Impact of Tax Avoidance on Corporate Performance

VerifiedAdded on 2021/04/24

|15

|2926

|131

AI Summary

This assignment requires students to analyze and summarize a collection of research papers and studies related to tax avoidance and its effects on corporate performance. The provided sources cover various aspects of tax avoidance, including its impact on earnings management, income shifting, and cash tax savings. Students are expected to carefully read and understand the content of each source, identifying key findings and insights that demonstrate the relationship between tax strategies and financial outcomes. By examining these research papers, students will gain a deeper understanding of the complex interactions between tax avoidance and corporate performance, as well as the potential implications for businesses and investors.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: BSBFIM601

BSBFIM601

Name of the Student:

Name of the University:

Author’s Note:

BSBFIM601

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

BSBFIM601

Table of Contents

Profit and Sales Budget...................................................................................................................2

GST Cash Flow Analysis/ Budget...................................................................................................4

Debtors Ageing Budget...................................................................................................................4

1. Identify the current statutory requirements for tax compliance and list and calculate the tax

liabilities for Houzit Pty Ltd under taxation legislation..................................................................6

2. Identify the current compliance requirements and liabilities for this organisation under the

Corporations Act 2001.....................................................................................................................7

3. Review commercially available financial management software to select the most suitable

software for Houzit Pty Ltd.............................................................................................................7

4. Explain how you can apply the following principles of accounting in developing the budgets

required for this task:.......................................................................................................................8

5. Explain and discuss the implications of probity when preparing and revising budgets...........9

6. List the critical dates and initiatives that will require or generate resources for Houzit Pty

Ltd in the next financial cycle.........................................................................................................9

7. List the items you would recommend for inclusion in the budgets for Houzit Pty Ltd.........10

8. List the new or modified internal controls that could improve risk management for Houzit

Pty Ltd including the maintenance of audit trails..........................................................................10

Bibliography..................................................................................................................................13

BSBFIM601

Table of Contents

Profit and Sales Budget...................................................................................................................2

GST Cash Flow Analysis/ Budget...................................................................................................4

Debtors Ageing Budget...................................................................................................................4

1. Identify the current statutory requirements for tax compliance and list and calculate the tax

liabilities for Houzit Pty Ltd under taxation legislation..................................................................6

2. Identify the current compliance requirements and liabilities for this organisation under the

Corporations Act 2001.....................................................................................................................7

3. Review commercially available financial management software to select the most suitable

software for Houzit Pty Ltd.............................................................................................................7

4. Explain how you can apply the following principles of accounting in developing the budgets

required for this task:.......................................................................................................................8

5. Explain and discuss the implications of probity when preparing and revising budgets...........9

6. List the critical dates and initiatives that will require or generate resources for Houzit Pty

Ltd in the next financial cycle.........................................................................................................9

7. List the items you would recommend for inclusion in the budgets for Houzit Pty Ltd.........10

8. List the new or modified internal controls that could improve risk management for Houzit

Pty Ltd including the maintenance of audit trails..........................................................................10

Bibliography..................................................................................................................................13

2

BSBFIM601

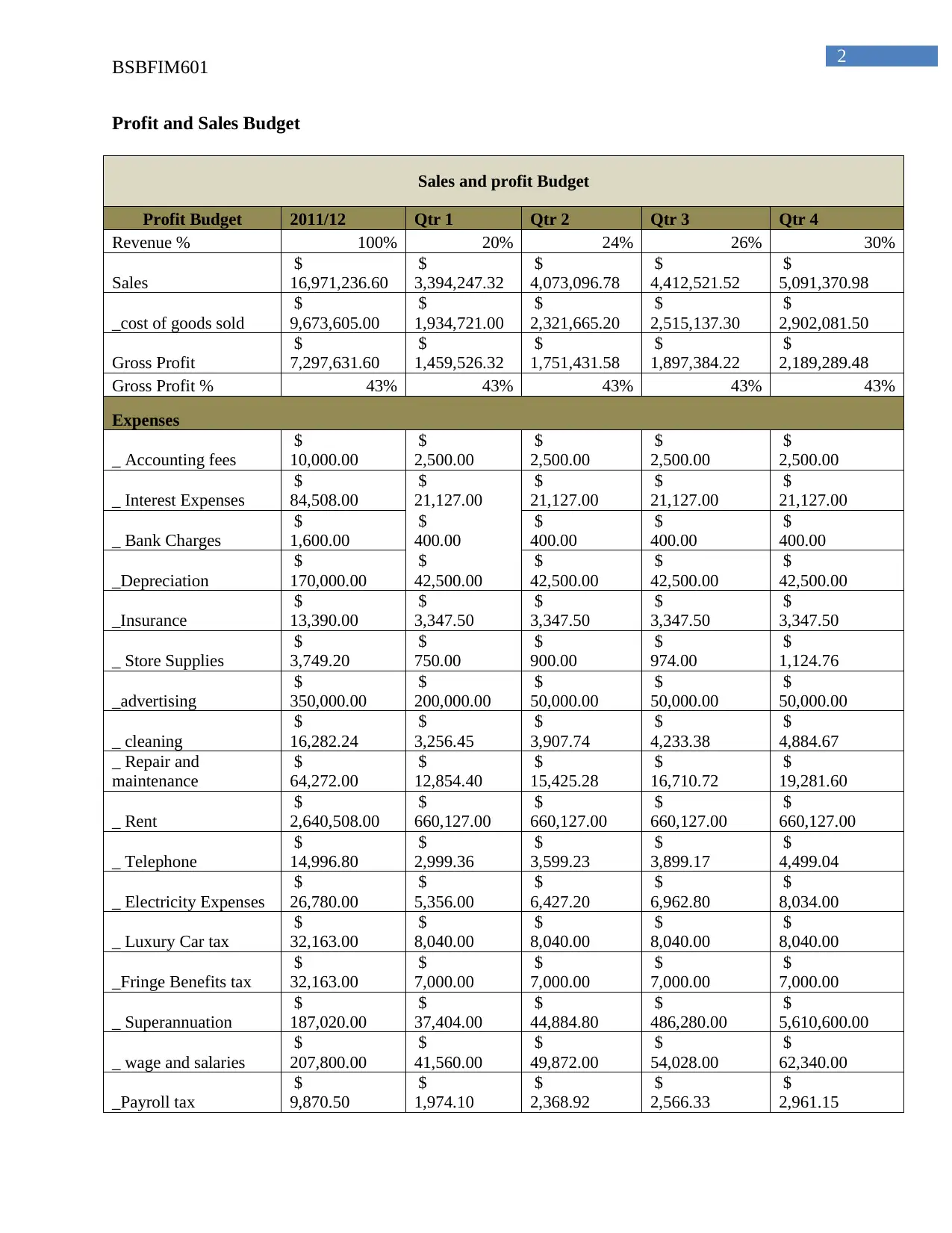

Profit and Sales Budget

Sales and profit Budget

Profit Budget 2011/12 Qtr 1 Qtr 2 Qtr 3 Qtr 4

Revenue % 100% 20% 24% 26% 30%

Sales

$

16,971,236.60

$

3,394,247.32

$

4,073,096.78

$

4,412,521.52

$

5,091,370.98

_cost of goods sold

$

9,673,605.00

$

1,934,721.00

$

2,321,665.20

$

2,515,137.30

$

2,902,081.50

Gross Profit

$

7,297,631.60

$

1,459,526.32

$

1,751,431.58

$

1,897,384.22

$

2,189,289.48

Gross Profit % 43% 43% 43% 43% 43%

Expenses

_ Accounting fees

$

10,000.00

$

2,500.00

$

2,500.00

$

2,500.00

$

2,500.00

_ Interest Expenses

$

84,508.00

$

21,127.00

$

21,127.00

$

21,127.00

$

21,127.00

_ Bank Charges

$

1,600.00

$

400.00

$

400.00

$

400.00

$

400.00

_Depreciation

$

170,000.00

$

42,500.00

$

42,500.00

$

42,500.00

$

42,500.00

_Insurance

$

13,390.00

$

3,347.50

$

3,347.50

$

3,347.50

$

3,347.50

_ Store Supplies

$

3,749.20

$

750.00

$

900.00

$

974.00

$

1,124.76

_advertising

$

350,000.00

$

200,000.00

$

50,000.00

$

50,000.00

$

50,000.00

_ cleaning

$

16,282.24

$

3,256.45

$

3,907.74

$

4,233.38

$

4,884.67

_ Repair and

maintenance

$

64,272.00

$

12,854.40

$

15,425.28

$

16,710.72

$

19,281.60

_ Rent

$

2,640,508.00

$

660,127.00

$

660,127.00

$

660,127.00

$

660,127.00

_ Telephone

$

14,996.80

$

2,999.36

$

3,599.23

$

3,899.17

$

4,499.04

_ Electricity Expenses

$

26,780.00

$

5,356.00

$

6,427.20

$

6,962.80

$

8,034.00

_ Luxury Car tax

$

32,163.00

$

8,040.00

$

8,040.00

$

8,040.00

$

8,040.00

_Fringe Benefits tax

$

32,163.00

$

7,000.00

$

7,000.00

$

7,000.00

$

7,000.00

_ Superannuation

$

187,020.00

$

37,404.00

$

44,884.80

$

486,280.00

$

5,610,600.00

_ wage and salaries

$

207,800.00

$

41,560.00

$

49,872.00

$

54,028.00

$

62,340.00

_Payroll tax

$

9,870.50

$

1,974.10

$

2,368.92

$

2,566.33

$

2,961.15

BSBFIM601

Profit and Sales Budget

Sales and profit Budget

Profit Budget 2011/12 Qtr 1 Qtr 2 Qtr 3 Qtr 4

Revenue % 100% 20% 24% 26% 30%

Sales

$

16,971,236.60

$

3,394,247.32

$

4,073,096.78

$

4,412,521.52

$

5,091,370.98

_cost of goods sold

$

9,673,605.00

$

1,934,721.00

$

2,321,665.20

$

2,515,137.30

$

2,902,081.50

Gross Profit

$

7,297,631.60

$

1,459,526.32

$

1,751,431.58

$

1,897,384.22

$

2,189,289.48

Gross Profit % 43% 43% 43% 43% 43%

Expenses

_ Accounting fees

$

10,000.00

$

2,500.00

$

2,500.00

$

2,500.00

$

2,500.00

_ Interest Expenses

$

84,508.00

$

21,127.00

$

21,127.00

$

21,127.00

$

21,127.00

_ Bank Charges

$

1,600.00

$

400.00

$

400.00

$

400.00

$

400.00

_Depreciation

$

170,000.00

$

42,500.00

$

42,500.00

$

42,500.00

$

42,500.00

_Insurance

$

13,390.00

$

3,347.50

$

3,347.50

$

3,347.50

$

3,347.50

_ Store Supplies

$

3,749.20

$

750.00

$

900.00

$

974.00

$

1,124.76

_advertising

$

350,000.00

$

200,000.00

$

50,000.00

$

50,000.00

$

50,000.00

_ cleaning

$

16,282.24

$

3,256.45

$

3,907.74

$

4,233.38

$

4,884.67

_ Repair and

maintenance

$

64,272.00

$

12,854.40

$

15,425.28

$

16,710.72

$

19,281.60

_ Rent

$

2,640,508.00

$

660,127.00

$

660,127.00

$

660,127.00

$

660,127.00

_ Telephone

$

14,996.80

$

2,999.36

$

3,599.23

$

3,899.17

$

4,499.04

_ Electricity Expenses

$

26,780.00

$

5,356.00

$

6,427.20

$

6,962.80

$

8,034.00

_ Luxury Car tax

$

32,163.00

$

8,040.00

$

8,040.00

$

8,040.00

$

8,040.00

_Fringe Benefits tax

$

32,163.00

$

7,000.00

$

7,000.00

$

7,000.00

$

7,000.00

_ Superannuation

$

187,020.00

$

37,404.00

$

44,884.80

$

486,280.00

$

5,610,600.00

_ wage and salaries

$

207,800.00

$

41,560.00

$

49,872.00

$

54,028.00

$

62,340.00

_Payroll tax

$

9,870.50

$

1,974.10

$

2,368.92

$

2,566.33

$

2,961.15

3

BSBFIM601

_workers'

Compensation

$

4,156.00

$

831.20

$

997.44

$

1,080.56

$

1,246.80

Total Expenses $ 2,812,141.24

$

696,730.71

$

701,773.95

$

697,331.77

$

713,837.61

Net Profit (before

tax) $ 4,505,653.36

$

762,795.61

$

1,049,657.63

$

1,200,052.45

$

1,306,580.63

Income tax $ 1,340,250.24

$

228,838.68

$

314,897.29

$

360,015.73

$

391,974.19

Net Profit $ 3,165,403.12

$

533,956.93

$

734,760.34

$

840,036.71

$

914,606.44

Sales budget for the financial year 2011-2012

Total Budget: 16971237

Departmen

t

Sale

percentage

(%)

Total budget

2011-2012

Qtr 1 Qtr 2 Qtr 3 Qtr4

20% 24% 26% 30%

Bathroon

fitting 30%

$

5,091,371.10

$

1,018,274.2

2

$

1,221,929.0

6

$

132,756.49

$

152,741,133.0

0

Bedroom

fitting 25%

$

4,242,809.25

$

848,561.85

$

1,018,274.2

2

$

1,103,130.4

1

$

1,272,842.78

Mirrors 15%

$

2,545,685.55

$

509,137.11

$

610,964.53

$

661,878.24

$

763,705.67

decorative

items 10%

$

1,697,123.70

$

339,424.74

$

407,309.69

$

441,252.16

$

509,137.11

lighting

fixtures 20%

$

3,394,247.40

$

678,849.48

$

814,619.38

$

882,504.32

$

1,018,274.22

Total 100% 1697123700 339424740 407309688 441252162 5091371.1

Departmen

t

Sale

percentage

(%)

Total budget

2011-2012

Qtr 1 Qtr 2 Qtr 3 Qtr4

20% 24% 26% 30%

Total 100%

$

16,971,237.00 3394247.4 4073096.88 4412521.62 0

BSBFIM601

_workers'

Compensation

$

4,156.00

$

831.20

$

997.44

$

1,080.56

$

1,246.80

Total Expenses $ 2,812,141.24

$

696,730.71

$

701,773.95

$

697,331.77

$

713,837.61

Net Profit (before

tax) $ 4,505,653.36

$

762,795.61

$

1,049,657.63

$

1,200,052.45

$

1,306,580.63

Income tax $ 1,340,250.24

$

228,838.68

$

314,897.29

$

360,015.73

$

391,974.19

Net Profit $ 3,165,403.12

$

533,956.93

$

734,760.34

$

840,036.71

$

914,606.44

Sales budget for the financial year 2011-2012

Total Budget: 16971237

Departmen

t

Sale

percentage

(%)

Total budget

2011-2012

Qtr 1 Qtr 2 Qtr 3 Qtr4

20% 24% 26% 30%

Bathroon

fitting 30%

$

5,091,371.10

$

1,018,274.2

2

$

1,221,929.0

6

$

132,756.49

$

152,741,133.0

0

Bedroom

fitting 25%

$

4,242,809.25

$

848,561.85

$

1,018,274.2

2

$

1,103,130.4

1

$

1,272,842.78

Mirrors 15%

$

2,545,685.55

$

509,137.11

$

610,964.53

$

661,878.24

$

763,705.67

decorative

items 10%

$

1,697,123.70

$

339,424.74

$

407,309.69

$

441,252.16

$

509,137.11

lighting

fixtures 20%

$

3,394,247.40

$

678,849.48

$

814,619.38

$

882,504.32

$

1,018,274.22

Total 100% 1697123700 339424740 407309688 441252162 5091371.1

Departmen

t

Sale

percentage

(%)

Total budget

2011-2012

Qtr 1 Qtr 2 Qtr 3 Qtr4

20% 24% 26% 30%

Total 100%

$

16,971,237.00 3394247.4 4073096.88 4412521.62 0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

BSBFIM601

GST Cash Flow Analysis/ Budget

GST Cash Flow Analysis/budget

Cash flow analysis -

GST 2011/12 Qtr 1 ( 20%) Qtr2-(24%) Qtr3 (26%) Qtr4 (30%)

GST collected

$

1,697,123.70

$

339,424.74

$

407,309.69

$

441,252.16

$

509,137.11

Less GST paid

$

1,281,358.30

$

256,271.66

$

307,525.99

$

333,153.16

$

36,407.49

GST payable

$

1,568,988.40

$

83,153.08

$

99,783.70

$

108,099.00

$

472,729.62

Debtors Ageing Budget

Debtors Ageing Budget

Aged debtor

budget

total budget

2011/12

Qtr 1 Qtr2 Qtr 3 Qtr4

20% 24% 26% 30%

Sales

$

16,971,237.00

$

3,394,247.40

$

4,073,096.88 4412521.62 5091371.1

% debtor

balance 20% 20% 20% 20%

Total debtor

$

678,849.48

$

814,619.38

$

882,504.32

$

1,018,274.22

total debtor % 100%

90 days 1%

$

6,788.49

$

8,146.19

$

8,825.04

$

10,182.74

60 days 5%

$

33,942.47

$

40,730.97

$

44,125.22

$

50,913.71

30 days 10%

$

67,884.95

$

81,461.94

$

88,250.43

$

101,827.42

current 84%

$

570,233.56

$

684,280.28

$

741,303.63

$

855,350.34

B: Budget Notes:

BSBFIM601

GST Cash Flow Analysis/ Budget

GST Cash Flow Analysis/budget

Cash flow analysis -

GST 2011/12 Qtr 1 ( 20%) Qtr2-(24%) Qtr3 (26%) Qtr4 (30%)

GST collected

$

1,697,123.70

$

339,424.74

$

407,309.69

$

441,252.16

$

509,137.11

Less GST paid

$

1,281,358.30

$

256,271.66

$

307,525.99

$

333,153.16

$

36,407.49

GST payable

$

1,568,988.40

$

83,153.08

$

99,783.70

$

108,099.00

$

472,729.62

Debtors Ageing Budget

Debtors Ageing Budget

Aged debtor

budget

total budget

2011/12

Qtr 1 Qtr2 Qtr 3 Qtr4

20% 24% 26% 30%

Sales

$

16,971,237.00

$

3,394,247.40

$

4,073,096.88 4412521.62 5091371.1

% debtor

balance 20% 20% 20% 20%

Total debtor

$

678,849.48

$

814,619.38

$

882,504.32

$

1,018,274.22

total debtor % 100%

90 days 1%

$

6,788.49

$

8,146.19

$

8,825.04

$

10,182.74

60 days 5%

$

33,942.47

$

40,730.97

$

44,125.22

$

50,913.71

30 days 10%

$

67,884.95

$

81,461.94

$

88,250.43

$

101,827.42

current 84%

$

570,233.56

$

684,280.28

$

741,303.63

$

855,350.34

B: Budget Notes:

5

BSBFIM601

The notes are inclusive of the following items:

Update the suppositions of spending

The bottlenecks have been reviewed

The focus has been step costing

Available amount of subsidizing

Attain the income conjecture

Attain the spending plan for the office

Attain the demands for the purpose of capital spending

Update the spending framework

Assessment of the financial plan

Issuance of the financial plan

Load the financial plan

Budget Implementation

Generation of revenue and mobilisation

Award of the agreement as mentioned in the budget

Fund release

Physical supervision of the programmes and the project sites

Budget Audit

Physical evaluation in order to ascertain the value for money

Restrict and reduce the effect of the losses and the frauds

Ascertain the violations or the compliance of the financial rules and processes

Receipt of the overview of the expenses and the revenue

BSBFIM601

The notes are inclusive of the following items:

Update the suppositions of spending

The bottlenecks have been reviewed

The focus has been step costing

Available amount of subsidizing

Attain the income conjecture

Attain the spending plan for the office

Attain the demands for the purpose of capital spending

Update the spending framework

Assessment of the financial plan

Issuance of the financial plan

Load the financial plan

Budget Implementation

Generation of revenue and mobilisation

Award of the agreement as mentioned in the budget

Fund release

Physical supervision of the programmes and the project sites

Budget Audit

Physical evaluation in order to ascertain the value for money

Restrict and reduce the effect of the losses and the frauds

Ascertain the violations or the compliance of the financial rules and processes

Receipt of the overview of the expenses and the revenue

6

BSBFIM601

Ministerial monitoring of the procedure

1. Identify the current statutory requirements for tax compliance and list and

calculate the tax liabilities for Houzit Pty Ltd under taxation legislation

The current compliance requirements and the liabilities for the company under the

Corporations Act of 2001 are given as follows:

Income Tax: This is known as the tax that each and every company and entity has to pay on

their net income that is earned within a year.

GST: This is the tax that is paid by the companies, which provides any kind of services and

goods. This tax can be different with respect to the sort of services and goods and certain things

that could be free from this kind of tax.

Company Tax: This tax is paid by the organizations on the total assessable income and the tax

rate is fixed and the percentage is 30% of the overall income.

Superannuation: This is the tax that is paid by the companies on behalf of their employees and

it is computed by the payroll process of the companies.

The tax that is calculated for the company has been given as follows:

Income Tax: $436,878

Payroll Tax: $98,705

Superannuation: $187,020

Fringe Benefit Tax: $28,000

Luxury Car Tax: $12,000

BSBFIM601

Ministerial monitoring of the procedure

1. Identify the current statutory requirements for tax compliance and list and

calculate the tax liabilities for Houzit Pty Ltd under taxation legislation

The current compliance requirements and the liabilities for the company under the

Corporations Act of 2001 are given as follows:

Income Tax: This is known as the tax that each and every company and entity has to pay on

their net income that is earned within a year.

GST: This is the tax that is paid by the companies, which provides any kind of services and

goods. This tax can be different with respect to the sort of services and goods and certain things

that could be free from this kind of tax.

Company Tax: This tax is paid by the organizations on the total assessable income and the tax

rate is fixed and the percentage is 30% of the overall income.

Superannuation: This is the tax that is paid by the companies on behalf of their employees and

it is computed by the payroll process of the companies.

The tax that is calculated for the company has been given as follows:

Income Tax: $436,878

Payroll Tax: $98,705

Superannuation: $187,020

Fringe Benefit Tax: $28,000

Luxury Car Tax: $12,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

BSBFIM601

2. Identify the current compliance requirements and liabilities for this organisation

under the Corporations Act 2001.

In accordance to the Corporations Act 2001, the companies need to maintain the statement of

the financial performance and the financial position statement with them. The records that are

required to be maintained are explained as follows:

Financial Statement

Cash Record

Debtor/ Sales Record

Creditors Record

Superannuation and wages record

3. Review commercially available financial management software to select the most

suitable software for Houzit Pty Ltd.

The assessment of the current software accounting process that is utilised by Houzit Pty leads

to the discovery and development of the software and the hardware that can be implemented by

the companies. The organization in an effective manner exploits the most innovative and the

current software but is limited to the utilisation of only computers and does not use phone or any

other electronic gadgets. The non-existence of the servers and the latest and innovative

technologies may not be supportive in protecting the data and even ensures financial

confidentiality of the organization. The company can even exploit the SAP software but as the

company is small, the incorporation of SAP can be expensive. The other software is the arrow

business software creators that have user experience with dynamic and standardised menu dock

able panels and unified integration to MYOB and Quick Books.

BSBFIM601

2. Identify the current compliance requirements and liabilities for this organisation

under the Corporations Act 2001.

In accordance to the Corporations Act 2001, the companies need to maintain the statement of

the financial performance and the financial position statement with them. The records that are

required to be maintained are explained as follows:

Financial Statement

Cash Record

Debtor/ Sales Record

Creditors Record

Superannuation and wages record

3. Review commercially available financial management software to select the most

suitable software for Houzit Pty Ltd.

The assessment of the current software accounting process that is utilised by Houzit Pty leads

to the discovery and development of the software and the hardware that can be implemented by

the companies. The organization in an effective manner exploits the most innovative and the

current software but is limited to the utilisation of only computers and does not use phone or any

other electronic gadgets. The non-existence of the servers and the latest and innovative

technologies may not be supportive in protecting the data and even ensures financial

confidentiality of the organization. The company can even exploit the SAP software but as the

company is small, the incorporation of SAP can be expensive. The other software is the arrow

business software creators that have user experience with dynamic and standardised menu dock

able panels and unified integration to MYOB and Quick Books.

8

BSBFIM601

These two software are notable towards what they perform. Both the software have similar

weaknesses and strengths. But after the development of the accounts of the business there can be

little disapproval that is seen in one of these products for Houzit. It is seen that Quick Book is not

supported in Macbooks and MYOB on the other permits multiplication inventory and on the

other hand the Quick Book does not do the same. MYOB permits several entities at one time but

Quick Book does not. Therefore, for Houzit Pty Plc MYOB is recommended after assessing the

other kinds of software.

4. Explain how you can apply the following principles of accounting in developing the

budgets required for this task:

Matching principle

Account groups

Time periods

Matching Principles:

A precise and authentic budget can be constructed by utilising the matching principle that

will be helpful in mitigating and reducing the unfavourable variances. An example can be taken

as for the fact that the matching principle helps the company to identify the percentage of the

expenses which are gained from sales.

Account Groups

The account group has a key role to play in order to reduce and mitigate the chaos, which can

be constructed during the framing and computation of the final accounts. By taking assistance of

the account group, the company is able to discover the supportive incomes and the expenses,

which Houzit undertakes during the accounting year.

BSBFIM601

These two software are notable towards what they perform. Both the software have similar

weaknesses and strengths. But after the development of the accounts of the business there can be

little disapproval that is seen in one of these products for Houzit. It is seen that Quick Book is not

supported in Macbooks and MYOB on the other permits multiplication inventory and on the

other hand the Quick Book does not do the same. MYOB permits several entities at one time but

Quick Book does not. Therefore, for Houzit Pty Plc MYOB is recommended after assessing the

other kinds of software.

4. Explain how you can apply the following principles of accounting in developing the

budgets required for this task:

Matching principle

Account groups

Time periods

Matching Principles:

A precise and authentic budget can be constructed by utilising the matching principle that

will be helpful in mitigating and reducing the unfavourable variances. An example can be taken

as for the fact that the matching principle helps the company to identify the percentage of the

expenses which are gained from sales.

Account Groups

The account group has a key role to play in order to reduce and mitigate the chaos, which can

be constructed during the framing and computation of the final accounts. By taking assistance of

the account group, the company is able to discover the supportive incomes and the expenses,

which Houzit undertakes during the accounting year.

9

BSBFIM601

Time Period

The time period is utilised primarily in discovering the debtor payment period, which is

significant and mandatory for the company in order to maintain their extent of liquidity. The

collection time of the debtors primarily helps the maintenance of the budget and addresses the

adequate cash availability during the current accounting year.

5. Explain and discuss the implications of probity when preparing and revising

budgets

Probity is primarily helpful in explaining the implications and consequences of the budget.

They have been explained as follows:

It brings forth transparency and purity and even addresses a clear image and liability of

the overall financial report, which is disclosed by the organization.

It is helpful in eliminating partiality and introducing validity and authenticity in the data

and the records which are constructed by the company.

It is significant to explain the security and the confidentiality of the data which are used

in order to calculate the actual and the overall budget of the company.

6. List the critical dates and initiatives that will require or generate resources for

Houzit Pty Ltd in the next financial cycle

The significant time for the construction of the budget is generally subsequent to the

disclosure of the financial records and statements at the end of the accounting year. The date of

constructing a budget can be helpful to the company in projecting the overall expenditure, which

are paid out during the several quarters of the accounting year.

The dates are as follows:

BSBFIM601

Time Period

The time period is utilised primarily in discovering the debtor payment period, which is

significant and mandatory for the company in order to maintain their extent of liquidity. The

collection time of the debtors primarily helps the maintenance of the budget and addresses the

adequate cash availability during the current accounting year.

5. Explain and discuss the implications of probity when preparing and revising

budgets

Probity is primarily helpful in explaining the implications and consequences of the budget.

They have been explained as follows:

It brings forth transparency and purity and even addresses a clear image and liability of

the overall financial report, which is disclosed by the organization.

It is helpful in eliminating partiality and introducing validity and authenticity in the data

and the records which are constructed by the company.

It is significant to explain the security and the confidentiality of the data which are used

in order to calculate the actual and the overall budget of the company.

6. List the critical dates and initiatives that will require or generate resources for

Houzit Pty Ltd in the next financial cycle

The significant time for the construction of the budget is generally subsequent to the

disclosure of the financial records and statements at the end of the accounting year. The date of

constructing a budget can be helpful to the company in projecting the overall expenditure, which

are paid out during the several quarters of the accounting year.

The dates are as follows:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

BSBFIM601

$100000 taken as loan on December 31st

Advertisement budget increased by $70,000 in the year 2011/12

Rise in the amount of wages and salaries to $172,500 in the year 2011/12

7. List the items you would recommend for inclusion in the budgets for Houzit Pty Ltd

The entire amount of tools and items that can be incorporated in the future and the coming

budget are highlighted as follows:

The incorporation of an accounting process that will be used as a tool for the purpose of

budgeting in order to perform accurately and in a precise manner.

The utilisation of practical and fair valuation mechanism for the projection of the budget

that can be helpful in reducing the variances that are unfavourable in nature.

The improvement and development on the privacy and safety that can be helpful in

reducing the extent of influences that may take place during the computation of the

budget.

Amenities for the employees

Transpiration

Office costs

Water bill

8. List the new or modified internal controls that could improve risk management for

Houzit Pty Ltd including the maintenance of audit trails

The enhanced internal controls that could develop the process of risk management for the

organization are:

The company needs to follow the regulations and the rules

BSBFIM601

$100000 taken as loan on December 31st

Advertisement budget increased by $70,000 in the year 2011/12

Rise in the amount of wages and salaries to $172,500 in the year 2011/12

7. List the items you would recommend for inclusion in the budgets for Houzit Pty Ltd

The entire amount of tools and items that can be incorporated in the future and the coming

budget are highlighted as follows:

The incorporation of an accounting process that will be used as a tool for the purpose of

budgeting in order to perform accurately and in a precise manner.

The utilisation of practical and fair valuation mechanism for the projection of the budget

that can be helpful in reducing the variances that are unfavourable in nature.

The improvement and development on the privacy and safety that can be helpful in

reducing the extent of influences that may take place during the computation of the

budget.

Amenities for the employees

Transpiration

Office costs

Water bill

8. List the new or modified internal controls that could improve risk management for

Houzit Pty Ltd including the maintenance of audit trails

The enhanced internal controls that could develop the process of risk management for the

organization are:

The company needs to follow the regulations and the rules

11

BSBFIM601

The company even needs to incorporate and apply all the processes

The operating hours and the time sheets need to be noted as well.

BSBFIM601

The company even needs to incorporate and apply all the processes

The operating hours and the time sheets need to be noted as well.

12

BSBFIM601

BSBFIM601

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13

BSBFIM601

Bibliography

Akamah, H., Hope, O. K., & Thomas, W. B. (2018). Tax havens and disclosure

aggregation. Journal of International Business Studies, 49(1), 49-69.

Ato.gov.au, (2018). Working out the LCT on an import. [online] Available at:

https://www.ato.gov.au/Business/Luxury-car-tax/Working-out-the-LCT-amount/

Working-out-the-LCT-on-an-import/ [Accessed 13 Mar. 2018].

Barth, M. E., Gomez-Biscarri, J., Kasznik, R., &López-Espinosa, G. (2017). Bank earnings and

regulatory capital management using available for sale securities. Review of Accounting

Studies, 22(4), 1761-1792.

Cazier, R., Rego, S., Tian, X., & Wilson, R. (2015). The impact of increased disclosure

requirements and the standardization of accounting practices on earnings management

through the reserve for income taxes. Review of Accounting Studies, 20(1), 436-469.

Christensen, D. M., Dhaliwal, D. S., Boivie, S., &Graffin, S. D. (2015). Top management

conservatism and corporate risk strategies: Evidence from managers' personal political

orientation and corporate tax avoidance. Strategic Management Journal, 36(12), 1918-

1938.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially responsible

firms pay more taxes?. The accounting review, 91(1), 47-68.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially responsible

firms pay more taxes?. The accounting review, 91(1), 47-68.

BSBFIM601

Bibliography

Akamah, H., Hope, O. K., & Thomas, W. B. (2018). Tax havens and disclosure

aggregation. Journal of International Business Studies, 49(1), 49-69.

Ato.gov.au, (2018). Working out the LCT on an import. [online] Available at:

https://www.ato.gov.au/Business/Luxury-car-tax/Working-out-the-LCT-amount/

Working-out-the-LCT-on-an-import/ [Accessed 13 Mar. 2018].

Barth, M. E., Gomez-Biscarri, J., Kasznik, R., &López-Espinosa, G. (2017). Bank earnings and

regulatory capital management using available for sale securities. Review of Accounting

Studies, 22(4), 1761-1792.

Cazier, R., Rego, S., Tian, X., & Wilson, R. (2015). The impact of increased disclosure

requirements and the standardization of accounting practices on earnings management

through the reserve for income taxes. Review of Accounting Studies, 20(1), 436-469.

Christensen, D. M., Dhaliwal, D. S., Boivie, S., &Graffin, S. D. (2015). Top management

conservatism and corporate risk strategies: Evidence from managers' personal political

orientation and corporate tax avoidance. Strategic Management Journal, 36(12), 1918-

1938.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially responsible

firms pay more taxes?. The accounting review, 91(1), 47-68.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially responsible

firms pay more taxes?. The accounting review, 91(1), 47-68.

14

BSBFIM601

DeAngelo, H., &Stulz, R. M. (2015). Liquid-claim production, risk management, and bank

capital structure: Why high leverage is optimal for banks. Journal of Financial

Economics, 116(2), 219-236.

Donohoe, M. P. (2015). The economic effects of financial derivatives on corporate tax

avoidance. Journal of Accounting and Economics, 59(1), 1-24.

Dyreng, S. D., &Markle, K. S. (2016). The effect of financial constraints on income shifting by

US multinationals. The Accounting Review, 91(6), 1601-1627.

Edwards, A., Schwab, C., &Shevlin, T. (2015). Financial constraints and cash tax savings. The

Accounting Review, 91(3), 859-881.

Gallemore, J., &Labro, E. (2015). The importance of the internal information environment for

tax avoidance. Journal of Accounting and Economics, 60(1), 149-167.

Goh, B. W., Lee, J., Lim, C. Y., &Shevlin, T. (2016). The effect of corporate tax avoidance on

the cost of equity. The Accounting Review, 91(6), 1647-1670.

Hanlon, M., Hoopes, J. L., & Shroff, N. (2014). The effect of tax authority monitoring and

enforcement on financial reporting quality. The Journal of the American Taxation

Association, 36(2), 137-170.

Kothari, S. P., Mizik, N., &Roychowdhury, S. (2015). Managing for the moment: The role of

earnings management via real activities versus accruals in SEO valuation. The

Accounting Review, 91(2), 559-586.

Muller, A., &Kolk, A. (2015). Responsible tax as corporate social responsibility: the case of

multinational enterprises and effective tax in India. Business & Society, 54(4), 435-463.

BSBFIM601

DeAngelo, H., &Stulz, R. M. (2015). Liquid-claim production, risk management, and bank

capital structure: Why high leverage is optimal for banks. Journal of Financial

Economics, 116(2), 219-236.

Donohoe, M. P. (2015). The economic effects of financial derivatives on corporate tax

avoidance. Journal of Accounting and Economics, 59(1), 1-24.

Dyreng, S. D., &Markle, K. S. (2016). The effect of financial constraints on income shifting by

US multinationals. The Accounting Review, 91(6), 1601-1627.

Edwards, A., Schwab, C., &Shevlin, T. (2015). Financial constraints and cash tax savings. The

Accounting Review, 91(3), 859-881.

Gallemore, J., &Labro, E. (2015). The importance of the internal information environment for

tax avoidance. Journal of Accounting and Economics, 60(1), 149-167.

Goh, B. W., Lee, J., Lim, C. Y., &Shevlin, T. (2016). The effect of corporate tax avoidance on

the cost of equity. The Accounting Review, 91(6), 1647-1670.

Hanlon, M., Hoopes, J. L., & Shroff, N. (2014). The effect of tax authority monitoring and

enforcement on financial reporting quality. The Journal of the American Taxation

Association, 36(2), 137-170.

Kothari, S. P., Mizik, N., &Roychowdhury, S. (2015). Managing for the moment: The role of

earnings management via real activities versus accruals in SEO valuation. The

Accounting Review, 91(2), 559-586.

Muller, A., &Kolk, A. (2015). Responsible tax as corporate social responsibility: the case of

multinational enterprises and effective tax in India. Business & Society, 54(4), 435-463.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.