Analysis of Rosetta Stone's IPO and Valuation Methods

VerifiedAdded on 2019/12/28

|14

|3462

|69

Report

AI Summary

This report provides an in-depth analysis of the Rosetta Stone IPO, examining its business model, and strategic initiatives. It delves into the IPO process, detailing the steps involved and discussing the advantages and disadvantages of going public. The report employs various valuation methods, including market-multiples and discounted cash flow, to determine a fair share price range. It calculates the reasonable rate of return, cost of equity, and weighted average cost of capital (WACC) to assess the financial feasibility of the IPO. The report includes detailed calculations of cash flows, enterprise value, and equity value, culminating in an offer price recommendation for the IPO. Working notes and illustrations support the financial analysis, providing a comprehensive overview of the company's financial position and the rationale behind the valuation.

FINANCING ENTERPRISE

INITIATIVE

INITIATIVE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Rosetta Stone introduction...............................................................................................................3

1. Characteristics of Rosetta Stone's business model and its strategy....................................3

2. IPO process and its advantages as well as disadvantage....................................................4

3. Market-Multiples approach to identify range of prices for an IPO....................................7

4. Market-Multiple approach and its use for identifying fair value of shares........................7

5 Reasonable rate of return for Rosetta Stone shares .........................................................10

6 Cash flow model and explanation on calculations...........................................................10

7 Offer price for IPO............................................................................................................12

REFERENCES..............................................................................................................................13

ILLUSTRATION INDEX

Illustration 1: Average of EV/EBITDA for 2008............................................................................8

Illustration 2: Average of EV/EBITDA for 2009...........................................................................8

Illustration 3: PE ratio for 2008.......................................................................................................8

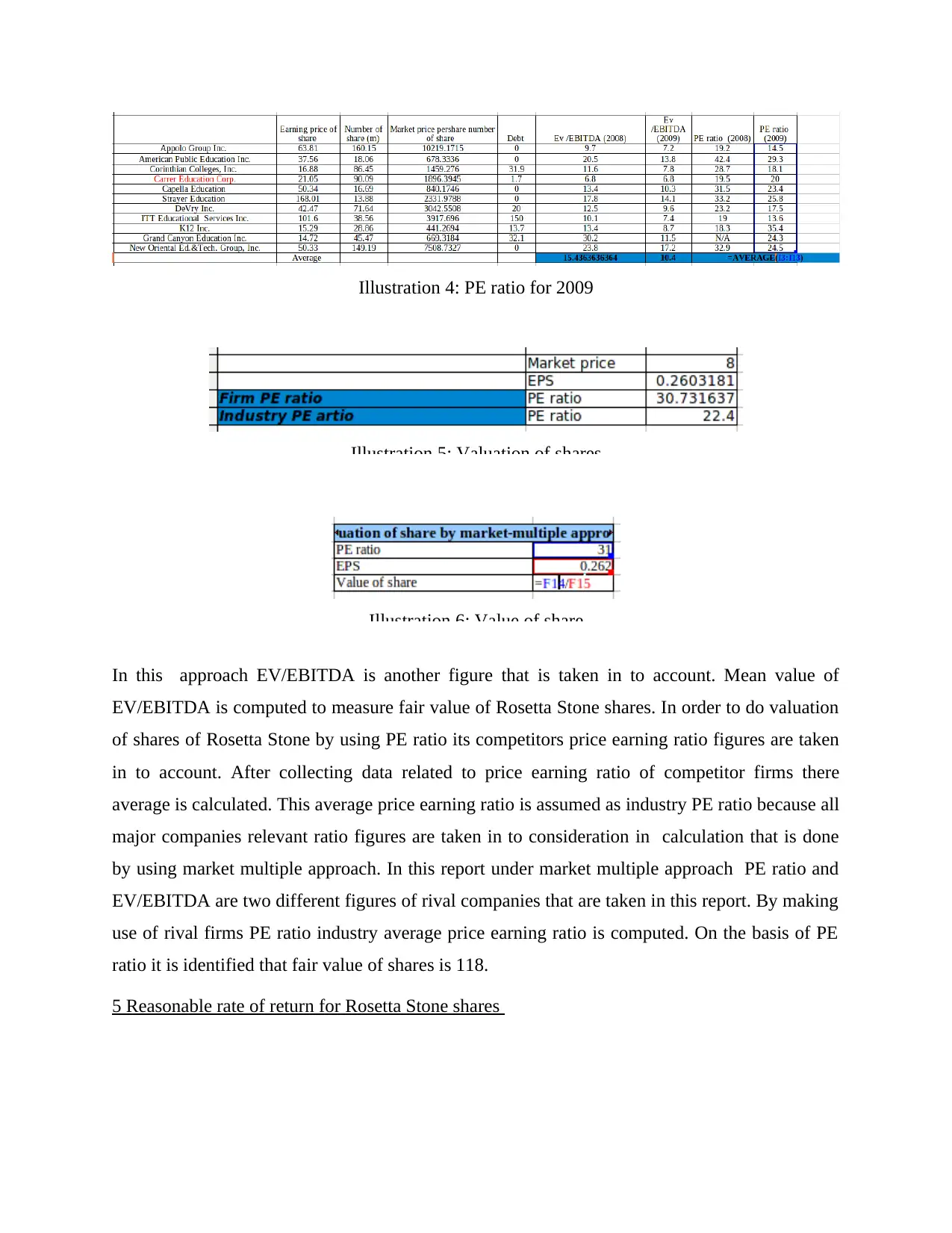

Illustration 4: PE ratio for 2009.......................................................................................................9

Illustration 5: Valuation of shares....................................................................................................9

Illustration 6: Value of share............................................................................................................9

Illustration 7: Required rate of return............................................................................................10

Illustration 8: Calculation of cost of equity...................................................................................10

Illustration 9: Calculation of Enterprise value...............................................................................10

Illustration 10: WACC calculation................................................................................................10

Illustration 11: Calculation of cash flows......................................................................................11

Illustration 12: Computation of present value...............................................................................11

Illustration 13: Calculation of equity value...................................................................................11

Illustration 14: Calculation of intrinsic value of shares.................................................................12

Rosetta Stone introduction...............................................................................................................3

1. Characteristics of Rosetta Stone's business model and its strategy....................................3

2. IPO process and its advantages as well as disadvantage....................................................4

3. Market-Multiples approach to identify range of prices for an IPO....................................7

4. Market-Multiple approach and its use for identifying fair value of shares........................7

5 Reasonable rate of return for Rosetta Stone shares .........................................................10

6 Cash flow model and explanation on calculations...........................................................10

7 Offer price for IPO............................................................................................................12

REFERENCES..............................................................................................................................13

ILLUSTRATION INDEX

Illustration 1: Average of EV/EBITDA for 2008............................................................................8

Illustration 2: Average of EV/EBITDA for 2009...........................................................................8

Illustration 3: PE ratio for 2008.......................................................................................................8

Illustration 4: PE ratio for 2009.......................................................................................................9

Illustration 5: Valuation of shares....................................................................................................9

Illustration 6: Value of share............................................................................................................9

Illustration 7: Required rate of return............................................................................................10

Illustration 8: Calculation of cost of equity...................................................................................10

Illustration 9: Calculation of Enterprise value...............................................................................10

Illustration 10: WACC calculation................................................................................................10

Illustration 11: Calculation of cash flows......................................................................................11

Illustration 12: Computation of present value...............................................................................11

Illustration 13: Calculation of equity value...................................................................................11

Illustration 14: Calculation of intrinsic value of shares.................................................................12

Rosetta Stone introduction

Rosetta Stone is the firm that is across the globe for developing software's by using which

one can easily learn programming languages. Firm wants to bring its IPO in the market to raise

funds that will be used to make heavy investment in the business. In order to determine fair value

of share to determine offer price some specific methods like discounted cash flow and multiple

method are used in the report. At end of the report working notes are enclosed in image format

and briefly same are discussed.

1. Characteristics of Rosetta Stone's business model and its strategy

In current time period there is heavy demand of the experts that have expertise in specific

programming language. In this regard there are several websites where students visit and lean

new things. Rosetta stone develop its own software's by using which one can easily learn

programming languages. Firm is making available programming language related solutions to

the students and those who intends to learn programming language. With passage of time firm is

adding many new things in its software's or it can be said that it bring updates on same with

passage of specific duration. Rosetta stone understand that competition is fierce and it is very

important to remain in the market. Hence, it is focusing on eliminating its competitors and in this

regard in past years it purchase many firms. Some of the firms that are acquired by the Rosetta

stone are Tell Me More and Livemocha etc (Cullinan and Zheng, 2014). The main advantage of

merger and acquisition is that through this firm is able to get access to infrastructure that belong

to other company. Firms does not need to spend time on developing its own infrastructure of

technology base. It can be said that merger and acquisition that are done by the firms to great

extent helps firm in increasing its business size. Rosetta stone have individual customer's and

business customer's and according to there needs to develop its products. Company is paying

due attention on developing its core competency because it is a thing that provide edge to the

firm over its competitors. Firm is focusing on developing a workforce that is highly competent

and in this regard it is hiring talented candidates as its employees. The main thing that company

is doing is that it is not dependent on single product line in order to earn profit (Bricker and

Chandar, 2012). It can be said that firm is offering multiple products to meet the needs of

customer's. Presently, in its product portfolio there are products that meet needs of individuals,

business customers and government departments etc. it can be said that firm is focusing on same

Rosetta Stone is the firm that is across the globe for developing software's by using which

one can easily learn programming languages. Firm wants to bring its IPO in the market to raise

funds that will be used to make heavy investment in the business. In order to determine fair value

of share to determine offer price some specific methods like discounted cash flow and multiple

method are used in the report. At end of the report working notes are enclosed in image format

and briefly same are discussed.

1. Characteristics of Rosetta Stone's business model and its strategy

In current time period there is heavy demand of the experts that have expertise in specific

programming language. In this regard there are several websites where students visit and lean

new things. Rosetta stone develop its own software's by using which one can easily learn

programming languages. Firm is making available programming language related solutions to

the students and those who intends to learn programming language. With passage of time firm is

adding many new things in its software's or it can be said that it bring updates on same with

passage of specific duration. Rosetta stone understand that competition is fierce and it is very

important to remain in the market. Hence, it is focusing on eliminating its competitors and in this

regard in past years it purchase many firms. Some of the firms that are acquired by the Rosetta

stone are Tell Me More and Livemocha etc (Cullinan and Zheng, 2014). The main advantage of

merger and acquisition is that through this firm is able to get access to infrastructure that belong

to other company. Firms does not need to spend time on developing its own infrastructure of

technology base. It can be said that merger and acquisition that are done by the firms to great

extent helps firm in increasing its business size. Rosetta stone have individual customer's and

business customer's and according to there needs to develop its products. Company is paying

due attention on developing its core competency because it is a thing that provide edge to the

firm over its competitors. Firm is focusing on developing a workforce that is highly competent

and in this regard it is hiring talented candidates as its employees. The main thing that company

is doing is that it is not dependent on single product line in order to earn profit (Bricker and

Chandar, 2012). It can be said that firm is offering multiple products to meet the needs of

customer's. Presently, in its product portfolio there are products that meet needs of individuals,

business customers and government departments etc. it can be said that firm is focusing on same

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

type of product but in same it is offering different varieties to meet needs of different type of

people. Firm is focusing on innovating its existing product line and developing new features in

its product. It can be said that this is the thing that is differentiating firm from its competitors.

Rosetta stone makes investment on its research and development projects in order to enable itself

to add new features on its software. Firm understand that it needs to make heavy investment on

its project and on same time it is equal important to maintain profit in the business. Thus, it is

following cost control strategy in its business so as to elevate profitability in the business to

maximum level. In order to implement its cost control strategy firm is purchasing material in

optimum quantity and it is also following good cash management strategy in its business (Ayadi

and Wang, 2013). Gradually, Rosetta stone is shifting from its traditional product line and now it

is involved in developing varied sort of applications. This step will help firm is increasing its

customer's base. It can be said that this product line will to some extent reduce firm dependency

on traditional products.

2. IPO process and its advantages as well as disadvantage

There are many operations and process through which Rosetta stone needs to pass in order to

launch its IPO.SEC is the regulatory authority that looks after entire process of listing of shares

and launch of IPO. It laid down some important parameters or standard that firm which intends

to issue shares in the market needs to follow in order to issue shares. These standards are

determined in terms of profit that must be earn by the firm in number of years under specific

duration. There are many other parameters that an organisation need to pass in order to issue

IPO. Steps that company needs to follow in order to issue its shares are given below.

1. Creating pitch: It is well known fact that there are many steps that managers of an

organization needs to follow or comply with in order to issue shares. In this regard

management of the firm collect all required information and carry out detail discussion

reading preparation of plan that will be followed to complete all require formalities

(Fernández Gimeno and et.al., 2012). In this stage managers will undertake meeting with

the underwriters and will convince them to purchase shares in case they are not

subscribed partially by the public.

2. Kick-off meeting: After determining each and every thing managers of the Rosetta stone

will conduct meeting with the important entities that will play major role in in facilitating

operations related to launch of IPO in the market. Some of these entities are investment

people. Firm is focusing on innovating its existing product line and developing new features in

its product. It can be said that this is the thing that is differentiating firm from its competitors.

Rosetta stone makes investment on its research and development projects in order to enable itself

to add new features on its software. Firm understand that it needs to make heavy investment on

its project and on same time it is equal important to maintain profit in the business. Thus, it is

following cost control strategy in its business so as to elevate profitability in the business to

maximum level. In order to implement its cost control strategy firm is purchasing material in

optimum quantity and it is also following good cash management strategy in its business (Ayadi

and Wang, 2013). Gradually, Rosetta stone is shifting from its traditional product line and now it

is involved in developing varied sort of applications. This step will help firm is increasing its

customer's base. It can be said that this product line will to some extent reduce firm dependency

on traditional products.

2. IPO process and its advantages as well as disadvantage

There are many operations and process through which Rosetta stone needs to pass in order to

launch its IPO.SEC is the regulatory authority that looks after entire process of listing of shares

and launch of IPO. It laid down some important parameters or standard that firm which intends

to issue shares in the market needs to follow in order to issue shares. These standards are

determined in terms of profit that must be earn by the firm in number of years under specific

duration. There are many other parameters that an organisation need to pass in order to issue

IPO. Steps that company needs to follow in order to issue its shares are given below.

1. Creating pitch: It is well known fact that there are many steps that managers of an

organization needs to follow or comply with in order to issue shares. In this regard

management of the firm collect all required information and carry out detail discussion

reading preparation of plan that will be followed to complete all require formalities

(Fernández Gimeno and et.al., 2012). In this stage managers will undertake meeting with

the underwriters and will convince them to purchase shares in case they are not

subscribed partially by the public.

2. Kick-off meeting: After determining each and every thing managers of the Rosetta stone

will conduct meeting with the important entities that will play major role in in facilitating

operations related to launch of IPO in the market. Some of these entities are investment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

bank and underwriters etc. Decision on number of things will be taken under this step by

taking advise from important stakeholders. In this stage it is member of the Investment

bank that will communicate the offer price for share at which shares can be issued in the

primary market. There are various models that are used by investment bank to determine

offer price of shares. Some of these methods are discounted cash flow and multiple

method. The work of preparation of prospectus is given to the investment banker and in

this meeting it present same before top managers. It is like a book in which detail

information is provided about the firm business its profitability, future plans and places

where it will make an investment. When investors will subscribe share at that time they

will receive prospectus (Branch, Ma and Sawyer, 2010). Prospectus are also available on

internet and investors can download same from firm website.

3. Filling registration statement and due diligence: In this stage registration statement is

filed in the office of SEC by the firm that wants to launch its IPO in the primary market.

In this stage copy of agreement that is signed by the firm with an underwriter is also filed

in the SEC. Along with this, documents like charter and a specimen of security will also

be filled with SEC. It is important for the firm to obtain due diligence certificate which is

proof of the fact that Rosetta Stone had followed all rules and regulations in systematic

way to launch its IPO. This certificate is issued after all documents are submitted by the

firm with SEC. It can be said that it is one of the most important step and after clearing

this stage one can launch its IPO.

4. SEC review: Under previous stage all required documents are submitted with SEC but

they are not checked by the regulatory authority. In this stage after issuance of due

diligence certificate documents are checked and verified by SEC. Detail procedure is

followed for verifying documents and it is ensured that fraud is not done by the firm to

list its shares. If in any case it is identified that firm dos not make available accurate

document that regulatory authority will send letter of comment to the firm and will give

20 days time to again fill registration form with the former entity (Lenkey, 2015).

5. Road show: In this stage firm will make an efforts to establish contact with the people or

large business entities and will asked them to make investment in firm shares. Road

shows of one to two weeks will be organized by the underwriter from firm side.

taking advise from important stakeholders. In this stage it is member of the Investment

bank that will communicate the offer price for share at which shares can be issued in the

primary market. There are various models that are used by investment bank to determine

offer price of shares. Some of these methods are discounted cash flow and multiple

method. The work of preparation of prospectus is given to the investment banker and in

this meeting it present same before top managers. It is like a book in which detail

information is provided about the firm business its profitability, future plans and places

where it will make an investment. When investors will subscribe share at that time they

will receive prospectus (Branch, Ma and Sawyer, 2010). Prospectus are also available on

internet and investors can download same from firm website.

3. Filling registration statement and due diligence: In this stage registration statement is

filed in the office of SEC by the firm that wants to launch its IPO in the primary market.

In this stage copy of agreement that is signed by the firm with an underwriter is also filed

in the SEC. Along with this, documents like charter and a specimen of security will also

be filled with SEC. It is important for the firm to obtain due diligence certificate which is

proof of the fact that Rosetta Stone had followed all rules and regulations in systematic

way to launch its IPO. This certificate is issued after all documents are submitted by the

firm with SEC. It can be said that it is one of the most important step and after clearing

this stage one can launch its IPO.

4. SEC review: Under previous stage all required documents are submitted with SEC but

they are not checked by the regulatory authority. In this stage after issuance of due

diligence certificate documents are checked and verified by SEC. Detail procedure is

followed for verifying documents and it is ensured that fraud is not done by the firm to

list its shares. If in any case it is identified that firm dos not make available accurate

document that regulatory authority will send letter of comment to the firm and will give

20 days time to again fill registration form with the former entity (Lenkey, 2015).

5. Road show: In this stage firm will make an efforts to establish contact with the people or

large business entities and will asked them to make investment in firm shares. Road

shows of one to two weeks will be organized by the underwriter from firm side.

6. Pricing meeting: In this stage negotiation round is carried out with the underwriter in

relation to share price. Detail discussion is carried out on the extent up to which discount

will be given to the underwriters when they will make purchase of shares in case they

remain unsubscribe from general public.

7. Allocation: In this stage syndicate members of the firm will sale there shares in the

primary market and those who wants to make purchase of shares will buy same.

Underwriters will get information about same and under this copy of sales confirmation

will be provided to the underwriters (Kisaka, S.E. and et.al., 2014). It can be said that this

stage is also very important in IPO process.

8. Trading: It is a final stage in which trading get commenced and people or firms start

making investment in the firm. After ten days from commencing date purchase of shares

in the IPO get closed. After this security certificate is issued to the underwriter and

comfort letter is given to the individual.

Advantage of IPO

The main advantage of IPO is that it helps firm in adjusting its finance cost. If firm will

only finance its operations by taking a debt then its interest cost will increase. Rosetta

Stone will need to pay interest every year irrespective of its profitability. On other hand,

in case of equity it is not necessary to pay dividend every year. It is clear that equity helps

in adjusting finance cost.

When firm launch its IPO its name become popular among the people. This help firm in

establishing its business relationship with new entities. Contrary to this, if firm never

issue shares in primary market then other entities after considering lots of factors

establish business relationship with the firm (Souther,2016). It can be said that IPO not

only help firm in raising capital but it also help it in creating its good image among the

customer's. By issue of shares company bring balance in its capital structure and maintain equal

proportion of both in the IPO. This help firm in maintaining its good performance in the

business.

Disadvantage of IPO

When firm issue its shares control of owners of the firm get diluted and there decision

making power get reduced.

relation to share price. Detail discussion is carried out on the extent up to which discount

will be given to the underwriters when they will make purchase of shares in case they

remain unsubscribe from general public.

7. Allocation: In this stage syndicate members of the firm will sale there shares in the

primary market and those who wants to make purchase of shares will buy same.

Underwriters will get information about same and under this copy of sales confirmation

will be provided to the underwriters (Kisaka, S.E. and et.al., 2014). It can be said that this

stage is also very important in IPO process.

8. Trading: It is a final stage in which trading get commenced and people or firms start

making investment in the firm. After ten days from commencing date purchase of shares

in the IPO get closed. After this security certificate is issued to the underwriter and

comfort letter is given to the individual.

Advantage of IPO

The main advantage of IPO is that it helps firm in adjusting its finance cost. If firm will

only finance its operations by taking a debt then its interest cost will increase. Rosetta

Stone will need to pay interest every year irrespective of its profitability. On other hand,

in case of equity it is not necessary to pay dividend every year. It is clear that equity helps

in adjusting finance cost.

When firm launch its IPO its name become popular among the people. This help firm in

establishing its business relationship with new entities. Contrary to this, if firm never

issue shares in primary market then other entities after considering lots of factors

establish business relationship with the firm (Souther,2016). It can be said that IPO not

only help firm in raising capital but it also help it in creating its good image among the

customer's. By issue of shares company bring balance in its capital structure and maintain equal

proportion of both in the IPO. This help firm in maintaining its good performance in the

business.

Disadvantage of IPO

When firm issue its shares control of owners of the firm get diluted and there decision

making power get reduced.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of equity is always higher then equity which means that amount of dividend paid by

the firm is always high then interest amount.

3. Market-Multiples approach to identify range of prices for an IPO

It totally different methods of valuation because under this method if one is doing

valuation of shares then he will make use of other companies shares that belongs to same price

range. This method is commonly used by the investors in order to do valuation of shares. In the

market multiple method there are number of things that are considered for valuation of shares

like earning per share, PE ratio and market price. Price earning ratio is one of the most important

ratio because it helps one to measure whether shares are overvalued or undervalued (Ji and Kim,

2013). Under this method first of all company PE ratio is computed and then it is compared with

the industry price earning ratio in order to identify whether shares of the specific firm are fairly

valued. If any case if equity research analyst find that PE ratio of the firm is above industry PE

ratio then it means that shares are overvalued and they are not trading in stock exchange at fair

value. Contrary to this if it is identified that price earning ratio of the firm is below industry ratio

then it indicate that firm shares are undervalued and they are available at fair value. In this case

companies like Apollo Group Inc and American Public Education Inc etc are taken in to

consideration for doing calculation. DCF analysis is the another method of valuation that is used

in this report which is used to compute intrinsic value of shares. In this enterprise value is also

computed which reflects entire capitalization amount of the firm. It can be said that by using

multiple methods shares are valued in proper way.

4. Market-Multiple approach and its use for identifying fair value of shares

Market multiple method and discounted cash flow model both are different approaches that are

used for doing valuation of shares. The main difference between both methods is that in market

multiple approach competitors firms data is also taken in to consideration (Cullinan and Zheng,

2012). Whereas, in case of discounted cash flow model firm data is used to do valuation of share.

Following calculations are done to do valuation of shares on the basis of market multiple

approach.

the firm is always high then interest amount.

3. Market-Multiples approach to identify range of prices for an IPO

It totally different methods of valuation because under this method if one is doing

valuation of shares then he will make use of other companies shares that belongs to same price

range. This method is commonly used by the investors in order to do valuation of shares. In the

market multiple method there are number of things that are considered for valuation of shares

like earning per share, PE ratio and market price. Price earning ratio is one of the most important

ratio because it helps one to measure whether shares are overvalued or undervalued (Ji and Kim,

2013). Under this method first of all company PE ratio is computed and then it is compared with

the industry price earning ratio in order to identify whether shares of the specific firm are fairly

valued. If any case if equity research analyst find that PE ratio of the firm is above industry PE

ratio then it means that shares are overvalued and they are not trading in stock exchange at fair

value. Contrary to this if it is identified that price earning ratio of the firm is below industry ratio

then it indicate that firm shares are undervalued and they are available at fair value. In this case

companies like Apollo Group Inc and American Public Education Inc etc are taken in to

consideration for doing calculation. DCF analysis is the another method of valuation that is used

in this report which is used to compute intrinsic value of shares. In this enterprise value is also

computed which reflects entire capitalization amount of the firm. It can be said that by using

multiple methods shares are valued in proper way.

4. Market-Multiple approach and its use for identifying fair value of shares

Market multiple method and discounted cash flow model both are different approaches that are

used for doing valuation of shares. The main difference between both methods is that in market

multiple approach competitors firms data is also taken in to consideration (Cullinan and Zheng,

2012). Whereas, in case of discounted cash flow model firm data is used to do valuation of share.

Following calculations are done to do valuation of shares on the basis of market multiple

approach.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

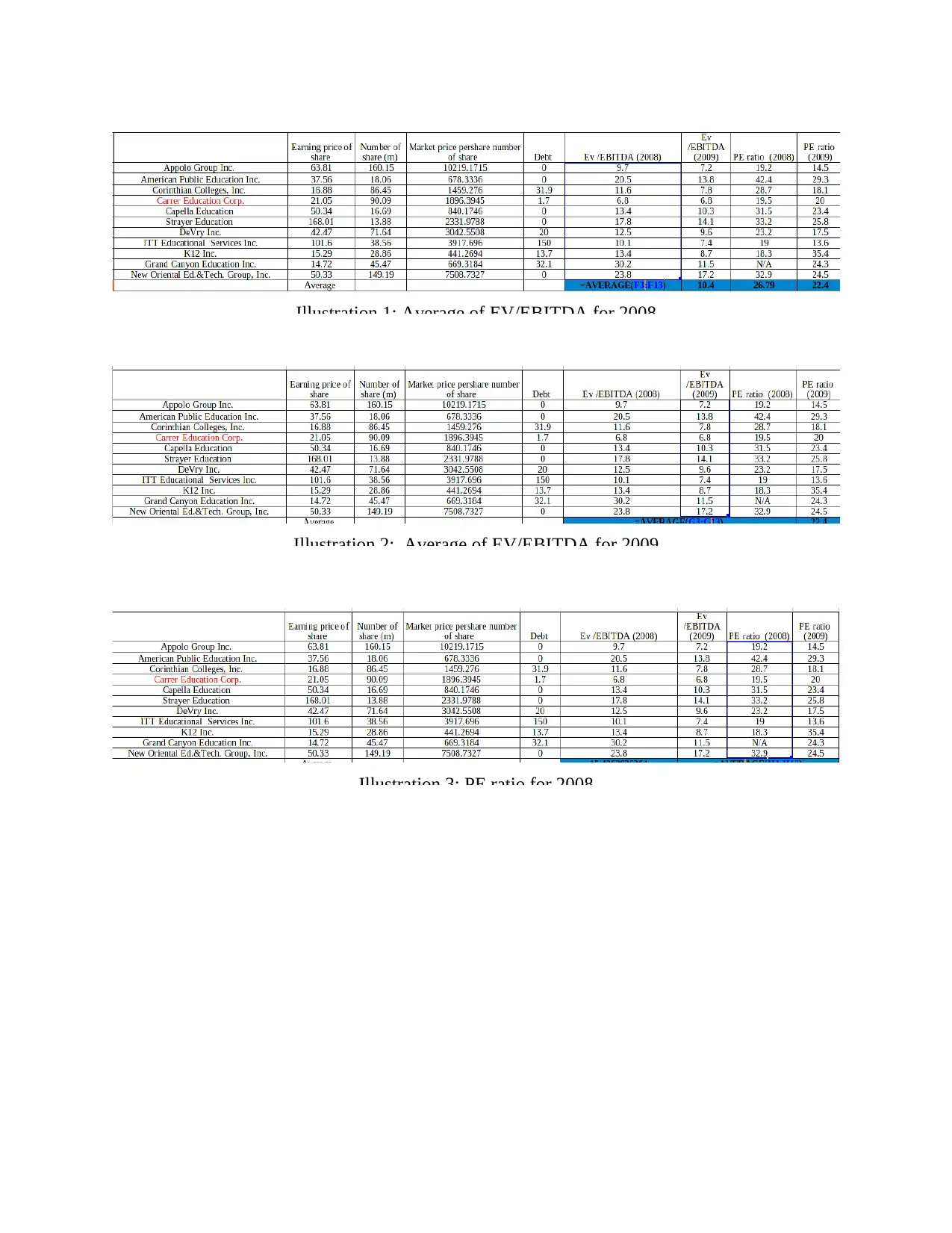

Illustration 1: Average of EV/EBITDA for 2008

Illustration 2: Average of EV/EBITDA for 2009

Illustration 3: PE ratio for 2008

Illustration 2: Average of EV/EBITDA for 2009

Illustration 3: PE ratio for 2008

Illustration 4: PE ratio for 2009

In this approach EV/EBITDA is another figure that is taken in to account. Mean value of

EV/EBITDA is computed to measure fair value of Rosetta Stone shares. In order to do valuation

of shares of Rosetta Stone by using PE ratio its competitors price earning ratio figures are taken

in to account. After collecting data related to price earning ratio of competitor firms there

average is calculated. This average price earning ratio is assumed as industry PE ratio because all

major companies relevant ratio figures are taken in to consideration in calculation that is done

by using market multiple approach. In this report under market multiple approach PE ratio and

EV/EBITDA are two different figures of rival companies that are taken in this report. By making

use of rival firms PE ratio industry average price earning ratio is computed. On the basis of PE

ratio it is identified that fair value of shares is 118.

5 Reasonable rate of return for Rosetta Stone shares

Illustration 6: Value of share

Illustration 5: Valuation of shares

In this approach EV/EBITDA is another figure that is taken in to account. Mean value of

EV/EBITDA is computed to measure fair value of Rosetta Stone shares. In order to do valuation

of shares of Rosetta Stone by using PE ratio its competitors price earning ratio figures are taken

in to account. After collecting data related to price earning ratio of competitor firms there

average is calculated. This average price earning ratio is assumed as industry PE ratio because all

major companies relevant ratio figures are taken in to consideration in calculation that is done

by using market multiple approach. In this report under market multiple approach PE ratio and

EV/EBITDA are two different figures of rival companies that are taken in this report. By making

use of rival firms PE ratio industry average price earning ratio is computed. On the basis of PE

ratio it is identified that fair value of shares is 118.

5 Reasonable rate of return for Rosetta Stone shares

Illustration 6: Value of share

Illustration 5: Valuation of shares

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

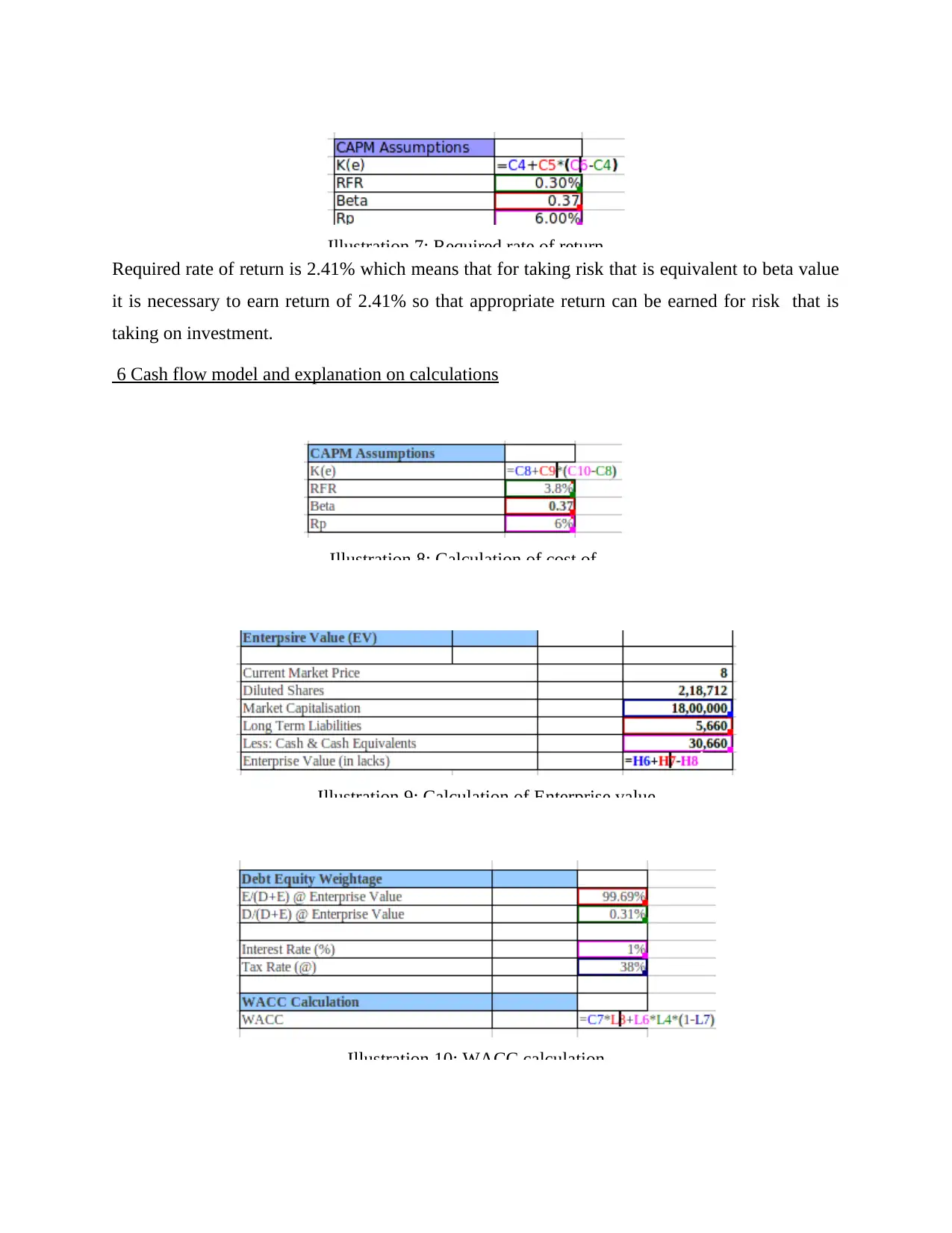

Required rate of return is 2.41% which means that for taking risk that is equivalent to beta value

it is necessary to earn return of 2.41% so that appropriate return can be earned for risk that is

taking on investment.

6 Cash flow model and explanation on calculations

Illustration 7: Required rate of return

Illustration 8: Calculation of cost of

Illustration 9: Calculation of Enterprise value

Illustration 10: WACC calculation

it is necessary to earn return of 2.41% so that appropriate return can be earned for risk that is

taking on investment.

6 Cash flow model and explanation on calculations

Illustration 7: Required rate of return

Illustration 8: Calculation of cost of

Illustration 9: Calculation of Enterprise value

Illustration 10: WACC calculation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Illustration 11: Calculation of cash flows

Illustration 12: Computation of present value

Illustration 13: Calculation of equity value

Illustration 12: Computation of present value

Illustration 13: Calculation of equity value

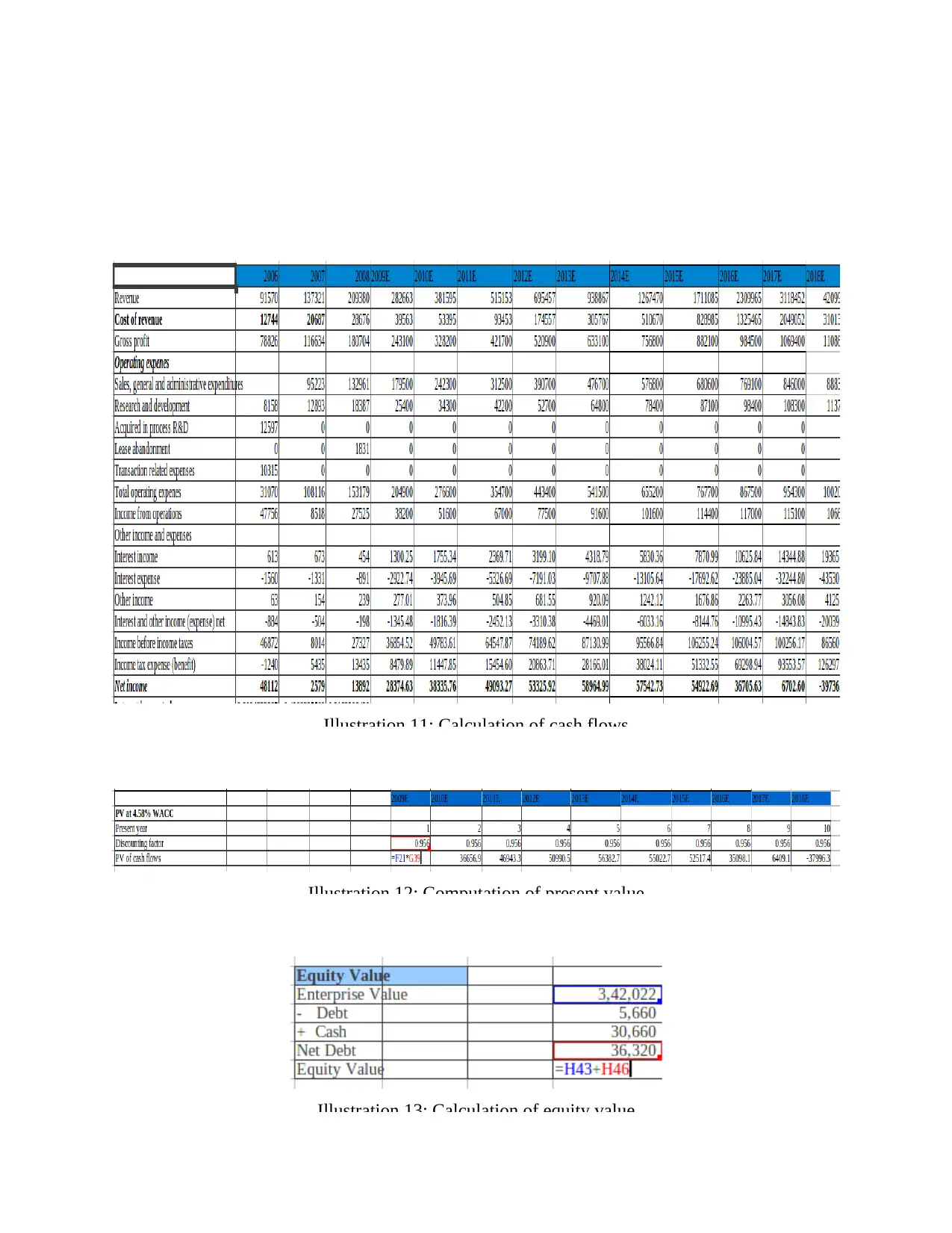

In this model first of all WACC is computed using cost of equity, interest, market capitalization

and debt values. This is computed by using formulae Ke*weight of equity+Kd*weight of

debt*(1-tax rate) (Discounted cash flow model (DCF) analysis, 2016). After this cash flows are

computed on the basis of inputs provided by PDF. Finally, present value of cash flow is

computed and then by using equity value intrinsic value is computed.

7 Offer price for IPO

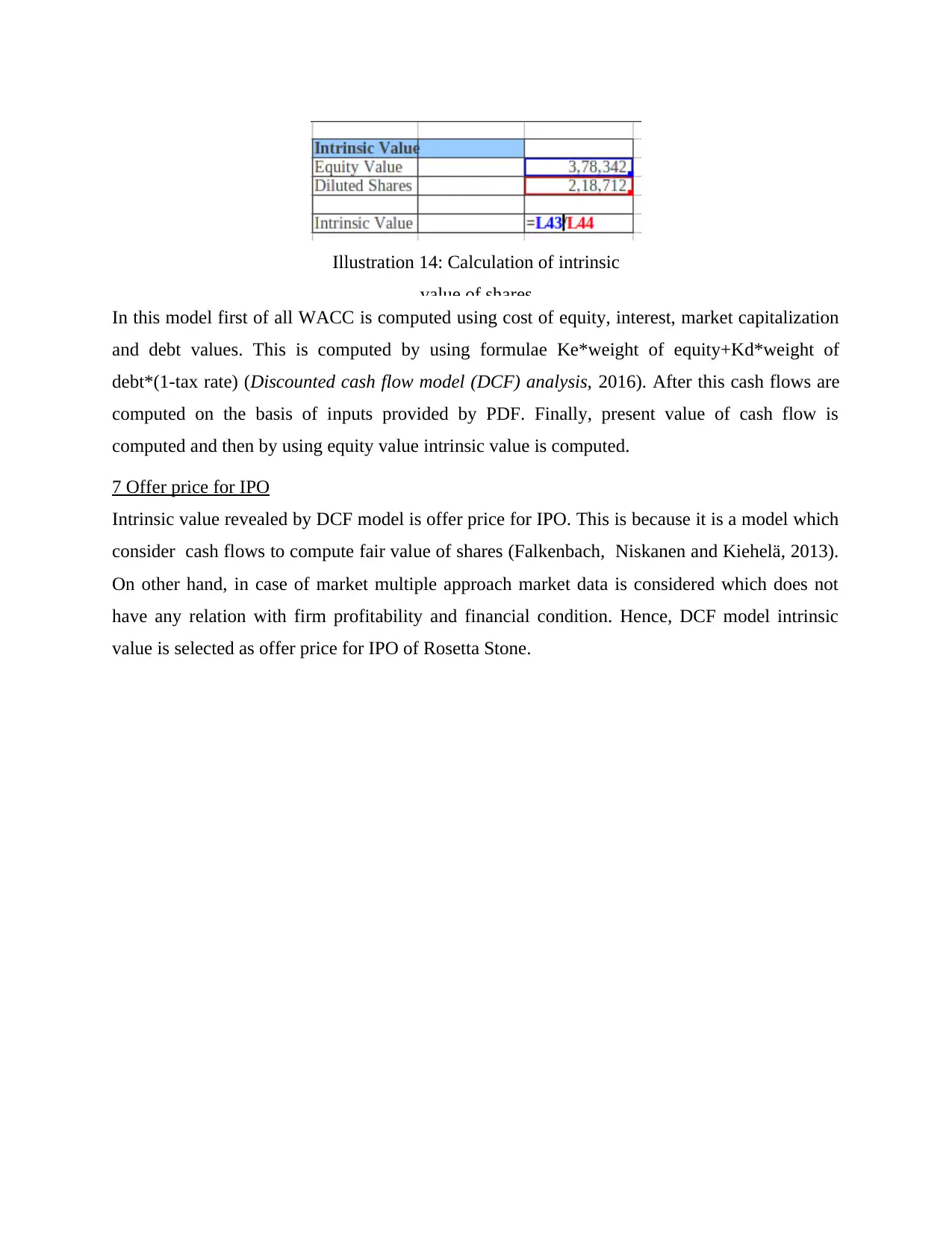

Intrinsic value revealed by DCF model is offer price for IPO. This is because it is a model which

consider cash flows to compute fair value of shares (Falkenbach, Niskanen and Kiehelä, 2013).

On other hand, in case of market multiple approach market data is considered which does not

have any relation with firm profitability and financial condition. Hence, DCF model intrinsic

value is selected as offer price for IPO of Rosetta Stone.

Illustration 14: Calculation of intrinsic

value of shares

and debt values. This is computed by using formulae Ke*weight of equity+Kd*weight of

debt*(1-tax rate) (Discounted cash flow model (DCF) analysis, 2016). After this cash flows are

computed on the basis of inputs provided by PDF. Finally, present value of cash flow is

computed and then by using equity value intrinsic value is computed.

7 Offer price for IPO

Intrinsic value revealed by DCF model is offer price for IPO. This is because it is a model which

consider cash flows to compute fair value of shares (Falkenbach, Niskanen and Kiehelä, 2013).

On other hand, in case of market multiple approach market data is considered which does not

have any relation with firm profitability and financial condition. Hence, DCF model intrinsic

value is selected as offer price for IPO of Rosetta Stone.

Illustration 14: Calculation of intrinsic

value of shares

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.