Exploring Appropriate Sources of Finance for Startup Businesses: A Focus on Manufacturing Sector

VerifiedAdded on 2023/04/25

|27

|5564

|267

AI Summary

In this document we will discuss about Exploring Appropriate Sources of Finance for Startup Businesses and below are the summary points of this document:-

The text discusses appropriate sources of finance for a startup business in the manufacturing sector, including bank loans, venture capital, personal investment, angel investors, and incubators.

It mentions that bank loans are secured, have adjustable repayment schedules, and lower interest rates. Venture capital involves long-term investment in exchange for ownership stake.

Personal investment and angel investors provide funding and expertise, while incubators offer resources in return for equity.

Bank overdrafts and bank bills are also mentioned as potential sources of finance, but with different structures and higher interest rates.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: INTRODUCTION TO ACCOUNTING AND FINANCE

Introduction to Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Introduction to Accounting and Finance

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1BUSINESS MANAGEMENT TECHNIQUES

Table of Contents

Part 1A:............................................................................................................................................2

Part 1B:............................................................................................................................................3

Part 2:...............................................................................................................................................5

Part 3:.............................................................................................................................................12

Part 4:.............................................................................................................................................15

Part 5:.............................................................................................................................................18

Part 6A:..........................................................................................................................................20

Part 6B:..........................................................................................................................................23

References and Bibliography:........................................................................................................25

Table of Contents

Part 1A:............................................................................................................................................2

Part 1B:............................................................................................................................................3

Part 2:...............................................................................................................................................5

Part 3:.............................................................................................................................................12

Part 4:.............................................................................................................................................15

Part 5:.............................................................................................................................................18

Part 6A:..........................................................................................................................................20

Part 6B:..........................................................................................................................................23

References and Bibliography:........................................................................................................25

2BUSINESS MANAGEMENT TECHNIQUES

Part 1A:

List the most appropriate sources of finance for THIS business in the start-up phase. Briefly

explain why these are the most appropriate, and also discuss the reasons why other sources of

finance would not be appropriate for this company.

Sources of finance for the manufacturing of miscellaneous items:

1.Bank loans: It is completely external and long term finance also secured. It will be approved

against collateral. Repayment method/schedule can also be adjusted. The interest rates can be

less compared to other sources. Also, it guarantees money for longer period and they charge only

interest for the loan amount.

2.Venture Capital: It is a private equity given by firms to startups which have higher growth

potential in exchange for ownership stake or equity. It is a long term investment by the firm.

Investors play a major role in management decision.

3.Personal Investment or Friends & Family: It could be our savings or assets an individual

possess. Also, we can ask our friends or family members to invest or lend the money it is usually

referred as patient capital and it is repaid when startup is profitable.

4.Angel Investors: They are wealthy individuals who can also be retired executives. They also

help by providing their experience in technical and management knowledge. They also can check

your startup management and would look to take part in decisions.

5.Incubators:It is a type of organization which provides you the resources for startup it includes

marketing, cash and consulting. In return they would ask for equity so they can get benefitted from

profits in the future.

6.Bank Overdrafts: It is similar to a bank loan but has completely different structure. Company

will have permission to withdraw more money beyond its balance in the account and they have

pay interest only for the outstanding amount and interest rates are high.

7.Bank Bills: Bank would be the guarantor for this type and risk will lie on bank not on the

borrower for the repayment .They would charge certain amount of fee for being the guarantor or

for taking the risk.

Banks would be the convenient and secured for the finance as we can deposit and withdraw and

interest is very low. Also, they do not interfere in the management. There can be tax benefits

small business owners would highly benefit from this. Loan approval is lengthy and time taking

process. They also disburse only 70-80% of sanctioned amount in parts. For manufacturing of

miscellaneous items main source of funds can be from bank as everything else is sorted out.

Other sources of funds can be risky because of the interest rates, investors will be involved in

decision making where not all will be benefitted by that as they become part owner would look for

returns rather benefit of other people.

Part 1A:

List the most appropriate sources of finance for THIS business in the start-up phase. Briefly

explain why these are the most appropriate, and also discuss the reasons why other sources of

finance would not be appropriate for this company.

Sources of finance for the manufacturing of miscellaneous items:

1.Bank loans: It is completely external and long term finance also secured. It will be approved

against collateral. Repayment method/schedule can also be adjusted. The interest rates can be

less compared to other sources. Also, it guarantees money for longer period and they charge only

interest for the loan amount.

2.Venture Capital: It is a private equity given by firms to startups which have higher growth

potential in exchange for ownership stake or equity. It is a long term investment by the firm.

Investors play a major role in management decision.

3.Personal Investment or Friends & Family: It could be our savings or assets an individual

possess. Also, we can ask our friends or family members to invest or lend the money it is usually

referred as patient capital and it is repaid when startup is profitable.

4.Angel Investors: They are wealthy individuals who can also be retired executives. They also

help by providing their experience in technical and management knowledge. They also can check

your startup management and would look to take part in decisions.

5.Incubators:It is a type of organization which provides you the resources for startup it includes

marketing, cash and consulting. In return they would ask for equity so they can get benefitted from

profits in the future.

6.Bank Overdrafts: It is similar to a bank loan but has completely different structure. Company

will have permission to withdraw more money beyond its balance in the account and they have

pay interest only for the outstanding amount and interest rates are high.

7.Bank Bills: Bank would be the guarantor for this type and risk will lie on bank not on the

borrower for the repayment .They would charge certain amount of fee for being the guarantor or

for taking the risk.

Banks would be the convenient and secured for the finance as we can deposit and withdraw and

interest is very low. Also, they do not interfere in the management. There can be tax benefits

small business owners would highly benefit from this. Loan approval is lengthy and time taking

process. They also disburse only 70-80% of sanctioned amount in parts. For manufacturing of

miscellaneous items main source of funds can be from bank as everything else is sorted out.

Other sources of funds can be risky because of the interest rates, investors will be involved in

decision making where not all will be benefitted by that as they become part owner would look for

returns rather benefit of other people.

3BUSINESS MANAGEMENT TECHNIQUES

Part 1B:

List the most appropriate sources of finance for THIS business for future expansion. Briefly

explain why these are the most appropriate, and also discuss the reasons why other sources of

finance would not be appropriate for this company.

1.Partnership: If there are more partners involved in the business then there will be plenty of

funds. Establishment of the business would be easy with less cost. Management decisions will be

internal, there will be no external involvement. Each person would be responsible for their debts

and shares. Any changes can be faster like increasing the production, wages and more like legal

structure. There might be a disagreement between the partners. Life of partnership depends on

the understanding between them.

2.Retained Earnings: It would be the best option for future expansion as it will not lead to any

change in the structure and everything will be same just a decision has to be made between the

partners or a resolution must be passed. It also increases the market value. It doesn’t add in a

liability. It doesn’t involve any outsiders so control on the firm will be same.

3.Franchising:It is one of the best options and most effective. Profits will be from the extra

sales. Owner gets an equity for using the firm name. It also increases the popularity among the

customers. It would concentrate more on purchases used for manufacturing. Training and

guidance should be given to new employees. Franchisee’s owner also gets a benefit for using the

name of established firm.

4.Venture capital: As the firms are interested to invest in startups they can also invest for

expansion of the business. If they see huge growth and profits or demand in the future of the

company. They would always work towards the betterment of the enterprises. Owner would not

be in the driver's seat anymore as they involve in management decision.

Part 1 mainly comprises of information that is used for the organization to detect the level

of different source of finance, which can help in supporting their operations. The most

appropriate source of finance has been listed in this part, which can be used by the organization

for improving their operations to support the cash requirements. From the overall evaluation, it is

detected that finance source from banks is much more convenient and secured for the

organization, as deposits and withdrawals can be conducted adequately with low interest rates. In

addition, the bank source of finance will not interfere with the management and allow full

control to the owners of the business. Furthermore, adequate benefits are mainly detected for

Part 1B:

List the most appropriate sources of finance for THIS business for future expansion. Briefly

explain why these are the most appropriate, and also discuss the reasons why other sources of

finance would not be appropriate for this company.

1.Partnership: If there are more partners involved in the business then there will be plenty of

funds. Establishment of the business would be easy with less cost. Management decisions will be

internal, there will be no external involvement. Each person would be responsible for their debts

and shares. Any changes can be faster like increasing the production, wages and more like legal

structure. There might be a disagreement between the partners. Life of partnership depends on

the understanding between them.

2.Retained Earnings: It would be the best option for future expansion as it will not lead to any

change in the structure and everything will be same just a decision has to be made between the

partners or a resolution must be passed. It also increases the market value. It doesn’t add in a

liability. It doesn’t involve any outsiders so control on the firm will be same.

3.Franchising:It is one of the best options and most effective. Profits will be from the extra

sales. Owner gets an equity for using the firm name. It also increases the popularity among the

customers. It would concentrate more on purchases used for manufacturing. Training and

guidance should be given to new employees. Franchisee’s owner also gets a benefit for using the

name of established firm.

4.Venture capital: As the firms are interested to invest in startups they can also invest for

expansion of the business. If they see huge growth and profits or demand in the future of the

company. They would always work towards the betterment of the enterprises. Owner would not

be in the driver's seat anymore as they involve in management decision.

Part 1 mainly comprises of information that is used for the organization to detect the level

of different source of finance, which can help in supporting their operations. The most

appropriate source of finance has been listed in this part, which can be used by the organization

for improving their operations to support the cash requirements. From the overall evaluation, it is

detected that finance source from banks is much more convenient and secured for the

organization, as deposits and withdrawals can be conducted adequately with low interest rates. In

addition, the bank source of finance will not interfere with the management and allow full

control to the owners of the business. Furthermore, adequate benefits are mainly detected for

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4BUSINESS MANAGEMENT TECHNIQUES

small business owners, as they can get tax benefits after the loans taken from banks. Hence, the

finance source of banks can eventually allow the business to conduct their operations smoothly

with low interest rates, which are mainly imposed by other sources of finance. Lastly, other

forms of business can be risky for the organization, as investors will increase their exposure in

the organization, which will negatively affect its operations (Maskell, Baggaley and Grasso

2016).

The second part mainly provides information regarding the appropriate source of finance

of different business, which can support them during the expansion process. The partnership

firms mainly gather the required funds from partner, where any debt incurred by the organization

will be distributed within the partners. Furthermore, the retained earnings are the best possible

option, which can eventually help the organization to increase their operations. Moreover,

franchising is the best possible option and effective measure, which can improve the operations

of the organization by increasing their operational capability. Lastly, venture capital is mainly

conducted used by start-ups for increasing the expansion condition of the new business, which

can surge operations of the organization. Therefore, specific sources of finance can be used for

improving the level of operations of the organization, which can raise their income in the long

run (Crawford and Wang 2014).

small business owners, as they can get tax benefits after the loans taken from banks. Hence, the

finance source of banks can eventually allow the business to conduct their operations smoothly

with low interest rates, which are mainly imposed by other sources of finance. Lastly, other

forms of business can be risky for the organization, as investors will increase their exposure in

the organization, which will negatively affect its operations (Maskell, Baggaley and Grasso

2016).

The second part mainly provides information regarding the appropriate source of finance

of different business, which can support them during the expansion process. The partnership

firms mainly gather the required funds from partner, where any debt incurred by the organization

will be distributed within the partners. Furthermore, the retained earnings are the best possible

option, which can eventually help the organization to increase their operations. Moreover,

franchising is the best possible option and effective measure, which can improve the operations

of the organization by increasing their operational capability. Lastly, venture capital is mainly

conducted used by start-ups for increasing the expansion condition of the new business, which

can surge operations of the organization. Therefore, specific sources of finance can be used for

improving the level of operations of the organization, which can raise their income in the long

run (Crawford and Wang 2014).

5BUSINESS MANAGEMENT TECHNIQUES

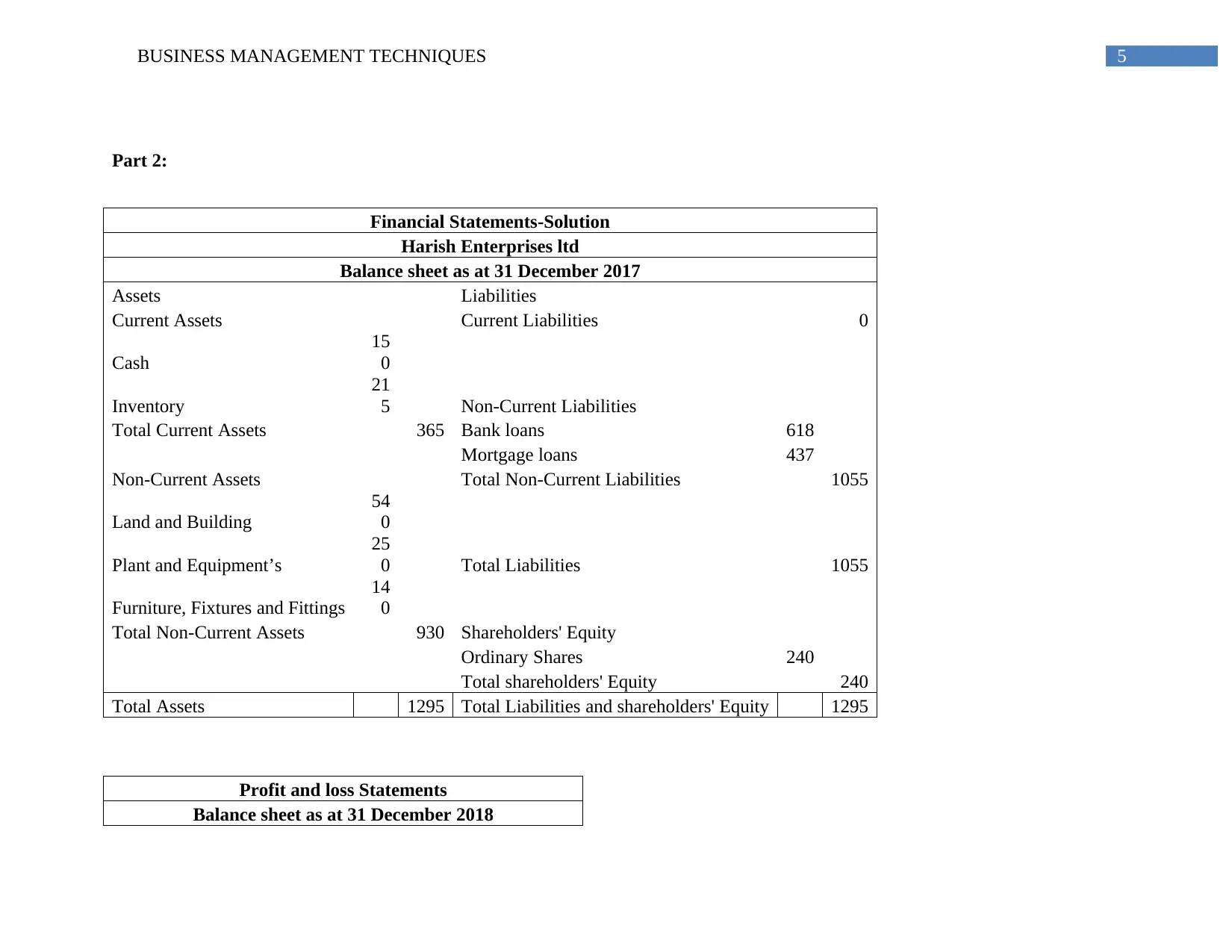

Part 2:

Financial Statements-Solution

Harish Enterprises ltd

Balance sheet as at 31 December 2017

Assets Liabilities

Current Assets Current Liabilities 0

Cash

15

0

Inventory

21

5 Non-Current Liabilities

Total Current Assets 365 Bank loans 618

Mortgage loans 437

Non-Current Assets Total Non-Current Liabilities 1055

Land and Building

54

0

Plant and Equipment’s

25

0 Total Liabilities 1055

Furniture, Fixtures and Fittings

14

0

Total Non-Current Assets 930 Shareholders' Equity

Ordinary Shares 240

Total shareholders' Equity 240

Total Assets 1295 Total Liabilities and shareholders' Equity 1295

Profit and loss Statements

Balance sheet as at 31 December 2018

Part 2:

Financial Statements-Solution

Harish Enterprises ltd

Balance sheet as at 31 December 2017

Assets Liabilities

Current Assets Current Liabilities 0

Cash

15

0

Inventory

21

5 Non-Current Liabilities

Total Current Assets 365 Bank loans 618

Mortgage loans 437

Non-Current Assets Total Non-Current Liabilities 1055

Land and Building

54

0

Plant and Equipment’s

25

0 Total Liabilities 1055

Furniture, Fixtures and Fittings

14

0

Total Non-Current Assets 930 Shareholders' Equity

Ordinary Shares 240

Total shareholders' Equity 240

Total Assets 1295 Total Liabilities and shareholders' Equity 1295

Profit and loss Statements

Balance sheet as at 31 December 2018

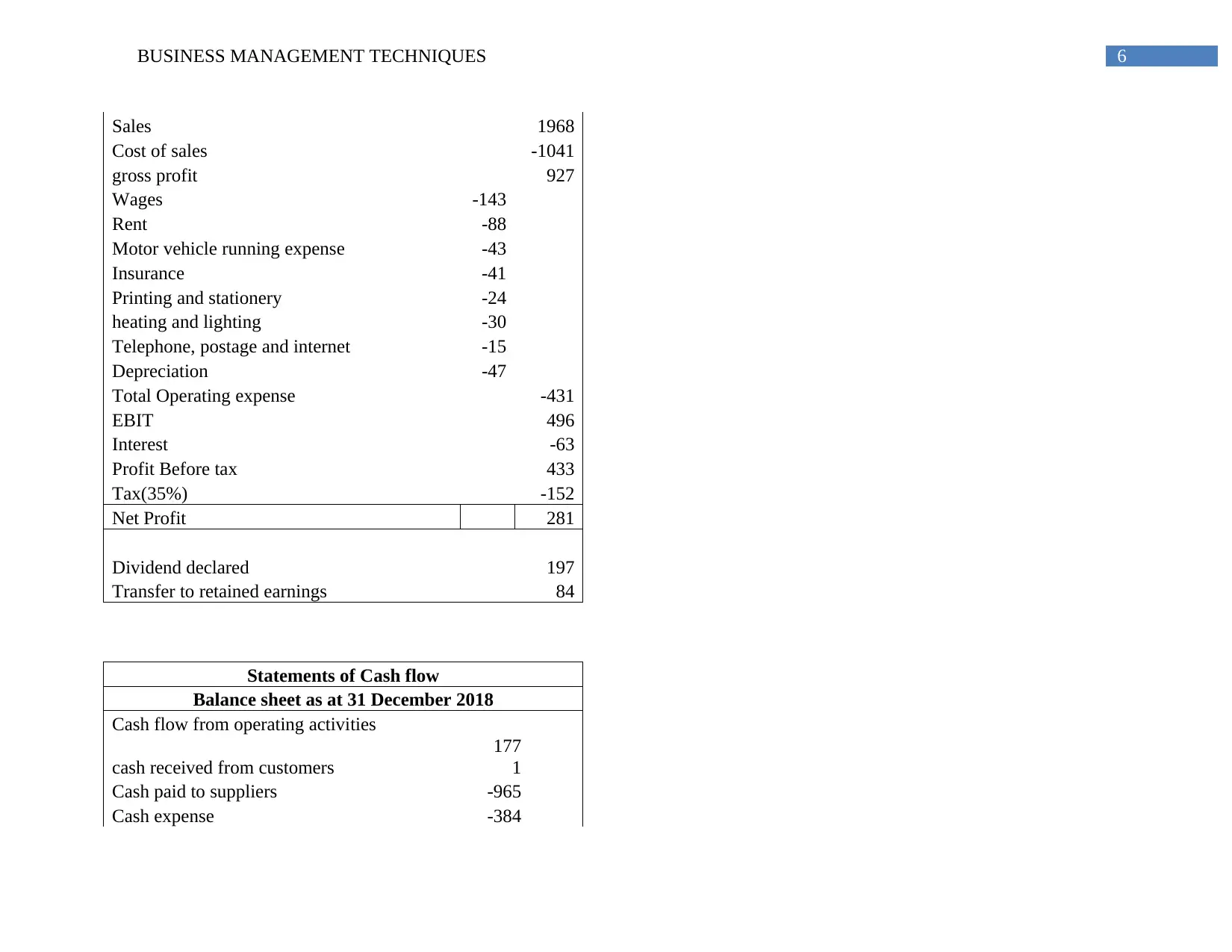

6BUSINESS MANAGEMENT TECHNIQUES

Sales 1968

Cost of sales -1041

gross profit 927

Wages -143

Rent -88

Motor vehicle running expense -43

Insurance -41

Printing and stationery -24

heating and lighting -30

Telephone, postage and internet -15

Depreciation -47

Total Operating expense -431

EBIT 496

Interest -63

Profit Before tax 433

Tax(35%) -152

Net Profit 281

Dividend declared 197

Transfer to retained earnings 84

Statements of Cash flow

Balance sheet as at 31 December 2018

Cash flow from operating activities

cash received from customers

177

1

Cash paid to suppliers -965

Cash expense -384

Sales 1968

Cost of sales -1041

gross profit 927

Wages -143

Rent -88

Motor vehicle running expense -43

Insurance -41

Printing and stationery -24

heating and lighting -30

Telephone, postage and internet -15

Depreciation -47

Total Operating expense -431

EBIT 496

Interest -63

Profit Before tax 433

Tax(35%) -152

Net Profit 281

Dividend declared 197

Transfer to retained earnings 84

Statements of Cash flow

Balance sheet as at 31 December 2018

Cash flow from operating activities

cash received from customers

177

1

Cash paid to suppliers -965

Cash expense -384

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

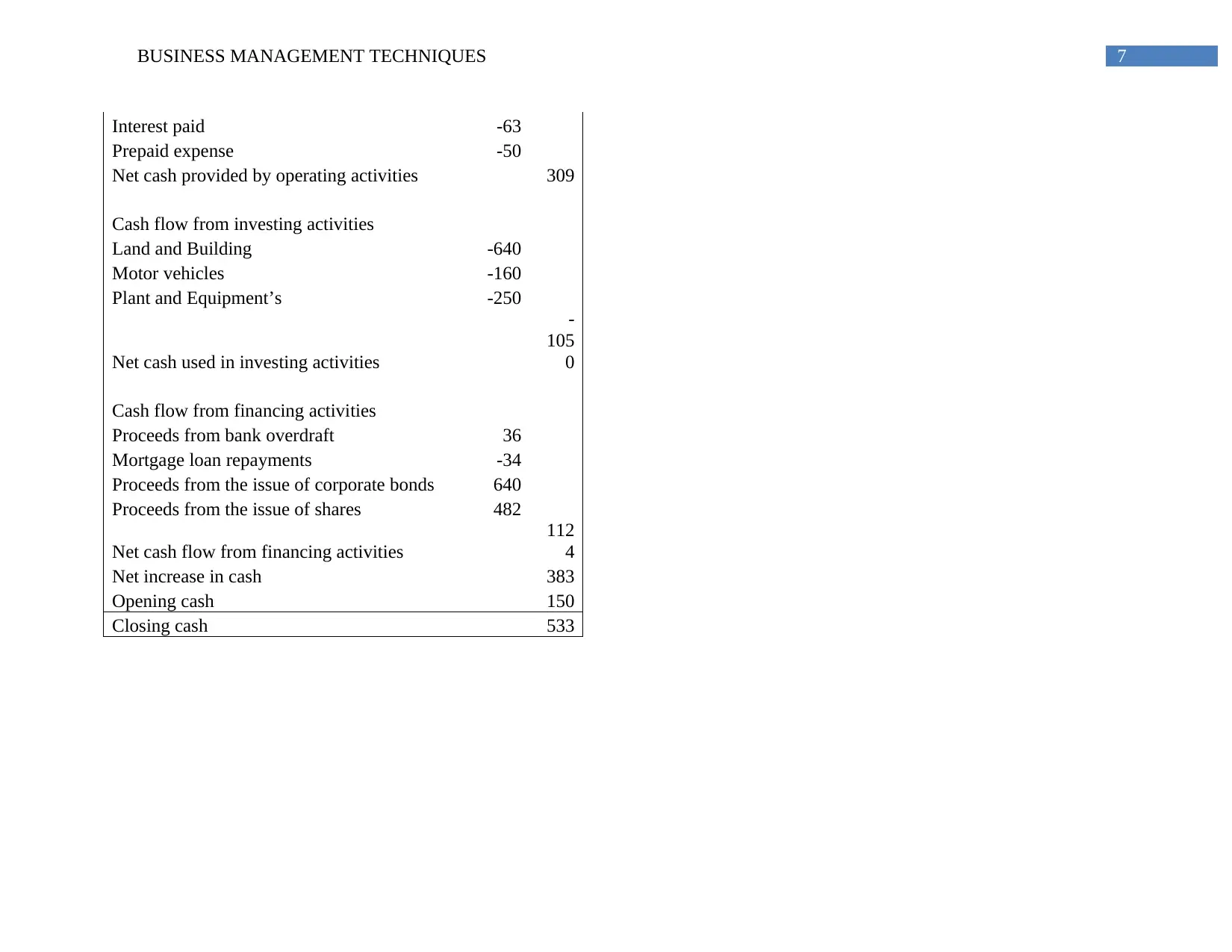

7BUSINESS MANAGEMENT TECHNIQUES

Interest paid -63

Prepaid expense -50

Net cash provided by operating activities 309

Cash flow from investing activities

Land and Building -640

Motor vehicles -160

Plant and Equipment’s -250

Net cash used in investing activities

-

105

0

Cash flow from financing activities

Proceeds from bank overdraft 36

Mortgage loan repayments -34

Proceeds from the issue of corporate bonds 640

Proceeds from the issue of shares 482

Net cash flow from financing activities

112

4

Net increase in cash 383

Opening cash 150

Closing cash 533

Interest paid -63

Prepaid expense -50

Net cash provided by operating activities 309

Cash flow from investing activities

Land and Building -640

Motor vehicles -160

Plant and Equipment’s -250

Net cash used in investing activities

-

105

0

Cash flow from financing activities

Proceeds from bank overdraft 36

Mortgage loan repayments -34

Proceeds from the issue of corporate bonds 640

Proceeds from the issue of shares 482

Net cash flow from financing activities

112

4

Net increase in cash 383

Opening cash 150

Closing cash 533

8BUSINESS MANAGEMENT TECHNIQUES

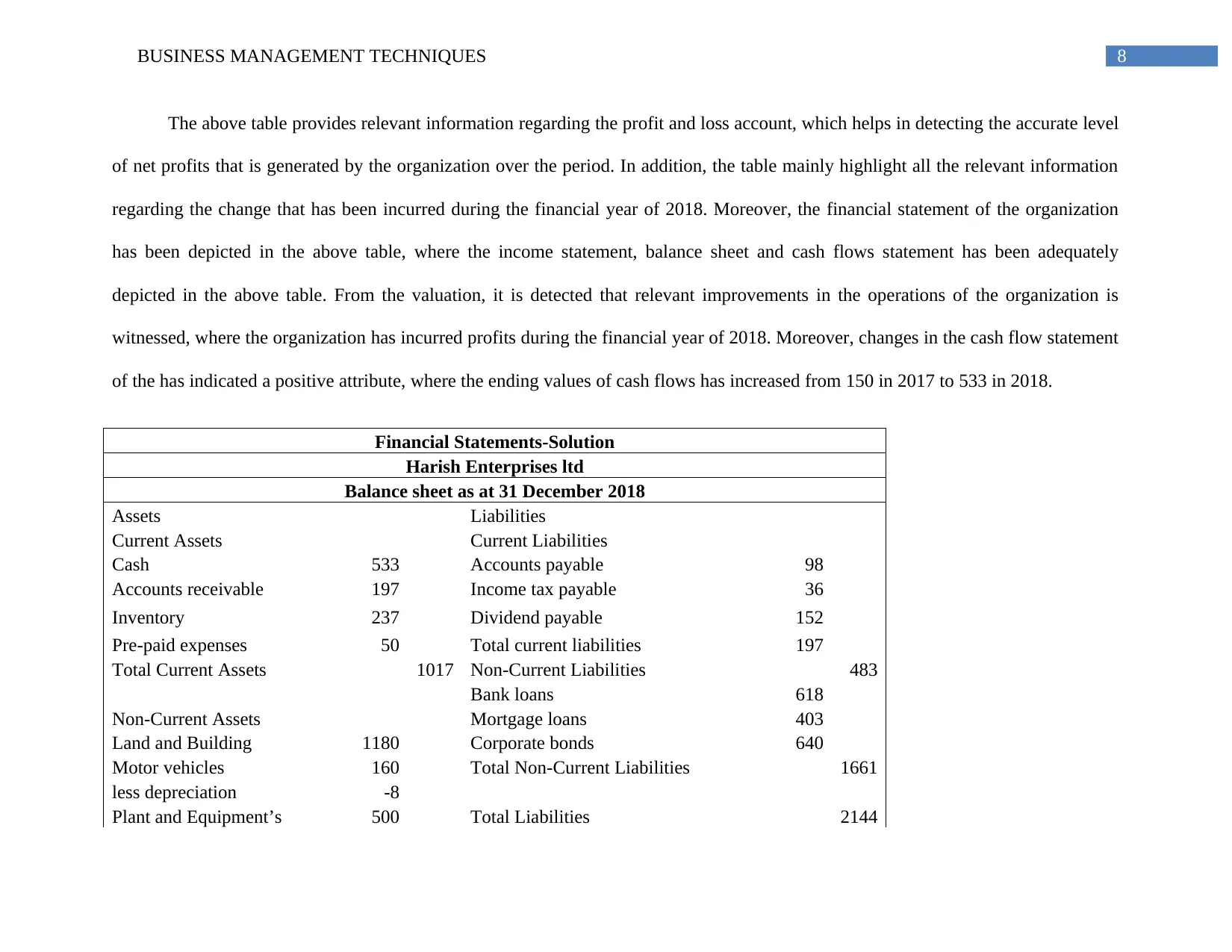

The above table provides relevant information regarding the profit and loss account, which helps in detecting the accurate level

of net profits that is generated by the organization over the period. In addition, the table mainly highlight all the relevant information

regarding the change that has been incurred during the financial year of 2018. Moreover, the financial statement of the organization

has been depicted in the above table, where the income statement, balance sheet and cash flows statement has been adequately

depicted in the above table. From the valuation, it is detected that relevant improvements in the operations of the organization is

witnessed, where the organization has incurred profits during the financial year of 2018. Moreover, changes in the cash flow statement

of the has indicated a positive attribute, where the ending values of cash flows has increased from 150 in 2017 to 533 in 2018.

Financial Statements-Solution

Harish Enterprises ltd

Balance sheet as at 31 December 2018

Assets Liabilities

Current Assets Current Liabilities

Cash 533 Accounts payable 98

Accounts receivable 197 Income tax payable 36

Inventory 237 Dividend payable 152

Pre-paid expenses 50 Total current liabilities 197

Total Current Assets 1017 Non-Current Liabilities 483

Bank loans 618

Non-Current Assets Mortgage loans 403

Land and Building 1180 Corporate bonds 640

Motor vehicles 160 Total Non-Current Liabilities 1661

less depreciation -8

Plant and Equipment’s 500 Total Liabilities 2144

The above table provides relevant information regarding the profit and loss account, which helps in detecting the accurate level

of net profits that is generated by the organization over the period. In addition, the table mainly highlight all the relevant information

regarding the change that has been incurred during the financial year of 2018. Moreover, the financial statement of the organization

has been depicted in the above table, where the income statement, balance sheet and cash flows statement has been adequately

depicted in the above table. From the valuation, it is detected that relevant improvements in the operations of the organization is

witnessed, where the organization has incurred profits during the financial year of 2018. Moreover, changes in the cash flow statement

of the has indicated a positive attribute, where the ending values of cash flows has increased from 150 in 2017 to 533 in 2018.

Financial Statements-Solution

Harish Enterprises ltd

Balance sheet as at 31 December 2018

Assets Liabilities

Current Assets Current Liabilities

Cash 533 Accounts payable 98

Accounts receivable 197 Income tax payable 36

Inventory 237 Dividend payable 152

Pre-paid expenses 50 Total current liabilities 197

Total Current Assets 1017 Non-Current Liabilities 483

Bank loans 618

Non-Current Assets Mortgage loans 403

Land and Building 1180 Corporate bonds 640

Motor vehicles 160 Total Non-Current Liabilities 1661

less depreciation -8

Plant and Equipment’s 500 Total Liabilities 2144

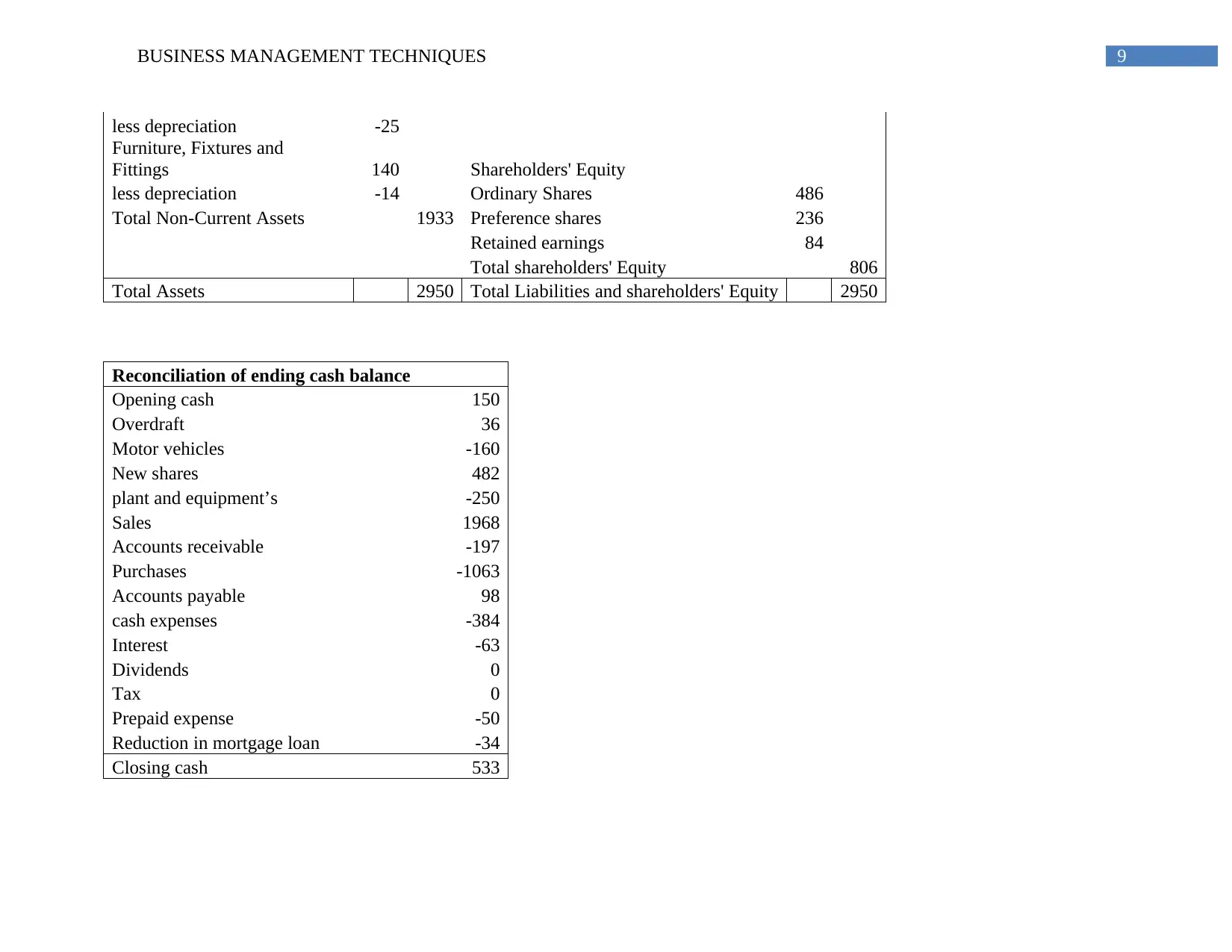

9BUSINESS MANAGEMENT TECHNIQUES

less depreciation -25

Furniture, Fixtures and

Fittings 140 Shareholders' Equity

less depreciation -14 Ordinary Shares 486

Total Non-Current Assets 1933 Preference shares 236

Retained earnings 84

Total shareholders' Equity 806

Total Assets 2950 Total Liabilities and shareholders' Equity 2950

Reconciliation of ending cash balance

Opening cash 150

Overdraft 36

Motor vehicles -160

New shares 482

plant and equipment’s -250

Sales 1968

Accounts receivable -197

Purchases -1063

Accounts payable 98

cash expenses -384

Interest -63

Dividends 0

Tax 0

Prepaid expense -50

Reduction in mortgage loan -34

Closing cash 533

less depreciation -25

Furniture, Fixtures and

Fittings 140 Shareholders' Equity

less depreciation -14 Ordinary Shares 486

Total Non-Current Assets 1933 Preference shares 236

Retained earnings 84

Total shareholders' Equity 806

Total Assets 2950 Total Liabilities and shareholders' Equity 2950

Reconciliation of ending cash balance

Opening cash 150

Overdraft 36

Motor vehicles -160

New shares 482

plant and equipment’s -250

Sales 1968

Accounts receivable -197

Purchases -1063

Accounts payable 98

cash expenses -384

Interest -63

Dividends 0

Tax 0

Prepaid expense -50

Reduction in mortgage loan -34

Closing cash 533

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10BUSINESS MANAGEMENT TECHNIQUES

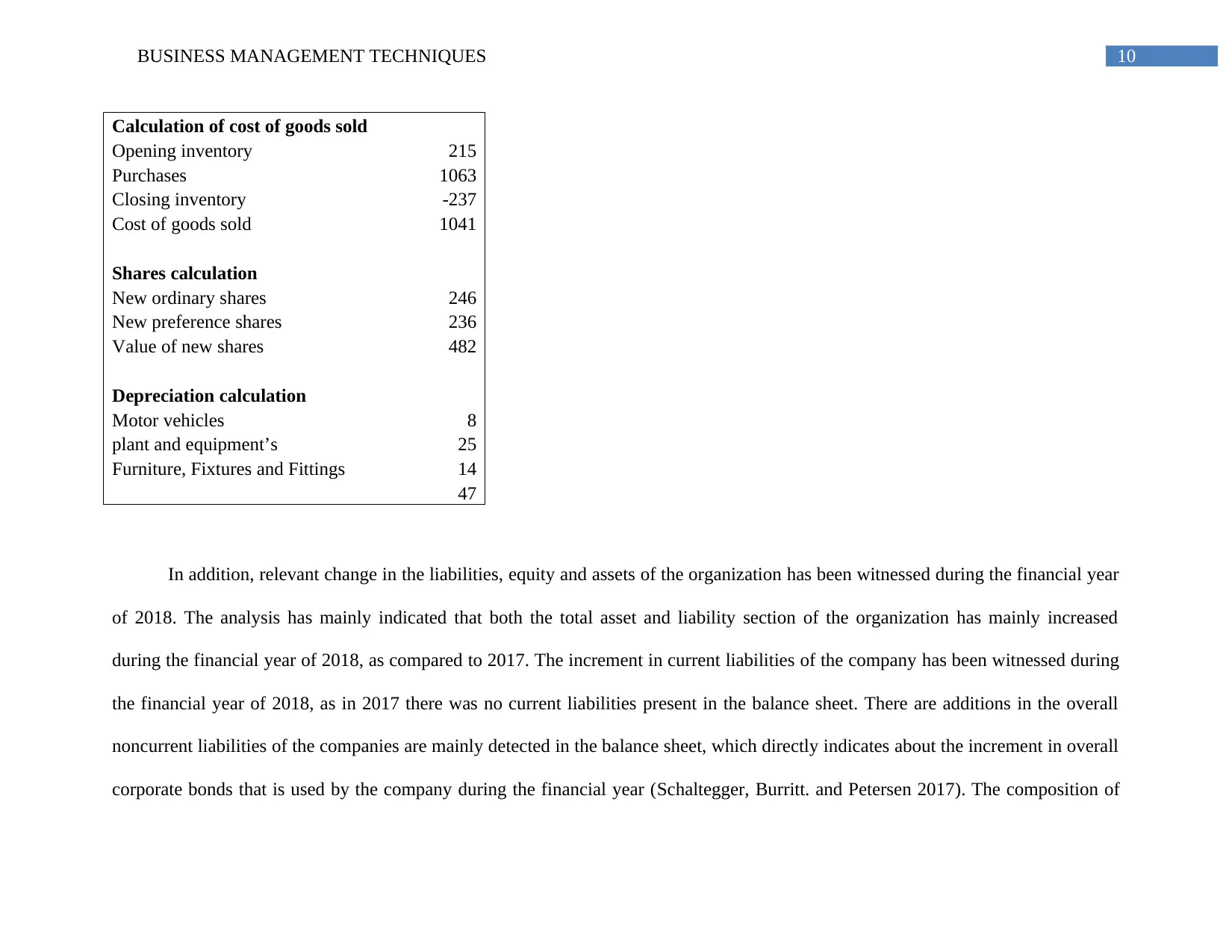

Calculation of cost of goods sold

Opening inventory 215

Purchases 1063

Closing inventory -237

Cost of goods sold 1041

Shares calculation

New ordinary shares 246

New preference shares 236

Value of new shares 482

Depreciation calculation

Motor vehicles 8

plant and equipment’s 25

Furniture, Fixtures and Fittings 14

47

In addition, relevant change in the liabilities, equity and assets of the organization has been witnessed during the financial year

of 2018. The analysis has mainly indicated that both the total asset and liability section of the organization has mainly increased

during the financial year of 2018, as compared to 2017. The increment in current liabilities of the company has been witnessed during

the financial year of 2018, as in 2017 there was no current liabilities present in the balance sheet. There are additions in the overall

noncurrent liabilities of the companies are mainly detected in the balance sheet, which directly indicates about the increment in overall

corporate bonds that is used by the company during the financial year (Schaltegger, Burritt. and Petersen 2017). The composition of

Calculation of cost of goods sold

Opening inventory 215

Purchases 1063

Closing inventory -237

Cost of goods sold 1041

Shares calculation

New ordinary shares 246

New preference shares 236

Value of new shares 482

Depreciation calculation

Motor vehicles 8

plant and equipment’s 25

Furniture, Fixtures and Fittings 14

47

In addition, relevant change in the liabilities, equity and assets of the organization has been witnessed during the financial year

of 2018. The analysis has mainly indicated that both the total asset and liability section of the organization has mainly increased

during the financial year of 2018, as compared to 2017. The increment in current liabilities of the company has been witnessed during

the financial year of 2018, as in 2017 there was no current liabilities present in the balance sheet. There are additions in the overall

noncurrent liabilities of the companies are mainly detected in the balance sheet, which directly indicates about the increment in overall

corporate bonds that is used by the company during the financial year (Schaltegger, Burritt. and Petersen 2017). The composition of

11BUSINESS MANAGEMENT TECHNIQUES

total liabilities is relevantly low than the total assets of the organization, where the equity section has mainly provided adequate

composition in the financial statement. The adequate calculation of cost of goods sold, shares and depreciation is mainly conducted for

preparing the annual report, which can provide adequate information regarding the financial position of the company.

total liabilities is relevantly low than the total assets of the organization, where the equity section has mainly provided adequate

composition in the financial statement. The adequate calculation of cost of goods sold, shares and depreciation is mainly conducted for

preparing the annual report, which can provide adequate information regarding the financial position of the company.

12BUSINESS MANAGEMENT TECHNIQUES

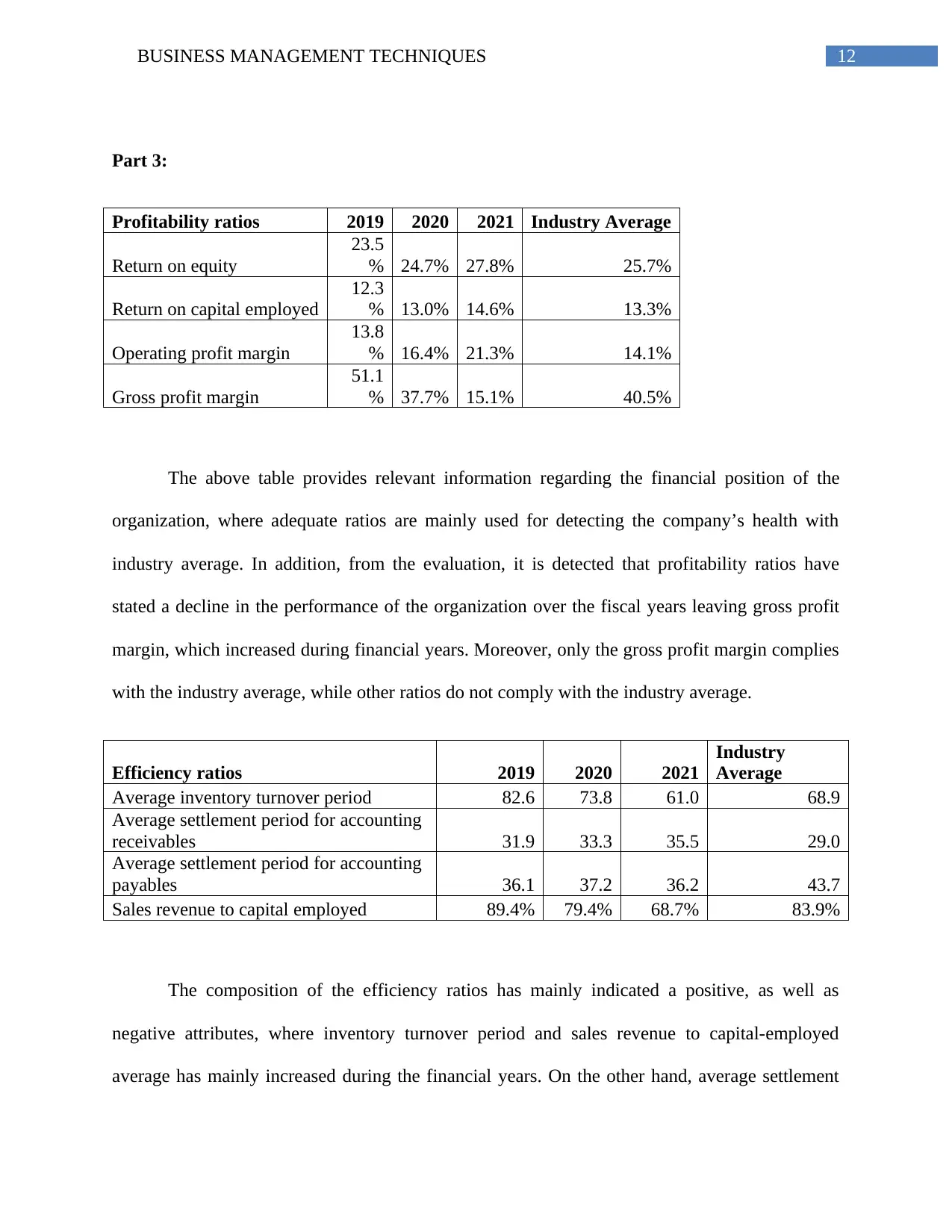

Part 3:

Profitability ratios 2019 2020 2021 Industry Average

Return on equity

23.5

% 24.7% 27.8% 25.7%

Return on capital employed

12.3

% 13.0% 14.6% 13.3%

Operating profit margin

13.8

% 16.4% 21.3% 14.1%

Gross profit margin

51.1

% 37.7% 15.1% 40.5%

The above table provides relevant information regarding the financial position of the

organization, where adequate ratios are mainly used for detecting the company’s health with

industry average. In addition, from the evaluation, it is detected that profitability ratios have

stated a decline in the performance of the organization over the fiscal years leaving gross profit

margin, which increased during financial years. Moreover, only the gross profit margin complies

with the industry average, while other ratios do not comply with the industry average.

Efficiency ratios 2019 2020 2021

Industry

Average

Average inventory turnover period 82.6 73.8 61.0 68.9

Average settlement period for accounting

receivables 31.9 33.3 35.5 29.0

Average settlement period for accounting

payables 36.1 37.2 36.2 43.7

Sales revenue to capital employed 89.4% 79.4% 68.7% 83.9%

The composition of the efficiency ratios has mainly indicated a positive, as well as

negative attributes, where inventory turnover period and sales revenue to capital-employed

average has mainly increased during the financial years. On the other hand, average settlement

Part 3:

Profitability ratios 2019 2020 2021 Industry Average

Return on equity

23.5

% 24.7% 27.8% 25.7%

Return on capital employed

12.3

% 13.0% 14.6% 13.3%

Operating profit margin

13.8

% 16.4% 21.3% 14.1%

Gross profit margin

51.1

% 37.7% 15.1% 40.5%

The above table provides relevant information regarding the financial position of the

organization, where adequate ratios are mainly used for detecting the company’s health with

industry average. In addition, from the evaluation, it is detected that profitability ratios have

stated a decline in the performance of the organization over the fiscal years leaving gross profit

margin, which increased during financial years. Moreover, only the gross profit margin complies

with the industry average, while other ratios do not comply with the industry average.

Efficiency ratios 2019 2020 2021

Industry

Average

Average inventory turnover period 82.6 73.8 61.0 68.9

Average settlement period for accounting

receivables 31.9 33.3 35.5 29.0

Average settlement period for accounting

payables 36.1 37.2 36.2 43.7

Sales revenue to capital employed 89.4% 79.4% 68.7% 83.9%

The composition of the efficiency ratios has mainly indicated a positive, as well as

negative attributes, where inventory turnover period and sales revenue to capital-employed

average has mainly increased during the financial years. On the other hand, average settlement

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13BUSINESS MANAGEMENT TECHNIQUES

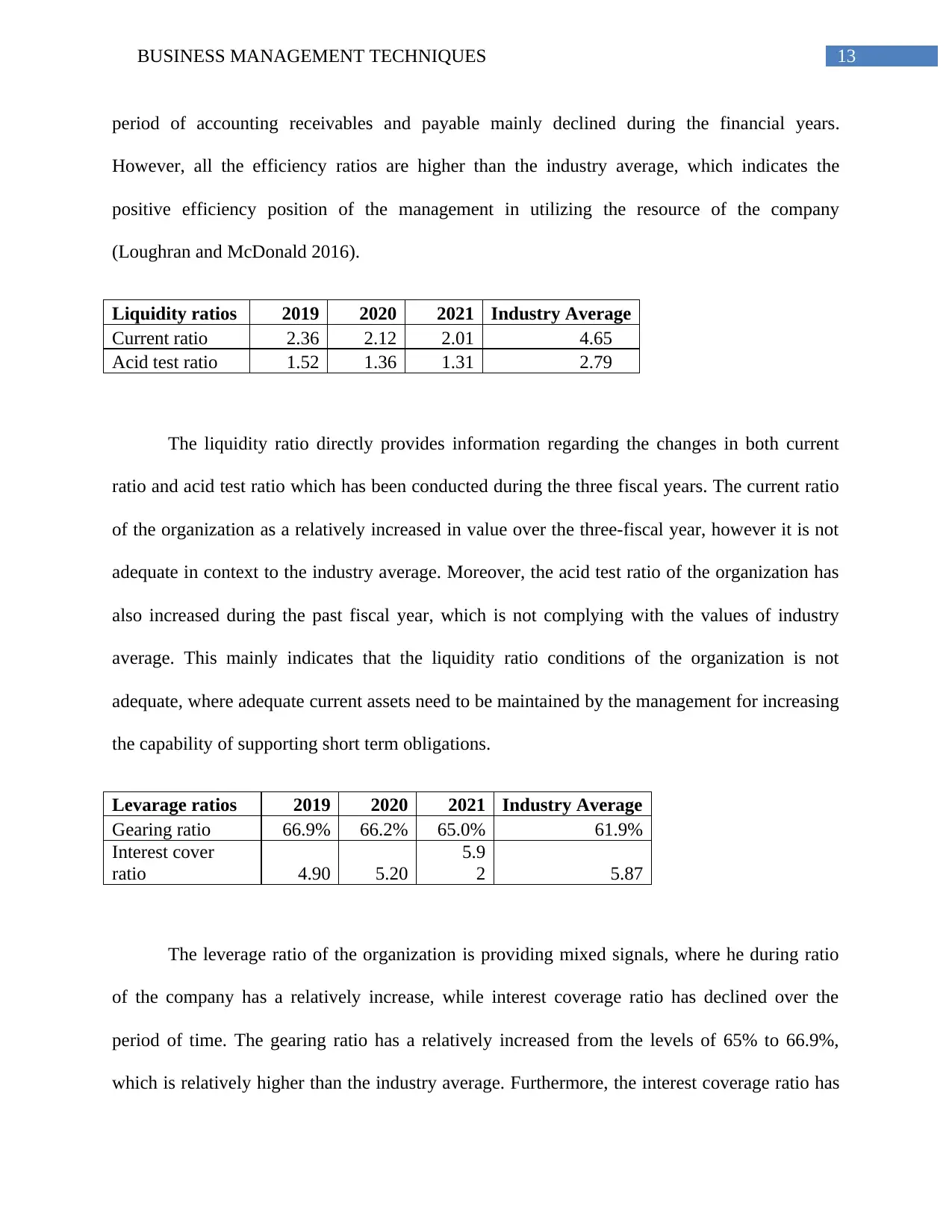

period of accounting receivables and payable mainly declined during the financial years.

However, all the efficiency ratios are higher than the industry average, which indicates the

positive efficiency position of the management in utilizing the resource of the company

(Loughran and McDonald 2016).

Liquidity ratios 2019 2020 2021 Industry Average

Current ratio 2.36 2.12 2.01 4.65

Acid test ratio 1.52 1.36 1.31 2.79

The liquidity ratio directly provides information regarding the changes in both current

ratio and acid test ratio which has been conducted during the three fiscal years. The current ratio

of the organization as a relatively increased in value over the three-fiscal year, however it is not

adequate in context to the industry average. Moreover, the acid test ratio of the organization has

also increased during the past fiscal year, which is not complying with the values of industry

average. This mainly indicates that the liquidity ratio conditions of the organization is not

adequate, where adequate current assets need to be maintained by the management for increasing

the capability of supporting short term obligations.

Levarage ratios 2019 2020 2021 Industry Average

Gearing ratio 66.9% 66.2% 65.0% 61.9%

Interest cover

ratio 4.90 5.20

5.9

2 5.87

The leverage ratio of the organization is providing mixed signals, where he during ratio

of the company has a relatively increase, while interest coverage ratio has declined over the

period of time. The gearing ratio has a relatively increased from the levels of 65% to 66.9%,

which is relatively higher than the industry average. Furthermore, the interest coverage ratio has

period of accounting receivables and payable mainly declined during the financial years.

However, all the efficiency ratios are higher than the industry average, which indicates the

positive efficiency position of the management in utilizing the resource of the company

(Loughran and McDonald 2016).

Liquidity ratios 2019 2020 2021 Industry Average

Current ratio 2.36 2.12 2.01 4.65

Acid test ratio 1.52 1.36 1.31 2.79

The liquidity ratio directly provides information regarding the changes in both current

ratio and acid test ratio which has been conducted during the three fiscal years. The current ratio

of the organization as a relatively increased in value over the three-fiscal year, however it is not

adequate in context to the industry average. Moreover, the acid test ratio of the organization has

also increased during the past fiscal year, which is not complying with the values of industry

average. This mainly indicates that the liquidity ratio conditions of the organization is not

adequate, where adequate current assets need to be maintained by the management for increasing

the capability of supporting short term obligations.

Levarage ratios 2019 2020 2021 Industry Average

Gearing ratio 66.9% 66.2% 65.0% 61.9%

Interest cover

ratio 4.90 5.20

5.9

2 5.87

The leverage ratio of the organization is providing mixed signals, where he during ratio

of the company has a relatively increase, while interest coverage ratio has declined over the

period of time. The gearing ratio has a relatively increased from the levels of 65% to 66.9%,

which is relatively higher than the industry average. Furthermore, the interest coverage ratio has

14BUSINESS MANAGEMENT TECHNIQUES

relatively declined over the period and is lower than the industry average, which indicates that

the organizations profit is not suitable to incur additional debts.

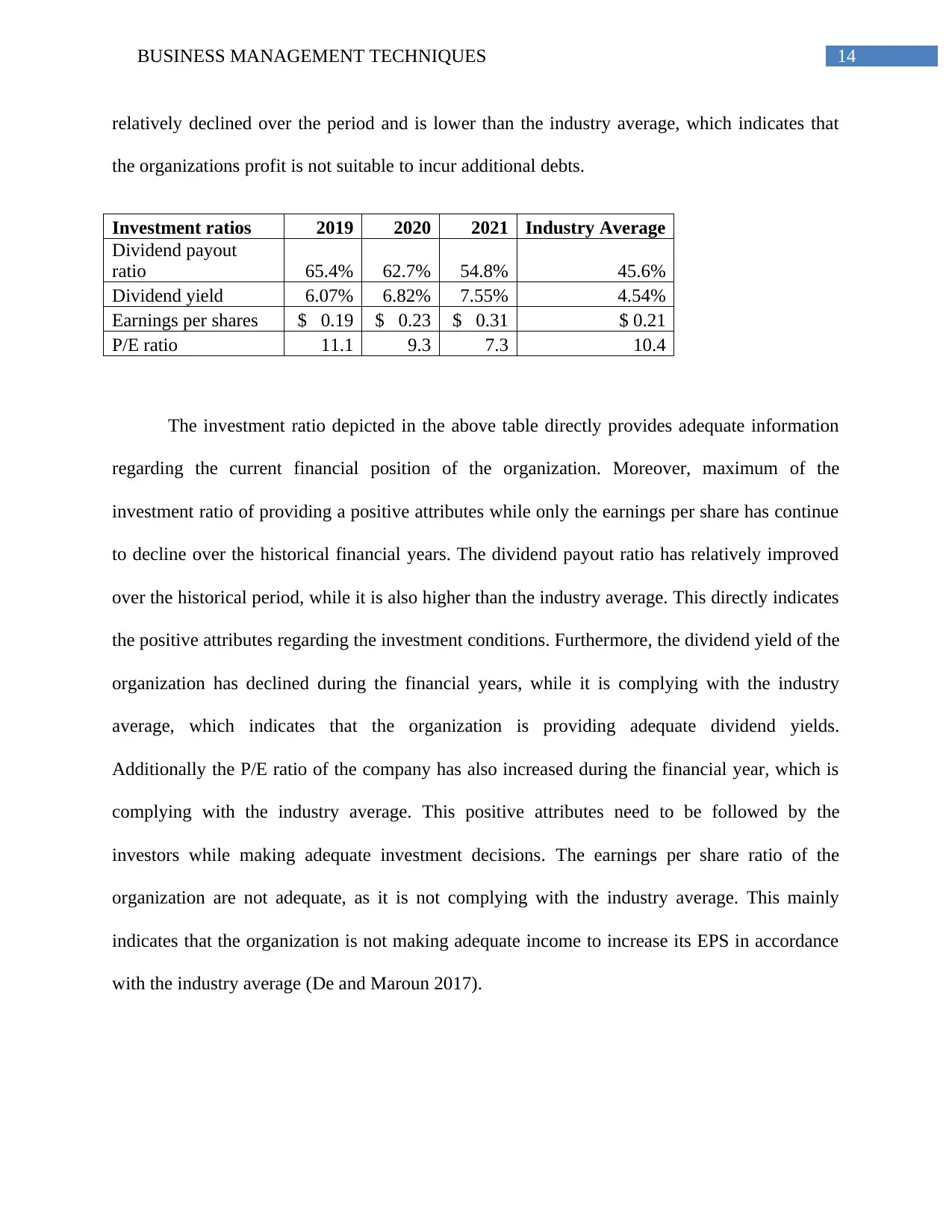

Investment ratios 2019 2020 2021 Industry Average

Dividend payout

ratio 65.4% 62.7% 54.8% 45.6%

Dividend yield 6.07% 6.82% 7.55% 4.54%

Earnings per shares $ 0.19 $ 0.23 $ 0.31 $ 0.21

P/E ratio 11.1 9.3 7.3 10.4

The investment ratio depicted in the above table directly provides adequate information

regarding the current financial position of the organization. Moreover, maximum of the

investment ratio of providing a positive attributes while only the earnings per share has continue

to decline over the historical financial years. The dividend payout ratio has relatively improved

over the historical period, while it is also higher than the industry average. This directly indicates

the positive attributes regarding the investment conditions. Furthermore, the dividend yield of the

organization has declined during the financial years, while it is complying with the industry

average, which indicates that the organization is providing adequate dividend yields.

Additionally the P/E ratio of the company has also increased during the financial year, which is

complying with the industry average. This positive attributes need to be followed by the

investors while making adequate investment decisions. The earnings per share ratio of the

organization are not adequate, as it is not complying with the industry average. This mainly

indicates that the organization is not making adequate income to increase its EPS in accordance

with the industry average (De and Maroun 2017).

relatively declined over the period and is lower than the industry average, which indicates that

the organizations profit is not suitable to incur additional debts.

Investment ratios 2019 2020 2021 Industry Average

Dividend payout

ratio 65.4% 62.7% 54.8% 45.6%

Dividend yield 6.07% 6.82% 7.55% 4.54%

Earnings per shares $ 0.19 $ 0.23 $ 0.31 $ 0.21

P/E ratio 11.1 9.3 7.3 10.4

The investment ratio depicted in the above table directly provides adequate information

regarding the current financial position of the organization. Moreover, maximum of the

investment ratio of providing a positive attributes while only the earnings per share has continue

to decline over the historical financial years. The dividend payout ratio has relatively improved

over the historical period, while it is also higher than the industry average. This directly indicates

the positive attributes regarding the investment conditions. Furthermore, the dividend yield of the

organization has declined during the financial years, while it is complying with the industry

average, which indicates that the organization is providing adequate dividend yields.

Additionally the P/E ratio of the company has also increased during the financial year, which is

complying with the industry average. This positive attributes need to be followed by the

investors while making adequate investment decisions. The earnings per share ratio of the

organization are not adequate, as it is not complying with the industry average. This mainly

indicates that the organization is not making adequate income to increase its EPS in accordance

with the industry average (De and Maroun 2017).

15BUSINESS MANAGEMENT TECHNIQUES

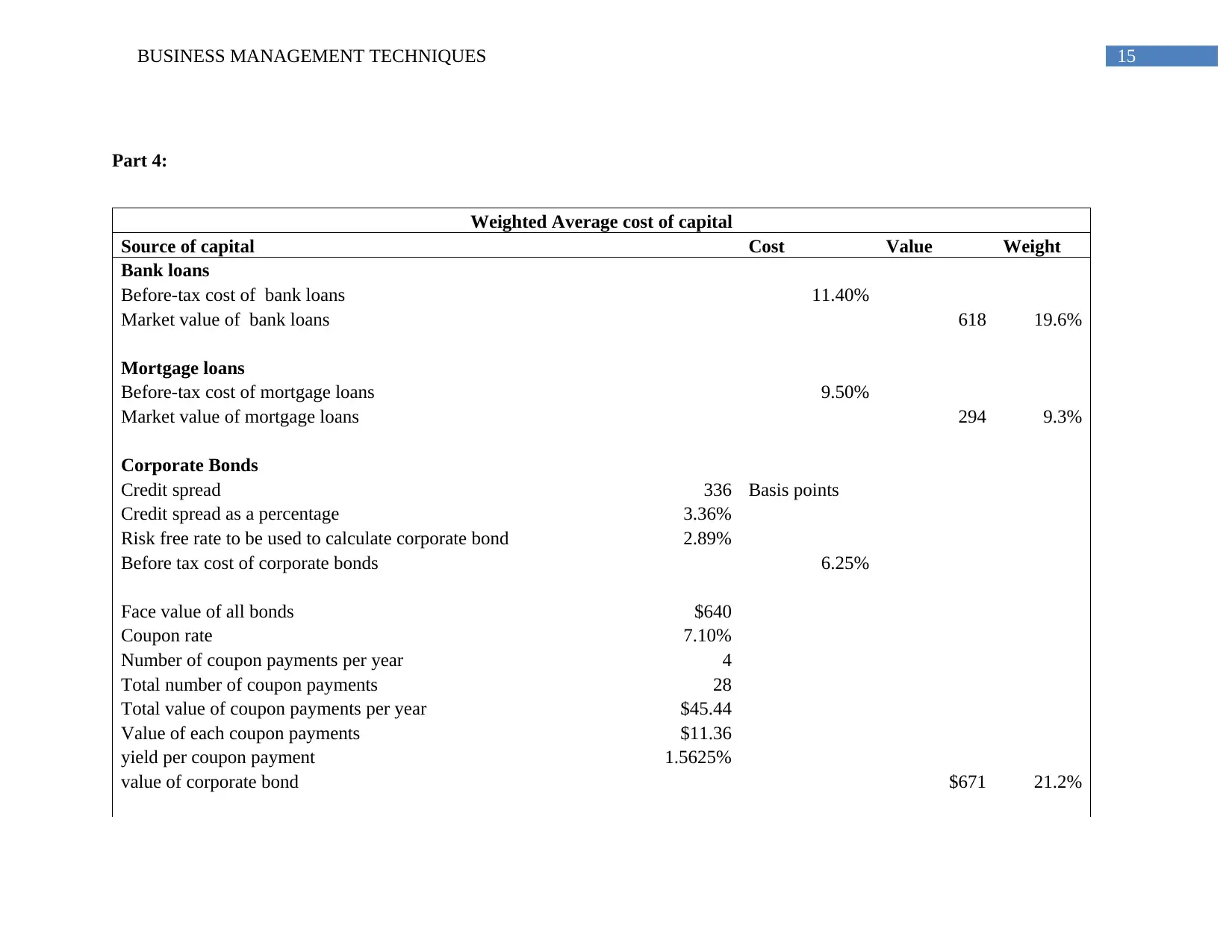

Part 4:

Weighted Average cost of capital

Source of capital Cost Value Weight

Bank loans

Before-tax cost of bank loans 11.40%

Market value of bank loans 618 19.6%

Mortgage loans

Before-tax cost of mortgage loans 9.50%

Market value of mortgage loans 294 9.3%

Corporate Bonds

Credit spread 336 Basis points

Credit spread as a percentage 3.36%

Risk free rate to be used to calculate corporate bond 2.89%

Before tax cost of corporate bonds 6.25%

Face value of all bonds $640

Coupon rate 7.10%

Number of coupon payments per year 4

Total number of coupon payments 28

Total value of coupon payments per year $45.44

Value of each coupon payments $11.36

yield per coupon payment 1.5625%

value of corporate bond $671 21.2%

Part 4:

Weighted Average cost of capital

Source of capital Cost Value Weight

Bank loans

Before-tax cost of bank loans 11.40%

Market value of bank loans 618 19.6%

Mortgage loans

Before-tax cost of mortgage loans 9.50%

Market value of mortgage loans 294 9.3%

Corporate Bonds

Credit spread 336 Basis points

Credit spread as a percentage 3.36%

Risk free rate to be used to calculate corporate bond 2.89%

Before tax cost of corporate bonds 6.25%

Face value of all bonds $640

Coupon rate 7.10%

Number of coupon payments per year 4

Total number of coupon payments 28

Total value of coupon payments per year $45.44

Value of each coupon payments $11.36

yield per coupon payment 1.5625%

value of corporate bond $671 21.2%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16BUSINESS MANAGEMENT TECHNIQUES

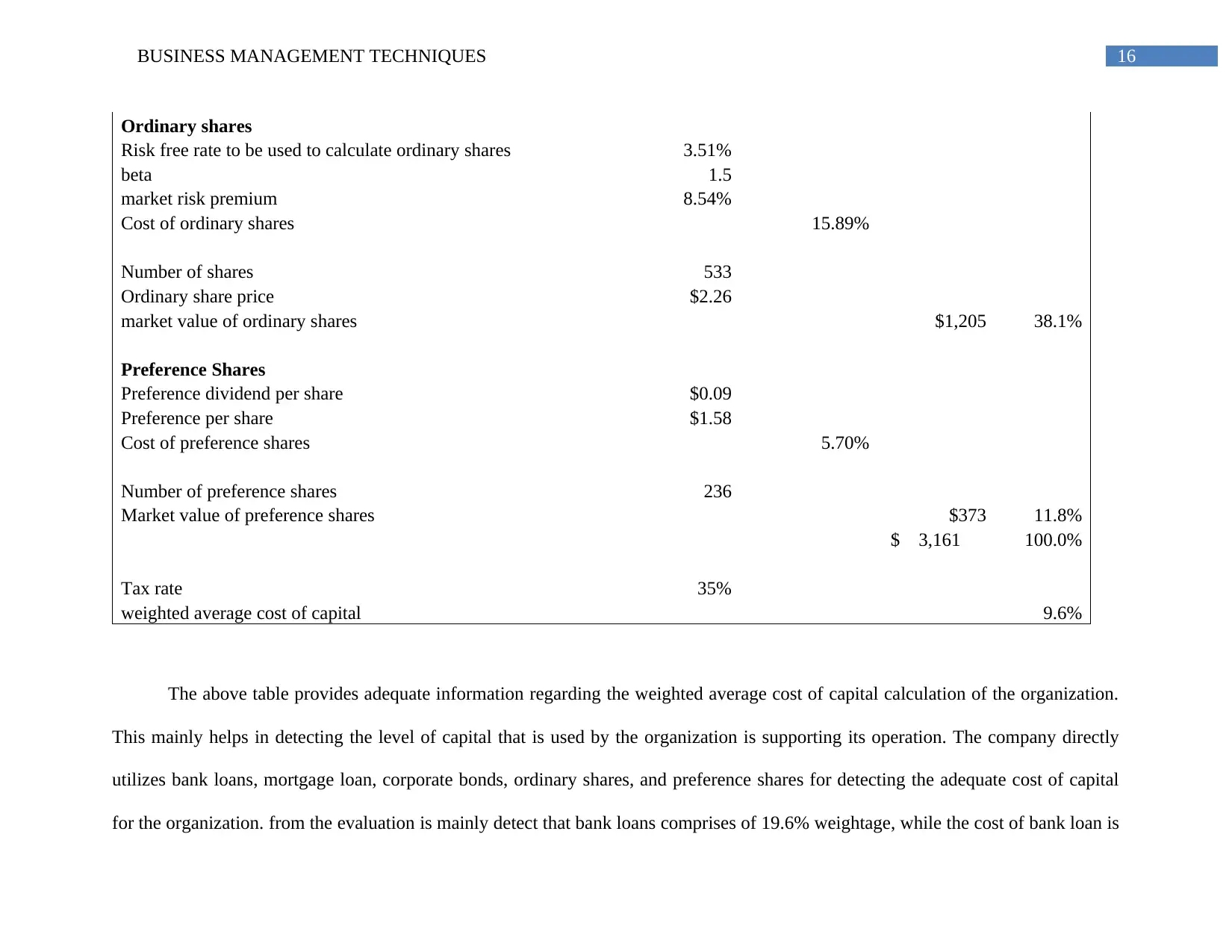

Ordinary shares

Risk free rate to be used to calculate ordinary shares 3.51%

beta 1.5

market risk premium 8.54%

Cost of ordinary shares 15.89%

Number of shares 533

Ordinary share price $2.26

market value of ordinary shares $1,205 38.1%

Preference Shares

Preference dividend per share $0.09

Preference per share $1.58

Cost of preference shares 5.70%

Number of preference shares 236

Market value of preference shares $373 11.8%

$ 3,161 100.0%

Tax rate 35%

weighted average cost of capital 9.6%

The above table provides adequate information regarding the weighted average cost of capital calculation of the organization.

This mainly helps in detecting the level of capital that is used by the organization is supporting its operation. The company directly

utilizes bank loans, mortgage loan, corporate bonds, ordinary shares, and preference shares for detecting the adequate cost of capital

for the organization. from the evaluation is mainly detect that bank loans comprises of 19.6% weightage, while the cost of bank loan is

Ordinary shares

Risk free rate to be used to calculate ordinary shares 3.51%

beta 1.5

market risk premium 8.54%

Cost of ordinary shares 15.89%

Number of shares 533

Ordinary share price $2.26

market value of ordinary shares $1,205 38.1%

Preference Shares

Preference dividend per share $0.09

Preference per share $1.58

Cost of preference shares 5.70%

Number of preference shares 236

Market value of preference shares $373 11.8%

$ 3,161 100.0%

Tax rate 35%

weighted average cost of capital 9.6%

The above table provides adequate information regarding the weighted average cost of capital calculation of the organization.

This mainly helps in detecting the level of capital that is used by the organization is supporting its operation. The company directly

utilizes bank loans, mortgage loan, corporate bonds, ordinary shares, and preference shares for detecting the adequate cost of capital

for the organization. from the evaluation is mainly detect that bank loans comprises of 19.6% weightage, while the cost of bank loan is

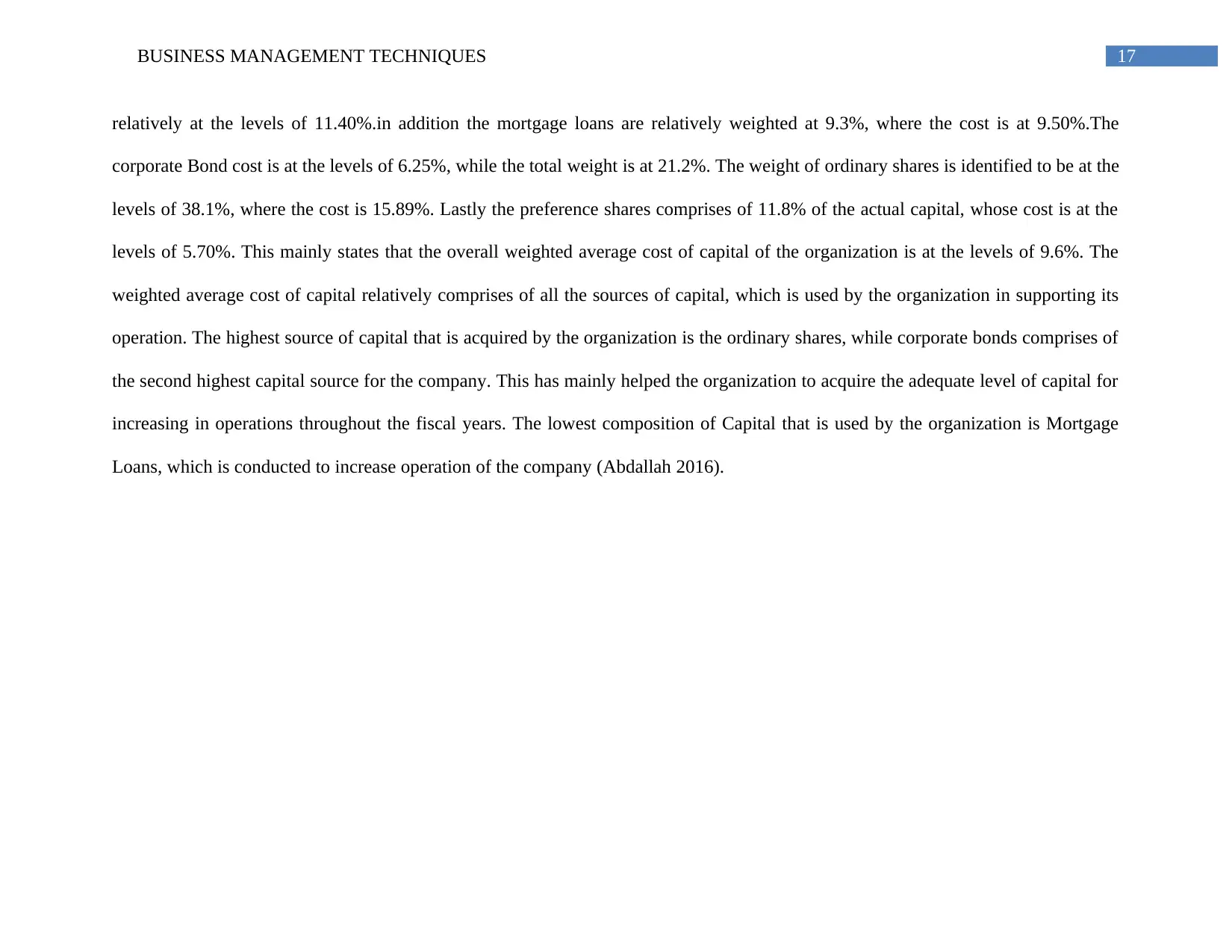

17BUSINESS MANAGEMENT TECHNIQUES

relatively at the levels of 11.40%.in addition the mortgage loans are relatively weighted at 9.3%, where the cost is at 9.50%.The

corporate Bond cost is at the levels of 6.25%, while the total weight is at 21.2%. The weight of ordinary shares is identified to be at the

levels of 38.1%, where the cost is 15.89%. Lastly the preference shares comprises of 11.8% of the actual capital, whose cost is at the

levels of 5.70%. This mainly states that the overall weighted average cost of capital of the organization is at the levels of 9.6%. The

weighted average cost of capital relatively comprises of all the sources of capital, which is used by the organization in supporting its

operation. The highest source of capital that is acquired by the organization is the ordinary shares, while corporate bonds comprises of

the second highest capital source for the company. This has mainly helped the organization to acquire the adequate level of capital for

increasing in operations throughout the fiscal years. The lowest composition of Capital that is used by the organization is Mortgage

Loans, which is conducted to increase operation of the company (Abdallah 2016).

relatively at the levels of 11.40%.in addition the mortgage loans are relatively weighted at 9.3%, where the cost is at 9.50%.The

corporate Bond cost is at the levels of 6.25%, while the total weight is at 21.2%. The weight of ordinary shares is identified to be at the

levels of 38.1%, where the cost is 15.89%. Lastly the preference shares comprises of 11.8% of the actual capital, whose cost is at the

levels of 5.70%. This mainly states that the overall weighted average cost of capital of the organization is at the levels of 9.6%. The

weighted average cost of capital relatively comprises of all the sources of capital, which is used by the organization in supporting its

operation. The highest source of capital that is acquired by the organization is the ordinary shares, while corporate bonds comprises of

the second highest capital source for the company. This has mainly helped the organization to acquire the adequate level of capital for

increasing in operations throughout the fiscal years. The lowest composition of Capital that is used by the organization is Mortgage

Loans, which is conducted to increase operation of the company (Abdallah 2016).

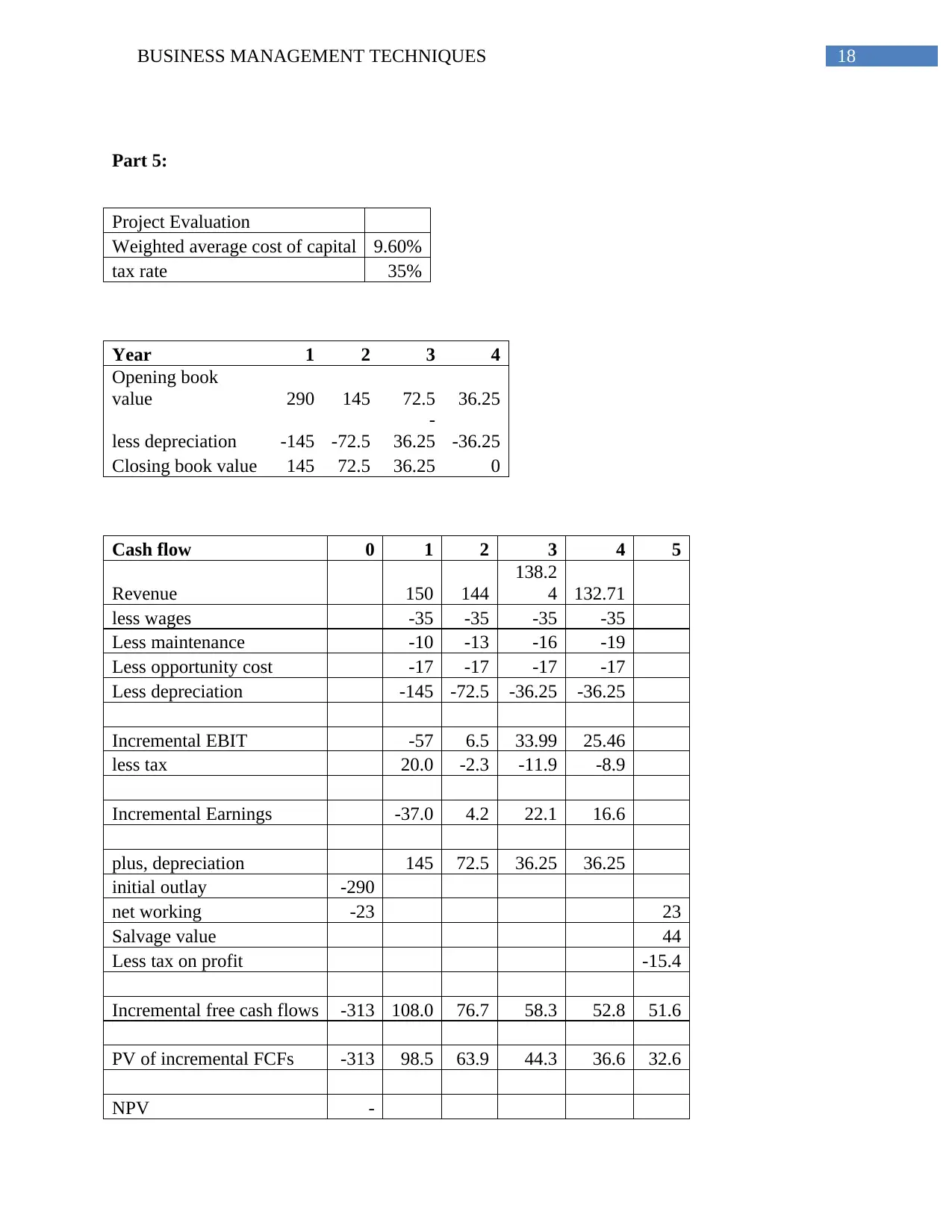

BUSINESS MANAGEMENT TECHNIQUES 18

Part 5:

Project Evaluation

Weighted average cost of capital 9.60%

tax rate 35%

Year 1 2 3 4

Opening book

value 290 145 72.5 36.25

less depreciation -145 -72.5

-

36.25 -36.25

Closing book value 145 72.5 36.25 0

Cash flow 0 1 2 3 4 5

Revenue 150 144

138.2

4 132.71

less wages -35 -35 -35 -35

Less maintenance -10 -13 -16 -19

Less opportunity cost -17 -17 -17 -17

Less depreciation -145 -72.5 -36.25 -36.25

Incremental EBIT -57 6.5 33.99 25.46

less tax 20.0 -2.3 -11.9 -8.9

Incremental Earnings -37.0 4.2 22.1 16.6

plus, depreciation 145 72.5 36.25 36.25

initial outlay -290

net working -23 23

Salvage value 44

Less tax on profit -15.4

Incremental free cash flows -313 108.0 76.7 58.3 52.8 51.6

PV of incremental FCFs -313 98.5 63.9 44.3 36.6 32.6

NPV -

Part 5:

Project Evaluation

Weighted average cost of capital 9.60%

tax rate 35%

Year 1 2 3 4

Opening book

value 290 145 72.5 36.25

less depreciation -145 -72.5

-

36.25 -36.25

Closing book value 145 72.5 36.25 0

Cash flow 0 1 2 3 4 5

Revenue 150 144

138.2

4 132.71

less wages -35 -35 -35 -35

Less maintenance -10 -13 -16 -19

Less opportunity cost -17 -17 -17 -17

Less depreciation -145 -72.5 -36.25 -36.25

Incremental EBIT -57 6.5 33.99 25.46

less tax 20.0 -2.3 -11.9 -8.9

Incremental Earnings -37.0 4.2 22.1 16.6

plus, depreciation 145 72.5 36.25 36.25

initial outlay -290

net working -23 23

Salvage value 44

Less tax on profit -15.4

Incremental free cash flows -313 108.0 76.7 58.3 52.8 51.6

PV of incremental FCFs -313 98.5 63.9 44.3 36.6 32.6

NPV -

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS MANAGEMENT TECHNIQUES 19

37.1

The calculation provides all the relevant information regarding the net present value

calculation that is conducted for the organization. From the valuation detected that the

discounting rate is mainly calculated at the levels of 9.60%, while the overall tax rate is

considered as 35%. Moreover, the book value of the assets over the period of 4 years is mainly

calculated to detect the actual depreciation of the assets. This depreciation calculation will

eventually help in detecting the actual levels of tax saving that are conducted in the project. From

the calculation it is adequately depicted that the overall incremental free cash flows of the

organization is considered to be negative in nature, as the expense expenses conducted in the

initial year is not being complementary by the future cash flow. Wood (2016) argued that

discounting rate calculation can be manipulated, as organization needs to derive the values from

the actual cost of capital that is used by the company.

The cash flows anticipated for the project is relatively discounted to determine the

present value of the future cash flows. This eventually helps in selecting the actual value that will

be contributed by the project to the organization. However, the calculation of Net present value

directly indicates the negative figure, which states that the organization should not proceed with

the project, as it will incur loss for the organization. Brief (2014) indicated that net present value

calculation actually help in detecting the present value of future cash flows which allows the

organization to understand the project that could support their future operations.

37.1

The calculation provides all the relevant information regarding the net present value

calculation that is conducted for the organization. From the valuation detected that the

discounting rate is mainly calculated at the levels of 9.60%, while the overall tax rate is

considered as 35%. Moreover, the book value of the assets over the period of 4 years is mainly

calculated to detect the actual depreciation of the assets. This depreciation calculation will

eventually help in detecting the actual levels of tax saving that are conducted in the project. From

the calculation it is adequately depicted that the overall incremental free cash flows of the

organization is considered to be negative in nature, as the expense expenses conducted in the

initial year is not being complementary by the future cash flow. Wood (2016) argued that

discounting rate calculation can be manipulated, as organization needs to derive the values from

the actual cost of capital that is used by the company.

The cash flows anticipated for the project is relatively discounted to determine the

present value of the future cash flows. This eventually helps in selecting the actual value that will

be contributed by the project to the organization. However, the calculation of Net present value

directly indicates the negative figure, which states that the organization should not proceed with

the project, as it will incur loss for the organization. Brief (2014) indicated that net present value

calculation actually help in detecting the present value of future cash flows which allows the

organization to understand the project that could support their future operations.

BUSINESS MANAGEMENT TECHNIQUES 20

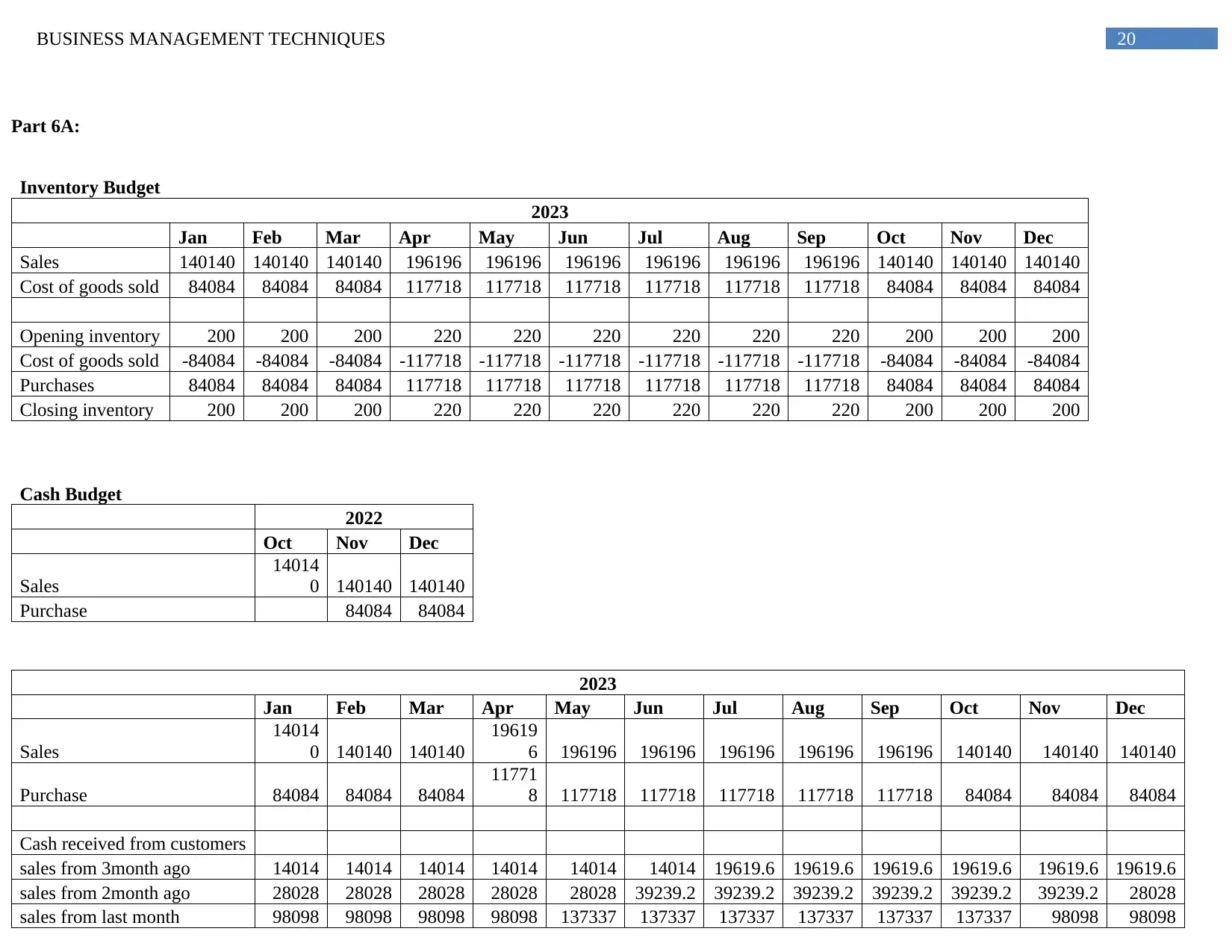

Part 6A:

Inventory Budget

2023

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Sales 140140 140140 140140 196196 196196 196196 196196 196196 196196 140140 140140 140140

Cost of goods sold 84084 84084 84084 117718 117718 117718 117718 117718 117718 84084 84084 84084

Opening inventory 200 200 200 220 220 220 220 220 220 200 200 200

Cost of goods sold -84084 -84084 -84084 -117718 -117718 -117718 -117718 -117718 -117718 -84084 -84084 -84084

Purchases 84084 84084 84084 117718 117718 117718 117718 117718 117718 84084 84084 84084

Closing inventory 200 200 200 220 220 220 220 220 220 200 200 200

Cash Budget

2022

Oct Nov Dec

Sales

14014

0 140140 140140

Purchase 84084 84084

2023

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Sales

14014

0 140140 140140

19619

6 196196 196196 196196 196196 196196 140140 140140 140140

Purchase 84084 84084 84084

11771

8 117718 117718 117718 117718 117718 84084 84084 84084

Cash received from customers

sales from 3month ago 14014 14014 14014 14014 14014 14014 19619.6 19619.6 19619.6 19619.6 19619.6 19619.6

sales from 2month ago 28028 28028 28028 28028 28028 39239.2 39239.2 39239.2 39239.2 39239.2 39239.2 28028

sales from last month 98098 98098 98098 98098 137337 137337 137337 137337 137337 137337 98098 98098

Part 6A:

Inventory Budget

2023

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Sales 140140 140140 140140 196196 196196 196196 196196 196196 196196 140140 140140 140140

Cost of goods sold 84084 84084 84084 117718 117718 117718 117718 117718 117718 84084 84084 84084

Opening inventory 200 200 200 220 220 220 220 220 220 200 200 200

Cost of goods sold -84084 -84084 -84084 -117718 -117718 -117718 -117718 -117718 -117718 -84084 -84084 -84084

Purchases 84084 84084 84084 117718 117718 117718 117718 117718 117718 84084 84084 84084

Closing inventory 200 200 200 220 220 220 220 220 220 200 200 200

Cash Budget

2022

Oct Nov Dec

Sales

14014

0 140140 140140

Purchase 84084 84084

2023

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Sales

14014

0 140140 140140

19619

6 196196 196196 196196 196196 196196 140140 140140 140140

Purchase 84084 84084 84084

11771

8 117718 117718 117718 117718 117718 84084 84084 84084

Cash received from customers

sales from 3month ago 14014 14014 14014 14014 14014 14014 19619.6 19619.6 19619.6 19619.6 19619.6 19619.6

sales from 2month ago 28028 28028 28028 28028 28028 39239.2 39239.2 39239.2 39239.2 39239.2 39239.2 28028

sales from last month 98098 98098 98098 98098 137337 137337 137337 137337 137337 137337 98098 98098

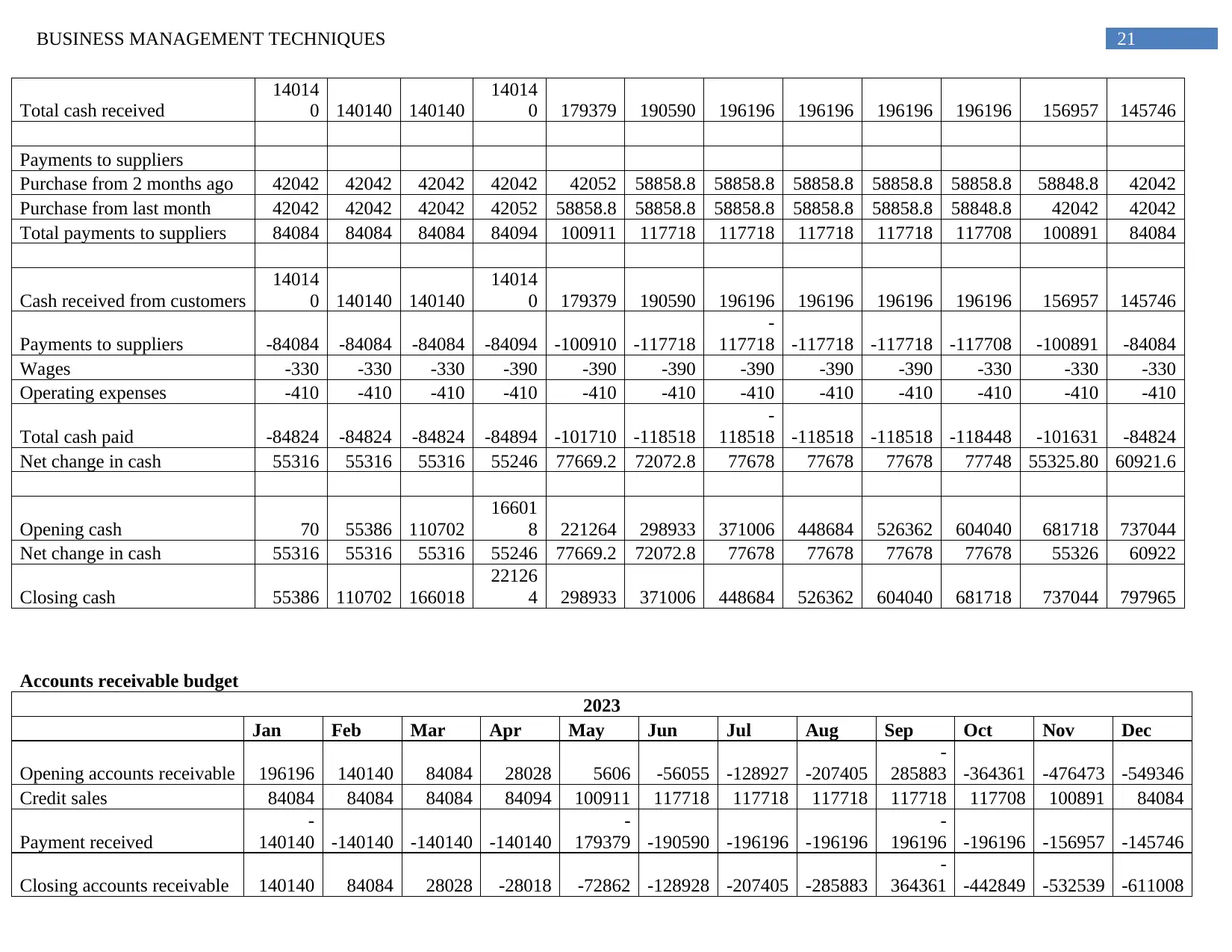

BUSINESS MANAGEMENT TECHNIQUES 21

Total cash received

14014

0 140140 140140

14014

0 179379 190590 196196 196196 196196 196196 156957 145746

Payments to suppliers

Purchase from 2 months ago 42042 42042 42042 42042 42052 58858.8 58858.8 58858.8 58858.8 58858.8 58848.8 42042

Purchase from last month 42042 42042 42042 42052 58858.8 58858.8 58858.8 58858.8 58858.8 58848.8 42042 42042

Total payments to suppliers 84084 84084 84084 84094 100911 117718 117718 117718 117718 117708 100891 84084

Cash received from customers

14014

0 140140 140140

14014

0 179379 190590 196196 196196 196196 196196 156957 145746

Payments to suppliers -84084 -84084 -84084 -84094 -100910 -117718

-

117718 -117718 -117718 -117708 -100891 -84084

Wages -330 -330 -330 -390 -390 -390 -390 -390 -390 -330 -330 -330

Operating expenses -410 -410 -410 -410 -410 -410 -410 -410 -410 -410 -410 -410

Total cash paid -84824 -84824 -84824 -84894 -101710 -118518

-

118518 -118518 -118518 -118448 -101631 -84824

Net change in cash 55316 55316 55316 55246 77669.2 72072.8 77678 77678 77678 77748 55325.80 60921.6

Opening cash 70 55386 110702

16601

8 221264 298933 371006 448684 526362 604040 681718 737044

Net change in cash 55316 55316 55316 55246 77669.2 72072.8 77678 77678 77678 77678 55326 60922

Closing cash 55386 110702 166018

22126

4 298933 371006 448684 526362 604040 681718 737044 797965

Accounts receivable budget

2023

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Opening accounts receivable 196196 140140 84084 28028 5606 -56055 -128927 -207405

-

285883 -364361 -476473 -549346

Credit sales 84084 84084 84084 84094 100911 117718 117718 117718 117718 117708 100891 84084

Payment received

-

140140 -140140 -140140 -140140

-

179379 -190590 -196196 -196196

-

196196 -196196 -156957 -145746

Closing accounts receivable 140140 84084 28028 -28018 -72862 -128928 -207405 -285883

-

364361 -442849 -532539 -611008

Total cash received

14014

0 140140 140140

14014

0 179379 190590 196196 196196 196196 196196 156957 145746

Payments to suppliers

Purchase from 2 months ago 42042 42042 42042 42042 42052 58858.8 58858.8 58858.8 58858.8 58858.8 58848.8 42042

Purchase from last month 42042 42042 42042 42052 58858.8 58858.8 58858.8 58858.8 58858.8 58848.8 42042 42042

Total payments to suppliers 84084 84084 84084 84094 100911 117718 117718 117718 117718 117708 100891 84084

Cash received from customers

14014

0 140140 140140

14014

0 179379 190590 196196 196196 196196 196196 156957 145746

Payments to suppliers -84084 -84084 -84084 -84094 -100910 -117718

-

117718 -117718 -117718 -117708 -100891 -84084

Wages -330 -330 -330 -390 -390 -390 -390 -390 -390 -330 -330 -330

Operating expenses -410 -410 -410 -410 -410 -410 -410 -410 -410 -410 -410 -410

Total cash paid -84824 -84824 -84824 -84894 -101710 -118518

-

118518 -118518 -118518 -118448 -101631 -84824

Net change in cash 55316 55316 55316 55246 77669.2 72072.8 77678 77678 77678 77748 55325.80 60921.6

Opening cash 70 55386 110702

16601

8 221264 298933 371006 448684 526362 604040 681718 737044

Net change in cash 55316 55316 55316 55246 77669.2 72072.8 77678 77678 77678 77678 55326 60922

Closing cash 55386 110702 166018

22126

4 298933 371006 448684 526362 604040 681718 737044 797965

Accounts receivable budget

2023

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Opening accounts receivable 196196 140140 84084 28028 5606 -56055 -128927 -207405

-

285883 -364361 -476473 -549346

Credit sales 84084 84084 84084 84094 100911 117718 117718 117718 117718 117708 100891 84084

Payment received

-

140140 -140140 -140140 -140140

-

179379 -190590 -196196 -196196

-

196196 -196196 -156957 -145746

Closing accounts receivable 140140 84084 28028 -28018 -72862 -128928 -207405 -285883

-

364361 -442849 -532539 -611008

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BUSINESS MANAGEMENT TECHNIQUES 22

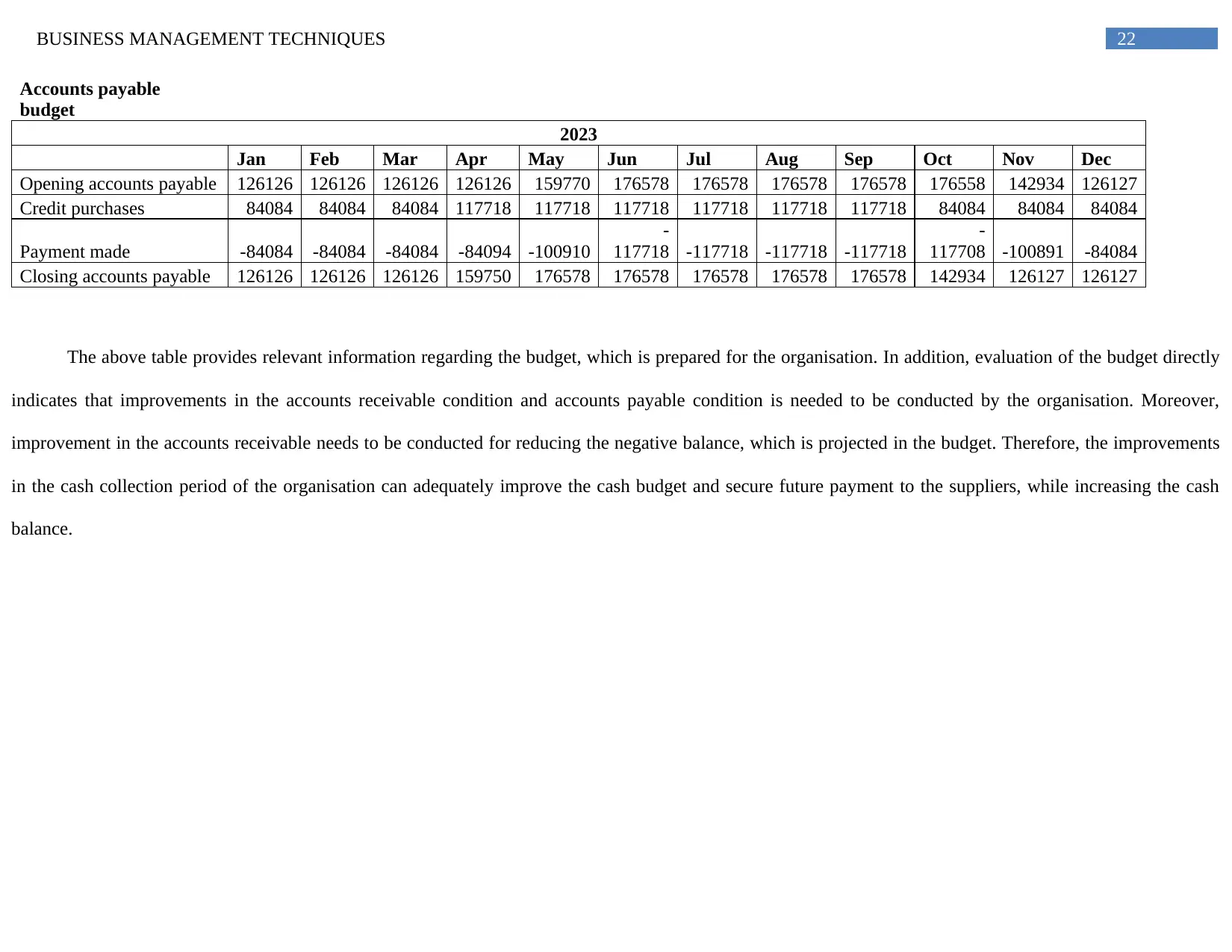

Accounts payable

budget

2023

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Opening accounts payable 126126 126126 126126 126126 159770 176578 176578 176578 176578 176558 142934 126127

Credit purchases 84084 84084 84084 117718 117718 117718 117718 117718 117718 84084 84084 84084

Payment made -84084 -84084 -84084 -84094 -100910

-

117718 -117718 -117718 -117718

-

117708 -100891 -84084

Closing accounts payable 126126 126126 126126 159750 176578 176578 176578 176578 176578 142934 126127 126127

The above table provides relevant information regarding the budget, which is prepared for the organisation. In addition, evaluation of the budget directly

indicates that improvements in the accounts receivable condition and accounts payable condition is needed to be conducted by the organisation. Moreover,

improvement in the accounts receivable needs to be conducted for reducing the negative balance, which is projected in the budget. Therefore, the improvements

in the cash collection period of the organisation can adequately improve the cash budget and secure future payment to the suppliers, while increasing the cash

balance.

Accounts payable

budget

2023

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

Opening accounts payable 126126 126126 126126 126126 159770 176578 176578 176578 176578 176558 142934 126127

Credit purchases 84084 84084 84084 117718 117718 117718 117718 117718 117718 84084 84084 84084

Payment made -84084 -84084 -84084 -84094 -100910

-

117718 -117718 -117718 -117718

-

117708 -100891 -84084

Closing accounts payable 126126 126126 126126 159750 176578 176578 176578 176578 176578 142934 126127 126127

The above table provides relevant information regarding the budget, which is prepared for the organisation. In addition, evaluation of the budget directly

indicates that improvements in the accounts receivable condition and accounts payable condition is needed to be conducted by the organisation. Moreover,

improvement in the accounts receivable needs to be conducted for reducing the negative balance, which is projected in the budget. Therefore, the improvements

in the cash collection period of the organisation can adequately improve the cash budget and secure future payment to the suppliers, while increasing the cash

balance.

BUSINESS MANAGEMENT TECHNIQUES 23

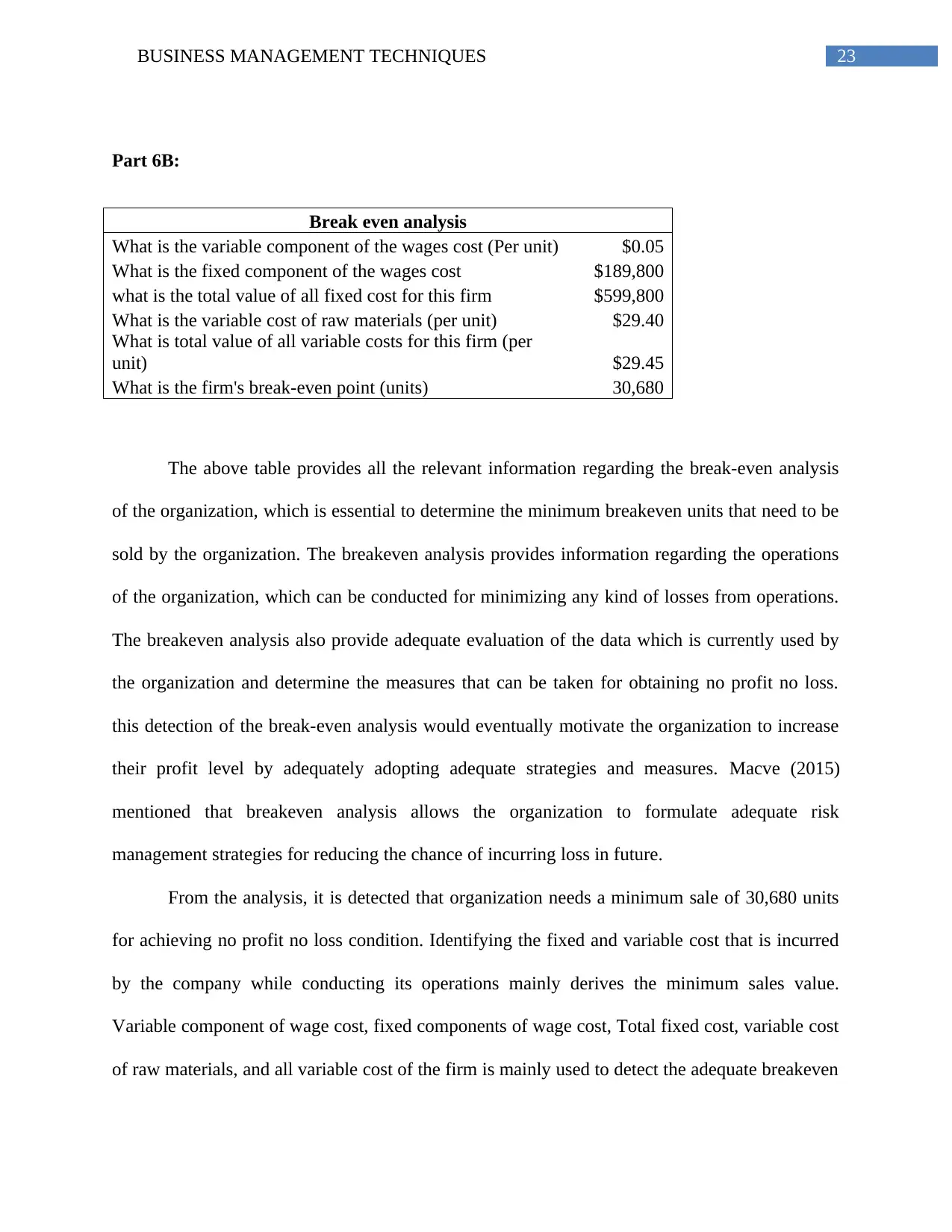

Part 6B:

Break even analysis

What is the variable component of the wages cost (Per unit) $0.05

What is the fixed component of the wages cost $189,800

what is the total value of all fixed cost for this firm $599,800

What is the variable cost of raw materials (per unit) $29.40

What is total value of all variable costs for this firm (per

unit) $29.45

What is the firm's break-even point (units) 30,680

The above table provides all the relevant information regarding the break-even analysis

of the organization, which is essential to determine the minimum breakeven units that need to be

sold by the organization. The breakeven analysis provides information regarding the operations

of the organization, which can be conducted for minimizing any kind of losses from operations.

The breakeven analysis also provide adequate evaluation of the data which is currently used by

the organization and determine the measures that can be taken for obtaining no profit no loss.

this detection of the break-even analysis would eventually motivate the organization to increase

their profit level by adequately adopting adequate strategies and measures. Macve (2015)

mentioned that breakeven analysis allows the organization to formulate adequate risk

management strategies for reducing the chance of incurring loss in future.

From the analysis, it is detected that organization needs a minimum sale of 30,680 units

for achieving no profit no loss condition. Identifying the fixed and variable cost that is incurred

by the company while conducting its operations mainly derives the minimum sales value.

Variable component of wage cost, fixed components of wage cost, Total fixed cost, variable cost

of raw materials, and all variable cost of the firm is mainly used to detect the adequate breakeven

Part 6B:

Break even analysis

What is the variable component of the wages cost (Per unit) $0.05

What is the fixed component of the wages cost $189,800

what is the total value of all fixed cost for this firm $599,800

What is the variable cost of raw materials (per unit) $29.40

What is total value of all variable costs for this firm (per

unit) $29.45

What is the firm's break-even point (units) 30,680

The above table provides all the relevant information regarding the break-even analysis

of the organization, which is essential to determine the minimum breakeven units that need to be

sold by the organization. The breakeven analysis provides information regarding the operations

of the organization, which can be conducted for minimizing any kind of losses from operations.

The breakeven analysis also provide adequate evaluation of the data which is currently used by

the organization and determine the measures that can be taken for obtaining no profit no loss.

this detection of the break-even analysis would eventually motivate the organization to increase

their profit level by adequately adopting adequate strategies and measures. Macve (2015)

mentioned that breakeven analysis allows the organization to formulate adequate risk

management strategies for reducing the chance of incurring loss in future.

From the analysis, it is detected that organization needs a minimum sale of 30,680 units

for achieving no profit no loss condition. Identifying the fixed and variable cost that is incurred

by the company while conducting its operations mainly derives the minimum sales value.

Variable component of wage cost, fixed components of wage cost, Total fixed cost, variable cost

of raw materials, and all variable cost of the firm is mainly used to detect the adequate breakeven

BUSINESS MANAGEMENT TECHNIQUES 24

point for the organization. Therefore, it could be understand that increasing the units for sale

from 30,680 can eventually allow the organization to generate adequate profits from operations.

Modell (2014) argued that without adequate Research and calculation the actual fixed and

variable cost is hard to determine, which can reduce the authenticity of the break-even analysis

conducted for the organization.

point for the organization. Therefore, it could be understand that increasing the units for sale

from 30,680 can eventually allow the organization to generate adequate profits from operations.

Modell (2014) argued that without adequate Research and calculation the actual fixed and

variable cost is hard to determine, which can reduce the authenticity of the break-even analysis

conducted for the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS MANAGEMENT TECHNIQUES 25

References and Bibliography:

Abdallah, W., 2016. Accounting, Finance, and Taxation in the Gulf Countries. Springer.

Bebbington, J., Unerman, J. and O’DWYER, B.R.E.N.D.A.N., 2014. Introduction to

sustainability accounting and accountability. In Sustainability accounting and accountability(pp.

21-32). Routledge.

Brief, R.P., 2014. The Continuing Debate Over Depreciation, Capital and Income (RLE

Accounting). Routledge.

Crawford, I. and Wang, Z., 2014. Why are first‐year accounting studies inclusive?. Accounting &

Finance, 54(2), pp.419-439.

De Villiers, C. and Maroun, W. eds., 2017. Sustainability accounting and integrated reporting.

Routledge.

Fourie, M.L., Opperman, L., Scott, D. and Kumar, K., 2015. Municipal finance and accounting.

Van Schaik Publishers.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Harun, H., Van-Peursem, K. and Eggleton, I.R., 2015. Indonesian public sector accounting

reforms: dialogic aspirations a step too far?. Accounting, Auditing & Accountability

Journal, 28(5), pp.706-738.

References and Bibliography:

Abdallah, W., 2016. Accounting, Finance, and Taxation in the Gulf Countries. Springer.

Bebbington, J., Unerman, J. and O’DWYER, B.R.E.N.D.A.N., 2014. Introduction to

sustainability accounting and accountability. In Sustainability accounting and accountability(pp.

21-32). Routledge.

Brief, R.P., 2014. The Continuing Debate Over Depreciation, Capital and Income (RLE

Accounting). Routledge.

Crawford, I. and Wang, Z., 2014. Why are first‐year accounting studies inclusive?. Accounting &

Finance, 54(2), pp.419-439.

De Villiers, C. and Maroun, W. eds., 2017. Sustainability accounting and integrated reporting.

Routledge.

Fourie, M.L., Opperman, L., Scott, D. and Kumar, K., 2015. Municipal finance and accounting.

Van Schaik Publishers.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Harun, H., Van-Peursem, K. and Eggleton, I.R., 2015. Indonesian public sector accounting

reforms: dialogic aspirations a step too far?. Accounting, Auditing & Accountability

Journal, 28(5), pp.706-738.

BUSINESS MANAGEMENT TECHNIQUES 26

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Maskell, B.H., Baggaley, B. and Grasso, L., 2016. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Modell, S., 2014. The societal relevance of management accounting: an introduction to the

special issue. Accounting and Business Research, 44(2), pp.83-103.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Smith, M., 2017. Research methods in accounting. Sage.

Watty, K., Jackling, B. and Wilson, R.M. eds., 2014. Personal transferable skills in Accounting

Education. Routledge.

Wood, D.A., 2016. Comparing the publication process in accounting, economics, finance,

management, marketing, psychology, and the natural sciences. Accounting Horizons, 30(3),

pp.341-361.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4), pp.1187-1230.

Macve, R., 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat?. Routledge.

Maskell, B.H., Baggaley, B. and Grasso, L., 2016. Practical lean accounting: a proven system

for measuring and managing the lean enterprise. Productivity Press.

Modell, S., 2014. The societal relevance of management accounting: an introduction to the

special issue. Accounting and Business Research, 44(2), pp.83-103.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Smith, M., 2017. Research methods in accounting. Sage.

Watty, K., Jackling, B. and Wilson, R.M. eds., 2014. Personal transferable skills in Accounting

Education. Routledge.

Wood, D.A., 2016. Comparing the publication process in accounting, economics, finance,

management, marketing, psychology, and the natural sciences. Accounting Horizons, 30(3),

pp.341-361.

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.