0

Other Current Assets 757.0 21.0 44.0 5.0 13.0 17.0

Total Current Assets 9,950.0 7,903.0 10,438.0 6,970.0 9,340.0 7,862.0

Gross Property, Plant & Equipment 59,339.0 60,984.0 62,668.0 65,329.0 64,960.0 64,312.0

Accumulated Depreciation (38,835.0) (40,658.0) (42,826.0) (44,879.0) (44,379.0) (42,962.0)

Net Property, Plant & Equipment 20,504.0 20,326.0 19,842.0 20,450.0 20,581.0 21,350.0

Long-term Investments 667.0 698.0 1,087.0 1,134.0 1,486.0 1,115.0

Goodw ill 1,289.0 1,382.0 395.0 1,652.0 1,346.0 1,269.0

Other Intangibles 5,343.0 5,965.0 5,144.0 6,725.0 6,740.0 7,048.0

Accounts Receivable Long-Term 371.0 469.0 501.0 677.0 709.0 361.0

Loans Receivable Long-Term 443.0 451.0 451.0 452.0 411.0 443.0

Deferred Tax Assets, LT 6.0 5.0 7.0 66.0 54.0 44.0

Deferred Charges, LT 789.0 855.0 843.0 955.0 1,143.0 1,241.0

Other Long-Term Assets 163.0 473.0 652.0 1,364.0 1,476.0 1,400.0

Total Assets 39,525.0 38,527.0 39,360.0 40,445.0 43,286.0 42,133.0

LIABILITIES

Accounts Payable 1,228.0 1,297.0 1,164.0 1,256.0 1,465.0 1,185.0

Accrued Exp. 2,883.0 2,931.0 2,765.0 2,832.0 2,483.0 2,854.0

Short-term Borrow ings 563.0 125.0 365.0 154.0 648.0 1,459.0

Curr. Port. of LT Debt 2,705.0 560.0 1,836.0 1,260.0 1,945.0 910.0

Curr. Port. of Cap. Leases 45.0 66.0 78.0 93.0 118.0 107.0

Curr. Income Taxes Payable 731.0 444.0 296.0 291.0 176.0 161.0

Unearned Revenue, Current 1,170.0 1,124.0 926.0 1,078.0 1,118.0 1,236.0

Other Current Liabilities 1,359.0 975.0 1,254.0 1,165.0 1,235.0 1,247.0

Total Current Liabilities 10,684.0 7,522.0 8,684.0 8,129.0 9,188.0 9,159.0

Long-Term Debt 12,540.0 14,686.0 13,896.0 14,498.0 14,959.0 14,993.0

Capital Leases 94.0 214.0 231.0 251.0 269.0 234.0

Unearned Revenue, Non-Current 469.0 381.0 387.0 837.0 1,022.0 1,161.0

Pension & Other Post-Retire. Benefits 831.0 42.0 - 151.0 173.0 166.0

Def. Tax Liability, Non-Curr. 1,107.0 1,330.0 1,286.0 1,558.0 1,493.0 1,539.0

Other Non-Current Liabilities 2,111.0 1,477.0 916.0 511.0 275.0 321.0

Total Liabilities 27,836.0 25,652.0 25,400.0 25,935.0 27,379.0 27,573.0

Common Stock 5,793.0 5,793.0 5,793.0 5,284.0 5,284.0 4,530.0

Additional Paid In Capital - - - - - -

Retained Earnings 6,683.0 7,491.0 8,311.0 8,842.0 10,640.0 10,221.0

Treasury Stock - - - - - -

Comprehensive Inc. and Other (996.0) (673.0) (282.0) (23.0) (53.0) (210.0)

Total Com m on Equity 11,480.0 12,611.0 13,822.0 14,103.0 15,871.0 14,541.0

Minority Interest 209.0 264.0 138.0 407.0 36.0 19.0

Total Equity 11,689.0 12,875.0 13,960.0 14,510.0 15,907.0 14,560.0

Total Liabilities And Equity 39,525.0 38,527.0 39,360.0 40,445.0 43,286.0 42,133.0

XYZ Company Limited > Balance Sheet

5 | P a g e

6

Given above is the net worth statement of XYZ Company Limited for the years 2012 to 2017.

With the use of hypothetical numbers we can see that the on the assets side, the cash and cash

equivalents keeps on decreasing as the company grows in the business because it doesn’t wants

to keep idle cash instead it invests it somewhere like inventory, investments, bank etc. Other

notable current assets include receivables and inventory which too has increased over time with

the growth in business. Talking on the non current assets, the PPE has increased marginally

whereas investments and other long term assets have increased over time (Dichev, 2017). On the

liabilities side, the short term borrowings have increased over time with the growth in business

whereas the trade creditors have remained more or less constant indicating that the business has

maintained good internal control and is paying to creditors on time. On the non current liabilities

side, both the long term borrowings and the equity has increased in the same proportion and has

not increased abruptly maintaining the ideal ratio of 1:1 marginally. Overall, the financial

position of the company appears to be good from the net worth statement of the company, other

factors being constant.

6 | P a g e

Given above is the net worth statement of XYZ Company Limited for the years 2012 to 2017.

With the use of hypothetical numbers we can see that the on the assets side, the cash and cash

equivalents keeps on decreasing as the company grows in the business because it doesn’t wants

to keep idle cash instead it invests it somewhere like inventory, investments, bank etc. Other

notable current assets include receivables and inventory which too has increased over time with

the growth in business. Talking on the non current assets, the PPE has increased marginally

whereas investments and other long term assets have increased over time (Dichev, 2017). On the

liabilities side, the short term borrowings have increased over time with the growth in business

whereas the trade creditors have remained more or less constant indicating that the business has

maintained good internal control and is paying to creditors on time. On the non current liabilities

side, both the long term borrowings and the equity has increased in the same proportion and has

not increased abruptly maintaining the ideal ratio of 1:1 marginally. Overall, the financial

position of the company appears to be good from the net worth statement of the company, other

factors being constant.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

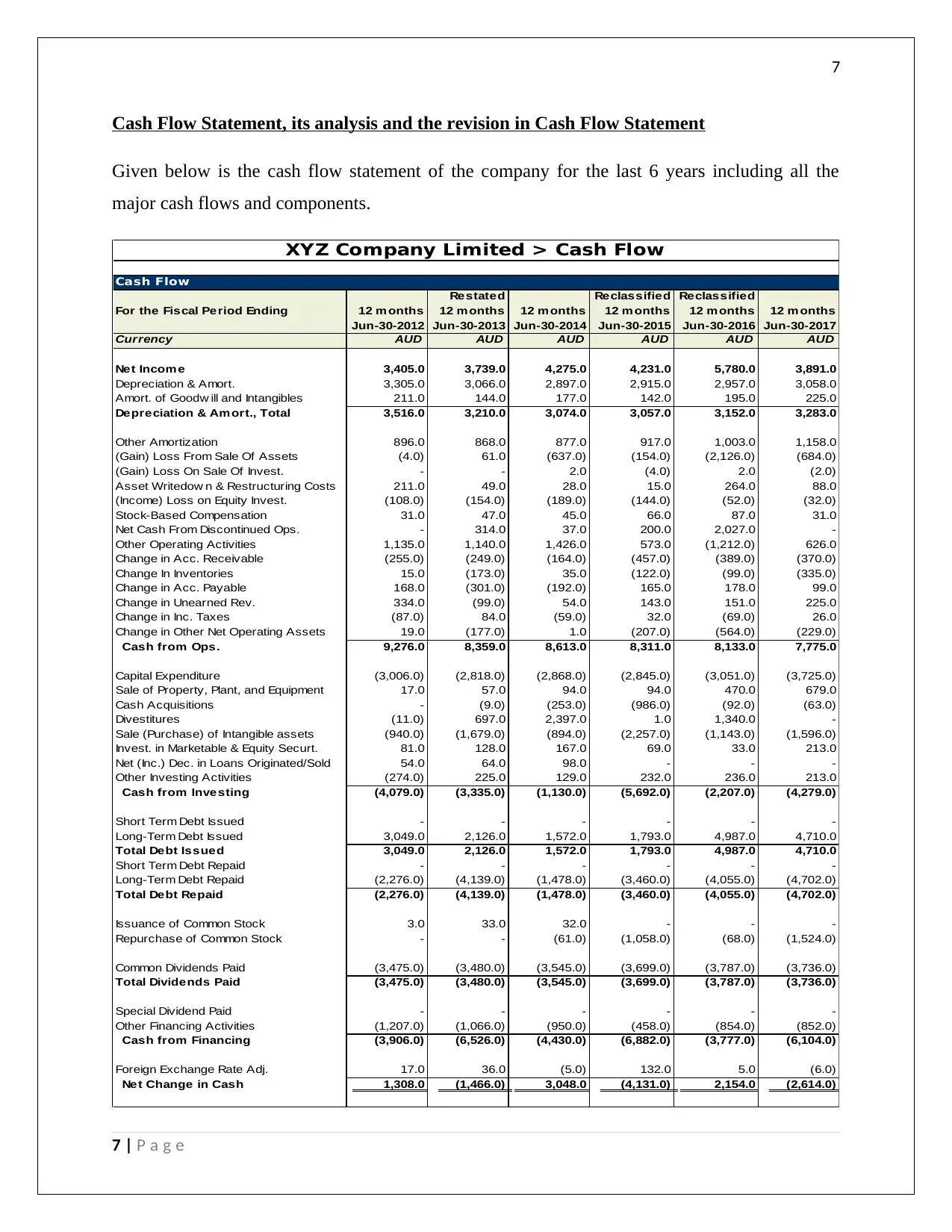

Cash Flow Statement, its analysis and the revision in Cash Flow Statement

Given below is the cash flow statement of the company for the last 6 years including all the

major cash flows and components.

Cash Flow

For the Fiscal Period Ending 12 m onths

Jun-30-2012

Restated

12 m onths

Jun-30-2013

12 m onths

Jun-30-2014

Reclassified

12 m onths

Jun-30-2015

Reclassified

12 m onths

Jun-30-2016

12 m onths

Jun-30-2017

Currency AUD AUD AUD AUD AUD AUD

Net Incom e 3,405.0 3,739.0 4,275.0 4,231.0 5,780.0 3,891.0

Depreciation & Amort. 3,305.0 3,066.0 2,897.0 2,915.0 2,957.0 3,058.0

Amort. of Goodw ill and Intangibles 211.0 144.0 177.0 142.0 195.0 225.0

Depreciation & Am ort., Total 3,516.0 3,210.0 3,074.0 3,057.0 3,152.0 3,283.0

Other Amortization 896.0 868.0 877.0 917.0 1,003.0 1,158.0

(Gain) Loss From Sale Of Assets (4.0) 61.0 (637.0) (154.0) (2,126.0) (684.0)

(Gain) Loss On Sale Of Invest. - - 2.0 (4.0) 2.0 (2.0)

Asset Writedow n & Restructuring Costs 211.0 49.0 28.0 15.0 264.0 88.0

(Income) Loss on Equity Invest. (108.0) (154.0) (189.0) (144.0) (52.0) (32.0)

Stock-Based Compensation 31.0 47.0 45.0 66.0 87.0 31.0

Net Cash From Discontinued Ops. - 314.0 37.0 200.0 2,027.0 -

Other Operating Activities 1,135.0 1,140.0 1,426.0 573.0 (1,212.0) 626.0

Change in Acc. Receivable (255.0) (249.0) (164.0) (457.0) (389.0) (370.0)

Change In Inventories 15.0 (173.0) 35.0 (122.0) (99.0) (335.0)

Change in Acc. Payable 168.0 (301.0) (192.0) 165.0 178.0 99.0

Change in Unearned Rev. 334.0 (99.0) 54.0 143.0 151.0 225.0

Change in Inc. Taxes (87.0) 84.0 (59.0) 32.0 (69.0) 26.0

Change in Other Net Operating Assets 19.0 (177.0) 1.0 (207.0) (564.0) (229.0)

Cash from Ops. 9,276.0 8,359.0 8,613.0 8,311.0 8,133.0 7,775.0

Capital Expenditure (3,006.0) (2,818.0) (2,868.0) (2,845.0) (3,051.0) (3,725.0)

Sale of Property, Plant, and Equipment 17.0 57.0 94.0 94.0 470.0 679.0

Cash Acquisitions - (9.0) (253.0) (986.0) (92.0) (63.0)

Divestitures (11.0) 697.0 2,397.0 1.0 1,340.0 -

Sale (Purchase) of Intangible assets (940.0) (1,679.0) (894.0) (2,257.0) (1,143.0) (1,596.0)

Invest. in Marketable & Equity Securt. 81.0 128.0 167.0 69.0 33.0 213.0

Net (Inc.) Dec. in Loans Originated/Sold 54.0 64.0 98.0 - - -

Other Investing Activities (274.0) 225.0 129.0 232.0 236.0 213.0

Cash from Investing (4,079.0) (3,335.0) (1,130.0) (5,692.0) (2,207.0) (4,279.0)

Short Term Debt Issued - - - - - -

Long-Term Debt Issued 3,049.0 2,126.0 1,572.0 1,793.0 4,987.0 4,710.0

Total Debt Issued 3,049.0 2,126.0 1,572.0 1,793.0 4,987.0 4,710.0

Short Term Debt Repaid - - - - - -

Long-Term Debt Repaid (2,276.0) (4,139.0) (1,478.0) (3,460.0) (4,055.0) (4,702.0)

Total Debt Repaid (2,276.0) (4,139.0) (1,478.0) (3,460.0) (4,055.0) (4,702.0)

Issuance of Common Stock 3.0 33.0 32.0 - - -

Repurchase of Common Stock - - (61.0) (1,058.0) (68.0) (1,524.0)

Common Dividends Paid (3,475.0) (3,480.0) (3,545.0) (3,699.0) (3,787.0) (3,736.0)

Total Dividends Paid (3,475.0) (3,480.0) (3,545.0) (3,699.0) (3,787.0) (3,736.0)

Special Dividend Paid - - - - - -

Other Financing Activities (1,207.0) (1,066.0) (950.0) (458.0) (854.0) (852.0)

Cash from Financing (3,906.0) (6,526.0) (4,430.0) (6,882.0) (3,777.0) (6,104.0)

Foreign Exchange Rate Adj. 17.0 36.0 (5.0) 132.0 5.0 (6.0)

Net Change in Cash 1,308.0 (1,466.0) 3,048.0 (4,131.0) 2,154.0 (2,614.0)

XYZ Company Limited > Cash Flow

7 | P a g e

Cash Flow Statement, its analysis and the revision in Cash Flow Statement

Given below is the cash flow statement of the company for the last 6 years including all the

major cash flows and components.

Cash Flow

For the Fiscal Period Ending 12 m onths

Jun-30-2012

Restated

12 m onths

Jun-30-2013

12 m onths

Jun-30-2014

Reclassified

12 m onths

Jun-30-2015

Reclassified

12 m onths

Jun-30-2016

12 m onths

Jun-30-2017

Currency AUD AUD AUD AUD AUD AUD

Net Incom e 3,405.0 3,739.0 4,275.0 4,231.0 5,780.0 3,891.0

Depreciation & Amort. 3,305.0 3,066.0 2,897.0 2,915.0 2,957.0 3,058.0

Amort. of Goodw ill and Intangibles 211.0 144.0 177.0 142.0 195.0 225.0

Depreciation & Am ort., Total 3,516.0 3,210.0 3,074.0 3,057.0 3,152.0 3,283.0

Other Amortization 896.0 868.0 877.0 917.0 1,003.0 1,158.0

(Gain) Loss From Sale Of Assets (4.0) 61.0 (637.0) (154.0) (2,126.0) (684.0)

(Gain) Loss On Sale Of Invest. - - 2.0 (4.0) 2.0 (2.0)

Asset Writedow n & Restructuring Costs 211.0 49.0 28.0 15.0 264.0 88.0

(Income) Loss on Equity Invest. (108.0) (154.0) (189.0) (144.0) (52.0) (32.0)

Stock-Based Compensation 31.0 47.0 45.0 66.0 87.0 31.0

Net Cash From Discontinued Ops. - 314.0 37.0 200.0 2,027.0 -

Other Operating Activities 1,135.0 1,140.0 1,426.0 573.0 (1,212.0) 626.0

Change in Acc. Receivable (255.0) (249.0) (164.0) (457.0) (389.0) (370.0)

Change In Inventories 15.0 (173.0) 35.0 (122.0) (99.0) (335.0)

Change in Acc. Payable 168.0 (301.0) (192.0) 165.0 178.0 99.0

Change in Unearned Rev. 334.0 (99.0) 54.0 143.0 151.0 225.0

Change in Inc. Taxes (87.0) 84.0 (59.0) 32.0 (69.0) 26.0

Change in Other Net Operating Assets 19.0 (177.0) 1.0 (207.0) (564.0) (229.0)

Cash from Ops. 9,276.0 8,359.0 8,613.0 8,311.0 8,133.0 7,775.0

Capital Expenditure (3,006.0) (2,818.0) (2,868.0) (2,845.0) (3,051.0) (3,725.0)

Sale of Property, Plant, and Equipment 17.0 57.0 94.0 94.0 470.0 679.0

Cash Acquisitions - (9.0) (253.0) (986.0) (92.0) (63.0)

Divestitures (11.0) 697.0 2,397.0 1.0 1,340.0 -

Sale (Purchase) of Intangible assets (940.0) (1,679.0) (894.0) (2,257.0) (1,143.0) (1,596.0)

Invest. in Marketable & Equity Securt. 81.0 128.0 167.0 69.0 33.0 213.0

Net (Inc.) Dec. in Loans Originated/Sold 54.0 64.0 98.0 - - -

Other Investing Activities (274.0) 225.0 129.0 232.0 236.0 213.0

Cash from Investing (4,079.0) (3,335.0) (1,130.0) (5,692.0) (2,207.0) (4,279.0)

Short Term Debt Issued - - - - - -

Long-Term Debt Issued 3,049.0 2,126.0 1,572.0 1,793.0 4,987.0 4,710.0

Total Debt Issued 3,049.0 2,126.0 1,572.0 1,793.0 4,987.0 4,710.0

Short Term Debt Repaid - - - - - -

Long-Term Debt Repaid (2,276.0) (4,139.0) (1,478.0) (3,460.0) (4,055.0) (4,702.0)

Total Debt Repaid (2,276.0) (4,139.0) (1,478.0) (3,460.0) (4,055.0) (4,702.0)

Issuance of Common Stock 3.0 33.0 32.0 - - -

Repurchase of Common Stock - - (61.0) (1,058.0) (68.0) (1,524.0)

Common Dividends Paid (3,475.0) (3,480.0) (3,545.0) (3,699.0) (3,787.0) (3,736.0)

Total Dividends Paid (3,475.0) (3,480.0) (3,545.0) (3,699.0) (3,787.0) (3,736.0)

Special Dividend Paid - - - - - -

Other Financing Activities (1,207.0) (1,066.0) (950.0) (458.0) (854.0) (852.0)

Cash from Financing (3,906.0) (6,526.0) (4,430.0) (6,882.0) (3,777.0) (6,104.0)

Foreign Exchange Rate Adj. 17.0 36.0 (5.0) 132.0 5.0 (6.0)

Net Change in Cash 1,308.0 (1,466.0) 3,048.0 (4,131.0) 2,154.0 (2,614.0)

XYZ Company Limited > Cash Flow

7 | P a g e

8

The above statements is indicative of the fact that the net income of the company has kept on

growing since 2012 to 2016, however in 2017 it dropped sharply because of competition and

other factors. The depreciation and amortization has remained more or less constant, whereas the

gain on the sale of the assets has increased. Change in the other operating assets and liabilities

have kept on increasing and decreasing simultaneously as per the business needs due to which

cash flow from operating activities have increased (Boccia & Leonardi, 2016). The purchase of

the tangible and intangible assets over this period has again been constant as reflected from the

cash outflow and increased sharply in 2015 as compared to 2014. Cash flow from financing

activity shows that from which source, the funds are being arranged from, whether it is debt or

equity issues and what is being paid in the form of dividend or interest to investors to arrange it.

In the above statement, the long term debt has increased sharply over the years whereas the same

has been paid regularly too as and when the debt becomes due. Equity hasn’t been issued that

much but the dividends have been paid depending on the profits of the company. All in all, the

changes in the net cash flow has been fluctuating over this period indicating that sometimes the

inflow has been more whereas at times outflow has been more (Heminway, 2017).

In the given sheet, 2016 data is on actual basis whereas 2017 is on estimated basis so 2016 can

be taken as current and 2017 as revised figures basis which we see that a change in profit is due

to many factors or changes on the other cash flows like loss on sale of assets, increase in capital

expenditure, increase in long term debts, etc. This shows that the debt or equity needs to be

issued for funding the business once there is a business requirement. It may be in the form of

long term investment like fixed assets or simply imvesting or in the form of short term assets like

receivables, inventory, etc.

8 | P a g e

The above statements is indicative of the fact that the net income of the company has kept on

growing since 2012 to 2016, however in 2017 it dropped sharply because of competition and

other factors. The depreciation and amortization has remained more or less constant, whereas the

gain on the sale of the assets has increased. Change in the other operating assets and liabilities

have kept on increasing and decreasing simultaneously as per the business needs due to which

cash flow from operating activities have increased (Boccia & Leonardi, 2016). The purchase of

the tangible and intangible assets over this period has again been constant as reflected from the

cash outflow and increased sharply in 2015 as compared to 2014. Cash flow from financing

activity shows that from which source, the funds are being arranged from, whether it is debt or

equity issues and what is being paid in the form of dividend or interest to investors to arrange it.

In the above statement, the long term debt has increased sharply over the years whereas the same

has been paid regularly too as and when the debt becomes due. Equity hasn’t been issued that

much but the dividends have been paid depending on the profits of the company. All in all, the

changes in the net cash flow has been fluctuating over this period indicating that sometimes the

inflow has been more whereas at times outflow has been more (Heminway, 2017).

In the given sheet, 2016 data is on actual basis whereas 2017 is on estimated basis so 2016 can

be taken as current and 2017 as revised figures basis which we see that a change in profit is due

to many factors or changes on the other cash flows like loss on sale of assets, increase in capital

expenditure, increase in long term debts, etc. This shows that the debt or equity needs to be

issued for funding the business once there is a business requirement. It may be in the form of

long term investment like fixed assets or simply imvesting or in the form of short term assets like

receivables, inventory, etc.

8 | P a g e

9

Debt Reduction Goal

The debt amount of the company has been shown at $17,302 as at June 20, 2016 and it comprises

of short term borrowings, like domestic, off shore, commercial paper, bank loans etc and is 20%

of the entire debt capital (Linden & Freeman, 2017). It also holds derivative financial

instruments and and long term debts (80%), which comprise of finance leases, borrowings and

loans from bank. The details is shown below:

The company maintains a debt equity ratio of 1:1 usually and has a gearing ratio of 50-70%

which also keeps the debt in check and helps the company to make use of the trading on equity

and leveraging as debt usually comes at a cheaper cost and helps a company to make good

margin for the shareholder’s. The component of debt can still be reduced further and thus the

interest cost as can be seen from the competing company’s balance sheet where the debt

proportion is very lower as compared to equity but again the absolute return may be higher for

investors but the return on investment will fall because of higher base. Here, the debt component

is required because the investment is mainly in the non current assets i.e., PPE instead of the

current assets or the working capital.

The company’s cost of debt is 1.125% currently which is way below the average debt rate of

5.6% to 5.8%. The same has reduced primarily due to the fall in the short term interest rates in

the recent past (Murray & Markey‐Towler, 2017). In case this is decreased, the monthly interest

will drop from $73 Mn to may be $ 60 Mn or maximum $ 50 Mn but the same will have an

impact on overall returns on equity and the equivalent funding is also required from equity for

the business to move forward.

Savings Goal

The savings goal of the company would be decrease the funds outflow by a reasonable amount

both on the short term as well as long term basis and the same to have positive impact on the

profits. From the below profit statement, we can see that the only reduction can be done in

monthly expenses are selling, general and administration expenses, cost of goods sold by

increasing the efficiency and cutting down on the direct costs, depreciation costs by investing a

bit less in the fixed assets and cutting down on the other operating expenses (Félix, 2017). The

9 | P a g e

Debt Reduction Goal

The debt amount of the company has been shown at $17,302 as at June 20, 2016 and it comprises

of short term borrowings, like domestic, off shore, commercial paper, bank loans etc and is 20%

of the entire debt capital (Linden & Freeman, 2017). It also holds derivative financial

instruments and and long term debts (80%), which comprise of finance leases, borrowings and

loans from bank. The details is shown below:

The company maintains a debt equity ratio of 1:1 usually and has a gearing ratio of 50-70%

which also keeps the debt in check and helps the company to make use of the trading on equity

and leveraging as debt usually comes at a cheaper cost and helps a company to make good

margin for the shareholder’s. The component of debt can still be reduced further and thus the

interest cost as can be seen from the competing company’s balance sheet where the debt

proportion is very lower as compared to equity but again the absolute return may be higher for

investors but the return on investment will fall because of higher base. Here, the debt component

is required because the investment is mainly in the non current assets i.e., PPE instead of the

current assets or the working capital.

The company’s cost of debt is 1.125% currently which is way below the average debt rate of

5.6% to 5.8%. The same has reduced primarily due to the fall in the short term interest rates in

the recent past (Murray & Markey‐Towler, 2017). In case this is decreased, the monthly interest

will drop from $73 Mn to may be $ 60 Mn or maximum $ 50 Mn but the same will have an

impact on overall returns on equity and the equivalent funding is also required from equity for

the business to move forward.

Savings Goal

The savings goal of the company would be decrease the funds outflow by a reasonable amount

both on the short term as well as long term basis and the same to have positive impact on the

profits. From the below profit statement, we can see that the only reduction can be done in

monthly expenses are selling, general and administration expenses, cost of goods sold by

increasing the efficiency and cutting down on the direct costs, depreciation costs by investing a

bit less in the fixed assets and cutting down on the other operating expenses (Félix, 2017). The

9 | P a g e

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

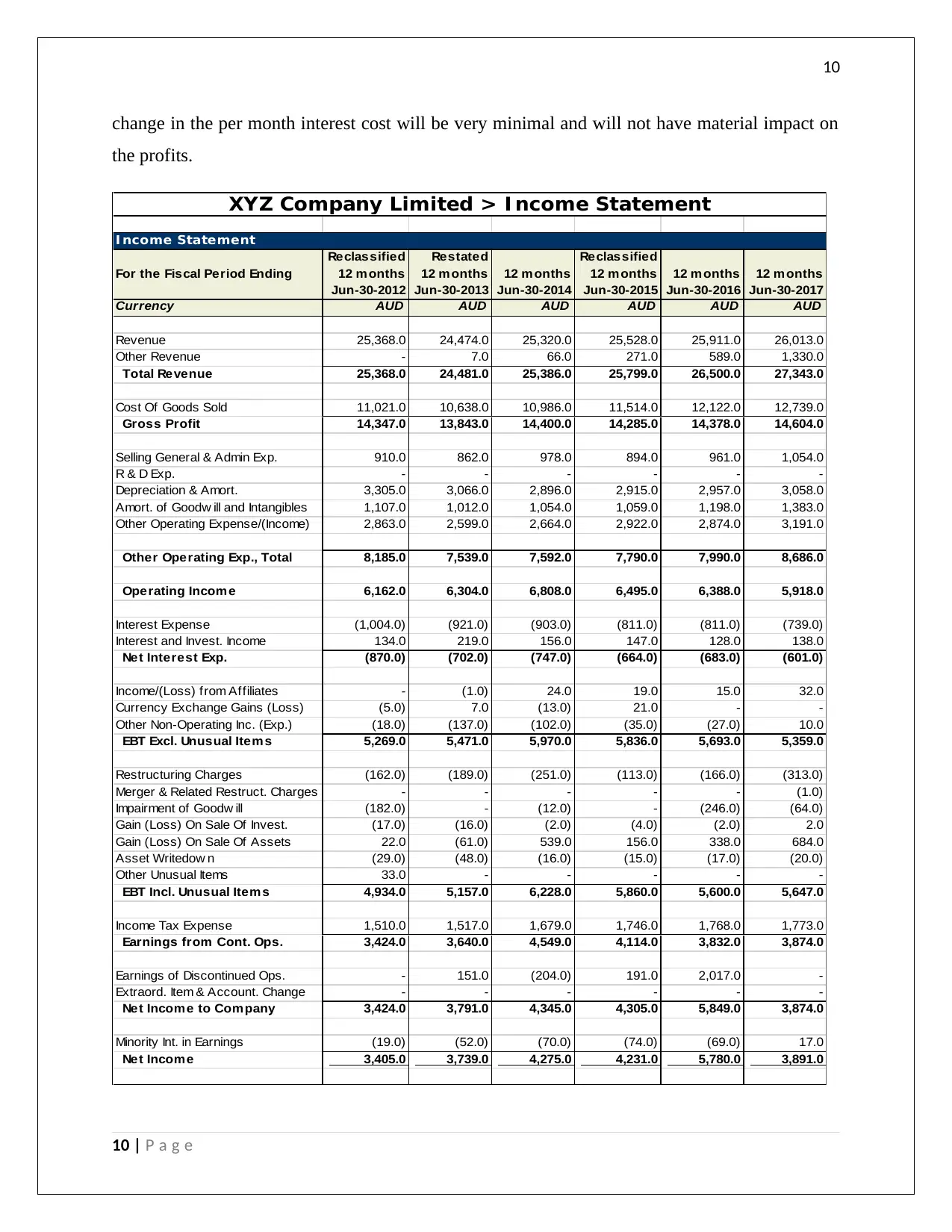

change in the per month interest cost will be very minimal and will not have material impact on

the profits.

I ncome Statement

For the Fiscal Period Ending

Reclassified

12 m onths

Jun-30-2012

Restated

12 m onths

Jun-30-2013

12 m onths

Jun-30-2014

Reclassified

12 m onths

Jun-30-2015

12 m onths

Jun-30-2016

12 m onths

Jun-30-2017

Currency AUD AUD AUD AUD AUD AUD

Revenue 25,368.0 24,474.0 25,320.0 25,528.0 25,911.0 26,013.0

Other Revenue - 7.0 66.0 271.0 589.0 1,330.0

Total Revenue 25,368.0 24,481.0 25,386.0 25,799.0 26,500.0 27,343.0

Cost Of Goods Sold 11,021.0 10,638.0 10,986.0 11,514.0 12,122.0 12,739.0

Gross Profit 14,347.0 13,843.0 14,400.0 14,285.0 14,378.0 14,604.0

Selling General & Admin Exp. 910.0 862.0 978.0 894.0 961.0 1,054.0

R & D Exp. - - - - - -

Depreciation & Amort. 3,305.0 3,066.0 2,896.0 2,915.0 2,957.0 3,058.0

Amort. of Goodw ill and Intangibles 1,107.0 1,012.0 1,054.0 1,059.0 1,198.0 1,383.0

Other Operating Expense/(Income) 2,863.0 2,599.0 2,664.0 2,922.0 2,874.0 3,191.0

Other Operating Exp., Total 8,185.0 7,539.0 7,592.0 7,790.0 7,990.0 8,686.0

Operating Income 6,162.0 6,304.0 6,808.0 6,495.0 6,388.0 5,918.0

Interest Expense (1,004.0) (921.0) (903.0) (811.0) (811.0) (739.0)

Interest and Invest. Income 134.0 219.0 156.0 147.0 128.0 138.0

Net Interest Exp. (870.0) (702.0) (747.0) (664.0) (683.0) (601.0)

Income/(Loss) from Affiliates - (1.0) 24.0 19.0 15.0 32.0

Currency Exchange Gains (Loss) (5.0) 7.0 (13.0) 21.0 - -

Other Non-Operating Inc. (Exp.) (18.0) (137.0) (102.0) (35.0) (27.0) 10.0

EBT Excl. Unusual Item s 5,269.0 5,471.0 5,970.0 5,836.0 5,693.0 5,359.0

Restructuring Charges (162.0) (189.0) (251.0) (113.0) (166.0) (313.0)

Merger & Related Restruct. Charges - - - - - (1.0)

Impairment of Goodw ill (182.0) - (12.0) - (246.0) (64.0)

Gain (Loss) On Sale Of Invest. (17.0) (16.0) (2.0) (4.0) (2.0) 2.0

Gain (Loss) On Sale Of Assets 22.0 (61.0) 539.0 156.0 338.0 684.0

Asset Writedow n (29.0) (48.0) (16.0) (15.0) (17.0) (20.0)

Other Unusual Items 33.0 - - - - -

EBT Incl. Unusual Item s 4,934.0 5,157.0 6,228.0 5,860.0 5,600.0 5,647.0

Income Tax Expense 1,510.0 1,517.0 1,679.0 1,746.0 1,768.0 1,773.0

Earnings from Cont. Ops. 3,424.0 3,640.0 4,549.0 4,114.0 3,832.0 3,874.0

Earnings of Discontinued Ops. - 151.0 (204.0) 191.0 2,017.0 -

Extraord. Item & Account. Change - - - - - -

Net Income to Company 3,424.0 3,791.0 4,345.0 4,305.0 5,849.0 3,874.0

Minority Int. in Earnings (19.0) (52.0) (70.0) (74.0) (69.0) 17.0

Net Income 3,405.0 3,739.0 4,275.0 4,231.0 5,780.0 3,891.0

XYZ Company Limited > I ncome Statement

10 | P a g e

change in the per month interest cost will be very minimal and will not have material impact on

the profits.

I ncome Statement

For the Fiscal Period Ending

Reclassified

12 m onths

Jun-30-2012

Restated

12 m onths

Jun-30-2013

12 m onths

Jun-30-2014

Reclassified

12 m onths

Jun-30-2015

12 m onths

Jun-30-2016

12 m onths

Jun-30-2017

Currency AUD AUD AUD AUD AUD AUD

Revenue 25,368.0 24,474.0 25,320.0 25,528.0 25,911.0 26,013.0

Other Revenue - 7.0 66.0 271.0 589.0 1,330.0

Total Revenue 25,368.0 24,481.0 25,386.0 25,799.0 26,500.0 27,343.0

Cost Of Goods Sold 11,021.0 10,638.0 10,986.0 11,514.0 12,122.0 12,739.0

Gross Profit 14,347.0 13,843.0 14,400.0 14,285.0 14,378.0 14,604.0

Selling General & Admin Exp. 910.0 862.0 978.0 894.0 961.0 1,054.0

R & D Exp. - - - - - -

Depreciation & Amort. 3,305.0 3,066.0 2,896.0 2,915.0 2,957.0 3,058.0

Amort. of Goodw ill and Intangibles 1,107.0 1,012.0 1,054.0 1,059.0 1,198.0 1,383.0

Other Operating Expense/(Income) 2,863.0 2,599.0 2,664.0 2,922.0 2,874.0 3,191.0

Other Operating Exp., Total 8,185.0 7,539.0 7,592.0 7,790.0 7,990.0 8,686.0

Operating Income 6,162.0 6,304.0 6,808.0 6,495.0 6,388.0 5,918.0

Interest Expense (1,004.0) (921.0) (903.0) (811.0) (811.0) (739.0)

Interest and Invest. Income 134.0 219.0 156.0 147.0 128.0 138.0

Net Interest Exp. (870.0) (702.0) (747.0) (664.0) (683.0) (601.0)

Income/(Loss) from Affiliates - (1.0) 24.0 19.0 15.0 32.0

Currency Exchange Gains (Loss) (5.0) 7.0 (13.0) 21.0 - -

Other Non-Operating Inc. (Exp.) (18.0) (137.0) (102.0) (35.0) (27.0) 10.0

EBT Excl. Unusual Item s 5,269.0 5,471.0 5,970.0 5,836.0 5,693.0 5,359.0

Restructuring Charges (162.0) (189.0) (251.0) (113.0) (166.0) (313.0)

Merger & Related Restruct. Charges - - - - - (1.0)

Impairment of Goodw ill (182.0) - (12.0) - (246.0) (64.0)

Gain (Loss) On Sale Of Invest. (17.0) (16.0) (2.0) (4.0) (2.0) 2.0

Gain (Loss) On Sale Of Assets 22.0 (61.0) 539.0 156.0 338.0 684.0

Asset Writedow n (29.0) (48.0) (16.0) (15.0) (17.0) (20.0)

Other Unusual Items 33.0 - - - - -

EBT Incl. Unusual Item s 4,934.0 5,157.0 6,228.0 5,860.0 5,600.0 5,647.0

Income Tax Expense 1,510.0 1,517.0 1,679.0 1,746.0 1,768.0 1,773.0

Earnings from Cont. Ops. 3,424.0 3,640.0 4,549.0 4,114.0 3,832.0 3,874.0

Earnings of Discontinued Ops. - 151.0 (204.0) 191.0 2,017.0 -

Extraord. Item & Account. Change - - - - - -

Net Income to Company 3,424.0 3,791.0 4,345.0 4,305.0 5,849.0 3,874.0

Minority Int. in Earnings (19.0) (52.0) (70.0) (74.0) (69.0) 17.0

Net Income 3,405.0 3,739.0 4,275.0 4,231.0 5,780.0 3,891.0

XYZ Company Limited > I ncome Statement

10 | P a g e

11

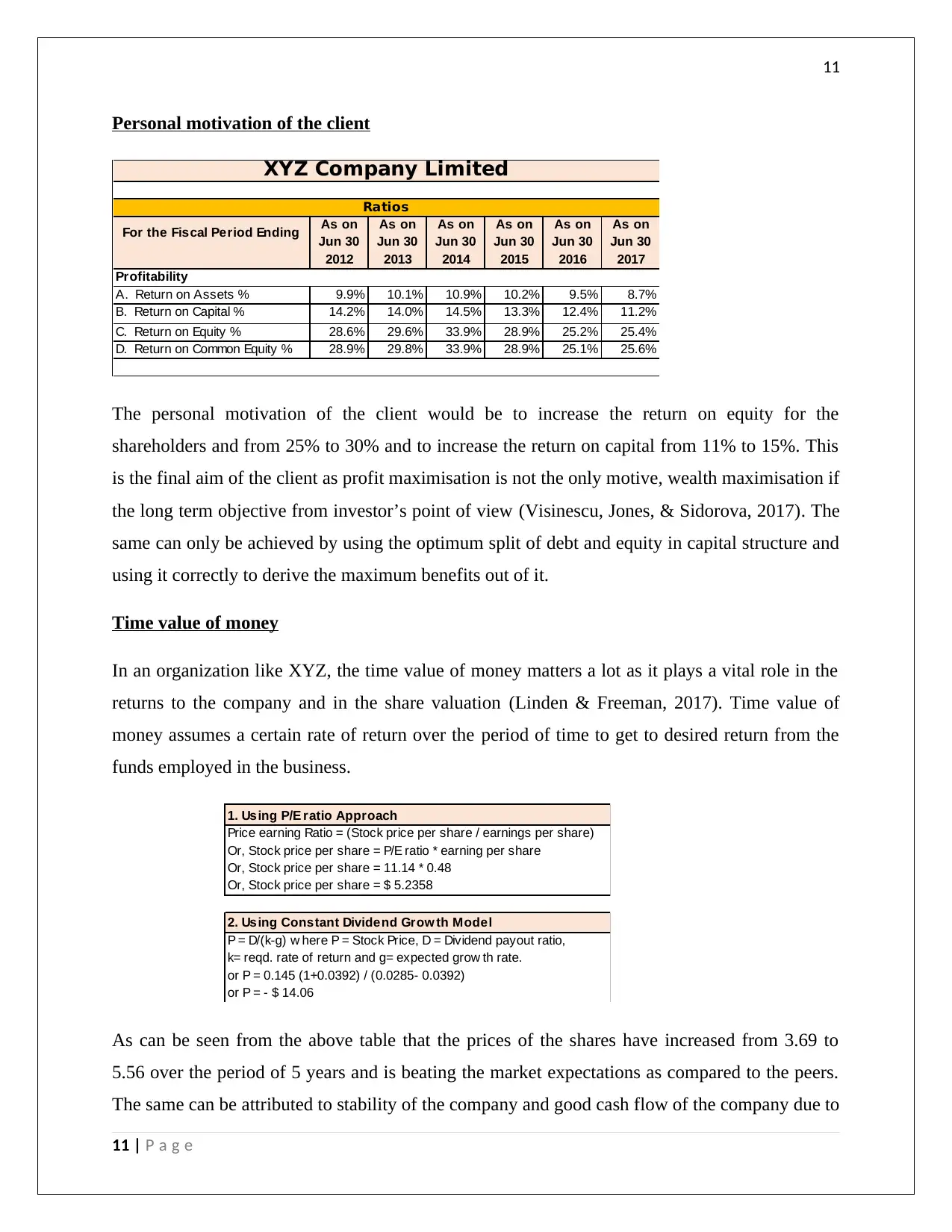

Personal motivation of the client

For the Fiscal Period Ending As on

Jun 30

2012

As on

Jun 30

2013

As on

Jun 30

2014

As on

Jun 30

2015

As on

Jun 30

2016

As on

Jun 30

2017

Profitability

A. Return on Assets % 9.9% 10.1% 10.9% 10.2% 9.5% 8.7%

B. Return on Capital % 14.2% 14.0% 14.5% 13.3% 12.4% 11.2%

C. Return on Equity % 28.6% 29.6% 33.9% 28.9% 25.2% 25.4%

D. Return on Common Equity % 28.9% 29.8% 33.9% 28.9% 25.1% 25.6%

XYZ Company Limited

Ratios

The personal motivation of the client would be to increase the return on equity for the

shareholders and from 25% to 30% and to increase the return on capital from 11% to 15%. This

is the final aim of the client as profit maximisation is not the only motive, wealth maximisation if

the long term objective from investor’s point of view (Visinescu, Jones, & Sidorova, 2017). The

same can only be achieved by using the optimum split of debt and equity in capital structure and

using it correctly to derive the maximum benefits out of it.

Time value of money

In an organization like XYZ, the time value of money matters a lot as it plays a vital role in the

returns to the company and in the share valuation (Linden & Freeman, 2017). Time value of

money assumes a certain rate of return over the period of time to get to desired return from the

funds employed in the business.

1. Using P/E ratio Approach

Price earning Ratio = (Stock price per share / earnings per share)

Or, Stock price per share = P/E ratio * earning per share

Or, Stock price per share = 11.14 * 0.48

Or, Stock price per share = $ 5.2358

2. Using Constant Dividend Grow th Model

P = D/(k-g) w here P = Stock Price, D = Dividend payout ratio,

k= reqd. rate of return and g= expected grow th rate.

or P = 0.145 (1+0.0392) / (0.0285- 0.0392)

or P = - $ 14.06

As can be seen from the above table that the prices of the shares have increased from 3.69 to

5.56 over the period of 5 years and is beating the market expectations as compared to the peers.

The same can be attributed to stability of the company and good cash flow of the company due to

11 | P a g e

Personal motivation of the client

For the Fiscal Period Ending As on

Jun 30

2012

As on

Jun 30

2013

As on

Jun 30

2014

As on

Jun 30

2015

As on

Jun 30

2016

As on

Jun 30

2017

Profitability

A. Return on Assets % 9.9% 10.1% 10.9% 10.2% 9.5% 8.7%

B. Return on Capital % 14.2% 14.0% 14.5% 13.3% 12.4% 11.2%

C. Return on Equity % 28.6% 29.6% 33.9% 28.9% 25.2% 25.4%

D. Return on Common Equity % 28.9% 29.8% 33.9% 28.9% 25.1% 25.6%

XYZ Company Limited

Ratios

The personal motivation of the client would be to increase the return on equity for the

shareholders and from 25% to 30% and to increase the return on capital from 11% to 15%. This

is the final aim of the client as profit maximisation is not the only motive, wealth maximisation if

the long term objective from investor’s point of view (Visinescu, Jones, & Sidorova, 2017). The

same can only be achieved by using the optimum split of debt and equity in capital structure and

using it correctly to derive the maximum benefits out of it.

Time value of money

In an organization like XYZ, the time value of money matters a lot as it plays a vital role in the

returns to the company and in the share valuation (Linden & Freeman, 2017). Time value of

money assumes a certain rate of return over the period of time to get to desired return from the

funds employed in the business.

1. Using P/E ratio Approach

Price earning Ratio = (Stock price per share / earnings per share)

Or, Stock price per share = P/E ratio * earning per share

Or, Stock price per share = 11.14 * 0.48

Or, Stock price per share = $ 5.2358

2. Using Constant Dividend Grow th Model

P = D/(k-g) w here P = Stock Price, D = Dividend payout ratio,

k= reqd. rate of return and g= expected grow th rate.

or P = 0.145 (1+0.0392) / (0.0285- 0.0392)

or P = - $ 14.06

As can be seen from the above table that the prices of the shares have increased from 3.69 to

5.56 over the period of 5 years and is beating the market expectations as compared to the peers.

The same can be attributed to stability of the company and good cash flow of the company due to

11 | P a g e

12

which it is able to pay the dividends as well (Das, 2017). If the company instead of paying the

dividends, reinvest at the required rate of return i.e., 12% as shown above (from the Annual

Report of the company), the company can earn on this well over the future years with the growth

being expected to be at 3.92% annually.

12 | P a g e

which it is able to pay the dividends as well (Das, 2017). If the company instead of paying the

dividends, reinvest at the required rate of return i.e., 12% as shown above (from the Annual

Report of the company), the company can earn on this well over the future years with the growth

being expected to be at 3.92% annually.

12 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

Recommendations:

Specific description of life style changes to change cash flow

As mentioned above, to change the cash flow some of the measures include reduction in the

direct expenses incurred by 10-15%, which will amount to AUD 1200-1400 Mn increase in

profits, Furthremore, indirect expenses in the form of S,G&A expenses and other operating

expenses can also be decreased by 10%, which will have an impact of nearly AUD 200-300 Mn.

Also, the depreciation and amortization expenses can be brought down by investing less in the

PPE and bringing the same down 5-8% considering the need of fixed assets in

telecommunication industry which again will impact profit positively by AUD 200-250 Mn

(Bromwich & Scapens, 2016). All together if all these expenses can be curtailed, the same will

increase the profit by AUD 1500-1700 Mn and will increase the cash flow by approximately

AUD 1500 Mn which again can be invested in the business to increase the returns and increase

the profit and return percentage.

13 | P a g e

Recommendations:

Specific description of life style changes to change cash flow

As mentioned above, to change the cash flow some of the measures include reduction in the

direct expenses incurred by 10-15%, which will amount to AUD 1200-1400 Mn increase in

profits, Furthremore, indirect expenses in the form of S,G&A expenses and other operating

expenses can also be decreased by 10%, which will have an impact of nearly AUD 200-300 Mn.

Also, the depreciation and amortization expenses can be brought down by investing less in the

PPE and bringing the same down 5-8% considering the need of fixed assets in

telecommunication industry which again will impact profit positively by AUD 200-250 Mn

(Bromwich & Scapens, 2016). All together if all these expenses can be curtailed, the same will

increase the profit by AUD 1500-1700 Mn and will increase the cash flow by approximately

AUD 1500 Mn which again can be invested in the business to increase the returns and increase

the profit and return percentage.

13 | P a g e

14

Conclusion

Basis the above report and the analysis done, it can concluded that it is not only about the cash

flow of the company or the returns given by the company but the type of business and its

requirements, the operational efficiency required and what is the amount of fund requirement and

for what purposes (Trieu, 2017). Also, the company should use the optimum capital structure to

derive the benefits of trading on equity and low interest cost on debt but the same time the

proportion of debt cannot be increased invariably as it will lead to dilution of ownership. Finally,

time value of money presupposes a rate of return over a period of time at which the estimated

earnings in future may be discounted but the same is not certain and can change over a period of

time depending on the business conditions. The above analysis indicates good competitive

position of the company.

14 | P a g e

Conclusion

Basis the above report and the analysis done, it can concluded that it is not only about the cash

flow of the company or the returns given by the company but the type of business and its

requirements, the operational efficiency required and what is the amount of fund requirement and

for what purposes (Trieu, 2017). Also, the company should use the optimum capital structure to

derive the benefits of trading on equity and low interest cost on debt but the same time the

proportion of debt cannot be increased invariably as it will lead to dilution of ownership. Finally,

time value of money presupposes a rate of return over a period of time at which the estimated

earnings in future may be discounted but the same is not certain and can change over a period of

time depending on the business conditions. The above analysis indicates good competitive

position of the company.

14 | P a g e

15

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education , 71 (4), 411-

431.

Boccia, F., & Leonardi, R. (2016). The Challenge of the Digital Economy. Markets, Taxation and

Appropriate Economic Models , 1-16.

Bromwich, M., & Scapens, R. (2016). Management Accounting Research: 25 years on. Management

Accounting Research , 31, 1-9.

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies , 2 (2), 10-17.

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research , 47 (6), 617-632.

Félix, M. (2017). A study on the expected impact of IFRS 17 on the transparency of financial statements

of insurance companies. MASTER THESIS , 1-69.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN , 1-35.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly , 27 (3), 353-379.

Murray, C., & Markey Towler, B. (2017). A Theory of Return-Seeking Firms.‐ SSRN , 1-14.

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems , 93, 111-124.

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems , 57 (1), 58-66.

15 | P a g e

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education , 71 (4), 411-

431.

Boccia, F., & Leonardi, R. (2016). The Challenge of the Digital Economy. Markets, Taxation and

Appropriate Economic Models , 1-16.

Bromwich, M., & Scapens, R. (2016). Management Accounting Research: 25 years on. Management

Accounting Research , 31, 1-9.

Das, P. (2017). Financing Pattern and Utilization of Fixed Assets - A Study. Asian Journal of Social Science

Studies , 2 (2), 10-17.

Dichev, I. (2017). On the conceptual foundations of financial reporting. Accounting and Business

Research , 47 (6), 617-632.

Félix, M. (2017). A study on the expected impact of IFRS 17 on the transparency of financial statements

of insurance companies. MASTER THESIS , 1-69.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN , 1-35.

Linden, B., & Freeman, R. (2017). Profit and Other Values: Thick Evaluation in Decision Making. Business

Ethics Quarterly , 27 (3), 353-379.

Murray, C., & Markey Towler, B. (2017). A Theory of Return-Seeking Firms.‐ SSRN , 1-14.

Trieu, V. (2017). Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems , 93, 111-124.

Visinescu, L., Jones, M., & Sidorova, A. (2017). Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems , 57 (1), 58-66.

15 | P a g e

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.