ACCY801 Report: In-depth Financial Analysis of BAP and KMD Companies

VerifiedAdded on 2022/09/15

|15

|3833

|15

Report

AI Summary

This report provides a comprehensive financial analysis of Bapcor (BAP) and Kathmandu Holdings Limited (KMD), comparing their performance based on 2019 annual reports. The analysis includes calculations and comparisons of various financial ratios, such as current and quick ratios for liquidity, debt ratio and interest coverage for capital structure, and receivable, inventory, and asset turnover ratios for asset management efficiency. The report also evaluates operating and net profit margins, return on assets, and return on equity to assess profitability and shareholder returns. The findings indicate that BAP generally maintains a better liquidity position, while KMD shows stronger performance in capital structure and profitability. The report highlights areas for improvement, such as asset management efficiency and cost control, and offers recommendations to enhance financial performance, particularly for BAP. Overall, the analysis provides insights into the companies' strengths, weaknesses, and strategic positioning within their respective markets.

1

Accounting & Financial Management

Accounting & Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

The report has been prepared in the context of BAP and KMD and in that it is identified that

KMD is a competitor of BAP and on that basis, the evaluation is made. There is the

calculation of ratios that are made and with that various areas have been analyzed. There is

the consideration of capital structure, liquidity and asset efficiency management. The need for

improvement in identified in all of the areas. The position of BAP is weak then that of KMD

and for that debt position will be considered. The assets will be required to be used by the

management in a more effective manner so that the revenue can be made more profitable.

There is the profitability consideration and in that the expenses are higher in BAP which

makes the profitability lower. The interest expense will be reduced and for that debt will be

avoided. The shareholders are provided with the adequate returns and they will be satisfied

with the returns. There is the consideration of the capital expenditures and all of them will be

beneficial in long terms for the companies.

Executive summary

The report has been prepared in the context of BAP and KMD and in that it is identified that

KMD is a competitor of BAP and on that basis, the evaluation is made. There is the

calculation of ratios that are made and with that various areas have been analyzed. There is

the consideration of capital structure, liquidity and asset efficiency management. The need for

improvement in identified in all of the areas. The position of BAP is weak then that of KMD

and for that debt position will be considered. The assets will be required to be used by the

management in a more effective manner so that the revenue can be made more profitable.

There is the profitability consideration and in that the expenses are higher in BAP which

makes the profitability lower. The interest expense will be reduced and for that debt will be

avoided. The shareholders are provided with the adequate returns and they will be satisfied

with the returns. There is the consideration of the capital expenditures and all of them will be

beneficial in long terms for the companies.

3

Table of Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Objectives and long term plans..................................................................................................4

Financial ratios...........................................................................................................................5

Liquidity, Capital structure and asset management efficiency..................................................6

Operating profitability................................................................................................................8

Returns on shareholders’ investment.........................................................................................9

Capital expenditures.................................................................................................................10

Conclusion and recommendations...........................................................................................11

References................................................................................................................................13

Appendix..................................................................................................................................15

Table of Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Objectives and long term plans..................................................................................................4

Financial ratios...........................................................................................................................5

Liquidity, Capital structure and asset management efficiency..................................................6

Operating profitability................................................................................................................8

Returns on shareholders’ investment.........................................................................................9

Capital expenditures.................................................................................................................10

Conclusion and recommendations...........................................................................................11

References................................................................................................................................13

Appendix..................................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

In the business, there are various areas that are involved and in that the evaluation is required

to be made so that the current position and performance of the company can be evaluated.

This is required to be with the help of suitable methods and approaches which are available.

The ratio analysis is one of the best techniques and the sane will be used in the given case.

There will be an evaluation of the two companies under this and they include Kathmandu

holdings limited and Bapcor. There will be consideration of the annual report of both the

companies and from that the relevant information will be used. The calculation will be made

and that will be used to make the comparison among both the companies. This will help in

identifying the areas in which improvement is required and then the decision by the

management will be undertaken to make the complete situation better. The overall results will

be enhanced and there will be the attainment of goals. The discussion in this respect will be

carried in the report for better understanding.

Objectives and long term plans

The companies in the market operate with the aim to make the profits and attain the best

position among all the competitors. By this, long-term sustainability is ensured and that is the

main aim of any business. The Kathmandu holdings have been considered and the main aim

of the business has been determined which is to inspire and incorporate the adventure in all

the people. The objective of the company is to perform the operations in such a manner that

diversity can be attained among all the generations and genders (KMD, 2019). The strategic

objective which is involved with the company is to increase the value for all the shareholders.

In the company, there is a five-year plan which is formulated in respect of sustainability. The

main long-term plan of the business is in relation to the creation of the sustainability plan.

Introduction

In the business, there are various areas that are involved and in that the evaluation is required

to be made so that the current position and performance of the company can be evaluated.

This is required to be with the help of suitable methods and approaches which are available.

The ratio analysis is one of the best techniques and the sane will be used in the given case.

There will be an evaluation of the two companies under this and they include Kathmandu

holdings limited and Bapcor. There will be consideration of the annual report of both the

companies and from that the relevant information will be used. The calculation will be made

and that will be used to make the comparison among both the companies. This will help in

identifying the areas in which improvement is required and then the decision by the

management will be undertaken to make the complete situation better. The overall results will

be enhanced and there will be the attainment of goals. The discussion in this respect will be

carried in the report for better understanding.

Objectives and long term plans

The companies in the market operate with the aim to make the profits and attain the best

position among all the competitors. By this, long-term sustainability is ensured and that is the

main aim of any business. The Kathmandu holdings have been considered and the main aim

of the business has been determined which is to inspire and incorporate the adventure in all

the people. The objective of the company is to perform the operations in such a manner that

diversity can be attained among all the generations and genders (KMD, 2019). The strategic

objective which is involved with the company is to increase the value for all the shareholders.

In the company, there is a five-year plan which is formulated in respect of sustainability. The

main long-term plan of the business is in relation to the creation of the sustainability plan.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

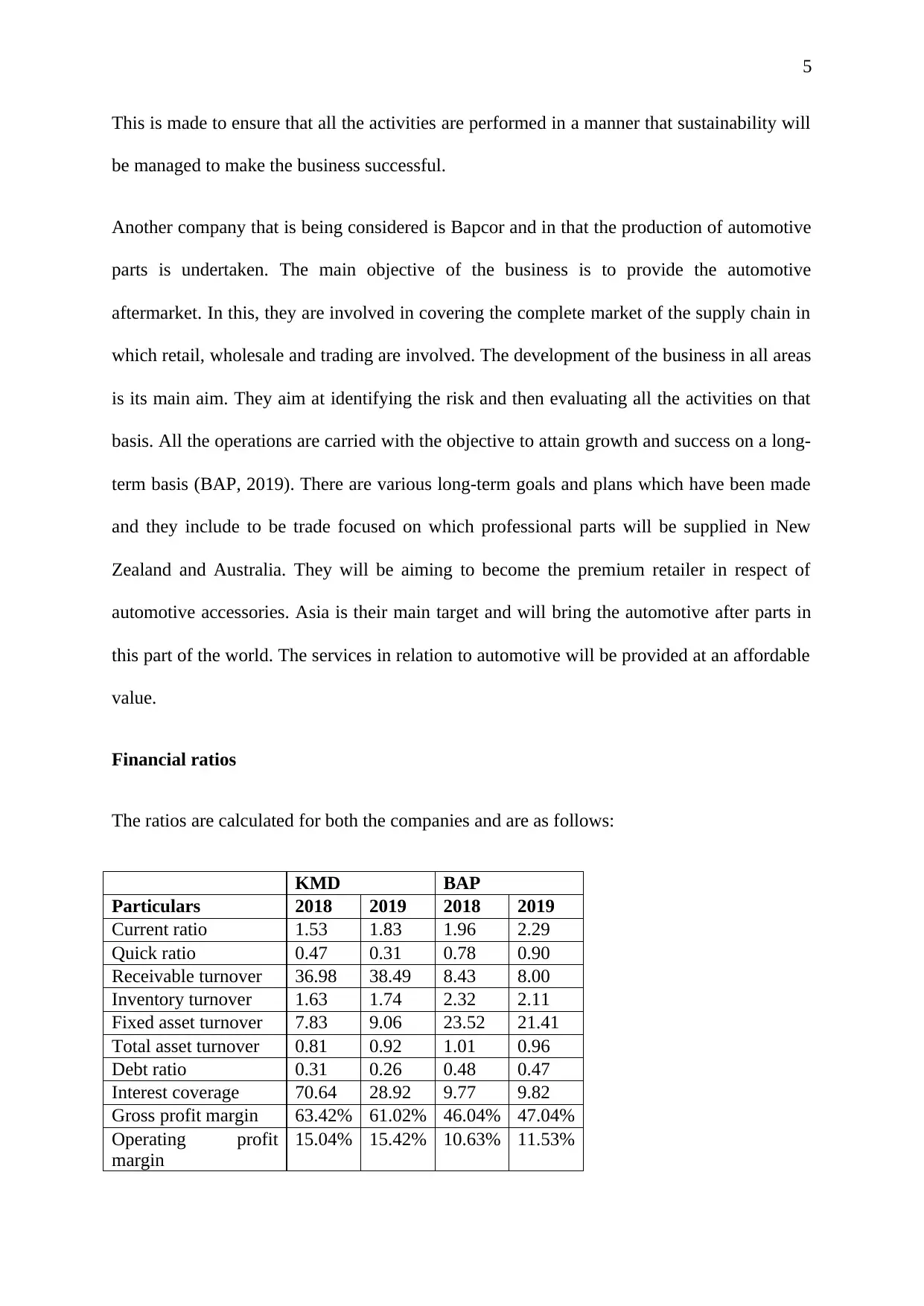

This is made to ensure that all the activities are performed in a manner that sustainability will

be managed to make the business successful.

Another company that is being considered is Bapcor and in that the production of automotive

parts is undertaken. The main objective of the business is to provide the automotive

aftermarket. In this, they are involved in covering the complete market of the supply chain in

which retail, wholesale and trading are involved. The development of the business in all areas

is its main aim. They aim at identifying the risk and then evaluating all the activities on that

basis. All the operations are carried with the objective to attain growth and success on a long-

term basis (BAP, 2019). There are various long-term goals and plans which have been made

and they include to be trade focused on which professional parts will be supplied in New

Zealand and Australia. They will be aiming to become the premium retailer in respect of

automotive accessories. Asia is their main target and will bring the automotive after parts in

this part of the world. The services in relation to automotive will be provided at an affordable

value.

Financial ratios

The ratios are calculated for both the companies and are as follows:

KMD BAP

Particulars 2018 2019 2018 2019

Current ratio 1.53 1.83 1.96 2.29

Quick ratio 0.47 0.31 0.78 0.90

Receivable turnover 36.98 38.49 8.43 8.00

Inventory turnover 1.63 1.74 2.32 2.11

Fixed asset turnover 7.83 9.06 23.52 21.41

Total asset turnover 0.81 0.92 1.01 0.96

Debt ratio 0.31 0.26 0.48 0.47

Interest coverage 70.64 28.92 9.77 9.82

Gross profit margin 63.42% 61.02% 46.04% 47.04%

Operating profit

margin

15.04% 15.42% 10.63% 11.53%

This is made to ensure that all the activities are performed in a manner that sustainability will

be managed to make the business successful.

Another company that is being considered is Bapcor and in that the production of automotive

parts is undertaken. The main objective of the business is to provide the automotive

aftermarket. In this, they are involved in covering the complete market of the supply chain in

which retail, wholesale and trading are involved. The development of the business in all areas

is its main aim. They aim at identifying the risk and then evaluating all the activities on that

basis. All the operations are carried with the objective to attain growth and success on a long-

term basis (BAP, 2019). There are various long-term goals and plans which have been made

and they include to be trade focused on which professional parts will be supplied in New

Zealand and Australia. They will be aiming to become the premium retailer in respect of

automotive accessories. Asia is their main target and will bring the automotive after parts in

this part of the world. The services in relation to automotive will be provided at an affordable

value.

Financial ratios

The ratios are calculated for both the companies and are as follows:

KMD BAP

Particulars 2018 2019 2018 2019

Current ratio 1.53 1.83 1.96 2.29

Quick ratio 0.47 0.31 0.78 0.90

Receivable turnover 36.98 38.49 8.43 8.00

Inventory turnover 1.63 1.74 2.32 2.11

Fixed asset turnover 7.83 9.06 23.52 21.41

Total asset turnover 0.81 0.92 1.01 0.96

Debt ratio 0.31 0.26 0.48 0.47

Interest coverage 70.64 28.92 9.77 9.82

Gross profit margin 63.42% 61.02% 46.04% 47.04%

Operating profit

margin

15.04% 15.42% 10.63% 11.53%

6

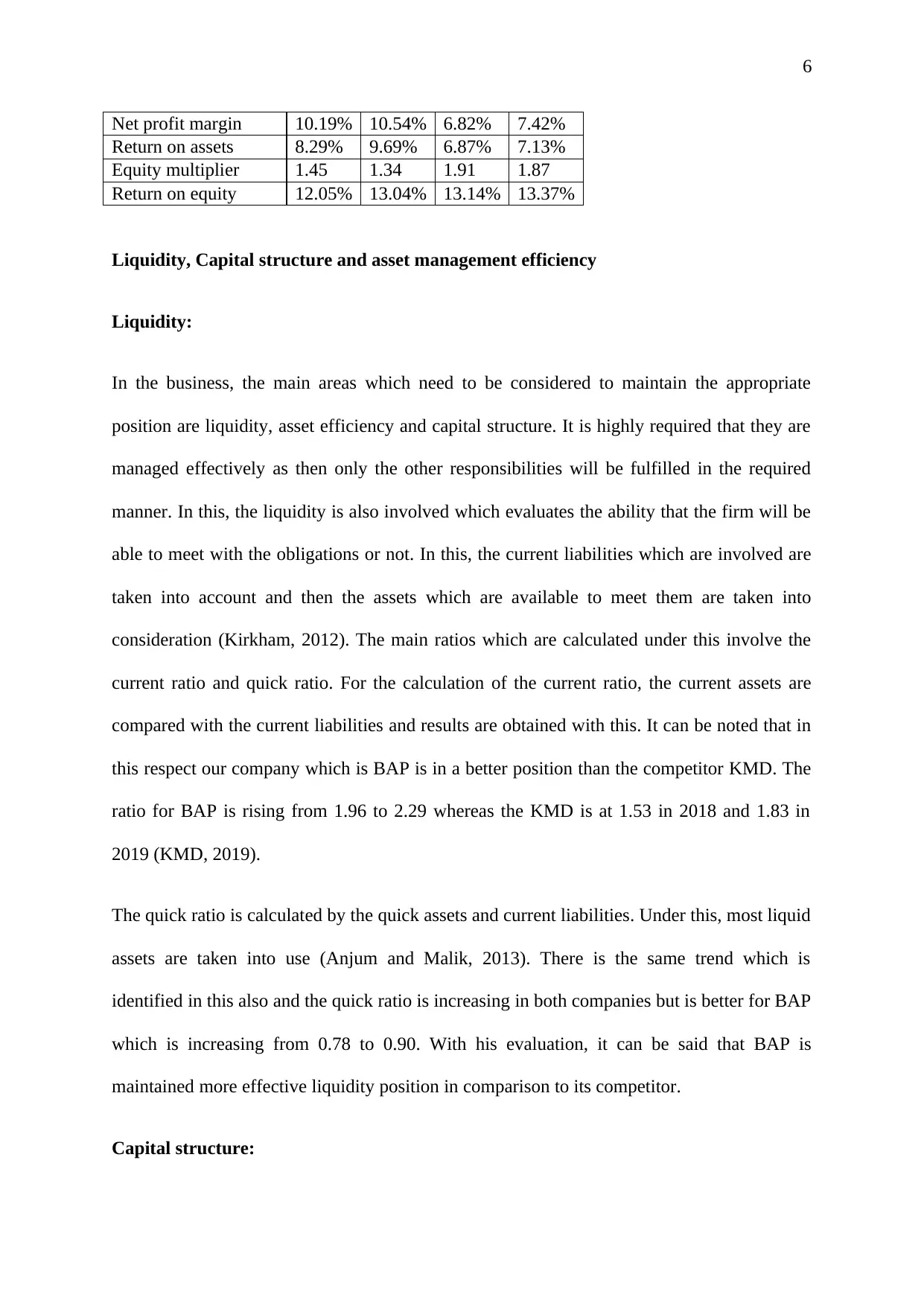

Net profit margin 10.19% 10.54% 6.82% 7.42%

Return on assets 8.29% 9.69% 6.87% 7.13%

Equity multiplier 1.45 1.34 1.91 1.87

Return on equity 12.05% 13.04% 13.14% 13.37%

Liquidity, Capital structure and asset management efficiency

Liquidity:

In the business, the main areas which need to be considered to maintain the appropriate

position are liquidity, asset efficiency and capital structure. It is highly required that they are

managed effectively as then only the other responsibilities will be fulfilled in the required

manner. In this, the liquidity is also involved which evaluates the ability that the firm will be

able to meet with the obligations or not. In this, the current liabilities which are involved are

taken into account and then the assets which are available to meet them are taken into

consideration (Kirkham, 2012). The main ratios which are calculated under this involve the

current ratio and quick ratio. For the calculation of the current ratio, the current assets are

compared with the current liabilities and results are obtained with this. It can be noted that in

this respect our company which is BAP is in a better position than the competitor KMD. The

ratio for BAP is rising from 1.96 to 2.29 whereas the KMD is at 1.53 in 2018 and 1.83 in

2019 (KMD, 2019).

The quick ratio is calculated by the quick assets and current liabilities. Under this, most liquid

assets are taken into use (Anjum and Malik, 2013). There is the same trend which is

identified in this also and the quick ratio is increasing in both companies but is better for BAP

which is increasing from 0.78 to 0.90. With his evaluation, it can be said that BAP is

maintained more effective liquidity position in comparison to its competitor.

Capital structure:

Net profit margin 10.19% 10.54% 6.82% 7.42%

Return on assets 8.29% 9.69% 6.87% 7.13%

Equity multiplier 1.45 1.34 1.91 1.87

Return on equity 12.05% 13.04% 13.14% 13.37%

Liquidity, Capital structure and asset management efficiency

Liquidity:

In the business, the main areas which need to be considered to maintain the appropriate

position are liquidity, asset efficiency and capital structure. It is highly required that they are

managed effectively as then only the other responsibilities will be fulfilled in the required

manner. In this, the liquidity is also involved which evaluates the ability that the firm will be

able to meet with the obligations or not. In this, the current liabilities which are involved are

taken into account and then the assets which are available to meet them are taken into

consideration (Kirkham, 2012). The main ratios which are calculated under this involve the

current ratio and quick ratio. For the calculation of the current ratio, the current assets are

compared with the current liabilities and results are obtained with this. It can be noted that in

this respect our company which is BAP is in a better position than the competitor KMD. The

ratio for BAP is rising from 1.96 to 2.29 whereas the KMD is at 1.53 in 2018 and 1.83 in

2019 (KMD, 2019).

The quick ratio is calculated by the quick assets and current liabilities. Under this, most liquid

assets are taken into use (Anjum and Malik, 2013). There is the same trend which is

identified in this also and the quick ratio is increasing in both companies but is better for BAP

which is increasing from 0.78 to 0.90. With his evaluation, it can be said that BAP is

maintained more effective liquidity position in comparison to its competitor.

Capital structure:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

The capital structure of the company shall be maintained adequately and in that debt and

equity are maintained. There is a need to manage the balance among them so that the best

outcomes can be achieved. In this, the ratios are calculated and they will be defining the

position of the companies. The debt ratio is calculated and in that total liabilities and assets

which are involved (Deran, Iskenderoglu and Erduru, 2014). It can be seen that there is a

decline in the ratio with a little position from 0.48 to 0.47 which is higher than the competitor

that has a ratio of 0.31 in 2018 and 0.26 in 2019. The interest coverage ratio is also calculated

is higher for the KMD than BAP which shows that in the company there is lower interest

coverage than the competitor because of the higher debt amount which is involved

(Serghiescu and Vaidean, 2014). The KMD coverage ratio is declining from 2018 due to the

increase in the amount of interest expense that is involved. The overall position is not better

than the competitor but there is some increment which is made and that shows some level of

improvement due to the increase in earnings. It can be said that the capital structure position

is improving little but it is not satisfactory and need to improve to beat the competition in the

market.

Asset management efficiency:

There are various assets that are involved with the company and they are required to be

managed in an effective manner. It is the duty of the management to manage them in an

effective manner so that the best results can be attained. For this, the asset management

efficiency ratios will be calculated by which the evaluation will be made (Babalola and

Abiola, 2013). The receivable turnover, inventory turnover, total asset and fixed asset

turnover are determined. All of them have declined from 2018 to 2019 and that shows the

inefficiency of the management in maintaining the assets which are available. The ratio of the

competitor is less than that of the BAP which shows that competitor is also not having

The capital structure of the company shall be maintained adequately and in that debt and

equity are maintained. There is a need to manage the balance among them so that the best

outcomes can be achieved. In this, the ratios are calculated and they will be defining the

position of the companies. The debt ratio is calculated and in that total liabilities and assets

which are involved (Deran, Iskenderoglu and Erduru, 2014). It can be seen that there is a

decline in the ratio with a little position from 0.48 to 0.47 which is higher than the competitor

that has a ratio of 0.31 in 2018 and 0.26 in 2019. The interest coverage ratio is also calculated

is higher for the KMD than BAP which shows that in the company there is lower interest

coverage than the competitor because of the higher debt amount which is involved

(Serghiescu and Vaidean, 2014). The KMD coverage ratio is declining from 2018 due to the

increase in the amount of interest expense that is involved. The overall position is not better

than the competitor but there is some increment which is made and that shows some level of

improvement due to the increase in earnings. It can be said that the capital structure position

is improving little but it is not satisfactory and need to improve to beat the competition in the

market.

Asset management efficiency:

There are various assets that are involved with the company and they are required to be

managed in an effective manner. It is the duty of the management to manage them in an

effective manner so that the best results can be attained. For this, the asset management

efficiency ratios will be calculated by which the evaluation will be made (Babalola and

Abiola, 2013). The receivable turnover, inventory turnover, total asset and fixed asset

turnover are determined. All of them have declined from 2018 to 2019 and that shows the

inefficiency of the management in maintaining the assets which are available. The ratio of the

competitor is less than that of the BAP which shows that competitor is also not having

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

efficient management. Although the position of BAP is better in overall terms there is a

declining trend that is identified and that is an adverse situation for the company. The assets

are increasing but the revenue is not growing in the same percentage. Due to this, it can be

said that the management needs to make improvements and take steps by which efficiency

can be increased.

Operating profitability

The main aim which is set in every business is to make the profit in adequate terms. There is

the need for the maintenance of proper profits as by that there will be the establishment of the

sustainability of the business (Kabajeh, Al Nuaimat and Dahmash, 2012). In that, there are

various aspects which are required to be considered and by that the profits which are made

will be taken into account. There is the revenue that is made and in that process, the expenses

which are incurred in that respect will be considered (Mousa, 2015). With the help of that, the

profits will be ascertained and there will be adequate ascertainment of the profitability

position of the business. In the given case the profitability of the BAP has been considered

and with that, the calculation is also made for KMD which is its competitor.

The calculation of the gross profit has been made and in that, it can be noted that there is an

increase in the gross profit margin from 46.04% to 47.04% which is good but after this rise

also the profits are lower in comparison to the competitor who is making the profits of

61.02% in 2019. This shows that the company is not maintaining the gross profits on

adequate levels. This difference is because of the high cost which is incurred in BAP in

comparison to the KMD. There is the need for the company to take the adequate steps by

which the cost of goods sold proportion with respect to sales will decline and that will

increase the overall gross profits.

efficient management. Although the position of BAP is better in overall terms there is a

declining trend that is identified and that is an adverse situation for the company. The assets

are increasing but the revenue is not growing in the same percentage. Due to this, it can be

said that the management needs to make improvements and take steps by which efficiency

can be increased.

Operating profitability

The main aim which is set in every business is to make the profit in adequate terms. There is

the need for the maintenance of proper profits as by that there will be the establishment of the

sustainability of the business (Kabajeh, Al Nuaimat and Dahmash, 2012). In that, there are

various aspects which are required to be considered and by that the profits which are made

will be taken into account. There is the revenue that is made and in that process, the expenses

which are incurred in that respect will be considered (Mousa, 2015). With the help of that, the

profits will be ascertained and there will be adequate ascertainment of the profitability

position of the business. In the given case the profitability of the BAP has been considered

and with that, the calculation is also made for KMD which is its competitor.

The calculation of the gross profit has been made and in that, it can be noted that there is an

increase in the gross profit margin from 46.04% to 47.04% which is good but after this rise

also the profits are lower in comparison to the competitor who is making the profits of

61.02% in 2019. This shows that the company is not maintaining the gross profits on

adequate levels. This difference is because of the high cost which is incurred in BAP in

comparison to the KMD. There is the need for the company to take the adequate steps by

which the cost of goods sold proportion with respect to sales will decline and that will

increase the overall gross profits.

9

The operating profit margin is also calculated and in that it can be seen that there is the same

trend that is involved and the ratios are increasing but there is a lesser margin which is

maintained in BAP than that of the KMD. This shows the inability of the company in

managing the operating expenses which are incurred. They are high and due to that, the

profitability is affected in an adverse manner (Delen, Kuzey and Uyar, 2013). There are

various such costs that are incurred in the business and can be eliminated with little care.

They are made but are not that relevant and the performance will not be affected by their

avoidance. Such costs will be identified by the company and that will led to the undertaking

of the proper process and the overall profitability position will be made better.

The net profit margin is also ascertained which is also in a downward position to the

competitor KMD. There is the increment which is made but then also the level at which

competitor is performing is not attained. The net profit margin of BAP is 7.42% in 2019

whereas that of KMD is 10.54% (KMD, 2019). This difference is because of the deviation in

the interest expenses which are incurred. There are higher debts that are involved with BAP

and due to that, the company is required to bear a higher amount of interest cost. Due to this,

the overall profit which is made reduces and the adverse impact is borne. This will be

improved by BAP with the reduction of the interest cost and that will happen when the

outstanding debt will be reducing. With that, the interest will decline and the profitability will

be enhanced.

The overall result which is drawn shows that the improvement will be made in BAP as it is

below the level of profits which are managed by KMT its competitor.

Returns on shareholders’ investment

The funds which are required in the business are collected with the help of shareholders who

invest their money in the company. This is the amount which is paid by them for the shares

The operating profit margin is also calculated and in that it can be seen that there is the same

trend that is involved and the ratios are increasing but there is a lesser margin which is

maintained in BAP than that of the KMD. This shows the inability of the company in

managing the operating expenses which are incurred. They are high and due to that, the

profitability is affected in an adverse manner (Delen, Kuzey and Uyar, 2013). There are

various such costs that are incurred in the business and can be eliminated with little care.

They are made but are not that relevant and the performance will not be affected by their

avoidance. Such costs will be identified by the company and that will led to the undertaking

of the proper process and the overall profitability position will be made better.

The net profit margin is also ascertained which is also in a downward position to the

competitor KMD. There is the increment which is made but then also the level at which

competitor is performing is not attained. The net profit margin of BAP is 7.42% in 2019

whereas that of KMD is 10.54% (KMD, 2019). This difference is because of the deviation in

the interest expenses which are incurred. There are higher debts that are involved with BAP

and due to that, the company is required to bear a higher amount of interest cost. Due to this,

the overall profit which is made reduces and the adverse impact is borne. This will be

improved by BAP with the reduction of the interest cost and that will happen when the

outstanding debt will be reducing. With that, the interest will decline and the profitability will

be enhanced.

The overall result which is drawn shows that the improvement will be made in BAP as it is

below the level of profits which are managed by KMT its competitor.

Returns on shareholders’ investment

The funds which are required in the business are collected with the help of shareholders who

invest their money in the company. This is the amount which is paid by them for the shares

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

which are issued by the company and on that they expect a certain return which will be paid

to them on a periodic basis. It is identified as the return on the shareholder investment. This is

the amount that is earned by them on the equity which is held by them in the company (Halim

et al., 2012). This will be available to them when the company will be making profits in a

particular year. The calculation for the same is made and return on the equity has been made.

There is growth that is identified in the company on the return on equity which was 13.14%

in 2018 but has reached 13.37% in 2019. This is good for the shareholders as they are getting

higher returns which will attract them. This will make them invest more in the company in

the coming period. On the contrary, the return on equity in the case of KMD is ascertained

which is increasing in the company but is lower than that of BAP. There is an increase which

is made from 12.05% to 13.04% in the span of one year but if the same is noticed then it is

determined that return is lower than the one made by the shareholders of BAP.

This shows that although the profitability position of BAP is not that good the return on

equity is maintained at a higher level. This will be beneficial for the company in the long run

as there will be more investment which will be available and so the hindrance of sources will

not be faced.

Capital expenditures

The capital expenditures are required to be made in the company in order to grow it and use

the expenses for the development of the business. There are various such areas in which

capital expenditure can be made. They are made by taking care of the return which will be

available with them. In the case of KMD, there is the capital expenditure that has been made

amounting to $15.7 million and has been used for the optimization of the store network.

There are various new stores that are opened and with that renovation has also been

undertaken in respect of the other stores (KMD, 2019). This expenditure is incurred one time

which are issued by the company and on that they expect a certain return which will be paid

to them on a periodic basis. It is identified as the return on the shareholder investment. This is

the amount that is earned by them on the equity which is held by them in the company (Halim

et al., 2012). This will be available to them when the company will be making profits in a

particular year. The calculation for the same is made and return on the equity has been made.

There is growth that is identified in the company on the return on equity which was 13.14%

in 2018 but has reached 13.37% in 2019. This is good for the shareholders as they are getting

higher returns which will attract them. This will make them invest more in the company in

the coming period. On the contrary, the return on equity in the case of KMD is ascertained

which is increasing in the company but is lower than that of BAP. There is an increase which

is made from 12.05% to 13.04% in the span of one year but if the same is noticed then it is

determined that return is lower than the one made by the shareholders of BAP.

This shows that although the profitability position of BAP is not that good the return on

equity is maintained at a higher level. This will be beneficial for the company in the long run

as there will be more investment which will be available and so the hindrance of sources will

not be faced.

Capital expenditures

The capital expenditures are required to be made in the company in order to grow it and use

the expenses for the development of the business. There are various such areas in which

capital expenditure can be made. They are made by taking care of the return which will be

available with them. In the case of KMD, there is the capital expenditure that has been made

amounting to $15.7 million and has been used for the optimization of the store network.

There are various new stores that are opened and with that renovation has also been

undertaken in respect of the other stores (KMD, 2019). This expenditure is incurred one time

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

but the benefit of the same is attained for a lifetime. The funding which is required in this

respect is made with the help of equity as there is a reduction in the debt balance (Emmanuel

and Oladiran, 2015). The amount is invested in such a manner that the benefit of the same

will be gained for a lifetime. The stores will be bringing more customers and the overall

improvement in the sales and performance will be made possible.

The capital expenditure has also been made in BAP and in that the parts of commercial trucks

have been acquired. This is the main requirement in the automotive business and as this is

made one time it is considered as the capital investment. This is financed by the company

with the help of issuing shares of the company (BAP, 2019). A certain portion of the capital

expenditure has also been financed with the help of debt funding. All of this ensures that the

growth is taking place and will be bringing benefits for the company in the long-run.

Conclusion and recommendations

The complete analysis has been made and in that, all the important areas have been covered.

There is the analysis that has been made for the evaluation of the performance which is made

and the position that is maintained by BAP and KMD. Under this, there is the identification

of the objectives of the Company for which the business is carried and with that, the long-

term plans which are framed and will be implemented are identified. By that, the main aim of

the business is made clear and the step it is taking towards the attainment of sustainability has

been demonstrated. The ratio analysis has been used and for that various financial ratios have

been calculated with the help of the information that is available in the annual report of the

company. This has been used for further evaluation and with that liquidity position is

ascertained together with the capital structure and efficiency of the assets. There is the

consideration of all the areas and it is identified that BAP is in the lower position and KMD is

acting as its competitor. The position maintained by KMD is better and there are several

but the benefit of the same is attained for a lifetime. The funding which is required in this

respect is made with the help of equity as there is a reduction in the debt balance (Emmanuel

and Oladiran, 2015). The amount is invested in such a manner that the benefit of the same

will be gained for a lifetime. The stores will be bringing more customers and the overall

improvement in the sales and performance will be made possible.

The capital expenditure has also been made in BAP and in that the parts of commercial trucks

have been acquired. This is the main requirement in the automotive business and as this is

made one time it is considered as the capital investment. This is financed by the company

with the help of issuing shares of the company (BAP, 2019). A certain portion of the capital

expenditure has also been financed with the help of debt funding. All of this ensures that the

growth is taking place and will be bringing benefits for the company in the long-run.

Conclusion and recommendations

The complete analysis has been made and in that, all the important areas have been covered.

There is the analysis that has been made for the evaluation of the performance which is made

and the position that is maintained by BAP and KMD. Under this, there is the identification

of the objectives of the Company for which the business is carried and with that, the long-

term plans which are framed and will be implemented are identified. By that, the main aim of

the business is made clear and the step it is taking towards the attainment of sustainability has

been demonstrated. The ratio analysis has been used and for that various financial ratios have

been calculated with the help of the information that is available in the annual report of the

company. This has been used for further evaluation and with that liquidity position is

ascertained together with the capital structure and efficiency of the assets. There is the

consideration of all the areas and it is identified that BAP is in the lower position and KMD is

acting as its competitor. The position maintained by KMD is better and there are several

12

reasons for the same which has been identified. The operating profitability has been

considered with the help of the findings which are made and that show the need for

improvement in the case of BAP. There is the proper evaluation that is made and it shows

that the company is maintaining lower profitability.

The returns which are made to the equity shareholders are better in the case of BAP and that

is a positive attribute. It will be making the investors satisfied and by that, there will be the

attainment of more funds. The capital expenditures which have been made are identified and

provided appropriately.

On the basis of all the findings which are made it can be noted that there is the need for

making changes by the BAP. There will be control which will be made on the expenses

which are made and with that the debt position will be reduced. The high interest led to the

decline in profits and so they will be controlled. The areas in which improvement will be

made are identified and they will be taken into consideration for further performance.

reasons for the same which has been identified. The operating profitability has been

considered with the help of the findings which are made and that show the need for

improvement in the case of BAP. There is the proper evaluation that is made and it shows

that the company is maintaining lower profitability.

The returns which are made to the equity shareholders are better in the case of BAP and that

is a positive attribute. It will be making the investors satisfied and by that, there will be the

attainment of more funds. The capital expenditures which have been made are identified and

provided appropriately.

On the basis of all the findings which are made it can be noted that there is the need for

making changes by the BAP. There will be control which will be made on the expenses

which are made and with that the debt position will be reduced. The high interest led to the

decline in profits and so they will be controlled. The areas in which improvement will be

made are identified and they will be taken into consideration for further performance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.