Financial Analysis of Vodafone Group and Deutsche Telekom (2017)

VerifiedAdded on 2022/11/25

|15

|3228

|66

Report

AI Summary

This report presents a comprehensive financial analysis of Vodafone Group's performance in 2017, employing ratio analysis to evaluate its financial health. The analysis encompasses profitability, liquidity, efficiency, and solvency, providing a detailed assessment of Vodafone's financial position. Furthermore, the report includes a comparative analysis with Deutsche Telekom, Vodafone's competitor, to benchmark its performance. Key financial ratios such as Return on Capital Employed (ROCE), Return on Sales, Gross Profit Margin, Return on Equity, Current Ratio, Quick Ratio, Asset Utilization Ratio, Gearing Ratio, and Interest Coverage Ratio are calculated and interpreted. The report identifies Vodafone's strengths and weaknesses, highlighting areas where it lags behind its competitor and suggesting potential improvements for future growth. The findings reveal that Vodafone's profitability ratios, such as Return on Sales and Return on Equity, are negative, while its liquidity ratios are relatively stable. The efficiency ratios indicate lower asset utilization compared to Deutsche Telekom. The report concludes with an overall assessment of Vodafone's financial performance and provides recommendations for enhancing its financial strategies.

1

Financial Analysis of Vodafone Group

Financial Analysis of Vodafone Group

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Introduction......................................................................................................................................3

Task 1: Finding financial information and Calculation of ratios.....................................................3

Task 2: Financial Performance Analysis of Vodafone as Compared to Deutsche Telekom with

the use of Ratio Analysis.................................................................................................................6

Profitability Analysis.......................................................................................................................6

Return on Capital Employed (ROCE).........................................................................................7

Return on Sales............................................................................................................................8

Gross Profit Margin.....................................................................................................................8

Return on Equity..........................................................................................................................8

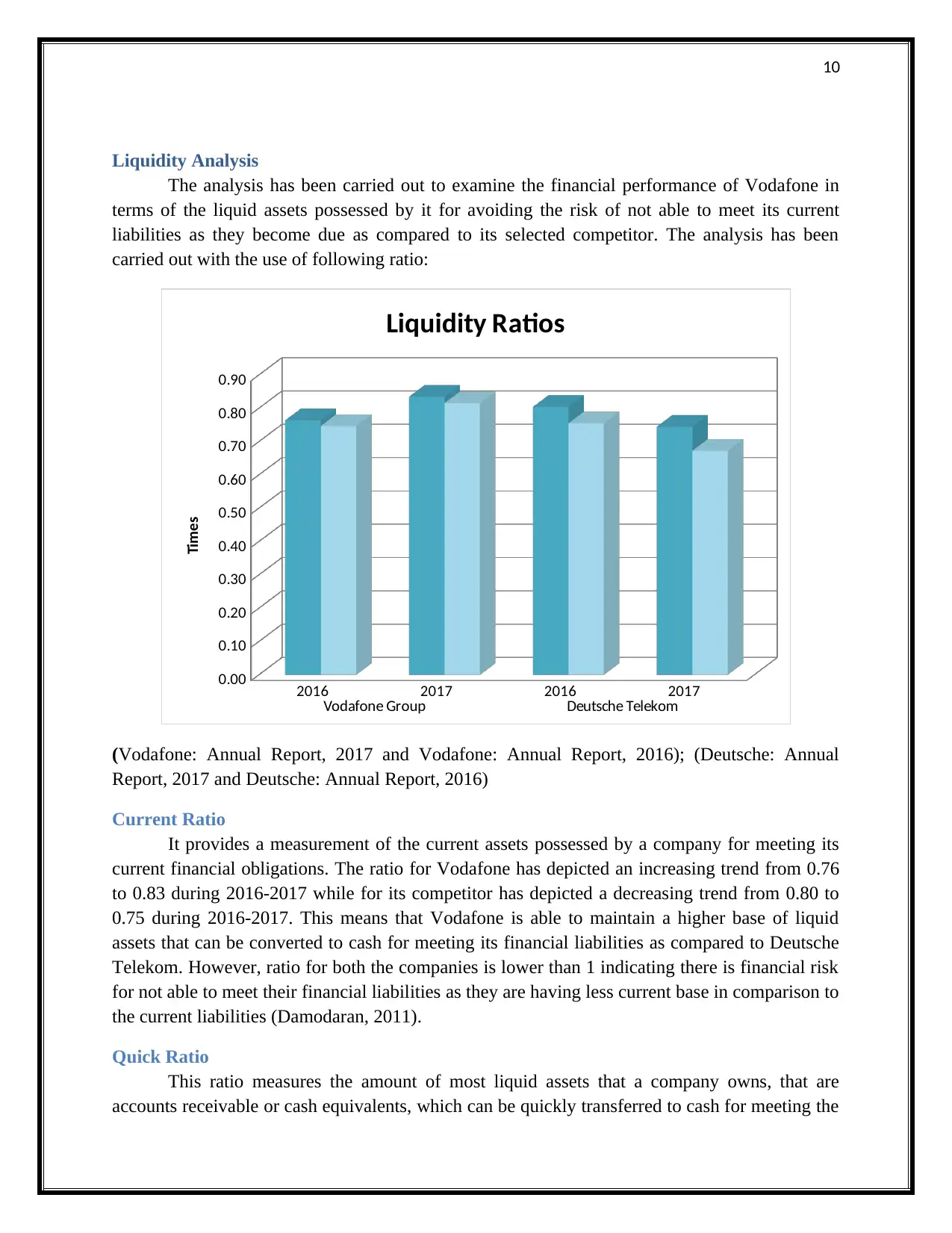

Liquidity Analysis...........................................................................................................................9

Current Ratio................................................................................................................................9

Quick Ratio..................................................................................................................................9

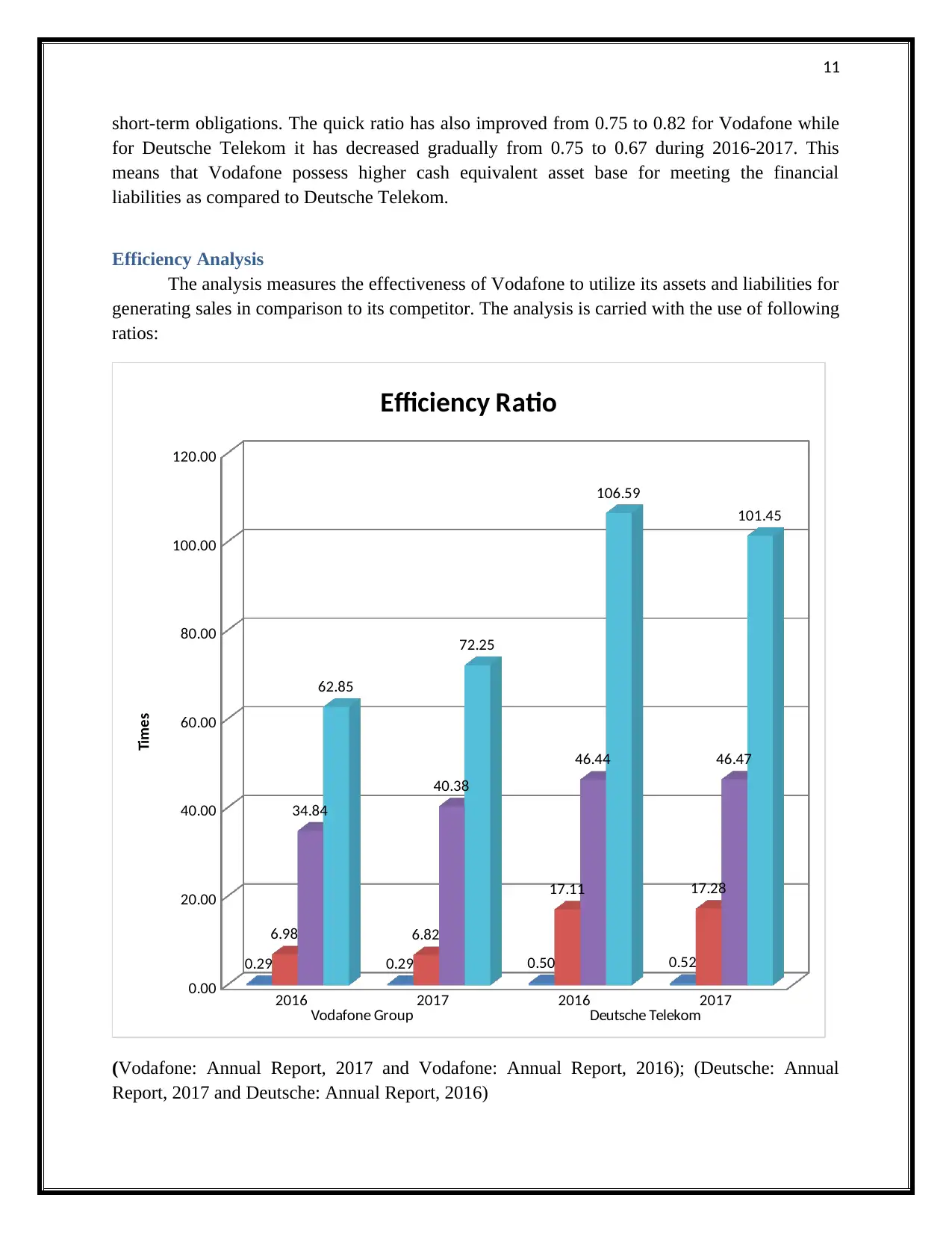

Efficiency Analysis........................................................................................................................10

Asset Utilization Ratio...............................................................................................................11

Stock Days.................................................................................................................................11

Current trade receivable days.....................................................................................................11

Current trade payable days.........................................................................................................11

Solvency Analysis.........................................................................................................................12

Gearing Ratio.............................................................................................................................12

Interest Coverage ratio...............................................................................................................12

Overall Assessment of Vodafone Financial Performance as Compared to Deutsche Telecom....13

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

Contents

Introduction......................................................................................................................................3

Task 1: Finding financial information and Calculation of ratios.....................................................3

Task 2: Financial Performance Analysis of Vodafone as Compared to Deutsche Telekom with

the use of Ratio Analysis.................................................................................................................6

Profitability Analysis.......................................................................................................................6

Return on Capital Employed (ROCE).........................................................................................7

Return on Sales............................................................................................................................8

Gross Profit Margin.....................................................................................................................8

Return on Equity..........................................................................................................................8

Liquidity Analysis...........................................................................................................................9

Current Ratio................................................................................................................................9

Quick Ratio..................................................................................................................................9

Efficiency Analysis........................................................................................................................10

Asset Utilization Ratio...............................................................................................................11

Stock Days.................................................................................................................................11

Current trade receivable days.....................................................................................................11

Current trade payable days.........................................................................................................11

Solvency Analysis.........................................................................................................................12

Gearing Ratio.............................................................................................................................12

Interest Coverage ratio...............................................................................................................12

Overall Assessment of Vodafone Financial Performance as Compared to Deutsche Telecom....13

Conclusion.....................................................................................................................................13

References......................................................................................................................................14

3

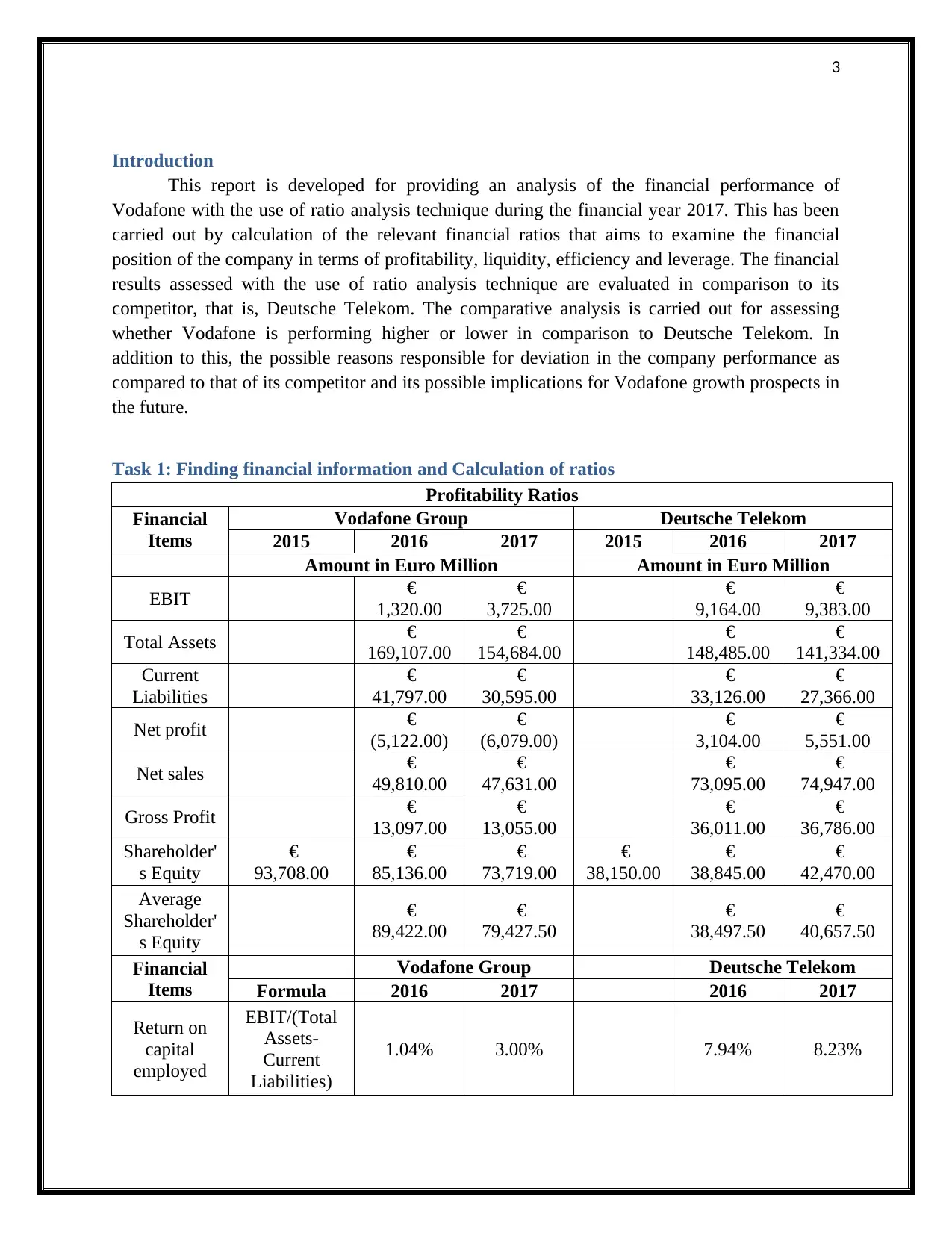

Introduction

This report is developed for providing an analysis of the financial performance of

Vodafone with the use of ratio analysis technique during the financial year 2017. This has been

carried out by calculation of the relevant financial ratios that aims to examine the financial

position of the company in terms of profitability, liquidity, efficiency and leverage. The financial

results assessed with the use of ratio analysis technique are evaluated in comparison to its

competitor, that is, Deutsche Telekom. The comparative analysis is carried out for assessing

whether Vodafone is performing higher or lower in comparison to Deutsche Telekom. In

addition to this, the possible reasons responsible for deviation in the company performance as

compared to that of its competitor and its possible implications for Vodafone growth prospects in

the future.

Task 1: Finding financial information and Calculation of ratios

Profitability Ratios

Financial

Items

Vodafone Group Deutsche Telekom

2015 2016 2017 2015 2016 2017

Amount in Euro Million Amount in Euro Million

EBIT €

1,320.00

€

3,725.00

€

9,164.00

€

9,383.00

Total Assets €

169,107.00

€

154,684.00

€

148,485.00

€

141,334.00

Current

Liabilities

€

41,797.00

€

30,595.00

€

33,126.00

€

27,366.00

Net profit €

(5,122.00)

€

(6,079.00)

€

3,104.00

€

5,551.00

Net sales €

49,810.00

€

47,631.00

€

73,095.00

€

74,947.00

Gross Profit €

13,097.00

€

13,055.00

€

36,011.00

€

36,786.00

Shareholder'

s Equity

€

93,708.00

€

85,136.00

€

73,719.00

€

38,150.00

€

38,845.00

€

42,470.00

Average

Shareholder'

s Equity

€

89,422.00

€

79,427.50

€

38,497.50

€

40,657.50

Financial

Items

Vodafone Group Deutsche Telekom

Formula 2016 2017 2016 2017

Return on

capital

employed

EBIT/(Total

Assets-

Current

Liabilities)

1.04% 3.00% 7.94% 8.23%

Introduction

This report is developed for providing an analysis of the financial performance of

Vodafone with the use of ratio analysis technique during the financial year 2017. This has been

carried out by calculation of the relevant financial ratios that aims to examine the financial

position of the company in terms of profitability, liquidity, efficiency and leverage. The financial

results assessed with the use of ratio analysis technique are evaluated in comparison to its

competitor, that is, Deutsche Telekom. The comparative analysis is carried out for assessing

whether Vodafone is performing higher or lower in comparison to Deutsche Telekom. In

addition to this, the possible reasons responsible for deviation in the company performance as

compared to that of its competitor and its possible implications for Vodafone growth prospects in

the future.

Task 1: Finding financial information and Calculation of ratios

Profitability Ratios

Financial

Items

Vodafone Group Deutsche Telekom

2015 2016 2017 2015 2016 2017

Amount in Euro Million Amount in Euro Million

EBIT €

1,320.00

€

3,725.00

€

9,164.00

€

9,383.00

Total Assets €

169,107.00

€

154,684.00

€

148,485.00

€

141,334.00

Current

Liabilities

€

41,797.00

€

30,595.00

€

33,126.00

€

27,366.00

Net profit €

(5,122.00)

€

(6,079.00)

€

3,104.00

€

5,551.00

Net sales €

49,810.00

€

47,631.00

€

73,095.00

€

74,947.00

Gross Profit €

13,097.00

€

13,055.00

€

36,011.00

€

36,786.00

Shareholder'

s Equity

€

93,708.00

€

85,136.00

€

73,719.00

€

38,150.00

€

38,845.00

€

42,470.00

Average

Shareholder'

s Equity

€

89,422.00

€

79,427.50

€

38,497.50

€

40,657.50

Financial

Items

Vodafone Group Deutsche Telekom

Formula 2016 2017 2016 2017

Return on

capital

employed

EBIT/(Total

Assets-

Current

Liabilities)

1.04% 3.00% 7.94% 8.23%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

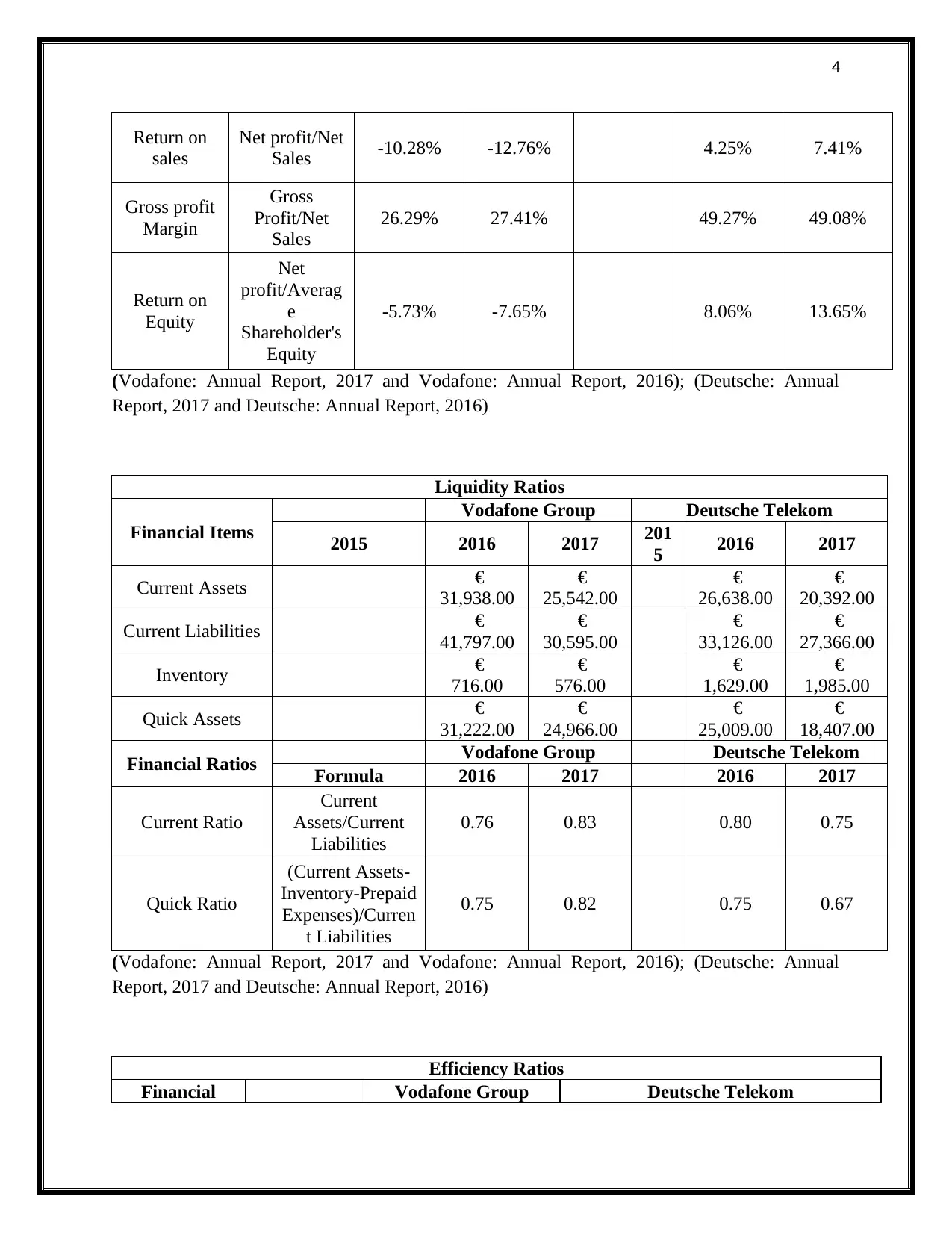

Return on

sales

Net profit/Net

Sales -10.28% -12.76% 4.25% 7.41%

Gross profit

Margin

Gross

Profit/Net

Sales

26.29% 27.41% 49.27% 49.08%

Return on

Equity

Net

profit/Averag

e

Shareholder's

Equity

-5.73% -7.65% 8.06% 13.65%

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Liquidity Ratios

Financial Items

Vodafone Group Deutsche Telekom

2015 2016 2017 201

5 2016 2017

Current Assets €

31,938.00

€

25,542.00

€

26,638.00

€

20,392.00

Current Liabilities €

41,797.00

€

30,595.00

€

33,126.00

€

27,366.00

Inventory €

716.00

€

576.00

€

1,629.00

€

1,985.00

Quick Assets €

31,222.00

€

24,966.00

€

25,009.00

€

18,407.00

Financial Ratios Vodafone Group Deutsche Telekom

Formula 2016 2017 2016 2017

Current Ratio

Current

Assets/Current

Liabilities

0.76 0.83 0.80 0.75

Quick Ratio

(Current Assets-

Inventory-Prepaid

Expenses)/Curren

t Liabilities

0.75 0.82 0.75 0.67

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Efficiency Ratios

Financial Vodafone Group Deutsche Telekom

Return on

sales

Net profit/Net

Sales -10.28% -12.76% 4.25% 7.41%

Gross profit

Margin

Gross

Profit/Net

Sales

26.29% 27.41% 49.27% 49.08%

Return on

Equity

Net

profit/Averag

e

Shareholder's

Equity

-5.73% -7.65% 8.06% 13.65%

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Liquidity Ratios

Financial Items

Vodafone Group Deutsche Telekom

2015 2016 2017 201

5 2016 2017

Current Assets €

31,938.00

€

25,542.00

€

26,638.00

€

20,392.00

Current Liabilities €

41,797.00

€

30,595.00

€

33,126.00

€

27,366.00

Inventory €

716.00

€

576.00

€

1,629.00

€

1,985.00

Quick Assets €

31,222.00

€

24,966.00

€

25,009.00

€

18,407.00

Financial Ratios Vodafone Group Deutsche Telekom

Formula 2016 2017 2016 2017

Current Ratio

Current

Assets/Current

Liabilities

0.76 0.83 0.80 0.75

Quick Ratio

(Current Assets-

Inventory-Prepaid

Expenses)/Curren

t Liabilities

0.75 0.82 0.75 0.67

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Efficiency Ratios

Financial Vodafone Group Deutsche Telekom

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

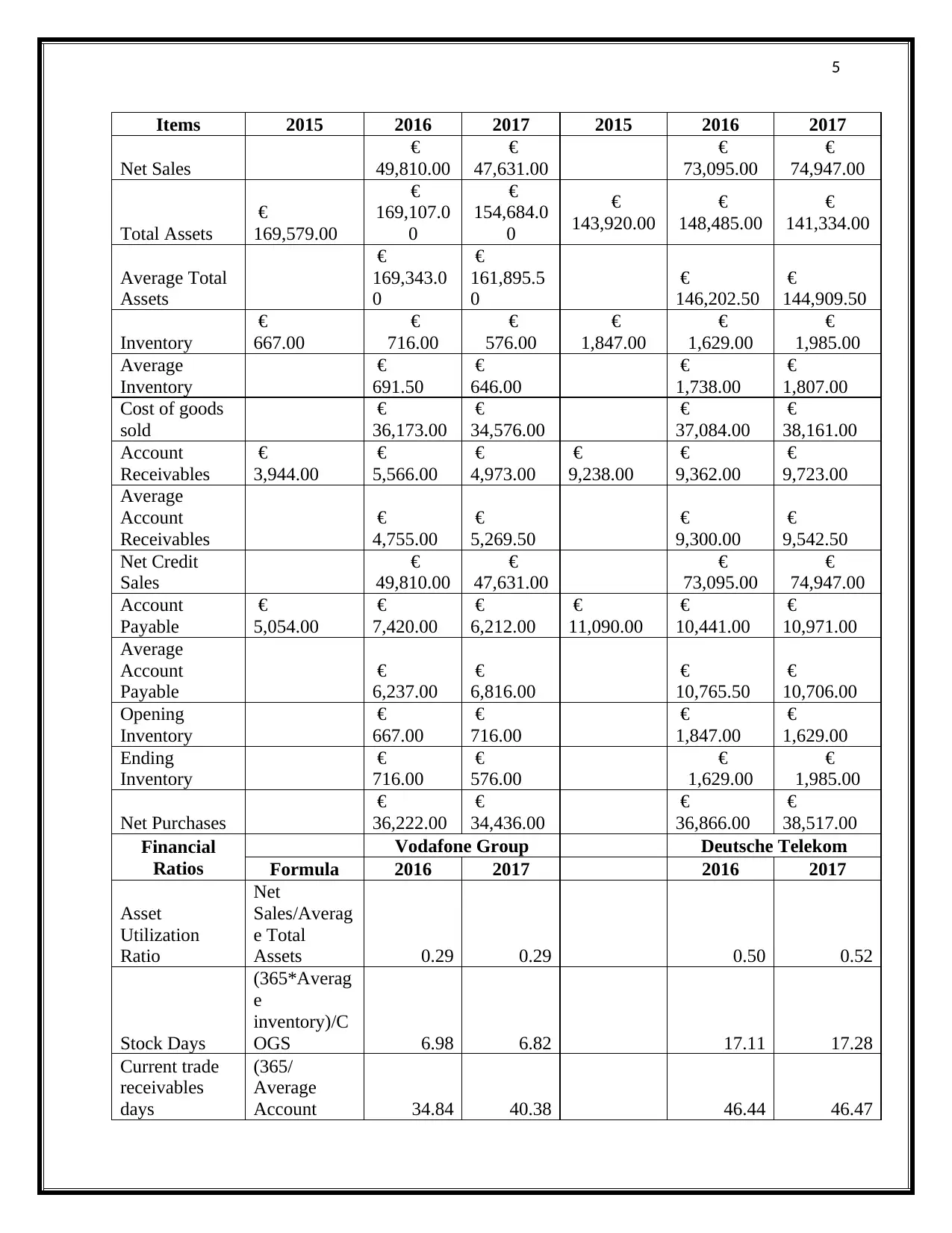

Items 2015 2016 2017 2015 2016 2017

Net Sales

€

49,810.00

€

47,631.00

€

73,095.00

€

74,947.00

Total Assets

€

169,579.00

€

169,107.0

0

€

154,684.0

0

€

143,920.00

€

148,485.00

€

141,334.00

Average Total

Assets

€

169,343.0

0

€

161,895.5

0

€

146,202.50

€

144,909.50

Inventory

€

667.00

€

716.00

€

576.00

€

1,847.00

€

1,629.00

€

1,985.00

Average

Inventory

€

691.50

€

646.00

€

1,738.00

€

1,807.00

Cost of goods

sold

€

36,173.00

€

34,576.00

€

37,084.00

€

38,161.00

Account

Receivables

€

3,944.00

€

5,566.00

€

4,973.00

€

9,238.00

€

9,362.00

€

9,723.00

Average

Account

Receivables

€

4,755.00

€

5,269.50

€

9,300.00

€

9,542.50

Net Credit

Sales

€

49,810.00

€

47,631.00

€

73,095.00

€

74,947.00

Account

Payable

€

5,054.00

€

7,420.00

€

6,212.00

€

11,090.00

€

10,441.00

€

10,971.00

Average

Account

Payable

€

6,237.00

€

6,816.00

€

10,765.50

€

10,706.00

Opening

Inventory

€

667.00

€

716.00

€

1,847.00

€

1,629.00

Ending

Inventory

€

716.00

€

576.00

€

1,629.00

€

1,985.00

Net Purchases

€

36,222.00

€

34,436.00

€

36,866.00

€

38,517.00

Financial

Ratios

Vodafone Group Deutsche Telekom

Formula 2016 2017 2016 2017

Asset

Utilization

Ratio

Net

Sales/Averag

e Total

Assets 0.29 0.29 0.50 0.52

Stock Days

(365*Averag

e

inventory)/C

OGS 6.98 6.82 17.11 17.28

Current trade

receivables

days

(365/

Average

Account 34.84 40.38 46.44 46.47

Items 2015 2016 2017 2015 2016 2017

Net Sales

€

49,810.00

€

47,631.00

€

73,095.00

€

74,947.00

Total Assets

€

169,579.00

€

169,107.0

0

€

154,684.0

0

€

143,920.00

€

148,485.00

€

141,334.00

Average Total

Assets

€

169,343.0

0

€

161,895.5

0

€

146,202.50

€

144,909.50

Inventory

€

667.00

€

716.00

€

576.00

€

1,847.00

€

1,629.00

€

1,985.00

Average

Inventory

€

691.50

€

646.00

€

1,738.00

€

1,807.00

Cost of goods

sold

€

36,173.00

€

34,576.00

€

37,084.00

€

38,161.00

Account

Receivables

€

3,944.00

€

5,566.00

€

4,973.00

€

9,238.00

€

9,362.00

€

9,723.00

Average

Account

Receivables

€

4,755.00

€

5,269.50

€

9,300.00

€

9,542.50

Net Credit

Sales

€

49,810.00

€

47,631.00

€

73,095.00

€

74,947.00

Account

Payable

€

5,054.00

€

7,420.00

€

6,212.00

€

11,090.00

€

10,441.00

€

10,971.00

Average

Account

Payable

€

6,237.00

€

6,816.00

€

10,765.50

€

10,706.00

Opening

Inventory

€

667.00

€

716.00

€

1,847.00

€

1,629.00

Ending

Inventory

€

716.00

€

576.00

€

1,629.00

€

1,985.00

Net Purchases

€

36,222.00

€

34,436.00

€

36,866.00

€

38,517.00

Financial

Ratios

Vodafone Group Deutsche Telekom

Formula 2016 2017 2016 2017

Asset

Utilization

Ratio

Net

Sales/Averag

e Total

Assets 0.29 0.29 0.50 0.52

Stock Days

(365*Averag

e

inventory)/C

OGS 6.98 6.82 17.11 17.28

Current trade

receivables

days

(365/

Average

Account 34.84 40.38 46.44 46.47

6

Receivables)/

Net Credit

Sales

Current trade

payables days

(365/

Average

Account

Payables)/To

tal Purchases 62.85 72.25 106.59 101.45

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

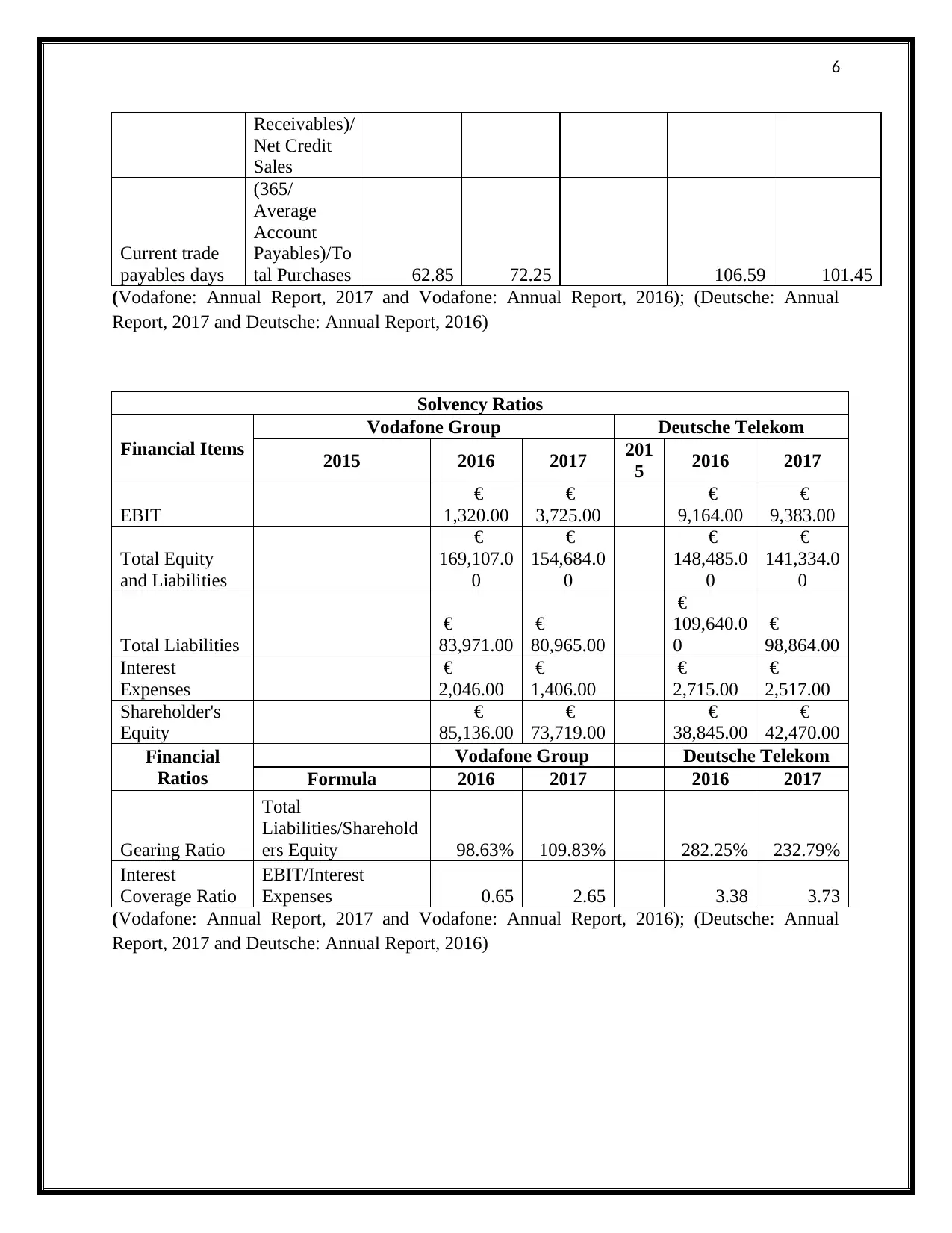

Solvency Ratios

Financial Items

Vodafone Group Deutsche Telekom

2015 2016 2017 201

5 2016 2017

EBIT

€

1,320.00

€

3,725.00

€

9,164.00

€

9,383.00

Total Equity

and Liabilities

€

169,107.0

0

€

154,684.0

0

€

148,485.0

0

€

141,334.0

0

Total Liabilities

€

83,971.00

€

80,965.00

€

109,640.0

0

€

98,864.00

Interest

Expenses

€

2,046.00

€

1,406.00

€

2,715.00

€

2,517.00

Shareholder's

Equity

€

85,136.00

€

73,719.00

€

38,845.00

€

42,470.00

Financial

Ratios

Vodafone Group Deutsche Telekom

Formula 2016 2017 2016 2017

Gearing Ratio

Total

Liabilities/Sharehold

ers Equity 98.63% 109.83% 282.25% 232.79%

Interest

Coverage Ratio

EBIT/Interest

Expenses 0.65 2.65 3.38 3.73

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Receivables)/

Net Credit

Sales

Current trade

payables days

(365/

Average

Account

Payables)/To

tal Purchases 62.85 72.25 106.59 101.45

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Solvency Ratios

Financial Items

Vodafone Group Deutsche Telekom

2015 2016 2017 201

5 2016 2017

EBIT

€

1,320.00

€

3,725.00

€

9,164.00

€

9,383.00

Total Equity

and Liabilities

€

169,107.0

0

€

154,684.0

0

€

148,485.0

0

€

141,334.0

0

Total Liabilities

€

83,971.00

€

80,965.00

€

109,640.0

0

€

98,864.00

Interest

Expenses

€

2,046.00

€

1,406.00

€

2,715.00

€

2,517.00

Shareholder's

Equity

€

85,136.00

€

73,719.00

€

38,845.00

€

42,470.00

Financial

Ratios

Vodafone Group Deutsche Telekom

Formula 2016 2017 2016 2017

Gearing Ratio

Total

Liabilities/Sharehold

ers Equity 98.63% 109.83% 282.25% 232.79%

Interest

Coverage Ratio

EBIT/Interest

Expenses 0.65 2.65 3.38 3.73

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Task 2: Financial Performance Analysis of Vodafone as Compared to Deutsche Telekom

with the use of Ratio Analysis

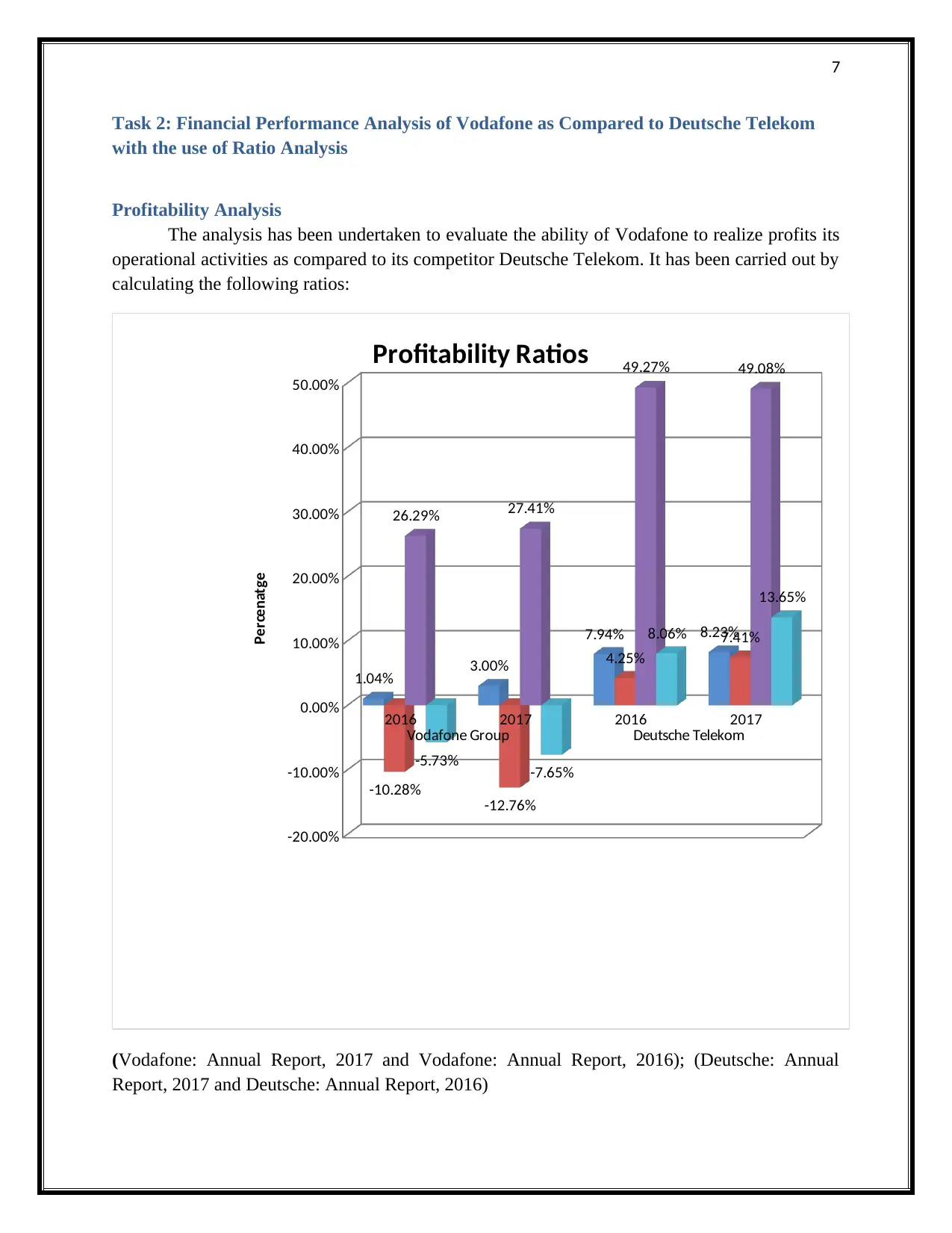

Profitability Analysis

The analysis has been undertaken to evaluate the ability of Vodafone to realize profits its

operational activities as compared to its competitor Deutsche Telekom. It has been carried out by

calculating the following ratios:

2016 2017 2016 2017

Vodafone Group Deutsche Telekom

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

1.04% 3.00%

7.94% 8.23%

-10.28%

-12.76%

4.25%

7.41%

26.29% 27.41%

49.27% 49.08%

-5.73% -7.65%

8.06%

13.65%

Profitability Ratios

Percenatge

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Task 2: Financial Performance Analysis of Vodafone as Compared to Deutsche Telekom

with the use of Ratio Analysis

Profitability Analysis

The analysis has been undertaken to evaluate the ability of Vodafone to realize profits its

operational activities as compared to its competitor Deutsche Telekom. It has been carried out by

calculating the following ratios:

2016 2017 2016 2017

Vodafone Group Deutsche Telekom

-20.00%

-10.00%

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

1.04% 3.00%

7.94% 8.23%

-10.28%

-12.76%

4.25%

7.41%

26.29% 27.41%

49.27% 49.08%

-5.73% -7.65%

8.06%

13.65%

Profitability Ratios

Percenatge

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Return on Capital Employed (ROCE)

The financial ratio provides a measure of the profitability realized by a company in

reference to the capital employed. The efficiency of a company to use its capital base for

realizing profits for Vodafone can be easily measured with the use of this ratio. The ratio for

Vodafone has been increased from 1.04% to 3% during the year 2016-2017. This depicts its

increasing profits realized from the use of capital base. The ratio for its competitor has also

reported an increase from 7.94% to 8.23% during 2016-2017 and it is also higher as compared to

Vodafone for the two years. The difference between the ratios for the two companies indicates

that Vodafone it is realizing lower profits from its capital use as compared to its competitor. This

implies that Vodafone need to incorporate the use of efficient plant and machinery or remove the

unnecessary asset base to maximize the use of its capital base and thus improving the ROCE

ratio.

Return on Sales

The ratio depicts the operating income realized by a company in comparison to the net

sales that has been incurred. Vodafone financial performance is an issue of concern on the basis

of the results of this ratio as it is realizing negative returns on its sales that is -10.28% to -12.76%

incurred during 2016-2017. On the contrary, its competitor is having an increasing trend of the

ratio for the financial period and has also maintained a higher positive return on the ratio that is

4.25% to 7.41%. This means that Vodafone is incurring significant financial loss for the selected

financial period while its competitor is able to realize a positive return on its sales. This implies

that Vodafone need to take measures for reducing its operational expenses for releasing profits

from its net sales incurred (Damodaran, 2011).

Gross Profit Margin

The ratio is used for examining the ability of a company to realize profit from it sales

after meeting the cost of sales. The gross profit margin of the company has depicted a slight

increase over 2016-2017 from 26.29% to 27.41% while its competitor Deutsche Telekom is

having a higher gross profit margin over the period. However, the ratio has depicted a slight

decrease from 49.27% to 49.08% for Deutsche Telekom but is better as compared to Vodafone.

This means that Vodafone is incurring higher cost in realizing sales as compared to its

competitor which is not good for supporting its future growth prospects.

Return on Equity

It depicts the returns realized by a company on the equity base invested by its

shareholders. Vodafone has realized negative returns on its equity base that has depicted an

increasing negative trend from -5.73% to -7.65% during 2016-2017. On the contrary, Deutsche

Telekom has reported an increase in its ROE from 8.065 to 13.65% during 2016-2017 and this

depicts that it has realized a higher returns on its equity investment of the shareholders. The

means that Vodafone is having higher liability as it is using higher debt proportion and is not

able to realize income for its shareholders. This is a potential red flag for Vodafone as it would

Return on Capital Employed (ROCE)

The financial ratio provides a measure of the profitability realized by a company in

reference to the capital employed. The efficiency of a company to use its capital base for

realizing profits for Vodafone can be easily measured with the use of this ratio. The ratio for

Vodafone has been increased from 1.04% to 3% during the year 2016-2017. This depicts its

increasing profits realized from the use of capital base. The ratio for its competitor has also

reported an increase from 7.94% to 8.23% during 2016-2017 and it is also higher as compared to

Vodafone for the two years. The difference between the ratios for the two companies indicates

that Vodafone it is realizing lower profits from its capital use as compared to its competitor. This

implies that Vodafone need to incorporate the use of efficient plant and machinery or remove the

unnecessary asset base to maximize the use of its capital base and thus improving the ROCE

ratio.

Return on Sales

The ratio depicts the operating income realized by a company in comparison to the net

sales that has been incurred. Vodafone financial performance is an issue of concern on the basis

of the results of this ratio as it is realizing negative returns on its sales that is -10.28% to -12.76%

incurred during 2016-2017. On the contrary, its competitor is having an increasing trend of the

ratio for the financial period and has also maintained a higher positive return on the ratio that is

4.25% to 7.41%. This means that Vodafone is incurring significant financial loss for the selected

financial period while its competitor is able to realize a positive return on its sales. This implies

that Vodafone need to take measures for reducing its operational expenses for releasing profits

from its net sales incurred (Damodaran, 2011).

Gross Profit Margin

The ratio is used for examining the ability of a company to realize profit from it sales

after meeting the cost of sales. The gross profit margin of the company has depicted a slight

increase over 2016-2017 from 26.29% to 27.41% while its competitor Deutsche Telekom is

having a higher gross profit margin over the period. However, the ratio has depicted a slight

decrease from 49.27% to 49.08% for Deutsche Telekom but is better as compared to Vodafone.

This means that Vodafone is incurring higher cost in realizing sales as compared to its

competitor which is not good for supporting its future growth prospects.

Return on Equity

It depicts the returns realized by a company on the equity base invested by its

shareholders. Vodafone has realized negative returns on its equity base that has depicted an

increasing negative trend from -5.73% to -7.65% during 2016-2017. On the contrary, Deutsche

Telekom has reported an increase in its ROE from 8.065 to 13.65% during 2016-2017 and this

depicts that it has realized a higher returns on its equity investment of the shareholders. The

means that Vodafone is having higher liability as it is using higher debt proportion and is not

able to realize income for its shareholders. This is a potential red flag for Vodafone as it would

9

have a negative impact on the mind of its future investors to invest within the company and this

can restrict its business growth and development (Damodaran, 2011).

have a negative impact on the mind of its future investors to invest within the company and this

can restrict its business growth and development (Damodaran, 2011).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Liquidity Analysis

The analysis has been carried out to examine the financial performance of Vodafone in

terms of the liquid assets possessed by it for avoiding the risk of not able to meet its current

liabilities as they become due as compared to its selected competitor. The analysis has been

carried out with the use of following ratio:

2016 2017 2016 2017

Vodafone Group Deutsche Telekom

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Liquidity Ratios

Times

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Current Ratio

It provides a measurement of the current assets possessed by a company for meeting its

current financial obligations. The ratio for Vodafone has depicted an increasing trend from 0.76

to 0.83 during 2016-2017 while for its competitor has depicted a decreasing trend from 0.80 to

0.75 during 2016-2017. This means that Vodafone is able to maintain a higher base of liquid

assets that can be converted to cash for meeting its financial liabilities as compared to Deutsche

Telekom. However, ratio for both the companies is lower than 1 indicating there is financial risk

for not able to meet their financial liabilities as they are having less current base in comparison to

the current liabilities (Damodaran, 2011).

Quick Ratio

This ratio measures the amount of most liquid assets that a company owns, that are

accounts receivable or cash equivalents, which can be quickly transferred to cash for meeting the

Liquidity Analysis

The analysis has been carried out to examine the financial performance of Vodafone in

terms of the liquid assets possessed by it for avoiding the risk of not able to meet its current

liabilities as they become due as compared to its selected competitor. The analysis has been

carried out with the use of following ratio:

2016 2017 2016 2017

Vodafone Group Deutsche Telekom

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Liquidity Ratios

Times

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

Current Ratio

It provides a measurement of the current assets possessed by a company for meeting its

current financial obligations. The ratio for Vodafone has depicted an increasing trend from 0.76

to 0.83 during 2016-2017 while for its competitor has depicted a decreasing trend from 0.80 to

0.75 during 2016-2017. This means that Vodafone is able to maintain a higher base of liquid

assets that can be converted to cash for meeting its financial liabilities as compared to Deutsche

Telekom. However, ratio for both the companies is lower than 1 indicating there is financial risk

for not able to meet their financial liabilities as they are having less current base in comparison to

the current liabilities (Damodaran, 2011).

Quick Ratio

This ratio measures the amount of most liquid assets that a company owns, that are

accounts receivable or cash equivalents, which can be quickly transferred to cash for meeting the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

short-term obligations. The quick ratio has also improved from 0.75 to 0.82 for Vodafone while

for Deutsche Telekom it has decreased gradually from 0.75 to 0.67 during 2016-2017. This

means that Vodafone possess higher cash equivalent asset base for meeting the financial

liabilities as compared to Deutsche Telekom.

Efficiency Analysis

The analysis measures the effectiveness of Vodafone to utilize its assets and liabilities for

generating sales in comparison to its competitor. The analysis is carried with the use of following

ratios:

2016 2017 2016 2017

Vodafone Group Deutsche Telekom

0.00

20.00

40.00

60.00

80.00

100.00

120.00

0.29 0.29 0.50 0.52

6.98 6.82

17.11 17.28

34.84

40.38

46.44 46.47

62.85

72.25

106.59

101.45

Efficiency Ratio

Times

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

short-term obligations. The quick ratio has also improved from 0.75 to 0.82 for Vodafone while

for Deutsche Telekom it has decreased gradually from 0.75 to 0.67 during 2016-2017. This

means that Vodafone possess higher cash equivalent asset base for meeting the financial

liabilities as compared to Deutsche Telekom.

Efficiency Analysis

The analysis measures the effectiveness of Vodafone to utilize its assets and liabilities for

generating sales in comparison to its competitor. The analysis is carried with the use of following

ratios:

2016 2017 2016 2017

Vodafone Group Deutsche Telekom

0.00

20.00

40.00

60.00

80.00

100.00

120.00

0.29 0.29 0.50 0.52

6.98 6.82

17.11 17.28

34.84

40.38

46.44 46.47

62.85

72.25

106.59

101.45

Efficiency Ratio

Times

(Vodafone: Annual Report, 2017 and Vodafone: Annual Report, 2016); (Deutsche: Annual

Report, 2017 and Deutsche: Annual Report, 2016)

12

Asset Utilization Ratio

The ratio provides a measure of the revenue realized by the company by the use of its

asset base. Vodafone has maintained a very low asset utilization ratio over the financial period

2016-2017 that ahs nearly remained constant over the selected financial period. The ratio for

Deutsche Telekom has been significantly improved from 0.50 to 0.52 over 2016-2017 and is

higher than Vodafone Group. This indicates that Vodafone is not able to use it asset base

properly as the ratio is very low as compared to its competitor. This means that Vodafone need to

improve the asset efficiency by maintaining updated asset base such as replacing the inefficient

plant and machinery so that it is able to provide higher productivity and sales.

Stock Days

The ratio is used for determining the effectiveness of a company to replace its inventory

and realizing sales. The ratio for Vodafone is consequently lower as compared to its competitor

Deutsche Telekom. It has depicted decreasing trend from 6.98 to 6.82 over the selected financial

period as compared to Deutsche which has depicted an increasing trend from 17.11 to 17.28 over

the financial years. This means that Vodafone possess higher efficiency to replace its inventory

and convert it into sales as compared to Deutsche Telecom. This implies that Vodafone is

incurring less cost in holding stock in hand as compared to Deutsche Telecom which is holding

stocks for higher number of days and thus it can negatively impact its operating income in the

future context (Damodaran, 2011).

Current trade receivable days

The ratio is helpful for knowing the number of days a customer invoice is outstanding

before it is collected. The ratio has increased from 34.84 to 40.38 for Vodafone which is

considerably lower as compared to Deutsche Telecom that is maintained 46.44 to 46.47 during

2016-2017. This implies that Vodafone efficiency to collect credit from its customers is good as

it is taking less number of days as compared to its competitor. However, the ratio for Vodafone

has depicted an increase over the selected financial period which cannot be regarded as good for

supporting its future growth plans. This implies that Vodafone need to take measures for

improving its efficiency to collect money from its debtors by improving its credit policies.

However, its efficiency to collect amount of credit sales is better as compared to Deutsche

Telecom which is means it is having good supplier relationships or credit payment policies.

Current trade payable days

The ratio is used to determine the number of days a company takes for settling its debts

from the suppliers. The ratio for Vodafone has depicted an increase from 62.85 to 72.25 but is

significantly lower as compared to Deutsche Telecom that ahs also reported a decline from

106.59 to 101.42 over the financial period 2016-2017. This means that Vodafone efficiency is

better to meet its debt obligations rising from its bills and invoices whereas Detusche Telecom

efficiency is lower to meet its bills and invoices obligations (Brigham and Michael, 2013).

Asset Utilization Ratio

The ratio provides a measure of the revenue realized by the company by the use of its

asset base. Vodafone has maintained a very low asset utilization ratio over the financial period

2016-2017 that ahs nearly remained constant over the selected financial period. The ratio for

Deutsche Telekom has been significantly improved from 0.50 to 0.52 over 2016-2017 and is

higher than Vodafone Group. This indicates that Vodafone is not able to use it asset base

properly as the ratio is very low as compared to its competitor. This means that Vodafone need to

improve the asset efficiency by maintaining updated asset base such as replacing the inefficient

plant and machinery so that it is able to provide higher productivity and sales.

Stock Days

The ratio is used for determining the effectiveness of a company to replace its inventory

and realizing sales. The ratio for Vodafone is consequently lower as compared to its competitor

Deutsche Telekom. It has depicted decreasing trend from 6.98 to 6.82 over the selected financial

period as compared to Deutsche which has depicted an increasing trend from 17.11 to 17.28 over

the financial years. This means that Vodafone possess higher efficiency to replace its inventory

and convert it into sales as compared to Deutsche Telecom. This implies that Vodafone is

incurring less cost in holding stock in hand as compared to Deutsche Telecom which is holding

stocks for higher number of days and thus it can negatively impact its operating income in the

future context (Damodaran, 2011).

Current trade receivable days

The ratio is helpful for knowing the number of days a customer invoice is outstanding

before it is collected. The ratio has increased from 34.84 to 40.38 for Vodafone which is

considerably lower as compared to Deutsche Telecom that is maintained 46.44 to 46.47 during

2016-2017. This implies that Vodafone efficiency to collect credit from its customers is good as

it is taking less number of days as compared to its competitor. However, the ratio for Vodafone

has depicted an increase over the selected financial period which cannot be regarded as good for

supporting its future growth plans. This implies that Vodafone need to take measures for

improving its efficiency to collect money from its debtors by improving its credit policies.

However, its efficiency to collect amount of credit sales is better as compared to Deutsche

Telecom which is means it is having good supplier relationships or credit payment policies.

Current trade payable days

The ratio is used to determine the number of days a company takes for settling its debts

from the suppliers. The ratio for Vodafone has depicted an increase from 62.85 to 72.25 but is

significantly lower as compared to Deutsche Telecom that ahs also reported a decline from

106.59 to 101.42 over the financial period 2016-2017. This means that Vodafone efficiency is

better to meet its debt obligations rising from its bills and invoices whereas Detusche Telecom

efficiency is lower to meet its bills and invoices obligations (Brigham and Michael, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.