Audit Test Assignment - Finance Module, Semester 1, University

VerifiedAdded on 2021/10/19

|9

|2225

|39

Homework Assignment

AI Summary

This assignment provides a comprehensive analysis of audit tests, covering various aspects of financial auditing. It begins by examining management assertions and audit objectives related to accounts receivable, followed by an analysis of cash receipts using sampling techniques. The assignment then delves into the types of audit evidence and their corresponding management assertions, providing practical examples. Further, it explores management assertions and persuasive evidence in different scenarios. A significant portion of the assignment addresses internal control weaknesses, specifically focusing on the materiality of such weaknesses. Finally, the assignment concludes with an application of Monetary Unit Sampling (MUS) to assess the accuracy of financial accounts, including calculations and interpretations of the results, providing a practical understanding of audit procedures and their implications.

Audit Test Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

By student name

Professor

University

Date: 25 April 2018.

1 | P a g e

2

Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................3

Question 5...................................................................................................................................................4

Question 6...................................................................................................................................................5

Question 7...................................................................................................................................................5

Question 8...................................................................................................................................................6

Multiple Choice...........................................................................................................................................7

References...................................................................................................................................................8

2 | P a g e

Contents

Question 1...................................................................................................................................................3

Question 2...................................................................................................................................................3

Question 5...................................................................................................................................................4

Question 6...................................................................................................................................................5

Question 7...................................................................................................................................................5

Question 8...................................................................................................................................................6

Multiple Choice...........................................................................................................................................7

References...................................................................................................................................................8

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

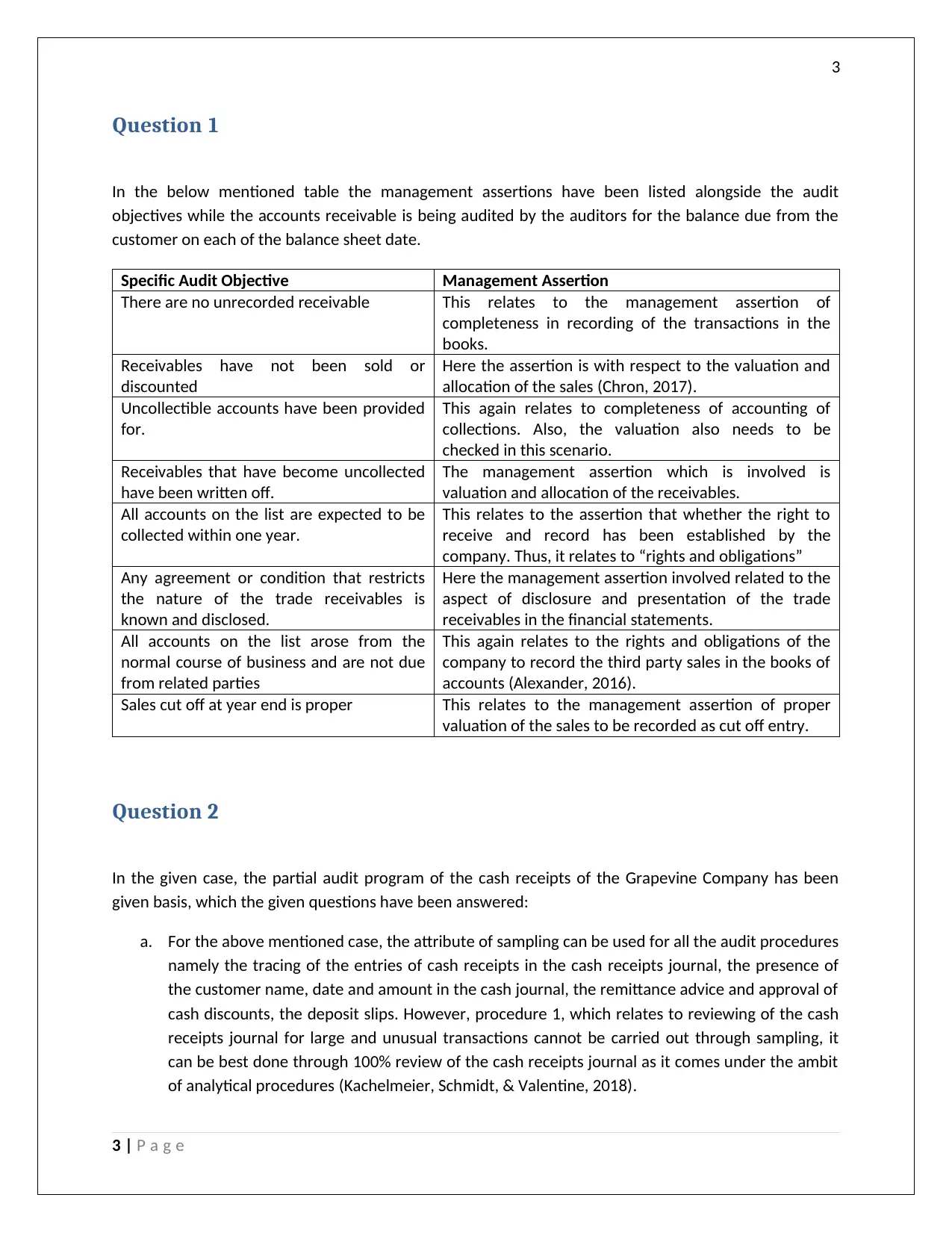

Question 1

In the below mentioned table the management assertions have been listed alongside the audit

objectives while the accounts receivable is being audited by the auditors for the balance due from the

customer on each of the balance sheet date.

Specific Audit Objective Management Assertion

There are no unrecorded receivable This relates to the management assertion of

completeness in recording of the transactions in the

books.

Receivables have not been sold or

discounted

Here the assertion is with respect to the valuation and

allocation of the sales (Chron, 2017).

Uncollectible accounts have been provided

for.

This again relates to completeness of accounting of

collections. Also, the valuation also needs to be

checked in this scenario.

Receivables that have become uncollected

have been written off.

The management assertion which is involved is

valuation and allocation of the receivables.

All accounts on the list are expected to be

collected within one year.

This relates to the assertion that whether the right to

receive and record has been established by the

company. Thus, it relates to “rights and obligations”

Any agreement or condition that restricts

the nature of the trade receivables is

known and disclosed.

Here the management assertion involved related to the

aspect of disclosure and presentation of the trade

receivables in the financial statements.

All accounts on the list arose from the

normal course of business and are not due

from related parties

This again relates to the rights and obligations of the

company to record the third party sales in the books of

accounts (Alexander, 2016).

Sales cut off at year end is proper This relates to the management assertion of proper

valuation of the sales to be recorded as cut off entry.

Question 2

In the given case, the partial audit program of the cash receipts of the Grapevine Company has been

given basis, which the given questions have been answered:

a. For the above mentioned case, the attribute of sampling can be used for all the audit procedures

namely the tracing of the entries of cash receipts in the cash receipts journal, the presence of

the customer name, date and amount in the cash journal, the remittance advice and approval of

cash discounts, the deposit slips. However, procedure 1, which relates to reviewing of the cash

receipts journal for large and unusual transactions cannot be carried out through sampling, it

can be best done through 100% review of the cash receipts journal as it comes under the ambit

of analytical procedures (Kachelmeier, Schmidt, & Valentine, 2018).

3 | P a g e

Question 1

In the below mentioned table the management assertions have been listed alongside the audit

objectives while the accounts receivable is being audited by the auditors for the balance due from the

customer on each of the balance sheet date.

Specific Audit Objective Management Assertion

There are no unrecorded receivable This relates to the management assertion of

completeness in recording of the transactions in the

books.

Receivables have not been sold or

discounted

Here the assertion is with respect to the valuation and

allocation of the sales (Chron, 2017).

Uncollectible accounts have been provided

for.

This again relates to completeness of accounting of

collections. Also, the valuation also needs to be

checked in this scenario.

Receivables that have become uncollected

have been written off.

The management assertion which is involved is

valuation and allocation of the receivables.

All accounts on the list are expected to be

collected within one year.

This relates to the assertion that whether the right to

receive and record has been established by the

company. Thus, it relates to “rights and obligations”

Any agreement or condition that restricts

the nature of the trade receivables is

known and disclosed.

Here the management assertion involved related to the

aspect of disclosure and presentation of the trade

receivables in the financial statements.

All accounts on the list arose from the

normal course of business and are not due

from related parties

This again relates to the rights and obligations of the

company to record the third party sales in the books of

accounts (Alexander, 2016).

Sales cut off at year end is proper This relates to the management assertion of proper

valuation of the sales to be recorded as cut off entry.

Question 2

In the given case, the partial audit program of the cash receipts of the Grapevine Company has been

given basis, which the given questions have been answered:

a. For the above mentioned case, the attribute of sampling can be used for all the audit procedures

namely the tracing of the entries of cash receipts in the cash receipts journal, the presence of

the customer name, date and amount in the cash journal, the remittance advice and approval of

cash discounts, the deposit slips. However, procedure 1, which relates to reviewing of the cash

receipts journal for large and unusual transactions cannot be carried out through sampling, it

can be best done through 100% review of the cash receipts journal as it comes under the ambit

of analytical procedures (Kachelmeier, Schmidt, & Valentine, 2018).

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

b. The primary emphasis or the management assertion about the above test of sampling will be on

the line item basis or the date on which the prelisting of the cash receipts was being prepared.

In case the audit procedure 2 and 5 is being focused, then we can see that the primary emphasis

is on completeness in recording of the transactions. In case the prelisting of the cash receipts is

being verified, then all the other audit procedures can be conducted effectively and efficiently.

c. The sampling unit for each of the audit procedure has been listed below:

Audit

Procedure

Appropriate Sampling Unit

2 To check if all the cash receipts have been appropriately recorded in the cash

receipts journal.

3 The name of the customer, the date and the amount should be same and equal

in the prelisting and the cash receipts journal (Goldmann, 2016).

4 To check if all the cash discounts which have been allowed have been approved.

5 To check if the cash which has been included in the prelisting was there in the

deposit slip as well.

d. The exceptions which would indicate that the operating control is not working effectively has

been shown below:

1. The name of the Customer, the date and the amount of the transaction does not matches to

that which has been listed in the cash receipts journal.

2. Cash discounts have been given to the customer and have been availed by the customers

but the same has not been approved (Choy, 2018).

Question 5

In the following case, the type of the audit evidence and the management assertion has been specified

against each of the case studies:

Sl. No. Type of Audit evidence Management Assertion

1 The auditor should check on the

collectability ratio of the past years and the

confirmation of the balances from the

debtors.

The management assertion here relates to if

the valuation of the debtors has been done

correctly and whether the right to record the

receivables has been established.

2 The audit evidences here will be the

shipping bills and the amount recorded in

the sales journal (Raiborn, Butler, & Martin,

2016).

The management assertion here will be the

completeness in recording of transactions.

3 The physical stock count sheet and the

inventory records in the system.

Existence of the physical inventory in the

warehouse compared to what is reflected as

per records.

4 The Sales invoices in the chronological The completeness in recording of all the

4 | P a g e

b. The primary emphasis or the management assertion about the above test of sampling will be on

the line item basis or the date on which the prelisting of the cash receipts was being prepared.

In case the audit procedure 2 and 5 is being focused, then we can see that the primary emphasis

is on completeness in recording of the transactions. In case the prelisting of the cash receipts is

being verified, then all the other audit procedures can be conducted effectively and efficiently.

c. The sampling unit for each of the audit procedure has been listed below:

Audit

Procedure

Appropriate Sampling Unit

2 To check if all the cash receipts have been appropriately recorded in the cash

receipts journal.

3 The name of the customer, the date and the amount should be same and equal

in the prelisting and the cash receipts journal (Goldmann, 2016).

4 To check if all the cash discounts which have been allowed have been approved.

5 To check if the cash which has been included in the prelisting was there in the

deposit slip as well.

d. The exceptions which would indicate that the operating control is not working effectively has

been shown below:

1. The name of the Customer, the date and the amount of the transaction does not matches to

that which has been listed in the cash receipts journal.

2. Cash discounts have been given to the customer and have been availed by the customers

but the same has not been approved (Choy, 2018).

Question 5

In the following case, the type of the audit evidence and the management assertion has been specified

against each of the case studies:

Sl. No. Type of Audit evidence Management Assertion

1 The auditor should check on the

collectability ratio of the past years and the

confirmation of the balances from the

debtors.

The management assertion here relates to if

the valuation of the debtors has been done

correctly and whether the right to record the

receivables has been established.

2 The audit evidences here will be the

shipping bills and the amount recorded in

the sales journal (Raiborn, Butler, & Martin,

2016).

The management assertion here will be the

completeness in recording of transactions.

3 The physical stock count sheet and the

inventory records in the system.

Existence of the physical inventory in the

warehouse compared to what is reflected as

per records.

4 The Sales invoices in the chronological The completeness in recording of all the

4 | P a g e

5

order and the sales journal listing. transactions in the sales journal would be the

assertion here.

5 The signature and the date and time on the

document stated (Jefferson, 2017).

Existence of the inventory with the company.

6 The approval regarding the withdrawal and

the deposit of the petty cash and the

frequency of the same.

The accuracy and completeness in recording

of the petty cash amount.

Question 6

The management assertion with respect to the given situations and the most persuasive evidence in this

regard has been stated below:

Sl. No. Management Assertion Most persuasive and why?

1(a) Valuation and existence of the

creditors as on the given date

The most persuasive evidence in this regard would

be the balance confirmation from the creditors or

vendors as it would help in checking both balances

as well as payments.

1(b) Completeness in recording of the

transaction of payment to vendors

and suppliers.

2(a) Completeness in recording of

transactions

The bank reconciliation statement would be the

most conclusive evidence in this regard as it would

help in reconciling both the year end bank balance

with the client’s banking institution and the bank

statement of the client.

2(b) Whether the cut off entries have

been passed accurately (Kew &

Stredwick, 2017).

3(a) The existence of inventory in the

warehouse needs to be checked.

The most persuasive evidence in this regard would

be the physical inventory records and the register in

which the inventory in and out is being recorded and

to reconcile the same with the system records.

3(b) The accuracy in the process of

client’s count of existing inventory

needs to be checked and evaluated.

Question 7

In the given case, Alana, a NSNG employee has been reconciling the bank statement with the cash

records but since she has not been taught how to do so, she has been doing it incorrectly for last 2

years. In order to determine whether it is a control weakness and if the same is material, the auditor

would first check on its likelihood and the magnitude and frequency (Lessambo, 2018). The event would

be significant or material only in case the likelihood of the event is probable or reasonably possible. In

the given case, the deficiency in control is quite probably prima facie, as the auditor also knows that the

requisite control has not been exercised for last 2 years. Once the likelihood has been established, the

auditor will now check on the magnitude of the misstatement. A misstatement is considered material,

5 | P a g e

order and the sales journal listing. transactions in the sales journal would be the

assertion here.

5 The signature and the date and time on the

document stated (Jefferson, 2017).

Existence of the inventory with the company.

6 The approval regarding the withdrawal and

the deposit of the petty cash and the

frequency of the same.

The accuracy and completeness in recording

of the petty cash amount.

Question 6

The management assertion with respect to the given situations and the most persuasive evidence in this

regard has been stated below:

Sl. No. Management Assertion Most persuasive and why?

1(a) Valuation and existence of the

creditors as on the given date

The most persuasive evidence in this regard would

be the balance confirmation from the creditors or

vendors as it would help in checking both balances

as well as payments.

1(b) Completeness in recording of the

transaction of payment to vendors

and suppliers.

2(a) Completeness in recording of

transactions

The bank reconciliation statement would be the

most conclusive evidence in this regard as it would

help in reconciling both the year end bank balance

with the client’s banking institution and the bank

statement of the client.

2(b) Whether the cut off entries have

been passed accurately (Kew &

Stredwick, 2017).

3(a) The existence of inventory in the

warehouse needs to be checked.

The most persuasive evidence in this regard would

be the physical inventory records and the register in

which the inventory in and out is being recorded and

to reconcile the same with the system records.

3(b) The accuracy in the process of

client’s count of existing inventory

needs to be checked and evaluated.

Question 7

In the given case, Alana, a NSNG employee has been reconciling the bank statement with the cash

records but since she has not been taught how to do so, she has been doing it incorrectly for last 2

years. In order to determine whether it is a control weakness and if the same is material, the auditor

would first check on its likelihood and the magnitude and frequency (Lessambo, 2018). The event would

be significant or material only in case the likelihood of the event is probable or reasonably possible. In

the given case, the deficiency in control is quite probably prima facie, as the auditor also knows that the

requisite control has not been exercised for last 2 years. Once the likelihood has been established, the

auditor will now check on the magnitude of the misstatement. A misstatement is considered material,

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

individual or in aggregate only if it has, the ability to change the decision of the economic users or else it

would be considered immaterial. A case where the chances are remote or less and the magnitude is low

then the same would be insignificant deficiency (Heminway, 2017). Significant deficiency is the situation

when there is a reasonable possibility of the misstatement but it is also known that the same is not

material but significant. Finally, material weakness is a situation where there is a significant deficiency as

well as the possibility of the misstatements is high as well as material.

As per the above definitions, the given case falls in the category of “material weakness”.

Question 8

In the given case, three CPAs namely Mary, Maria, & Mariah have decided to use Monetary Unit

Sampling to do the audit of Tom Music Store and its receivables accounts. It is also called probability-

proportional-to-size or dollar-unit sampling, to determine the accuracy of financial accounts. The

following is the calculation:

1. Ratio of expected to tolerable misstatement = 37500/150000 = 25%

Tolerable misstatement as a percentage of the population = 150000/2500000 = 6%

The sample size would therefore be 37500 and the sampling interval would be 66.67, which is

nearly 67.

2. The following table gives the output:

Recorded Amount Audit Amount Understatement/

overstatement

First misstatement 15000 12000 Overstatement – 3000

Second misstatement 5000 1000 Overstatement – 4000

Third misstatement 60000 50000 Overstatement – 10000

3. Given the results above, all of which shows the overstatement of the accounts receivable, it

shows that the company Tom Music Store has not made the fair representation of the Accounts

Receivable.

4. As per the above calculations, the amount of known misstatements in the Accounts Receivable

is altogether 17000 of the sample of 80000, which is near to 21.25% and is material.

6 | P a g e

individual or in aggregate only if it has, the ability to change the decision of the economic users or else it

would be considered immaterial. A case where the chances are remote or less and the magnitude is low

then the same would be insignificant deficiency (Heminway, 2017). Significant deficiency is the situation

when there is a reasonable possibility of the misstatement but it is also known that the same is not

material but significant. Finally, material weakness is a situation where there is a significant deficiency as

well as the possibility of the misstatements is high as well as material.

As per the above definitions, the given case falls in the category of “material weakness”.

Question 8

In the given case, three CPAs namely Mary, Maria, & Mariah have decided to use Monetary Unit

Sampling to do the audit of Tom Music Store and its receivables accounts. It is also called probability-

proportional-to-size or dollar-unit sampling, to determine the accuracy of financial accounts. The

following is the calculation:

1. Ratio of expected to tolerable misstatement = 37500/150000 = 25%

Tolerable misstatement as a percentage of the population = 150000/2500000 = 6%

The sample size would therefore be 37500 and the sampling interval would be 66.67, which is

nearly 67.

2. The following table gives the output:

Recorded Amount Audit Amount Understatement/

overstatement

First misstatement 15000 12000 Overstatement – 3000

Second misstatement 5000 1000 Overstatement – 4000

Third misstatement 60000 50000 Overstatement – 10000

3. Given the results above, all of which shows the overstatement of the accounts receivable, it

shows that the company Tom Music Store has not made the fair representation of the Accounts

Receivable.

4. As per the above calculations, the amount of known misstatements in the Accounts Receivable

is altogether 17000 of the sample of 80000, which is near to 21.25% and is material.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Multiple Choice

1. D. areas that may represent specific risks relevant to the audit.

2. C. Relationships involving income statement accounts

3. C. Additional tests of details are required

4. B. Management’s disregard of its responsibility to maintain an adequate control environment.

5. A. Scanning the general journal for unusual entries

6. B. The absence of misstatements in financial statements is considered evidence that the existing

controls are effective.

7. D. A requirement that management of the publicly traded company issues an assessment

regarding the efficiency of internal control for the year.

8. C. Qualified Opinion

9. D. Is comprised of audits of internal control over financial reporting and of financial statements

10. A. Affect the financial statement assertions

11. B. Creates a commitment for competence

12. A. Increased implementation of substantive audit procedures

13. B. Observation and Inquiry

14. C. Timing of substantive procedures from year-end to an interim date.

7 | P a g e

Multiple Choice

1. D. areas that may represent specific risks relevant to the audit.

2. C. Relationships involving income statement accounts

3. C. Additional tests of details are required

4. B. Management’s disregard of its responsibility to maintain an adequate control environment.

5. A. Scanning the general journal for unusual entries

6. B. The absence of misstatements in financial statements is considered evidence that the existing

controls are effective.

7. D. A requirement that management of the publicly traded company issues an assessment

regarding the efficiency of internal control for the year.

8. C. Qualified Opinion

9. D. Is comprised of audits of internal control over financial reporting and of financial statements

10. A. Affect the financial statement assertions

11. B. Creates a commitment for competence

12. A. Increased implementation of substantive audit procedures

13. B. Observation and Inquiry

14. C. Timing of substantive procedures from year-end to an interim date.

7 | P a g e

8

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07, 2017,

from http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kachelmeier, S., Schmidt, J., & Valentine, K. (2018). The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), 1-39.

Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (second ed.).

London: Chartered Institute of Personnel and Development.

Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), 183-202.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

8 | P a g e

References

Alexander, F. (2016). The Changing Face of Accountability. The Journal of Higher Education, 71(4), 411-

431.

Choy, Y. K. (2018). Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 145. Retrieved from

https://doi.org/10.1016/j.ecolecon.2017.08.005

Chron. (2017). five-common-features-internal-control-system-business. Retrieved december 07, 2017,

from http://smallbusiness.chron.com/five-common-features-internal-control-system-business-

430.html

Goldmann, K. (2016). Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, 4(3), 103-112.

Heminway, J. (2017). Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 1-35.

Jefferson, M. (2017). Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland .

Technological Forecasting and Social Change, 353-354.

Kachelmeier, S., Schmidt, J., & Valentine, K. (2018). The disclaimer effect of disclosing critical audit

matters in the auditor’s report. SSRN, 2(1), 1-39.

Kew, J., & Stredwick, J. (2017). Business Environment: Managing in a Strategic Context (second ed.).

London: Chartered Institute of Personnel and Development.

Lessambo, F. (2018). Audit Risks: Identification and Procedures. Auditing, Assurance Services, and

Forensics, 3(1), 183-202.

Raiborn, C., Butler, J., & Martin, K. (2016). The internal audit function: A prerequisite for Good

Governance. Journal of Corporate Accounting and Finance, 28(2), 10-21.

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9