Corporate Accounting: Analysis of Consolidated Financial Statements

VerifiedAdded on 2023/04/23

|10

|1435

|458

Report

AI Summary

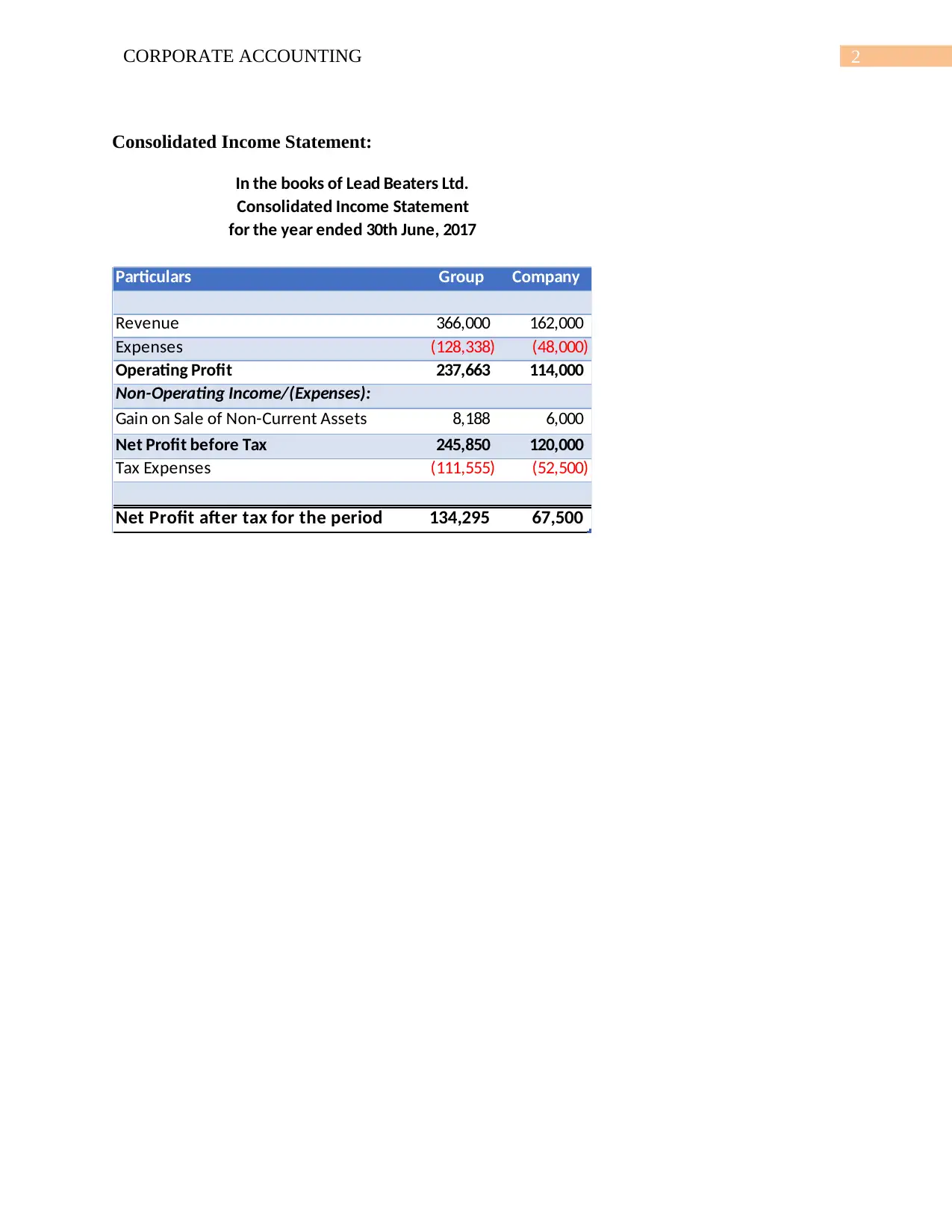

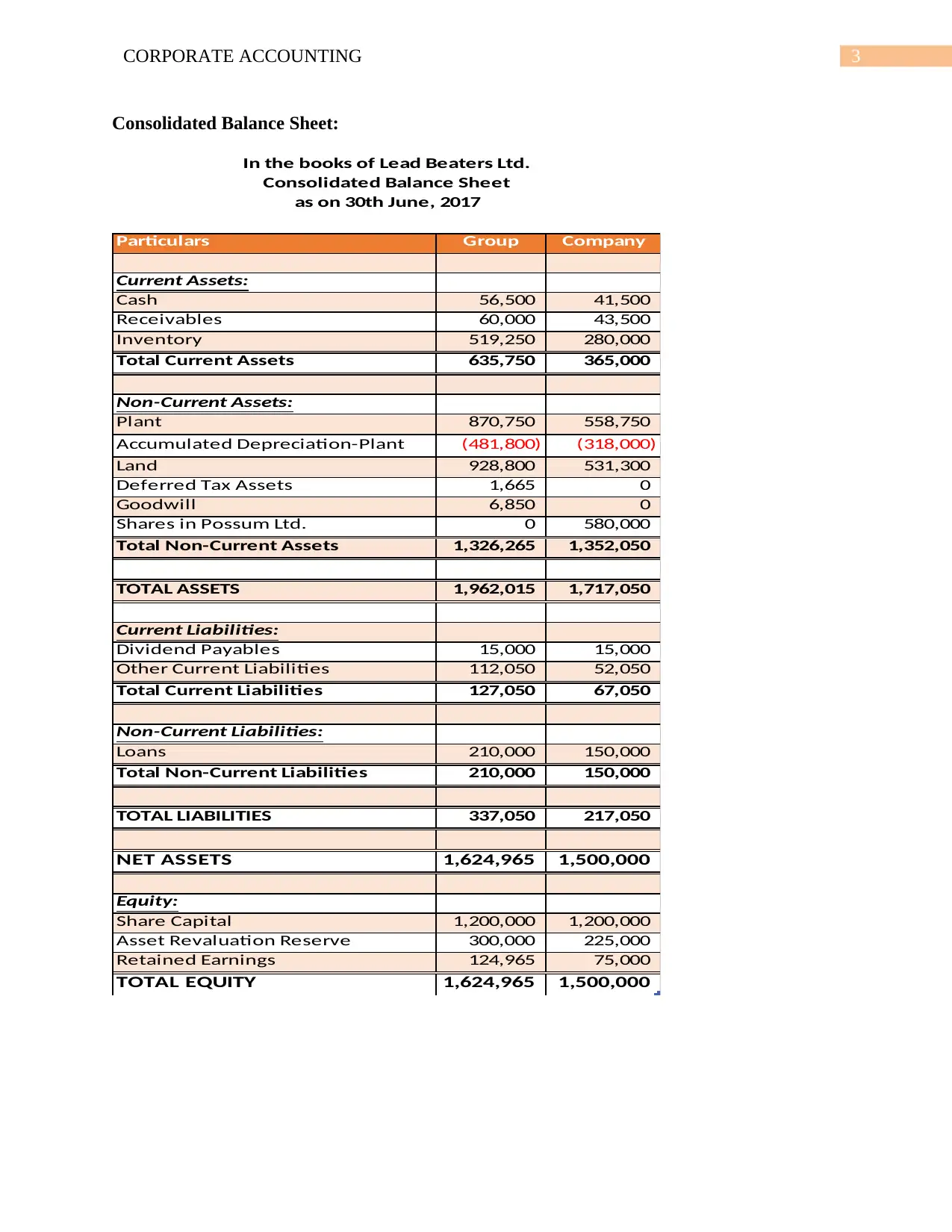

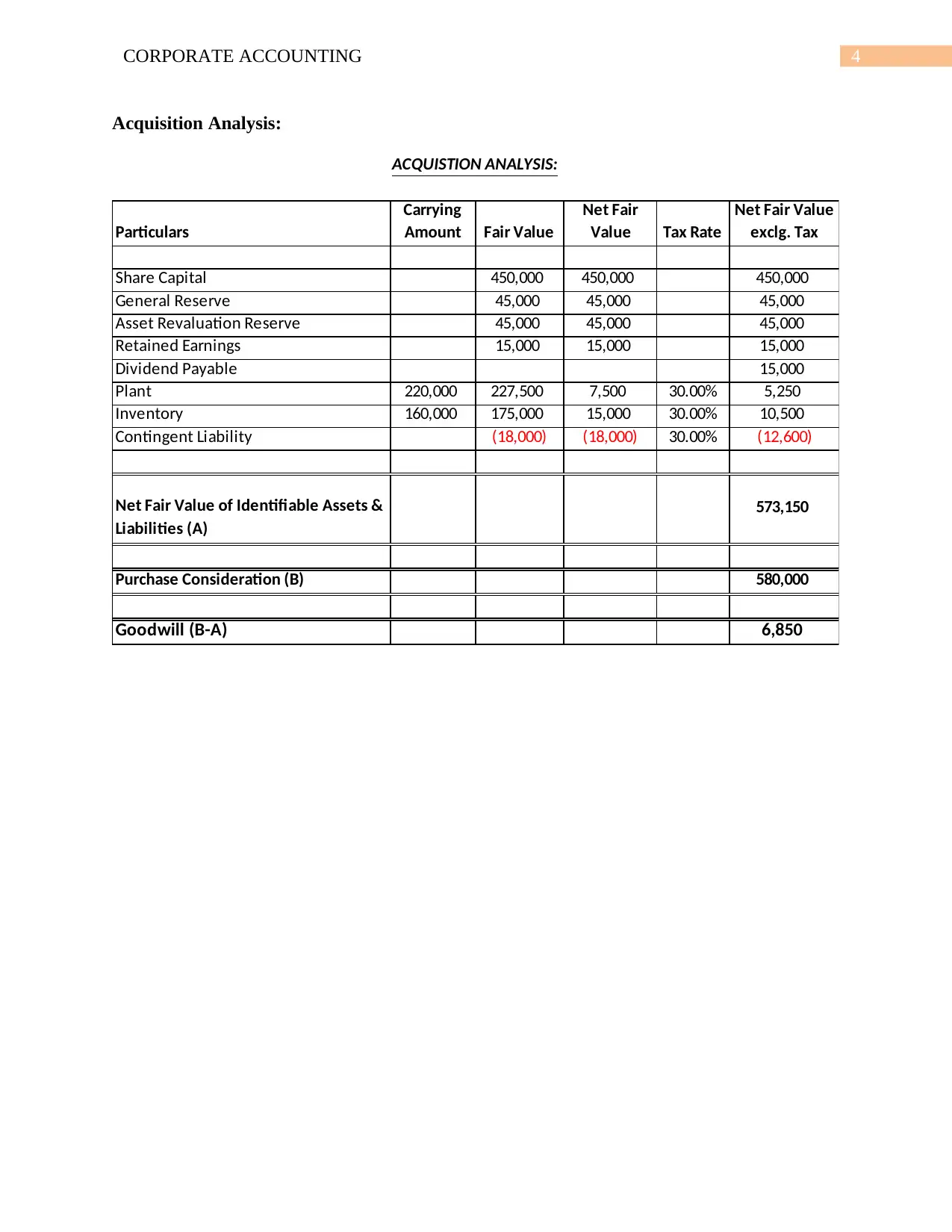

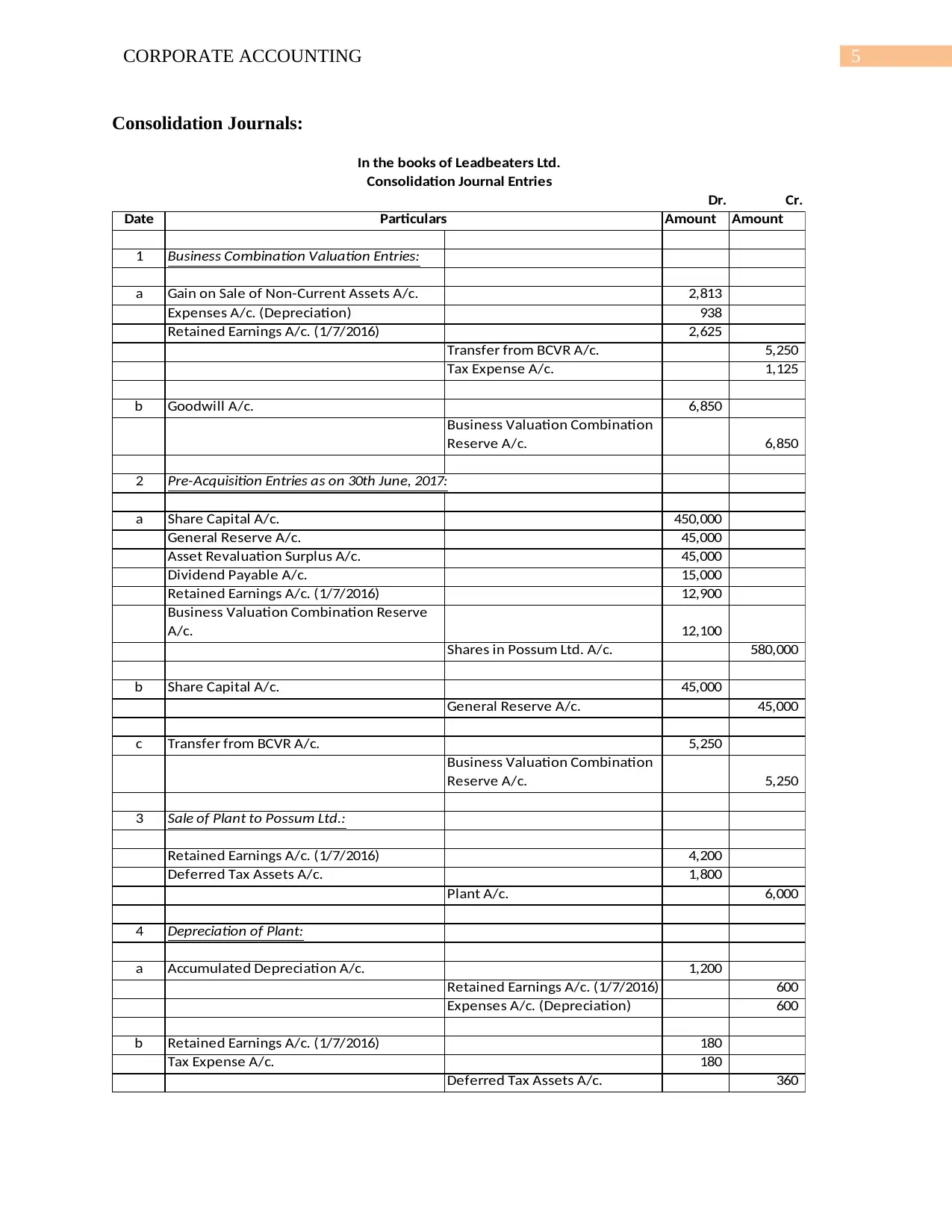

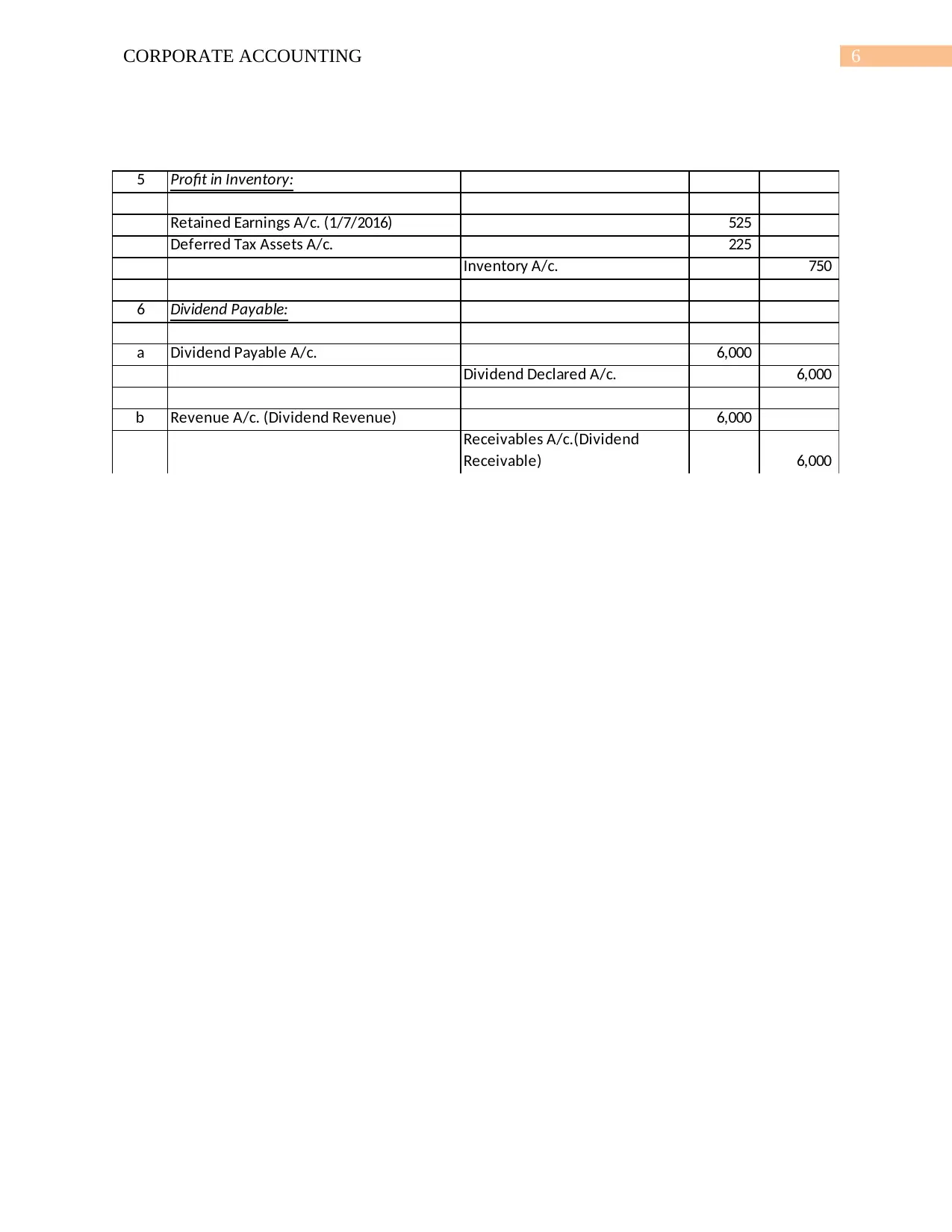

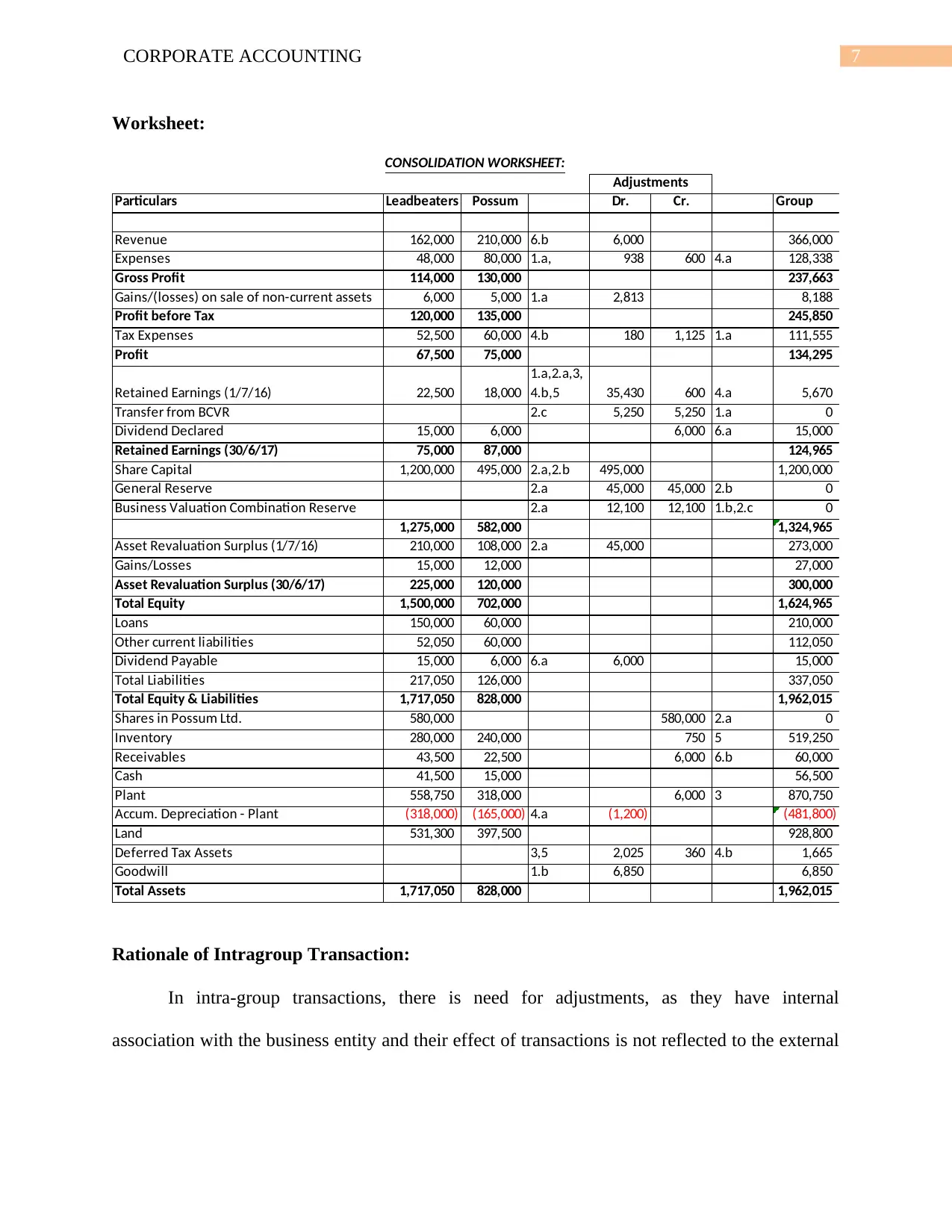

This report presents a detailed analysis of corporate accounting practices, focusing on the consolidated financial statements of Lead Beaters Ltd. The report includes a consolidated income statement and balance sheet, along with an acquisition analysis of Possum Ltd., which Lead Beaters Ltd. acquired. It provides a thorough examination of consolidation journals, a comprehensive consolidation worksheet, and a rationale for intragroup transactions. The analysis covers adjustments for inventory, income tax expenses, and retained earnings, ensuring a clear understanding of the financial reporting process. The report offers insights into the financial performance of Lead Beaters Ltd. and its subsidiary, Possum Ltd., providing a complete overview of the consolidation process and the impact of various accounting treatments. References and bibliography are included to support the analysis.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.