Audit and Assurance Services: Columbia Sportswear Company Report

VerifiedAdded on 2022/08/27

|17

|3196

|19

Report

AI Summary

This report presents a detailed audit plan for Columbia Sportswear Company, outlining the four phases of the audit process: planning and design, substantive tests and tests of controls, substantive analytical procedures and tests of details of balances, and completing the audit and issuing the audit report. The report covers key aspects such as client acceptance, understanding the business, preliminary analytical procedures, setting materiality levels, risk assessment, internal controls, and the finalization of the audit strategy. It discusses substantive tests, control risk reduction, and assessment of misstatements. Furthermore, it includes substantive analytical procedures, tests of details of balances, and procedures for the completion of the audit, including the audit report, and communication with the audit committee and management. The report uses Columbia Sportswear Company's 2018 annual report to provide a practical application of the audit plan.

Running head: AUDIT AND ASSURANCE SERVICES

Auditing and Assurance Services

Name of the Student:

Name of the University:

Authors Note:

Auditing and Assurance Services

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

Contents

Introduction:....................................................................................................................................3

Overview Memo:.............................................................................................................................3

Phase I -Planting and designing phase:...........................................................................................4

Acceptance of client and initial audit planning:..........................................................................4

Understanding the business of the client and the industry in which the client work:.................4

Performing preliminary analytical procedures necessary for the audit:......................................4

Setting the preliminary level of materiality and performing materiality tests for the audit:.......5

Identification of significant risks owing to the possibility of fraud and error:............................7

Assessment of inherent risk:........................................................................................................7

Verification of internal controls and assessing their effectiveness and efficiency:.....................8

Finalization of audit strategy and plan to conduct and efficient and effective audit of financial

statements:...................................................................................................................................8

Phase II –Substantive tests and test of controls:..............................................................................8

Necessary steps to reduce the assessed level of control risk:......................................................8

Performance of substantive test:..................................................................................................9

Assessment of the possibility of misstatements in financial statements:....................................9

Phase III –Substantive analytical procedures and tests of details of balances:.............................10

Substantive analytical procedures:............................................................................................10

Test of key items:.......................................................................................................................11

Contents

Introduction:....................................................................................................................................3

Overview Memo:.............................................................................................................................3

Phase I -Planting and designing phase:...........................................................................................4

Acceptance of client and initial audit planning:..........................................................................4

Understanding the business of the client and the industry in which the client work:.................4

Performing preliminary analytical procedures necessary for the audit:......................................4

Setting the preliminary level of materiality and performing materiality tests for the audit:.......5

Identification of significant risks owing to the possibility of fraud and error:............................7

Assessment of inherent risk:........................................................................................................7

Verification of internal controls and assessing their effectiveness and efficiency:.....................8

Finalization of audit strategy and plan to conduct and efficient and effective audit of financial

statements:...................................................................................................................................8

Phase II –Substantive tests and test of controls:..............................................................................8

Necessary steps to reduce the assessed level of control risk:......................................................8

Performance of substantive test:..................................................................................................9

Assessment of the possibility of misstatements in financial statements:....................................9

Phase III –Substantive analytical procedures and tests of details of balances:.............................10

Substantive analytical procedures:............................................................................................10

Test of key items:.......................................................................................................................11

2

Conducting additional tests of details of balances:....................................................................12

Phase IV –Complete the audit and issue an audit report:..............................................................12

Additional tests necessary for the presentation and disclosure:................................................12

Accumulation of final evidence:................................................................................................12

Evaluation of results:.................................................................................................................12

Issuance of audit report:.............................................................................................................12

Communication with audit committee and management:.........................................................13

Conclusion:....................................................................................................................................13

References:....................................................................................................................................14

Conducting additional tests of details of balances:....................................................................12

Phase IV –Complete the audit and issue an audit report:..............................................................12

Additional tests necessary for the presentation and disclosure:................................................12

Accumulation of final evidence:................................................................................................12

Evaluation of results:.................................................................................................................12

Issuance of audit report:.............................................................................................................12

Communication with audit committee and management:.........................................................13

Conclusion:....................................................................................................................................13

References:....................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Introduction:

Columbia Sportswear Company was founded by Paul Lamfrom in the year 1938 as a sole

proprietorship company. However, it is only as recently as 1998 when the company decided to

go public with its shares by issuing initial public offer (IPO). In the year 2018, the company

completed its 80 years in business. As per the annual report 2018, the company has achieved

ground breaking results and exceeded its own expectations as its share price which was $18 at

the time of IPO has risen to $309 per share as in February, 2019. In fact considering dividend

reinvestment the shareholders who invested in the shares of the company at the time of its IPO

there has been a 2,000 percent on that investment.

Overview Memo:

The objective of this document is to prepare an audit plan for the company to assess whether the

financial statements of the company reflects the true and fair position of the company as on the

date of the financial statements.

An audit is about auditing the financial statements of an organization with the objective of

providing an appropriate opinion on the financial statements of the organization. The audit report

states whether the financial statements of an organization have been prepared in accordance with

the accounting standards applicable for such organization to reflect the true and fair picture of

the organization’s performance and position as on the date of the financial statements. The 2018

annual report of Columbia Sportswear Company contains the financial statements of the

company for the year shall be audited in accordance with the following audit plan to allow the

auditors to give appropriate opinion on the financial statements of the company. Collection of

Introduction:

Columbia Sportswear Company was founded by Paul Lamfrom in the year 1938 as a sole

proprietorship company. However, it is only as recently as 1998 when the company decided to

go public with its shares by issuing initial public offer (IPO). In the year 2018, the company

completed its 80 years in business. As per the annual report 2018, the company has achieved

ground breaking results and exceeded its own expectations as its share price which was $18 at

the time of IPO has risen to $309 per share as in February, 2019. In fact considering dividend

reinvestment the shareholders who invested in the shares of the company at the time of its IPO

there has been a 2,000 percent on that investment.

Overview Memo:

The objective of this document is to prepare an audit plan for the company to assess whether the

financial statements of the company reflects the true and fair position of the company as on the

date of the financial statements.

An audit is about auditing the financial statements of an organization with the objective of

providing an appropriate opinion on the financial statements of the organization. The audit report

states whether the financial statements of an organization have been prepared in accordance with

the accounting standards applicable for such organization to reflect the true and fair picture of

the organization’s performance and position as on the date of the financial statements. The 2018

annual report of Columbia Sportswear Company contains the financial statements of the

company for the year shall be audited in accordance with the following audit plan to allow the

auditors to give appropriate opinion on the financial statements of the company. Collection of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

evidence to support the audit conclusion and opinion of the auditors by conducting an efficient

and effective audit is the prime objective of an audit plan.

An efficient audit must have four different and separate phases with each phase having specific

goals and objectives. An audit must be conducted in accordance with an efficient audit plan to

conduct an efficient and effective audit. A detailed discussion on the four different phases in an

audit in respect to Columbia Sportswear Company is provided below.

Phase I -Planting and designing phase:

Acceptance of client and initial audit planning:

An auditor before accepting an audit must carry out necessary pre-audit operations to decide

whether to accept the audit engagement or not. It is the responsibility of the present auditor to

communicate with the previous auditor of the company as to whether there is any reason for the

former to not accept the audit engagement. The present auditor shall also discuss whether there is

any audit fees due which has not been paid to the previous auditor along with other reasons if

any to not accept the audit engagement (Smith & Stephens, 2020).

On the basis of discussion with the previous auditor and other necessary steps the auditor should

decide whether to accept the audit engagement. In this case there is no reason for not accepting

the audit engagement of Columbia Sportswear Company thus, the auditor should accept the offer

of auditing the financial statements of the company (Sheshukova & Beresneva, 2017).

Understanding the business of the client and the industry in which the client work:

Performing preliminary analytical procedures necessary for the audit:

AS 2101 issued by the Public Company Accounting Oversight Board (PCAOB) on audit

planning provides detailed guidelines for the auditors to plan an efficient audit. In order to

evidence to support the audit conclusion and opinion of the auditors by conducting an efficient

and effective audit is the prime objective of an audit plan.

An efficient audit must have four different and separate phases with each phase having specific

goals and objectives. An audit must be conducted in accordance with an efficient audit plan to

conduct an efficient and effective audit. A detailed discussion on the four different phases in an

audit in respect to Columbia Sportswear Company is provided below.

Phase I -Planting and designing phase:

Acceptance of client and initial audit planning:

An auditor before accepting an audit must carry out necessary pre-audit operations to decide

whether to accept the audit engagement or not. It is the responsibility of the present auditor to

communicate with the previous auditor of the company as to whether there is any reason for the

former to not accept the audit engagement. The present auditor shall also discuss whether there is

any audit fees due which has not been paid to the previous auditor along with other reasons if

any to not accept the audit engagement (Smith & Stephens, 2020).

On the basis of discussion with the previous auditor and other necessary steps the auditor should

decide whether to accept the audit engagement. In this case there is no reason for not accepting

the audit engagement of Columbia Sportswear Company thus, the auditor should accept the offer

of auditing the financial statements of the company (Sheshukova & Beresneva, 2017).

Understanding the business of the client and the industry in which the client work:

Performing preliminary analytical procedures necessary for the audit:

AS 2101 issued by the Public Company Accounting Oversight Board (PCAOB) on audit

planning provides detailed guidelines for the auditors to plan an efficient audit. In order to

5

conduct an audit efficiently the auditor must have necessary knowledge about the business of the

client and the industry to which the client belongs. Columbia Sportswear Company (CSC) is

involved in manufacturing and distribution of sportswear, footwear, headgear, outwear, ski

apparel, camping equipment and other accessories (Kilgore, Radich & Harrison, 2018).

Setting the preliminary level of materiality and performing materiality tests for the audit:

AS 2105 provides extensive guidelines for the auditors to consider materiality in planning and

performing an audit. Generally, the auditor is responsible to set initial preliminary level of

materiality on the basis of his knowledge about the financial transactions of client’s business.

Generally percentages are used to set preliminary materiality level to preform materiality tests

for an audit. In case of audit of CSC each and every account balances shall be checked and

verified along with all transactions in excess of $1000 (Yakimova & Radomskii, 2017). In

addition the items of revenue and expenses which are 1% or higher in respect of overall sales of

the company shall be specifically tested and verified by conducting a throughput tests on such

transactions. Each asset and liabilities shall be verified with appropriate document to assess their

validity and correctness. In order to set the preliminary materiality level for the audit of items of

income and expenditures, the following balances from the income statement of the company

shall be used (Ismajli, Perjuci, Prenaj & Braha, 2019).

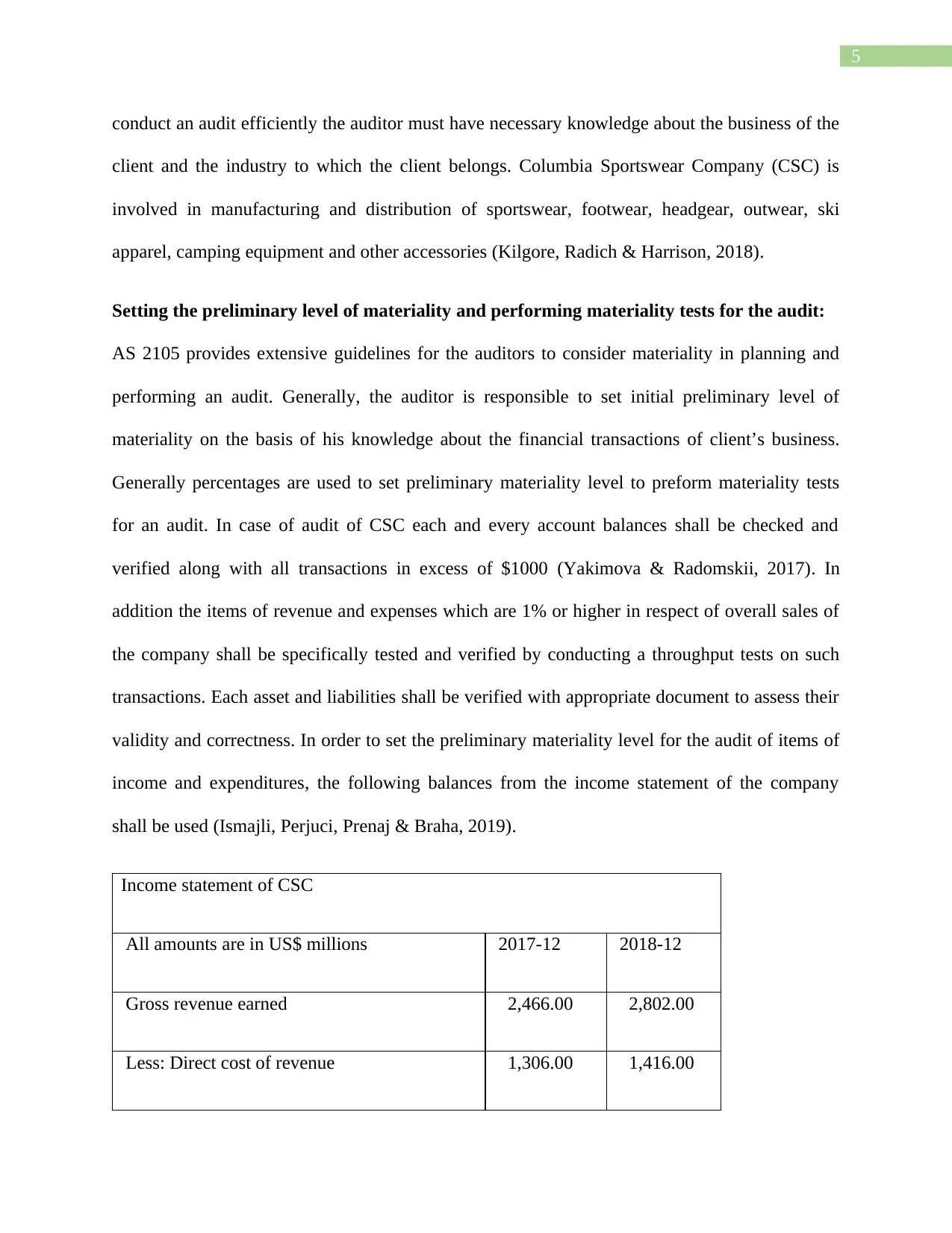

Income statement of CSC

All amounts are in US$ millions 2017-12 2018-12

Gross revenue earned 2,466.00 2,802.00

Less: Direct cost of revenue 1,306.00 1,416.00

conduct an audit efficiently the auditor must have necessary knowledge about the business of the

client and the industry to which the client belongs. Columbia Sportswear Company (CSC) is

involved in manufacturing and distribution of sportswear, footwear, headgear, outwear, ski

apparel, camping equipment and other accessories (Kilgore, Radich & Harrison, 2018).

Setting the preliminary level of materiality and performing materiality tests for the audit:

AS 2105 provides extensive guidelines for the auditors to consider materiality in planning and

performing an audit. Generally, the auditor is responsible to set initial preliminary level of

materiality on the basis of his knowledge about the financial transactions of client’s business.

Generally percentages are used to set preliminary materiality level to preform materiality tests

for an audit. In case of audit of CSC each and every account balances shall be checked and

verified along with all transactions in excess of $1000 (Yakimova & Radomskii, 2017). In

addition the items of revenue and expenses which are 1% or higher in respect of overall sales of

the company shall be specifically tested and verified by conducting a throughput tests on such

transactions. Each asset and liabilities shall be verified with appropriate document to assess their

validity and correctness. In order to set the preliminary materiality level for the audit of items of

income and expenditures, the following balances from the income statement of the company

shall be used (Ismajli, Perjuci, Prenaj & Braha, 2019).

Income statement of CSC

All amounts are in US$ millions 2017-12 2018-12

Gross revenue earned 2,466.00 2,802.00

Less: Direct cost of revenue 1,306.00 1,416.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

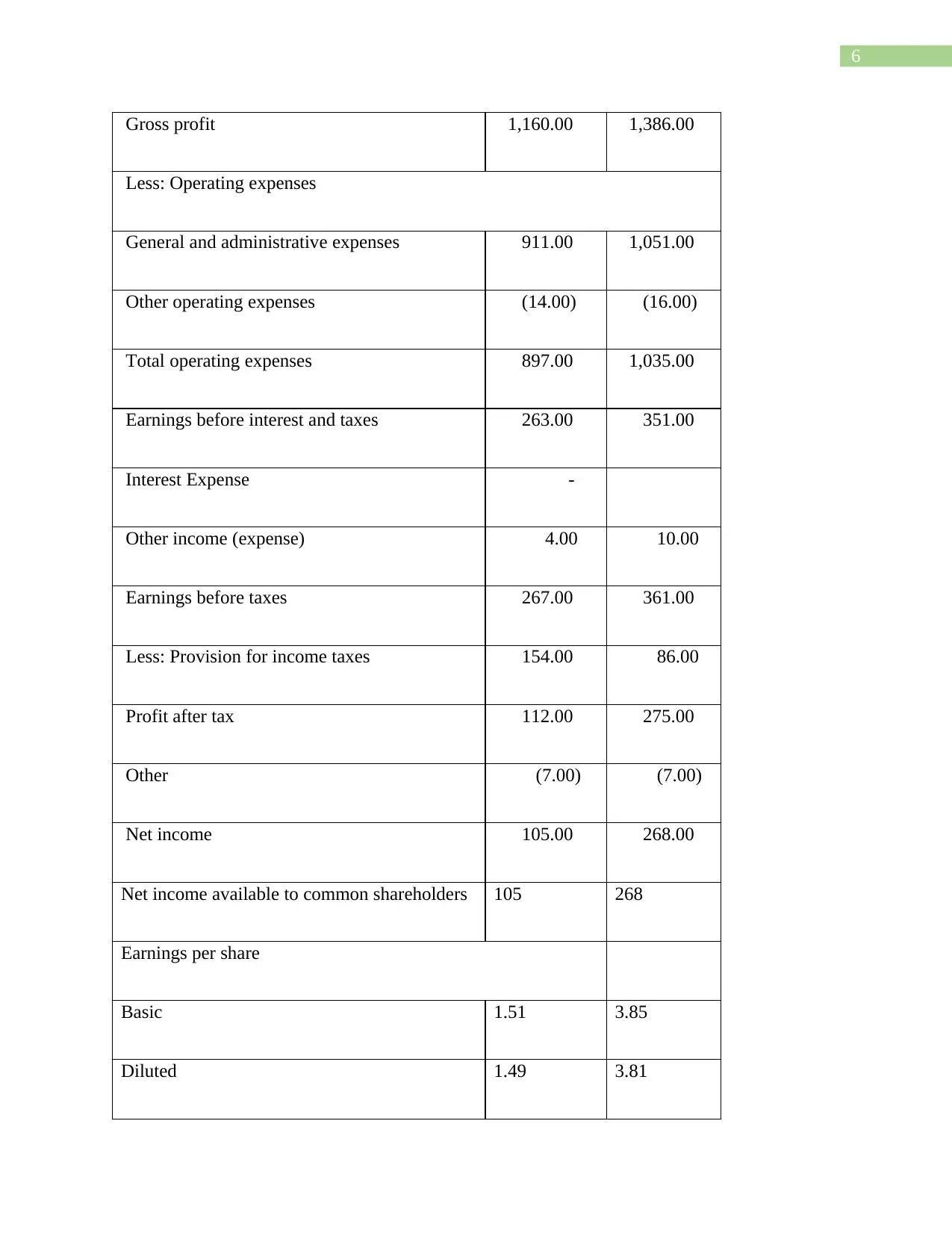

Gross profit 1,160.00 1,386.00

Less: Operating expenses

General and administrative expenses 911.00 1,051.00

Other operating expenses (14.00) (16.00)

Total operating expenses 897.00 1,035.00

Earnings before interest and taxes 263.00 351.00

Interest Expense -

Other income (expense) 4.00 10.00

Earnings before taxes 267.00 361.00

Less: Provision for income taxes 154.00 86.00

Profit after tax 112.00 275.00

Other (7.00) (7.00)

Net income 105.00 268.00

Net income available to common shareholders 105 268

Earnings per share

Basic 1.51 3.85

Diluted 1.49 3.81

Gross profit 1,160.00 1,386.00

Less: Operating expenses

General and administrative expenses 911.00 1,051.00

Other operating expenses (14.00) (16.00)

Total operating expenses 897.00 1,035.00

Earnings before interest and taxes 263.00 351.00

Interest Expense -

Other income (expense) 4.00 10.00

Earnings before taxes 267.00 361.00

Less: Provision for income taxes 154.00 86.00

Profit after tax 112.00 275.00

Other (7.00) (7.00)

Net income 105.00 268.00

Net income available to common shareholders 105 268

Earnings per share

Basic 1.51 3.85

Diluted 1.49 3.81

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Considering that the initial materiality level for items of income and expenditures has been set at

1% of the gross revenue hence, any financial transaction in excess of $28.02 million ($2,802 x

1%) must be checked from its initiation to its recording phase, i.e. such transactions are subjected

to throughput test. In addition each transaction in excess of $1,000 shall be verified and checked

with supporting document to identify whether there is any fraud and error in the financial

statements (Sikka, 2017).

Identification of significant risks owing to the possibility of fraud and error:

The company is involved in manufacturing and distribution of sportswear and other accessories

including headgear, camping equipment and others. Conducting an initial assessment of client’s

business and the industry showed us the risks of constant changes in customer preferences and

tastes when it comes to sportswear and outwear apparel. Thus, the significant risk of obsolete

stock and the possibility of fraud and error in inventory valuation must be specifically verified

and tested by the auditor by using appropriate audit techniques and procedures (HIRST &

KOONCE, 2018).

Assessment of inherent risk:

AS 2110 discusses importance of identification and assessment of risks of material

misstatements in financial statements. Inherent risk is the risk inherent in audit, i.e. irrespective

of audit procedures and effectiveness of those procedures there would be some error in the

financial statements. However, the extent of inherent risk must be low or within the reals and

bounds to carry out the audit efficiently. In this case the inherent audit risk is quite low as the

Considering that the initial materiality level for items of income and expenditures has been set at

1% of the gross revenue hence, any financial transaction in excess of $28.02 million ($2,802 x

1%) must be checked from its initiation to its recording phase, i.e. such transactions are subjected

to throughput test. In addition each transaction in excess of $1,000 shall be verified and checked

with supporting document to identify whether there is any fraud and error in the financial

statements (Sikka, 2017).

Identification of significant risks owing to the possibility of fraud and error:

The company is involved in manufacturing and distribution of sportswear and other accessories

including headgear, camping equipment and others. Conducting an initial assessment of client’s

business and the industry showed us the risks of constant changes in customer preferences and

tastes when it comes to sportswear and outwear apparel. Thus, the significant risk of obsolete

stock and the possibility of fraud and error in inventory valuation must be specifically verified

and tested by the auditor by using appropriate audit techniques and procedures (HIRST &

KOONCE, 2018).

Assessment of inherent risk:

AS 2110 discusses importance of identification and assessment of risks of material

misstatements in financial statements. Inherent risk is the risk inherent in audit, i.e. irrespective

of audit procedures and effectiveness of those procedures there would be some error in the

financial statements. However, the extent of inherent risk must be low or within the reals and

bounds to carry out the audit efficiently. In this case the inherent audit risk is quite low as the

8

auditor has decided to use extensive analytical and substantive tests to conduct the audit

efficiently.

Verification of internal controls and assessing their effectiveness and efficiency:

The company has standard internal controls in place which have been in operation throughout the

previous financial year and earlier hence, the auditor can rely on these internal controls while

carrying out necessary audit procedures to conduct the audit of the company. The internal control

in respect of stock taking of the company is however not up to the scratch hence, extensive audit

procedures shall be used by auditors in respect of inventory valuation including physical

verification of inventories while carrying out the audit (HIRST & KOONCE, 2018).

Finalization of audit strategy and plan to conduct and efficient and effective audit of

financial statements:

Apart from vouching which includes verification of each voucher along with supporting

document to justify the payments and received the auditor will conduct detailed analytical test on

the account balances and various items of financial statements to identify abnormal fluctuations

in different account balances and transactions to determine the extent of substantive procedures

necessary for the auditing of various accounts balances, class of transactions and items within the

financial statements of the company (Ismajli, Perjuci, Prenaj & Braha, 2019).

Phase II –Substantive tests and test of controls:

Necessary steps to reduce the assessed level of control risk:

As already discussed that apart from the stocking taking and inventory valuation of the company,

there is no major control risk in the audit of the company. However, despite that the auditor has

auditor has decided to use extensive analytical and substantive tests to conduct the audit

efficiently.

Verification of internal controls and assessing their effectiveness and efficiency:

The company has standard internal controls in place which have been in operation throughout the

previous financial year and earlier hence, the auditor can rely on these internal controls while

carrying out necessary audit procedures to conduct the audit of the company. The internal control

in respect of stock taking of the company is however not up to the scratch hence, extensive audit

procedures shall be used by auditors in respect of inventory valuation including physical

verification of inventories while carrying out the audit (HIRST & KOONCE, 2018).

Finalization of audit strategy and plan to conduct and efficient and effective audit of

financial statements:

Apart from vouching which includes verification of each voucher along with supporting

document to justify the payments and received the auditor will conduct detailed analytical test on

the account balances and various items of financial statements to identify abnormal fluctuations

in different account balances and transactions to determine the extent of substantive procedures

necessary for the auditing of various accounts balances, class of transactions and items within the

financial statements of the company (Ismajli, Perjuci, Prenaj & Braha, 2019).

Phase II –Substantive tests and test of controls:

Necessary steps to reduce the assessed level of control risk:

As already discussed that apart from the stocking taking and inventory valuation of the company,

there is no major control risk in the audit of the company. However, despite that the auditor has

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

decided to conduct physical verification of assets including inventory of the company and cash

balances. Apart from that the following steps shall be taken to reduce the overall control risks.

I. Verification of each internal control.

II. Effectiveness of the internal controls verification.

III. Assessment of whether these controls have been in place throughout the year.

IV. Verification of accounting system and software used within the company.

V. Carrying out sample transactions in the accounting system and software to understand

how the system works.

Performance of substantive test:

Financial transactions and account balances of the company in accordance with the pre-

determined materiality level shall be verified along with supporting documents against these

transactions and account balances. The supporting documents along with vouchers must be

verified to check whither these have been recorded correctly or not (Hellman, 2019).

Assessment of the possibility of misstatements in financial statements:

The auditor must verify whether the applicable accounting standards have been followed or not

in preparation and presentation of the financial statements of the company. The company has

prepared a complete set of financial statements including income statement, financial position

statement, cash flow statements, statements of changes in equity and notes to accounts. The

annual report of the company clearly states that the company has complied with the applicable

accounting standards to prepare and present its financial statements. The verification of accounts

balances and financial transactions along with the accounting records show that the company has

decided to conduct physical verification of assets including inventory of the company and cash

balances. Apart from that the following steps shall be taken to reduce the overall control risks.

I. Verification of each internal control.

II. Effectiveness of the internal controls verification.

III. Assessment of whether these controls have been in place throughout the year.

IV. Verification of accounting system and software used within the company.

V. Carrying out sample transactions in the accounting system and software to understand

how the system works.

Performance of substantive test:

Financial transactions and account balances of the company in accordance with the pre-

determined materiality level shall be verified along with supporting documents against these

transactions and account balances. The supporting documents along with vouchers must be

verified to check whither these have been recorded correctly or not (Hellman, 2019).

Assessment of the possibility of misstatements in financial statements:

The auditor must verify whether the applicable accounting standards have been followed or not

in preparation and presentation of the financial statements of the company. The company has

prepared a complete set of financial statements including income statement, financial position

statement, cash flow statements, statements of changes in equity and notes to accounts. The

annual report of the company clearly states that the company has complied with the applicable

accounting standards to prepare and present its financial statements. The verification of accounts

balances and financial transactions along with the accounting records show that the company has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

followed the accounting standards properly in preparation and presentation of financial

statements of the company (Heintz, White & Bedard, 2016).

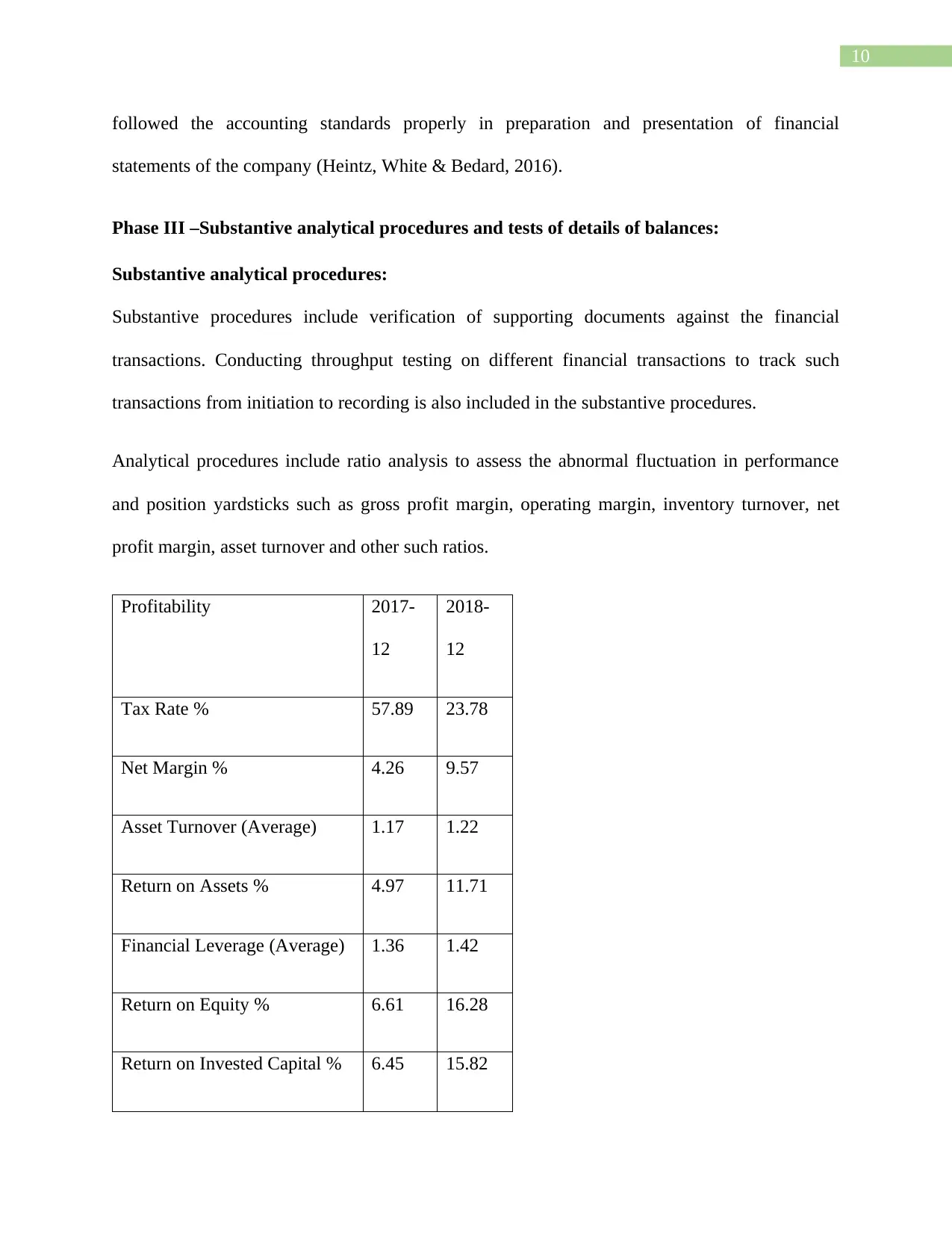

Phase III –Substantive analytical procedures and tests of details of balances:

Substantive analytical procedures:

Substantive procedures include verification of supporting documents against the financial

transactions. Conducting throughput testing on different financial transactions to track such

transactions from initiation to recording is also included in the substantive procedures.

Analytical procedures include ratio analysis to assess the abnormal fluctuation in performance

and position yardsticks such as gross profit margin, operating margin, inventory turnover, net

profit margin, asset turnover and other such ratios.

Profitability 2017-

12

2018-

12

Tax Rate % 57.89 23.78

Net Margin % 4.26 9.57

Asset Turnover (Average) 1.17 1.22

Return on Assets % 4.97 11.71

Financial Leverage (Average) 1.36 1.42

Return on Equity % 6.61 16.28

Return on Invested Capital % 6.45 15.82

followed the accounting standards properly in preparation and presentation of financial

statements of the company (Heintz, White & Bedard, 2016).

Phase III –Substantive analytical procedures and tests of details of balances:

Substantive analytical procedures:

Substantive procedures include verification of supporting documents against the financial

transactions. Conducting throughput testing on different financial transactions to track such

transactions from initiation to recording is also included in the substantive procedures.

Analytical procedures include ratio analysis to assess the abnormal fluctuation in performance

and position yardsticks such as gross profit margin, operating margin, inventory turnover, net

profit margin, asset turnover and other such ratios.

Profitability 2017-

12

2018-

12

Tax Rate % 57.89 23.78

Net Margin % 4.26 9.57

Asset Turnover (Average) 1.17 1.22

Return on Assets % 4.97 11.71

Financial Leverage (Average) 1.36 1.42

Return on Equity % 6.61 16.28

Return on Invested Capital % 6.45 15.82

11

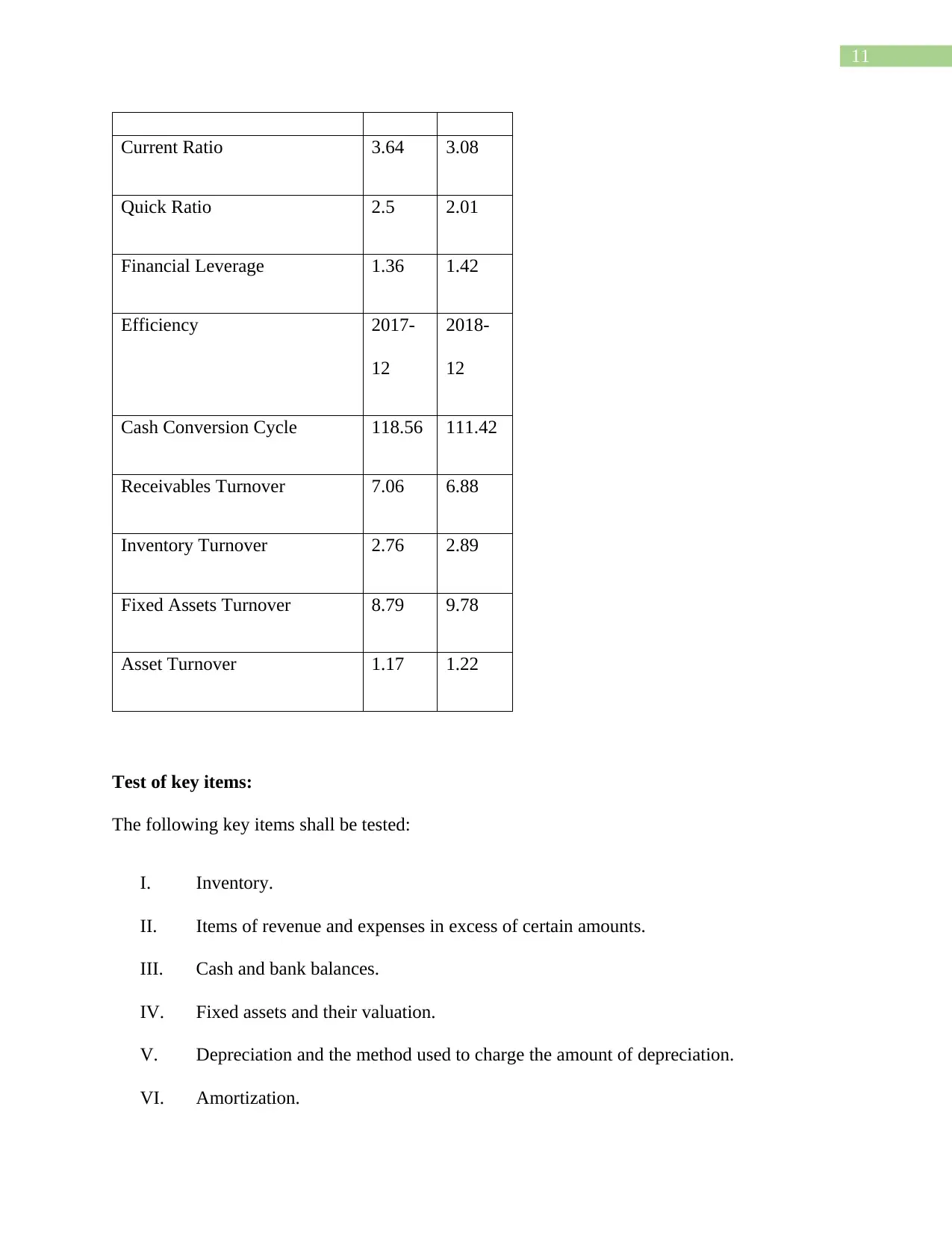

Current Ratio 3.64 3.08

Quick Ratio 2.5 2.01

Financial Leverage 1.36 1.42

Efficiency 2017-

12

2018-

12

Cash Conversion Cycle 118.56 111.42

Receivables Turnover 7.06 6.88

Inventory Turnover 2.76 2.89

Fixed Assets Turnover 8.79 9.78

Asset Turnover 1.17 1.22

Test of key items:

The following key items shall be tested:

I. Inventory.

II. Items of revenue and expenses in excess of certain amounts.

III. Cash and bank balances.

IV. Fixed assets and their valuation.

V. Depreciation and the method used to charge the amount of depreciation.

VI. Amortization.

Current Ratio 3.64 3.08

Quick Ratio 2.5 2.01

Financial Leverage 1.36 1.42

Efficiency 2017-

12

2018-

12

Cash Conversion Cycle 118.56 111.42

Receivables Turnover 7.06 6.88

Inventory Turnover 2.76 2.89

Fixed Assets Turnover 8.79 9.78

Asset Turnover 1.17 1.22

Test of key items:

The following key items shall be tested:

I. Inventory.

II. Items of revenue and expenses in excess of certain amounts.

III. Cash and bank balances.

IV. Fixed assets and their valuation.

V. Depreciation and the method used to charge the amount of depreciation.

VI. Amortization.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.