AASB 138 Report: Australian Accounting Standard on Intangible Assets

VerifiedAdded on 2022/08/26

|12

|3018

|22

Report

AI Summary

This report provides a comprehensive analysis of AASB 138, the Australian accounting standard governing intangible assets. It defines intangible assets, outlines the standard's scope, and details the criteria for recognizing these assets. The report explores various valuation methods, including those for assets acquired through government grants, purchases, or internal generation, and discusses how amortization is determined. A key focus is the accounting discrepancy between internally generated and acquired intangible assets, highlighting differences in valuation that can lead to potential earnings management. The report examines the impact of these differences, illustrated with an example of goodwill calculation, and concludes by summarizing the accounting standard's implications and its effect on financial reporting. The report underscores the significance of intangible assets in today's business environment and the importance of understanding their accounting treatment.

Running head: AASB 138

AASB 138

Name of the Student:

Name of the University:

Author Note:

AASB 138

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AASB 138

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Meaning of AASB 138 / IAS 38:...........................................................................................2

Coverage of assets under this standard:.................................................................................3

Criteria for Recognition of the Intangible Assets:.................................................................3

Valuation of the intangible assets:.........................................................................................5

How to determine Amortization of the asset:........................................................................6

Accounting discrepancy in the valuation of internally generated asset and acquired asset:..6

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Introduction:...............................................................................................................................2

Discussion:.................................................................................................................................2

Meaning of AASB 138 / IAS 38:...........................................................................................2

Coverage of assets under this standard:.................................................................................3

Criteria for Recognition of the Intangible Assets:.................................................................3

Valuation of the intangible assets:.........................................................................................5

How to determine Amortization of the asset:........................................................................6

Accounting discrepancy in the valuation of internally generated asset and acquired asset:..6

Conclusion:................................................................................................................................8

References:.................................................................................................................................9

2AASB 138

Introduction:

In this report the Australian accounting standard 138 is discussed in regards to its

impact on the treatment of the internally generated intangibles and acquired intangibles. The

meaning of the standard AASB 138 is discussed in this report. Also the definition of the

intangibles which are accounted under this standard is discussed in this report. The

measurement of value of the intangibles which are acquired or generated is highlighted in this

report (Russell, 2017). The valuation of the intangibles after they have been recognized is

discussed in this report. Finally the differences which arise due to the different valuation

treatment of intangibles which are internally generated and which are acquired is highlighted

in this report. The issues which are created due to this accounting difference is discussed and

the impact of the difference is analysed. Thus at the end of this report a conclusion is based

on the accounting standard which summarises all the discussion which is presented with in

this report (Steenkamp & Steenkamp, 2016).

Discussion:

Meaning of AASB 138 / IAS 38:

The AASB 138 / IAS 38 is an accounting standard in the Australian Accounting

standard board which applies to the identification, measurement of the intangible assets

which are not covered in any other standards. Thus the accounting of the various intangible

assets is done as per the rules which are prescribed in this accounting standard. The intangible

assets need not be covered by any other accounting standards and then only the provision of

this standard are applicable to the intangible assets of the company (Su, & Wells, 2018).

Introduction:

In this report the Australian accounting standard 138 is discussed in regards to its

impact on the treatment of the internally generated intangibles and acquired intangibles. The

meaning of the standard AASB 138 is discussed in this report. Also the definition of the

intangibles which are accounted under this standard is discussed in this report. The

measurement of value of the intangibles which are acquired or generated is highlighted in this

report (Russell, 2017). The valuation of the intangibles after they have been recognized is

discussed in this report. Finally the differences which arise due to the different valuation

treatment of intangibles which are internally generated and which are acquired is highlighted

in this report. The issues which are created due to this accounting difference is discussed and

the impact of the difference is analysed. Thus at the end of this report a conclusion is based

on the accounting standard which summarises all the discussion which is presented with in

this report (Steenkamp & Steenkamp, 2016).

Discussion:

Meaning of AASB 138 / IAS 38:

The AASB 138 / IAS 38 is an accounting standard in the Australian Accounting

standard board which applies to the identification, measurement of the intangible assets

which are not covered in any other standards. Thus the accounting of the various intangible

assets is done as per the rules which are prescribed in this accounting standard. The intangible

assets need not be covered by any other accounting standards and then only the provision of

this standard are applicable to the intangible assets of the company (Su, & Wells, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AASB 138

Coverage of assets under this standard:

All the intangible assets of the company whether internally generated or acquired

through business combination is covered under this standard with the few exceptions

highlighted in the following points.

The assets which are generated during the exploration and mining of non-renewable

energy resources.

Assets which fall under the accounting standards AASB 132 / IAS 32 related to

financial accounts presentation.

Assets which are intangible but are covered under the provisions of another

accounting standards. Hence they are not covered under the accounting standard

AASB 138 / IAS 38 (Tran, & Zhu, 2017).

Criteria for Recognition of the Intangible Assets:

The criteria for the recognition of the assets to be intangible needs to fulfil the

following criteria to be identified as intangible assets.

The assets should be able to complete the meaning or definition of intangible assets

which involves the assets to be recognised, the company has a control over the assets

and economic benefits from the assets is possible in the future.

The assets can be recognised as intangible assets only if the future economic benefit

from the asset will flow or be earned by the company. Also the cost of the asset of the

company can be measured accurately (Sharma, & Dharni, 2019).

If the assets are internally generated by the firm they can be only recognized when the

entity classifies the generation of the asset either as research phase or as development phase.

Thus the assets which are classified in the research phase are excluded to be identified as

Coverage of assets under this standard:

All the intangible assets of the company whether internally generated or acquired

through business combination is covered under this standard with the few exceptions

highlighted in the following points.

The assets which are generated during the exploration and mining of non-renewable

energy resources.

Assets which fall under the accounting standards AASB 132 / IAS 32 related to

financial accounts presentation.

Assets which are intangible but are covered under the provisions of another

accounting standards. Hence they are not covered under the accounting standard

AASB 138 / IAS 38 (Tran, & Zhu, 2017).

Criteria for Recognition of the Intangible Assets:

The criteria for the recognition of the assets to be intangible needs to fulfil the

following criteria to be identified as intangible assets.

The assets should be able to complete the meaning or definition of intangible assets

which involves the assets to be recognised, the company has a control over the assets

and economic benefits from the assets is possible in the future.

The assets can be recognised as intangible assets only if the future economic benefit

from the asset will flow or be earned by the company. Also the cost of the asset of the

company can be measured accurately (Sharma, & Dharni, 2019).

If the assets are internally generated by the firm they can be only recognized when the

entity classifies the generation of the asset either as research phase or as development phase.

Thus the assets which are classified in the research phase are excluded to be identified as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AASB 138

intangible assets (Bodle, Brimble, Weaven, Frazer, & Blue, 2018). Also some other assets

which are not identified as intangible assets are,

The goodwill which is generated in the business is prohibited to be recognized as

intangible assets.

The titles which are used by the publishing company are excluded to be recognized as

intangible assets.

The database of customers of the company which are valuable to a business are

excluded and not recognized as intangible assets.

The brands and the brand value which is generated by the business in its normal

operations are not recognized as intangible assets.

All assets which cannot be separated from the business and no value can be attached

when separated from the business are not classified as intangible assets (Miah, Jiang,

Rahman, & Stent 2020).

The assets which are classified to be in the development phase shall be recognized as

intangible assets if they fulfil all of the following conditions,

The asset which is being developed can be used or be sold upon completion.

The purpose to complete the asset to be either used by the company or be sold to other

business.

The asset has the ability that it can be used or sold by the business.

The future expected benefits from the asset can be determined by the company and

also the procedure to generate the benefits can be determined.

The resources which would be required for the asset to be sold or to be used in the

business are available by the company.

intangible assets (Bodle, Brimble, Weaven, Frazer, & Blue, 2018). Also some other assets

which are not identified as intangible assets are,

The goodwill which is generated in the business is prohibited to be recognized as

intangible assets.

The titles which are used by the publishing company are excluded to be recognized as

intangible assets.

The database of customers of the company which are valuable to a business are

excluded and not recognized as intangible assets.

The brands and the brand value which is generated by the business in its normal

operations are not recognized as intangible assets.

All assets which cannot be separated from the business and no value can be attached

when separated from the business are not classified as intangible assets (Miah, Jiang,

Rahman, & Stent 2020).

The assets which are classified to be in the development phase shall be recognized as

intangible assets if they fulfil all of the following conditions,

The asset which is being developed can be used or be sold upon completion.

The purpose to complete the asset to be either used by the company or be sold to other

business.

The asset has the ability that it can be used or sold by the business.

The future expected benefits from the asset can be determined by the company and

also the procedure to generate the benefits can be determined.

The resources which would be required for the asset to be sold or to be used in the

business are available by the company.

5AASB 138

The cost which is incurred during the development of the asset can be determined and

the cost can be attributable to the asset (Miah, 2017).

Valuation of the intangible assets:

The method of valuation of the intangible assets depends on the way the asset is

acquired by a business. Thus the valuation of the asset is conducted using various methods

which are highlighted in the points below,

When an asset is acquired by a company in a way of government grant which can be

either be free of charge or for a small fee. The asset should be recognized and be

valued using the fair value of the asset on the day of acquisition.

When a company purchases the asset from another company who has developed the

asset or has acquired from some other company, the valuation of the asset is to be

done at cost. The cost of the asset includes all the cost such as the price paid for the

asset and all relevant expense which is incurred to purchase the asset. Also the cost

which is incurred to make the asset ready for use is also taken in the valuation of the

intangible assets (Fuad, & Gomes, 2017).

When an asset is recognized as intangible asset which has been generated by the

company its valuation is at the cost which has been incurred to develop the asset.

However, only the cost which have been incurred post the recognition of the asset as

intangible asset can be used to determine the value of internally generated intangible

asset (Mrša 2018).

When a company acquires an entire business and the all the assets and liabilities in

relation to the business, the intangible assets of the target company have to be

measured at fair value on the date of acquisition.

When an intangible asset is acquired by a company in a barter transaction for non-

monetary assets, the value is recorded at the fair value of the company. If the fair

The cost which is incurred during the development of the asset can be determined and

the cost can be attributable to the asset (Miah, 2017).

Valuation of the intangible assets:

The method of valuation of the intangible assets depends on the way the asset is

acquired by a business. Thus the valuation of the asset is conducted using various methods

which are highlighted in the points below,

When an asset is acquired by a company in a way of government grant which can be

either be free of charge or for a small fee. The asset should be recognized and be

valued using the fair value of the asset on the day of acquisition.

When a company purchases the asset from another company who has developed the

asset or has acquired from some other company, the valuation of the asset is to be

done at cost. The cost of the asset includes all the cost such as the price paid for the

asset and all relevant expense which is incurred to purchase the asset. Also the cost

which is incurred to make the asset ready for use is also taken in the valuation of the

intangible assets (Fuad, & Gomes, 2017).

When an asset is recognized as intangible asset which has been generated by the

company its valuation is at the cost which has been incurred to develop the asset.

However, only the cost which have been incurred post the recognition of the asset as

intangible asset can be used to determine the value of internally generated intangible

asset (Mrša 2018).

When a company acquires an entire business and the all the assets and liabilities in

relation to the business, the intangible assets of the target company have to be

measured at fair value on the date of acquisition.

When an intangible asset is acquired by a company in a barter transaction for non-

monetary assets, the value is recorded at the fair value of the company. If the fair

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AASB 138

value of the asset cannot be determined then the value of the assets which is given up

is taken as the value of the intangible assets (Sharma, & Kaur, 2019).

After the initial valuation of the intangible asset the company can value the asset at a future

date using either the cost model or the revaluation model. The cost model measures or values

the asset by deducting the amortization charges or any loss due to rise of impairment from the

cost of the asset. In the revaluation model the asset is revalued at its fair value on the date of

revaluation after deducting the amortization charges (Elsten, & Hill, 2017).

How to determine Amortization of the asset:

The assets are amortized over there useful life which has to be finite in nature or

infinite in nature. Also the amortization is conducted till the future benefits from the asset is

identifiable or till the asset is derecognized from being an intangible assets (Lim, Macias, &

Moeller, 2019).

Accounting discrepancy in the valuation of internally generated asset and acquired

asset:

The internally generated intangible assets which are generated by the business are

recorded in the financial statements of the company at the cost at which the asset is created in

the company. However, when an asset is acquired by a company which is intangible in nature

leads to the valuation at the fair value or the cost at which it is acquired. Thus the intangible

assets when acquired have a premium which is paid to the company from which the asset is

acquired. Thus, this leads to difference in the value of the intangibles of the same class and

the difference in the valuation leads to the possibility of earnings management (Visvanathan,

2017).

Since the assets do not have an active market from where the valuation of the

intangible assets can be determined and be considered as the fair value of the asset. This

value of the asset cannot be determined then the value of the assets which is given up

is taken as the value of the intangible assets (Sharma, & Kaur, 2019).

After the initial valuation of the intangible asset the company can value the asset at a future

date using either the cost model or the revaluation model. The cost model measures or values

the asset by deducting the amortization charges or any loss due to rise of impairment from the

cost of the asset. In the revaluation model the asset is revalued at its fair value on the date of

revaluation after deducting the amortization charges (Elsten, & Hill, 2017).

How to determine Amortization of the asset:

The assets are amortized over there useful life which has to be finite in nature or

infinite in nature. Also the amortization is conducted till the future benefits from the asset is

identifiable or till the asset is derecognized from being an intangible assets (Lim, Macias, &

Moeller, 2019).

Accounting discrepancy in the valuation of internally generated asset and acquired

asset:

The internally generated intangible assets which are generated by the business are

recorded in the financial statements of the company at the cost at which the asset is created in

the company. However, when an asset is acquired by a company which is intangible in nature

leads to the valuation at the fair value or the cost at which it is acquired. Thus the intangible

assets when acquired have a premium which is paid to the company from which the asset is

acquired. Thus, this leads to difference in the value of the intangibles of the same class and

the difference in the valuation leads to the possibility of earnings management (Visvanathan,

2017).

Since the assets do not have an active market from where the valuation of the

intangible assets can be determined and be considered as the fair value of the asset. This

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AASB 138

opens the possibility for the management to enable the earnings manipulation of the financial

statements. Since the internally generated assets which are to be valued at cost reduce the

total valuation of the company in the balance sheet. The company can sell those intangible

assets to other companies which will provide a payment of premium over and above the cost

of the asset. Thus the acquiring company of the asset will take the asset which is to be noted

at fair value which is the price paid for the asset (Lev, 2018).

As in the modern economy which is ruled by the sale and purchase of intangible

assets still off the balance sheet of companies even though they create a huge impact on the

financial possibility of many companies. The difference in the value of the intangible create a

huge impact as at one point of time the intangibles are valued at cost or maybe even 0. Thus

the value of the intangibles can change overnight to billions of dollars once they are sold to

other companies, creating a huge impact on the value of the company. Thus this issue can be

considered as one of the difference of the accounting treatment of internally generated

intangibles and acquired intangibles (King, Linsmeier, & Wangerin, 2019).

Also one of the difference of the accounting treatment of the intangibles create a

scenario for the management of earnings. Thus the company can capitalize the cost which is

undertaken to develop the asset rather than expensing the cost. Thus this increases the profit

for the company and manipulation of the financial statements is possible (Bryan, Rafferty, &

Wigan, 2017).

In the past few years, the impact of intangibles has been observed in the company

valuation which is highlighted by the $4.5 billion sale of Nortel’s Wireless patents and also

the $12.5 billion bid of Google for Motorola Holdings, which consists of 24500 patents and

remaining patent application. Thus this highlights the value of intangibles in the business

environment which is present today (Bianchi, 2017).

opens the possibility for the management to enable the earnings manipulation of the financial

statements. Since the internally generated assets which are to be valued at cost reduce the

total valuation of the company in the balance sheet. The company can sell those intangible

assets to other companies which will provide a payment of premium over and above the cost

of the asset. Thus the acquiring company of the asset will take the asset which is to be noted

at fair value which is the price paid for the asset (Lev, 2018).

As in the modern economy which is ruled by the sale and purchase of intangible

assets still off the balance sheet of companies even though they create a huge impact on the

financial possibility of many companies. The difference in the value of the intangible create a

huge impact as at one point of time the intangibles are valued at cost or maybe even 0. Thus

the value of the intangibles can change overnight to billions of dollars once they are sold to

other companies, creating a huge impact on the value of the company. Thus this issue can be

considered as one of the difference of the accounting treatment of internally generated

intangibles and acquired intangibles (King, Linsmeier, & Wangerin, 2019).

Also one of the difference of the accounting treatment of the intangibles create a

scenario for the management of earnings. Thus the company can capitalize the cost which is

undertaken to develop the asset rather than expensing the cost. Thus this increases the profit

for the company and manipulation of the financial statements is possible (Bryan, Rafferty, &

Wigan, 2017).

In the past few years, the impact of intangibles has been observed in the company

valuation which is highlighted by the $4.5 billion sale of Nortel’s Wireless patents and also

the $12.5 billion bid of Google for Motorola Holdings, which consists of 24500 patents and

remaining patent application. Thus this highlights the value of intangibles in the business

environment which is present today (Bianchi, 2017).

8AASB 138

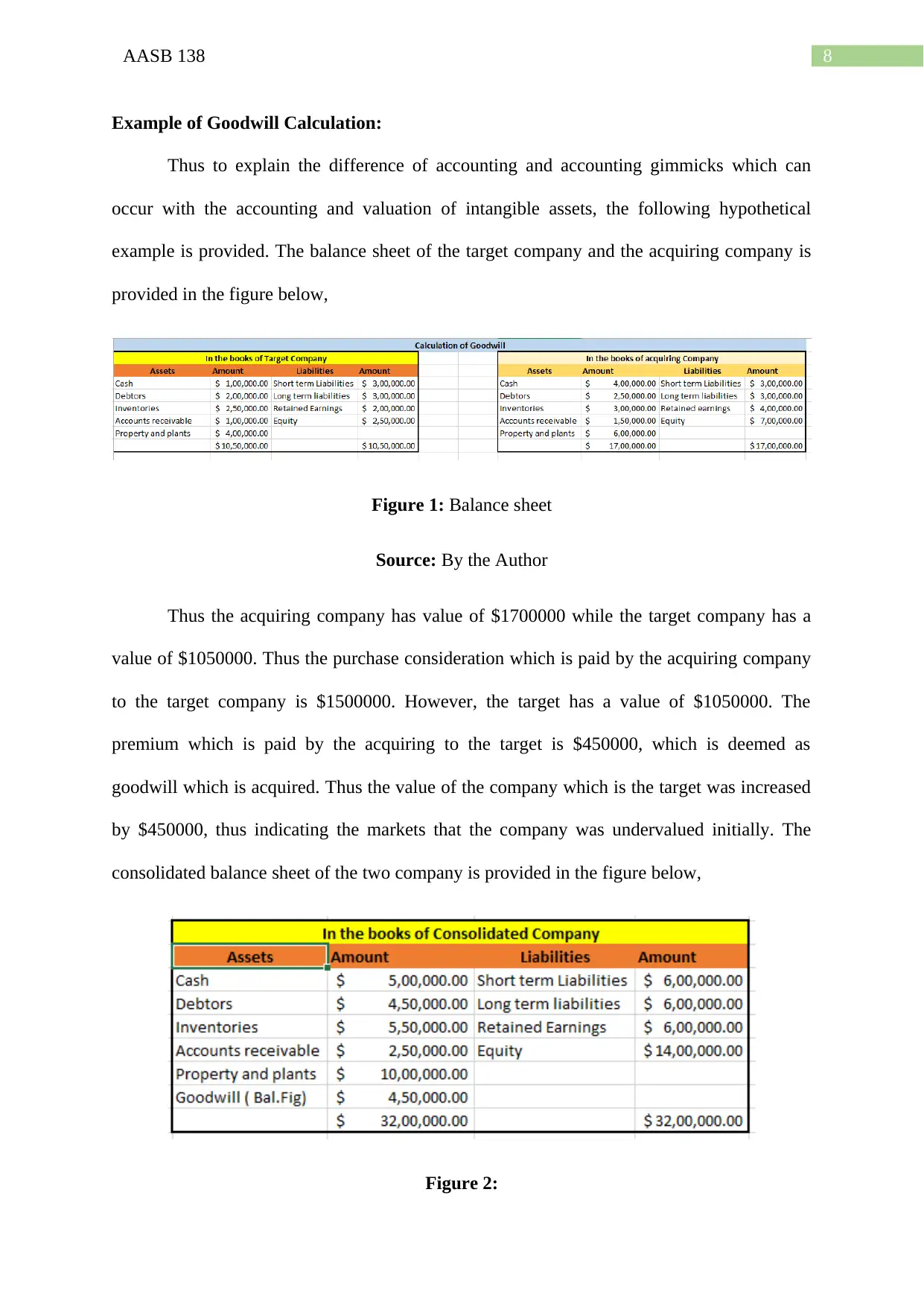

Example of Goodwill Calculation:

Thus to explain the difference of accounting and accounting gimmicks which can

occur with the accounting and valuation of intangible assets, the following hypothetical

example is provided. The balance sheet of the target company and the acquiring company is

provided in the figure below,

Figure 1: Balance sheet

Source: By the Author

Thus the acquiring company has value of $1700000 while the target company has a

value of $1050000. Thus the purchase consideration which is paid by the acquiring company

to the target company is $1500000. However, the target has a value of $1050000. The

premium which is paid by the acquiring to the target is $450000, which is deemed as

goodwill which is acquired. Thus the value of the company which is the target was increased

by $450000, thus indicating the markets that the company was undervalued initially. The

consolidated balance sheet of the two company is provided in the figure below,

Figure 2:

Example of Goodwill Calculation:

Thus to explain the difference of accounting and accounting gimmicks which can

occur with the accounting and valuation of intangible assets, the following hypothetical

example is provided. The balance sheet of the target company and the acquiring company is

provided in the figure below,

Figure 1: Balance sheet

Source: By the Author

Thus the acquiring company has value of $1700000 while the target company has a

value of $1050000. Thus the purchase consideration which is paid by the acquiring company

to the target company is $1500000. However, the target has a value of $1050000. The

premium which is paid by the acquiring to the target is $450000, which is deemed as

goodwill which is acquired. Thus the value of the company which is the target was increased

by $450000, thus indicating the markets that the company was undervalued initially. The

consolidated balance sheet of the two company is provided in the figure below,

Figure 2:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AASB 138

Source:

Thus as per the consolidated balance sheet it is visible that the goodwill which was a

premium is now shown in the balance sheet. Thus in a single merger deal the value of both

the company was raised by $450000, highlighting the impact of intangible assets on the

valuation of the company.

Conclusion:

Thus in this report which is related to the accounting treatment of the intangible assets

as per the AASB standards 138 / IAS 38. The meaning of the standard and its coverage is

analysed in this report along with the various conditions which has to be satisfied for an asset

to be considered as an intangible asset. The different accounting methods of the internally

generated assets and the assets acquired by the business is analysed. The difference leads to

creation of various accounting discrepancy which hurts the accurate valuation of companies

which are primarily comprised of intangibles. The intangibles which are valued at a lower

cost or 0 can turn out to be highly valuable in a matter of time when sold. Thus this leads to

rise in the value of the company and can make the stock price which is being currently traded

in the market to be under-priced. Also the different accounting policy in terms of intangibles

leaves a loop hole for manipulation of the financial statements such as increasing the earnings

by capitalizing expenses. Thus the presence of different accounting methods for intangibles

creates a difference in accounting for the companies.

Source:

Thus as per the consolidated balance sheet it is visible that the goodwill which was a

premium is now shown in the balance sheet. Thus in a single merger deal the value of both

the company was raised by $450000, highlighting the impact of intangible assets on the

valuation of the company.

Conclusion:

Thus in this report which is related to the accounting treatment of the intangible assets

as per the AASB standards 138 / IAS 38. The meaning of the standard and its coverage is

analysed in this report along with the various conditions which has to be satisfied for an asset

to be considered as an intangible asset. The different accounting methods of the internally

generated assets and the assets acquired by the business is analysed. The difference leads to

creation of various accounting discrepancy which hurts the accurate valuation of companies

which are primarily comprised of intangibles. The intangibles which are valued at a lower

cost or 0 can turn out to be highly valuable in a matter of time when sold. Thus this leads to

rise in the value of the company and can make the stock price which is being currently traded

in the market to be under-priced. Also the different accounting policy in terms of intangibles

leaves a loop hole for manipulation of the financial statements such as increasing the earnings

by capitalizing expenses. Thus the presence of different accounting methods for intangibles

creates a difference in accounting for the companies.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10AASB 138

References:

Bianchi, P., 2017. The economic importance of intangible assets. Routledge.

Bodle, K., Brimble, M., Weaven, S., Frazer, L. and Blue, L., 2018. Critical success factors in

managing sustainable Indigenous businesses in Australia. Pacific Accounting Review, 30(1),

pp.35-51.

Bryan, D., Rafferty, M. and Wigan, D., 2017. Capital unchained: finance, intangible assets

and the double life of capital in the offshore world. Review of International Political

Economy, 24(1), pp.56-86.

Elsten, C. and Hill, N., 2017. Intangible Asset Market Value Study?.

Fuad, S. and Gomes, J., 2017. Investigating the Impact of Valuing Intangible Assets on

Valuation Multiples.

King, Z., Linsmeier, T. and Wangerin, D., 2019. Differences in the Value Relevance of

Identifiable Intangible Assets Acquired in Business Combinations. Available at SSRN

3438250.

Lev, B., 2018. Intangibles.

Lim, S.C., Macias, A.J. and Moeller, T., 2019. Intangible assets and capital

structure. Available at SSRN 2514551.

Miah, M.S., 2017. Accounting standards complexity, audit fees and financial analyst

forecasts in Australia: a thesis submitted in fulfilment of the requirements for the degree of

Doctor of Philosophy in Accounting at Massey University, Albany, New Zealand (Doctoral

dissertation, Massey University).

References:

Bianchi, P., 2017. The economic importance of intangible assets. Routledge.

Bodle, K., Brimble, M., Weaven, S., Frazer, L. and Blue, L., 2018. Critical success factors in

managing sustainable Indigenous businesses in Australia. Pacific Accounting Review, 30(1),

pp.35-51.

Bryan, D., Rafferty, M. and Wigan, D., 2017. Capital unchained: finance, intangible assets

and the double life of capital in the offshore world. Review of International Political

Economy, 24(1), pp.56-86.

Elsten, C. and Hill, N., 2017. Intangible Asset Market Value Study?.

Fuad, S. and Gomes, J., 2017. Investigating the Impact of Valuing Intangible Assets on

Valuation Multiples.

King, Z., Linsmeier, T. and Wangerin, D., 2019. Differences in the Value Relevance of

Identifiable Intangible Assets Acquired in Business Combinations. Available at SSRN

3438250.

Lev, B., 2018. Intangibles.

Lim, S.C., Macias, A.J. and Moeller, T., 2019. Intangible assets and capital

structure. Available at SSRN 2514551.

Miah, M.S., 2017. Accounting standards complexity, audit fees and financial analyst

forecasts in Australia: a thesis submitted in fulfilment of the requirements for the degree of

Doctor of Philosophy in Accounting at Massey University, Albany, New Zealand (Doctoral

dissertation, Massey University).

11AASB 138

Miah, M.S., Jiang, H., Rahman, A. and Stent, W., 2020. Audit effort, materiality and audit

fees: evidence from the adoption of IFRS in Australia. Accounting Research Journal.

Mrša, J., 2018. Valuation of Internally Generated Intangible Assets in Accounting. Acta

Economica Et Turistica, 4(2), pp.181-195.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance, 57, pp.211-234.

Sharma, K. and Kaur, M., 2019. Intangible assets: reporting practices and hidden value

measurement. research journal of social sciences, 10(1).

Sharma, S. and Dharni, K., 2019. RELEVANCE OF INTANGIBLE ASSETS: AN OPINION

OF INDIAN PRACTITIONERS. Journal of Commerce & Accounting Research, 8(1).

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions

reducing R&D spending?. Journal of Financial Reporting and Accounting, 14(1), pp.116-

130.

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting Research

Journal, 31(2), pp.135-156.

Tran, A. and Zhu, Y.H., 2017. The impact of adopting IFRS on corporate ETR and book-tax

income gap. Austl. Tax F., 32, p.757.

Visvanathan, G., 2017. Intangible assets on the balance sheet and audit fees. International

Journal of Disclosure and Governance, 14(3), pp.241-250.

Miah, M.S., Jiang, H., Rahman, A. and Stent, W., 2020. Audit effort, materiality and audit

fees: evidence from the adoption of IFRS in Australia. Accounting Research Journal.

Mrša, J., 2018. Valuation of Internally Generated Intangible Assets in Accounting. Acta

Economica Et Turistica, 4(2), pp.181-195.

Russell, M., 2017. Management incentives to recognise intangible assets. Accounting &

Finance, 57, pp.211-234.

Sharma, K. and Kaur, M., 2019. Intangible assets: reporting practices and hidden value

measurement. research journal of social sciences, 10(1).

Sharma, S. and Dharni, K., 2019. RELEVANCE OF INTANGIBLE ASSETS: AN OPINION

OF INDIAN PRACTITIONERS. Journal of Commerce & Accounting Research, 8(1).

Steenkamp, N. and Steenkamp, S., 2016. AASB 138: catalyst for managerial decisions

reducing R&D spending?. Journal of Financial Reporting and Accounting, 14(1), pp.116-

130.

Su, W.H. and Wells, P., 2018. Acquisition premiums and the recognition of identifiable

intangible assets in business combinations pre-and post-IFRS adoption. Accounting Research

Journal, 31(2), pp.135-156.

Tran, A. and Zhu, Y.H., 2017. The impact of adopting IFRS on corporate ETR and book-tax

income gap. Austl. Tax F., 32, p.757.

Visvanathan, G., 2017. Intangible assets on the balance sheet and audit fees. International

Journal of Disclosure and Governance, 14(3), pp.241-250.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.