Auditing and Ethics in Australia: ST Barbara Limited (SBM)

Added on 2022-11-26

11 Pages2765 Words410 Views

5/2/2019

Student’s name

UNIVERSITY NAME

Auditing and

ethics in

Australia

ST Barbara Limited (SBM)

Student’s name

UNIVERSITY NAME

Auditing and

ethics in

Australia

ST Barbara Limited (SBM)

Table of Contents

Executive Summary................................................................................................... 2

Background of company............................................................................................. 3

Discussion and Analysis............................................................................................. 3

Section 1: Determination of Materiality...................................................................3

Review of the draft notes and disclosures...............................................................3

Section 2: Preliminary Analytical Review through Ratio Analysis............................4

Analysis of Ratios and Assertions and Audit procedures.........................................5

Section 3: Cash flow analysis..................................................................................5

Audit Report analysis.............................................................................................. 7

Conclusion.................................................................................................................. 8

References................................................................................................................. 9

Executive Summary................................................................................................... 2

Background of company............................................................................................. 3

Discussion and Analysis............................................................................................. 3

Section 1: Determination of Materiality...................................................................3

Review of the draft notes and disclosures...............................................................3

Section 2: Preliminary Analytical Review through Ratio Analysis............................4

Analysis of Ratios and Assertions and Audit procedures.........................................5

Section 3: Cash flow analysis..................................................................................5

Audit Report analysis.............................................................................................. 7

Conclusion.................................................................................................................. 8

References................................................................................................................. 9

Executive Summary

A report has been prepared on the company ST Barbara Limited, which is based out

of Australia and listed company on ASX. The report gives a brief outlook on the

company and its business. In the report, the concept of materiality has been

discussed and the quantitative estimate materiality to be considered has been

suggested. Several issues have been shown which do needs attention, these were

identified from the notes on accounts. The ratio analysis of the company shows

some of the major assertion which do needs to be verified and checked by applying

different audit procedures. The third part of the assignment is on cash flow

statement and the audit report published by the auditors of company. Based on the

same, the conclusion has been given as to whether the company is a going concern

or not. The objective of this assignment is to give a fair view in case the audit has

been conducted as per the minimum required standards or not.

A report has been prepared on the company ST Barbara Limited, which is based out

of Australia and listed company on ASX. The report gives a brief outlook on the

company and its business. In the report, the concept of materiality has been

discussed and the quantitative estimate materiality to be considered has been

suggested. Several issues have been shown which do needs attention, these were

identified from the notes on accounts. The ratio analysis of the company shows

some of the major assertion which do needs to be verified and checked by applying

different audit procedures. The third part of the assignment is on cash flow

statement and the audit report published by the auditors of company. Based on the

same, the conclusion has been given as to whether the company is a going concern

or not. The objective of this assignment is to give a fair view in case the audit has

been conducted as per the minimum required standards or not.

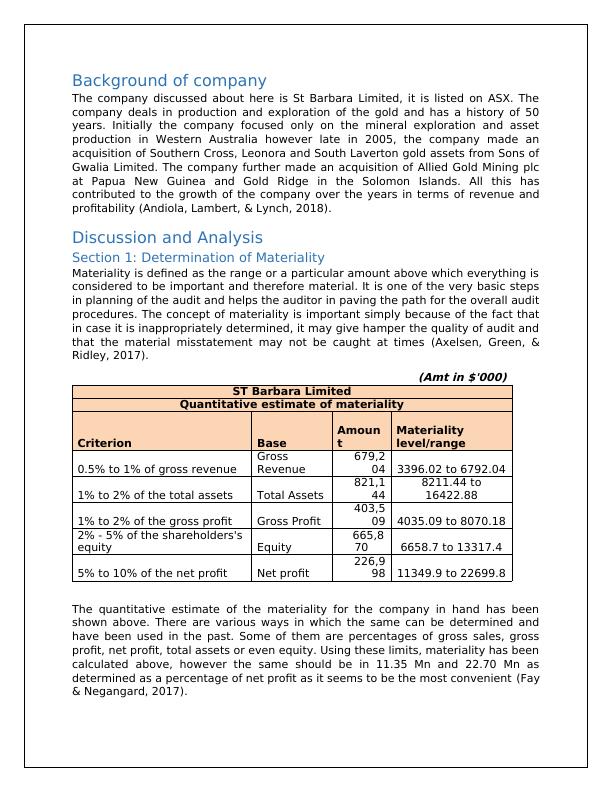

Background of company

The company discussed about here is St Barbara Limited, it is listed on ASX. The

company deals in production and exploration of the gold and has a history of 50

years. Initially the company focused only on the mineral exploration and asset

production in Western Australia however late in 2005, the company made an

acquisition of Southern Cross, Leonora and South Laverton gold assets from Sons of

Gwalia Limited. The company further made an acquisition of Allied Gold Mining plc

at Papua New Guinea and Gold Ridge in the Solomon Islands. All this has

contributed to the growth of the company over the years in terms of revenue and

profitability (Andiola, Lambert, & Lynch, 2018).

Discussion and Analysis

Section 1: Determination of Materiality

Materiality is defined as the range or a particular amount above which everything is

considered to be important and therefore material. It is one of the very basic steps

in planning of the audit and helps the auditor in paving the path for the overall audit

procedures. The concept of materiality is important simply because of the fact that

in case it is inappropriately determined, it may give hamper the quality of audit and

that the material misstatement may not be caught at times (Axelsen, Green, &

Ridley, 2017).

(Amt in $'000)

ST Barbara Limited

Quantitative estimate of materiality

Criterion Base

Amoun

t

Materiality

level/range

0.5% to 1% of gross revenue

Gross

Revenue

679,2

04 3396.02 to 6792.04

1% to 2% of the total assets Total Assets

821,1

44

8211.44 to

16422.88

1% to 2% of the gross profit Gross Profit

403,5

09 4035.09 to 8070.18

2% - 5% of the shareholders's

equity Equity

665,8

70 6658.7 to 13317.4

5% to 10% of the net profit Net profit

226,9

98 11349.9 to 22699.8

The quantitative estimate of the materiality for the company in hand has been

shown above. There are various ways in which the same can be determined and

have been used in the past. Some of them are percentages of gross sales, gross

profit, net profit, total assets or even equity. Using these limits, materiality has been

calculated above, however the same should be in 11.35 Mn and 22.70 Mn as

determined as a percentage of net profit as it seems to be the most convenient (Fay

& Negangard, 2017).

The company discussed about here is St Barbara Limited, it is listed on ASX. The

company deals in production and exploration of the gold and has a history of 50

years. Initially the company focused only on the mineral exploration and asset

production in Western Australia however late in 2005, the company made an

acquisition of Southern Cross, Leonora and South Laverton gold assets from Sons of

Gwalia Limited. The company further made an acquisition of Allied Gold Mining plc

at Papua New Guinea and Gold Ridge in the Solomon Islands. All this has

contributed to the growth of the company over the years in terms of revenue and

profitability (Andiola, Lambert, & Lynch, 2018).

Discussion and Analysis

Section 1: Determination of Materiality

Materiality is defined as the range or a particular amount above which everything is

considered to be important and therefore material. It is one of the very basic steps

in planning of the audit and helps the auditor in paving the path for the overall audit

procedures. The concept of materiality is important simply because of the fact that

in case it is inappropriately determined, it may give hamper the quality of audit and

that the material misstatement may not be caught at times (Axelsen, Green, &

Ridley, 2017).

(Amt in $'000)

ST Barbara Limited

Quantitative estimate of materiality

Criterion Base

Amoun

t

Materiality

level/range

0.5% to 1% of gross revenue

Gross

Revenue

679,2

04 3396.02 to 6792.04

1% to 2% of the total assets Total Assets

821,1

44

8211.44 to

16422.88

1% to 2% of the gross profit Gross Profit

403,5

09 4035.09 to 8070.18

2% - 5% of the shareholders's

equity Equity

665,8

70 6658.7 to 13317.4

5% to 10% of the net profit Net profit

226,9

98 11349.9 to 22699.8

The quantitative estimate of the materiality for the company in hand has been

shown above. There are various ways in which the same can be determined and

have been used in the past. Some of them are percentages of gross sales, gross

profit, net profit, total assets or even equity. Using these limits, materiality has been

calculated above, however the same should be in 11.35 Mn and 22.70 Mn as

determined as a percentage of net profit as it seems to be the most convenient (Fay

& Negangard, 2017).

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Auditing and Ethics in Australia - Metcash Limitedlg...

|9

|2375

|74

Auditing and Ethics in Australia - Woolworths Limitedlg...

|10

|2818

|180

Swot Analysis of St Barabara Limitedlg...

|17

|4275

|169

Auditing and Ethics in Australialg...

|9

|2893

|54

Analyzing Risk in Audit of Financial Reports: JB HI FI Limitedlg...

|10

|3232

|65

Auditing and Ethics in Australia - Tabcorp Holdings Limitedlg...

|9

|2653

|417