HI6028 Taxation Theory, Practice and Law Assignment: Analysis

VerifiedAdded on 2022/09/02

|8

|2387

|19

Homework Assignment

AI Summary

This assignment analyzes two taxation issues: the computation of Emmi's taxable income, considering tips, salary, gifts, and entertainment allowances; and the applicability of Capital Gains Tax (CGT) to Liu's transactions, including the sale of a house, car, business, furniture, and paintings. The solution references relevant legislation, including the Income Tax Assessment Act 1997 (ITAA 1997) and ATO guidelines, to determine assessable income and CGT liabilities. The first part calculates Emmi's assessable income, including tips, salary, and entertainment allowance, while excluding gifts. The second part examines Liu's CGT obligations, applying exemptions for main residences, cars, and personal use assets, and considering small business concessions and collectibles. The assignment provides detailed calculations and justifications based on tax laws and regulations.

Running head: INTERNATIONAL FINANCE

Taxation Theory, Practice and Law

Name of the Student

Name of the University

Author Note

Taxation Theory, Practice and Law

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION THEORY, PRACTICE AND LAW

Table of Contents

Answer to Question 1........................................................................................................2

Issue...............................................................................................................................2

Relevant Legislation.......................................................................................................2

Application of Law..........................................................................................................3

Annual Assessable Income of Emmi..............................................................................4

Answer to Question 2........................................................................................................5

Issue...............................................................................................................................5

Relevant Laws................................................................................................................6

Application......................................................................................................................7

Computation of Tax Liability of Liu.................................................................................8

References...................................................................................................................10

TAXATION THEORY, PRACTICE AND LAW

Table of Contents

Answer to Question 1........................................................................................................2

Issue...............................................................................................................................2

Relevant Legislation.......................................................................................................2

Application of Law..........................................................................................................3

Annual Assessable Income of Emmi..............................................................................4

Answer to Question 2........................................................................................................5

Issue...............................................................................................................................5

Relevant Laws................................................................................................................6

Application......................................................................................................................7

Computation of Tax Liability of Liu.................................................................................8

References...................................................................................................................10

2

TAXATION THEORY, PRACTICE AND LAW

Answer to Question 1

Issue

The issue is related to the computation of the taxable income of Emmi. She is

studying accounting at Holmes Institute and also working part-time in Crown Melbourne

restaurant. The main aspect to be discussed in this regard is whether the fringe benefits

and the income received by her are a part of her annual assessable income for taxation

purposes or not. The benefits received by her in the given financial year are as follows:

Received $335 from the customers of the restaurant in cash;

Her annual income from working in the Crown Melbourne Restaurants is $25000;

A gift received by her, a perfume is worth $250 from a regular customer as a part

of the Christmas benefits. However, she does not use this perfume and has

given the same to her mother;

Entertainment allowance received by her from her restaurant owner. The meals

consumed by her is worth $380. She considers them to be a part of the rewards

received for her hard work; and

$15000 has been received by her from father as a Christmas gift.

Relevant Legislation

The relevant legislations regarding the assessable income of Emmi are as

follows:

As per the guidelines of ATO, tips received from customers are a part of the

assessable income of an individual. This is the case in all situation irrespective of

the manner in which they are received by the individual, i.e. either directly from

the customer or the employer. As suggested by the case law Wrottesley v

Regent Street Florida Restaurant, a system may also be agreed with regards to

the tips by the employees and the employers. With regards to cash tips, the rules

of ATO suggest that they should be declared in the income tax return of an

individual (Ato.gov.au. 2020). The source of payment is irrelevant in this case;

According to section 6.5 of 1997, the assessable income of an individual

includes all income earned by them as a part of their job (Classic.austlii.edu.au.

2020). The provisions of ATO suggest that the salaries and wages received by

an individual form a part of the assessable income if they earn enough money to

cross the tax-threshold;

According to section 78A of ITAA 1936, there are a few circumstances under

which a Deductible Gift Recipient (DGR) is not an allowable deduction under

Division 30 of ITAA 1997. There is no fixed definition of the word ‘gift’ under ITAA

1997. In Federal Commissioner of Taxation v. McPhail (1968) 117 CLR 111

(McPhail), the same was suggested by the court. There are a few conditions that

the court has identified as a part of their characteristics. They include the transfer

of the beneficial interest in a property and it is made voluntarily. The giver also

does not expect anything in return for giving the gift to the other party. The rules

of ATO state that the rewards or gifts received on special occasions and gifts

received out of love are not taxable in the hands of an employee;

The provisions of ATO related to gifts suggest that gifts are included as a part of

the assessable income of an employee if they are received as part of a business-

TAXATION THEORY, PRACTICE AND LAW

Answer to Question 1

Issue

The issue is related to the computation of the taxable income of Emmi. She is

studying accounting at Holmes Institute and also working part-time in Crown Melbourne

restaurant. The main aspect to be discussed in this regard is whether the fringe benefits

and the income received by her are a part of her annual assessable income for taxation

purposes or not. The benefits received by her in the given financial year are as follows:

Received $335 from the customers of the restaurant in cash;

Her annual income from working in the Crown Melbourne Restaurants is $25000;

A gift received by her, a perfume is worth $250 from a regular customer as a part

of the Christmas benefits. However, she does not use this perfume and has

given the same to her mother;

Entertainment allowance received by her from her restaurant owner. The meals

consumed by her is worth $380. She considers them to be a part of the rewards

received for her hard work; and

$15000 has been received by her from father as a Christmas gift.

Relevant Legislation

The relevant legislations regarding the assessable income of Emmi are as

follows:

As per the guidelines of ATO, tips received from customers are a part of the

assessable income of an individual. This is the case in all situation irrespective of

the manner in which they are received by the individual, i.e. either directly from

the customer or the employer. As suggested by the case law Wrottesley v

Regent Street Florida Restaurant, a system may also be agreed with regards to

the tips by the employees and the employers. With regards to cash tips, the rules

of ATO suggest that they should be declared in the income tax return of an

individual (Ato.gov.au. 2020). The source of payment is irrelevant in this case;

According to section 6.5 of 1997, the assessable income of an individual

includes all income earned by them as a part of their job (Classic.austlii.edu.au.

2020). The provisions of ATO suggest that the salaries and wages received by

an individual form a part of the assessable income if they earn enough money to

cross the tax-threshold;

According to section 78A of ITAA 1936, there are a few circumstances under

which a Deductible Gift Recipient (DGR) is not an allowable deduction under

Division 30 of ITAA 1997. There is no fixed definition of the word ‘gift’ under ITAA

1997. In Federal Commissioner of Taxation v. McPhail (1968) 117 CLR 111

(McPhail), the same was suggested by the court. There are a few conditions that

the court has identified as a part of their characteristics. They include the transfer

of the beneficial interest in a property and it is made voluntarily. The giver also

does not expect anything in return for giving the gift to the other party. The rules

of ATO state that the rewards or gifts received on special occasions and gifts

received out of love are not taxable in the hands of an employee;

The provisions of ATO related to gifts suggest that gifts are included as a part of

the assessable income of an employee if they are received as part of a business-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION THEORY, PRACTICE AND LAW

like activity or related to the income-earning activities as an employee or

contractor;

The final aspect is related to the gift received as a part of the Christmas

presents. The rules of ATO state that any gift received as a part of special

occasions or birthday presents and gifts received out of love from relatives or out

of love are not to be considered as a part of the assessable income of the

individual.

Application of Law

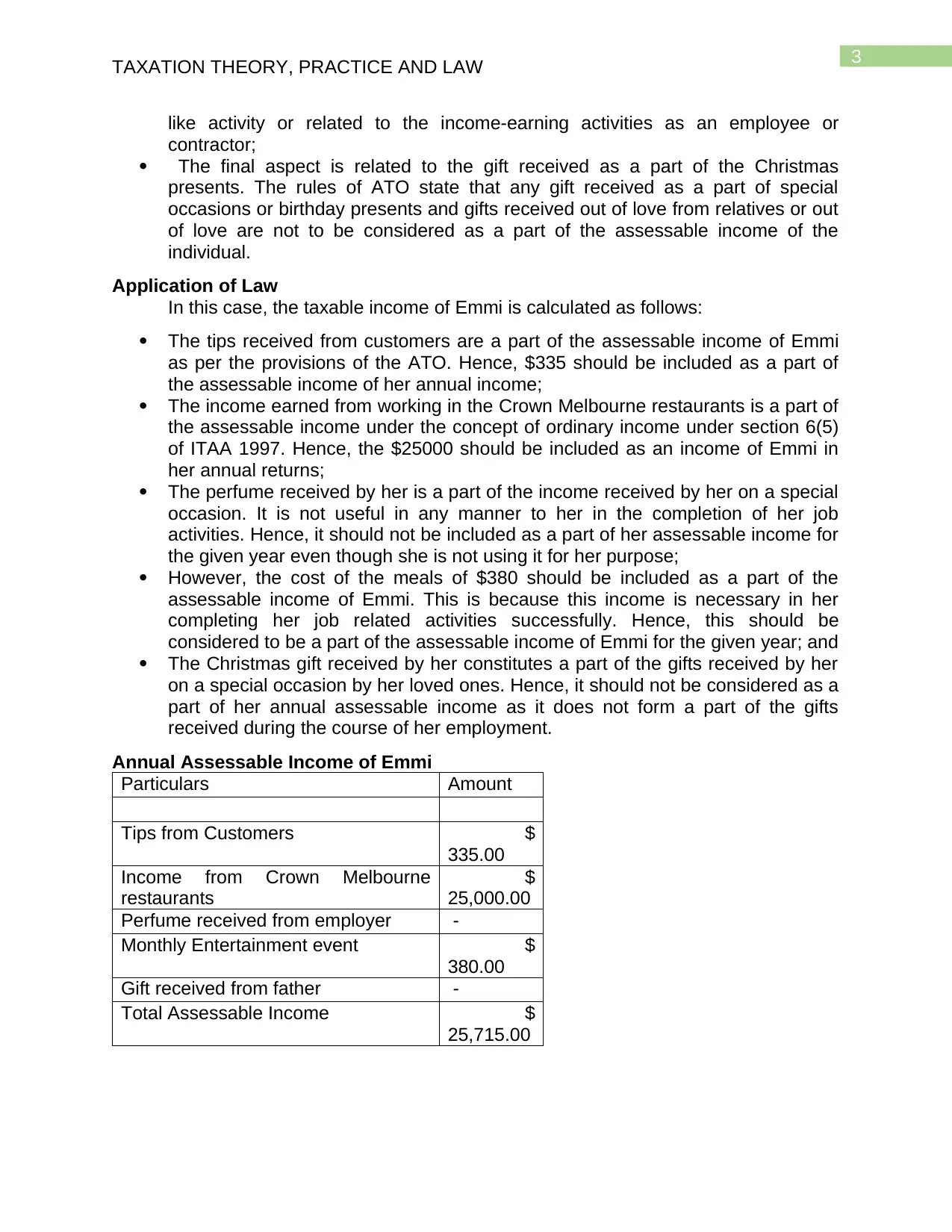

In this case, the taxable income of Emmi is calculated as follows:

The tips received from customers are a part of the assessable income of Emmi

as per the provisions of the ATO. Hence, $335 should be included as a part of

the assessable income of her annual income;

The income earned from working in the Crown Melbourne restaurants is a part of

the assessable income under the concept of ordinary income under section 6(5)

of ITAA 1997. Hence, the $25000 should be included as an income of Emmi in

her annual returns;

The perfume received by her is a part of the income received by her on a special

occasion. It is not useful in any manner to her in the completion of her job

activities. Hence, it should not be included as a part of her assessable income for

the given year even though she is not using it for her purpose;

However, the cost of the meals of $380 should be included as a part of the

assessable income of Emmi. This is because this income is necessary in her

completing her job related activities successfully. Hence, this should be

considered to be a part of the assessable income of Emmi for the given year; and

The Christmas gift received by her constitutes a part of the gifts received by her

on a special occasion by her loved ones. Hence, it should not be considered as a

part of her annual assessable income as it does not form a part of the gifts

received during the course of her employment.

Annual Assessable Income of Emmi

Particulars Amount

Tips from Customers $

335.00

Income from Crown Melbourne

restaurants

$

25,000.00

Perfume received from employer -

Monthly Entertainment event $

380.00

Gift received from father -

Total Assessable Income $

25,715.00

TAXATION THEORY, PRACTICE AND LAW

like activity or related to the income-earning activities as an employee or

contractor;

The final aspect is related to the gift received as a part of the Christmas

presents. The rules of ATO state that any gift received as a part of special

occasions or birthday presents and gifts received out of love from relatives or out

of love are not to be considered as a part of the assessable income of the

individual.

Application of Law

In this case, the taxable income of Emmi is calculated as follows:

The tips received from customers are a part of the assessable income of Emmi

as per the provisions of the ATO. Hence, $335 should be included as a part of

the assessable income of her annual income;

The income earned from working in the Crown Melbourne restaurants is a part of

the assessable income under the concept of ordinary income under section 6(5)

of ITAA 1997. Hence, the $25000 should be included as an income of Emmi in

her annual returns;

The perfume received by her is a part of the income received by her on a special

occasion. It is not useful in any manner to her in the completion of her job

activities. Hence, it should not be included as a part of her assessable income for

the given year even though she is not using it for her purpose;

However, the cost of the meals of $380 should be included as a part of the

assessable income of Emmi. This is because this income is necessary in her

completing her job related activities successfully. Hence, this should be

considered to be a part of the assessable income of Emmi for the given year; and

The Christmas gift received by her constitutes a part of the gifts received by her

on a special occasion by her loved ones. Hence, it should not be considered as a

part of her annual assessable income as it does not form a part of the gifts

received during the course of her employment.

Annual Assessable Income of Emmi

Particulars Amount

Tips from Customers $

335.00

Income from Crown Melbourne

restaurants

$

25,000.00

Perfume received from employer -

Monthly Entertainment event $

380.00

Gift received from father -

Total Assessable Income $

25,715.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION THEORY, PRACTICE AND LAW

Answer to Question 2

Issue

The issue in this case is related to Liu, a 65 year old Australian resident who was

born in China. The advice that needs to be provided to her is related to the applicability

of the Capital Gains Tax (CGT) on the transactions entered into her by the given

financial year. The transactions are as follows:

She is planning to sell a house which was purchased in 1981 and was her main

residence since she first purchased it. The purchase price of the house was

$55000 and its worth is now $630000;

The next sale is related to a car which was purchased for $37000 in 2011 but is

now worth around $8000;

Her photography business is worth $125000 in the present day. The

consideration received from the sale includes $53000 for equipment which cost

her $63000 and $50000 received for Goodwill;

The sale of the furniture is worth $4800. None of the items of the furniture cost

her more than $2000;

The sale of her paintings is worth $28000. Majority of the paintings were

purchased second hand and not a single painting cost her more than $500.

However, one of the paintings which cost her $1000 has been sold for an amount

of $8000.

Relevant Laws

According to section 102.20 of ITAA 1997, capital gains tax is applicable to

capital gains or losses when a CGT event occurs. The rules of ATO suggest that

the main residence exemption is not allowed for properties acquired after 9 May

2017 for foreign and temporary tax residents (Ato.gov.au. 2020). However, for a

permanent resident, the exemption is available on the capital gains under section

118.100. This section states that the exemption is available only if the property

was used exclusively for residential purposes and was not used for producing

any assessable income. It states that for properties purchased on or before 20th

September 1985, the capital gains are to be ignored if there are no capital

improvements made to the property;

The rules of ATO suggest that the capital gains or losses occurring on the sale of

a car are exempt provided that it meets the definition of car under section 995-1

of ITAA 1997. According to this section, a car or a motor vehicle is a vehicle

designed to carry a load of less than one tonne and fewer than 9 passengers;

The rules of ATO provide a varied range of exemptions to the small businesses

earning capital gains in a particular year. They are the 15 year exemption, 50%

active asset reduction, retirement exemption and rollover of the capital gains

earned by a business (Ato.gov.au. 2020). The retirement exemption is available

to residents who will be retiring from business after the disposal of the assets.

The capital gains from the sale of these active assets is exempt up to a lifetime

limit of $500000;

As per Section 108.20 of ITAA 1997, any capital gain or loss on a personal use

asset is disregarded if it is purchased for an amount of less than $10000. As per

the section, a personal use asset is one which is mainly kept for the personal use

TAXATION THEORY, PRACTICE AND LAW

Answer to Question 2

Issue

The issue in this case is related to Liu, a 65 year old Australian resident who was

born in China. The advice that needs to be provided to her is related to the applicability

of the Capital Gains Tax (CGT) on the transactions entered into her by the given

financial year. The transactions are as follows:

She is planning to sell a house which was purchased in 1981 and was her main

residence since she first purchased it. The purchase price of the house was

$55000 and its worth is now $630000;

The next sale is related to a car which was purchased for $37000 in 2011 but is

now worth around $8000;

Her photography business is worth $125000 in the present day. The

consideration received from the sale includes $53000 for equipment which cost

her $63000 and $50000 received for Goodwill;

The sale of the furniture is worth $4800. None of the items of the furniture cost

her more than $2000;

The sale of her paintings is worth $28000. Majority of the paintings were

purchased second hand and not a single painting cost her more than $500.

However, one of the paintings which cost her $1000 has been sold for an amount

of $8000.

Relevant Laws

According to section 102.20 of ITAA 1997, capital gains tax is applicable to

capital gains or losses when a CGT event occurs. The rules of ATO suggest that

the main residence exemption is not allowed for properties acquired after 9 May

2017 for foreign and temporary tax residents (Ato.gov.au. 2020). However, for a

permanent resident, the exemption is available on the capital gains under section

118.100. This section states that the exemption is available only if the property

was used exclusively for residential purposes and was not used for producing

any assessable income. It states that for properties purchased on or before 20th

September 1985, the capital gains are to be ignored if there are no capital

improvements made to the property;

The rules of ATO suggest that the capital gains or losses occurring on the sale of

a car are exempt provided that it meets the definition of car under section 995-1

of ITAA 1997. According to this section, a car or a motor vehicle is a vehicle

designed to carry a load of less than one tonne and fewer than 9 passengers;

The rules of ATO provide a varied range of exemptions to the small businesses

earning capital gains in a particular year. They are the 15 year exemption, 50%

active asset reduction, retirement exemption and rollover of the capital gains

earned by a business (Ato.gov.au. 2020). The retirement exemption is available

to residents who will be retiring from business after the disposal of the assets.

The capital gains from the sale of these active assets is exempt up to a lifetime

limit of $500000;

As per Section 108.20 of ITAA 1997, any capital gain or loss on a personal use

asset is disregarded if it is purchased for an amount of less than $10000. As per

the section, a personal use asset is one which is mainly kept for the personal use

5

TAXATION THEORY, PRACTICE AND LAW

or enjoyment of the taxpayer. It also includes an option or right to acquire such

an asset and a debt arising from a CGT event; and

As per section 108.10 of ITAA 1997, a collectible is defined as an artwork,

jewellery, an antique, or a medallion that is mainly kept for the enjoyment

purposes of the taxpayer. The capital gains arising from the sale of these

collectibles are to be ignored if the collectible was initially acquired for an amount

of less than $500.

Application

In case of the house property, the rules applicable to an ordinary Australian

resident are also applicable for Liu. According to these rules, any capital gains or

losses arising from the sale of the main residence of a taxpayer are to be ignored

from the CGT. Hence, the amount earned from the sale of the residential

property is to be ignored from the Capital Gains Tax. Therefore, the amount of

capital gains of $575000 ($630000-$55000) is not chargeable under CGT in the

hands of Liu;

The car as covered under Section 995-1 of ITAA 1997 is to be ignored from CGT

in the hands of the taxpayer. However, the car should meet the criteria

suggested under this section and should only be used for the purpose of the

personal use of the taxpayer;

The furniture is covered under the definition of personal use asset. Any capital

gains arising on the sale of this personal use asset are to be ignored if the initial

cost of acquisition of the asset was less than $10000. In this case, as none of the

furniture cost more than $2000, which is below the threshold limit of $10000, the

capital gains should not be considered to be a part of the assessable income of

Liu;

The paintings owned by Liu constitute a part of the collectibles defined under

section 108.10. If the cost of acquisition of these items was less than $500, then

they should not be considered to be a part of the assessable income of the

individual for that year. In Liu’s case, most of the paintings owned by her are to

be ignored from the amount of capital gains earned by her. However, the painting

that was purchased from the artist for $1000 should be taxable under CGT as per

the provisions of the ATO.

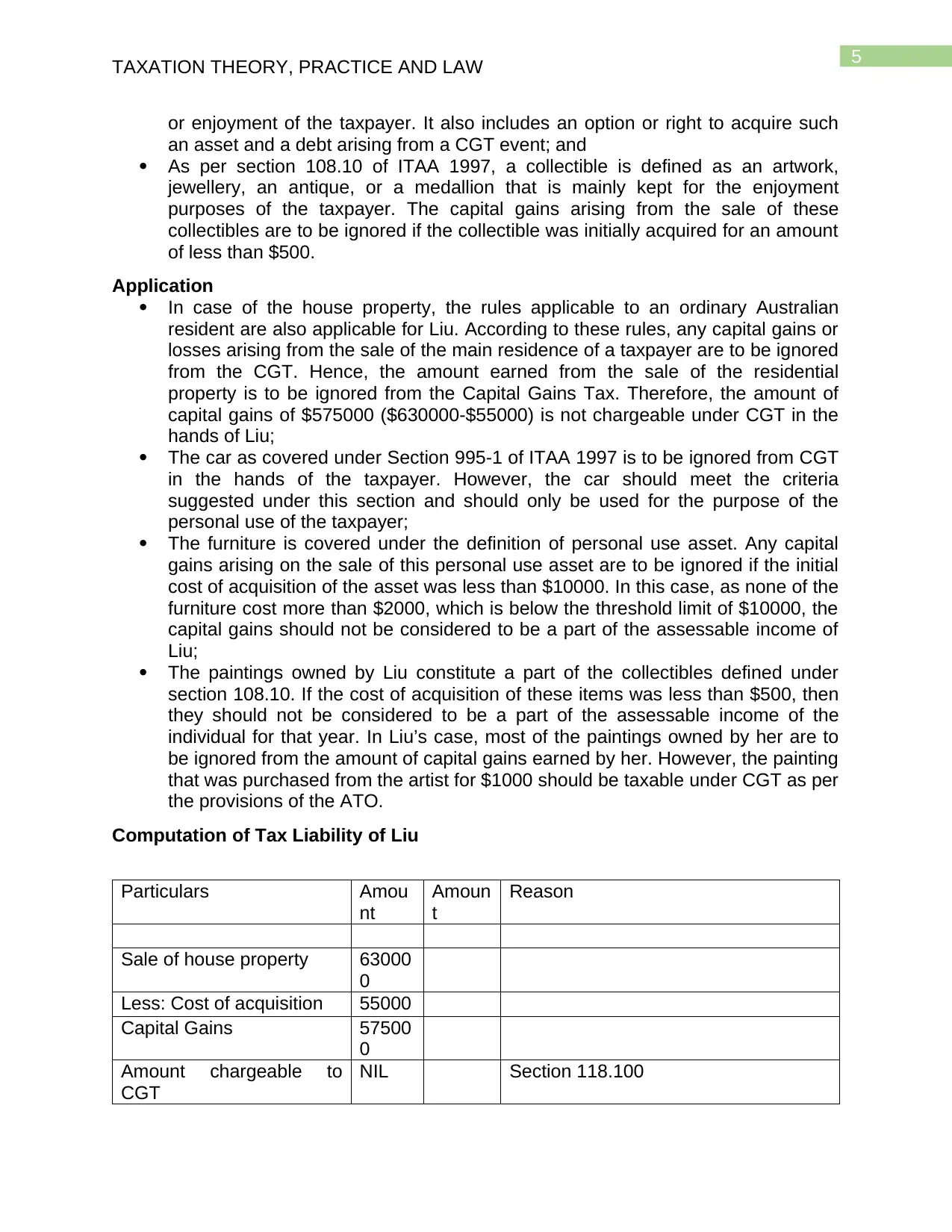

Computation of Tax Liability of Liu

Particulars Amou

nt

Amoun

t

Reason

Sale of house property 63000

0

Less: Cost of acquisition 55000

Capital Gains 57500

0

Amount chargeable to

CGT

NIL Section 118.100

TAXATION THEORY, PRACTICE AND LAW

or enjoyment of the taxpayer. It also includes an option or right to acquire such

an asset and a debt arising from a CGT event; and

As per section 108.10 of ITAA 1997, a collectible is defined as an artwork,

jewellery, an antique, or a medallion that is mainly kept for the enjoyment

purposes of the taxpayer. The capital gains arising from the sale of these

collectibles are to be ignored if the collectible was initially acquired for an amount

of less than $500.

Application

In case of the house property, the rules applicable to an ordinary Australian

resident are also applicable for Liu. According to these rules, any capital gains or

losses arising from the sale of the main residence of a taxpayer are to be ignored

from the CGT. Hence, the amount earned from the sale of the residential

property is to be ignored from the Capital Gains Tax. Therefore, the amount of

capital gains of $575000 ($630000-$55000) is not chargeable under CGT in the

hands of Liu;

The car as covered under Section 995-1 of ITAA 1997 is to be ignored from CGT

in the hands of the taxpayer. However, the car should meet the criteria

suggested under this section and should only be used for the purpose of the

personal use of the taxpayer;

The furniture is covered under the definition of personal use asset. Any capital

gains arising on the sale of this personal use asset are to be ignored if the initial

cost of acquisition of the asset was less than $10000. In this case, as none of the

furniture cost more than $2000, which is below the threshold limit of $10000, the

capital gains should not be considered to be a part of the assessable income of

Liu;

The paintings owned by Liu constitute a part of the collectibles defined under

section 108.10. If the cost of acquisition of these items was less than $500, then

they should not be considered to be a part of the assessable income of the

individual for that year. In Liu’s case, most of the paintings owned by her are to

be ignored from the amount of capital gains earned by her. However, the painting

that was purchased from the artist for $1000 should be taxable under CGT as per

the provisions of the ATO.

Computation of Tax Liability of Liu

Particulars Amou

nt

Amoun

t

Reason

Sale of house property 63000

0

Less: Cost of acquisition 55000

Capital Gains 57500

0

Amount chargeable to

CGT

NIL Section 118.100

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

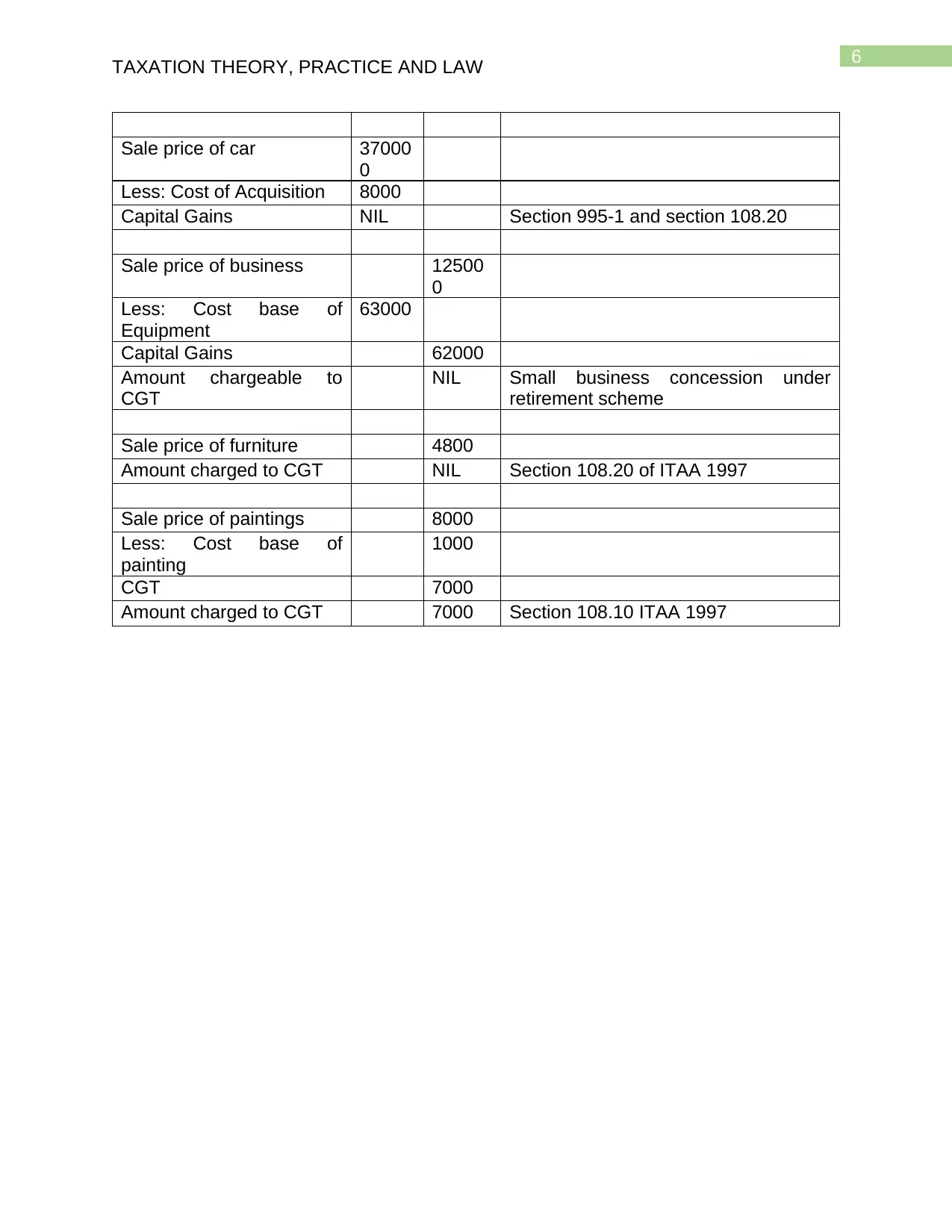

TAXATION THEORY, PRACTICE AND LAW

Sale price of car 37000

0

Less: Cost of Acquisition 8000

Capital Gains NIL Section 995-1 and section 108.20

Sale price of business 12500

0

Less: Cost base of

Equipment

63000

Capital Gains 62000

Amount chargeable to

CGT

NIL Small business concession under

retirement scheme

Sale price of furniture 4800

Amount charged to CGT NIL Section 108.20 of ITAA 1997

Sale price of paintings 8000

Less: Cost base of

painting

1000

CGT 7000

Amount charged to CGT 7000 Section 108.10 ITAA 1997

TAXATION THEORY, PRACTICE AND LAW

Sale price of car 37000

0

Less: Cost of Acquisition 8000

Capital Gains NIL Section 995-1 and section 108.20

Sale price of business 12500

0

Less: Cost base of

Equipment

63000

Capital Gains 62000

Amount chargeable to

CGT

NIL Small business concession under

retirement scheme

Sale price of furniture 4800

Amount charged to CGT NIL Section 108.20 of ITAA 1997

Sale price of paintings 8000

Less: Cost base of

painting

1000

CGT 7000

Amount charged to CGT 7000 Section 108.10 ITAA 1997

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION THEORY, PRACTICE AND LAW

References

Ato.gov.au. (2020). Amounts not included as income. [online] Available at:

https://www.ato.gov.au/Individuals/Income-and-deductions/Income-you-must-declare/

Amounts-not-included-as-income/ [Accessed 5 Jan. 2020].

Ato.gov.au. (2020). Calculators and tools_Host. [online] Available at:

https://www.ato.gov.au/Calculators-and-tools/Host/?

anchor=CGTPET&anchor=CGTPET/questions#CGTPET/questions [Accessed 5 Jan.

2020].

Ato.gov.au. (2020). CGT assets and exemptions. [online] Available at:

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

#Exemptions1 [Accessed 5 Jan. 2020].

Ato.gov.au. (2020). Small business CGT concessions. [online] Available at:

https://www.ato.gov.au/general/capital-gains-tax/small-business-cgt-concessions/

[Accessed 5 Jan. 2020].

Ato.gov.au. (2020). Your main residence. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/

Your-main-residence/ [Accessed 5 Jan. 2020].

Classic.austlii.edu.au. (2020). INCOME TAX ASSESSMENT ACT 1997 - SECT 6.5

Income according to ordinary concepts (ordinary income) . [online] Available at:

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s6.5.html [Accessed 5

Jan. 2020].

TAXATION THEORY, PRACTICE AND LAW

References

Ato.gov.au. (2020). Amounts not included as income. [online] Available at:

https://www.ato.gov.au/Individuals/Income-and-deductions/Income-you-must-declare/

Amounts-not-included-as-income/ [Accessed 5 Jan. 2020].

Ato.gov.au. (2020). Calculators and tools_Host. [online] Available at:

https://www.ato.gov.au/Calculators-and-tools/Host/?

anchor=CGTPET&anchor=CGTPET/questions#CGTPET/questions [Accessed 5 Jan.

2020].

Ato.gov.au. (2020). CGT assets and exemptions. [online] Available at:

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

#Exemptions1 [Accessed 5 Jan. 2020].

Ato.gov.au. (2020). Small business CGT concessions. [online] Available at:

https://www.ato.gov.au/general/capital-gains-tax/small-business-cgt-concessions/

[Accessed 5 Jan. 2020].

Ato.gov.au. (2020). Your main residence. [online] Available at:

https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/

Your-main-residence/ [Accessed 5 Jan. 2020].

Classic.austlii.edu.au. (2020). INCOME TAX ASSESSMENT ACT 1997 - SECT 6.5

Income according to ordinary concepts (ordinary income) . [online] Available at:

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s6.5.html [Accessed 5

Jan. 2020].

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.