Performance, Liquidity and Financial Structure of Tesco Plc

Analyse and evaluate the performance, liquidity and financial structure of Tesco plc over the three-year period 2015 – 2018 using accounting ratios and other relevant information.

11 Pages2220 Words441 Views

Added on 2022-10-17

About This Document

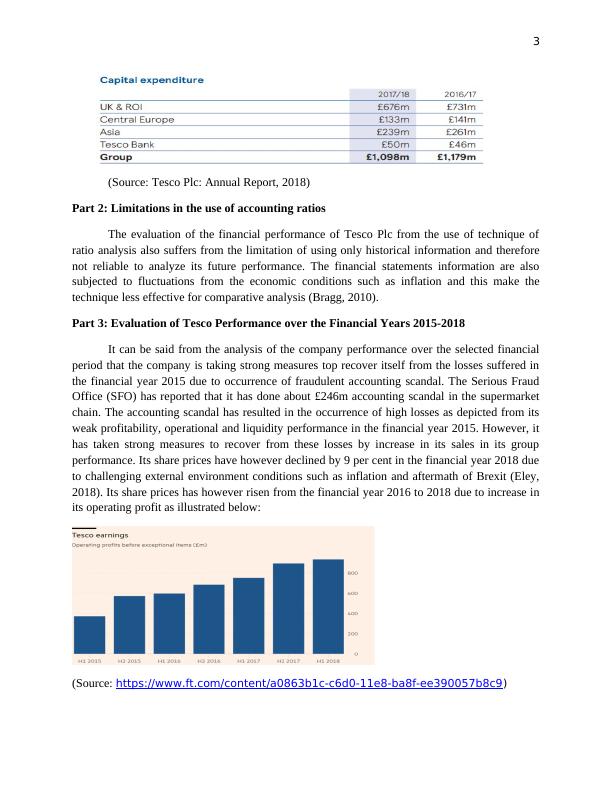

3 BA 4008 Business Decision Making Coursework Task One Part 1: Analysis and Evaluation of the Performance, Liquidity and Financial Structure of Tesco over the Financial Period 2015-2018 Profitability Analysis Tesco Plc has largely improved its profitability position as evident from increasing trend of the ratios such as return on shareholder funds with increase in its statutory profit from 2015-2018 enabling it to pay larger dividends for the shareholders (Tesco PLC: Understanding Tesco, 2018). The company has also depicted a decrease in the capital expenditure in the financial year

Performance, Liquidity and Financial Structure of Tesco Plc

Analyse and evaluate the performance, liquidity and financial structure of Tesco plc over the three-year period 2015 – 2018 using accounting ratios and other relevant information.

Added on 2022-10-17

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

Report on Accounting & Financial Management

|7

|1525

|84

Financial Performance Analysis of Royal Mail Plc : Report

|19

|5462

|61

Accounting Coursework Assignment - Tesco Plc and LMU Plc

|12

|1884

|318

Business Decision Making: Analysis of Tesco's Accounting Ratios, Limitations, and Factors Affecting Performance in 2019

|8

|2050

|90

Financial Analysis of BHP Billiton

|10

|2401

|337

Financial Accounting Ratios and Annual Reports: A Case Study of Tesco PLC

|7

|1853

|437