Corporate Accounting ACC202: Essay on Fair Value Accounting

VerifiedAdded on 2022/11/17

|9

|1799

|173

Essay

AI Summary

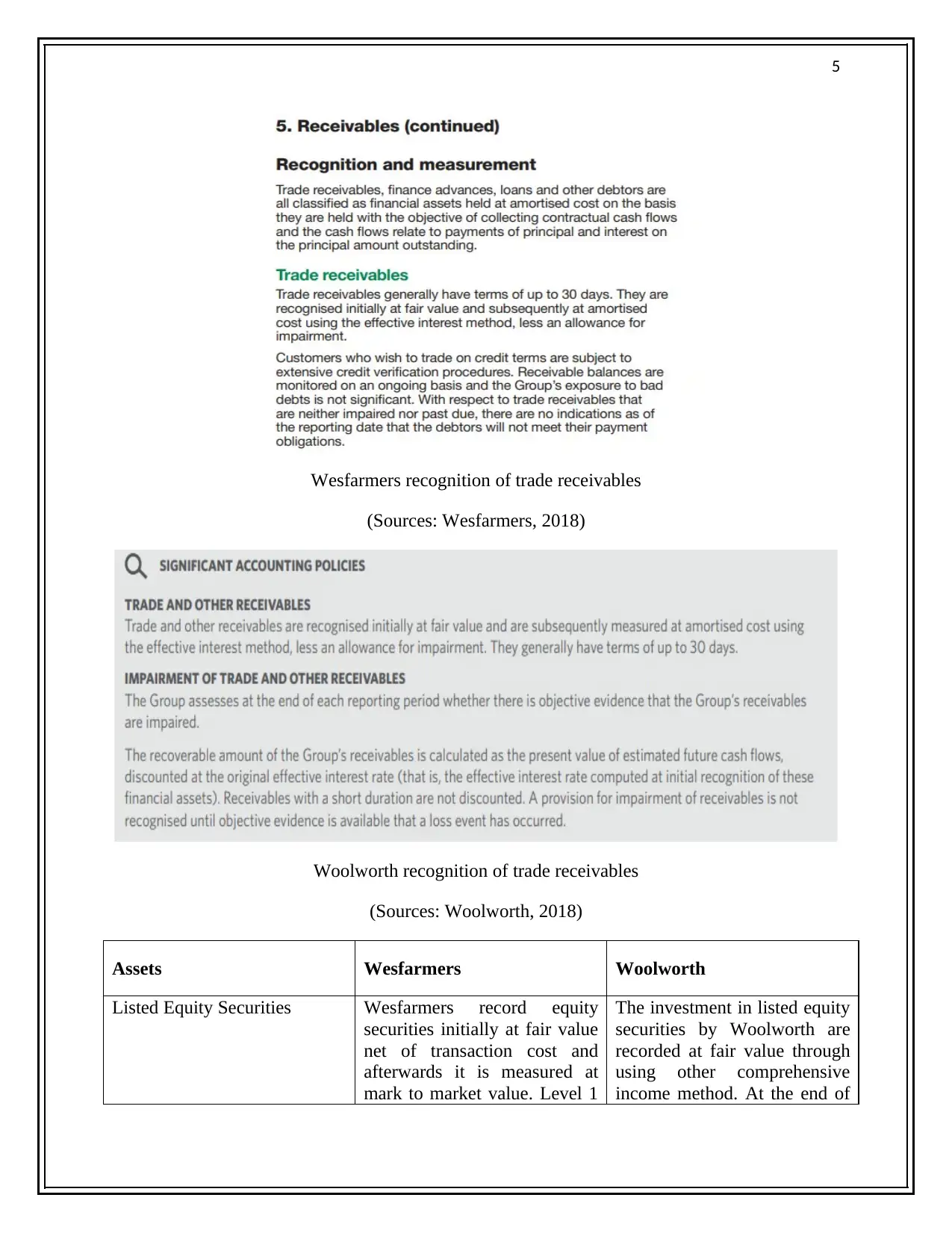

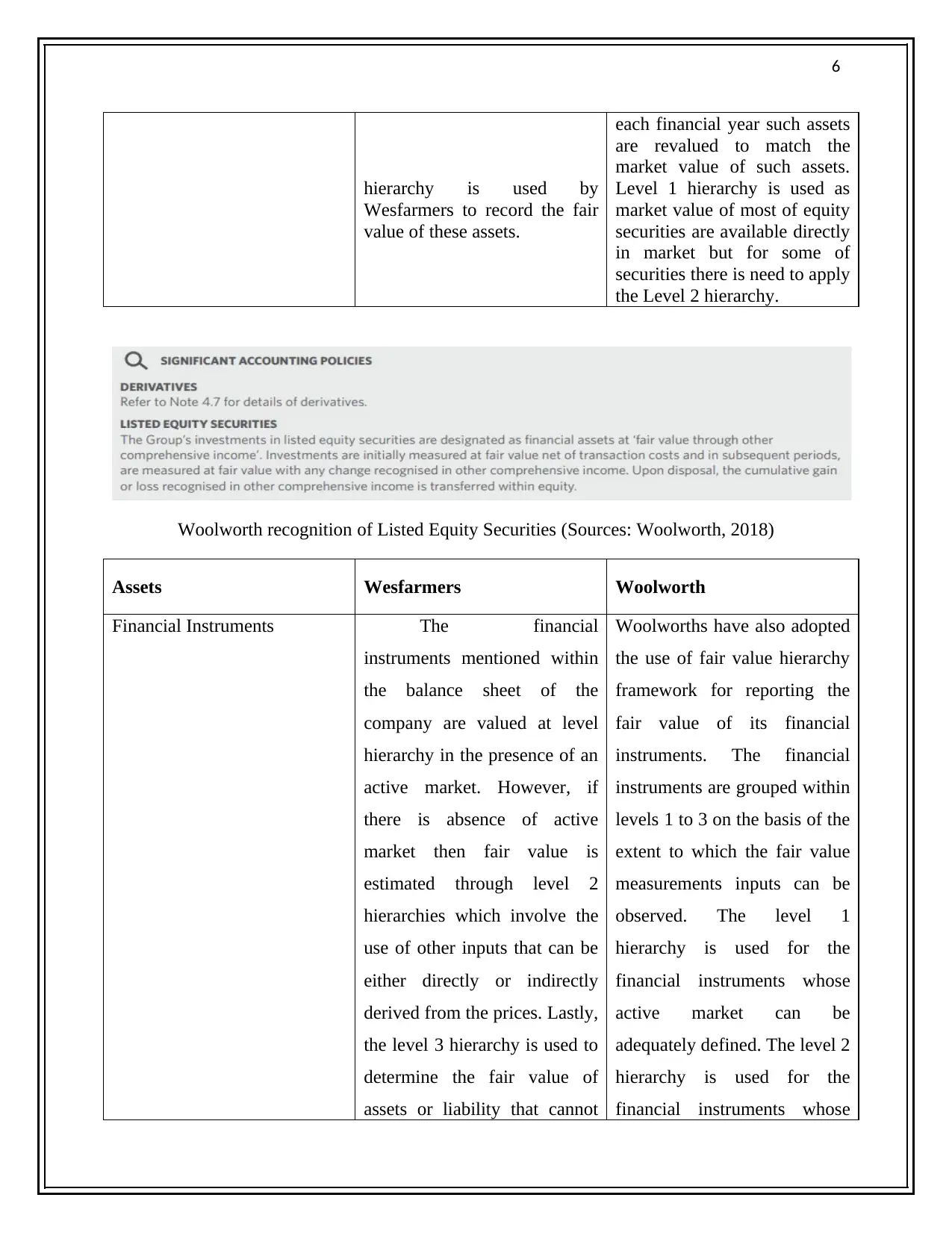

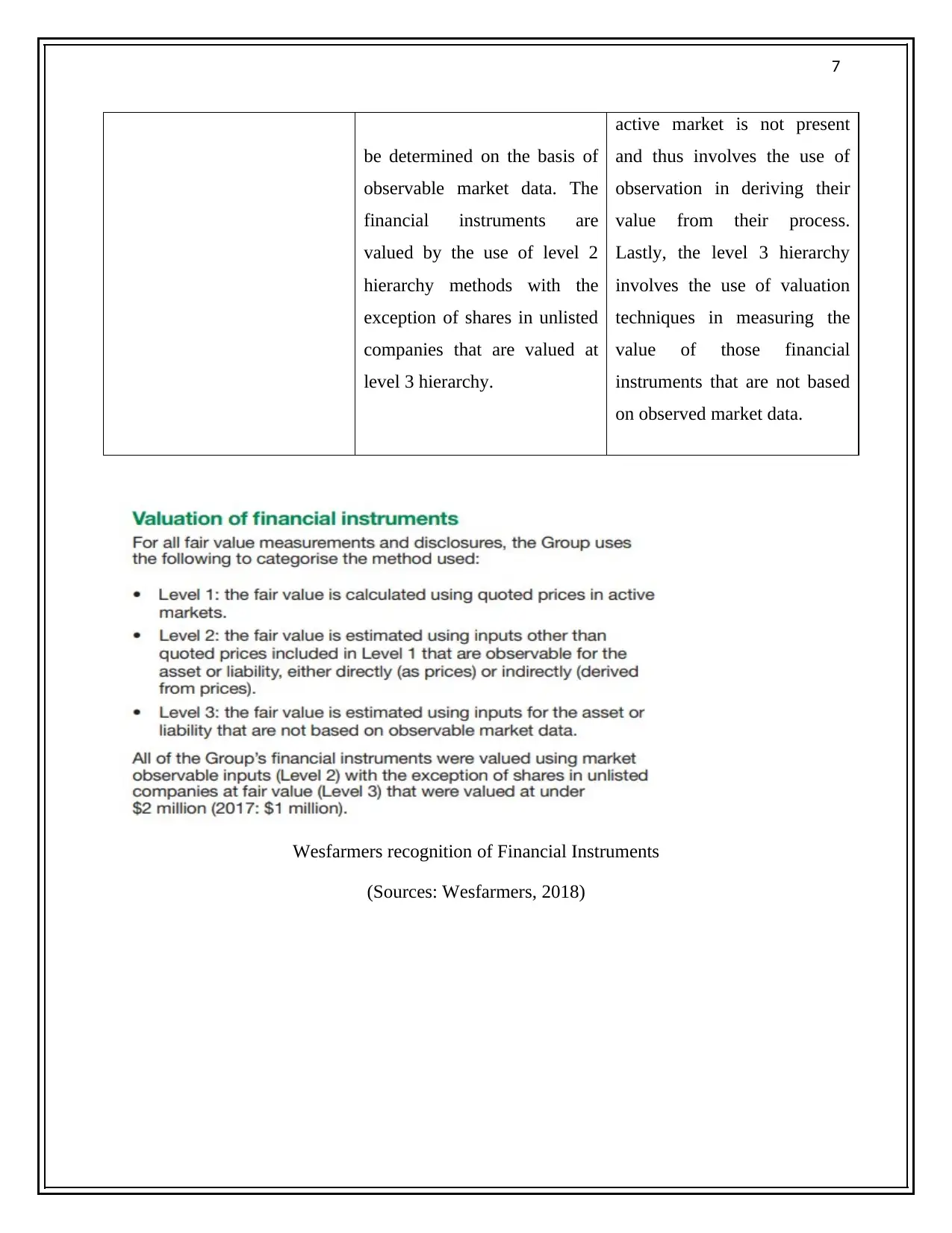

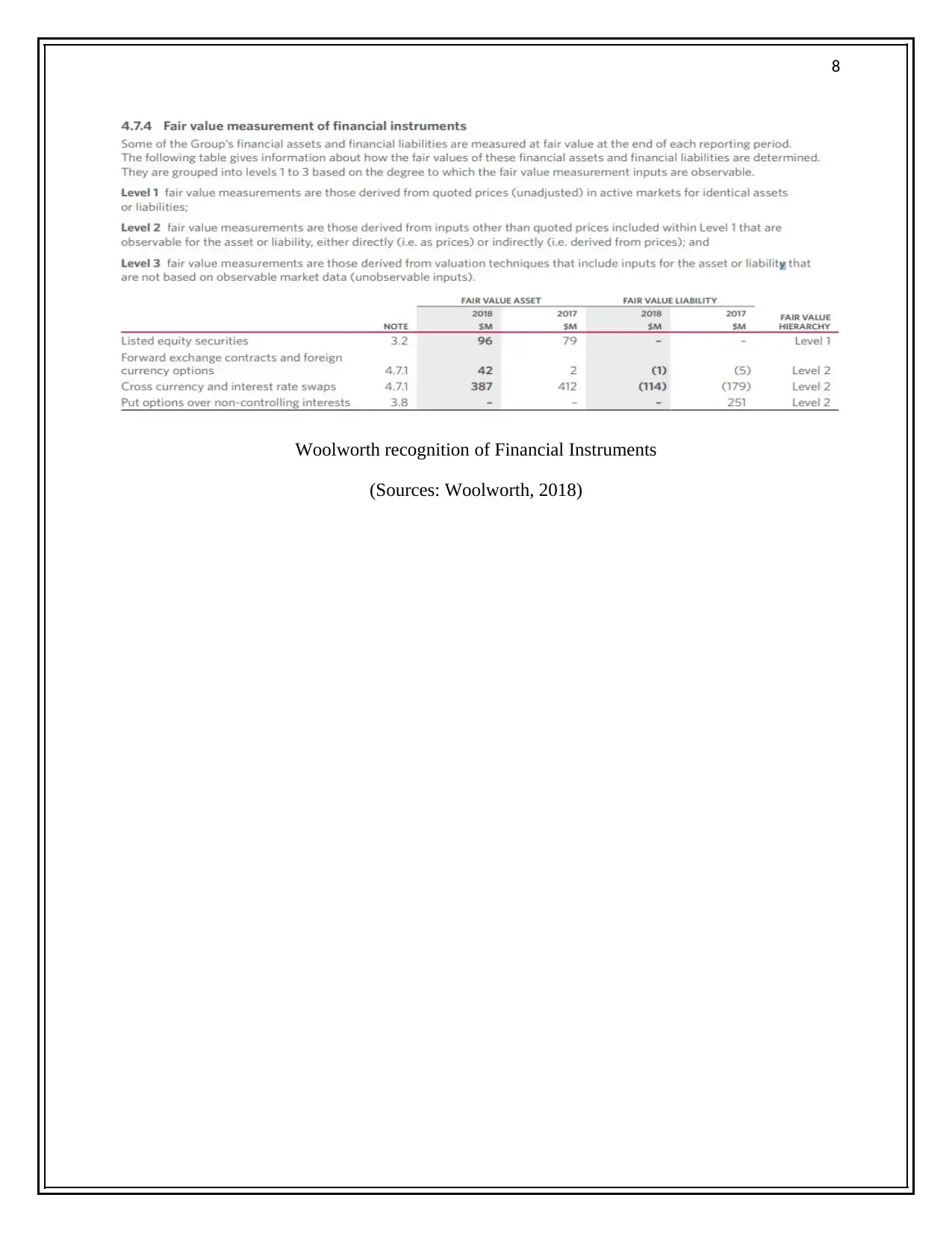

This essay delves into the importance of employing a suitable measurement approach for the development and presentation of financial information within corporate accounts, with a specific focus on fair value accounting. It examines the relevance of fair value accounting in the modern business environment, highlighting its applicability across various private and public sector organizations. The essay also evaluates the impact of fair value accounting on financial crises, such as the subprime mortgage crisis. Part B includes a case study comparing Wesfarmers and Woolworths, analyzing their application of fair value accounting for assets like accounts receivables, equity securities, and financial instruments, referencing their 2018 annual reports and the fair value hierarchy levels used. The essay references the works of Laux and Leuz (2009), Whittington (2008) and other academic sources.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.