Advanced Financial Analysis: Capital Budgeting, WACC, and Bond Pricing

VerifiedAdded on 2022/11/24

|11

|1361

|57

Homework Assignment

AI Summary

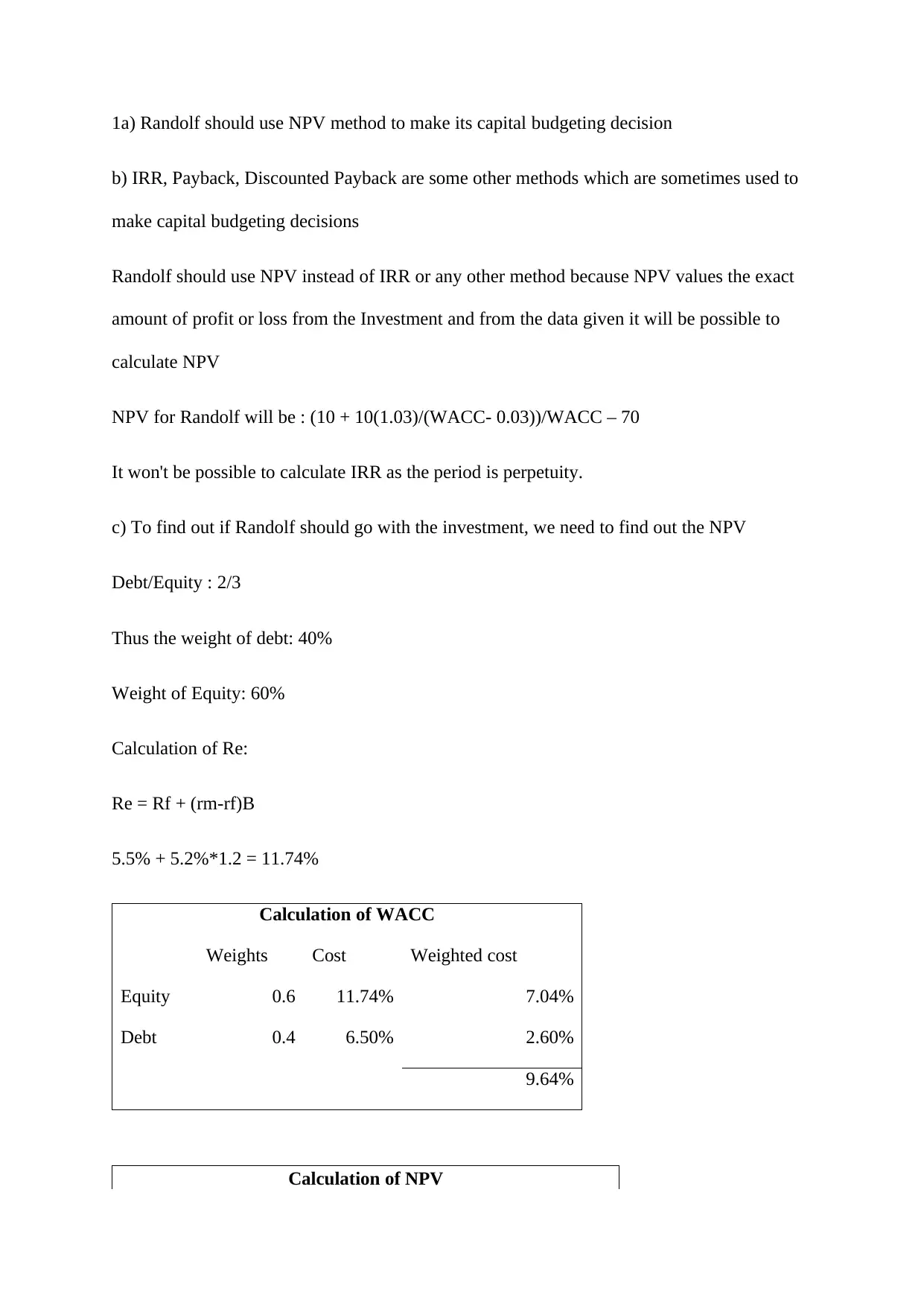

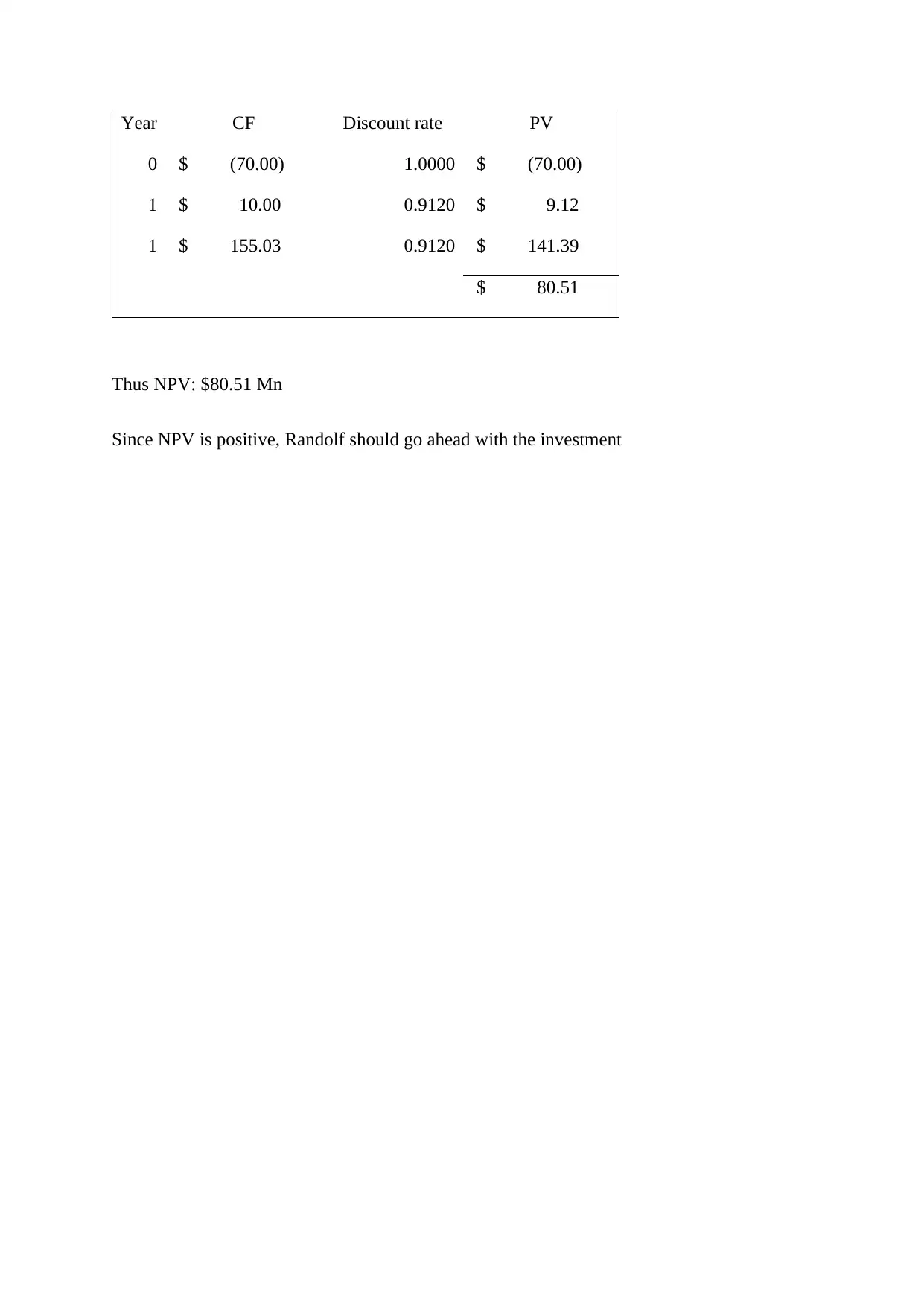

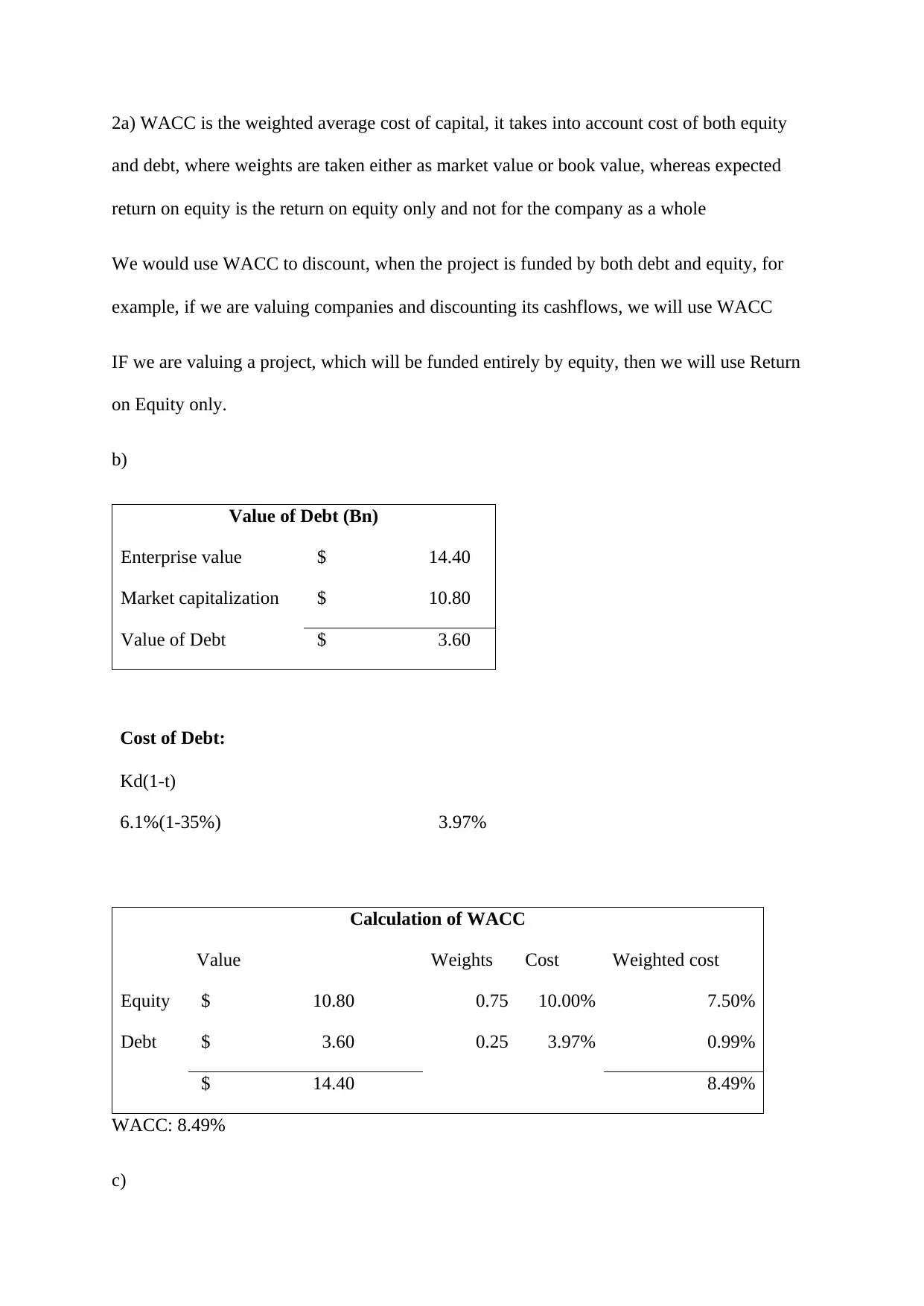

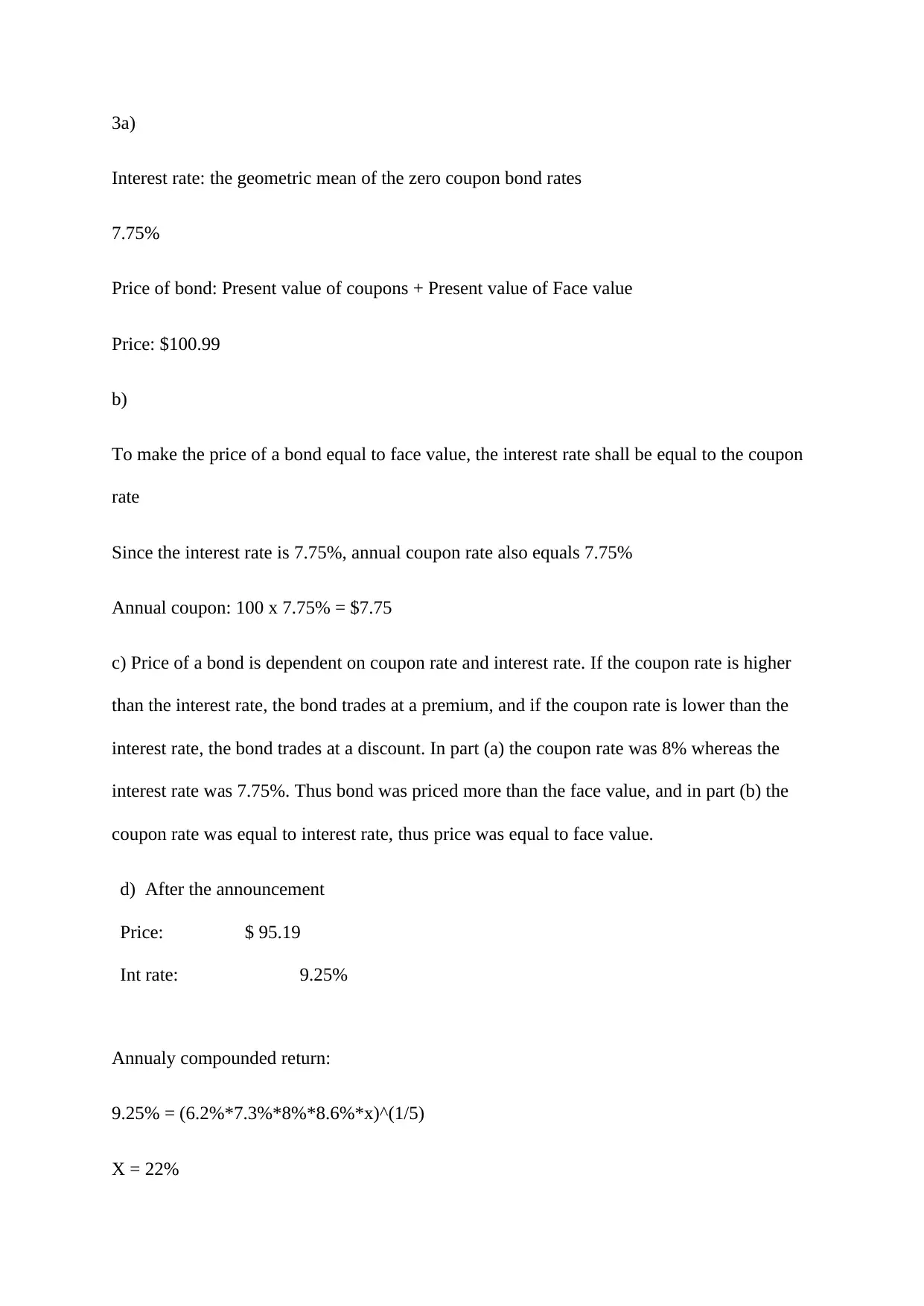

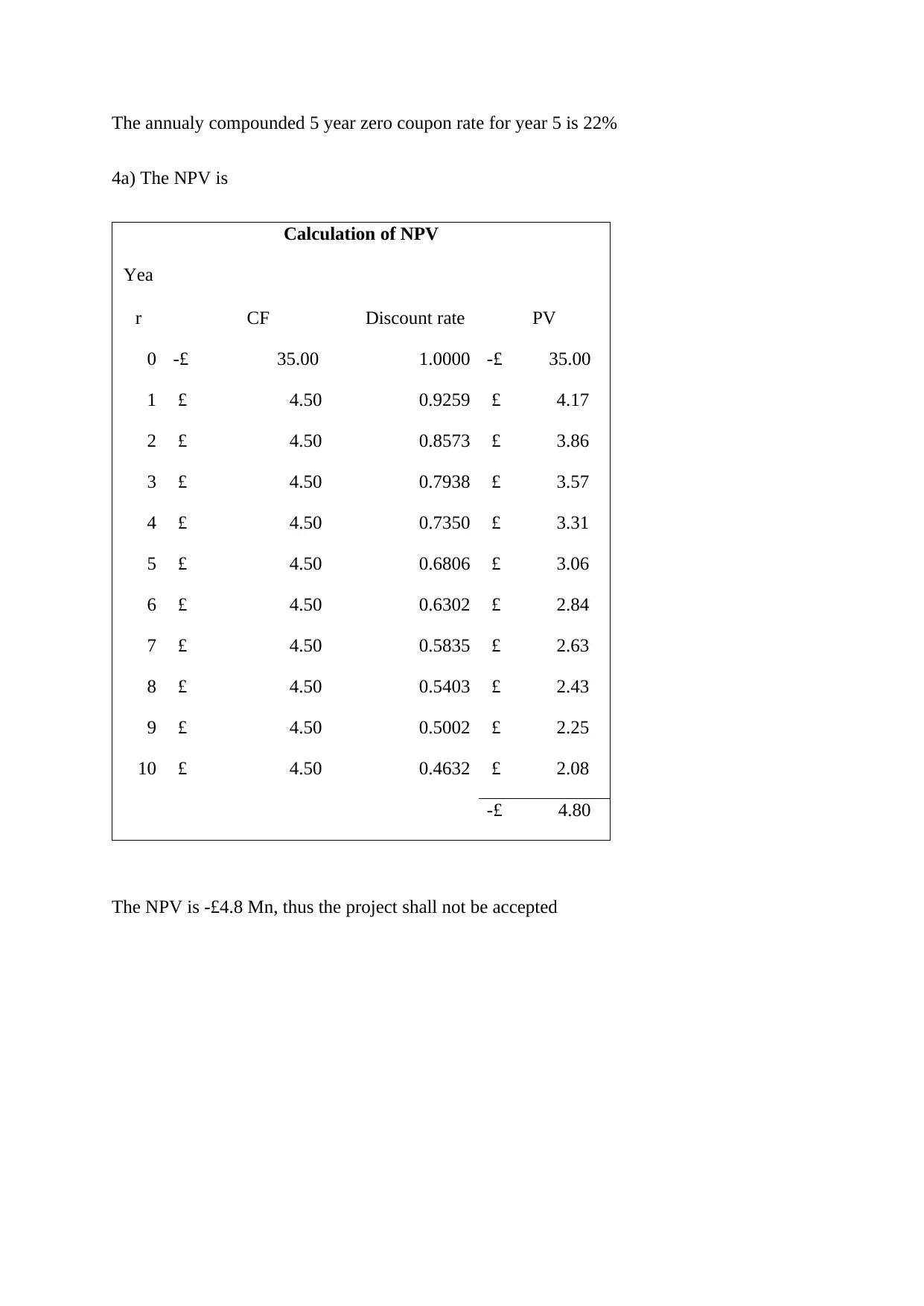

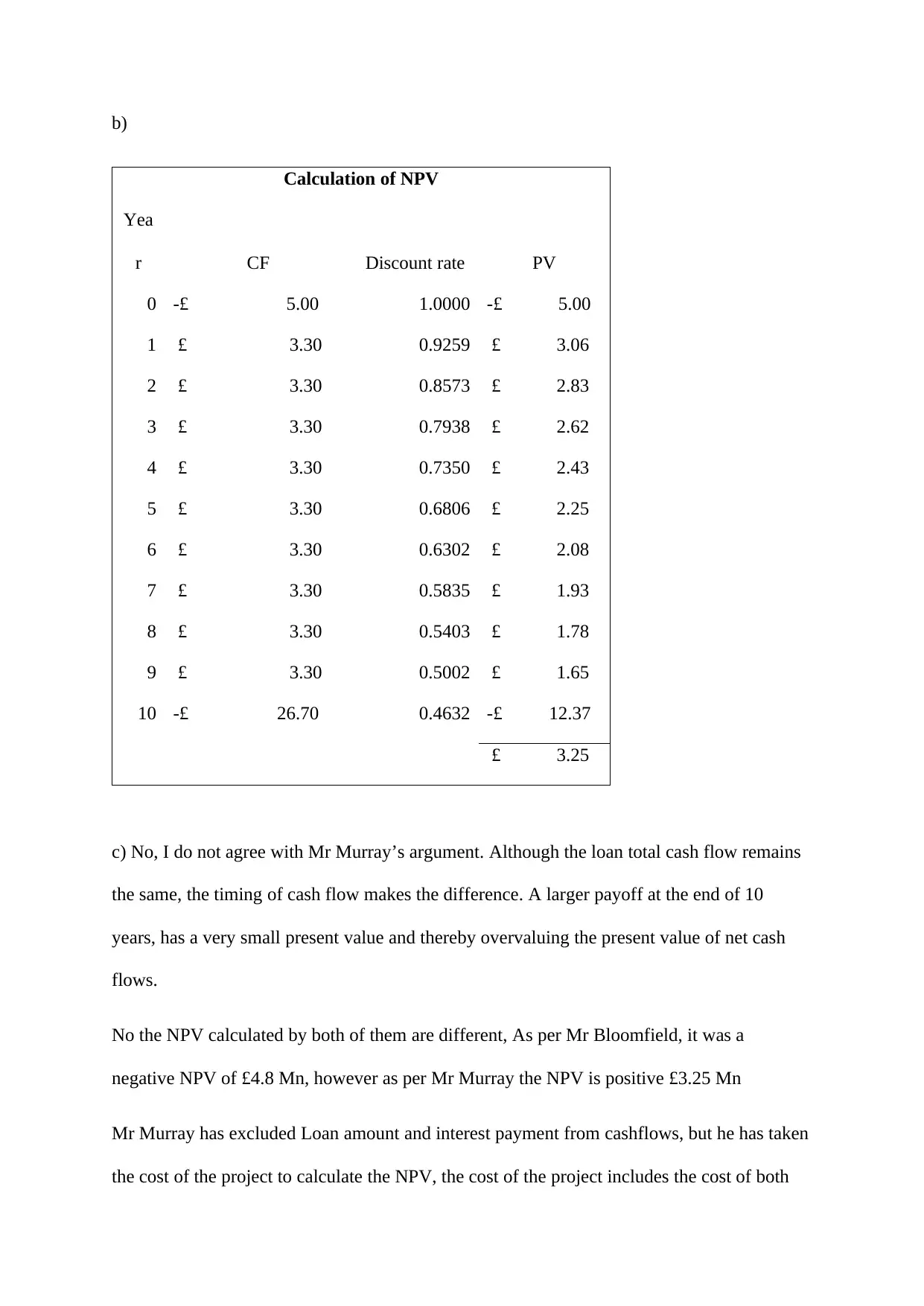

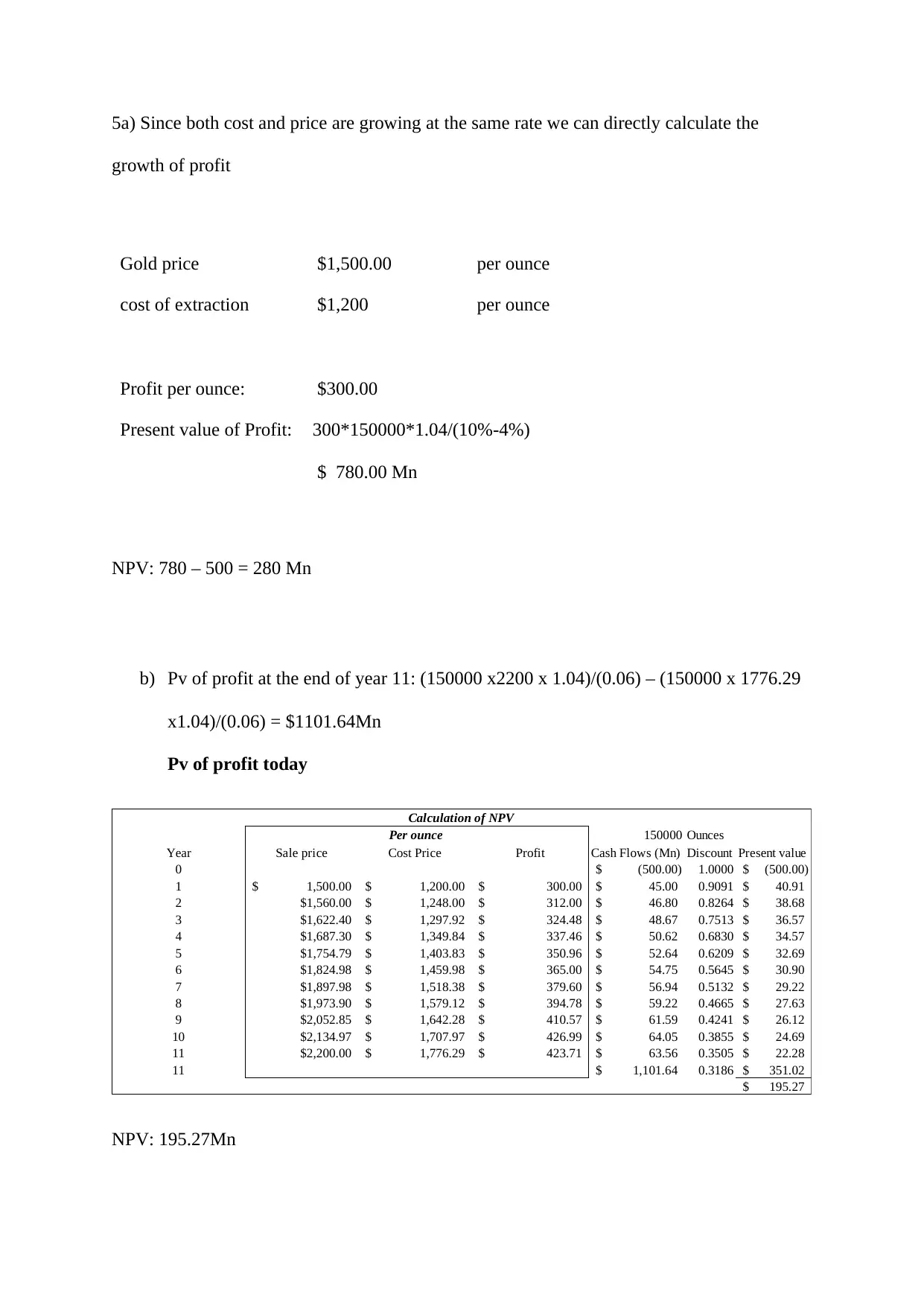

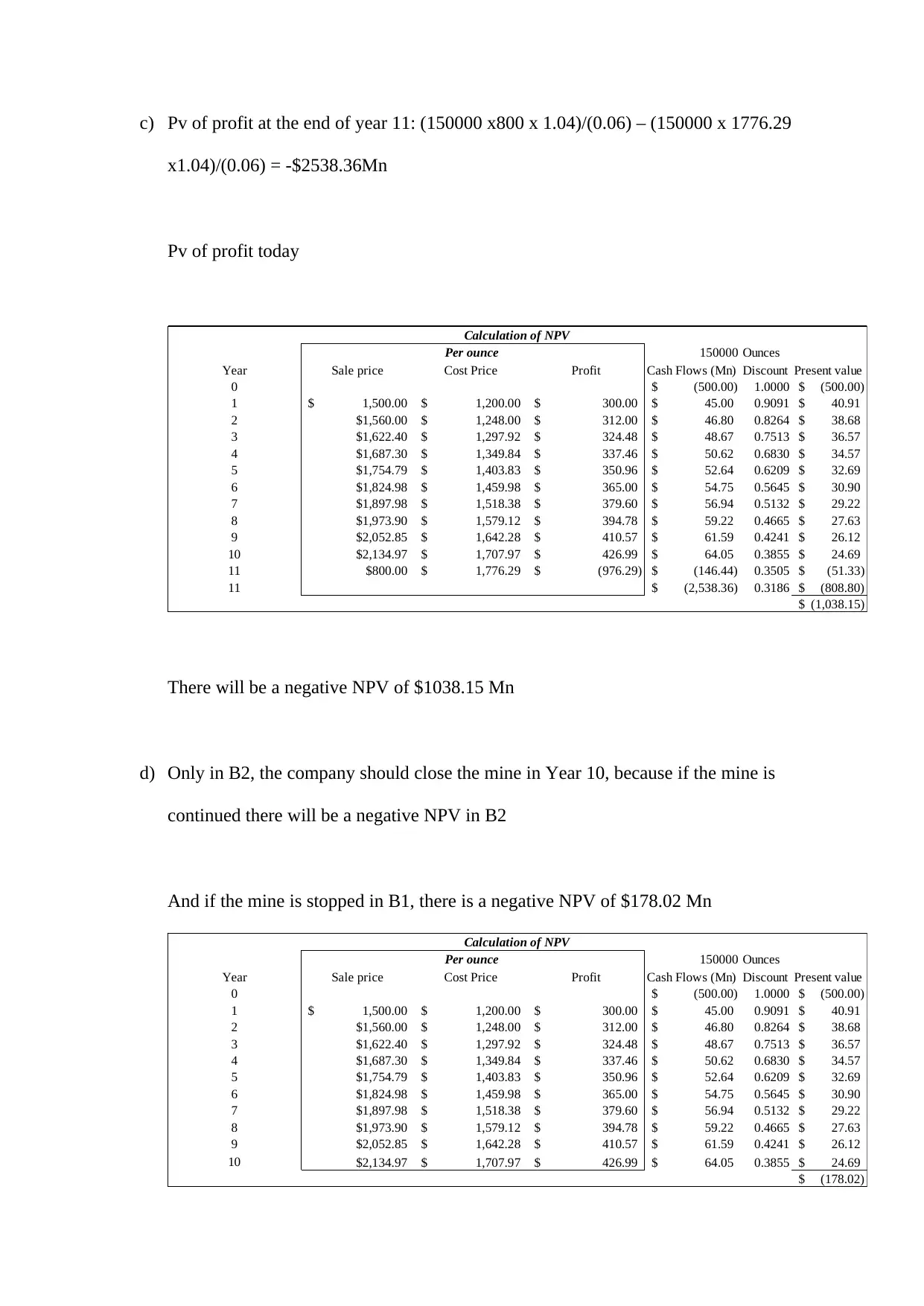

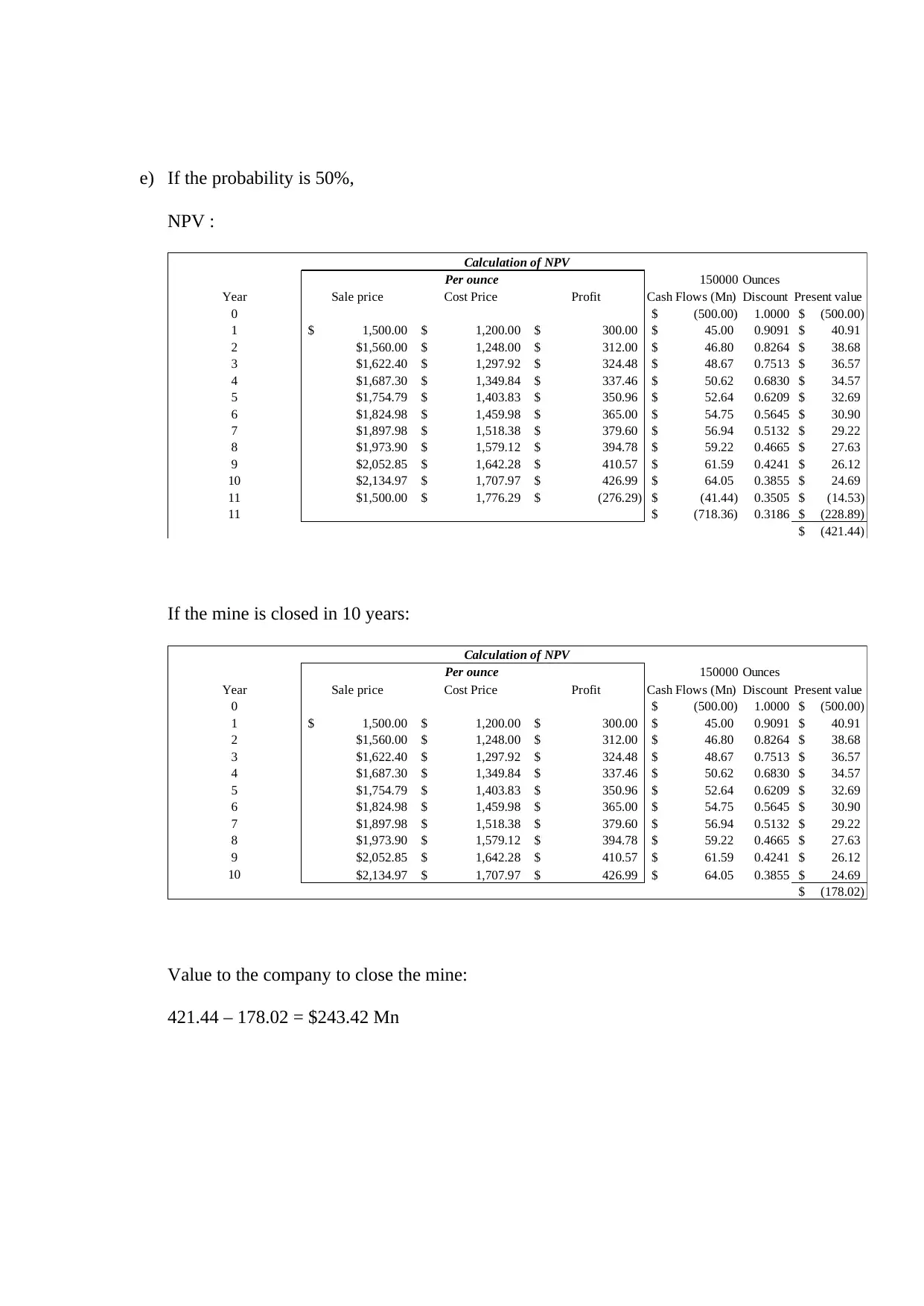

This assignment solution delves into various capital budgeting techniques, including Net Present Value (NPV), Internal Rate of Return (IRR), and Weighted Average Cost of Capital (WACC), to evaluate investment decisions. The analysis includes calculating NPV for different scenarios, determining the appropriate discount rates using WACC, and assessing the impact of debt and equity financing. Furthermore, the solution explores bond valuation, examining the relationship between coupon rates, interest rates, and bond prices. It also addresses the importance of considering project-specific risks and the timing of cash flows in capital budgeting. The assignment concludes with a case study involving a gold mine, where the student applies these concepts to determine the optimal time to close the mine based on NPV calculations under different scenarios.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.