Calculating WACC and Analyzing Foreign Exchange Risk and Hedging

VerifiedAdded on 2019/09/18

|5

|1292

|370

Project

AI Summary

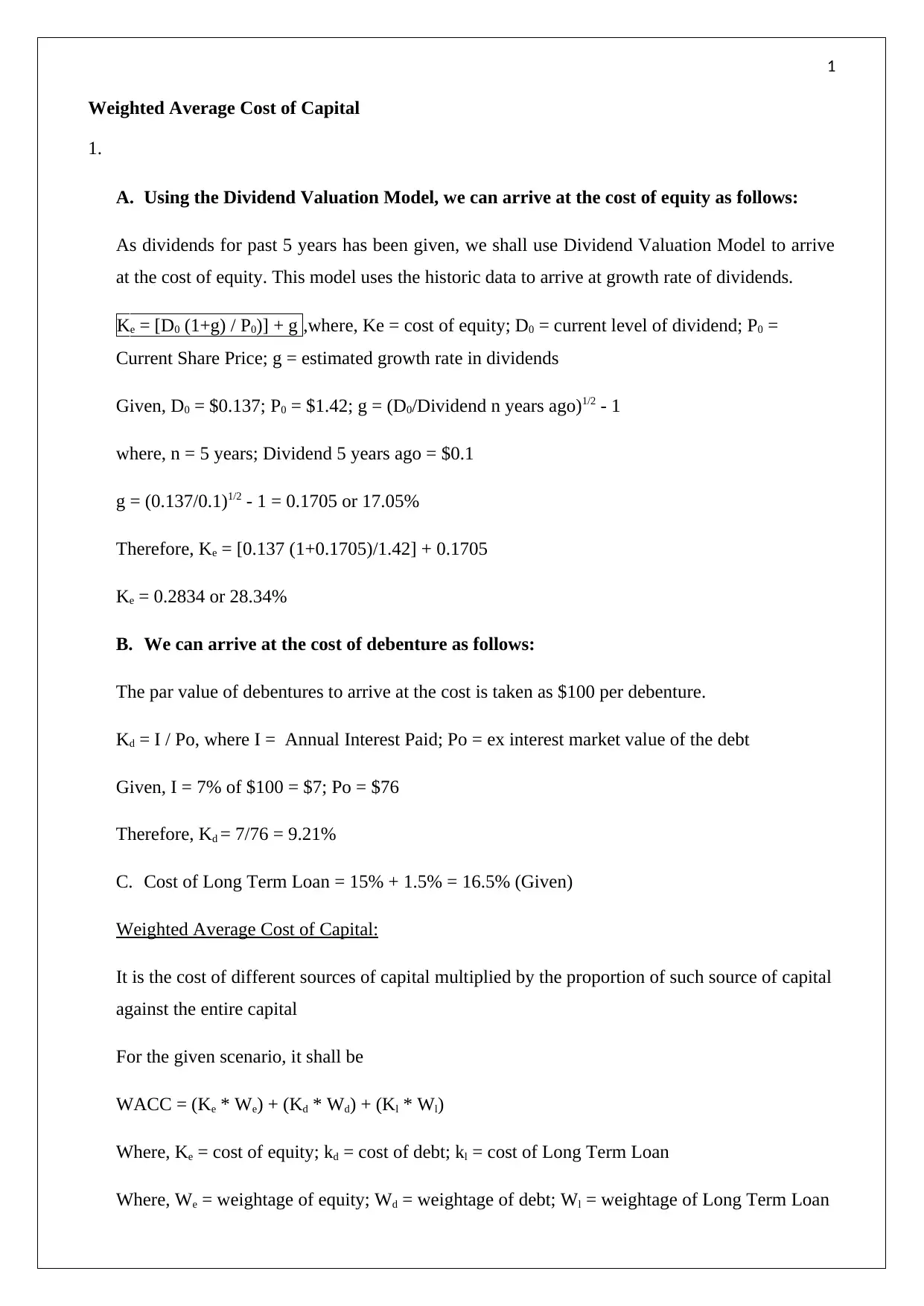

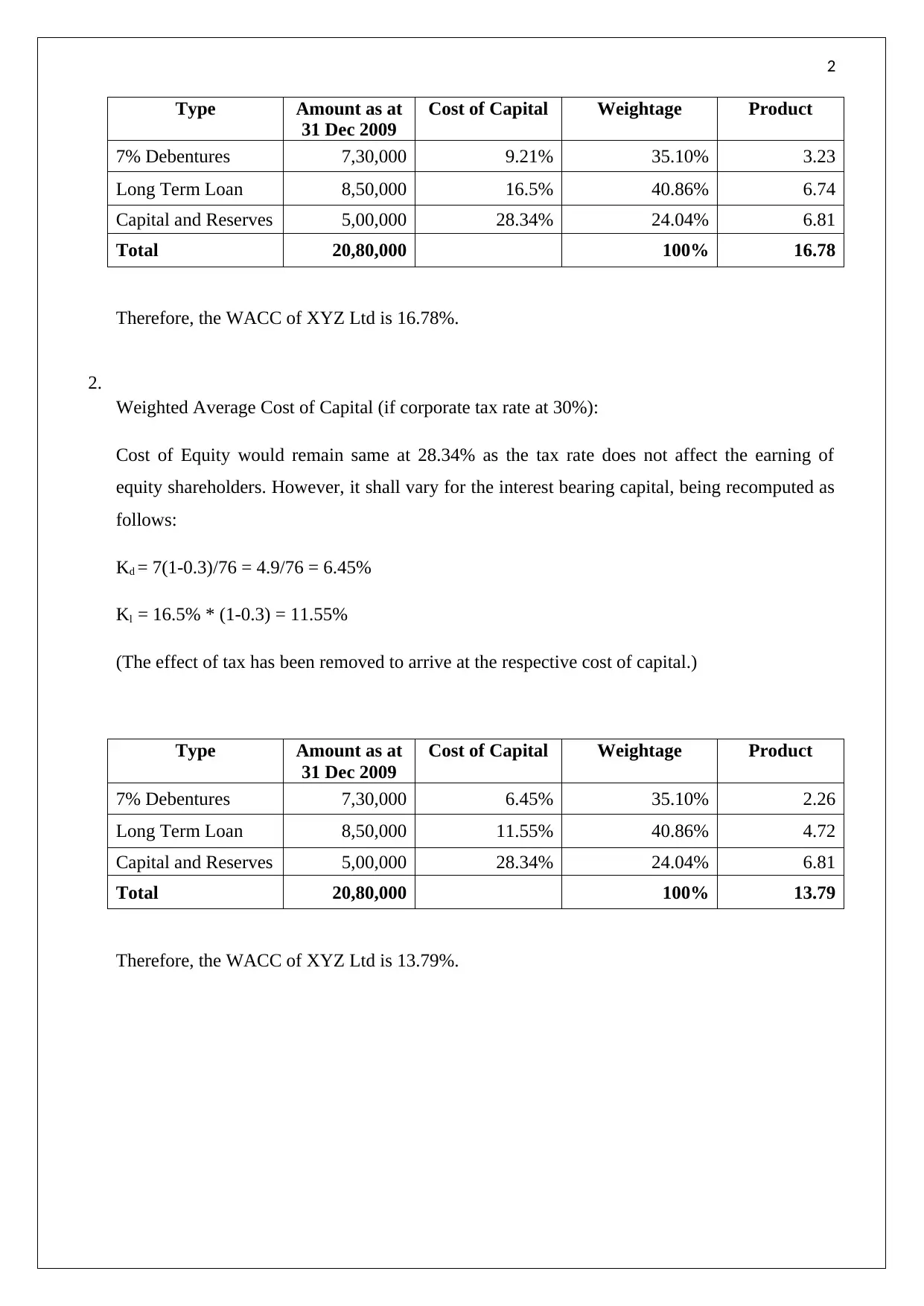

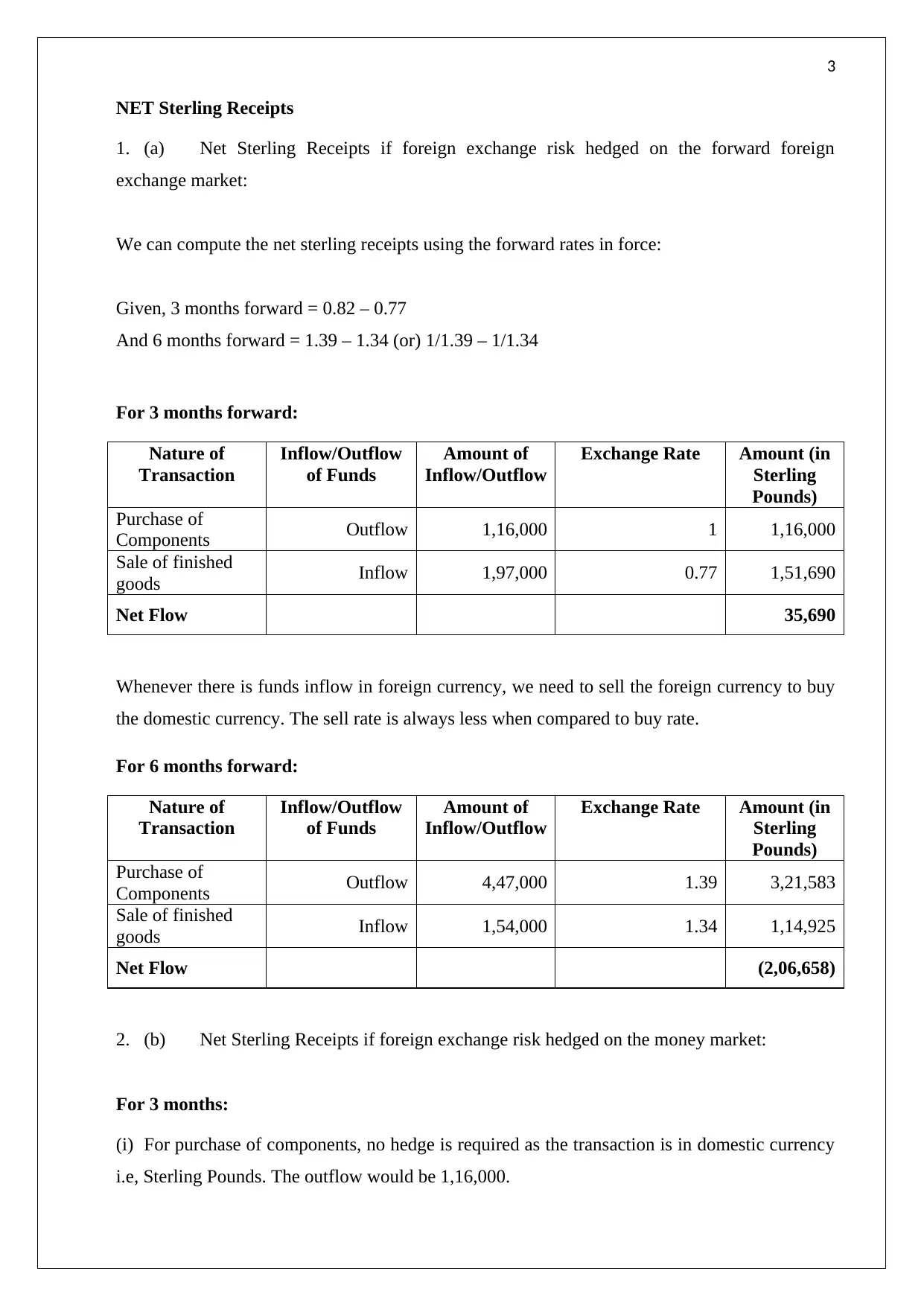

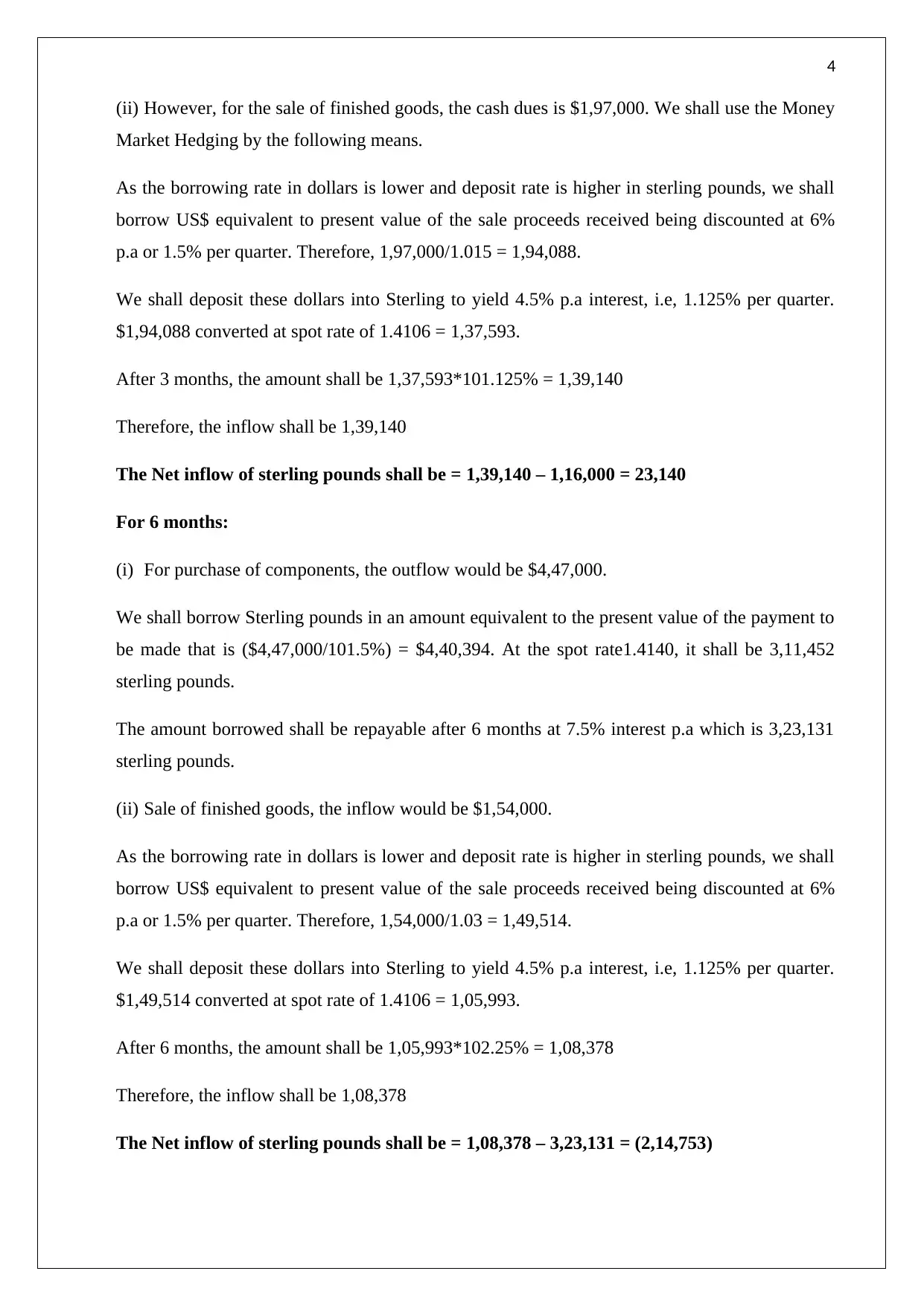

This project delves into the calculation of the Weighted Average Cost of Capital (WACC) for XYZ Ltd, incorporating both the cost of equity, cost of debt, and the cost of long-term loans. The analysis includes determining WACC with and without corporate tax considerations. Furthermore, the project explores foreign exchange risk management, evaluating the impact of hedging strategies using both forward foreign exchange markets and money market hedges for transactions involving the purchase of components and sale of finished goods. It provides detailed calculations of net sterling receipts under each hedging method and discusses the critical factors to consider when selecting the most appropriate risk mitigation approach. The project concludes with references to relevant financial resources.

1 out of 5

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.