Financial and Economic Literacy Report: UK Macroeconomic Analysis

VerifiedAdded on 2021/04/21

|21

|4203

|48

Report

AI Summary

This report provides a detailed analysis of financial and economic literacy, focusing on the UK market. It begins with an examination of small and medium-sized enterprises (SMEs) and their role in the UK economy, followed by a case study on the Waitrose supermarket chain, including its market structure, growth, and marketing strategies. The report then delves into the UK housing market, exploring factors affecting demand and supply, interest rates, and the Bank of England's interventions. Finally, it assesses the macroeconomic performance of the UK, covering output performance (GDP), labor market indicators (unemployment), and price level movements. The report integrates statistical data and economic principles to provide a comprehensive overview of the topics discussed.

Running Head: FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Financial and Economic Literacy for Managers

Name of the Student

Name of the University

Author note

Financial and Economic Literacy for Managers

Name of the Student

Name of the University

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Table of Contents

Answer to question 1..................................................................................................................2

Waitrose.................................................................................................................................2

Market structure of supermarket chain in UK........................................................................2

Growth and Marketing strategy of Waitrose..........................................................................3

Answer to question 2..................................................................................................................5

Factor affecting demand of housing.......................................................................................5

Interest rate.............................................................................................................................6

Factors affecting supply of housing.......................................................................................8

Bank of England’s action in the housing market...................................................................9

Answer to question 3................................................................................................................10

Output Performance.............................................................................................................10

Labor market performance...................................................................................................13

Movement of Price level......................................................................................................14

Answer to question 4:...............................................................................................................15

Answer to question 5:...............................................................................................................17

Answer to A:........................................................................................................................17

Answer to B:........................................................................................................................19

Answer to C:........................................................................................................................19

Reference List:.........................................................................................................................21

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Table of Contents

Answer to question 1..................................................................................................................2

Waitrose.................................................................................................................................2

Market structure of supermarket chain in UK........................................................................2

Growth and Marketing strategy of Waitrose..........................................................................3

Answer to question 2..................................................................................................................5

Factor affecting demand of housing.......................................................................................5

Interest rate.............................................................................................................................6

Factors affecting supply of housing.......................................................................................8

Bank of England’s action in the housing market...................................................................9

Answer to question 3................................................................................................................10

Output Performance.............................................................................................................10

Labor market performance...................................................................................................13

Movement of Price level......................................................................................................14

Answer to question 4:...............................................................................................................15

Answer to question 5:...............................................................................................................17

Answer to A:........................................................................................................................17

Answer to B:........................................................................................................................19

Answer to C:........................................................................................................................19

Reference List:.........................................................................................................................21

2

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Answer to question 1

Small and Medium sized enterprises provide a great support to UK economy. The

expansion strategies of SMEs open up new market and create new job opportunities. In order

to grow bigger these companies invest in innovation leading to intense competition in the

marketplace. As per 2014 statistics, UK has nearly 5.2 million SMEs. In UK, a wide majority

of business is currently employing less than 10 people, accounted for 33 percent employment

and enjoys a turnover of 19 percent (uk.wsj.com 2018). However, the small and medium

enterprises has accounted a disproportionate growth rate. It is found that 6% of total SMEs in

UK experience higher growth rate and responsible for generating fifty percent of new jobs

between 2002 and 2008 (fsb.org.uk, 2018). The grocery supermarket chain in UK is one of

the interesting aspect to be discussed. The supermarket chains some large and small retailers.

Waitrose

Waitrose belongs to the chain of British supermarket structure, forming the division

of food retailers in Britain. It has nearly 352 branches in United Kingdom. Among these

branches 30 are convenience shops. Currently Waitrose occupies a market share of 5.1

percent in grocery supermarket chain.

Market structure of supermarket chain in UK

The supermarket structure in UK resembles the feature of an oligopoly market. An

oligopoly market is characterized by the dominance of few large firms in the market (Sloman

and Jones 2017). The grocery supermarket in UK is now increasingly dominated by few large

sized firm such as Tesco, Sainsbury and ASDA. The concentration has been accelerated

largely until 2012. Thereafter, two low cost retailers Aldi and Lidle have successfully

expanded their business. this has reduced the four firm concentration ratio from 75% in 2011

to 72.3% in 2016 (ibisworld.co.uk, 2018).

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Answer to question 1

Small and Medium sized enterprises provide a great support to UK economy. The

expansion strategies of SMEs open up new market and create new job opportunities. In order

to grow bigger these companies invest in innovation leading to intense competition in the

marketplace. As per 2014 statistics, UK has nearly 5.2 million SMEs. In UK, a wide majority

of business is currently employing less than 10 people, accounted for 33 percent employment

and enjoys a turnover of 19 percent (uk.wsj.com 2018). However, the small and medium

enterprises has accounted a disproportionate growth rate. It is found that 6% of total SMEs in

UK experience higher growth rate and responsible for generating fifty percent of new jobs

between 2002 and 2008 (fsb.org.uk, 2018). The grocery supermarket chain in UK is one of

the interesting aspect to be discussed. The supermarket chains some large and small retailers.

Waitrose

Waitrose belongs to the chain of British supermarket structure, forming the division

of food retailers in Britain. It has nearly 352 branches in United Kingdom. Among these

branches 30 are convenience shops. Currently Waitrose occupies a market share of 5.1

percent in grocery supermarket chain.

Market structure of supermarket chain in UK

The supermarket structure in UK resembles the feature of an oligopoly market. An

oligopoly market is characterized by the dominance of few large firms in the market (Sloman

and Jones 2017). The grocery supermarket in UK is now increasingly dominated by few large

sized firm such as Tesco, Sainsbury and ASDA. The concentration has been accelerated

largely until 2012. Thereafter, two low cost retailers Aldi and Lidle have successfully

expanded their business. this has reduced the four firm concentration ratio from 75% in 2011

to 72.3% in 2016 (ibisworld.co.uk, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

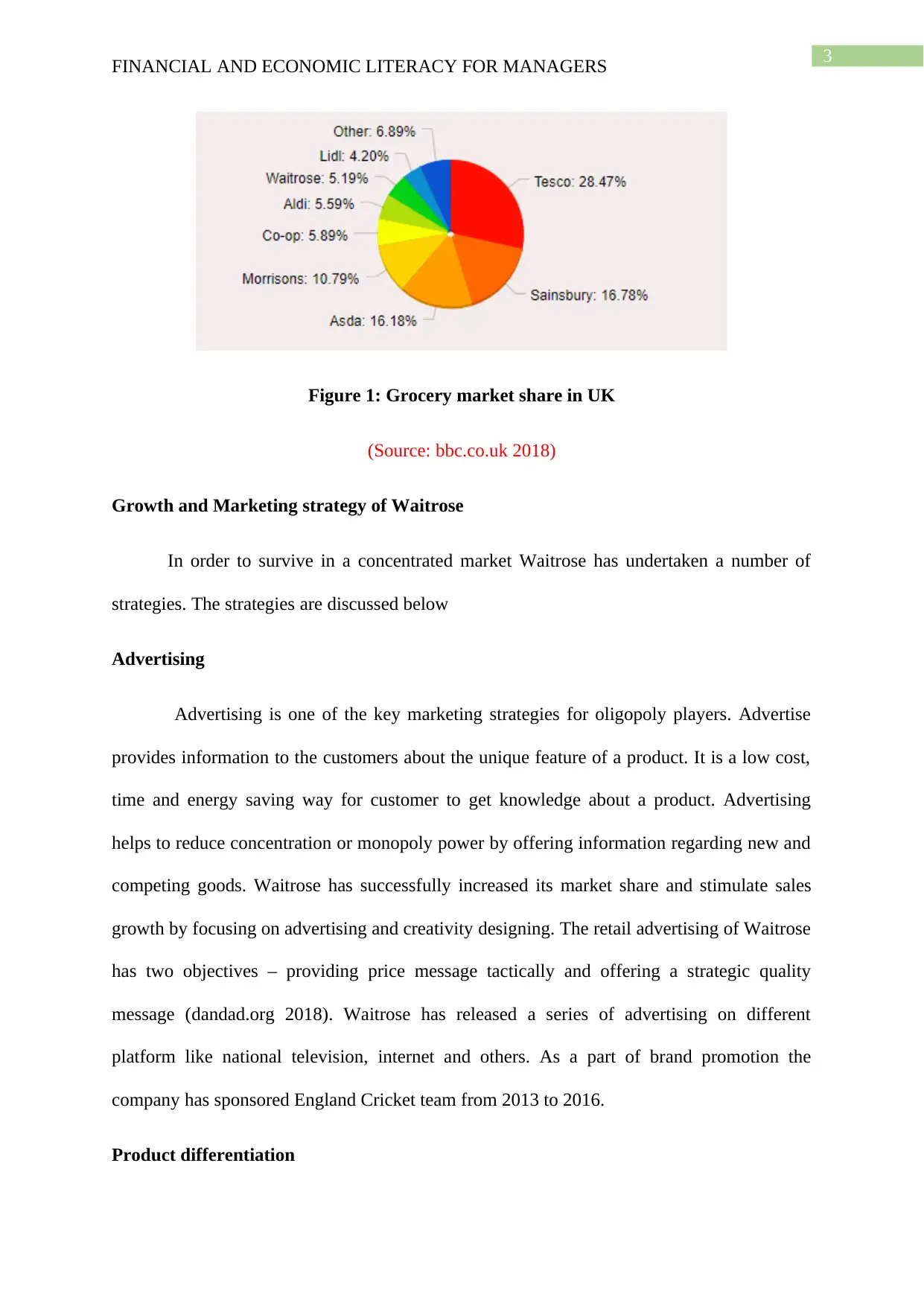

Figure 1: Grocery market share in UK

(Source: bbc.co.uk 2018)

Growth and Marketing strategy of Waitrose

In order to survive in a concentrated market Waitrose has undertaken a number of

strategies. The strategies are discussed below

Advertising

Advertising is one of the key marketing strategies for oligopoly players. Advertise

provides information to the customers about the unique feature of a product. It is a low cost,

time and energy saving way for customer to get knowledge about a product. Advertising

helps to reduce concentration or monopoly power by offering information regarding new and

competing goods. Waitrose has successfully increased its market share and stimulate sales

growth by focusing on advertising and creativity designing. The retail advertising of Waitrose

has two objectives – providing price message tactically and offering a strategic quality

message (dandad.org 2018). Waitrose has released a series of advertising on different

platform like national television, internet and others. As a part of brand promotion the

company has sponsored England Cricket team from 2013 to 2016.

Product differentiation

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Figure 1: Grocery market share in UK

(Source: bbc.co.uk 2018)

Growth and Marketing strategy of Waitrose

In order to survive in a concentrated market Waitrose has undertaken a number of

strategies. The strategies are discussed below

Advertising

Advertising is one of the key marketing strategies for oligopoly players. Advertise

provides information to the customers about the unique feature of a product. It is a low cost,

time and energy saving way for customer to get knowledge about a product. Advertising

helps to reduce concentration or monopoly power by offering information regarding new and

competing goods. Waitrose has successfully increased its market share and stimulate sales

growth by focusing on advertising and creativity designing. The retail advertising of Waitrose

has two objectives – providing price message tactically and offering a strategic quality

message (dandad.org 2018). Waitrose has released a series of advertising on different

platform like national television, internet and others. As a part of brand promotion the

company has sponsored England Cricket team from 2013 to 2016.

Product differentiation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Product differentiation is another important strategy devised by business to increase

its market share. The objective of product differentiation is to make own product different

from its rival as much as possible. A differentiated product attracts more attention of the

customers and thus helps to achieve sales growth. Waitrose has a differentiation strategy

covering both the price and quality aspects. Waitrose differentiation strategy focuses on

upper market segments and offers a wide range of fresh products with good quality services

(accaglobal.com, 2018). Unlike taking a diversification strategy of four big retailers,

operation of the company is mainly concentrated on the market of food and drinks. Waitrose

make its stores the most convenient place for customer to have desired product at the

cheapest price. The Waitrose customers have low stress regarding quality of product and

often willing to pay premium price.

Marketing Mix of Waitrose

The term marketing mix refers to the business strategy where business uses a

combination of different tactics to achieve the marketing objective for different targeted

customer group (businessinsider.com 2018). Different factors encourage the company to vary

product mix. Waitrose use promotional offer pricing varied from stores to store.

The different marketing strategy of Waitrose provide the company an important

position in the grocery supermarket chain and opens up future scope for business expansion.

Answer to question 2

By definition, housing market indicates a market that deals with demand and supply

of housing in a specific nation or region. The housing market of UK has experienced some

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Product differentiation is another important strategy devised by business to increase

its market share. The objective of product differentiation is to make own product different

from its rival as much as possible. A differentiated product attracts more attention of the

customers and thus helps to achieve sales growth. Waitrose has a differentiation strategy

covering both the price and quality aspects. Waitrose differentiation strategy focuses on

upper market segments and offers a wide range of fresh products with good quality services

(accaglobal.com, 2018). Unlike taking a diversification strategy of four big retailers,

operation of the company is mainly concentrated on the market of food and drinks. Waitrose

make its stores the most convenient place for customer to have desired product at the

cheapest price. The Waitrose customers have low stress regarding quality of product and

often willing to pay premium price.

Marketing Mix of Waitrose

The term marketing mix refers to the business strategy where business uses a

combination of different tactics to achieve the marketing objective for different targeted

customer group (businessinsider.com 2018). Different factors encourage the company to vary

product mix. Waitrose use promotional offer pricing varied from stores to store.

The different marketing strategy of Waitrose provide the company an important

position in the grocery supermarket chain and opens up future scope for business expansion.

Answer to question 2

By definition, housing market indicates a market that deals with demand and supply

of housing in a specific nation or region. The housing market of UK has experienced some

5

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

dramatic changes since 1990s. The ownership trend in the housing market of UK gradually

shifted from private ownership to a continuous rise of public housing offered by local

authorities. There are different factor affecting demand and supply of housing and hence,

play an important role in determining housing price.

Factor affecting demand of housing

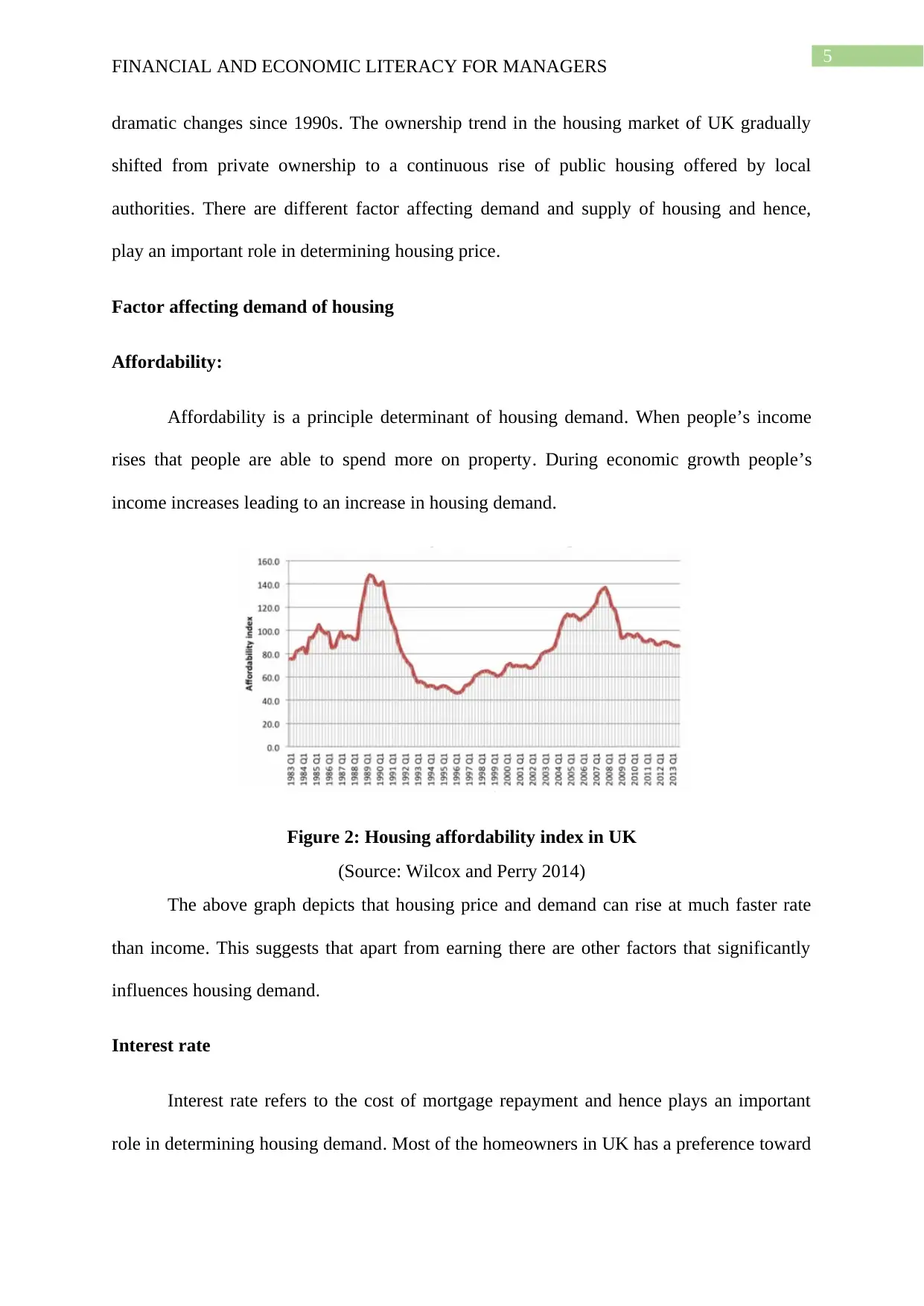

Affordability:

Affordability is a principle determinant of housing demand. When people’s income

rises that people are able to spend more on property. During economic growth people’s

income increases leading to an increase in housing demand.

Figure 2: Housing affordability index in UK

(Source: Wilcox and Perry 2014)

The above graph depicts that housing price and demand can rise at much faster rate

than income. This suggests that apart from earning there are other factors that significantly

influences housing demand.

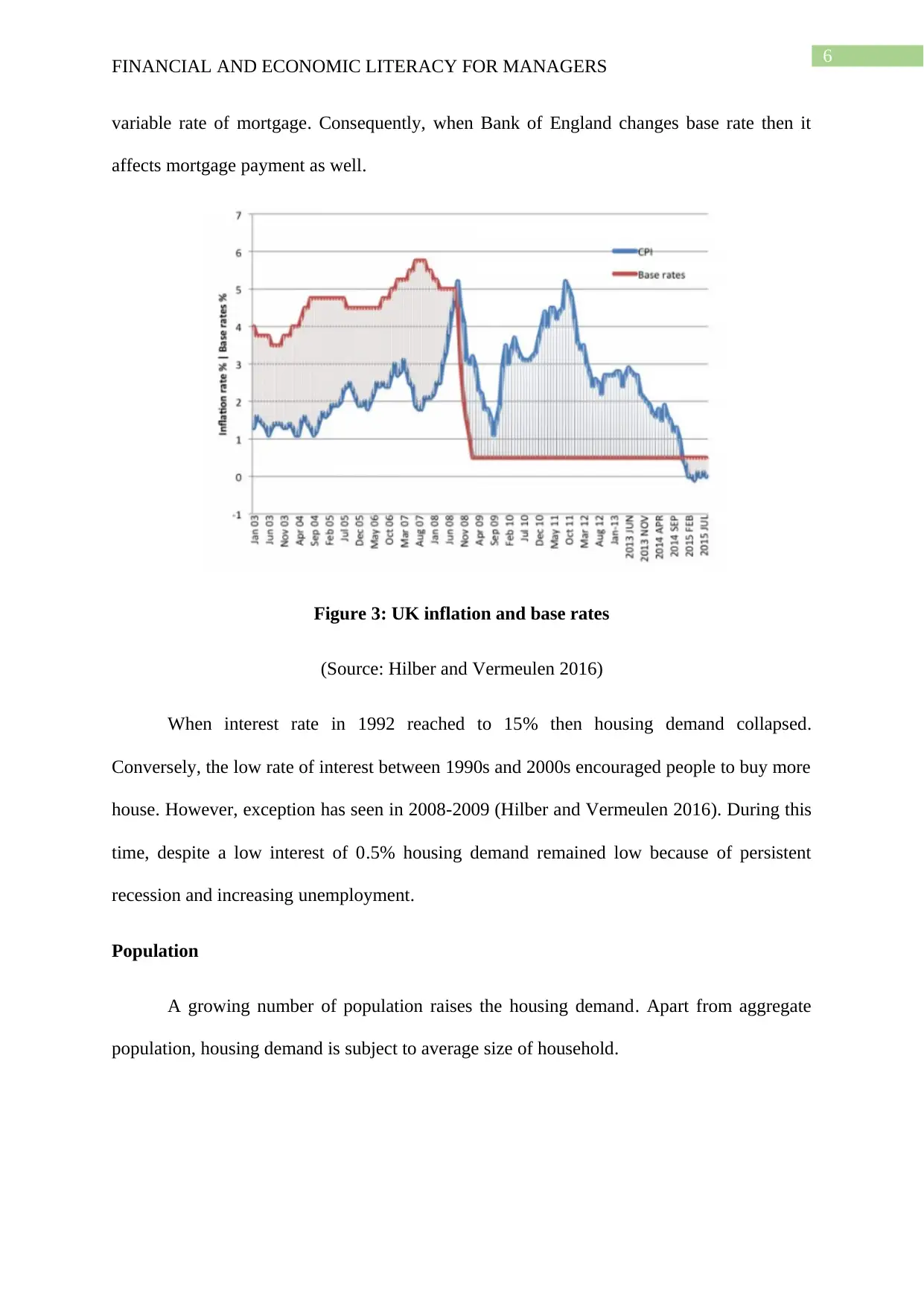

Interest rate

Interest rate refers to the cost of mortgage repayment and hence plays an important

role in determining housing demand. Most of the homeowners in UK has a preference toward

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

dramatic changes since 1990s. The ownership trend in the housing market of UK gradually

shifted from private ownership to a continuous rise of public housing offered by local

authorities. There are different factor affecting demand and supply of housing and hence,

play an important role in determining housing price.

Factor affecting demand of housing

Affordability:

Affordability is a principle determinant of housing demand. When people’s income

rises that people are able to spend more on property. During economic growth people’s

income increases leading to an increase in housing demand.

Figure 2: Housing affordability index in UK

(Source: Wilcox and Perry 2014)

The above graph depicts that housing price and demand can rise at much faster rate

than income. This suggests that apart from earning there are other factors that significantly

influences housing demand.

Interest rate

Interest rate refers to the cost of mortgage repayment and hence plays an important

role in determining housing demand. Most of the homeowners in UK has a preference toward

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

variable rate of mortgage. Consequently, when Bank of England changes base rate then it

affects mortgage payment as well.

Figure 3: UK inflation and base rates

(Source: Hilber and Vermeulen 2016)

When interest rate in 1992 reached to 15% then housing demand collapsed.

Conversely, the low rate of interest between 1990s and 2000s encouraged people to buy more

house. However, exception has seen in 2008-2009 (Hilber and Vermeulen 2016). During this

time, despite a low interest of 0.5% housing demand remained low because of persistent

recession and increasing unemployment.

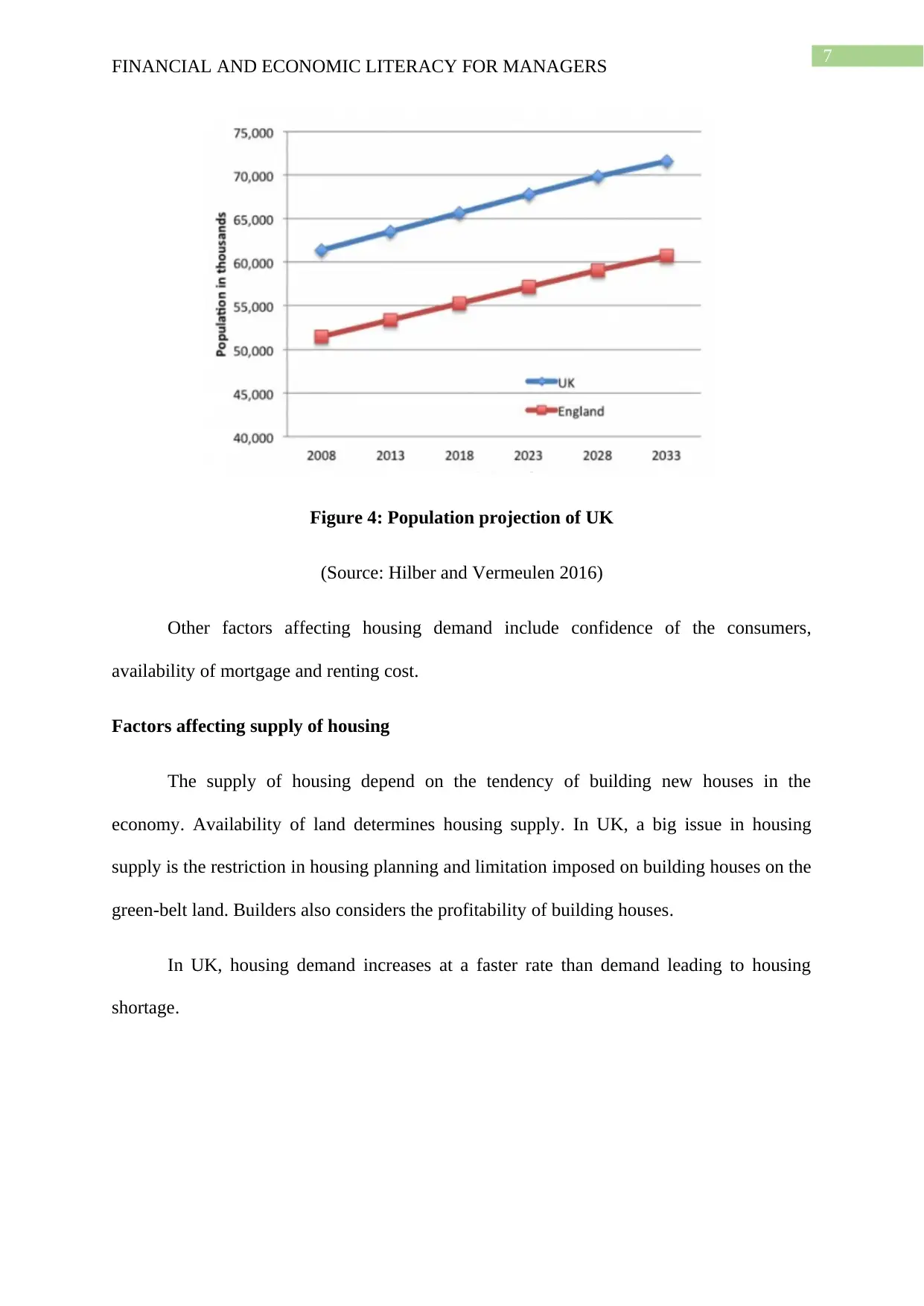

Population

A growing number of population raises the housing demand. Apart from aggregate

population, housing demand is subject to average size of household.

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

variable rate of mortgage. Consequently, when Bank of England changes base rate then it

affects mortgage payment as well.

Figure 3: UK inflation and base rates

(Source: Hilber and Vermeulen 2016)

When interest rate in 1992 reached to 15% then housing demand collapsed.

Conversely, the low rate of interest between 1990s and 2000s encouraged people to buy more

house. However, exception has seen in 2008-2009 (Hilber and Vermeulen 2016). During this

time, despite a low interest of 0.5% housing demand remained low because of persistent

recession and increasing unemployment.

Population

A growing number of population raises the housing demand. Apart from aggregate

population, housing demand is subject to average size of household.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Figure 4: Population projection of UK

(Source: Hilber and Vermeulen 2016)

Other factors affecting housing demand include confidence of the consumers,

availability of mortgage and renting cost.

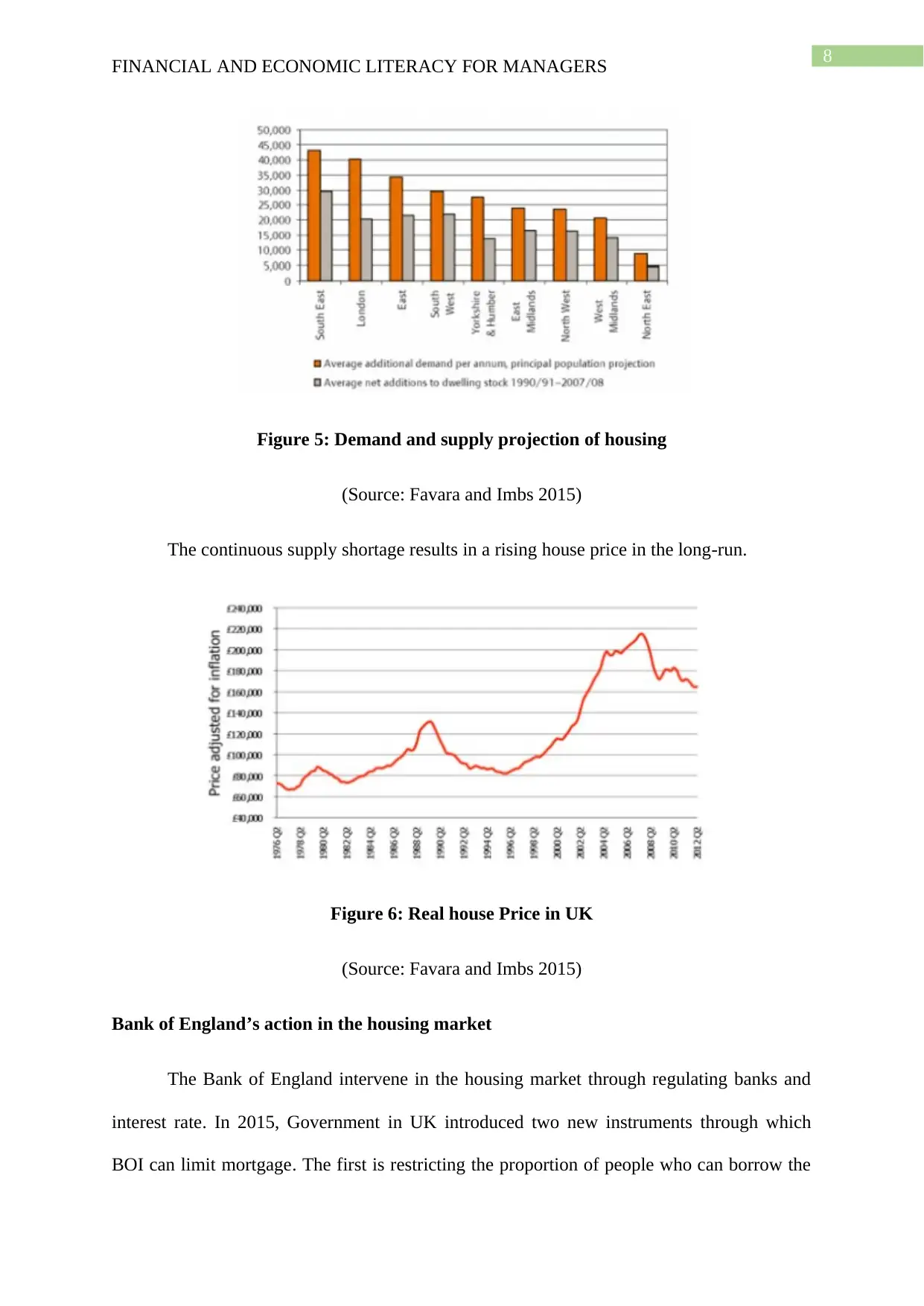

Factors affecting supply of housing

The supply of housing depend on the tendency of building new houses in the

economy. Availability of land determines housing supply. In UK, a big issue in housing

supply is the restriction in housing planning and limitation imposed on building houses on the

green-belt land. Builders also considers the profitability of building houses.

In UK, housing demand increases at a faster rate than demand leading to housing

shortage.

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Figure 4: Population projection of UK

(Source: Hilber and Vermeulen 2016)

Other factors affecting housing demand include confidence of the consumers,

availability of mortgage and renting cost.

Factors affecting supply of housing

The supply of housing depend on the tendency of building new houses in the

economy. Availability of land determines housing supply. In UK, a big issue in housing

supply is the restriction in housing planning and limitation imposed on building houses on the

green-belt land. Builders also considers the profitability of building houses.

In UK, housing demand increases at a faster rate than demand leading to housing

shortage.

8

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Figure 5: Demand and supply projection of housing

(Source: Favara and Imbs 2015)

The continuous supply shortage results in a rising house price in the long-run.

Figure 6: Real house Price in UK

(Source: Favara and Imbs 2015)

Bank of England’s action in the housing market

The Bank of England intervene in the housing market through regulating banks and

interest rate. In 2015, Government in UK introduced two new instruments through which

BOI can limit mortgage. The first is restricting the proportion of people who can borrow the

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Figure 5: Demand and supply projection of housing

(Source: Favara and Imbs 2015)

The continuous supply shortage results in a rising house price in the long-run.

Figure 6: Real house Price in UK

(Source: Favara and Imbs 2015)

Bank of England’s action in the housing market

The Bank of England intervene in the housing market through regulating banks and

interest rate. In 2015, Government in UK introduced two new instruments through which

BOI can limit mortgage. The first is restricting the proportion of people who can borrow the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

money relative to their housing valuation. This is done to reduce loss of the banks. When

house price declines and borrowers fail to repay loans then bank loss money in situation

where housing valued less than loan (McCrone and Stephens 2017). The second restriction is

placed in form of limiting borrowing in relation to income. People taking large amount of

loans tend to cut their spending in times of rising interest rate.

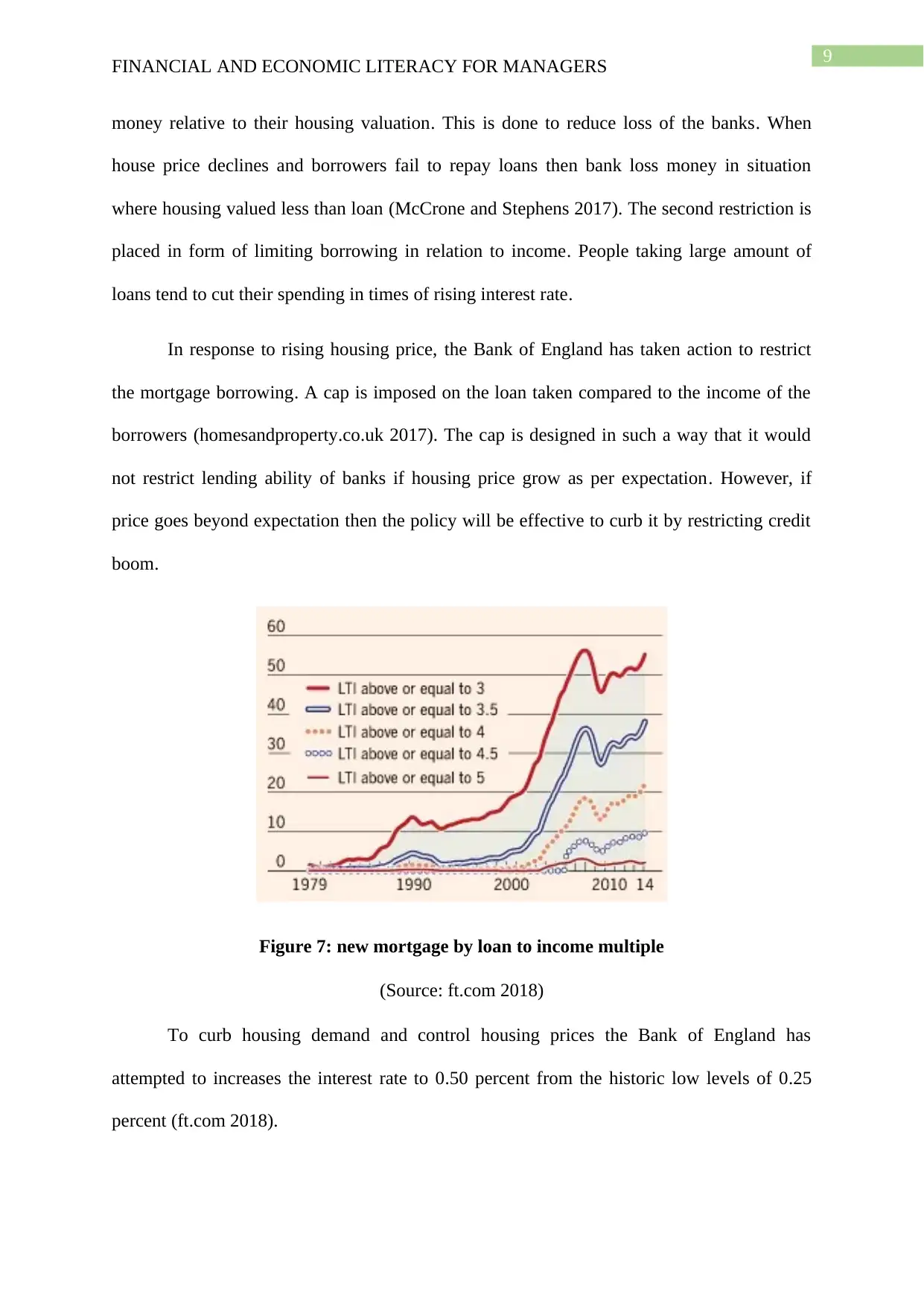

In response to rising housing price, the Bank of England has taken action to restrict

the mortgage borrowing. A cap is imposed on the loan taken compared to the income of the

borrowers (homesandproperty.co.uk 2017). The cap is designed in such a way that it would

not restrict lending ability of banks if housing price grow as per expectation. However, if

price goes beyond expectation then the policy will be effective to curb it by restricting credit

boom.

Figure 7: new mortgage by loan to income multiple

(Source: ft.com 2018)

To curb housing demand and control housing prices the Bank of England has

attempted to increases the interest rate to 0.50 percent from the historic low levels of 0.25

percent (ft.com 2018).

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

money relative to their housing valuation. This is done to reduce loss of the banks. When

house price declines and borrowers fail to repay loans then bank loss money in situation

where housing valued less than loan (McCrone and Stephens 2017). The second restriction is

placed in form of limiting borrowing in relation to income. People taking large amount of

loans tend to cut their spending in times of rising interest rate.

In response to rising housing price, the Bank of England has taken action to restrict

the mortgage borrowing. A cap is imposed on the loan taken compared to the income of the

borrowers (homesandproperty.co.uk 2017). The cap is designed in such a way that it would

not restrict lending ability of banks if housing price grow as per expectation. However, if

price goes beyond expectation then the policy will be effective to curb it by restricting credit

boom.

Figure 7: new mortgage by loan to income multiple

(Source: ft.com 2018)

To curb housing demand and control housing prices the Bank of England has

attempted to increases the interest rate to 0.50 percent from the historic low levels of 0.25

percent (ft.com 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Answer to question 3

The macroeconomics performance of a nation depends on a number of indicators.

These indicators are related to output market, labor market, price level and other related

measures.

Output Performance

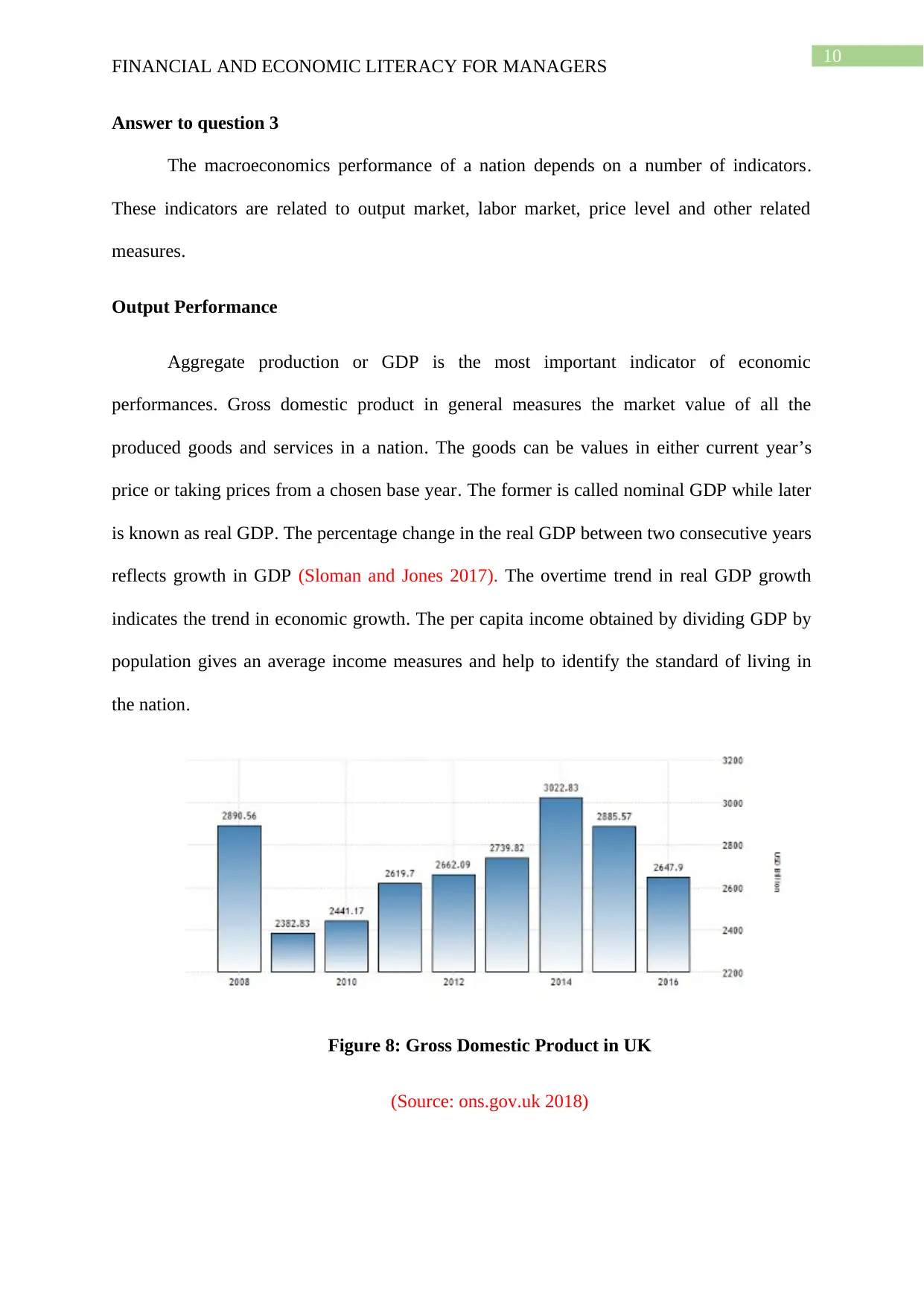

Aggregate production or GDP is the most important indicator of economic

performances. Gross domestic product in general measures the market value of all the

produced goods and services in a nation. The goods can be values in either current year’s

price or taking prices from a chosen base year. The former is called nominal GDP while later

is known as real GDP. The percentage change in the real GDP between two consecutive years

reflects growth in GDP (Sloman and Jones 2017). The overtime trend in real GDP growth

indicates the trend in economic growth. The per capita income obtained by dividing GDP by

population gives an average income measures and help to identify the standard of living in

the nation.

Figure 8: Gross Domestic Product in UK

(Source: ons.gov.uk 2018)

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

Answer to question 3

The macroeconomics performance of a nation depends on a number of indicators.

These indicators are related to output market, labor market, price level and other related

measures.

Output Performance

Aggregate production or GDP is the most important indicator of economic

performances. Gross domestic product in general measures the market value of all the

produced goods and services in a nation. The goods can be values in either current year’s

price or taking prices from a chosen base year. The former is called nominal GDP while later

is known as real GDP. The percentage change in the real GDP between two consecutive years

reflects growth in GDP (Sloman and Jones 2017). The overtime trend in real GDP growth

indicates the trend in economic growth. The per capita income obtained by dividing GDP by

population gives an average income measures and help to identify the standard of living in

the nation.

Figure 8: Gross Domestic Product in UK

(Source: ons.gov.uk 2018)

11

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

In 2016, the Gross Domestic Product of UK was valued 2647.90 billion US dollar.

The GDP in UK represents 4.27% of average world’s average income. The average GDP

between 1960 and 2016 is stood at 1137.23 billion. In the last ten years, the highest GDP was

recorded in 2014 with GDP valued at 3022.83 billion USD. After than growth slows down.

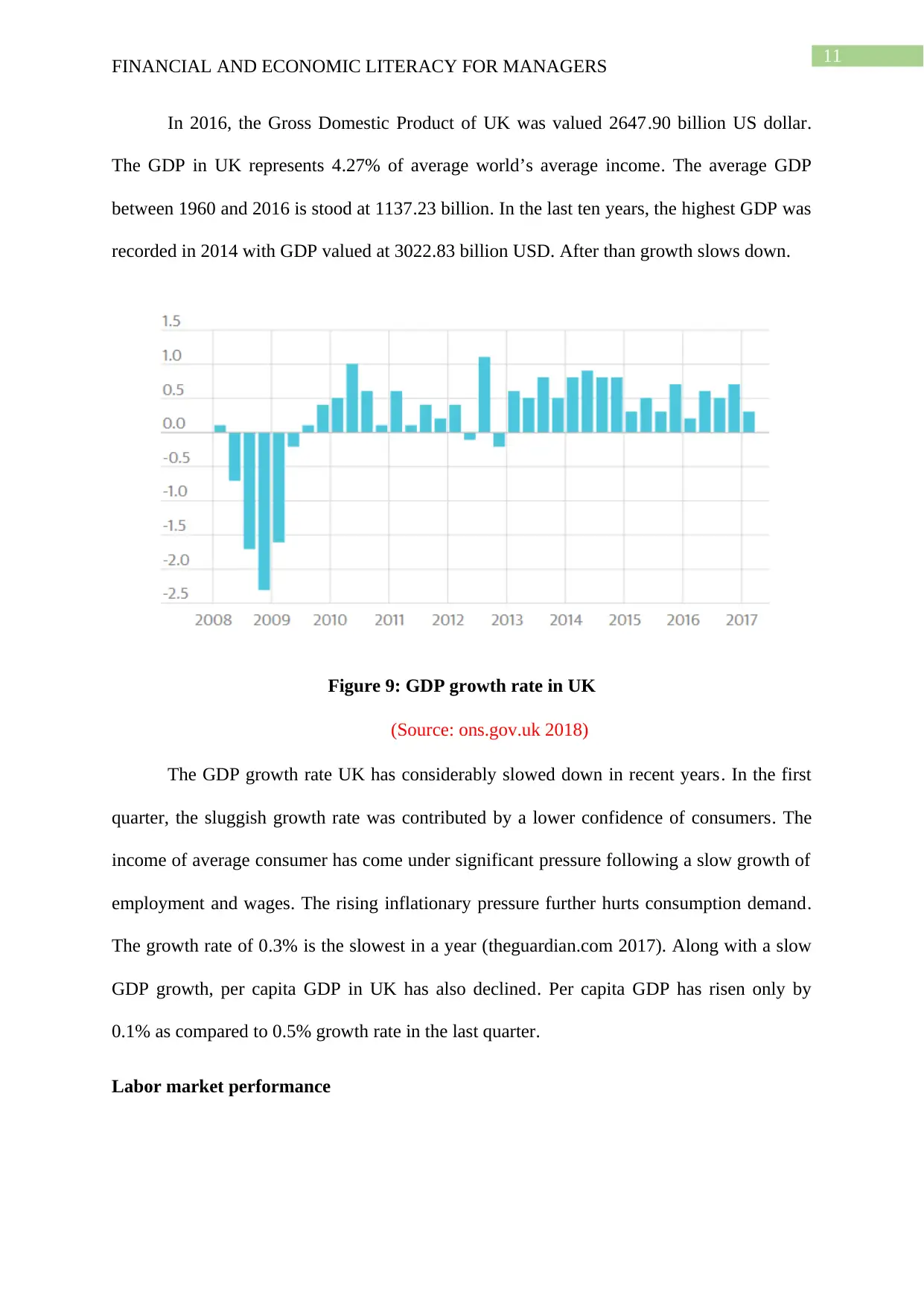

Figure 9: GDP growth rate in UK

(Source: ons.gov.uk 2018)

The GDP growth rate UK has considerably slowed down in recent years. In the first

quarter, the sluggish growth rate was contributed by a lower confidence of consumers. The

income of average consumer has come under significant pressure following a slow growth of

employment and wages. The rising inflationary pressure further hurts consumption demand.

The growth rate of 0.3% is the slowest in a year (theguardian.com 2017). Along with a slow

GDP growth, per capita GDP in UK has also declined. Per capita GDP has risen only by

0.1% as compared to 0.5% growth rate in the last quarter.

Labor market performance

FINANCIAL AND ECONOMIC LITERACY FOR MANAGERS

In 2016, the Gross Domestic Product of UK was valued 2647.90 billion US dollar.

The GDP in UK represents 4.27% of average world’s average income. The average GDP

between 1960 and 2016 is stood at 1137.23 billion. In the last ten years, the highest GDP was

recorded in 2014 with GDP valued at 3022.83 billion USD. After than growth slows down.

Figure 9: GDP growth rate in UK

(Source: ons.gov.uk 2018)

The GDP growth rate UK has considerably slowed down in recent years. In the first

quarter, the sluggish growth rate was contributed by a lower confidence of consumers. The

income of average consumer has come under significant pressure following a slow growth of

employment and wages. The rising inflationary pressure further hurts consumption demand.

The growth rate of 0.3% is the slowest in a year (theguardian.com 2017). Along with a slow

GDP growth, per capita GDP in UK has also declined. Per capita GDP has risen only by

0.1% as compared to 0.5% growth rate in the last quarter.

Labor market performance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21