Business Entity in Australia

Added on 2022-09-15

12 Pages2103 Words17 Views

Running head: ANALYSIS REPORT

ANALYSIS REPORT

Name of the Student;

Name of the University:

Author Note:

ANALYSIS REPORT

Name of the Student;

Name of the University:

Author Note:

ANALYSIS REPORT

1

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................4

Conclusion..................................................................................................................................8

References..................................................................................................................................9

1

Table of Contents

Introduction................................................................................................................................2

Discussion..................................................................................................................................4

Conclusion..................................................................................................................................8

References..................................................................................................................................9

ANALYSIS REPORT

2

Introduction

AGL Energy Ltd is a public listed business entity in Australia. The business operates

in energy and utility sector and has its headquarters at Sydney and New South Wales. The

organization work with various products and services such as producing wind power, natural

gas, coal steam gas and many other products related to generation of energy. AGL primary

operations are related to manufacturing and dispensing of gas and energy for both residential

and business purpose. The company offers certain other services related to energy generation

and distribution of natural gas. Primary investment of organization are done in gas and

electricity sectors. AGL is leading private owner and inventor of renewable sources of assets

related to energy in Australia (Agl.com.au, 2020). The company has a leading position in the

ASX listed investor in the field of renewable source of energy. If Australia electricity

generation portfolio is taken into consideration, then AGL occupies the largest position. The

company provides a secure, affordable, and sustainable source of energy to the people of

Australia. Approximately 20% of the energy generation portfolio is covered by AGL within

Australia’s National Electricity Market. The business entity deals in gas, electricity wholesale

market where customers belong to residential, large and small work houses, and many other

wholesale customers. The corporate governance structure of business is extremely impressive

as it consists of policies and regulations that exhibit a high standard of the company and even

the framework takes into account the emerging trends related to corporate governance to

meet stakeholder’s expectations. The company has a clear viewpoint that appropriate and

strong corporate governance will help the company to sustain for an extended period in the

competitive market.

2

Introduction

AGL Energy Ltd is a public listed business entity in Australia. The business operates

in energy and utility sector and has its headquarters at Sydney and New South Wales. The

organization work with various products and services such as producing wind power, natural

gas, coal steam gas and many other products related to generation of energy. AGL primary

operations are related to manufacturing and dispensing of gas and energy for both residential

and business purpose. The company offers certain other services related to energy generation

and distribution of natural gas. Primary investment of organization are done in gas and

electricity sectors. AGL is leading private owner and inventor of renewable sources of assets

related to energy in Australia (Agl.com.au, 2020). The company has a leading position in the

ASX listed investor in the field of renewable source of energy. If Australia electricity

generation portfolio is taken into consideration, then AGL occupies the largest position. The

company provides a secure, affordable, and sustainable source of energy to the people of

Australia. Approximately 20% of the energy generation portfolio is covered by AGL within

Australia’s National Electricity Market. The business entity deals in gas, electricity wholesale

market where customers belong to residential, large and small work houses, and many other

wholesale customers. The corporate governance structure of business is extremely impressive

as it consists of policies and regulations that exhibit a high standard of the company and even

the framework takes into account the emerging trends related to corporate governance to

meet stakeholder’s expectations. The company has a clear viewpoint that appropriate and

strong corporate governance will help the company to sustain for an extended period in the

competitive market.

ANALYSIS REPORT

3

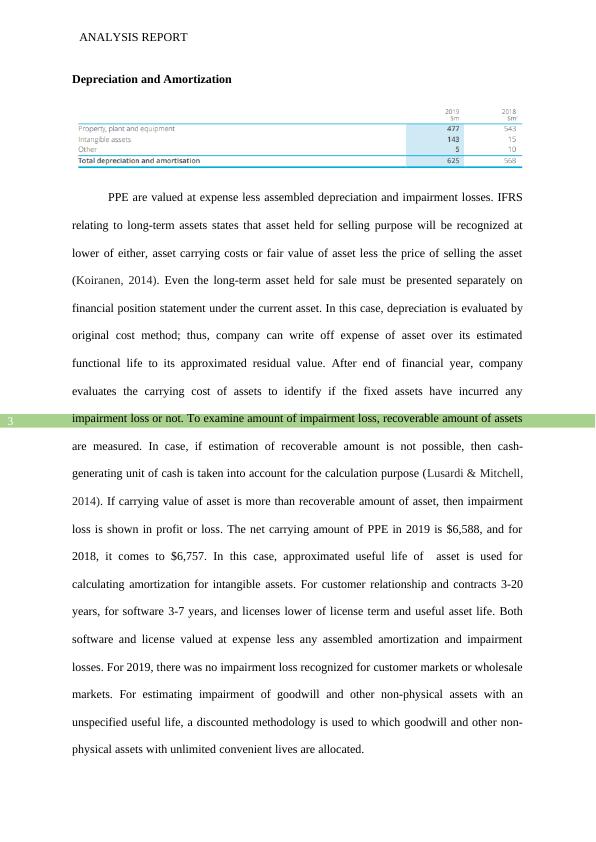

Depreciation and Amortization

PPE are valued at expense less assembled depreciation and impairment losses. IFRS

relating to long-term assets states that asset held for selling purpose will be recognized at

lower of either, asset carrying costs or fair value of asset less the price of selling the asset

(Koiranen, 2014). Even the long-term asset held for sale must be presented separately on

financial position statement under the current asset. In this case, depreciation is evaluated by

original cost method; thus, company can write off expense of asset over its estimated

functional life to its approximated residual value. After end of financial year, company

evaluates the carrying cost of assets to identify if the fixed assets have incurred any

impairment loss or not. To examine amount of impairment loss, recoverable amount of assets

are measured. In case, if estimation of recoverable amount is not possible, then cash-

generating unit of cash is taken into account for the calculation purpose (Lusardi & Mitchell,

2014). If carrying value of asset is more than recoverable amount of asset, then impairment

loss is shown in profit or loss. The net carrying amount of PPE in 2019 is $6,588, and for

2018, it comes to $6,757. In this case, approximated useful life of asset is used for

calculating amortization for intangible assets. For customer relationship and contracts 3-20

years, for software 3-7 years, and licenses lower of license term and useful asset life. Both

software and license valued at expense less any assembled amortization and impairment

losses. For 2019, there was no impairment loss recognized for customer markets or wholesale

markets. For estimating impairment of goodwill and other non-physical assets with an

unspecified useful life, a discounted methodology is used to which goodwill and other non-

physical assets with unlimited convenient lives are allocated.

3

Depreciation and Amortization

PPE are valued at expense less assembled depreciation and impairment losses. IFRS

relating to long-term assets states that asset held for selling purpose will be recognized at

lower of either, asset carrying costs or fair value of asset less the price of selling the asset

(Koiranen, 2014). Even the long-term asset held for sale must be presented separately on

financial position statement under the current asset. In this case, depreciation is evaluated by

original cost method; thus, company can write off expense of asset over its estimated

functional life to its approximated residual value. After end of financial year, company

evaluates the carrying cost of assets to identify if the fixed assets have incurred any

impairment loss or not. To examine amount of impairment loss, recoverable amount of assets

are measured. In case, if estimation of recoverable amount is not possible, then cash-

generating unit of cash is taken into account for the calculation purpose (Lusardi & Mitchell,

2014). If carrying value of asset is more than recoverable amount of asset, then impairment

loss is shown in profit or loss. The net carrying amount of PPE in 2019 is $6,588, and for

2018, it comes to $6,757. In this case, approximated useful life of asset is used for

calculating amortization for intangible assets. For customer relationship and contracts 3-20

years, for software 3-7 years, and licenses lower of license term and useful asset life. Both

software and license valued at expense less any assembled amortization and impairment

losses. For 2019, there was no impairment loss recognized for customer markets or wholesale

markets. For estimating impairment of goodwill and other non-physical assets with an

unspecified useful life, a discounted methodology is used to which goodwill and other non-

physical assets with unlimited convenient lives are allocated.

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Pacific-Basin Finance Journallg...

|12

|2451

|19

Accounting Policies and Estimates on PPElg...

|6

|848

|455

Accounting and Financial Managementlg...

|6

|1244

|77

Concept of Impairment Assignment PDFlg...

|7

|1571

|53

Source of Finance Assignment 2022lg...

|13

|1929

|33

Corporate Accounting Assignment | AGLlg...

|11

|2252

|404