Analyzing the Causes and Impacts of the 1997 Asian Financial Crisis

VerifiedAdded on 2021/06/30

|10

|2608

|81

Essay

AI Summary

The Asian Financial Crisis of 1997, or the Asian Contagion, initiated in Thailand due to currency devaluations and spread across East Asia, causing stock market crashes and economic turmoil. This essay explores the crisis's origins in asset bubbles, excessive borrowing, and vulnerabilities underestimated by foreign investors, highlighting policy shortcomings that were exposed as the crisis deepened. It examines the role of the IMF and the impact of devaluation on Asian economies, leading to the adoption of protectionist measures and business enterprise changes. The essay also delves into the lessons learned, including the dangers of asset bubbles and the importance of fiscal prudence, while also analyzing the role of the IMF and the critique of its policies. The crisis exposed the vulnerabilities of regional organizations and prompted discussions on international frameworks to control the global economy. The essay concludes by highlighting the recovery of affected countries and the re-emergence of Asia as a powerful investment destination.

1

Essay Topic: The Asian Crisis of 1997

Asian financial situation, sometimes known as "Asian Contagion." started a

series of monetary system devaluations or different occurrences in the season of 1997

that outspread across numerous Asian economies. The monetary system marketplace

first collapsed in Thailand as an outcome of the government's no longer desire to strap

the localized currency to the U.S. dollar (USD). Currency losses extended quickly

through East Asia, sparking stock market falls, lower import sales, or authority’s

turmoil in turn (Kalkavan, Hakan & Irfan Ersin).

The Asian financial crisis started with a series of asset bubbles, as did several

other financial problems before and after it. In the country's export markets, growth

has led to advanced levels of international direct investment, that has led to increasing

real estate prices, bolder business spending, or even major public substructure

projects. Most of the funding was provided by massive borrowing from banks.

The East Asian nations at the center of the recent recession have been revered

for years as some of the most promising emerging market economies owing to their

steady growth and the remarkable gains in the living conditions of their populations.

They have been widely used as templates for many other nations, with their generally

prudent monetary policy and vital private saving rates. No one could have foreseen

that one of the most significant financial crises of the post-war era could embroil these

nations unexpectedly (Climent, Francisco & Vicente Meneu).

Their popularity led to the underestimation of their inherent economic

vulnerabilities by foreign investors. In part, because of the large-scale capital inflows

encouraged by their economic development, advanced production has also been

placed on policies and institutions, in particular those that protect the banking

Essay Topic: The Asian Crisis of 1997

Asian financial situation, sometimes known as "Asian Contagion." started a

series of monetary system devaluations or different occurrences in the season of 1997

that outspread across numerous Asian economies. The monetary system marketplace

first collapsed in Thailand as an outcome of the government's no longer desire to strap

the localized currency to the U.S. dollar (USD). Currency losses extended quickly

through East Asia, sparking stock market falls, lower import sales, or authority’s

turmoil in turn (Kalkavan, Hakan & Irfan Ersin).

The Asian financial crisis started with a series of asset bubbles, as did several

other financial problems before and after it. In the country's export markets, growth

has led to advanced levels of international direct investment, that has led to increasing

real estate prices, bolder business spending, or even major public substructure

projects. Most of the funding was provided by massive borrowing from banks.

The East Asian nations at the center of the recent recession have been revered

for years as some of the most promising emerging market economies owing to their

steady growth and the remarkable gains in the living conditions of their populations.

They have been widely used as templates for many other nations, with their generally

prudent monetary policy and vital private saving rates. No one could have foreseen

that one of the most significant financial crises of the post-war era could embroil these

nations unexpectedly (Climent, Francisco & Vicente Meneu).

Their popularity led to the underestimation of their inherent economic

vulnerabilities by foreign investors. In part, because of the large-scale capital inflows

encouraged by their economic development, advanced production has also been

placed on policies and institutions, in particular those that protect the banking

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

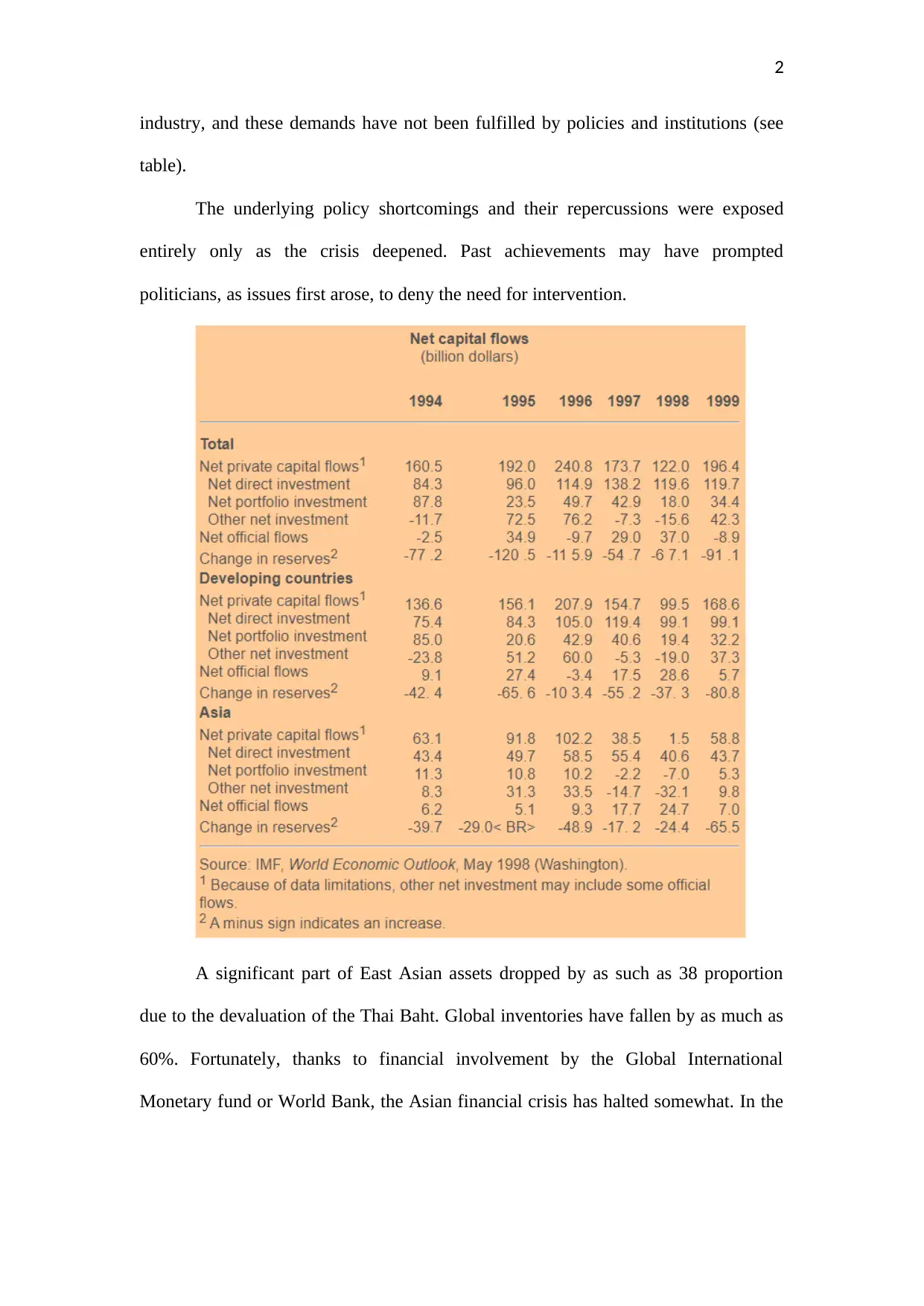

industry, and these demands have not been fulfilled by policies and institutions (see

table).

The underlying policy shortcomings and their repercussions were exposed

entirely only as the crisis deepened. Past achievements may have prompted

politicians, as issues first arose, to deny the need for intervention.

A significant part of East Asian assets dropped by as such as 38 proportion

due to the devaluation of the Thai Baht. Global inventories have fallen by as much as

60%. Fortunately, thanks to financial involvement by the Global International

Monetary fund or World Bank, the Asian financial crisis has halted somewhat. In the

industry, and these demands have not been fulfilled by policies and institutions (see

table).

The underlying policy shortcomings and their repercussions were exposed

entirely only as the crisis deepened. Past achievements may have prompted

politicians, as issues first arose, to deny the need for intervention.

A significant part of East Asian assets dropped by as such as 38 proportion

due to the devaluation of the Thai Baht. Global inventories have fallen by as much as

60%. Fortunately, thanks to financial involvement by the Global International

Monetary fund or World Bank, the Asian financial crisis has halted somewhat. In the

3

United States, Europe, and Russia, however when the Asian markets crashed, the

company losses were already felt.

As a result of the recession, protectionist measures have been adopted by

many nations to guarantee the stableness of their medium of exchange This has also

led to huge U.S. treasury transactions, that are used as multinational portfolios for

many of the worldwide governments, medium of exchange institutions, and leading

banks. The Asian crisis has diode to some necessary dependent on business enterprise

changes in nations like Thailand, South Korea, Japan, and Indonesia. Its further

functions as a helpful report for the economists attempting to understand today's

intertwined economies, especially in terms of currency trade and national accounts

management.

There were many threads embedded in the recession of commercial enterprise,

environmental, monetary phenomena. Put simply, all of these correlates to the

produce economic growth policy implemented over the years major up to the

situation, through rising East Asian economic system. This policy considers strong

government coordination with commercial enterprise of export goods, regard

discounts, lucrative financial transactions, and a medium of exchange peg to the U.S.

dollar, to guarantee a transaction rate beneficial to trade good.

This has goodness East Asia's flourishing industries, there have also been

some risks involved. The formal and informal government ensures that domestic

companies and banks are bailed out; comfortable relationships among East Asian

corporation, commercial banks and controller; and the cleaning of international

financial outflows with little regard to future threats have all lend significantly to a

huge moral danger in Asian countries (Jeon & Bang Nam).

United States, Europe, and Russia, however when the Asian markets crashed, the

company losses were already felt.

As a result of the recession, protectionist measures have been adopted by

many nations to guarantee the stableness of their medium of exchange This has also

led to huge U.S. treasury transactions, that are used as multinational portfolios for

many of the worldwide governments, medium of exchange institutions, and leading

banks. The Asian crisis has diode to some necessary dependent on business enterprise

changes in nations like Thailand, South Korea, Japan, and Indonesia. Its further

functions as a helpful report for the economists attempting to understand today's

intertwined economies, especially in terms of currency trade and national accounts

management.

There were many threads embedded in the recession of commercial enterprise,

environmental, monetary phenomena. Put simply, all of these correlates to the

produce economic growth policy implemented over the years major up to the

situation, through rising East Asian economic system. This policy considers strong

government coordination with commercial enterprise of export goods, regard

discounts, lucrative financial transactions, and a medium of exchange peg to the U.S.

dollar, to guarantee a transaction rate beneficial to trade good.

This has goodness East Asia's flourishing industries, there have also been

some risks involved. The formal and informal government ensures that domestic

companies and banks are bailed out; comfortable relationships among East Asian

corporation, commercial banks and controller; and the cleaning of international

financial outflows with little regard to future threats have all lend significantly to a

huge moral danger in Asian countries (Jeon & Bang Nam).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

The U.S. Governments, Europe and Asia agreed to organize the termination of

the Plaza Accord in 1995 in order to allow the U.S. dollar to appreciate relative to the

yen or the Deutsche Mark. As Japanese and German exports became more and more

competitive with other East Asian exports, it also meant the stabilization of East

Asian currencies pegged to the U.S. dollar, which contributed to substantial financial

pressures accumulating in those economies. Exports declined, and company profits

decreased. For East Asian governments and associated financial institutions,

borrowing U.S. dollars to subsidize their domestic producers and maintain their

currency pegs has been highly troublesome. These tensions came to a head in 1997

when they left their pegs one after another and devalued their exchange rates.

As mentioned earlier, the IMF interfered by offering debt to support the Asian

economies, also notable as "tiger economies." Thailand, Indonesia, and South Korea

have been issued nearly $110 billion in short-run loans to strengthen their economies.

Strict requirements, including higher tax increases and decreased public spending, had

to be met in exchange. By 1999, numerous of the impacted nations were starting to

show mark of recovery.

Many of the lessons learned from the Asian financial crisis can also be

extended to existing conditions and can still be used in the future to help alleviate

issues. Second, investors should be wary about asset bubbles, some of which may end

up collapsing, if they do, leaving investors in the lurch. For policymakers to keep an

eye on spending, another potential lesson is. The asset bubbles that sparked this crisis

may have led to any capital investment dictated by the government, and the same can

also be said of any potential incidents (Somanath, 2011).

Over the past two years from the beginning of 2015 to the second quarter of

2016, financial stocks have fluctuated dramatically. This caused the Federal Reserve

The U.S. Governments, Europe and Asia agreed to organize the termination of

the Plaza Accord in 1995 in order to allow the U.S. dollar to appreciate relative to the

yen or the Deutsche Mark. As Japanese and German exports became more and more

competitive with other East Asian exports, it also meant the stabilization of East

Asian currencies pegged to the U.S. dollar, which contributed to substantial financial

pressures accumulating in those economies. Exports declined, and company profits

decreased. For East Asian governments and associated financial institutions,

borrowing U.S. dollars to subsidize their domestic producers and maintain their

currency pegs has been highly troublesome. These tensions came to a head in 1997

when they left their pegs one after another and devalued their exchange rates.

As mentioned earlier, the IMF interfered by offering debt to support the Asian

economies, also notable as "tiger economies." Thailand, Indonesia, and South Korea

have been issued nearly $110 billion in short-run loans to strengthen their economies.

Strict requirements, including higher tax increases and decreased public spending, had

to be met in exchange. By 1999, numerous of the impacted nations were starting to

show mark of recovery.

Many of the lessons learned from the Asian financial crisis can also be

extended to existing conditions and can still be used in the future to help alleviate

issues. Second, investors should be wary about asset bubbles, some of which may end

up collapsing, if they do, leaving investors in the lurch. For policymakers to keep an

eye on spending, another potential lesson is. The asset bubbles that sparked this crisis

may have led to any capital investment dictated by the government, and the same can

also be said of any potential incidents (Somanath, 2011).

Over the past two years from the beginning of 2015 to the second quarter of

2016, financial stocks have fluctuated dramatically. This caused the Federal Reserve

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

to think about the risk of a second financial crash in Asia. On August 11, 2015, China

sent a shockwave across the capital markets in the United States when it depreciated

the yuan against the USD. This triggered the exit of the Chinese economy, leading to

lower domestic interest rates and a wide float of securities.

Other Asian countries have been motivated by China's low interest rates to

decrease their domestic interest rates. For instance, in early 2016, Japan decreased its

already low short-term interest rates to harmful levels. This extended period of low

interest rates has encouraged Japan to lend more and more funds to invest in

worldwide financial markets. By increasing value, making Japanese exports more

costly, and further undermining the economy, the Japanese yen reacted intuitively.

With a collapse of 11.5% from January 1 to February 11, 2016, the U.S.

capital markets responded. Although shares gradually rebounded by 13% in the next

year, instability continued throughout 2016 until the consequences of this crisis fully

dissipated (Cheng & Tun‐jen).

For the most part, the common belief that IMF prescriptions did more harm

than good cantered particular emphasis on the IMF and other structures for global

governance. The IMF was blamed for a "one size fits all" policy, which uncritically

reapplied drugs tailored for Latin America to East Asia, as well as its intrusive and

uncompromising conditionality. In East Asia, fiscal austerity policies have been

criticized for being particularly inappropriate and for prolonging and intensifying

economic and political crises. In addition to questioning the technical merits of the

IMF's policies, the policies of the IMF and the overall lack of accountability in its

decision-making have also been criticized. The small participation of East Asia in the

IMF and the World Bank has underlined the impotence of the impacted economies

to think about the risk of a second financial crash in Asia. On August 11, 2015, China

sent a shockwave across the capital markets in the United States when it depreciated

the yuan against the USD. This triggered the exit of the Chinese economy, leading to

lower domestic interest rates and a wide float of securities.

Other Asian countries have been motivated by China's low interest rates to

decrease their domestic interest rates. For instance, in early 2016, Japan decreased its

already low short-term interest rates to harmful levels. This extended period of low

interest rates has encouraged Japan to lend more and more funds to invest in

worldwide financial markets. By increasing value, making Japanese exports more

costly, and further undermining the economy, the Japanese yen reacted intuitively.

With a collapse of 11.5% from January 1 to February 11, 2016, the U.S.

capital markets responded. Although shares gradually rebounded by 13% in the next

year, instability continued throughout 2016 until the consequences of this crisis fully

dissipated (Cheng & Tun‐jen).

For the most part, the common belief that IMF prescriptions did more harm

than good cantered particular emphasis on the IMF and other structures for global

governance. The IMF was blamed for a "one size fits all" policy, which uncritically

reapplied drugs tailored for Latin America to East Asia, as well as its intrusive and

uncompromising conditionality. In East Asia, fiscal austerity policies have been

criticized for being particularly inappropriate and for prolonging and intensifying

economic and political crises. In addition to questioning the technical merits of the

IMF's policies, the policies of the IMF and the overall lack of accountability in its

decision-making have also been criticized. The small participation of East Asia in the

IMF and the World Bank has underlined the impotence of the impacted economies

6

and their lack of access to the existing provisions of global governance. The

accumulated critique of the IMF has undermined the legitimacy, if not the authority,

of the IMF, and has contributed to intensified demands for a new international

framework to control the global economy. Indonesia, Korea, and Thailand, three of

the country’s most seriously affected by the crisis, were called in to provide financial

aid to the IMF. To address the problem, there were three main components of the

plan:

IMF financial support of some US$35 billion was given for change and reform

programs in Indonesia, Korea, and Thailand, with assistance to Indonesia being

further expanded in 1998-99. Other multilateral and bilateral outlets have pledged

around US$85 billion in aid, but not all of this funding has fully materialized. In

addition, the proactive effort was taken to curb private capital outflows (at varying

points since the launch of these projects, in separate countries).

Monetary policy was reinforced (in separate countries at various times to

avoid the decline in the exchange rates of the countries, which went way beyond what

the fundamentals might have required, and to discourage currency deflation from

leading to an inflation cycle and further depreciation. Appropriately, the monetary

easing was temporary: borrowing costs were cut before sentiment started to stabilise

and financial conditions changed. Monetary policy was essentially to be kept firm in

Indonesia and Korea, while fiscal easing was supposed to reverse the spike in the

deficit in Thailand a year before the crisis.

Measures to fix the gaps in the financial and business sectors have been taken.

Other efforts were purpose at relieve the social effects of the financial condition and

setting the way for improvement to resume.

and their lack of access to the existing provisions of global governance. The

accumulated critique of the IMF has undermined the legitimacy, if not the authority,

of the IMF, and has contributed to intensified demands for a new international

framework to control the global economy. Indonesia, Korea, and Thailand, three of

the country’s most seriously affected by the crisis, were called in to provide financial

aid to the IMF. To address the problem, there were three main components of the

plan:

IMF financial support of some US$35 billion was given for change and reform

programs in Indonesia, Korea, and Thailand, with assistance to Indonesia being

further expanded in 1998-99. Other multilateral and bilateral outlets have pledged

around US$85 billion in aid, but not all of this funding has fully materialized. In

addition, the proactive effort was taken to curb private capital outflows (at varying

points since the launch of these projects, in separate countries).

Monetary policy was reinforced (in separate countries at various times to

avoid the decline in the exchange rates of the countries, which went way beyond what

the fundamentals might have required, and to discourage currency deflation from

leading to an inflation cycle and further depreciation. Appropriately, the monetary

easing was temporary: borrowing costs were cut before sentiment started to stabilise

and financial conditions changed. Monetary policy was essentially to be kept firm in

Indonesia and Korea, while fiscal easing was supposed to reverse the spike in the

deficit in Thailand a year before the crisis.

Measures to fix the gaps in the financial and business sectors have been taken.

Other efforts were purpose at relieve the social effects of the financial condition and

setting the way for improvement to resume.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Prepared investors and simple lending almost always lead to a reduction in the

quality of investments, and these economies soon began to show excess capacity. To

offset inflation, the U.S. Federal Reserve has started to increase its interest rates at

this time, which contributed to less lucrative exports (for those with currency fixed to

the dollar) and much less foreign investment.

The turning factor was the recognition by Thailand's capitalist that the charge

of appreciation in the market prices of that country had slowed and that its terms

increases were uncontrollable. This was demonstrated by the default of Comprising

Estate, the property developer, and the 1997 bankruptcy of Finance One, Thailand's

largest financial company.4 5 After that, currency traders started targeting the Thai

baht U.S. dollar peg. This evidenced popular and the medium of exchange was

subsequently floating and worth.

After this devaluation, several Asian currencies, including the Malaysian

Ringgit, the Indian rupee, and the Singapore dollar, every moved dramatically lower.

These numerical quantities have contributed to advanced deflation and the number of

difficulties which have outspread to Japan and South Korea.

The business enterprise crisis has eventually been remedied by International

Financial Institution (IMF), that has supported the debt needed to support the

struggling Asian economies. The group promised more than $110 billion in simple

terms debt to Singapore, Indonesia and Thailand in late 1997 to moreover support the

economies. It was more than double the most valuable debt ever from the IMF.

The IMF requested state to comply with stringent necessitate in return for

financing, involving higher taxes, decreased budget spending, social control of state-

owned companies, and rising interest taxation to temper overstressed economic

Prepared investors and simple lending almost always lead to a reduction in the

quality of investments, and these economies soon began to show excess capacity. To

offset inflation, the U.S. Federal Reserve has started to increase its interest rates at

this time, which contributed to less lucrative exports (for those with currency fixed to

the dollar) and much less foreign investment.

The turning factor was the recognition by Thailand's capitalist that the charge

of appreciation in the market prices of that country had slowed and that its terms

increases were uncontrollable. This was demonstrated by the default of Comprising

Estate, the property developer, and the 1997 bankruptcy of Finance One, Thailand's

largest financial company.4 5 After that, currency traders started targeting the Thai

baht U.S. dollar peg. This evidenced popular and the medium of exchange was

subsequently floating and worth.

After this devaluation, several Asian currencies, including the Malaysian

Ringgit, the Indian rupee, and the Singapore dollar, every moved dramatically lower.

These numerical quantities have contributed to advanced deflation and the number of

difficulties which have outspread to Japan and South Korea.

The business enterprise crisis has eventually been remedied by International

Financial Institution (IMF), that has supported the debt needed to support the

struggling Asian economies. The group promised more than $110 billion in simple

terms debt to Singapore, Indonesia and Thailand in late 1997 to moreover support the

economies. It was more than double the most valuable debt ever from the IMF.

The IMF requested state to comply with stringent necessitate in return for

financing, involving higher taxes, decreased budget spending, social control of state-

owned companies, and rising interest taxation to temper overstressed economic

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

system. Some other constraints made it possible for nations, without caring about lost

jobs, to close illiquid financial institutions (Sharma & Shalendra).

By 1999, many of the crisis-affected countries had shown a healing and survey

gross domestic product (GDP) development. Many countries have seen a sharp

decline in their capital marketplace and currency numerical quantity from pre-1997

peaks, but the enforced remedies have set the phase for Asia to re-emerge as a

powerful investment finish. The Asian financial crisis has also exposed the

vulnerabilities of regional organizations, especially the Asia-Pacific Economic

Cooperation Organization (APEC) and the Association of Southeast Asian Nations

(ASEAN), which have created a great deal of controversy on the future of the two

organizations. In particular, the critique focused on the casual, non-legalistic

institutionalism of both organizations. However, whereas ASEAN has demonstrated

greater sensitivity to structural change, the informal theoretical structure continues to

be the standard in East Asia's regional forums.

The foreclosures Asian crisis made it possible to explain and critique the

significant shortcomings within the NCM architecture models, since they did not

provide adequate policy instruments to respond to a Global Financial Crisis. New

Keynesians even acknowledged many weaknesses in their theories, intensifying the

search for answers to the new questions, rather than a declaration of historically

critical schools of thought. We plan to show in this section, from a meaningful review

of new Keynesian viewpoints, it for them, their models can be fixed with few (but not

necessarily easy) incremental changes. By revising current previous Keynesian papers

on the ways wherein the models collapsed and what insights might be learnt, we

develop this conversation and address how or how these concepts have been

system. Some other constraints made it possible for nations, without caring about lost

jobs, to close illiquid financial institutions (Sharma & Shalendra).

By 1999, many of the crisis-affected countries had shown a healing and survey

gross domestic product (GDP) development. Many countries have seen a sharp

decline in their capital marketplace and currency numerical quantity from pre-1997

peaks, but the enforced remedies have set the phase for Asia to re-emerge as a

powerful investment finish. The Asian financial crisis has also exposed the

vulnerabilities of regional organizations, especially the Asia-Pacific Economic

Cooperation Organization (APEC) and the Association of Southeast Asian Nations

(ASEAN), which have created a great deal of controversy on the future of the two

organizations. In particular, the critique focused on the casual, non-legalistic

institutionalism of both organizations. However, whereas ASEAN has demonstrated

greater sensitivity to structural change, the informal theoretical structure continues to

be the standard in East Asia's regional forums.

The foreclosures Asian crisis made it possible to explain and critique the

significant shortcomings within the NCM architecture models, since they did not

provide adequate policy instruments to respond to a Global Financial Crisis. New

Keynesians even acknowledged many weaknesses in their theories, intensifying the

search for answers to the new questions, rather than a declaration of historically

critical schools of thought. We plan to show in this section, from a meaningful review

of new Keynesian viewpoints, it for them, their models can be fixed with few (but not

necessarily easy) incremental changes. By revising current previous Keynesian papers

on the ways wherein the models collapsed and what insights might be learnt, we

develop this conversation and address how or how these concepts have been

9

implemented into macroeconomic theory. So we know the Keynesians theory point

about the Asian crisis.

implemented into macroeconomic theory. So we know the Keynesians theory point

about the Asian crisis.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

References:

Cheng & Tun‐jen. " "APEC and the Asian financial crisis: A lost opportunity for

institution‐building?"" Asian Journal of Political Science 6.2 (1998): 21-32.

Climent, Francisco & Vicente Meneu. ""Has 1997 Asian crisis increased information

flows between international markets." International Review of Economics &

Finance (2003): 111-143.

Jeon & Bang Nam. . ""From the 1997-97 Asian Financial Crisis to the 2008-09

Global Economic Crisis: Lessons from Korea's Experience." E. Asia L. Rev. 5

(2010): (2010): 103.

Kalkavan, Hakan & Irfan Ersin. " "Determination of factors affecting the South East

Asian crisis of 1997 probit-logit panel regression: The South East Asian

crisis." Handbook of research on global issues in financial communication and

investment decision." IGI Global, 2019. 148-167. (2019).

Sharma & Shalendra D. ""Bitter Medicine for Sick Tigers: The IMF and Asia's

Financial Crisis." Survival (1998)." (1998).

Somanath. "International financial management. IK International Pvt Ltd," (2011).

References:

Cheng & Tun‐jen. " "APEC and the Asian financial crisis: A lost opportunity for

institution‐building?"" Asian Journal of Political Science 6.2 (1998): 21-32.

Climent, Francisco & Vicente Meneu. ""Has 1997 Asian crisis increased information

flows between international markets." International Review of Economics &

Finance (2003): 111-143.

Jeon & Bang Nam. . ""From the 1997-97 Asian Financial Crisis to the 2008-09

Global Economic Crisis: Lessons from Korea's Experience." E. Asia L. Rev. 5

(2010): (2010): 103.

Kalkavan, Hakan & Irfan Ersin. " "Determination of factors affecting the South East

Asian crisis of 1997 probit-logit panel regression: The South East Asian

crisis." Handbook of research on global issues in financial communication and

investment decision." IGI Global, 2019. 148-167. (2019).

Sharma & Shalendra D. ""Bitter Medicine for Sick Tigers: The IMF and Asia's

Financial Crisis." Survival (1998)." (1998).

Somanath. "International financial management. IK International Pvt Ltd," (2011).

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.