Carsales.com Ltd: Financial Analysis and Performance Review

VerifiedAdded on 2020/03/23

|16

|2865

|108

Report

AI Summary

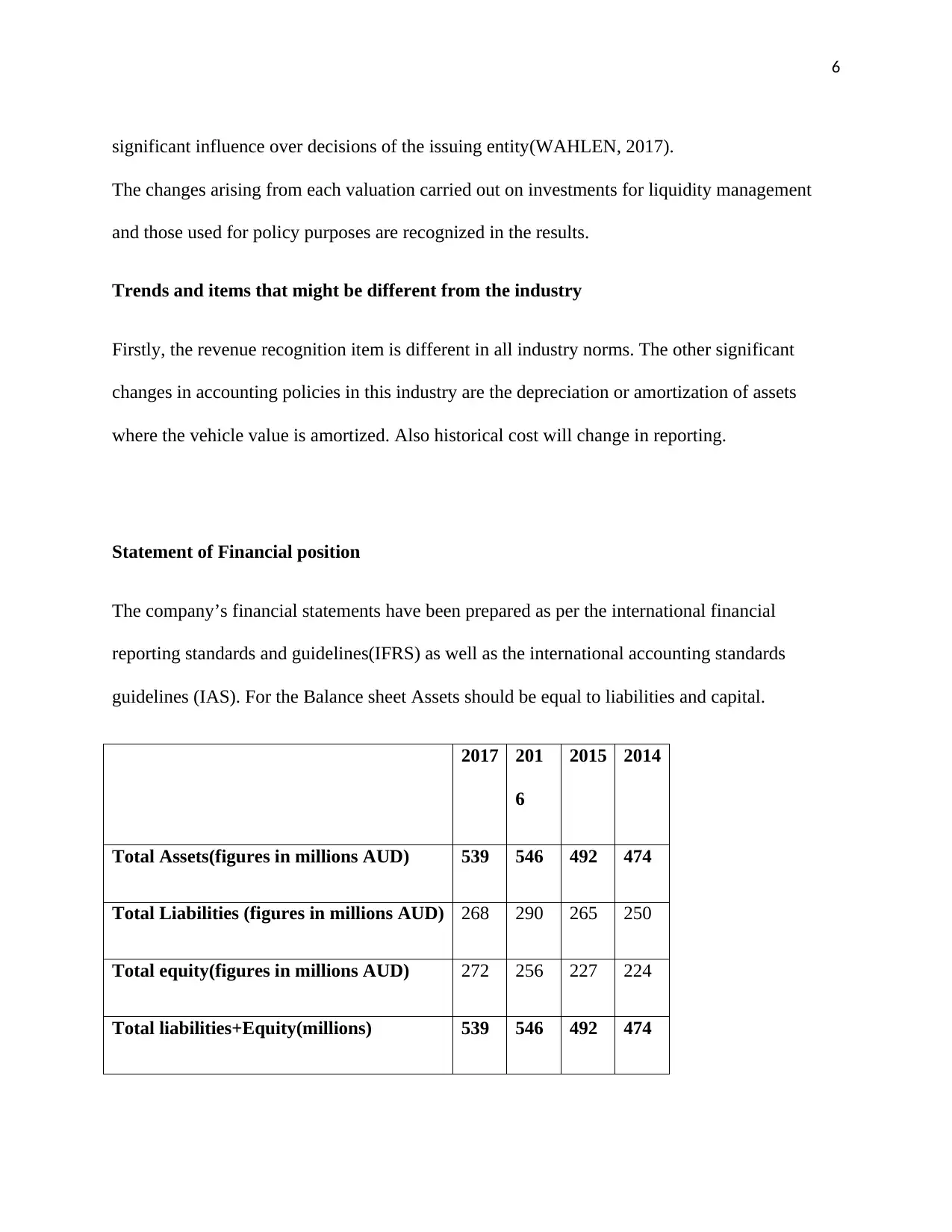

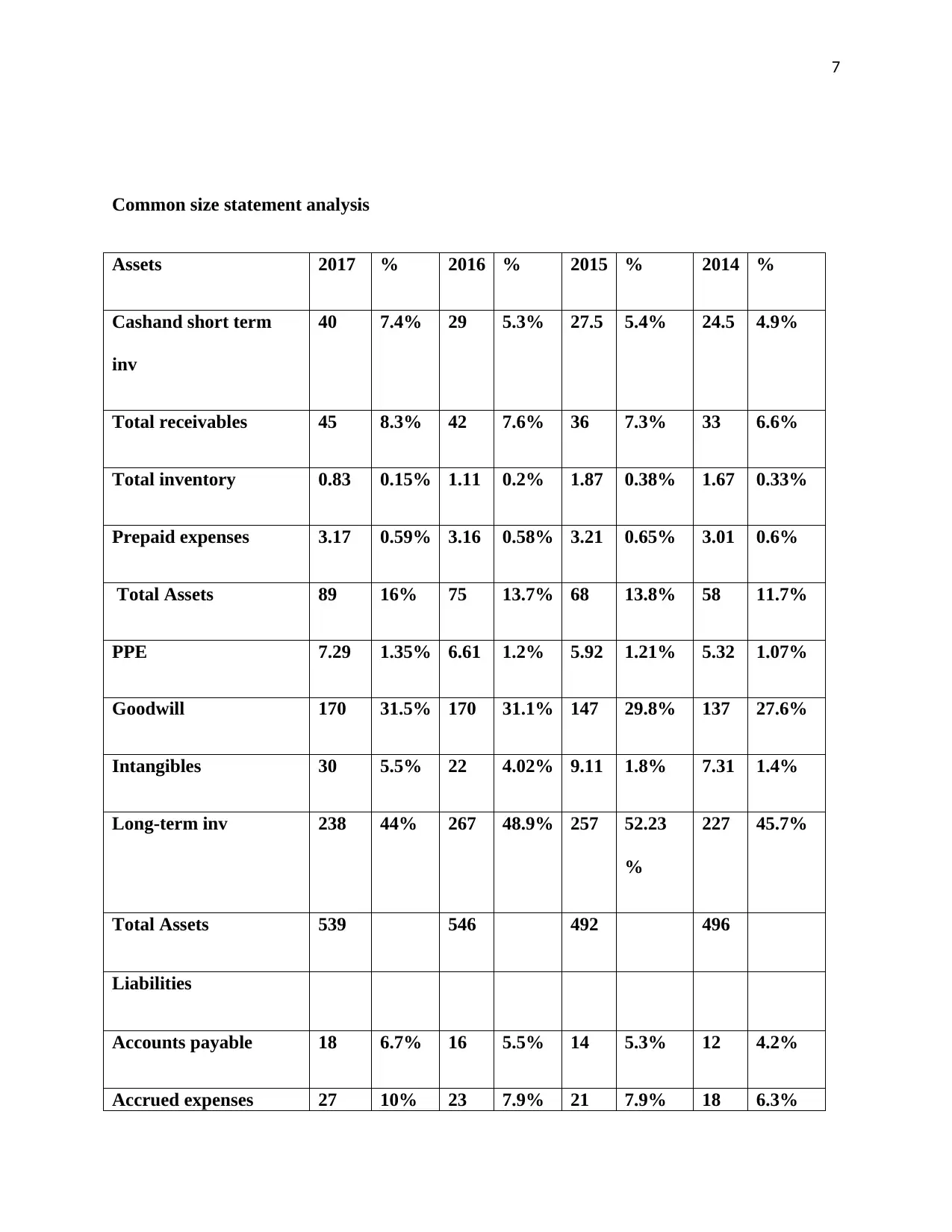

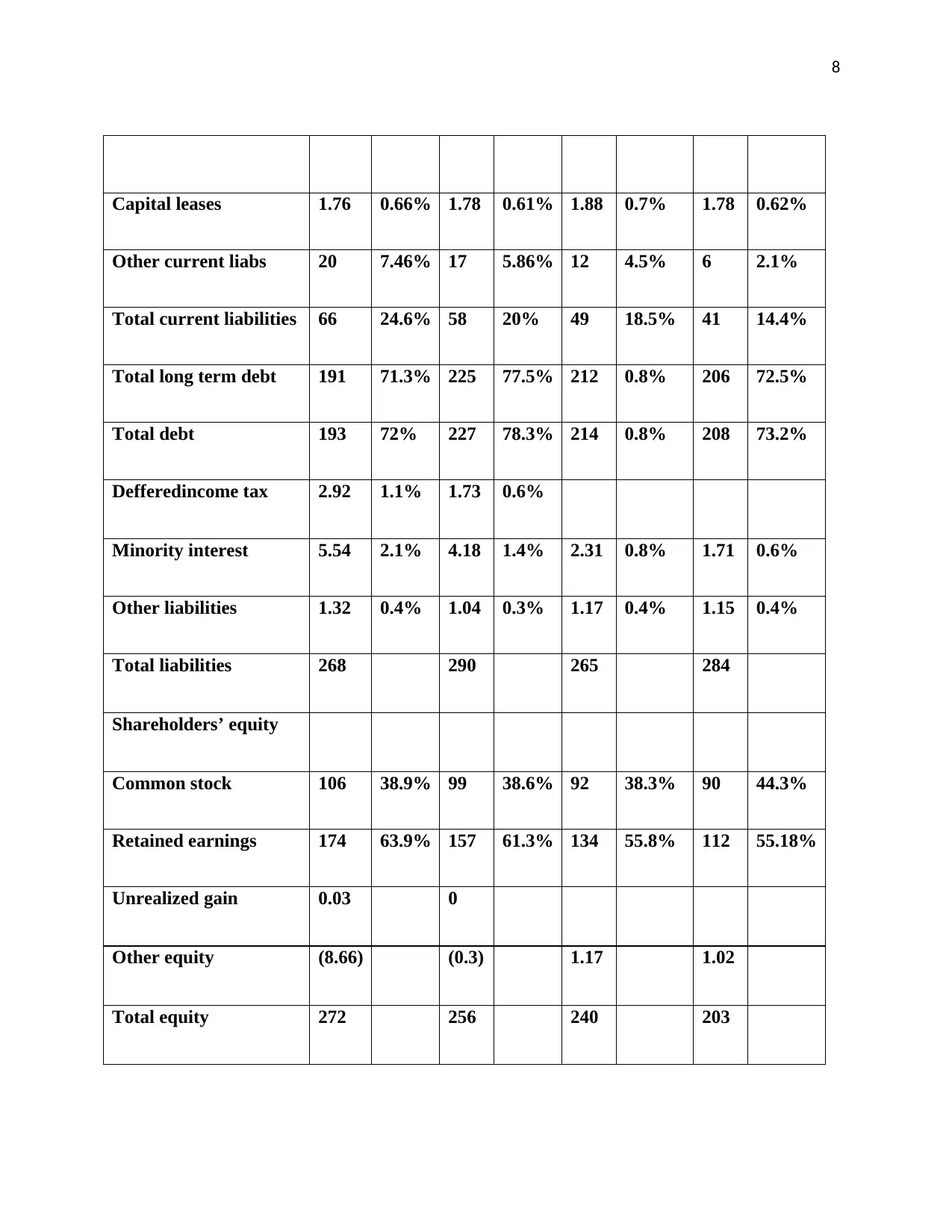

This report provides a comprehensive financial analysis of Carsales.com Ltd, a leading online automotive business in Australia. It begins with an introduction to the company, its industry position, and future plans, followed by an in-depth examination of its financial statements from 2014 to 2017. The analysis includes common-size statement analysis, trend analysis, and a review of revenue recognition changes and significant accounting policies. The report also presents a detailed statement of financial position, analyzing assets, liabilities, and shareholders' equity. Furthermore, it delves into the company's cash flow statements, comparing operating cash flows with net income and examining investing and financing activities. Ratio analysis is conducted, covering liquidity, profitability, long-term solvency, and market strength ratios. The report concludes with an evaluation of the company's strengths and weaknesses, providing insights into its financial performance and strategic positioning within the automotive industry.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.