Demand Factors of Cyber Insurance

VerifiedAdded on 2023/01/19

|11

|4017

|43

AI Summary

This report analyzes the demand factors and their impact on the market share of cyber insurance. It discusses the high cybercrime rate, GDPR act, digital payments, and IT security as driving factors. AXA's cyber insurance products and coverage are also highlighted.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Coursework assignment 1 answer template530Coursework submission rules and important notes

Before you start your assignment, it is essential that you familiarise yourself with the

Coursework assessment guidelines and instructions available on RevisionMate.

This includes the following information:

Important rules relating to referencing all sources including the study text, regulations and

citing statute and case law.

Penalties for contravention of the rules relating to plagiarism and collaboration.

Coursework marking criteria applied by markers to submitted answers.

Deadlines for submission of coursework answers.

There are 80 marks available per coursework assignment. You must obtain a minimum of 40

marks (50%) per coursework assignment to achieve a pass.

Your answer must be submitted on the correct answer template in Arial font, size 11.

Your answer must include a brief context, at the start of your answer, and should be referred

to throughout your answer.

Each assignment submission should be a maximum of 3,200 words.

Do not include your name or CII PIN anywhere in your answer.

Top tips for answering coursework assignments

Read the 530 Specimen coursework assignment and answer, available on RevisionMate.

Read the assignments carefully and ensure you answer all parts of the assignments.

You are encouraged to choose a context that is based on a real organisation or a division of

an organisation.

For assignments relating to regulation and law, knowledge of the UK regulatory framework is

appropriate. However, marks can be awarded for non-UK examples if they are more relevant

to your context.

There is no minimum word requirement, but an answer with fewer than 2,800 words may be

insufficiently comprehensive.

To be completed before submission:

Word count: 2686

Start typing your answer here:

Introduction

Business insurance is a concept which protects a business form several losses which occur

in day to day business operations (Serpa, 2016). There are several types of business

insurance such as commercial vehicle insurance, Professional liability insurance, property

insurance, home based business, product liability insurance and vehicle insurance and cyber

insurance (Les, et al., 2011). Companies assess their business

January 2019 1

Before you start your assignment, it is essential that you familiarise yourself with the

Coursework assessment guidelines and instructions available on RevisionMate.

This includes the following information:

Important rules relating to referencing all sources including the study text, regulations and

citing statute and case law.

Penalties for contravention of the rules relating to plagiarism and collaboration.

Coursework marking criteria applied by markers to submitted answers.

Deadlines for submission of coursework answers.

There are 80 marks available per coursework assignment. You must obtain a minimum of 40

marks (50%) per coursework assignment to achieve a pass.

Your answer must be submitted on the correct answer template in Arial font, size 11.

Your answer must include a brief context, at the start of your answer, and should be referred

to throughout your answer.

Each assignment submission should be a maximum of 3,200 words.

Do not include your name or CII PIN anywhere in your answer.

Top tips for answering coursework assignments

Read the 530 Specimen coursework assignment and answer, available on RevisionMate.

Read the assignments carefully and ensure you answer all parts of the assignments.

You are encouraged to choose a context that is based on a real organisation or a division of

an organisation.

For assignments relating to regulation and law, knowledge of the UK regulatory framework is

appropriate. However, marks can be awarded for non-UK examples if they are more relevant

to your context.

There is no minimum word requirement, but an answer with fewer than 2,800 words may be

insufficiently comprehensive.

To be completed before submission:

Word count: 2686

Start typing your answer here:

Introduction

Business insurance is a concept which protects a business form several losses which occur

in day to day business operations (Serpa, 2016). There are several types of business

insurance such as commercial vehicle insurance, Professional liability insurance, property

insurance, home based business, product liability insurance and vehicle insurance and cyber

insurance (Les, et al., 2011). Companies assess their business

January 2019 1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

530Coursework assignment 1 answer template

insurance requirements based on potential risk indulge in the environment in which a

company operates (Secretan, 2018).

AXA is an insurance service provider. The company is the French multinational insurance

company based in the 8th arrondissement of Paris which provides insurance services and

products also other financial services across the globe (AXA, 2018).

AXA's service of cyber insurance is most demandable in the market due to increased

demand for cybersecurity.

This report will analyse the demand factors and the impacts these factors having on the

market share of this product also giving some recommendation to AXA for increasing its

market share.

AXA Business insurance

AXA is one of the biggest companies offering financial insurance to the international market

with headquarter in France. However, AXA is the representation of the group of many

companies but it is organized independently in many different countries as per the country’s

laws and regulations.

The company works under five different business felids: Life and Savings, Property and

Casualty, International Insurance, Asset Management, and Banking. The Life and Savings

fragment offers items including individual and gathering investment funds items, life and

wellbeing items for both individual and business customers. The Property and Casualty

portion offer items including engine, family unit, property and general risk insurance for both

individual and business clients, principally little to medium estimated organizations. The

International Insurance section centres on risks, reinsurance, and help. The Asset

Management fragment incorporates broadened resource the board and related

administrations. The Banking portion includes in the financial exercises, which incorporates

retail banking, contracts credits and reserve funds led principally in France, Belgium, and

Germany.

AXA has built up itself as a key player in the riches the board/insurance area in creating

nations. Today, 52 million customers on the planet trust AXA and the AXA name. Since

1998, the AXA Group has been working together under a solitary brand with worldwide

reach.

AXA is the UK’s biggest start up business insurance provider.

AXA trades in the UK as AXA UK using several subsidies such as AXA sun life, AXA

investment manager, AXA PPP health care AXA Wealth. Company’s market capitalization is

around 64.1 B USD. The company is listed in a Forbes as 65th top regarded company 2018,

and 97th most valuable brand in 2013.

Cyber insurance

In today’s technology world, social media and internet play a key role in the many

transactions o the business and these key aspects serves many kinds of cybercrime and

attacks. Regardless of whether propelled by ordinary programmers, crooks, insiders or even

country states, cyber-attacks are probably going to happen and can make moderate extreme

misfortunes for associations expansive and little. As a part of risk

January 2019 2

insurance requirements based on potential risk indulge in the environment in which a

company operates (Secretan, 2018).

AXA is an insurance service provider. The company is the French multinational insurance

company based in the 8th arrondissement of Paris which provides insurance services and

products also other financial services across the globe (AXA, 2018).

AXA's service of cyber insurance is most demandable in the market due to increased

demand for cybersecurity.

This report will analyse the demand factors and the impacts these factors having on the

market share of this product also giving some recommendation to AXA for increasing its

market share.

AXA Business insurance

AXA is one of the biggest companies offering financial insurance to the international market

with headquarter in France. However, AXA is the representation of the group of many

companies but it is organized independently in many different countries as per the country’s

laws and regulations.

The company works under five different business felids: Life and Savings, Property and

Casualty, International Insurance, Asset Management, and Banking. The Life and Savings

fragment offers items including individual and gathering investment funds items, life and

wellbeing items for both individual and business customers. The Property and Casualty

portion offer items including engine, family unit, property and general risk insurance for both

individual and business clients, principally little to medium estimated organizations. The

International Insurance section centres on risks, reinsurance, and help. The Asset

Management fragment incorporates broadened resource the board and related

administrations. The Banking portion includes in the financial exercises, which incorporates

retail banking, contracts credits and reserve funds led principally in France, Belgium, and

Germany.

AXA has built up itself as a key player in the riches the board/insurance area in creating

nations. Today, 52 million customers on the planet trust AXA and the AXA name. Since

1998, the AXA Group has been working together under a solitary brand with worldwide

reach.

AXA is the UK’s biggest start up business insurance provider.

AXA trades in the UK as AXA UK using several subsidies such as AXA sun life, AXA

investment manager, AXA PPP health care AXA Wealth. Company’s market capitalization is

around 64.1 B USD. The company is listed in a Forbes as 65th top regarded company 2018,

and 97th most valuable brand in 2013.

Cyber insurance

In today’s technology world, social media and internet play a key role in the many

transactions o the business and these key aspects serves many kinds of cybercrime and

attacks. Regardless of whether propelled by ordinary programmers, crooks, insiders or even

country states, cyber-attacks are probably going to happen and can make moderate extreme

misfortunes for associations expansive and little. As a part of risk

January 2019 2

530Coursework assignment 1 answer template

management plan cyber insurance is an important product to purchase to secure the

organizations from several cyber-attacks.

Cyber insurance policies, additionally alluded to as cybersecurity insurance or digital

obligation insurance coverage (CLIC), is intended to enable an association to moderate

hazard introduction by counterbalancing costs required with recuperation after a digital

related security rupture or comparative occasion (AON, 2017).

European regulation introduced an act general data protection regulation act on 25 May

2018 (Groot, 2019). These standards basically protect a business from several cybercrimes

such as data security breaches and non-compliance management. AXA launches many

kinds of cyber insurance.

AXA XL Insurance's cybersecurity insurance approach accompanies extended coverage and

considerably more extensive terms to ensure against the present rising dangers. AXA offers

coverage for information insurance risks, both for the outsider cases and first-party

moderation costs following an innovation or digital occasion. Its products capacity is around

15 mn USD. The company cyber insurance includes coverage of several risks:

Privacy and scrutiny liability

Data Breach Response and managing crisis

Privacy regulatory defence costs an coverage

Data recovery

Cyber extortion (XL, 2018).

In 2018 AXA also provide new service of cyber insurance policy specifically designed for

small and mid-sized businesses (SMBs).

the on-request, AI-powered digital insurance service grows the backup plan's scope in the

digital insurance market and gives SMBs access to wide digital insurance, also digital

security assets to enable them to ensure their income, gainfulness and client connections.

AXA XL's digital insurance service is designed for organizations under $20 million in yearly

income and offers limits from $250 thousand up to $3 million. Using Slice's E&S business

permit, the advanced stage gives extensive coverage that can without much of a stretch be

bought in only minutes for qualifying SMBs. This straightforward on boarding process

enables clients to effectively obtain an approach as well as submit the first notice of

misfortune through our cases bot (Insurance Journal, 2018).

The policy incorporates coverage for information security and risks Insurance, both for

outsider cases and first-party moderation costs. These are frequently connected with a

digital attack, such costs for notice, credit checking, information recovery, notoriety the

board, loss of business and additional cost. The coverage also gives insurance to digital

blackmail threats and other breach-related liabilities including administrative penalties,

GDPR and Merchant Services Agreements. The AXA XL cybersecurity insurance

arrangement is conveyed with canny information to help SMBs comprehend their digital risks

introduction and figure out how to reinforce their digital defences. Clients have furnished an

individualized dashboard with a general digital hazard evaluation and scores alongside

benchmark scores of their industry peers over each hazard category (XL, 2018).

January 2019 3

management plan cyber insurance is an important product to purchase to secure the

organizations from several cyber-attacks.

Cyber insurance policies, additionally alluded to as cybersecurity insurance or digital

obligation insurance coverage (CLIC), is intended to enable an association to moderate

hazard introduction by counterbalancing costs required with recuperation after a digital

related security rupture or comparative occasion (AON, 2017).

European regulation introduced an act general data protection regulation act on 25 May

2018 (Groot, 2019). These standards basically protect a business from several cybercrimes

such as data security breaches and non-compliance management. AXA launches many

kinds of cyber insurance.

AXA XL Insurance's cybersecurity insurance approach accompanies extended coverage and

considerably more extensive terms to ensure against the present rising dangers. AXA offers

coverage for information insurance risks, both for the outsider cases and first-party

moderation costs following an innovation or digital occasion. Its products capacity is around

15 mn USD. The company cyber insurance includes coverage of several risks:

Privacy and scrutiny liability

Data Breach Response and managing crisis

Privacy regulatory defence costs an coverage

Data recovery

Cyber extortion (XL, 2018).

In 2018 AXA also provide new service of cyber insurance policy specifically designed for

small and mid-sized businesses (SMBs).

the on-request, AI-powered digital insurance service grows the backup plan's scope in the

digital insurance market and gives SMBs access to wide digital insurance, also digital

security assets to enable them to ensure their income, gainfulness and client connections.

AXA XL's digital insurance service is designed for organizations under $20 million in yearly

income and offers limits from $250 thousand up to $3 million. Using Slice's E&S business

permit, the advanced stage gives extensive coverage that can without much of a stretch be

bought in only minutes for qualifying SMBs. This straightforward on boarding process

enables clients to effectively obtain an approach as well as submit the first notice of

misfortune through our cases bot (Insurance Journal, 2018).

The policy incorporates coverage for information security and risks Insurance, both for

outsider cases and first-party moderation costs. These are frequently connected with a

digital attack, such costs for notice, credit checking, information recovery, notoriety the

board, loss of business and additional cost. The coverage also gives insurance to digital

blackmail threats and other breach-related liabilities including administrative penalties,

GDPR and Merchant Services Agreements. The AXA XL cybersecurity insurance

arrangement is conveyed with canny information to help SMBs comprehend their digital risks

introduction and figure out how to reinforce their digital defences. Clients have furnished an

individualized dashboard with a general digital hazard evaluation and scores alongside

benchmark scores of their industry peers over each hazard category (XL, 2018).

January 2019 3

530Coursework assignment 1 answer template

Demand Factors of Cyber insurance

In this digital world, digitalization becomes a key aspect for many businesses, without

internet and digitalization it’s impossible to run a business however these involve many

cyber risks and breaches. The impacts of cyber breaches on organizations, governments,

and charities effects millions of customer’s data and security breaches and different kinds of

breaches such as phishing, theft identity, hacking, and many others (EIOPA , 2018). In the

UK in the year 2015, there are 38 firms hit by cyber-attacks and 24 firms in 2016 and around

69 firms hit in 2017. According to National cybersecurity centre, there are around 109 million

incidents of cyber frauds and around 1100 cyber-attacks in last 12 months, and around 590

of these observed as substantial and 30 other which needs necessary action by

governments. Increased cybercrime creates worries for many organizations and

governments also (Thomas, 2018). These risks create many kinds of losses for

organizations whether they are large or small, and these risks created demand for cyber

insurance. Cyber insurance is playing and key role in helping all the organizations and build

resilience. Here are several factors which drive the demand for cyber insurance.

• High cybercrime rate

• GDPR Act

• Digital payments and connectivity

• IT security and risk management

High cyber-crime rate

In the UK Cybercrime reached 63% (Ashford, 2018). Precisely 1,769, 185,063 client records

were leaked in all over the world (Mason, 2019). In 2017 the insurance world substantial

threat of ransomware software in the form of Peaty, not Peta ad malware attacks that

messed the computer system over 150 countries and other operations of numerous

industries includes hospitals, universities and shipping companies, and governments.

Although no one can ever measure the exact losses associated with these incidents.

NotPetya attacks stances at around 10bn, and WannaCry at 4bn $ and some estimates

have the Petty attack costing around 10times that of WannaCry (Gittle, 2019).

This increased cybercrime creates worries for cybersecurity, as a result, these worries

creates plenty of opportunities for AXA and many other companies.

GDPR Act and regulatory environment

The increment of cyber-attacks lead crates the worries of governments. The General Data

Protection Regulation is a European law on data privacy and security for all the organization

to protect their customer’s personal data. This becomes effective on 25 May 2018. All the

organizations across the globe required to compliant with the law and must protect the data

of all the EU citizens (Groot, 2019). Cyber insurance decreases the risk exposure to cyber

threats such as coverage of third-party liability, financial losses.

Digital payments and connectivity

Cybersecurity is one of the big challenges faced by stakeholders of the digital payment

ecosystem. With more and more users preferring digital payments, the chances of getting

exposed to cybersecurity risks such as online fraud, information theft, and malware or virus

January 2019 4

Demand Factors of Cyber insurance

In this digital world, digitalization becomes a key aspect for many businesses, without

internet and digitalization it’s impossible to run a business however these involve many

cyber risks and breaches. The impacts of cyber breaches on organizations, governments,

and charities effects millions of customer’s data and security breaches and different kinds of

breaches such as phishing, theft identity, hacking, and many others (EIOPA , 2018). In the

UK in the year 2015, there are 38 firms hit by cyber-attacks and 24 firms in 2016 and around

69 firms hit in 2017. According to National cybersecurity centre, there are around 109 million

incidents of cyber frauds and around 1100 cyber-attacks in last 12 months, and around 590

of these observed as substantial and 30 other which needs necessary action by

governments. Increased cybercrime creates worries for many organizations and

governments also (Thomas, 2018). These risks create many kinds of losses for

organizations whether they are large or small, and these risks created demand for cyber

insurance. Cyber insurance is playing and key role in helping all the organizations and build

resilience. Here are several factors which drive the demand for cyber insurance.

• High cybercrime rate

• GDPR Act

• Digital payments and connectivity

• IT security and risk management

High cyber-crime rate

In the UK Cybercrime reached 63% (Ashford, 2018). Precisely 1,769, 185,063 client records

were leaked in all over the world (Mason, 2019). In 2017 the insurance world substantial

threat of ransomware software in the form of Peaty, not Peta ad malware attacks that

messed the computer system over 150 countries and other operations of numerous

industries includes hospitals, universities and shipping companies, and governments.

Although no one can ever measure the exact losses associated with these incidents.

NotPetya attacks stances at around 10bn, and WannaCry at 4bn $ and some estimates

have the Petty attack costing around 10times that of WannaCry (Gittle, 2019).

This increased cybercrime creates worries for cybersecurity, as a result, these worries

creates plenty of opportunities for AXA and many other companies.

GDPR Act and regulatory environment

The increment of cyber-attacks lead crates the worries of governments. The General Data

Protection Regulation is a European law on data privacy and security for all the organization

to protect their customer’s personal data. This becomes effective on 25 May 2018. All the

organizations across the globe required to compliant with the law and must protect the data

of all the EU citizens (Groot, 2019). Cyber insurance decreases the risk exposure to cyber

threats such as coverage of third-party liability, financial losses.

Digital payments and connectivity

Cybersecurity is one of the big challenges faced by stakeholders of the digital payment

ecosystem. With more and more users preferring digital payments, the chances of getting

exposed to cybersecurity risks such as online fraud, information theft, and malware or virus

January 2019 4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

530Coursework assignment 1 answer template

attacks are also increasing. Lack of awareness and poor digital payment ecosystem are

some of the primary reasons that have led to an increase in these attacks (KPMG, 2017).

IT security and risk management

With these digital market create many facilities, however, it creates huge IT risks for every

organization. Increasing cyber-crime becomes a key concern for an organization’s risk and

planning management part and leads them to purchase cybersecurity insurance.

Analysing the demand factors and their impact on market share

There is widespread estimation in the market that the implementation of the GDPR act-

organizations which are in non-compliance with this Act may face a huge amount of fines, as

result, these factors will stimulate a considerable rise in the demand for this cyber insurance

of the company. The major view of the defendants is that the estimated rise in demand in

this area will be more common instead of unexpected. Reason for this is that it is yet

uncertain whether this Act fines would be insurable and the fact that this law is very

extensive, with many organizations Concentrate on compliance for now. Inclusive, although

it is assumed that the GDPR Act will ultimately raise awareness of cyber risk and drives

demand for cyber insurance.

Apart from the GDPR, increased cybercrime rate and digital payment concept keep the

organization awake at night. These major risks are the driver of the operational risk and that

organizations looking to the insurance industry to deliver wide coverage for the cyber risk

they face. Most organizations in recent years faced cybercrime which contains a huge

amount of direct and indirect cost to the company, by providing cyber insurance, the

insurance company provides defence cost to the victim company. Insurer Company provides

coverage to their losses, however, the defence cost coverage is lower than their direct cost

of losses from cybercrime and most companies ask for expanded coverage (OCED, 2017).

AXA insurance provides increasingly comprehensive coverage. From supports to extended

coverage language, bearers are revising arrangements to meet a lot more torment focuses

on their purchasers. A few supports have started to show up, covering things like framework

disappointments, social designing misfortunes, considerable reputational misfortune, and

equipment misfortune. In like manner, a few supports give purchasers the decision of

choosing which arrangement will deal with their case on account of a business intrusion

misfortune where there might cover coverage with their property approach as well as a

social designing misfortune in which their wrongdoing strategy may react (XL, 2018).

AXA’s products coverage:

Third party liability

Data breach security and privacy liability

Media internet communication

First Party losses

Business interruption and extra expense

Loss/destruction of electronic assets

First party incident responses including IT forensics, notification costs, call centre,

and PR expenses

January 2019 5

attacks are also increasing. Lack of awareness and poor digital payment ecosystem are

some of the primary reasons that have led to an increase in these attacks (KPMG, 2017).

IT security and risk management

With these digital market create many facilities, however, it creates huge IT risks for every

organization. Increasing cyber-crime becomes a key concern for an organization’s risk and

planning management part and leads them to purchase cybersecurity insurance.

Analysing the demand factors and their impact on market share

There is widespread estimation in the market that the implementation of the GDPR act-

organizations which are in non-compliance with this Act may face a huge amount of fines, as

result, these factors will stimulate a considerable rise in the demand for this cyber insurance

of the company. The major view of the defendants is that the estimated rise in demand in

this area will be more common instead of unexpected. Reason for this is that it is yet

uncertain whether this Act fines would be insurable and the fact that this law is very

extensive, with many organizations Concentrate on compliance for now. Inclusive, although

it is assumed that the GDPR Act will ultimately raise awareness of cyber risk and drives

demand for cyber insurance.

Apart from the GDPR, increased cybercrime rate and digital payment concept keep the

organization awake at night. These major risks are the driver of the operational risk and that

organizations looking to the insurance industry to deliver wide coverage for the cyber risk

they face. Most organizations in recent years faced cybercrime which contains a huge

amount of direct and indirect cost to the company, by providing cyber insurance, the

insurance company provides defence cost to the victim company. Insurer Company provides

coverage to their losses, however, the defence cost coverage is lower than their direct cost

of losses from cybercrime and most companies ask for expanded coverage (OCED, 2017).

AXA insurance provides increasingly comprehensive coverage. From supports to extended

coverage language, bearers are revising arrangements to meet a lot more torment focuses

on their purchasers. A few supports have started to show up, covering things like framework

disappointments, social designing misfortunes, considerable reputational misfortune, and

equipment misfortune. In like manner, a few supports give purchasers the decision of

choosing which arrangement will deal with their case on account of a business intrusion

misfortune where there might cover coverage with their property approach as well as a

social designing misfortune in which their wrongdoing strategy may react (XL, 2018).

AXA’s products coverage:

Third party liability

Data breach security and privacy liability

Media internet communication

First Party losses

Business interruption and extra expense

Loss/destruction of electronic assets

First party incident responses including IT forensics, notification costs, call centre,

and PR expenses

January 2019 5

530Coursework assignment 1 answer template

Privacy regulatory defence costs and coverage of regulatory fines and penalties

(where insurable by law) arising from a privacy or security wrongful act

Data restoration

Cyber extortion (XL, 2018).

These coverage policies influence buyers to buy this product and keep them safe from cyber

risk and increased demand lead to an increase in this product’s market share.

Conclusion

This report concluded that the market is continuing its digital transformation with no sign of

risks these digital facilities contains. On the other side hackers are becoming more

sophisticated at exploiting the networks and leak the confidential information to achieve their

goal and the amount of high profile case cyber-attacks are keeps increasing. These

breaches create more challenges for organizations to keep the latest security solutions. In

this context being the largest insurance provider across the world AXA having plenty of

opportunities. As the technology and digital environment develop, new risk will rise and

opportunity will appear as the demand for service and products develops.

Recommendations to increase market share

The potential for cyber insurance coverage to contribute to risk and loss reduction of the

company, management of this loss and market share can be increased id the market is able

to solve and reduce the most important risks and problems for the victim organizations. AXA

can possibly increase its market share and maximizing the contribution and coverage which

makes to deal with these quick evolving risks by analysing ways to deliver the fundamental

hindrances to market share improvement, especially over the accompanying policies:

Understanding impediments and gaps of the market: As misfortunes from digital

episodes increment, the advantages of and enthusiasm for having insurance coverage for

this hazard is expanding. Anyway, with the goal for coverage to turn out to be generally

accessible and receptive to request, there are a number of obstacles and holes in the market

(OCED, 2017). AXA ought to be urged to work further toward this path, and has to distribute

an arrangement report that could propose strategy suggestions that address the hindrances

to advertise improvement and the accessibility of digital insurance.

Improving the data available for quantifying exposures: Increasingly extensive

information on the recurrence and effect of cyber incidents (and the related cases payments)

would provide more trust in the endorsing of insurance coverage for cybercrime – AXA has

to provide greater clarity and quantify exposure that AXA is offering for cyber risks and crime

and furthermore, in which policies that coverage is being offered, involving: (I) a reasonable

proclamation about the coverage for cyber risk in customary policies; and (ii) blended

terminology for characterizing the coverage provided for various incidents types and losses

as well as noteworthy consistency as far as the triggers for that coverage, perceiving that

terminology may need to advance as the idea of cyber risk changes. AXA should mean to

keep extending the extent of coverage accommodated digital risk, involving for existing risk

not at present secured by insurance policies and for new kinds of losses that may develop

because of an advancing digital risks environment, while guaranteeing that the dangers

associated with any extended coverage provided are surely known and would not harm its

capacity to meet its commitments to policyholders. AXA needs to Reinsurance markets

(customary and elective) should keep on looking at policies to extend

January 2019 6

Privacy regulatory defence costs and coverage of regulatory fines and penalties

(where insurable by law) arising from a privacy or security wrongful act

Data restoration

Cyber extortion (XL, 2018).

These coverage policies influence buyers to buy this product and keep them safe from cyber

risk and increased demand lead to an increase in this product’s market share.

Conclusion

This report concluded that the market is continuing its digital transformation with no sign of

risks these digital facilities contains. On the other side hackers are becoming more

sophisticated at exploiting the networks and leak the confidential information to achieve their

goal and the amount of high profile case cyber-attacks are keeps increasing. These

breaches create more challenges for organizations to keep the latest security solutions. In

this context being the largest insurance provider across the world AXA having plenty of

opportunities. As the technology and digital environment develop, new risk will rise and

opportunity will appear as the demand for service and products develops.

Recommendations to increase market share

The potential for cyber insurance coverage to contribute to risk and loss reduction of the

company, management of this loss and market share can be increased id the market is able

to solve and reduce the most important risks and problems for the victim organizations. AXA

can possibly increase its market share and maximizing the contribution and coverage which

makes to deal with these quick evolving risks by analysing ways to deliver the fundamental

hindrances to market share improvement, especially over the accompanying policies:

Understanding impediments and gaps of the market: As misfortunes from digital

episodes increment, the advantages of and enthusiasm for having insurance coverage for

this hazard is expanding. Anyway, with the goal for coverage to turn out to be generally

accessible and receptive to request, there are a number of obstacles and holes in the market

(OCED, 2017). AXA ought to be urged to work further toward this path, and has to distribute

an arrangement report that could propose strategy suggestions that address the hindrances

to advertise improvement and the accessibility of digital insurance.

Improving the data available for quantifying exposures: Increasingly extensive

information on the recurrence and effect of cyber incidents (and the related cases payments)

would provide more trust in the endorsing of insurance coverage for cybercrime – AXA has

to provide greater clarity and quantify exposure that AXA is offering for cyber risks and crime

and furthermore, in which policies that coverage is being offered, involving: (I) a reasonable

proclamation about the coverage for cyber risk in customary policies; and (ii) blended

terminology for characterizing the coverage provided for various incidents types and losses

as well as noteworthy consistency as far as the triggers for that coverage, perceiving that

terminology may need to advance as the idea of cyber risk changes. AXA should mean to

keep extending the extent of coverage accommodated digital risk, involving for existing risk

not at present secured by insurance policies and for new kinds of losses that may develop

because of an advancing digital risks environment, while guaranteeing that the dangers

associated with any extended coverage provided are surely known and would not harm its

capacity to meet its commitments to policyholders. AXA needs to Reinsurance markets

(customary and elective) should keep on looking at policies to extend

January 2019 6

530Coursework assignment 1 answer template

the extent of coverage that they make accessible to essential safety net providers for cyber

risks that are surely known also, The company should make unmanageable dimensions of

conglomeration risk (OCED, 2018).

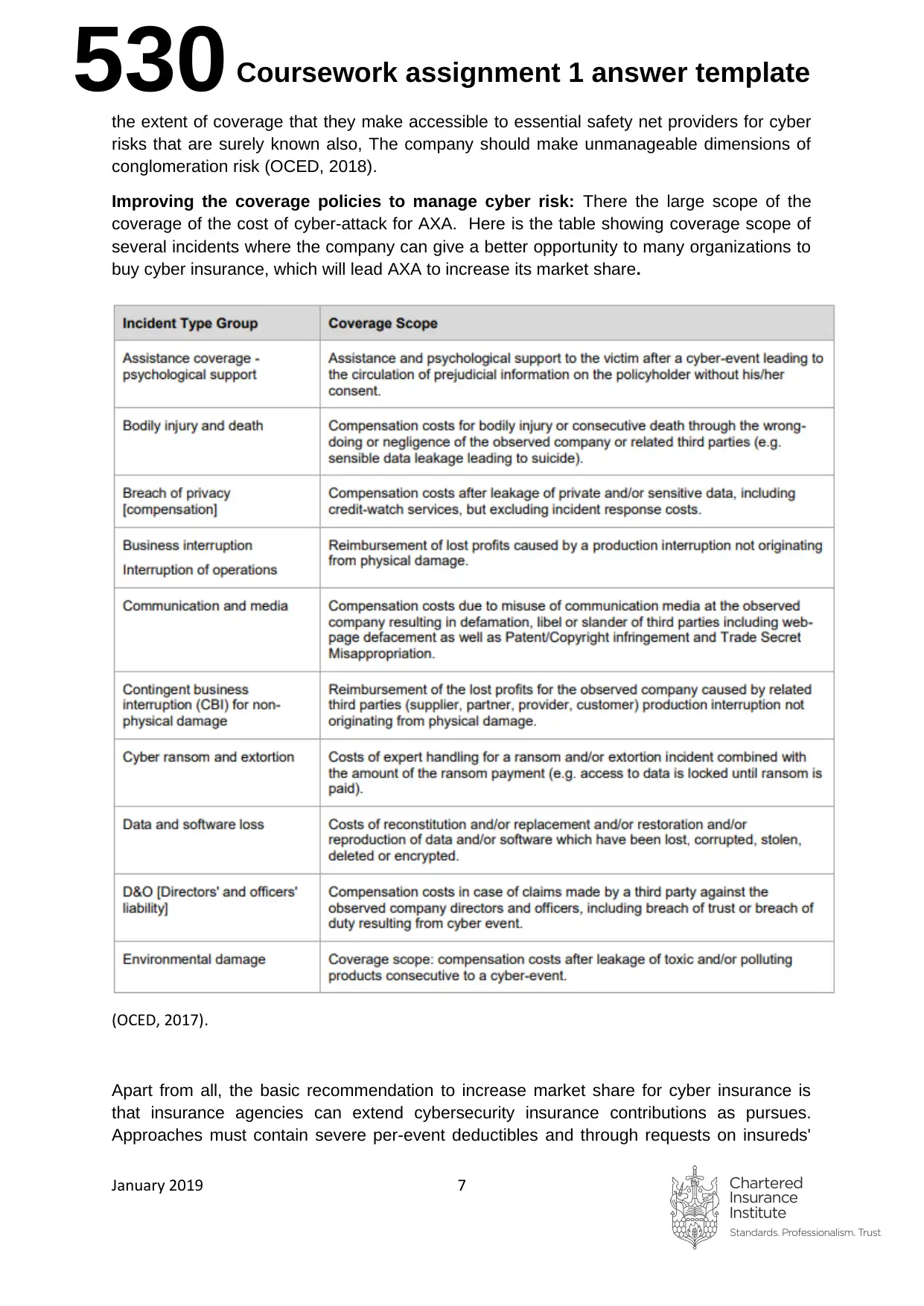

Improving the coverage policies to manage cyber risk: There the large scope of the

coverage of the cost of cyber-attack for AXA. Here is the table showing coverage scope of

several incidents where the company can give a better opportunity to many organizations to

buy cyber insurance, which will lead AXA to increase its market share.

(OCED, 2017).

Apart from all, the basic recommendation to increase market share for cyber insurance is

that insurance agencies can extend cybersecurity insurance contributions as pursues.

Approaches must contain severe per-event deductibles and through requests on insureds'

January 2019 7

the extent of coverage that they make accessible to essential safety net providers for cyber

risks that are surely known also, The company should make unmanageable dimensions of

conglomeration risk (OCED, 2018).

Improving the coverage policies to manage cyber risk: There the large scope of the

coverage of the cost of cyber-attack for AXA. Here is the table showing coverage scope of

several incidents where the company can give a better opportunity to many organizations to

buy cyber insurance, which will lead AXA to increase its market share.

(OCED, 2017).

Apart from all, the basic recommendation to increase market share for cyber insurance is

that insurance agencies can extend cybersecurity insurance contributions as pursues.

Approaches must contain severe per-event deductibles and through requests on insureds'

January 2019 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

530Coursework assignment 1 answer template

cybersecurity assurance. This will keep premiums moderate while urging insureds to

alleviate their dangers.

Points of confinement ought to be liberal on both per-events also, total bases, since bearers

are progressively capable to accept the danger of high-seriousness misfortunes than

insureds, and there is restricted open door for insureds to limit these low-recurrence

occasions. Coverage ought to be adaptable to address insureds' specific concerns.

While cyber risk is related with some staggering losses, a lack of information and lack of

accord in the technology world with respect to how to treat it, this is decisively why

statisticians' particular range of abilities and experience can include value. As I compose, the

biggest insurance organizations are growing their cyber liability teams, considering this

coverage's colossal potential. The individuals who can settle the riddles of digital coverage

and address their customers' issues will be remunerated. Opportunity thumps! (EIOPA ,

2018).

January 2019 8

cybersecurity assurance. This will keep premiums moderate while urging insureds to

alleviate their dangers.

Points of confinement ought to be liberal on both per-events also, total bases, since bearers

are progressively capable to accept the danger of high-seriousness misfortunes than

insureds, and there is restricted open door for insureds to limit these low-recurrence

occasions. Coverage ought to be adaptable to address insureds' specific concerns.

While cyber risk is related with some staggering losses, a lack of information and lack of

accord in the technology world with respect to how to treat it, this is decisively why

statisticians' particular range of abilities and experience can include value. As I compose, the

biggest insurance organizations are growing their cyber liability teams, considering this

coverage's colossal potential. The individuals who can settle the riddles of digital coverage

and address their customers' issues will be remunerated. Opportunity thumps! (EIOPA ,

2018).

January 2019 8

530Coursework assignment 1 answer template

Referencing must be completed before submission

All sources must be referenced in the body of your answer as well as in your reference list. See

the 530 Specimen coursework assignment and answer for examples of how to reference

correctly in text and in your reference list.

References

AON, 2017. Global Cybe Markey Overview. [Online]

Available at: https://www.aon.com/inpoint/bin/pdfs/white-papers/Cyber.pdf

Ashford, W., 2018. Cyber crime in UK. [Online]

Available at: https://www.computerweekly.com/news/252433873/Business-cyber-crime-up-

63-UK-stats-show

AXA, 2018. About us. [Online]

Available at: https://axainsurancecompany.com/

EIOPA , 2018. Understanding Cyber insurance. [Online]

Available at: https://eiopa.europa.eu/Publications/Reports/EIOPA%20Understanding

%20cyber%20insurance.pdf

Gittle, J. C. a. J., 2019. Cyber insurance market: The year in review. [Online]

Available at: https://axaxl.com/fast-fast-forward/articles/cyber-insurance-market_the-year-in-

review

Groot, J. D., 2019. What is the General DataProtection Regulation? Understanding &

Complying with GDPR Requirements in 2019. [Online]

Available at: https://digitalguardian.com/blog/what-gdpr-general-data-protection-regulation-

understanding-and-complying-gdpr-data-protection

Insurance Journal, 2018. AXA XL, Slice Labs Launch On-Demand Cyber Coverage for

Small, Mid-Size Businesses. Insurace journal.

KPMG, 2017. Digital paymentsAnalysing the. [Online]

Available at: https://assets.kpmg/content/dam/kpmg/ca/pdf/2017/04/digital-payments-

analysing-the-cyber-landscape-kpmg-canada.pdf

Les, D., Burrlow, J. L. & Kleindl, B., 2011. Principles of Business. s.l.:Cengage Learning.

Mason, J., 2019. 14 Most Alarming Cyber Security Statistics in 2019. [Online]

Available at: https://thebestvpn.com/cyber-security-statistics-2019/

OCED, 2017. Supporting an effective Cyber insurance market. [Online]

Available at: https://www.oecd.org/daf/fin/insurance/Supporting-an-effective-cyber-

insurance-market.pdf

OCED, 2018. Unleashing the Potential of Cyber insurance. [Online]

Available at: https://www.oecd.org/daf/fin/insurance/Unleashing-Potential-Cyber-Insurance-

Market-Summary.pdf

January 2019 9

Referencing must be completed before submission

All sources must be referenced in the body of your answer as well as in your reference list. See

the 530 Specimen coursework assignment and answer for examples of how to reference

correctly in text and in your reference list.

References

AON, 2017. Global Cybe Markey Overview. [Online]

Available at: https://www.aon.com/inpoint/bin/pdfs/white-papers/Cyber.pdf

Ashford, W., 2018. Cyber crime in UK. [Online]

Available at: https://www.computerweekly.com/news/252433873/Business-cyber-crime-up-

63-UK-stats-show

AXA, 2018. About us. [Online]

Available at: https://axainsurancecompany.com/

EIOPA , 2018. Understanding Cyber insurance. [Online]

Available at: https://eiopa.europa.eu/Publications/Reports/EIOPA%20Understanding

%20cyber%20insurance.pdf

Gittle, J. C. a. J., 2019. Cyber insurance market: The year in review. [Online]

Available at: https://axaxl.com/fast-fast-forward/articles/cyber-insurance-market_the-year-in-

review

Groot, J. D., 2019. What is the General DataProtection Regulation? Understanding &

Complying with GDPR Requirements in 2019. [Online]

Available at: https://digitalguardian.com/blog/what-gdpr-general-data-protection-regulation-

understanding-and-complying-gdpr-data-protection

Insurance Journal, 2018. AXA XL, Slice Labs Launch On-Demand Cyber Coverage for

Small, Mid-Size Businesses. Insurace journal.

KPMG, 2017. Digital paymentsAnalysing the. [Online]

Available at: https://assets.kpmg/content/dam/kpmg/ca/pdf/2017/04/digital-payments-

analysing-the-cyber-landscape-kpmg-canada.pdf

Les, D., Burrlow, J. L. & Kleindl, B., 2011. Principles of Business. s.l.:Cengage Learning.

Mason, J., 2019. 14 Most Alarming Cyber Security Statistics in 2019. [Online]

Available at: https://thebestvpn.com/cyber-security-statistics-2019/

OCED, 2017. Supporting an effective Cyber insurance market. [Online]

Available at: https://www.oecd.org/daf/fin/insurance/Supporting-an-effective-cyber-

insurance-market.pdf

OCED, 2018. Unleashing the Potential of Cyber insurance. [Online]

Available at: https://www.oecd.org/daf/fin/insurance/Unleashing-Potential-Cyber-Insurance-

Market-Summary.pdf

January 2019 9

530Coursework assignment 1 answer template

Secretan, P., 2018. Aquaculture insurance. [Online]

Available at: http://www.fao.org/3/a1455e/a1455e02.pdf

Serpa, J. a. K. H., 2016. The strategic role of business insurance.. Management Science.,

pp. 384-404.

Thomas, B., 2018. The role of Cyber Insurance (and why it’s important). [Online]

Available at: https://www.proteanrisk.com/insights/2018/the-role-of-cyber-insurance/

XL, A., 2018. AXA- Cyber insurance. [Online]

Available at: https://axaxl.com/insurance/insurance-coverage/professional-insurance/cyber-

and-technology

Glossary of key words

Analyse

Find the relevant facts and examine these in depth. Examine the relationship between

various facts and make conclusions or recommendations.

Construct

To build or make something; construct a table.

Describe

Give an account in words (someone or something) including all relevant characteristics,

qualities or events.

Devise

To plan or create a method, procedure or system.

Discuss

To consider something in detail; examining the different ideas and opinions about

something, for example to weigh up alternative views.

Explain

To make something clear and easy to understand with reasoning and/or justification.

Identify

Recognise and name.

Justify

Support an argument or conclusion. Prove or show grounds for a decision.

Outline

Give a general description briefly showing the essential features.

January 2019 10

Secretan, P., 2018. Aquaculture insurance. [Online]

Available at: http://www.fao.org/3/a1455e/a1455e02.pdf

Serpa, J. a. K. H., 2016. The strategic role of business insurance.. Management Science.,

pp. 384-404.

Thomas, B., 2018. The role of Cyber Insurance (and why it’s important). [Online]

Available at: https://www.proteanrisk.com/insights/2018/the-role-of-cyber-insurance/

XL, A., 2018. AXA- Cyber insurance. [Online]

Available at: https://axaxl.com/insurance/insurance-coverage/professional-insurance/cyber-

and-technology

Glossary of key words

Analyse

Find the relevant facts and examine these in depth. Examine the relationship between

various facts and make conclusions or recommendations.

Construct

To build or make something; construct a table.

Describe

Give an account in words (someone or something) including all relevant characteristics,

qualities or events.

Devise

To plan or create a method, procedure or system.

Discuss

To consider something in detail; examining the different ideas and opinions about

something, for example to weigh up alternative views.

Explain

To make something clear and easy to understand with reasoning and/or justification.

Identify

Recognise and name.

Justify

Support an argument or conclusion. Prove or show grounds for a decision.

Outline

Give a general description briefly showing the essential features.

January 2019 10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

530Coursework assignment 1 answer template

Recommend with reasons

Provide reasons in favour.

State

Express main points in brief, clear form.

January 2019 11

Recommend with reasons

Provide reasons in favour.

State

Express main points in brief, clear form.

January 2019 11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.