Winning Smile: Accounting Homework - Trial Balance and Ledger

VerifiedAdded on 2022/09/05

|9

|1081

|13

Homework Assignment

AI Summary

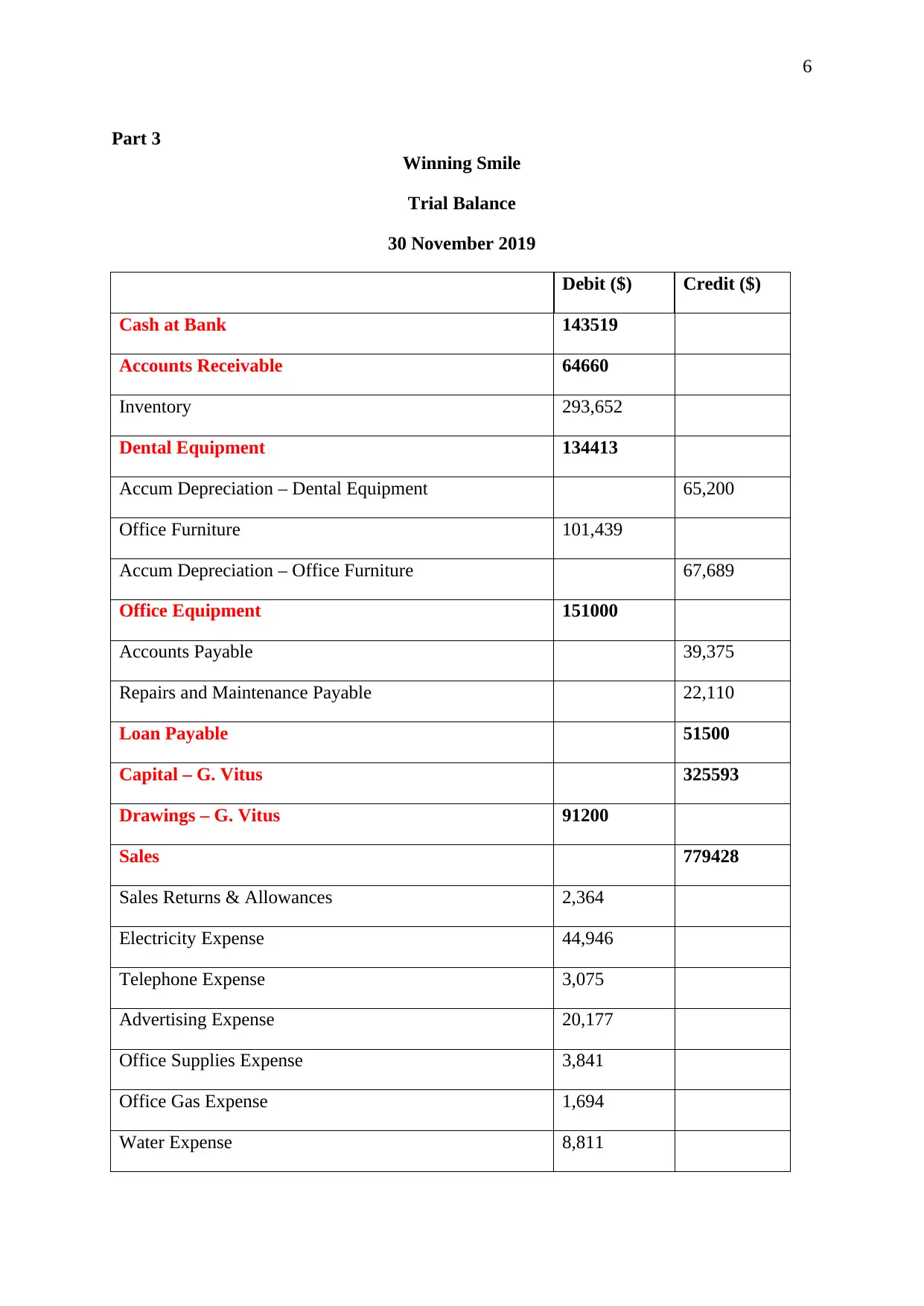

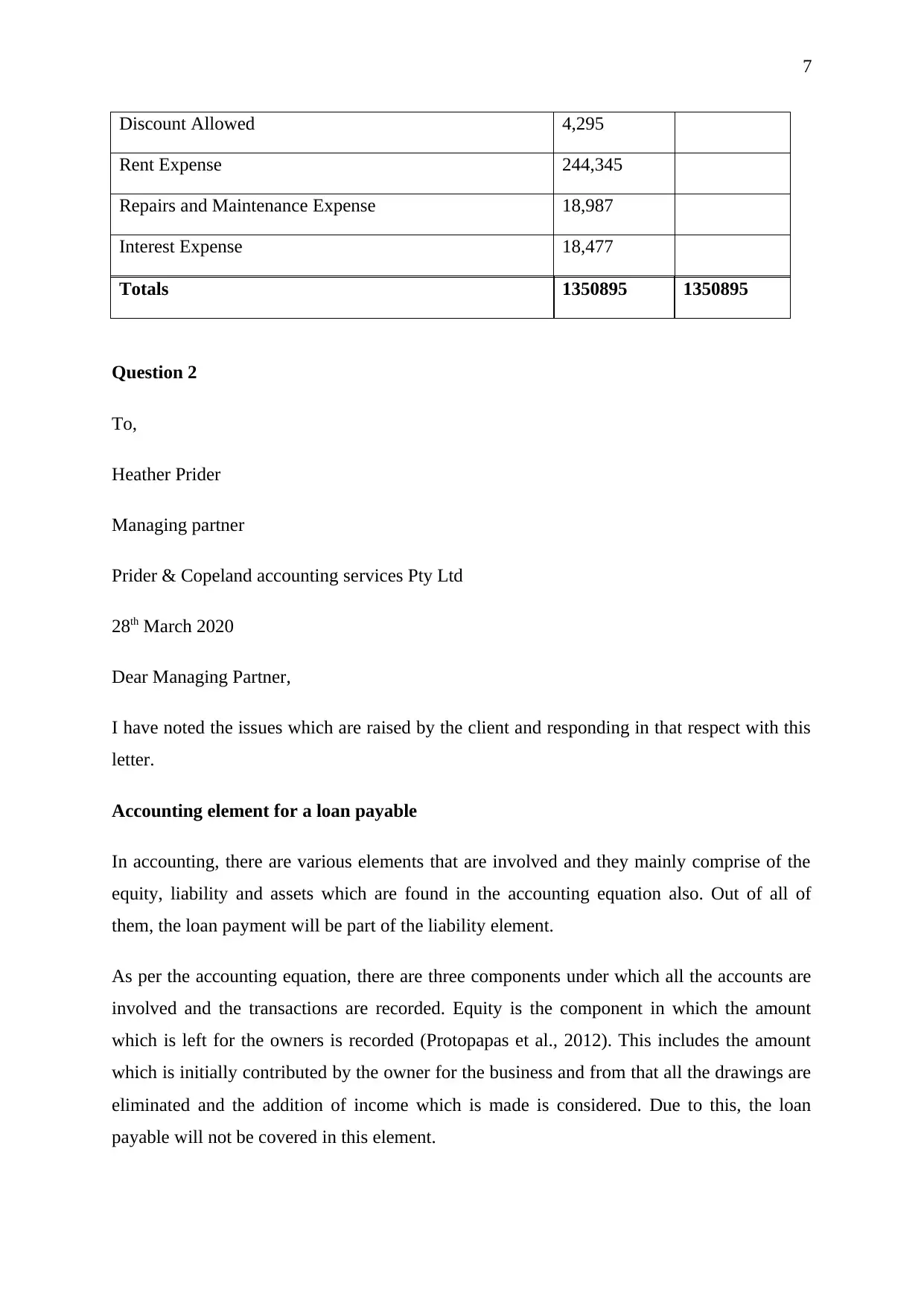

This document presents a comprehensive solution to an accounting homework assignment. The solution begins with journal entries detailing various transactions, followed by the creation of general ledgers for accounts like Cash at Bank, Accounts Receivable, and Loan Payable. The assignment then progresses to a trial balance, incorporating balances from the general ledger and addressing accounting elements and assumptions, particularly focusing on loan payables and the separate entity assumption. The solution also includes a discussion of accounting elements, the accounting equation, and relevant references, providing a complete overview of the accounting process and financial statement preparation. The document is a valuable resource for students seeking to understand and solve accounting problems related to trial balances and general ledgers.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.