Financial Services and Credit Regulations

VerifiedAdded on 2021/04/24

|32

|3641

|20

AI Summary

This assignment delves into the realm of financial services and credit regulations, focusing on key concepts such as responsible lending practices, assessing credit risks, and providing suitable advice to customers. The scenario involves a client, Adam, who is seeking various financial products and services, including home and contents insurance, redraw facilities, and mortgage protection insurance. Through this assignment, students demonstrate their understanding of Australian regulatory frameworks, such as the Australian Financial Security Authority (AFSA) and Credit Ombudsman Services Limited (COSL), and apply theoretical knowledge to real-world scenarios.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Name:

Course

Professor’s name

University name

City, State

Date of submission

154673931491949908.docx Version 2 Page 1 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Course

Professor’s name

University name

City, State

Date of submission

154673931491949908.docx Version 2 Page 1 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Scenario

You are the owner/office manager of Careful Financial Services (“CFF”) - a mortgage

broking business in Fedtown.

The business has been successfully operating for 5 years and a recent increase in loan

applications has you considering whether to employ a new loan writer.

One of the reasons for the increase in applications is the approval by local council of a

development application for a site that will contain 500 new houses. Off the plan sales

have been popular for the first release with an average sale price of $350,000.

The economy is reasonably stable with interest rates at 5.7%, they have not changed

in the past 6 months and are not predicted to change in the next quarter.

No risk management planning has ever been completed and you feel it is needed so

that both opportunities and risks are effectively identified and treated.

Relevant information:

There is one other mortgage broking business in Fedtown.

154673931491949908.docx Version 2 Page 2 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

You are the owner/office manager of Careful Financial Services (“CFF”) - a mortgage

broking business in Fedtown.

The business has been successfully operating for 5 years and a recent increase in loan

applications has you considering whether to employ a new loan writer.

One of the reasons for the increase in applications is the approval by local council of a

development application for a site that will contain 500 new houses. Off the plan sales

have been popular for the first release with an average sale price of $350,000.

The economy is reasonably stable with interest rates at 5.7%, they have not changed

in the past 6 months and are not predicted to change in the next quarter.

No risk management planning has ever been completed and you feel it is needed so

that both opportunities and risks are effectively identified and treated.

Relevant information:

There is one other mortgage broking business in Fedtown.

154673931491949908.docx Version 2 Page 2 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Your business has 6 employees who have all been with the business for 3

years or more. 1 Business Development Manager, 3 loan writers, 1 support

officer, 1 administration assistant.

Premises are owned.

Spare office space is limited in the current premises.

Business borrowings:

Term loan $200,000

Overdraft $20,000

Procedure manuals completed when business first opened (never reviewed).

Monthly workplace inspections are conducted.

The business operates a company car that is leased.

All computers are networked and basic virus protection is installed.

Training of new staff and ongoing training is not well structured and is a bit

“hit and miss”.

Business insurance is current – including personal injury and property damage,

fire, storm, malicious damage and other defined events, business vehicle

insurance, business interruption, personal accident or illness.

Audits have not been completed as regularly as needed due to Office Manager

being too busy.

A recent customer satisfaction survey showed excellent results, which has

been very positive for the business with a high level of referrals being

received.

Business sponsors the local Under 10’s soccer team and has participated in

Clean up Australia day for the last 5 years.

Aged debtors and creditors listing shows some long overdue accounts.

154673931491949908.docx Version 2 Page 3 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

years or more. 1 Business Development Manager, 3 loan writers, 1 support

officer, 1 administration assistant.

Premises are owned.

Spare office space is limited in the current premises.

Business borrowings:

Term loan $200,000

Overdraft $20,000

Procedure manuals completed when business first opened (never reviewed).

Monthly workplace inspections are conducted.

The business operates a company car that is leased.

All computers are networked and basic virus protection is installed.

Training of new staff and ongoing training is not well structured and is a bit

“hit and miss”.

Business insurance is current – including personal injury and property damage,

fire, storm, malicious damage and other defined events, business vehicle

insurance, business interruption, personal accident or illness.

Audits have not been completed as regularly as needed due to Office Manager

being too busy.

A recent customer satisfaction survey showed excellent results, which has

been very positive for the business with a high level of referrals being

received.

Business sponsors the local Under 10’s soccer team and has participated in

Clean up Australia day for the last 5 years.

Aged debtors and creditors listing shows some long overdue accounts.

154673931491949908.docx Version 2 Page 3 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Answer the following questions using the above scenario:

Please note: The answers provided should relate directly to the scenario and be in

your own words to demonstrate your understanding (do not copy directly from the

notes). The case study in the learners guide is there to assist in your completion of

the assessment.

Question 1 – Establish the Context

a) Identify at least 5 external and 2 internal stakeholders:

External Stakeholders Internal Stakeholders

Suppliers

Customers

Local council

Society

competitors

Employees

Owners

154673931491949908.docx Version 2 Page 4 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Please note: The answers provided should relate directly to the scenario and be in

your own words to demonstrate your understanding (do not copy directly from the

notes). The case study in the learners guide is there to assist in your completion of

the assessment.

Question 1 – Establish the Context

a) Identify at least 5 external and 2 internal stakeholders:

External Stakeholders Internal Stakeholders

Suppliers

Customers

Local council

Society

competitors

Employees

Owners

154673931491949908.docx Version 2 Page 4 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

b) Identify at least 4 external and 3 internal influences:

External Internal

Staff

Money

Company culture

The economy

Competition

Technology

Politics

Customers and suppliers

c) List 5 key business drivers:

1. Cash

2. Profit

154673931491949908.docx Version 2 Page 5 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

External Internal

Staff

Money

Company culture

The economy

Competition

Technology

Politics

Customers and suppliers

c) List 5 key business drivers:

1. Cash

2. Profit

154673931491949908.docx Version 2 Page 5 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

3. Assets

4. Growth

5. People

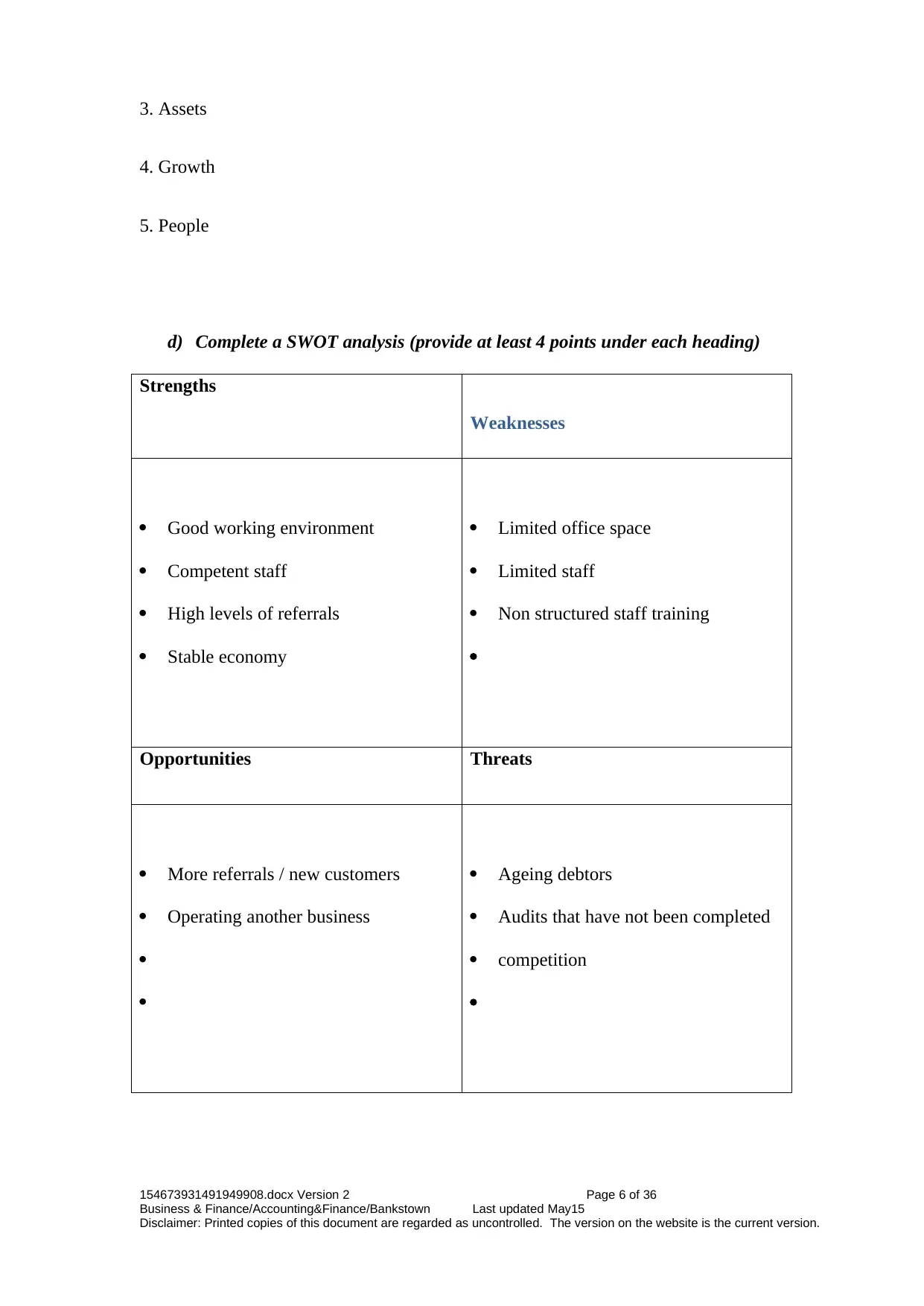

d) Complete a SWOT analysis (provide at least 4 points under each heading)

Strengths

Weaknesses

Good working environment

Competent staff

High levels of referrals

Stable economy

Limited office space

Limited staff

Non structured staff training

Opportunities Threats

More referrals / new customers

Operating another business

Ageing debtors

Audits that have not been completed

competition

154673931491949908.docx Version 2 Page 6 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

4. Growth

5. People

d) Complete a SWOT analysis (provide at least 4 points under each heading)

Strengths

Weaknesses

Good working environment

Competent staff

High levels of referrals

Stable economy

Limited office space

Limited staff

Non structured staff training

Opportunities Threats

More referrals / new customers

Operating another business

Ageing debtors

Audits that have not been completed

competition

154673931491949908.docx Version 2 Page 6 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

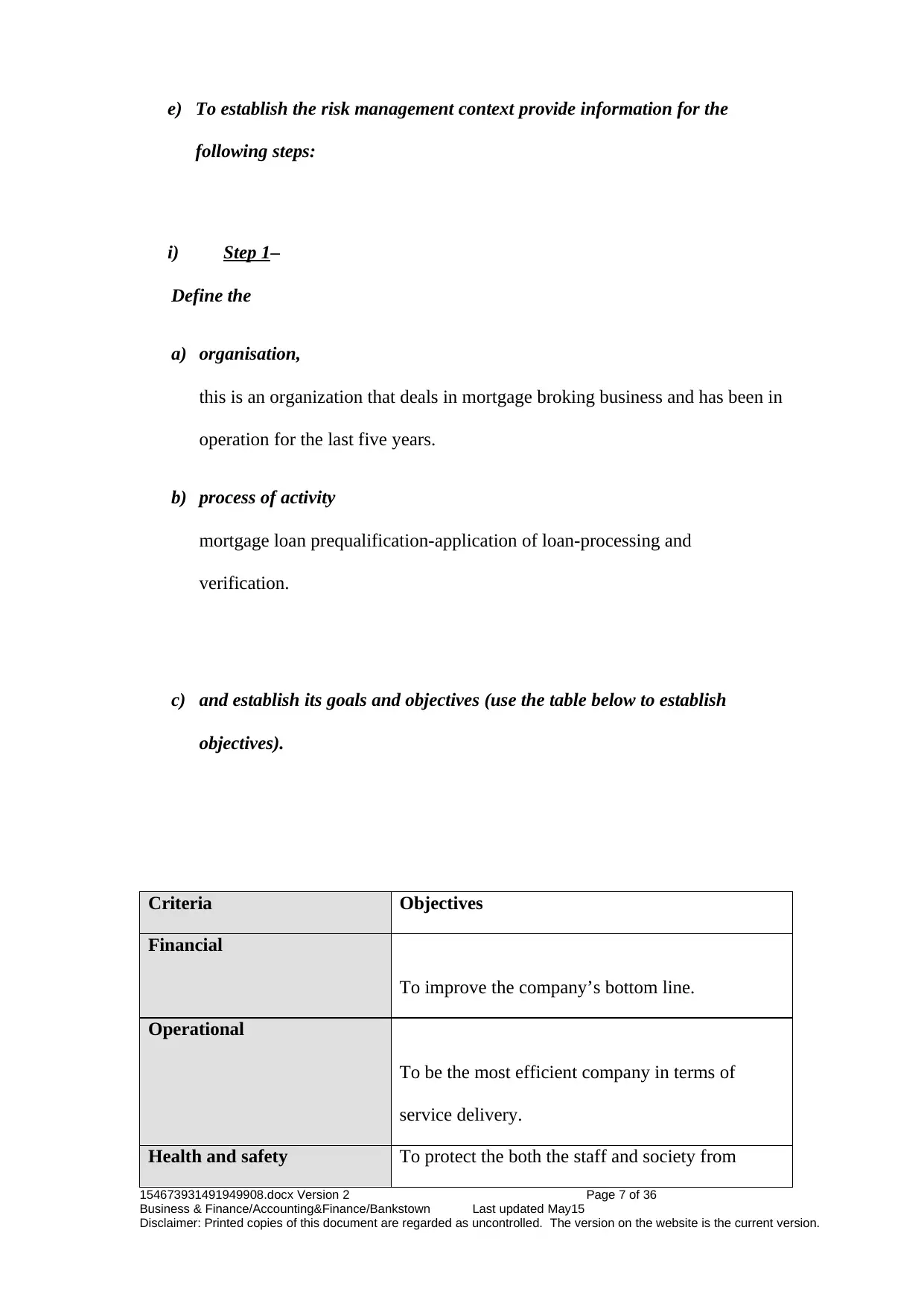

e) To establish the risk management context provide information for the

following steps:

i) Step 1–

Define the

a) organisation,

this is an organization that deals in mortgage broking business and has been in

operation for the last five years.

b) process of activity

mortgage loan prequalification-application of loan-processing and

verification.

c) and establish its goals and objectives (use the table below to establish

objectives).

Criteria Objectives

Financial

To improve the company’s bottom line.

Operational

To be the most efficient company in terms of

service delivery.

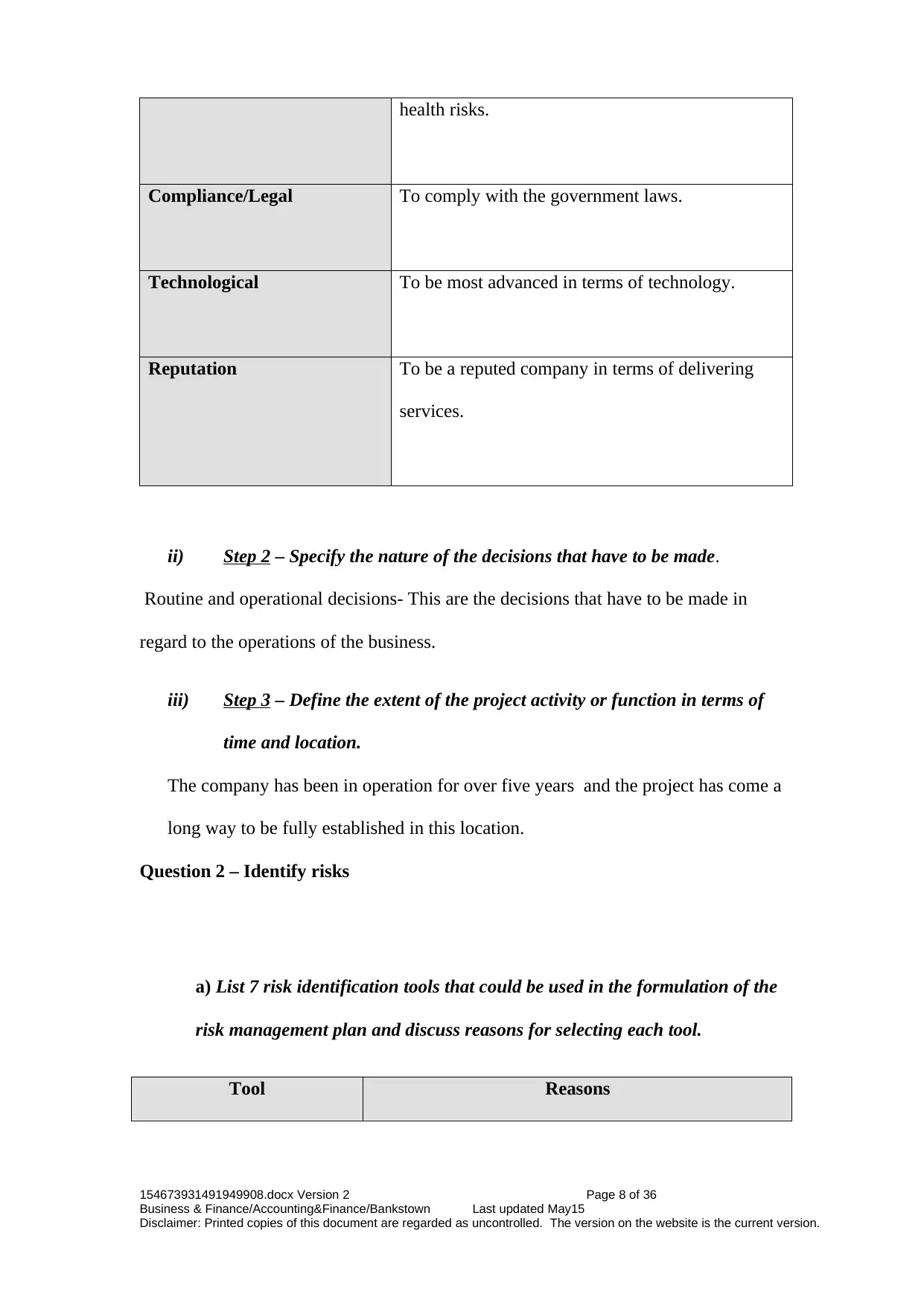

Health and safety To protect the both the staff and society from

154673931491949908.docx Version 2 Page 7 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

following steps:

i) Step 1–

Define the

a) organisation,

this is an organization that deals in mortgage broking business and has been in

operation for the last five years.

b) process of activity

mortgage loan prequalification-application of loan-processing and

verification.

c) and establish its goals and objectives (use the table below to establish

objectives).

Criteria Objectives

Financial

To improve the company’s bottom line.

Operational

To be the most efficient company in terms of

service delivery.

Health and safety To protect the both the staff and society from

154673931491949908.docx Version 2 Page 7 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

health risks.

Compliance/Legal To comply with the government laws.

Technological To be most advanced in terms of technology.

Reputation To be a reputed company in terms of delivering

services.

ii) Step 2 – Specify the nature of the decisions that have to be made.

Routine and operational decisions- This are the decisions that have to be made in

regard to the operations of the business.

iii) Step 3 – Define the extent of the project activity or function in terms of

time and location.

The company has been in operation for over five years and the project has come a

long way to be fully established in this location.

Question 2 – Identify risks

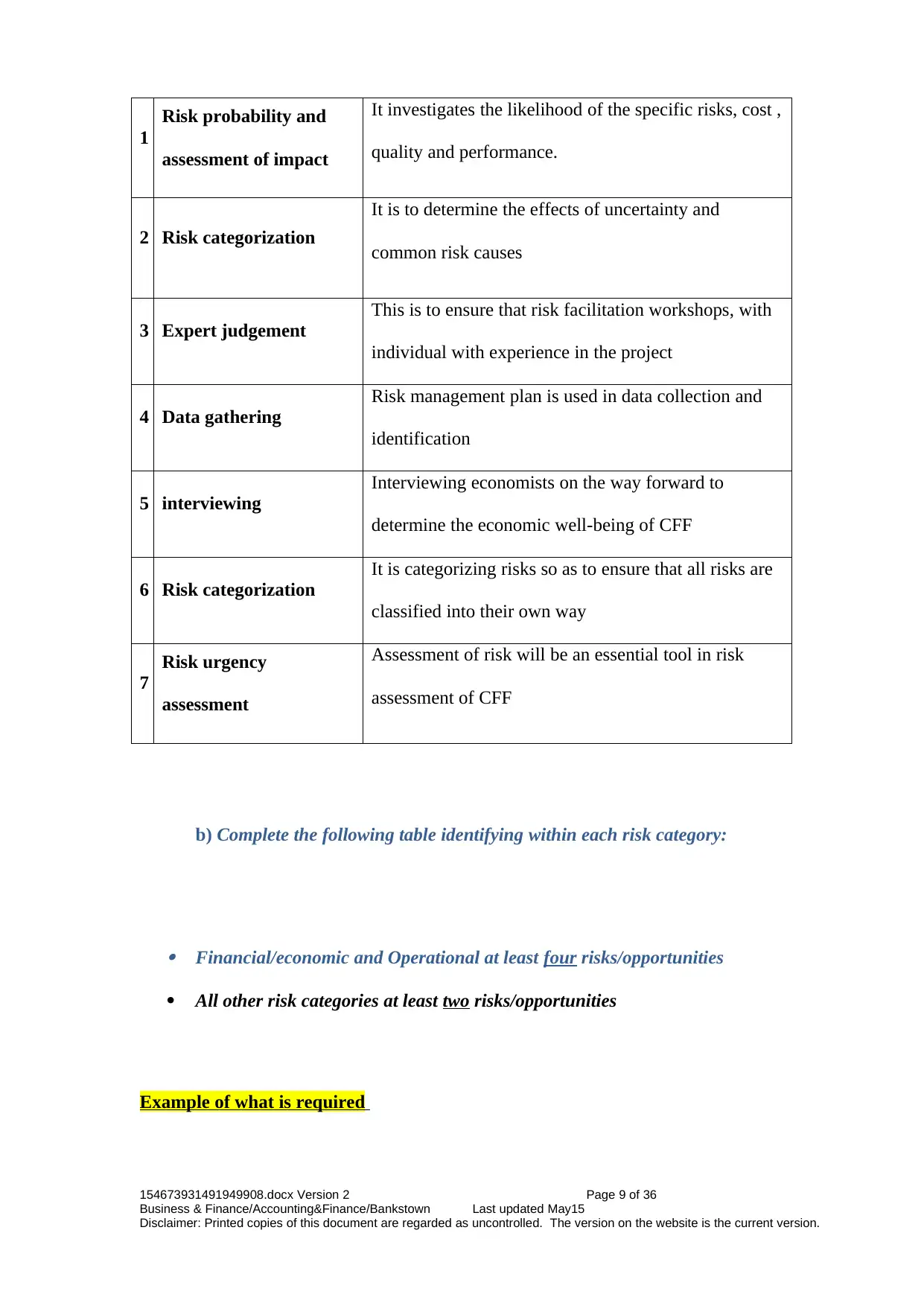

a) List 7 risk identification tools that could be used in the formulation of the

risk management plan and discuss reasons for selecting each tool.

Tool Reasons

154673931491949908.docx Version 2 Page 8 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Compliance/Legal To comply with the government laws.

Technological To be most advanced in terms of technology.

Reputation To be a reputed company in terms of delivering

services.

ii) Step 2 – Specify the nature of the decisions that have to be made.

Routine and operational decisions- This are the decisions that have to be made in

regard to the operations of the business.

iii) Step 3 – Define the extent of the project activity or function in terms of

time and location.

The company has been in operation for over five years and the project has come a

long way to be fully established in this location.

Question 2 – Identify risks

a) List 7 risk identification tools that could be used in the formulation of the

risk management plan and discuss reasons for selecting each tool.

Tool Reasons

154673931491949908.docx Version 2 Page 8 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

1

Risk probability and

assessment of impact

It investigates the likelihood of the specific risks, cost ,

quality and performance.

2 Risk categorization

It is to determine the effects of uncertainty and

common risk causes

3 Expert judgement

This is to ensure that risk facilitation workshops, with

individual with experience in the project

4 Data gathering

Risk management plan is used in data collection and

identification

5 interviewing

Interviewing economists on the way forward to

determine the economic well-being of CFF

6 Risk categorization

It is categorizing risks so as to ensure that all risks are

classified into their own way

7

Risk urgency

assessment

Assessment of risk will be an essential tool in risk

assessment of CFF

b) Complete the following table identifying within each risk category:

Financial/economic and Operational at least four risks/opportunities

All other risk categories at least two risks/opportunities

Example of what is required

154673931491949908.docx Version 2 Page 9 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Risk probability and

assessment of impact

It investigates the likelihood of the specific risks, cost ,

quality and performance.

2 Risk categorization

It is to determine the effects of uncertainty and

common risk causes

3 Expert judgement

This is to ensure that risk facilitation workshops, with

individual with experience in the project

4 Data gathering

Risk management plan is used in data collection and

identification

5 interviewing

Interviewing economists on the way forward to

determine the economic well-being of CFF

6 Risk categorization

It is categorizing risks so as to ensure that all risks are

classified into their own way

7

Risk urgency

assessment

Assessment of risk will be an essential tool in risk

assessment of CFF

b) Complete the following table identifying within each risk category:

Financial/economic and Operational at least four risks/opportunities

All other risk categories at least two risks/opportunities

Example of what is required

154673931491949908.docx Version 2 Page 9 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

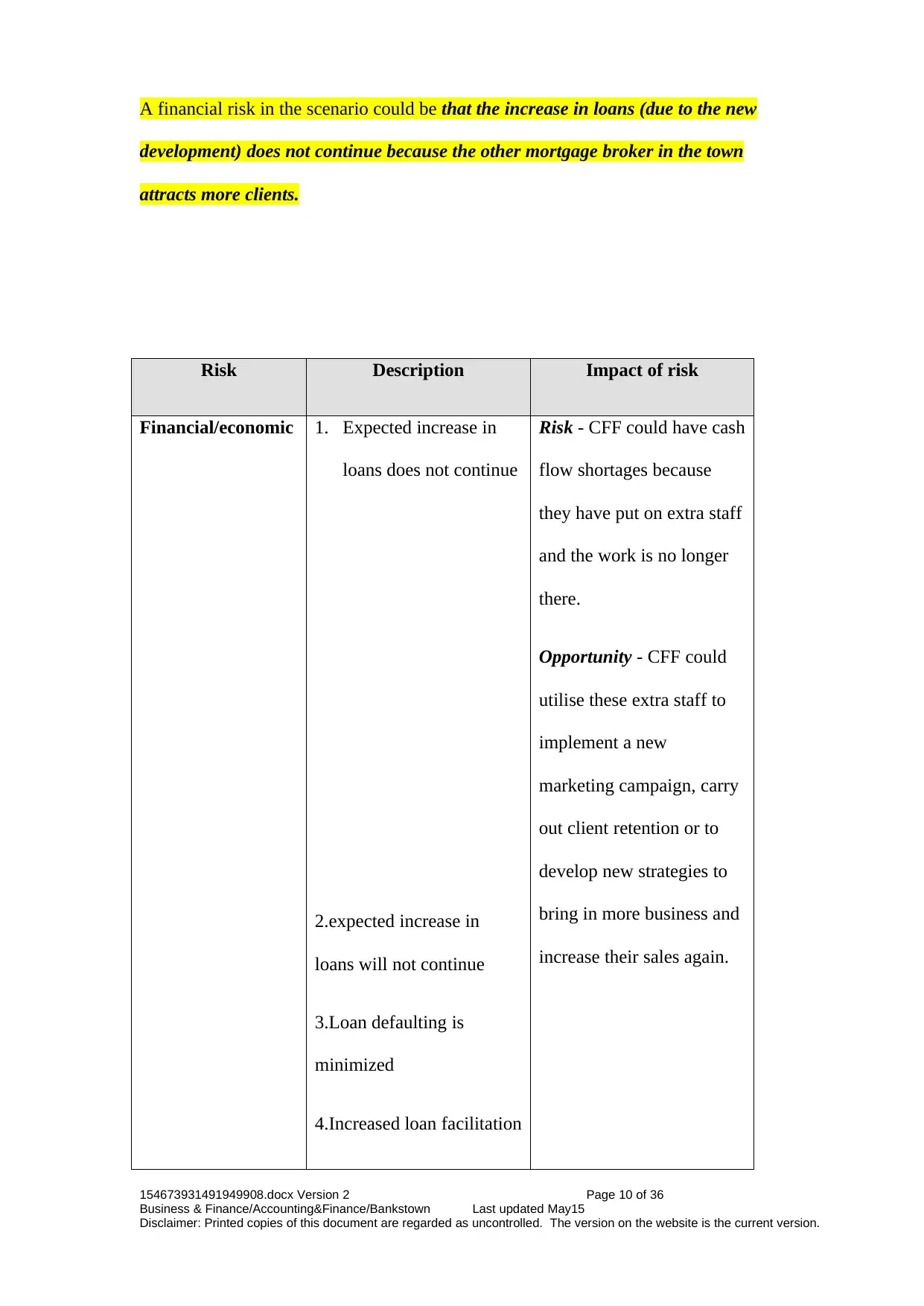

A financial risk in the scenario could be that the increase in loans (due to the new

development) does not continue because the other mortgage broker in the town

attracts more clients.

Risk Description Impact of risk

Financial/economic 1. Expected increase in

loans does not continue

2.expected increase in

loans will not continue

3.Loan defaulting is

minimized

4.Increased loan facilitation

Risk - CFF could have cash

flow shortages because

they have put on extra staff

and the work is no longer

there.

Opportunity - CFF could

utilise these extra staff to

implement a new

marketing campaign, carry

out client retention or to

develop new strategies to

bring in more business and

increase their sales again.

154673931491949908.docx Version 2 Page 10 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

development) does not continue because the other mortgage broker in the town

attracts more clients.

Risk Description Impact of risk

Financial/economic 1. Expected increase in

loans does not continue

2.expected increase in

loans will not continue

3.Loan defaulting is

minimized

4.Increased loan facilitation

Risk - CFF could have cash

flow shortages because

they have put on extra staff

and the work is no longer

there.

Opportunity - CFF could

utilise these extra staff to

implement a new

marketing campaign, carry

out client retention or to

develop new strategies to

bring in more business and

increase their sales again.

154673931491949908.docx Version 2 Page 10 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

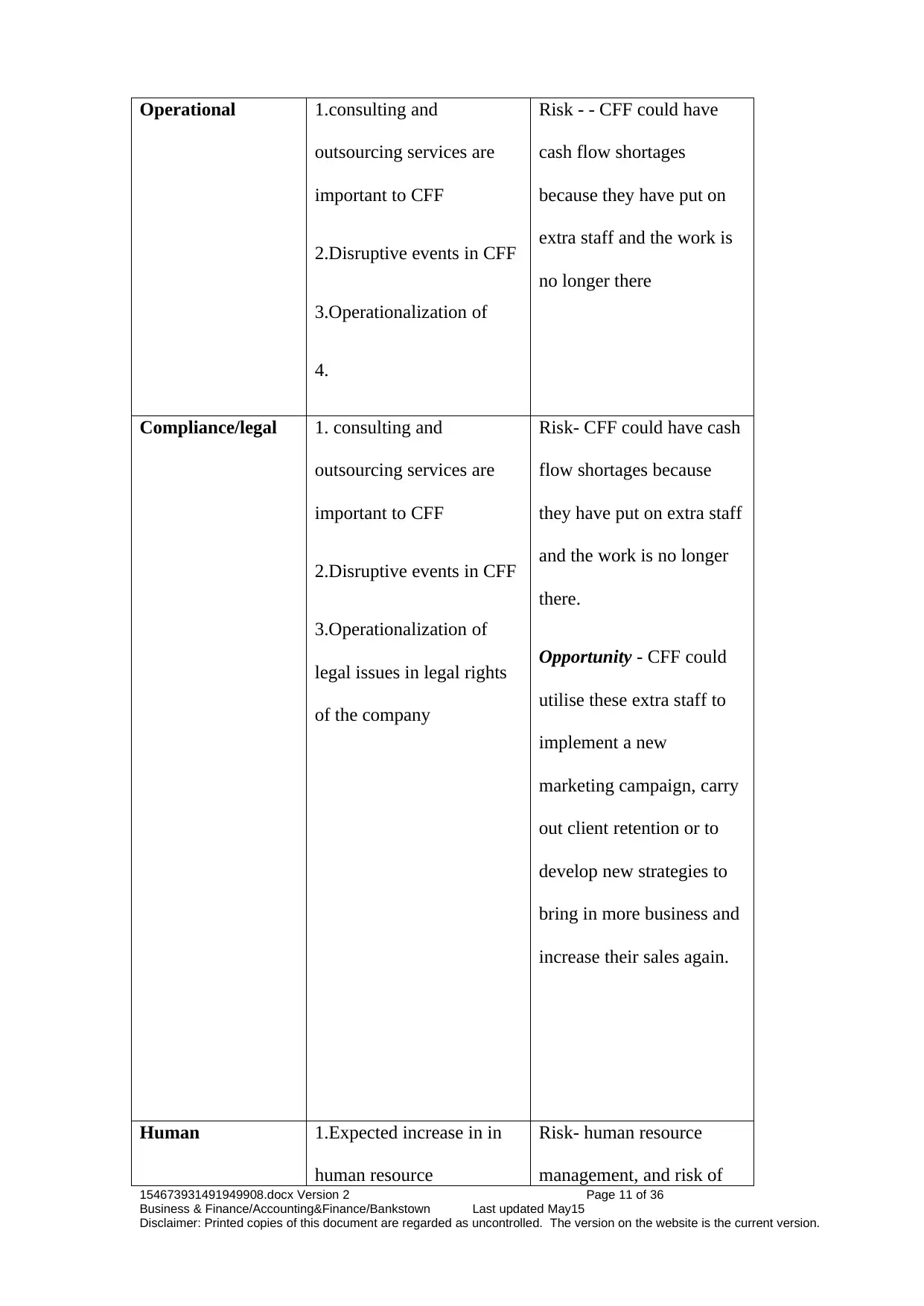

Operational 1.consulting and

outsourcing services are

important to CFF

2.Disruptive events in CFF

3.Operationalization of

4.

Risk - - CFF could have

cash flow shortages

because they have put on

extra staff and the work is

no longer there

Compliance/legal 1. consulting and

outsourcing services are

important to CFF

2.Disruptive events in CFF

3.Operationalization of

legal issues in legal rights

of the company

Risk- CFF could have cash

flow shortages because

they have put on extra staff

and the work is no longer

there.

Opportunity - CFF could

utilise these extra staff to

implement a new

marketing campaign, carry

out client retention or to

develop new strategies to

bring in more business and

increase their sales again.

Human 1.Expected increase in in

human resource

Risk- human resource

management, and risk of

154673931491949908.docx Version 2 Page 11 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

outsourcing services are

important to CFF

2.Disruptive events in CFF

3.Operationalization of

4.

Risk - - CFF could have

cash flow shortages

because they have put on

extra staff and the work is

no longer there

Compliance/legal 1. consulting and

outsourcing services are

important to CFF

2.Disruptive events in CFF

3.Operationalization of

legal issues in legal rights

of the company

Risk- CFF could have cash

flow shortages because

they have put on extra staff

and the work is no longer

there.

Opportunity - CFF could

utilise these extra staff to

implement a new

marketing campaign, carry

out client retention or to

develop new strategies to

bring in more business and

increase their sales again.

Human 1.Expected increase in in

human resource

Risk- human resource

management, and risk of

154673931491949908.docx Version 2 Page 11 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

management

2.

labour turnover.

Health & Safety 1.increased health and

safety

2

Risk- CFF could have cash

flow shortages because

they have put on extra staff

and the work is no longer

there.

Reputation 1.expected risk of

reputational damage

2

Risk- CFF could have cash

flow shortages because

they have put on extra staff

and the work is no longer

there.

154673931491949908.docx Version 2 Page 12 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

2.

labour turnover.

Health & Safety 1.increased health and

safety

2

Risk- CFF could have cash

flow shortages because

they have put on extra staff

and the work is no longer

there.

Reputation 1.expected risk of

reputational damage

2

Risk- CFF could have cash

flow shortages because

they have put on extra staff

and the work is no longer

there.

154673931491949908.docx Version 2 Page 12 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Question 3 – Analyse and evaluate risks

a) From the risks identified in question 2b) complete a risk register

(appendix 1) for the following risk categories:

1. Financial/economic

2. Operational

3. Compliance/legal

Example of what is required

What can happen? - again relate it to the scenario

Look at what may or may not happen in the business

Eg loans decrease

How can it happen

List how it might happen – eg the competitor may attract more loans from the new

development to his business

Identify existing controls

What has CFF done to identify this risk? Nothing/something?

Adequacy of existing controls?

154673931491949908.docx Version 2 Page 13 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

a) From the risks identified in question 2b) complete a risk register

(appendix 1) for the following risk categories:

1. Financial/economic

2. Operational

3. Compliance/legal

Example of what is required

What can happen? - again relate it to the scenario

Look at what may or may not happen in the business

Eg loans decrease

How can it happen

List how it might happen – eg the competitor may attract more loans from the new

development to his business

Identify existing controls

What has CFF done to identify this risk? Nothing/something?

Adequacy of existing controls?

154673931491949908.docx Version 2 Page 13 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

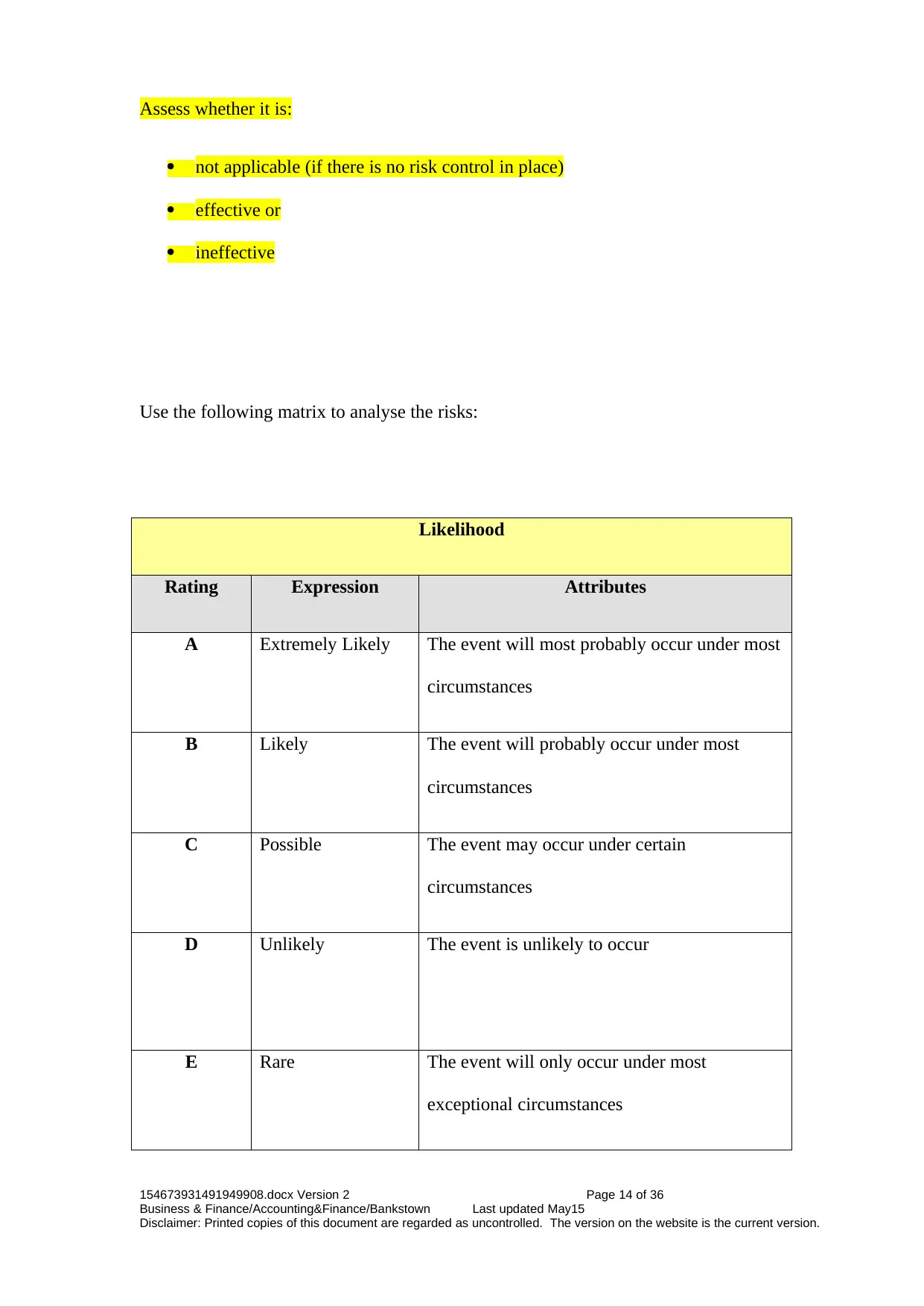

Assess whether it is:

not applicable (if there is no risk control in place)

effective or

ineffective

Use the following matrix to analyse the risks:

Likelihood

Rating Expression Attributes

A Extremely Likely The event will most probably occur under most

circumstances

B Likely The event will probably occur under most

circumstances

C Possible The event may occur under certain

circumstances

D Unlikely The event is unlikely to occur

E Rare The event will only occur under most

exceptional circumstances

154673931491949908.docx Version 2 Page 14 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

not applicable (if there is no risk control in place)

effective or

ineffective

Use the following matrix to analyse the risks:

Likelihood

Rating Expression Attributes

A Extremely Likely The event will most probably occur under most

circumstances

B Likely The event will probably occur under most

circumstances

C Possible The event may occur under certain

circumstances

D Unlikely The event is unlikely to occur

E Rare The event will only occur under most

exceptional circumstances

154673931491949908.docx Version 2 Page 14 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

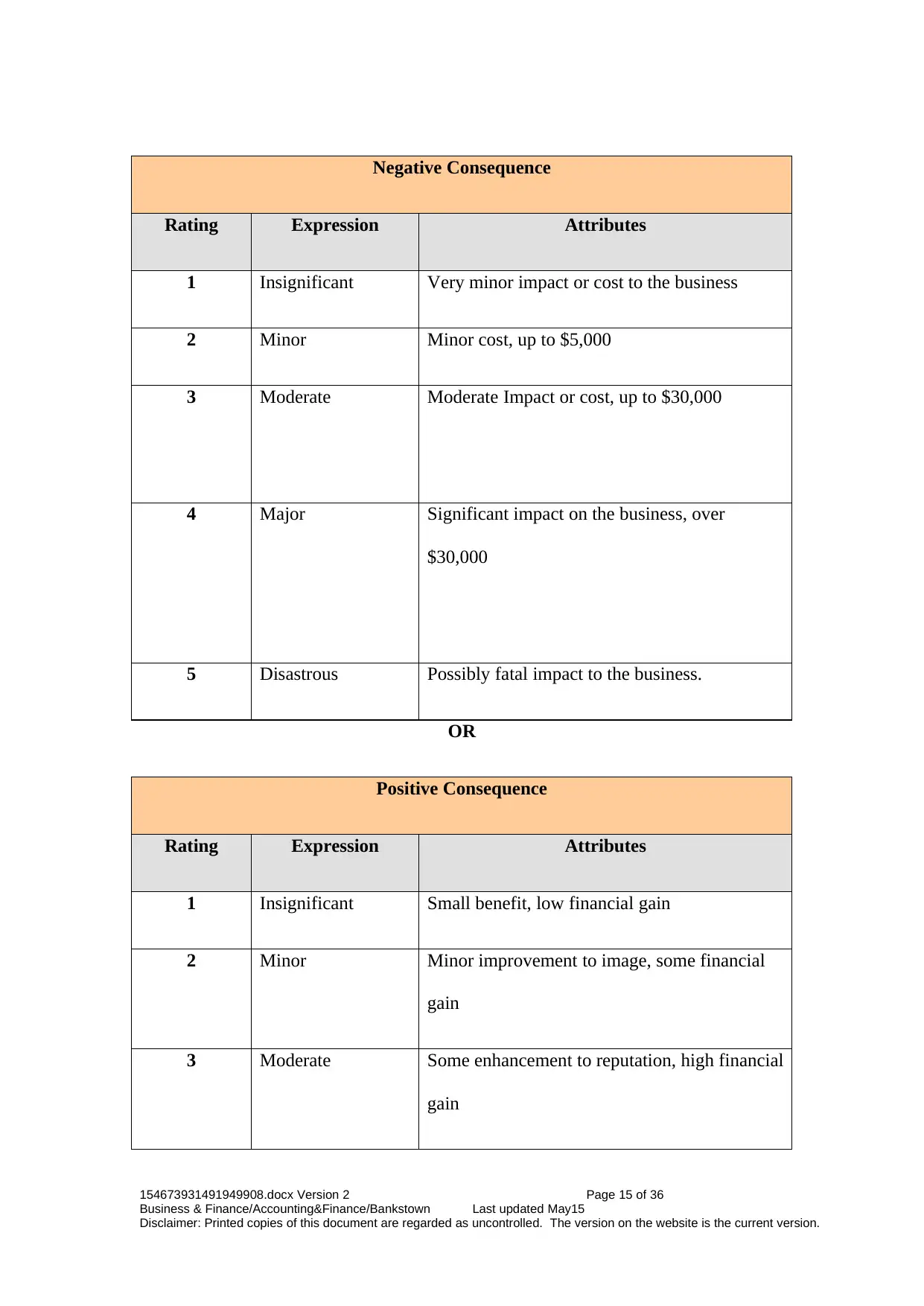

Negative Consequence

Rating Expression Attributes

1 Insignificant Very minor impact or cost to the business

2 Minor Minor cost, up to $5,000

3 Moderate Moderate Impact or cost, up to $30,000

4 Major Significant impact on the business, over

$30,000

5 Disastrous Possibly fatal impact to the business.

OR

Positive Consequence

Rating Expression Attributes

1 Insignificant Small benefit, low financial gain

2 Minor Minor improvement to image, some financial

gain

3 Moderate Some enhancement to reputation, high financial

gain

154673931491949908.docx Version 2 Page 15 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Rating Expression Attributes

1 Insignificant Very minor impact or cost to the business

2 Minor Minor cost, up to $5,000

3 Moderate Moderate Impact or cost, up to $30,000

4 Major Significant impact on the business, over

$30,000

5 Disastrous Possibly fatal impact to the business.

OR

Positive Consequence

Rating Expression Attributes

1 Insignificant Small benefit, low financial gain

2 Minor Minor improvement to image, some financial

gain

3 Moderate Some enhancement to reputation, high financial

gain

154673931491949908.docx Version 2 Page 15 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

4 Major Enhanced reputation, major financial gain

5 Significant Significantly enhanced reputation, high

financial gain

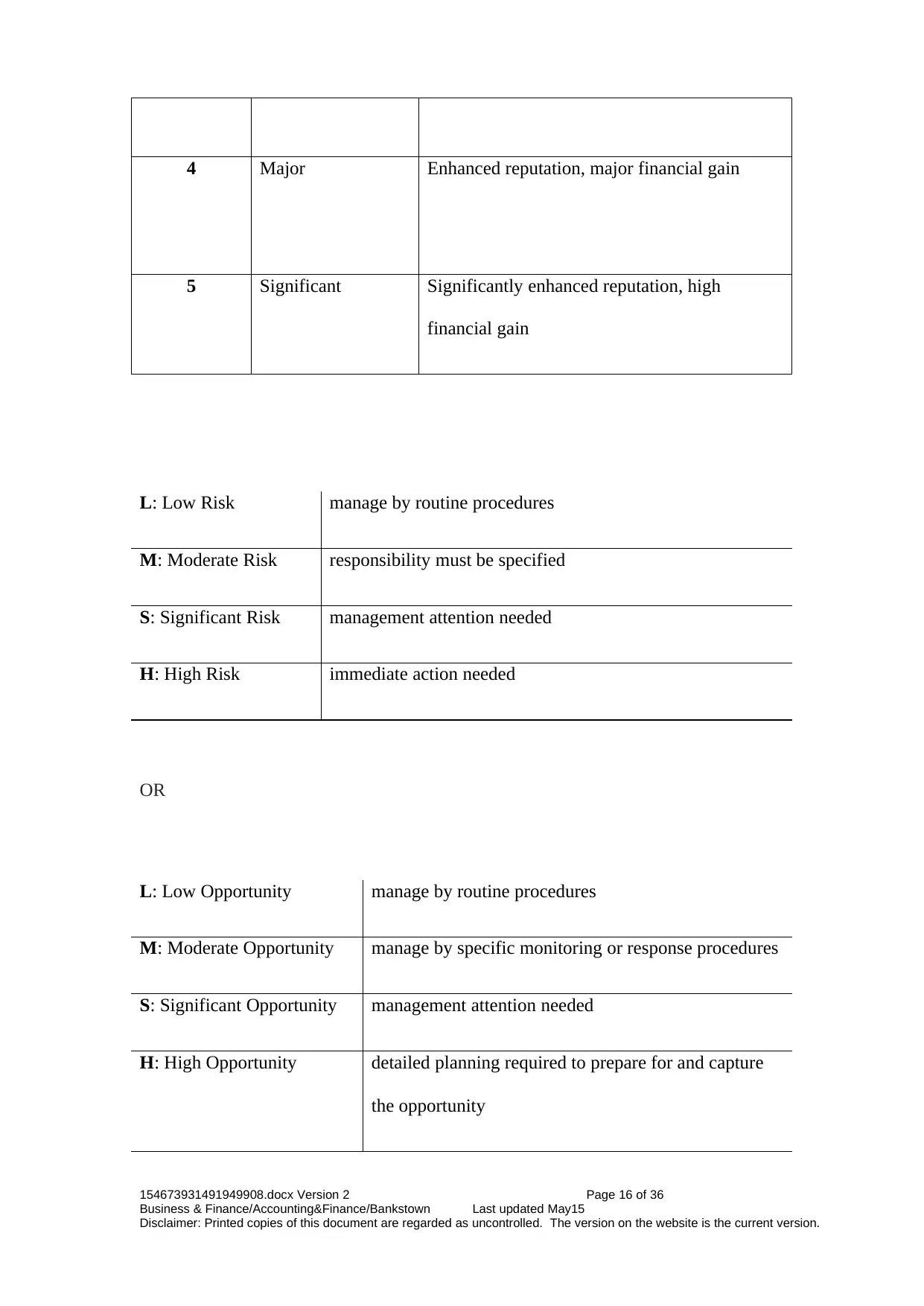

L: Low Risk manage by routine procedures

M: Moderate Risk responsibility must be specified

S: Significant Risk management attention needed

H: High Risk immediate action needed

OR

L: Low Opportunity manage by routine procedures

M: Moderate Opportunity manage by specific monitoring or response procedures

S: Significant Opportunity management attention needed

H: High Opportunity detailed planning required to prepare for and capture

the opportunity

154673931491949908.docx Version 2 Page 16 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

5 Significant Significantly enhanced reputation, high

financial gain

L: Low Risk manage by routine procedures

M: Moderate Risk responsibility must be specified

S: Significant Risk management attention needed

H: High Risk immediate action needed

OR

L: Low Opportunity manage by routine procedures

M: Moderate Opportunity manage by specific monitoring or response procedures

S: Significant Opportunity management attention needed

H: High Opportunity detailed planning required to prepare for and capture

the opportunity

154673931491949908.docx Version 2 Page 16 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

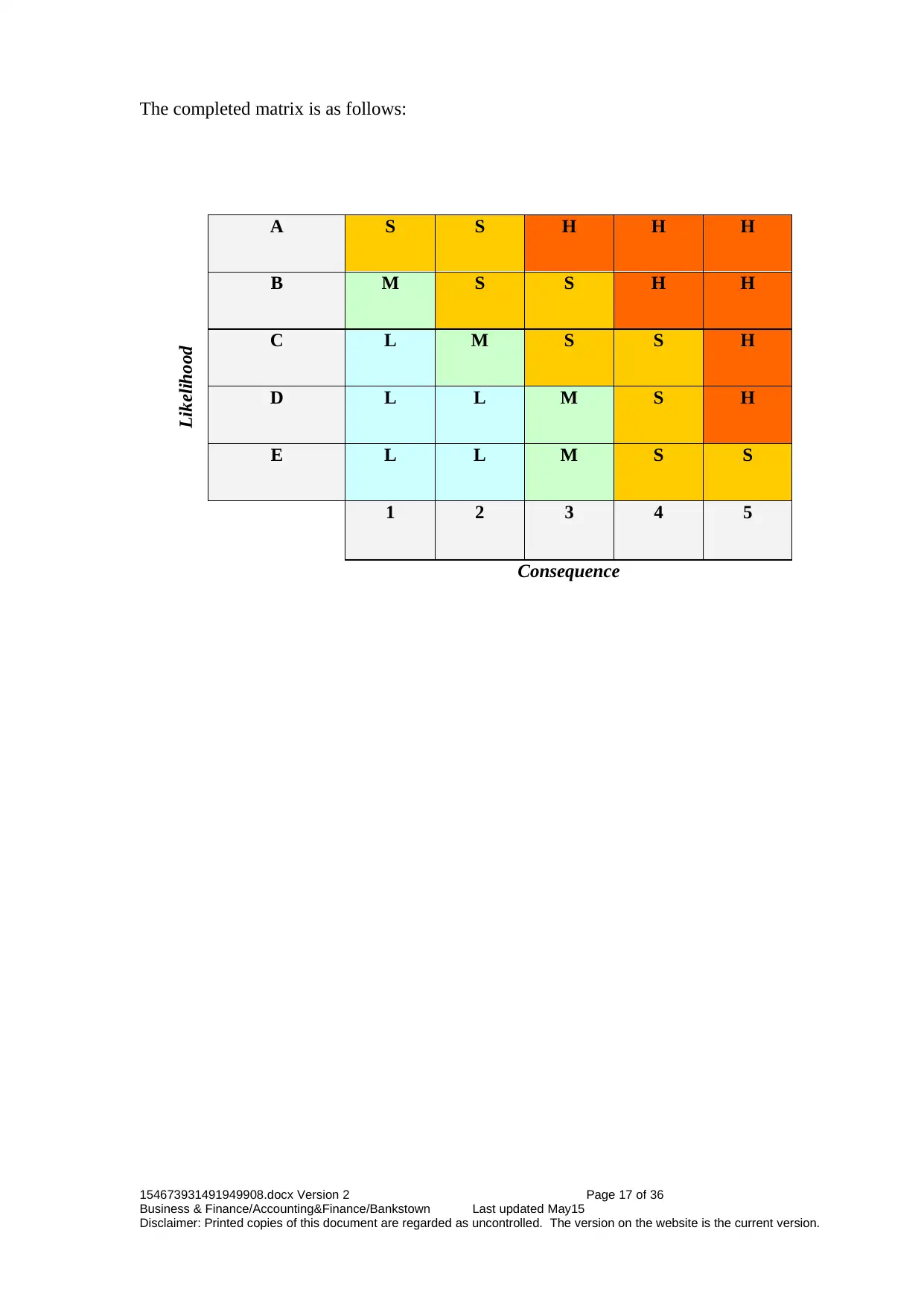

The completed matrix is as follows:

Likelihood

A S S H H H

B M S S H H

C L M S S H

D L L M S H

E L L M S S

1 2 3 4 5

Consequence

154673931491949908.docx Version 2 Page 17 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Likelihood

A S S H H H

B M S S H H

C L M S S H

D L L M S H

E L L M S S

1 2 3 4 5

Consequence

154673931491949908.docx Version 2 Page 17 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Question 4 – Treat risks

Using the risk register completed in question 3 complete a Risk Treatment Plan

(Risk Treatment section in appendix 2).

Note: the Monitor and Review section of appendix 2 will be completed in Q6 below.

Question 5 – Communicate and consult

To ensure that all stakeholders are kept informed complete a communication plan

(appendix 3).

Question 6 – Monitor and review

Part A:

154673931491949908.docx Version 2 Page 18 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Using the risk register completed in question 3 complete a Risk Treatment Plan

(Risk Treatment section in appendix 2).

Note: the Monitor and Review section of appendix 2 will be completed in Q6 below.

Question 5 – Communicate and consult

To ensure that all stakeholders are kept informed complete a communication plan

(appendix 3).

Question 6 – Monitor and review

Part A:

154673931491949908.docx Version 2 Page 18 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Complete the first 3 columns of the Monitor and Review section of appendix 2

using the risks identified in Question 4 and the communication plan devised in

Question 5 to ensure they are reviewed in terms of their required timing.

Part B:

Assume that 2 of your risk treatment plans did not achieve the Measures of Success

you developed in part A above (appendix 2).

(i) Record two hypothetical results in the Result column to reflect this

unsuccessfulness.

Hypothetical results

1. Financial risks will determine the level of profit or loss that the company

will make

2. Operational risk will raise the levels of operational efficiency in the

company

and

154673931491949908.docx Version 2 Page 19 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

using the risks identified in Question 4 and the communication plan devised in

Question 5 to ensure they are reviewed in terms of their required timing.

Part B:

Assume that 2 of your risk treatment plans did not achieve the Measures of Success

you developed in part A above (appendix 2).

(i) Record two hypothetical results in the Result column to reflect this

unsuccessfulness.

Hypothetical results

1. Financial risks will determine the level of profit or loss that the company

will make

2. Operational risk will raise the levels of operational efficiency in the

company

and

154673931491949908.docx Version 2 Page 19 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(ii) Recommend an option for improvement for both results in the Options for

Improvement column for all results recorded in (i) above

Option for improvement

1. Creating good financial structures that will be important in reducing

financial risks

2. Making a good operational system that involves the use of structures and

systems that are good to the company.

154673931491949908.docx Version 2 Page 20 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Improvement column for all results recorded in (i) above

Option for improvement

1. Creating good financial structures that will be important in reducing

financial risks

2. Making a good operational system that involves the use of structures and

systems that are good to the company.

154673931491949908.docx Version 2 Page 20 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

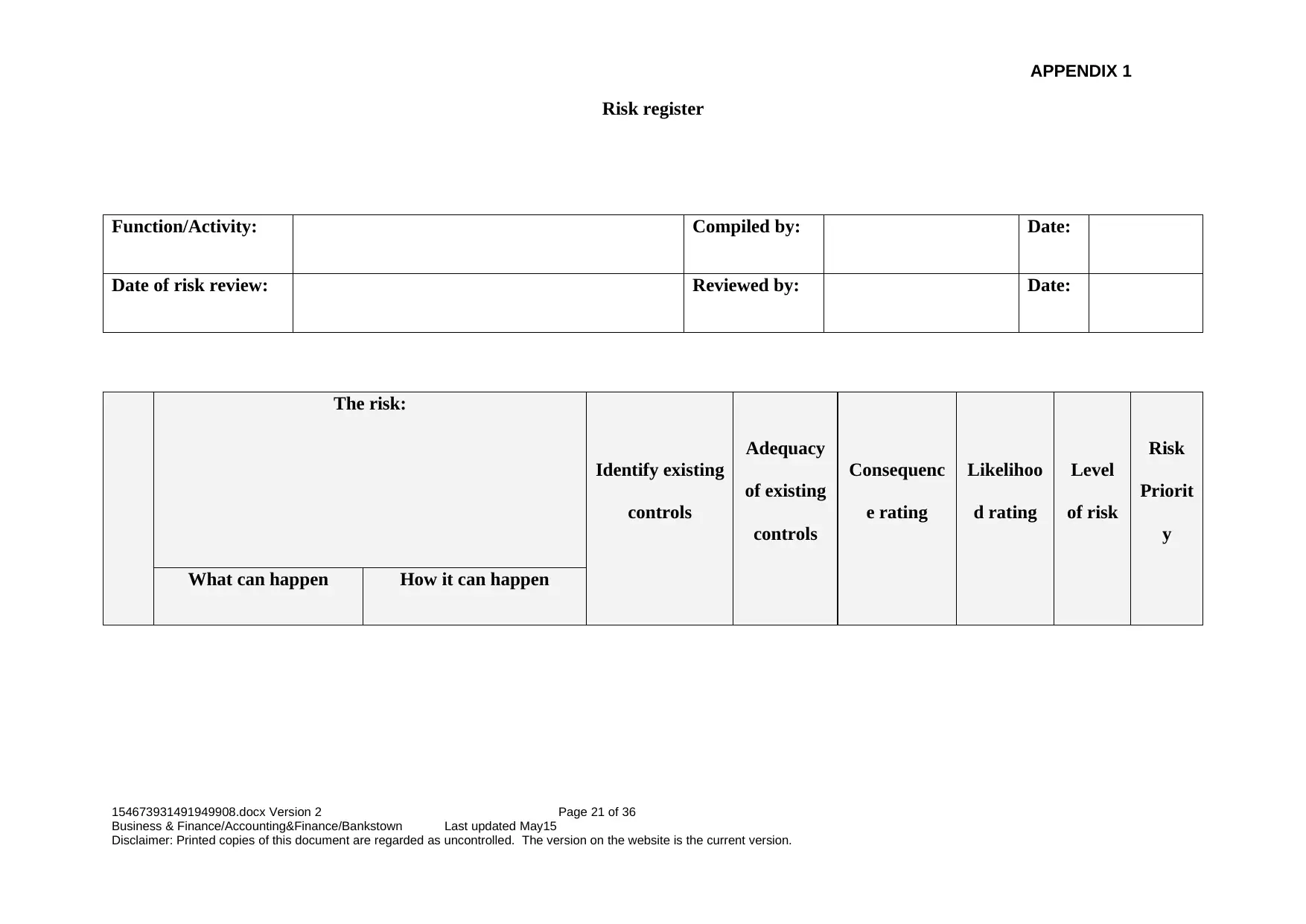

Risk register

Function/Activity: Compiled by: Date:

Date of risk review: Reviewed by: Date:

The risk:

Identify existing

controls

Adequacy

of existing

controls

Consequenc

e rating

Likelihoo

d rating

Level

of risk

Risk

Priorit

y

What can happen How it can happen

154673931491949908.docx Version 2 Page 21 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

APPENDIX 1

Function/Activity: Compiled by: Date:

Date of risk review: Reviewed by: Date:

The risk:

Identify existing

controls

Adequacy

of existing

controls

Consequenc

e rating

Likelihoo

d rating

Level

of risk

Risk

Priorit

y

What can happen How it can happen

154673931491949908.docx Version 2 Page 21 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

APPENDIX 1

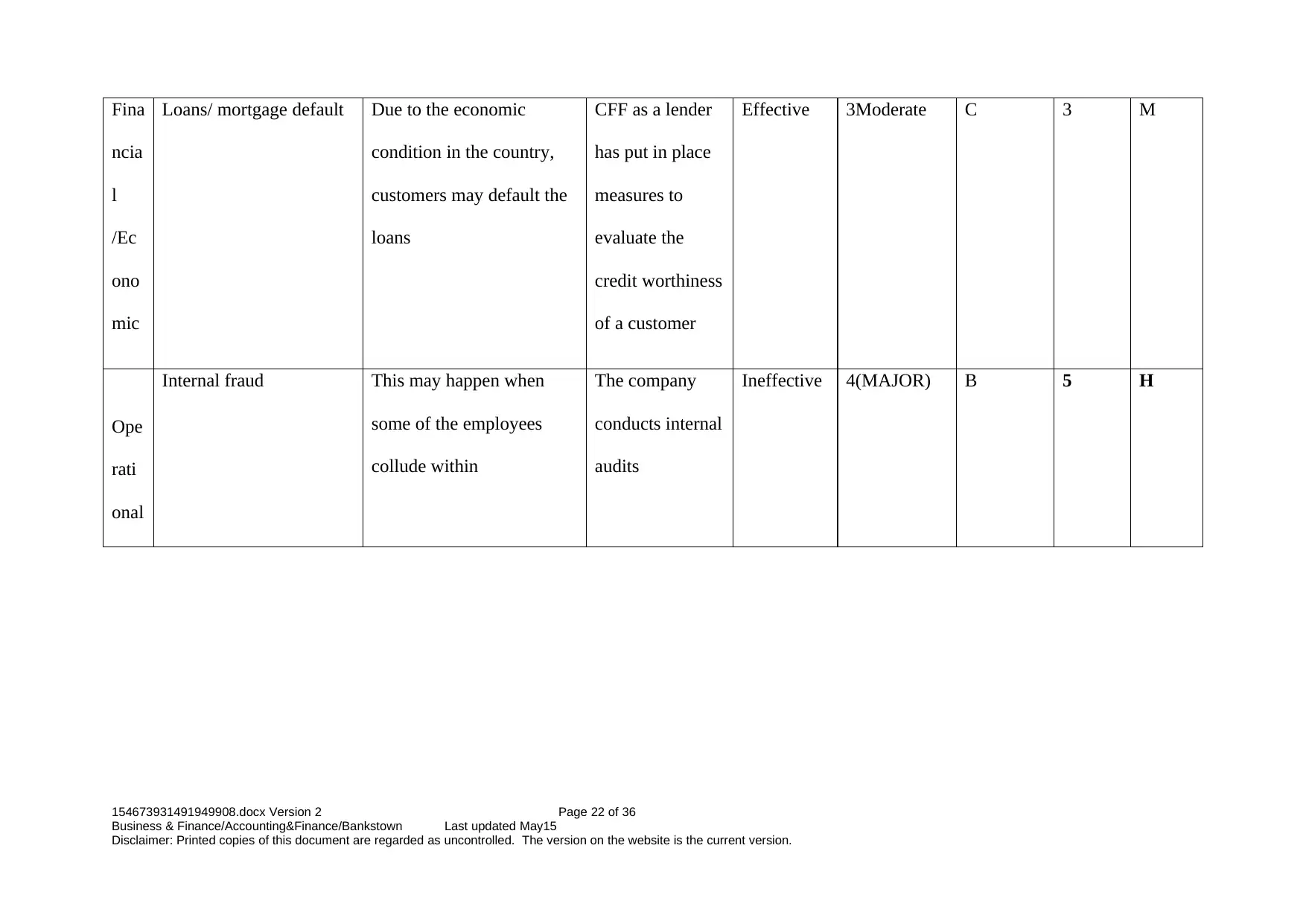

Fina

ncia

l

/Ec

ono

mic

Loans/ mortgage default Due to the economic

condition in the country,

customers may default the

loans

CFF as a lender

has put in place

measures to

evaluate the

credit worthiness

of a customer

Effective 3Moderate C 3 M

Ope

rati

onal

Internal fraud This may happen when

some of the employees

collude within

The company

conducts internal

audits

Ineffective 4(MAJOR) B 5 H

154673931491949908.docx Version 2 Page 22 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

ncia

l

/Ec

ono

mic

Loans/ mortgage default Due to the economic

condition in the country,

customers may default the

loans

CFF as a lender

has put in place

measures to

evaluate the

credit worthiness

of a customer

Effective 3Moderate C 3 M

Ope

rati

onal

Internal fraud This may happen when

some of the employees

collude within

The company

conducts internal

audits

Ineffective 4(MAJOR) B 5 H

154673931491949908.docx Version 2 Page 22 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

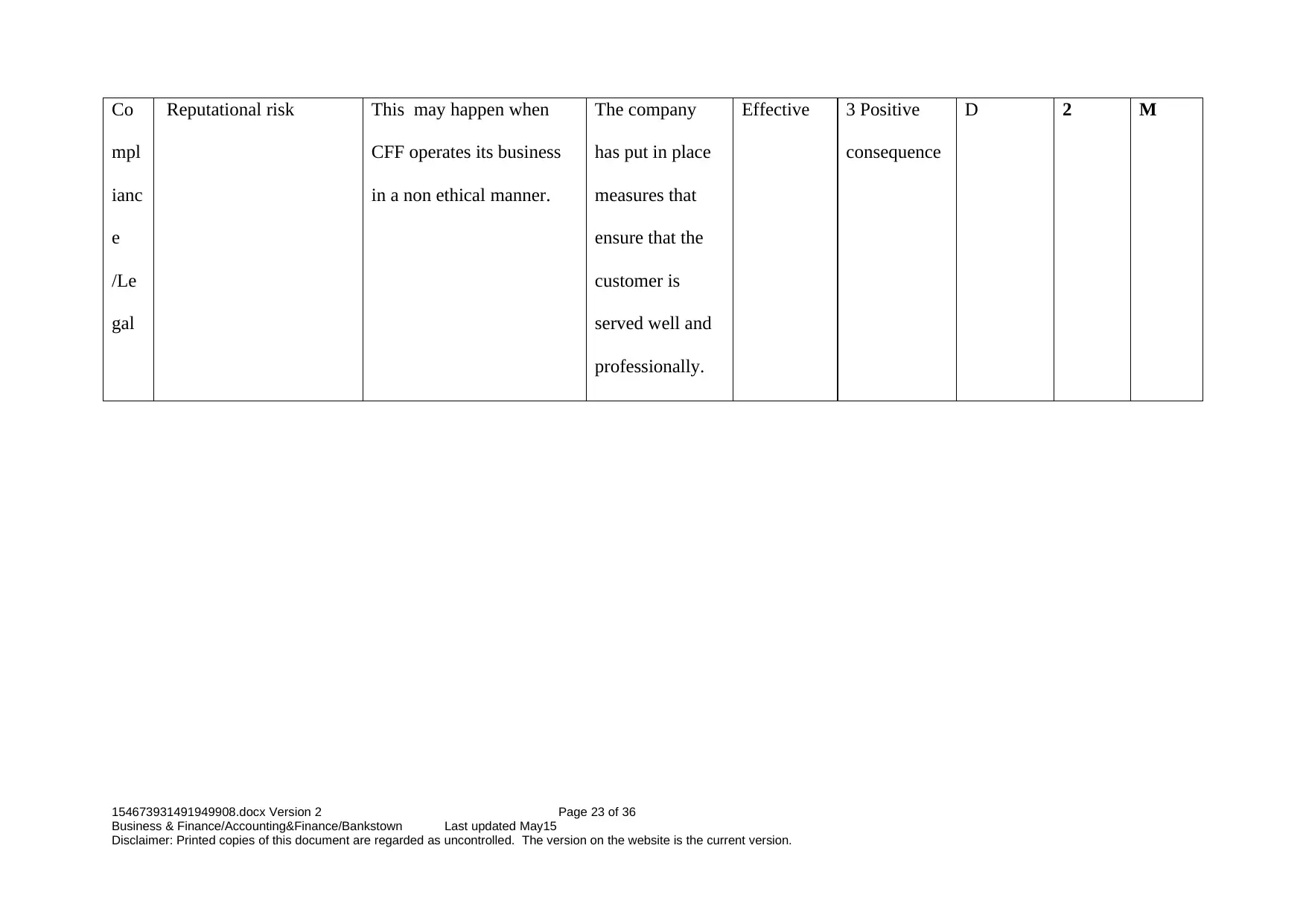

Co

mpl

ianc

e

/Le

gal

Reputational risk This may happen when

CFF operates its business

in a non ethical manner.

The company

has put in place

measures that

ensure that the

customer is

served well and

professionally.

Effective 3 Positive

consequence

D 2 M

154673931491949908.docx Version 2 Page 23 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

mpl

ianc

e

/Le

gal

Reputational risk This may happen when

CFF operates its business

in a non ethical manner.

The company

has put in place

measures that

ensure that the

customer is

served well and

professionally.

Effective 3 Positive

consequence

D 2 M

154673931491949908.docx Version 2 Page 23 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Extract of Risk Treatment Plan

Function/activity:

Risk Treatment Plan Monitor & Review

Risk

reference

Treatment

strategy

Resources

required

Responsible

person

Timing Monitoring

requirements

Review

completion

date

Measures of

success

Results Options for

improvement

Financial

risk

Creating

financial risk

mitigation

strategies

finances

Financial

risk manager

One

year

Financial

statements

12.12.2017 Profit or loss Profits Creating

financial risk

management

strategy

154673931491949908.docx Version 2 Page 24 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

APPENDIX 2

Function/activity:

Risk Treatment Plan Monitor & Review

Risk

reference

Treatment

strategy

Resources

required

Responsible

person

Timing Monitoring

requirements

Review

completion

date

Measures of

success

Results Options for

improvement

Financial

risk

Creating

financial risk

mitigation

strategies

finances

Financial

risk manager

One

year

Financial

statements

12.12.2017 Profit or loss Profits Creating

financial risk

management

strategy

154673931491949908.docx Version 2 Page 24 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

APPENDIX 2

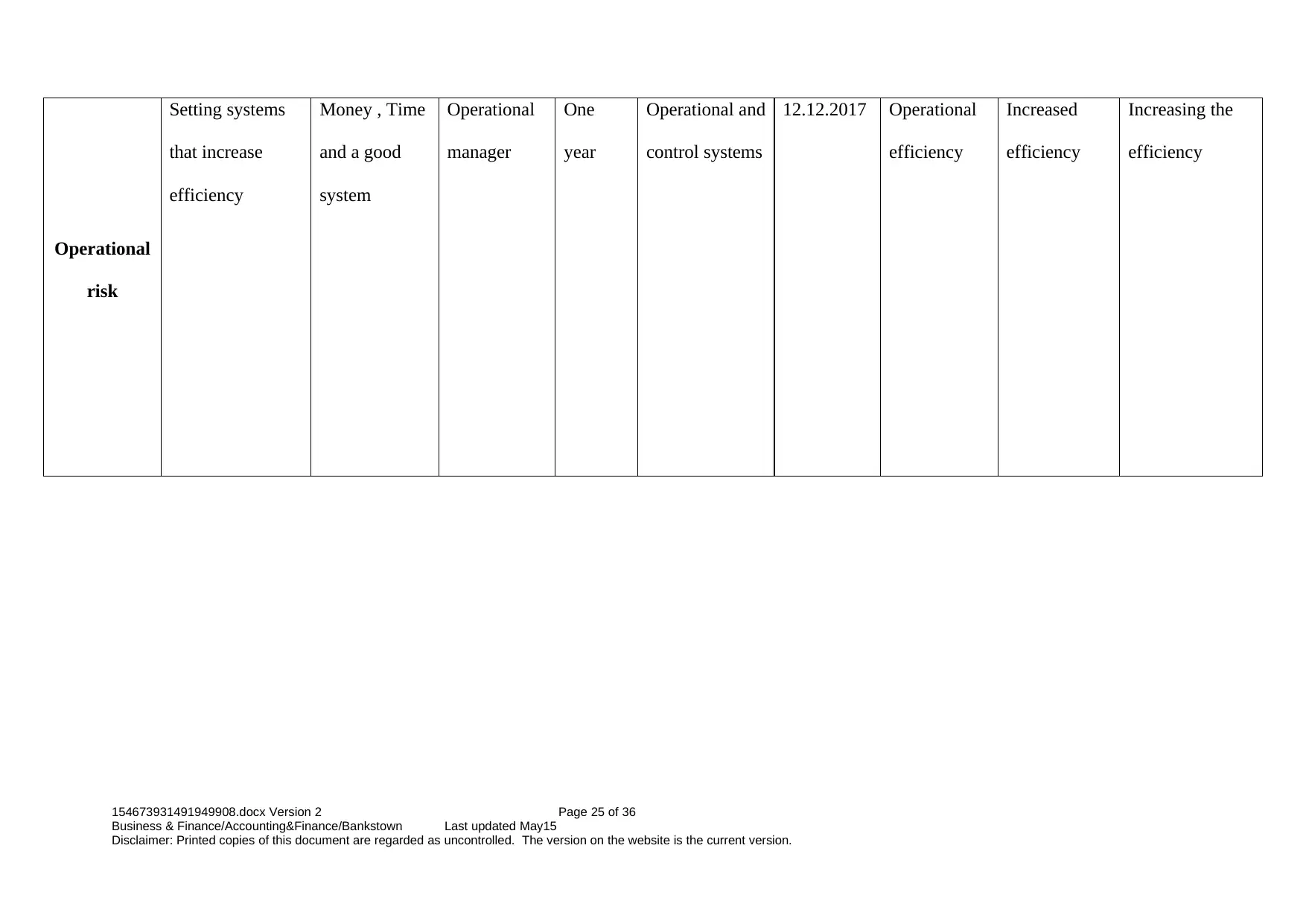

Operational

risk

Setting systems

that increase

efficiency

Money , Time

and a good

system

Operational

manager

One

year

Operational and

control systems

12.12.2017 Operational

efficiency

Increased

efficiency

Increasing the

efficiency

154673931491949908.docx Version 2 Page 25 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

risk

Setting systems

that increase

efficiency

Money , Time

and a good

system

Operational

manager

One

year

Operational and

control systems

12.12.2017 Operational

efficiency

Increased

efficiency

Increasing the

efficiency

154673931491949908.docx Version 2 Page 25 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

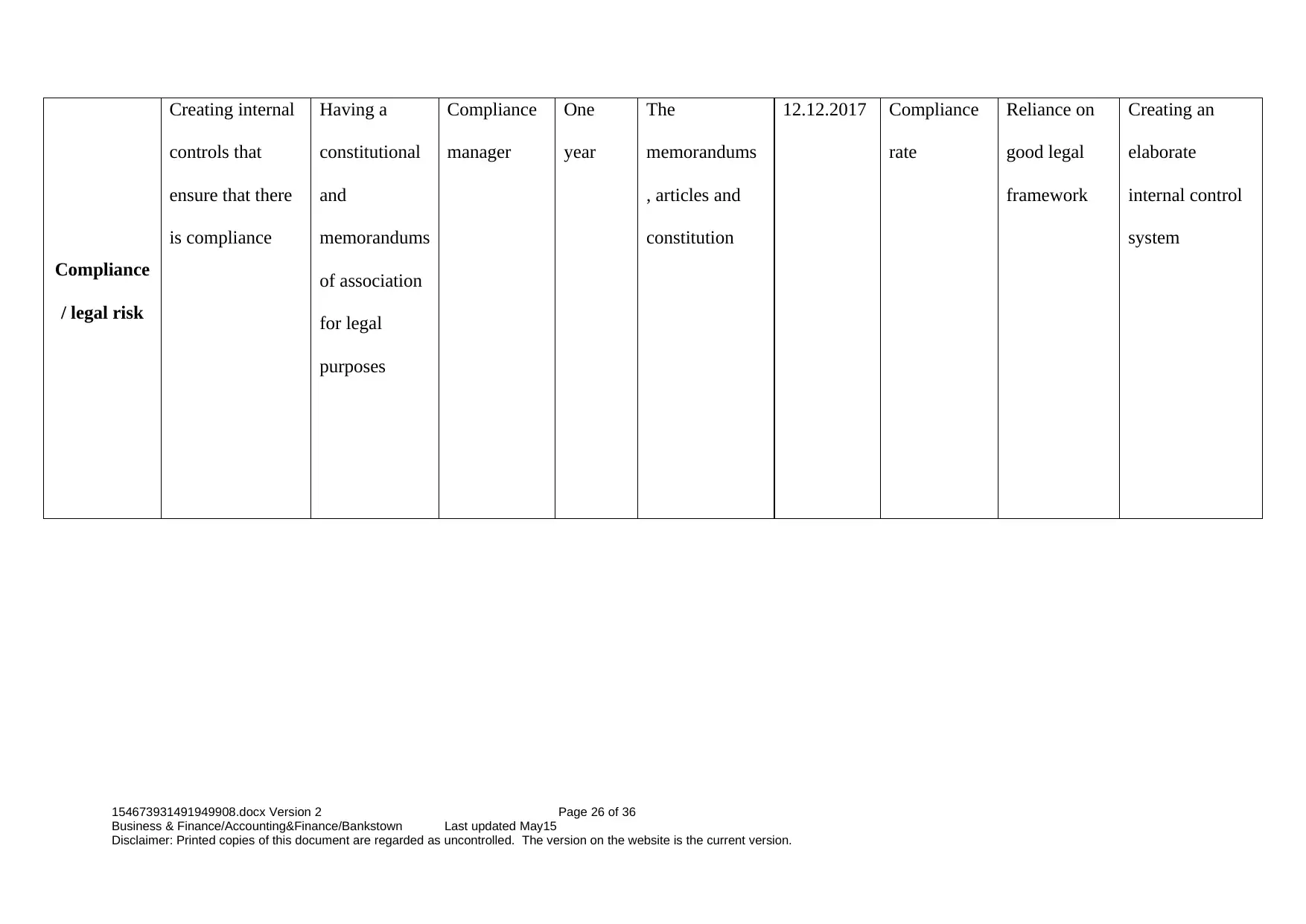

Compliance

/ legal risk

Creating internal

controls that

ensure that there

is compliance

Having a

constitutional

and

memorandums

of association

for legal

purposes

Compliance

manager

One

year

The

memorandums

, articles and

constitution

12.12.2017 Compliance

rate

Reliance on

good legal

framework

Creating an

elaborate

internal control

system

154673931491949908.docx Version 2 Page 26 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

/ legal risk

Creating internal

controls that

ensure that there

is compliance

Having a

constitutional

and

memorandums

of association

for legal

purposes

Compliance

manager

One

year

The

memorandums

, articles and

constitution

12.12.2017 Compliance

rate

Reliance on

good legal

framework

Creating an

elaborate

internal control

system

154673931491949908.docx Version 2 Page 26 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

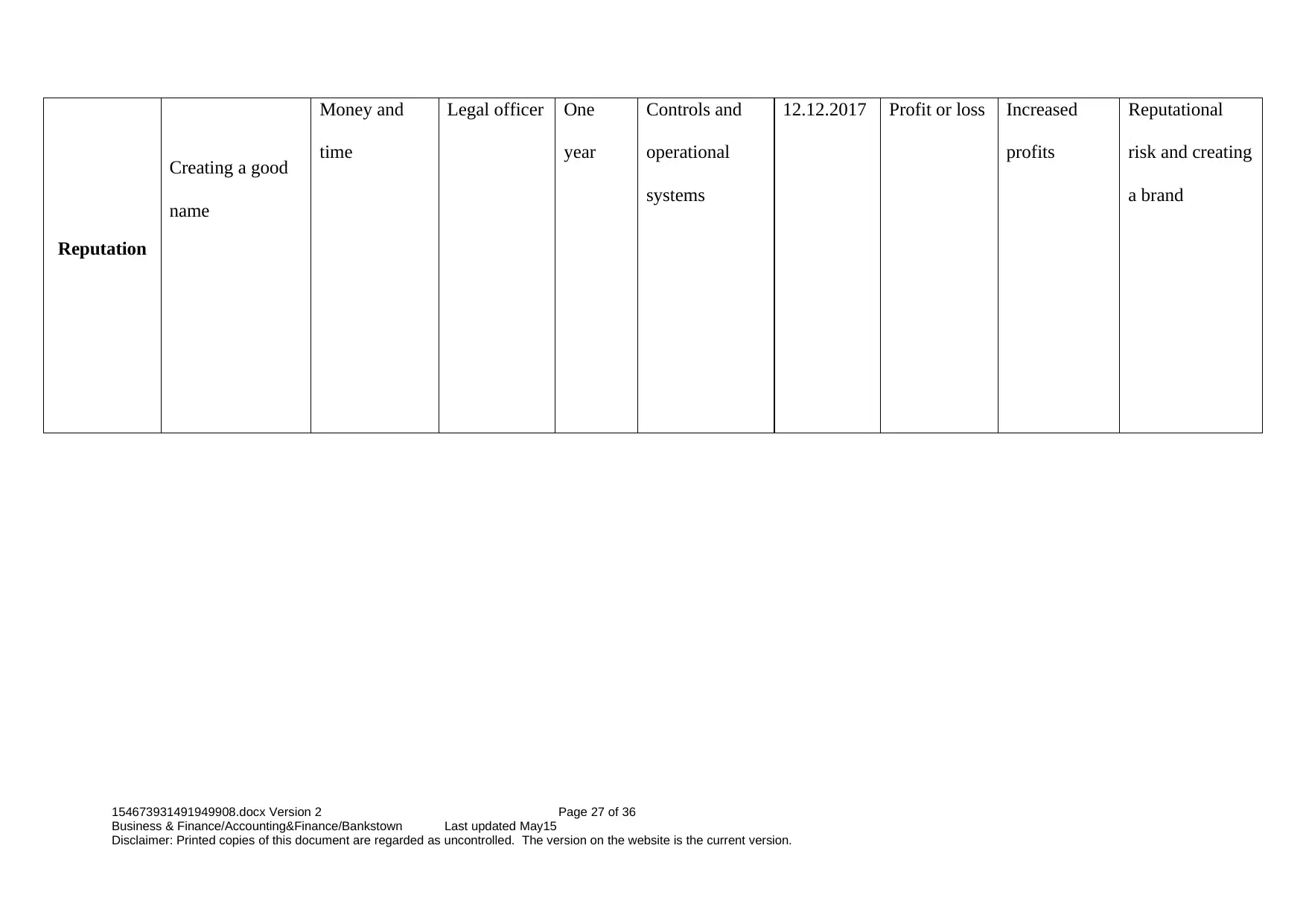

Reputation

Creating a good

name

Money and

time

Legal officer One

year

Controls and

operational

systems

12.12.2017 Profit or loss Increased

profits

Reputational

risk and creating

a brand

154673931491949908.docx Version 2 Page 27 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Creating a good

name

Money and

time

Legal officer One

year

Controls and

operational

systems

12.12.2017 Profit or loss Increased

profits

Reputational

risk and creating

a brand

154673931491949908.docx Version 2 Page 27 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

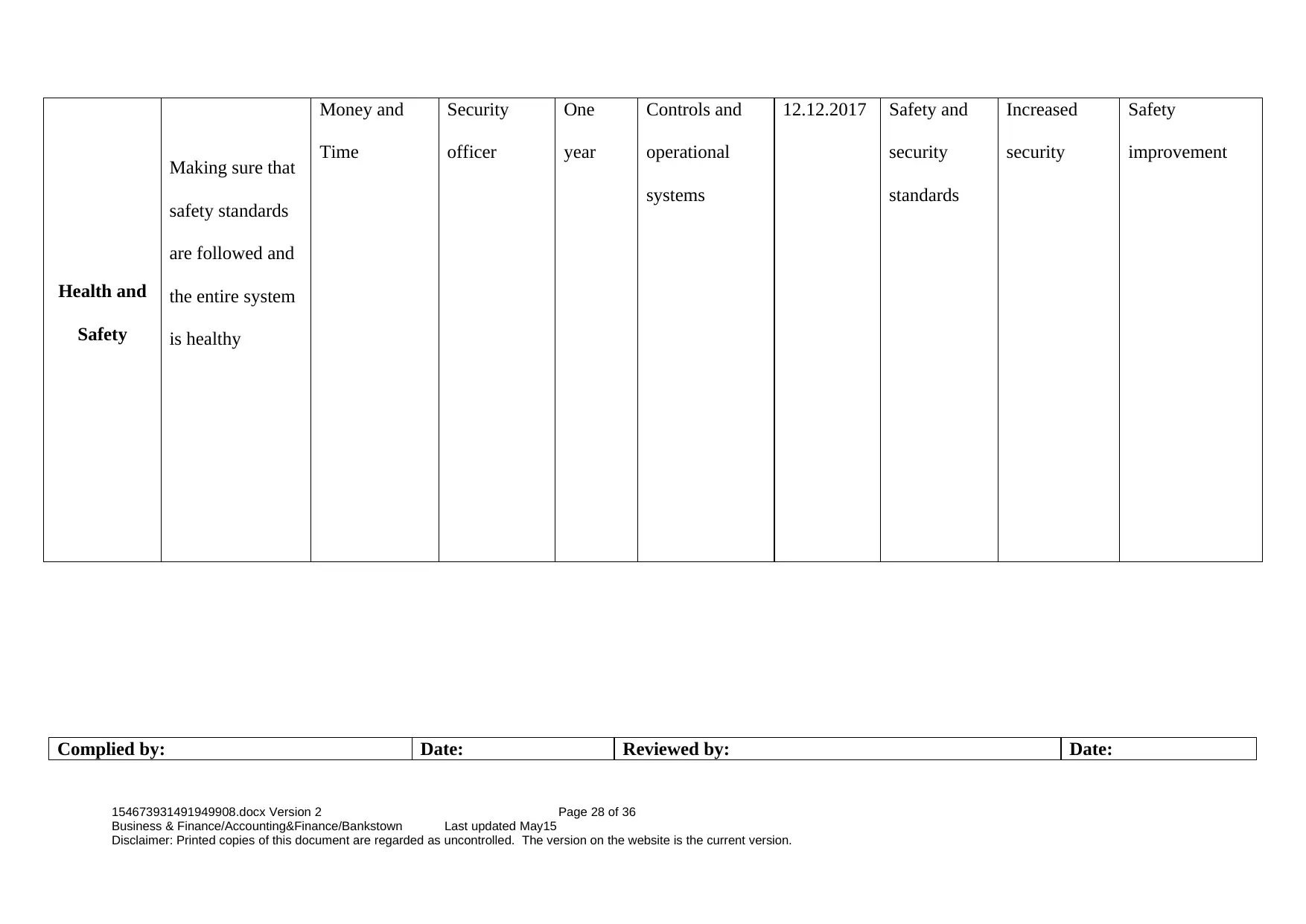

Health and

Safety

Making sure that

safety standards

are followed and

the entire system

is healthy

Money and

Time

Security

officer

One

year

Controls and

operational

systems

12.12.2017 Safety and

security

standards

Increased

security

Safety

improvement

Complied by: Date: Reviewed by: Date:

154673931491949908.docx Version 2 Page 28 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Safety

Making sure that

safety standards

are followed and

the entire system

is healthy

Money and

Time

Security

officer

One

year

Controls and

operational

systems

12.12.2017 Safety and

security

standards

Increased

security

Safety

improvement

Complied by: Date: Reviewed by: Date:

154673931491949908.docx Version 2 Page 28 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

154673931491949908.docx Version 2 Page 29 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

30

COMMUNICATION PLAN

Purpose

Who

Detail the relevant

audiences, include

internal and external

stakeholders

What

What information needs to

be communicated.

How

Communication method/s to

be used.

When

Ensure timing is accura

specific for each step in

risk management proce

154673931491949908.docx Version 2 Page 30 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

COMMUNICATION PLAN

Purpose

Who

Detail the relevant

audiences, include

internal and external

stakeholders

What

What information needs to

be communicated.

How

Communication method/s to

be used.

When

Ensure timing is accura

specific for each step in

risk management proce

154673931491949908.docx Version 2 Page 30 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

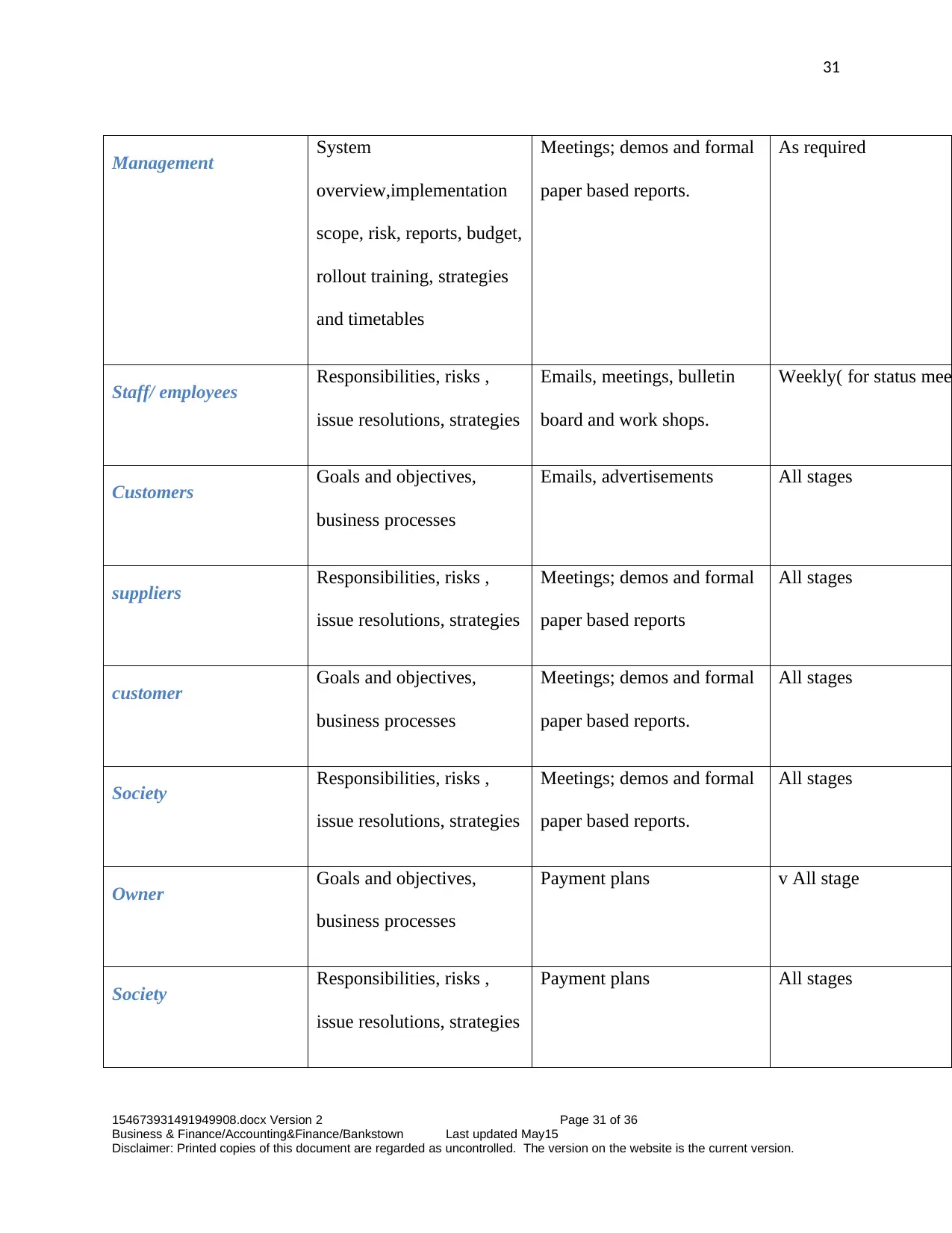

31

Management System

overview,implementation

scope, risk, reports, budget,

rollout training, strategies

and timetables

Meetings; demos and formal

paper based reports.

As required

Staff/ employees Responsibilities, risks ,

issue resolutions, strategies

Emails, meetings, bulletin

board and work shops.

Weekly( for status meet

Customers Goals and objectives,

business processes

Emails, advertisements All stages

suppliers Responsibilities, risks ,

issue resolutions, strategies

Meetings; demos and formal

paper based reports

All stages

customer Goals and objectives,

business processes

Meetings; demos and formal

paper based reports.

All stages

Society Responsibilities, risks ,

issue resolutions, strategies

Meetings; demos and formal

paper based reports.

All stages

Owner Goals and objectives,

business processes

Payment plans v All stage

Society Responsibilities, risks ,

issue resolutions, strategies

Payment plans All stages

154673931491949908.docx Version 2 Page 31 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Management System

overview,implementation

scope, risk, reports, budget,

rollout training, strategies

and timetables

Meetings; demos and formal

paper based reports.

As required

Staff/ employees Responsibilities, risks ,

issue resolutions, strategies

Emails, meetings, bulletin

board and work shops.

Weekly( for status meet

Customers Goals and objectives,

business processes

Emails, advertisements All stages

suppliers Responsibilities, risks ,

issue resolutions, strategies

Meetings; demos and formal

paper based reports

All stages

customer Goals and objectives,

business processes

Meetings; demos and formal

paper based reports.

All stages

Society Responsibilities, risks ,

issue resolutions, strategies

Meetings; demos and formal

paper based reports.

All stages

Owner Goals and objectives,

business processes

Payment plans v All stage

Society Responsibilities, risks ,

issue resolutions, strategies

Payment plans All stages

154673931491949908.docx Version 2 Page 31 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

32

Question 7

You are a mortgage broker at Thistown Brokers, Thistown. You do not hold an Australian

Financial Services (AFS) Licence. A prospective client calls into the office to discuss his

financial requirements. Adam Brody (the client) is interested in purchasing a house in Thistown

Heights. Adam recently sold his unit and will be living in the new property with his girlfriend

Rachel and dog Penny Lane. The property will be purchased in Adam’s name only. He has

$150,000 deposit towards the purchase and is seeking to borrow $400,000 to $450,000.

Adam works as a Sales Manager and earns $120,000 per annum. His fortnightly pay is deposited

direct to his transaction account. Adam is seeking a flexible product that does not have a fixed

interest rate. Under the FSRA a loan is not classified as a financial product.

After clarifying Adam’s situation and eligibility you have decided to recommend a standard

variable loan with FEDBANK. You outline the features and benefits of the product to him,

including the redraw facility. After considering these, Adam advises that he often has surplus

funds in his transaction account, however would prefer not to deposit these to the loan account in

case he needs the funds for other purposes. He often has a balance of $10,000 or more in the

154673931491949908.docx Version 2 Page 32 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

Question 7

You are a mortgage broker at Thistown Brokers, Thistown. You do not hold an Australian

Financial Services (AFS) Licence. A prospective client calls into the office to discuss his

financial requirements. Adam Brody (the client) is interested in purchasing a house in Thistown

Heights. Adam recently sold his unit and will be living in the new property with his girlfriend

Rachel and dog Penny Lane. The property will be purchased in Adam’s name only. He has

$150,000 deposit towards the purchase and is seeking to borrow $400,000 to $450,000.

Adam works as a Sales Manager and earns $120,000 per annum. His fortnightly pay is deposited

direct to his transaction account. Adam is seeking a flexible product that does not have a fixed

interest rate. Under the FSRA a loan is not classified as a financial product.

After clarifying Adam’s situation and eligibility you have decided to recommend a standard

variable loan with FEDBANK. You outline the features and benefits of the product to him,

including the redraw facility. After considering these, Adam advises that he often has surplus

funds in his transaction account, however would prefer not to deposit these to the loan account in

case he needs the funds for other purposes. He often has a balance of $10,000 or more in the

154673931491949908.docx Version 2 Page 32 of 36

Business & Finance/Accounting&Finance/Bankstown Last updated May15

Disclaimer: Printed copies of this document are regarded as uncontrolled. The version on the website is the current version.

1 out of 32

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.