5 year Weighted Average Growth Rate

VerifiedAdded on 2022/09/09

|3

|990

|25

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Crocs, Inc.

For the Crocs case please address the following questions:

Question 1

Which of the comparable companies appears to be a good match to Crocs at the time of

the case? Which would be a good match in five years? Use these multiples to provide

additional estimates of the value of Crocs (in other words, calculate a value for Crocs

using a current multiple, and calculate a value for Crocs using Yeung’s cash flow model

but with a terminal value based on a a multiple).

Answer

On the basis of data provided in Excel Sheet, there are 14 comparable data with

different market capitalization. The company current market capitalization is

approximately 7,154 Million US dollars. Thus, companies with similar market

capitalization shall be a good comparable company. Only one company shall satisfy the

said filter i.e. VF Corp which has a market capitalization of $. 8304 Millions. Further, if

we consider the EV/EBITDA Multiple Under Armour (25.93) is the best suitable

comparable as the ratio for both the companies are similar. Thus, Primary Apparel

companies are the most comparable companies

In addition to above if EV/Sales are considered for the purpose of selecting

comparables none of the companies shall come as comparable among which the most

nearest comparable shall be Lululemon (11.86).

In the time frame of 5 years, the market capitalisation of the company shall be double

from the present value based on the current multiple of 27.74 as computed under

exhibit 6. Thus, the market cap shall be approximate 15000 Mio Dollars and the

comparable industry shall be Primarily Footwear.

If the Enterprise Value is kept constant then the EV/EBITDA ratio shall change to 9 and

the comparable companies shall be Timberland (9.29), Columbia Sportswear(8.70), VF

Corp (9.31), Phillips Van-Husen (7.95) and Warnaco Corp (8.91).

If the Enterprise Value is kept constant then the EV/sales ratio shall change to 2.12 and

the comparable companies shall be Volcom (2.28) and Zumeiz (2.07)

Question 2

What would you consider reasonable, “high,” and “low” growth estimates (median, 25th,

and 75th percentile growth estimates) for 2008 and for the long run?

Answer 2

Based on 14 comparable data as provided in Exhibits, the 5 year weighted average

growth rate of the companies has been arranged on the basis of ascending order and

the percentile is computed based on same. The computation of 25th Percentile is 5.1%,

For the Crocs case please address the following questions:

Question 1

Which of the comparable companies appears to be a good match to Crocs at the time of

the case? Which would be a good match in five years? Use these multiples to provide

additional estimates of the value of Crocs (in other words, calculate a value for Crocs

using a current multiple, and calculate a value for Crocs using Yeung’s cash flow model

but with a terminal value based on a a multiple).

Answer

On the basis of data provided in Excel Sheet, there are 14 comparable data with

different market capitalization. The company current market capitalization is

approximately 7,154 Million US dollars. Thus, companies with similar market

capitalization shall be a good comparable company. Only one company shall satisfy the

said filter i.e. VF Corp which has a market capitalization of $. 8304 Millions. Further, if

we consider the EV/EBITDA Multiple Under Armour (25.93) is the best suitable

comparable as the ratio for both the companies are similar. Thus, Primary Apparel

companies are the most comparable companies

In addition to above if EV/Sales are considered for the purpose of selecting

comparables none of the companies shall come as comparable among which the most

nearest comparable shall be Lululemon (11.86).

In the time frame of 5 years, the market capitalisation of the company shall be double

from the present value based on the current multiple of 27.74 as computed under

exhibit 6. Thus, the market cap shall be approximate 15000 Mio Dollars and the

comparable industry shall be Primarily Footwear.

If the Enterprise Value is kept constant then the EV/EBITDA ratio shall change to 9 and

the comparable companies shall be Timberland (9.29), Columbia Sportswear(8.70), VF

Corp (9.31), Phillips Van-Husen (7.95) and Warnaco Corp (8.91).

If the Enterprise Value is kept constant then the EV/sales ratio shall change to 2.12 and

the comparable companies shall be Volcom (2.28) and Zumeiz (2.07)

Question 2

What would you consider reasonable, “high,” and “low” growth estimates (median, 25th,

and 75th percentile growth estimates) for 2008 and for the long run?

Answer 2

Based on 14 comparable data as provided in Exhibits, the 5 year weighted average

growth rate of the companies has been arranged on the basis of ascending order and

the percentile is computed based on same. The computation of 25th Percentile is 5.1%,

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Crocs, Inc.

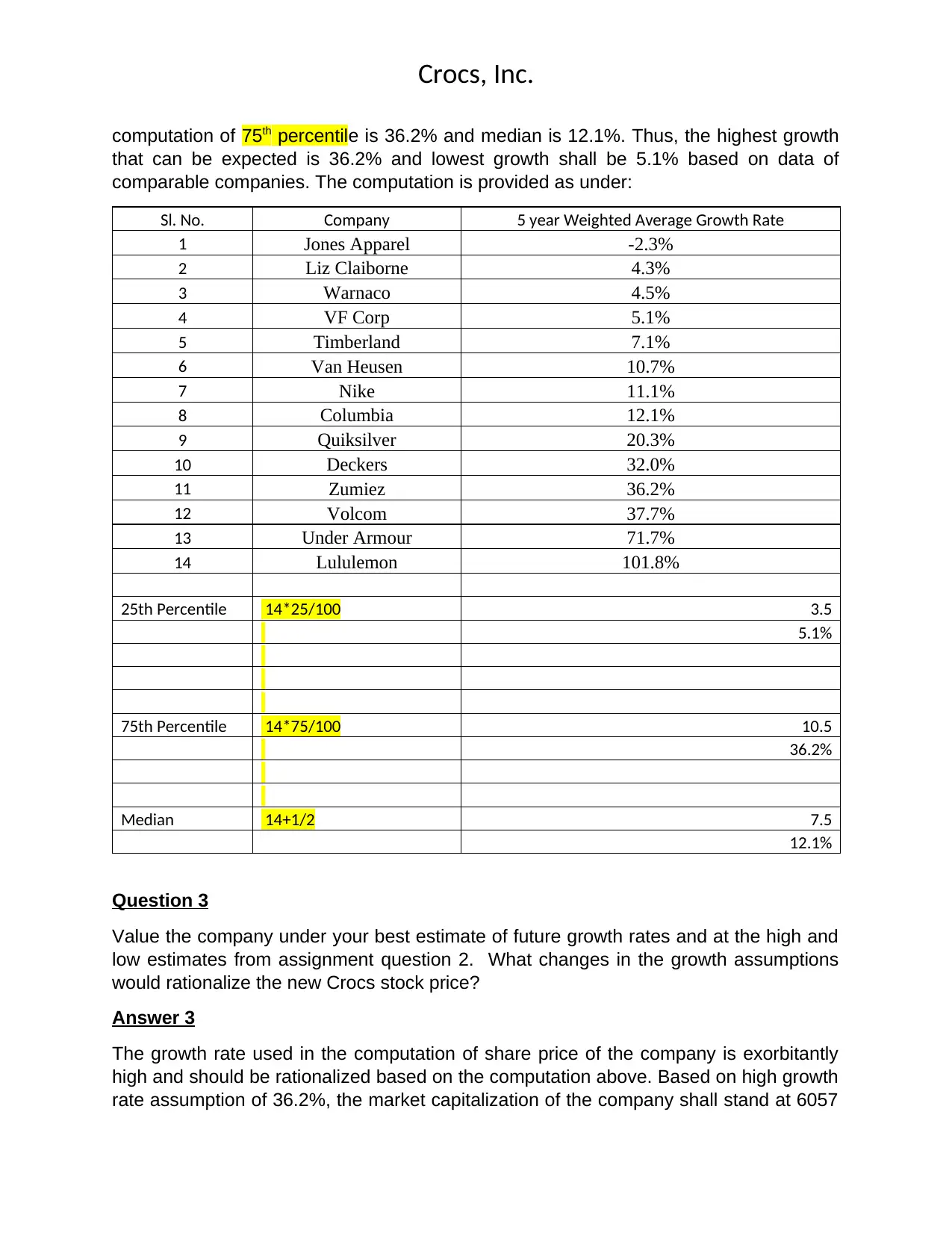

computation of 75th percentile is 36.2% and median is 12.1%. Thus, the highest growth

that can be expected is 36.2% and lowest growth shall be 5.1% based on data of

comparable companies. The computation is provided as under:

Sl. No. Company 5 year Weighted Average Growth Rate

1 Jones Apparel -2.3%

2 Liz Claiborne 4.3%

3 Warnaco 4.5%

4 VF Corp 5.1%

5 Timberland 7.1%

6 Van Heusen 10.7%

7 Nike 11.1%

8 Columbia 12.1%

9 Quiksilver 20.3%

10 Deckers 32.0%

11 Zumiez 36.2%

12 Volcom 37.7%

13 Under Armour 71.7%

14 Lululemon 101.8%

25th Percentile 14*25/100 3.5

5.1%

75th Percentile 14*75/100 10.5

36.2%

Median 14+1/2 7.5

12.1%

Question 3

Value the company under your best estimate of future growth rates and at the high and

low estimates from assignment question 2. What changes in the growth assumptions

would rationalize the new Crocs stock price?

Answer 3

The growth rate used in the computation of share price of the company is exorbitantly

high and should be rationalized based on the computation above. Based on high growth

rate assumption of 36.2%, the market capitalization of the company shall stand at 6057

computation of 75th percentile is 36.2% and median is 12.1%. Thus, the highest growth

that can be expected is 36.2% and lowest growth shall be 5.1% based on data of

comparable companies. The computation is provided as under:

Sl. No. Company 5 year Weighted Average Growth Rate

1 Jones Apparel -2.3%

2 Liz Claiborne 4.3%

3 Warnaco 4.5%

4 VF Corp 5.1%

5 Timberland 7.1%

6 Van Heusen 10.7%

7 Nike 11.1%

8 Columbia 12.1%

9 Quiksilver 20.3%

10 Deckers 32.0%

11 Zumiez 36.2%

12 Volcom 37.7%

13 Under Armour 71.7%

14 Lululemon 101.8%

25th Percentile 14*25/100 3.5

5.1%

75th Percentile 14*75/100 10.5

36.2%

Median 14+1/2 7.5

12.1%

Question 3

Value the company under your best estimate of future growth rates and at the high and

low estimates from assignment question 2. What changes in the growth assumptions

would rationalize the new Crocs stock price?

Answer 3

The growth rate used in the computation of share price of the company is exorbitantly

high and should be rationalized based on the computation above. Based on high growth

rate assumption of 36.2%, the market capitalization of the company shall stand at 6057

Crocs, Inc.

US Mio $ and the share price shall be $71.26. Thus, based on the percentile method

the valuation proposed in exhibit 6 seems infeasible.

Further, for 25th percentile the growth rate is 5.1% which is lower than the return

expected by equity shareholders and the valuation of the company shall stand at 2456

million Dollar and the share price shall be $28.89.

The growth assumptions shall be realistic given the scenarios of comparable

companies. Thus, company should use a growth of 36.2% as the base growth as

increased by 5%-10% on the basis of the company own capacity to grow. Thus,

company should expect a growth of 40% over the period of 4 years for valuation

Question 4

What is your opinion of the assumed profit margins? What alternative assumptions

would you consider reasonable?

Answer 4

The COGS to sales proportion of company is much lower than the margin of

comparable companies where in the COGS/Sales percentage is roughly 55%. As far as

SGA expense is considered, the same is in line with the comparable companies. Thus,

the opinion of assumed profit may not seem reliable in the given scenario as the Gross

profit of the company may fall down to 45% and an impact of 10% shall drop down the

valuation of the company very drastically. Thus, the assumption of 55% Gross margin

may seem unrealistic.

The alternative assumption that should be taken by the company is reducing the margin

gradually over the period so that the surplus enjoyed by the company is eliminated over

the years as in the long run company many not earn anything higher than the

comparable companies.

US Mio $ and the share price shall be $71.26. Thus, based on the percentile method

the valuation proposed in exhibit 6 seems infeasible.

Further, for 25th percentile the growth rate is 5.1% which is lower than the return

expected by equity shareholders and the valuation of the company shall stand at 2456

million Dollar and the share price shall be $28.89.

The growth assumptions shall be realistic given the scenarios of comparable

companies. Thus, company should use a growth of 36.2% as the base growth as

increased by 5%-10% on the basis of the company own capacity to grow. Thus,

company should expect a growth of 40% over the period of 4 years for valuation

Question 4

What is your opinion of the assumed profit margins? What alternative assumptions

would you consider reasonable?

Answer 4

The COGS to sales proportion of company is much lower than the margin of

comparable companies where in the COGS/Sales percentage is roughly 55%. As far as

SGA expense is considered, the same is in line with the comparable companies. Thus,

the opinion of assumed profit may not seem reliable in the given scenario as the Gross

profit of the company may fall down to 45% and an impact of 10% shall drop down the

valuation of the company very drastically. Thus, the assumption of 55% Gross margin

may seem unrealistic.

The alternative assumption that should be taken by the company is reducing the margin

gradually over the period so that the surplus enjoyed by the company is eliminated over

the years as in the long run company many not earn anything higher than the

comparable companies.

1 out of 3

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.