Risk Management of Securities: CML, SML, and CAPM Models

VerifiedAdded on 2022/08/27

|12

|2818

|15

Report

AI Summary

This report provides a comprehensive analysis of risk management strategies in securities investments, focusing on the Capital Market Line (CML) and Security Market Line (SML) approaches, alongside the Capital Asset Pricing Model (CAPM). The report explores the concept of investment in securities, emphasizing the inherent risks and the role of financial models in predicting risk and return relationships. It delves into the CML approach, illustrating how it helps investors achieve optimal returns based on their risk tolerance, and discusses the minimum variance portfolio and its significance in determining the efficient frontier. The report further examines the CAPM model, its underlying assumptions, and its advantages over other models, particularly its use of beta to measure systematic risk. The SML approach is then presented as a visual representation of CAPM, highlighting its role in evaluating undervalued and overvalued stocks. The importance of beta in assessing stock volatility and market sensitivity is also discussed. The report concludes with recommendations for investors, emphasizing the need for diversification and the use of CAPM and CML models to manage risk effectively. It highlights the importance of understanding both diversifiable and non-diversifiable risks to make informed investment decisions.

Risk management models of finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

RISK MANAGEMENT OF SECURITIES

Table of Contents

Introduction................................................................................................................................2

Concept of investment in securities...........................................................................................2

Analysis of CML approach........................................................................................................2

Concept of minimum variance portfolio................................................................................4

Importance of minimum variance portfolio...........................................................................4

Basic assumptions for CAPM model.........................................................................................5

Accuracy of CAPM model in the comparison of other models.............................................6

Concept of SML Approach....................................................................................................6

Special features of CAPM model...........................................................................................7

Importance of Beta.................................................................................................................8

Difference between CML and SML Lines.................................................................................9

Conclusion................................................................................................................................10

Recommendations for the investors.........................................................................................10

References................................................................................................................................12

RISK MANAGEMENT OF SECURITIES

Table of Contents

Introduction................................................................................................................................2

Concept of investment in securities...........................................................................................2

Analysis of CML approach........................................................................................................2

Concept of minimum variance portfolio................................................................................4

Importance of minimum variance portfolio...........................................................................4

Basic assumptions for CAPM model.........................................................................................5

Accuracy of CAPM model in the comparison of other models.............................................6

Concept of SML Approach....................................................................................................6

Special features of CAPM model...........................................................................................7

Importance of Beta.................................................................................................................8

Difference between CML and SML Lines.................................................................................9

Conclusion................................................................................................................................10

Recommendations for the investors.........................................................................................10

References................................................................................................................................12

2

RISK MANAGEMENT OF SECURITIES

Introduction

In this report, an analysis will be done over the CML and SML approach of portfolios. These

are related to the risk and return measures for any portfolio related to investment. The various

characteristics of CAPM will also be discussed in order to understand the relationship

between risk free assets and expected return. The focus will be given over the difference

between SML and CML approach. The importance of efficient frontier and Beta is also

analysed in this report. The focus is provided on the importance of the various models and

approaches of the investments by getting maximum return on portfolios. In the end,

recommendations are given on the bases of the analysis of different approaches of investment

management for protecting the investors from high level of risk.

Concept of investment in securities

The investment in securities is seems to be risky for investors because no tool can exactly

predict the return of the security with a certain level of risk. Different models and approaches

of finance can provide an idea about the risk and return relationship for individual stocks or

portfolios. That is why most of the investors are interested in knowing the expected return

within a certain amount of risk. CAPM model, SML and CML approaches offers the

guidelines to measure risk and return relationship of different securities (VI OSAYI, 2019).

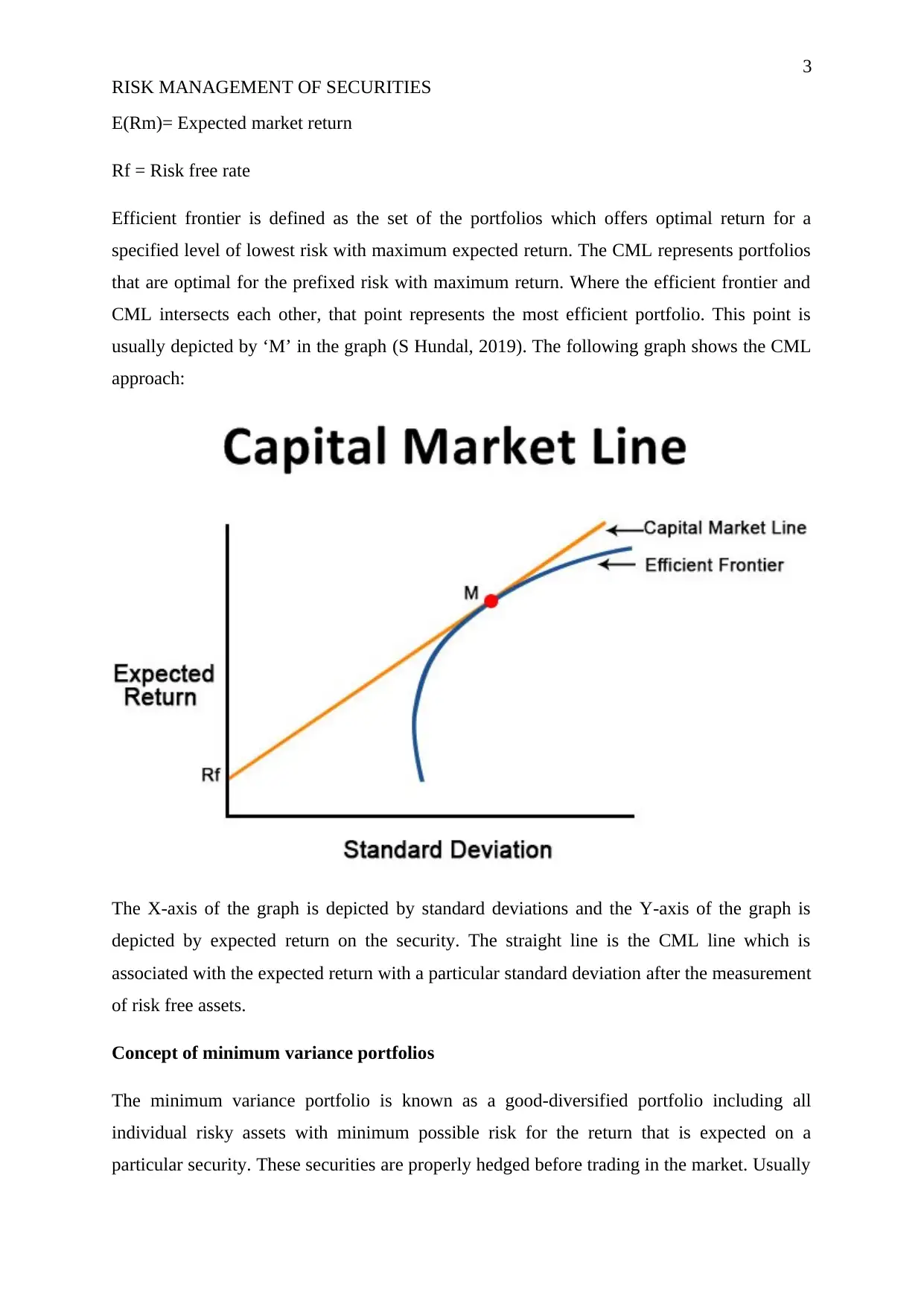

Analysis of CML approach

Capital market line is depicted by a graph with respect to expected return and risk of a

portfolio which is used by investors to obtain best return. The CML is calculated with the

help of market return on portfolio and risk free assets. In this approach risk is measured by

standard deviation.

The equation of CML is written below:

E(Rc) = Rf + SDc {E(Rm)- Rf/SDm}

E (Rc)= Expected return on portfolio C

SDc = Standard deviation for portfolio C

SDm= S.D. for market return

RISK MANAGEMENT OF SECURITIES

Introduction

In this report, an analysis will be done over the CML and SML approach of portfolios. These

are related to the risk and return measures for any portfolio related to investment. The various

characteristics of CAPM will also be discussed in order to understand the relationship

between risk free assets and expected return. The focus will be given over the difference

between SML and CML approach. The importance of efficient frontier and Beta is also

analysed in this report. The focus is provided on the importance of the various models and

approaches of the investments by getting maximum return on portfolios. In the end,

recommendations are given on the bases of the analysis of different approaches of investment

management for protecting the investors from high level of risk.

Concept of investment in securities

The investment in securities is seems to be risky for investors because no tool can exactly

predict the return of the security with a certain level of risk. Different models and approaches

of finance can provide an idea about the risk and return relationship for individual stocks or

portfolios. That is why most of the investors are interested in knowing the expected return

within a certain amount of risk. CAPM model, SML and CML approaches offers the

guidelines to measure risk and return relationship of different securities (VI OSAYI, 2019).

Analysis of CML approach

Capital market line is depicted by a graph with respect to expected return and risk of a

portfolio which is used by investors to obtain best return. The CML is calculated with the

help of market return on portfolio and risk free assets. In this approach risk is measured by

standard deviation.

The equation of CML is written below:

E(Rc) = Rf + SDc {E(Rm)- Rf/SDm}

E (Rc)= Expected return on portfolio C

SDc = Standard deviation for portfolio C

SDm= S.D. for market return

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

RISK MANAGEMENT OF SECURITIES

E(Rm)= Expected market return

Rf = Risk free rate

Efficient frontier is defined as the set of the portfolios which offers optimal return for a

specified level of lowest risk with maximum expected return. The CML represents portfolios

that are optimal for the prefixed risk with maximum return. Where the efficient frontier and

CML intersects each other, that point represents the most efficient portfolio. This point is

usually depicted by ‘M’ in the graph (S Hundal, 2019). The following graph shows the CML

approach:

The X-axis of the graph is depicted by standard deviations and the Y-axis of the graph is

depicted by expected return on the security. The straight line is the CML line which is

associated with the expected return with a particular standard deviation after the measurement

of risk free assets.

Concept of minimum variance portfolios

The minimum variance portfolio is known as a good-diversified portfolio including all

individual risky assets with minimum possible risk for the return that is expected on a

particular security. These securities are properly hedged before trading in the market. Usually

RISK MANAGEMENT OF SECURITIES

E(Rm)= Expected market return

Rf = Risk free rate

Efficient frontier is defined as the set of the portfolios which offers optimal return for a

specified level of lowest risk with maximum expected return. The CML represents portfolios

that are optimal for the prefixed risk with maximum return. Where the efficient frontier and

CML intersects each other, that point represents the most efficient portfolio. This point is

usually depicted by ‘M’ in the graph (S Hundal, 2019). The following graph shows the CML

approach:

The X-axis of the graph is depicted by standard deviations and the Y-axis of the graph is

depicted by expected return on the security. The straight line is the CML line which is

associated with the expected return with a particular standard deviation after the measurement

of risk free assets.

Concept of minimum variance portfolios

The minimum variance portfolio is known as a good-diversified portfolio including all

individual risky assets with minimum possible risk for the return that is expected on a

particular security. These securities are properly hedged before trading in the market. Usually

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

RISK MANAGEMENT OF SECURITIES

the investors are interested in knowing the expected return with minimum risk on their

minimum variance portfolios. CML approach focused on providing the return on the well-

diversified portfolios of the investors (TT Cai, 2019).

Importance of portfolios with minimum variance

The portfolios of minimum variance determine the minimum level of efficient frontier. It

means below the minimum variance related portfolio, all the portfolios are inefficient and that

is why no investor wants to invest in the portfolio which exists below the portfolios of

minimum variance. So the minimum variance of portfolio provides a guideline to protect the

investors from facing loss by investing in inefficient portfolios. This tool is very helpful for

the investors by protecting their portfolio against the high level of diversifiable risk.

However, non-diversifiable risk can-not be eliminated by using any method. It has to be bear

by the investors (O Tilfani, 2020).

Basic assumptions for CAPM model

CAPM model is based upon certain assumptions on the market conditions and the nature of

the investors on which the CAPM model calculated the expected return. Basic assumptions

are as follows:

(a) No taxation and no transaction fees are exist inside the market.

(b) All investors are risk averse.

(c) All investors have similar expectations with risk and return.

(d) All investors have homogeneous time horizon for buying the assets at a particular

time.

(e) All the assets are marketable and divisible.

(f) Total availability of assets.

(g) Markets are ideal.

(h) All investors have equal access of information.

(i) There are no restrictions in borrowing and lending of amount.

(j) Beta co-efficient is the only parameter to measure the risk.

(k) All the assets are in liquid form (JY Campbell, 2018).

(l) All the markets are in equilibrium position (S Hundal, 2019).

RISK MANAGEMENT OF SECURITIES

the investors are interested in knowing the expected return with minimum risk on their

minimum variance portfolios. CML approach focused on providing the return on the well-

diversified portfolios of the investors (TT Cai, 2019).

Importance of portfolios with minimum variance

The portfolios of minimum variance determine the minimum level of efficient frontier. It

means below the minimum variance related portfolio, all the portfolios are inefficient and that

is why no investor wants to invest in the portfolio which exists below the portfolios of

minimum variance. So the minimum variance of portfolio provides a guideline to protect the

investors from facing loss by investing in inefficient portfolios. This tool is very helpful for

the investors by protecting their portfolio against the high level of diversifiable risk.

However, non-diversifiable risk can-not be eliminated by using any method. It has to be bear

by the investors (O Tilfani, 2020).

Basic assumptions for CAPM model

CAPM model is based upon certain assumptions on the market conditions and the nature of

the investors on which the CAPM model calculated the expected return. Basic assumptions

are as follows:

(a) No taxation and no transaction fees are exist inside the market.

(b) All investors are risk averse.

(c) All investors have similar expectations with risk and return.

(d) All investors have homogeneous time horizon for buying the assets at a particular

time.

(e) All the assets are marketable and divisible.

(f) Total availability of assets.

(g) Markets are ideal.

(h) All investors have equal access of information.

(i) There are no restrictions in borrowing and lending of amount.

(j) Beta co-efficient is the only parameter to measure the risk.

(k) All the assets are in liquid form (JY Campbell, 2018).

(l) All the markets are in equilibrium position (S Hundal, 2019).

5

RISK MANAGEMENT OF SECURITIES

Accuracy of CAPM model in the comparison of other models

CAPM model is widely used by investor in comparison of other models because of its special

and unique features. The CAPM considers systematic risk into account with the help of beta,

which is mostly avoided by other models while calculating required rate of return. It also

considers financial risk variability into the calculation while the other models do not focus on

variability of risk with respect to time (L Qoqiauri, 2019). CAPM also based on the time

value of money concept while measuring the required rate of return which makes the model

more accurate and competent in comparison of other models like WACC model (S Hundal,

2019).

However the CAPM model is criticised due to the unrealistic assumptions. Like existence of

homogeneous market expectations involved in the assumptions of CAPM whereas it is very

unrealistic to have homogeneous market expectations. Still CAPM is widely used for its

accurate calculating features with the involvement of various risks (S Hundal, 2019).

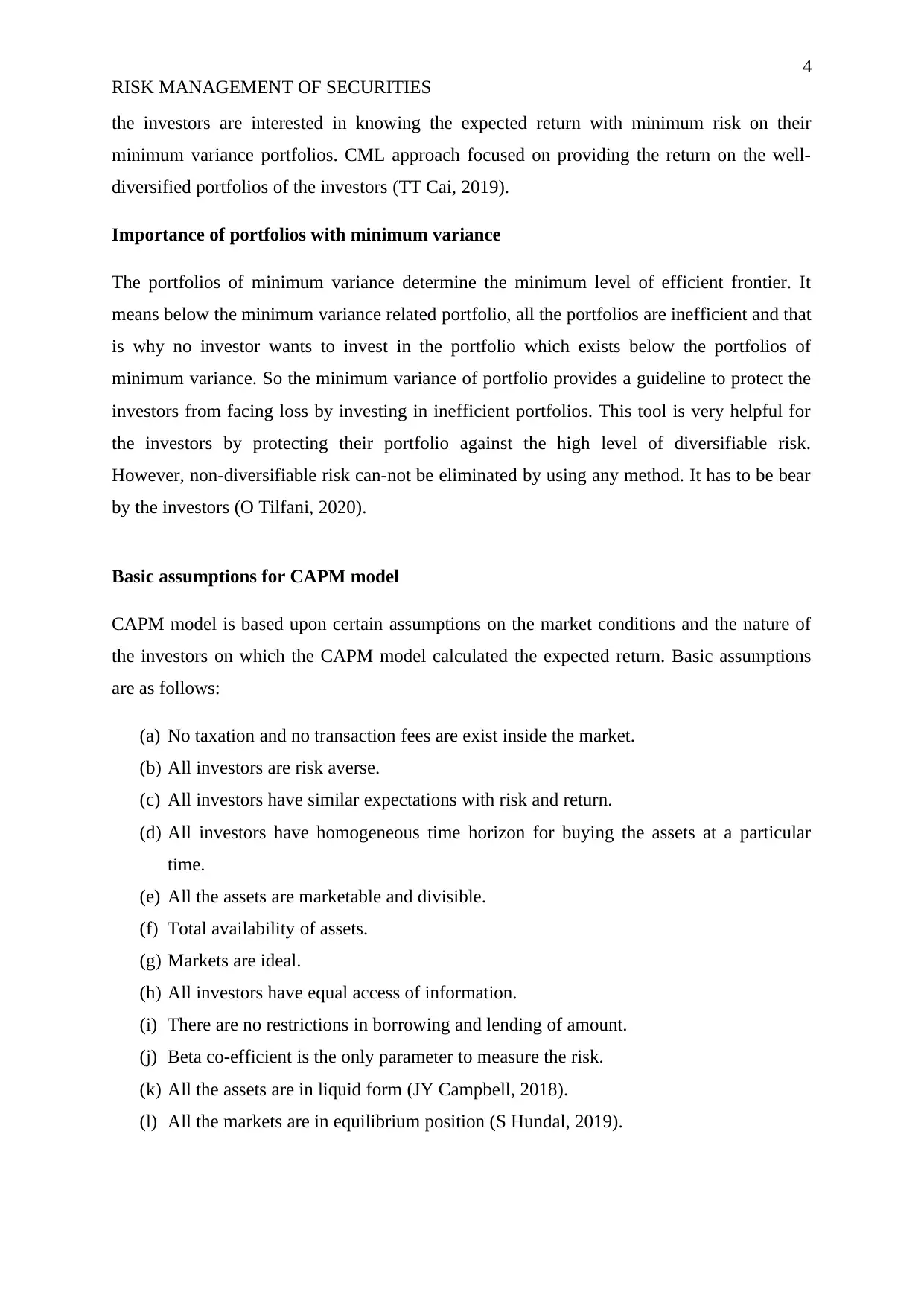

Concept of SML Approach

The SML approach or equation is a pictorial representation of the CAPM model, which

considers different level of risk with marketable securities. The X-axis on the chart represent

the risk factors associated with the securities in terms of beta whereas the Y-axis of the chart

represent the expected return on the security on a particular time with respect to certain risk.

It also takes undervalued and overvalued stock into consideration while measuring the risk

and return associated with any security (mojo, 2020).

RISK MANAGEMENT OF SECURITIES

Accuracy of CAPM model in the comparison of other models

CAPM model is widely used by investor in comparison of other models because of its special

and unique features. The CAPM considers systematic risk into account with the help of beta,

which is mostly avoided by other models while calculating required rate of return. It also

considers financial risk variability into the calculation while the other models do not focus on

variability of risk with respect to time (L Qoqiauri, 2019). CAPM also based on the time

value of money concept while measuring the required rate of return which makes the model

more accurate and competent in comparison of other models like WACC model (S Hundal,

2019).

However the CAPM model is criticised due to the unrealistic assumptions. Like existence of

homogeneous market expectations involved in the assumptions of CAPM whereas it is very

unrealistic to have homogeneous market expectations. Still CAPM is widely used for its

accurate calculating features with the involvement of various risks (S Hundal, 2019).

Concept of SML Approach

The SML approach or equation is a pictorial representation of the CAPM model, which

considers different level of risk with marketable securities. The X-axis on the chart represent

the risk factors associated with the securities in terms of beta whereas the Y-axis of the chart

represent the expected return on the security on a particular time with respect to certain risk.

It also takes undervalued and overvalued stock into consideration while measuring the risk

and return associated with any security (mojo, 2020).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

RISK MANAGEMENT OF SECURITIES

Special features of CAPM model

CAPM is one of the famous models of finance which is highly used by investors and known

to be very trustworthy model for investors. The model of Capital Asset Pricing (CAPM)

establishes the relationship between expected return and systematic risk for a particular asset

or stock. CAPM is majorly used for calculating expected returns for a particular risk (DR

Mishra, 2019).

Expected return = Risk Free Rate + [Beta * Market Return Premium]

It is depicted by the above stated equation, which calculates the future return on a given

security where the systematic risk is measured by beta coefficient (DR Mishra, 2019).

Here the Market Return Premium is calculated by the following formula:

Market Return Premium = E(Rm) - Rf

Beta co-efficient is a parameter that is used to measure the sensitivity of any stock. It is used

to measure the stock systematic risk which is an undiversified risk in the current market

scenario (C. Edward Chang, 2019). The formula of measuring beta is as follows:

Beta = Covariance of market return with stock return divided by variance of market

return.

RISK MANAGEMENT OF SECURITIES

Special features of CAPM model

CAPM is one of the famous models of finance which is highly used by investors and known

to be very trustworthy model for investors. The model of Capital Asset Pricing (CAPM)

establishes the relationship between expected return and systematic risk for a particular asset

or stock. CAPM is majorly used for calculating expected returns for a particular risk (DR

Mishra, 2019).

Expected return = Risk Free Rate + [Beta * Market Return Premium]

It is depicted by the above stated equation, which calculates the future return on a given

security where the systematic risk is measured by beta coefficient (DR Mishra, 2019).

Here the Market Return Premium is calculated by the following formula:

Market Return Premium = E(Rm) - Rf

Beta co-efficient is a parameter that is used to measure the sensitivity of any stock. It is used

to measure the stock systematic risk which is an undiversified risk in the current market

scenario (C. Edward Chang, 2019). The formula of measuring beta is as follows:

Beta = Covariance of market return with stock return divided by variance of market

return.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

RISK MANAGEMENT OF SECURITIES

Importance of Beta

Beta is very important parameter in investment management because it measures the risk of

an investment which cannot be diversified. Beta is used to measures the sensitivity of

systematic market risk which cannot be diversified by making changes in the portfolio. With

the help of Beta, investors may have an idea about the volatility in the market. Beta defines

the movement in securities returns with respect to the fluctuations in the market (Sunderman,

2019). However the Beta does not consider unsystematic risk into consideration but still it is

very helpful for the investors by having the idea about the volatility in the return of stock

related to fluctuations in the market (Glabadanidis, 2019).

Use of beta by investors:

(a) If any stock has Beta with exact numeric value 1, it represent that the stock is highly

co-related to the market fluctuations. It associated the same amount of systematic risk

with respect to the volatility of market (Sunderman, 2019).

(b) If any stock has Beta with numeric value less than 1, it represent that the stock is less

volatile with the fluctuations in the market. It shows that the stock has a very less

changes in its value with respect to changes in the systematic risk of market.

(c) If any stock has Beta with numeric value greater than 1, it represents the high

volatility with respect to the changes in the systematic risk of market. It shows that the

stock is very sensitive towards the fluctuations in the market (C. Edward Chang,

2019).

However, decision of the investor is very much depends upon the risk taking ability of

investors but still Beta represents a level of risk which is associated with any individual

asset or stock (C. Edward Chang, 2019).

The major differences between the concepts of CML and SML Lines

The full form of term CML is Capital market line whereas the SML presents the concept of

Security market line. The major difference between CML and SML is how the risk factor is

measured. Although, both of the approaches are used to measure the relationship between

risk and return but the difference is only in the process of calculating the risk factor in both

the approaches. Standard deviation is calculated to measure associated risk factors in CML

RISK MANAGEMENT OF SECURITIES

Importance of Beta

Beta is very important parameter in investment management because it measures the risk of

an investment which cannot be diversified. Beta is used to measures the sensitivity of

systematic market risk which cannot be diversified by making changes in the portfolio. With

the help of Beta, investors may have an idea about the volatility in the market. Beta defines

the movement in securities returns with respect to the fluctuations in the market (Sunderman,

2019). However the Beta does not consider unsystematic risk into consideration but still it is

very helpful for the investors by having the idea about the volatility in the return of stock

related to fluctuations in the market (Glabadanidis, 2019).

Use of beta by investors:

(a) If any stock has Beta with exact numeric value 1, it represent that the stock is highly

co-related to the market fluctuations. It associated the same amount of systematic risk

with respect to the volatility of market (Sunderman, 2019).

(b) If any stock has Beta with numeric value less than 1, it represent that the stock is less

volatile with the fluctuations in the market. It shows that the stock has a very less

changes in its value with respect to changes in the systematic risk of market.

(c) If any stock has Beta with numeric value greater than 1, it represents the high

volatility with respect to the changes in the systematic risk of market. It shows that the

stock is very sensitive towards the fluctuations in the market (C. Edward Chang,

2019).

However, decision of the investor is very much depends upon the risk taking ability of

investors but still Beta represents a level of risk which is associated with any individual

asset or stock (C. Edward Chang, 2019).

The major differences between the concepts of CML and SML Lines

The full form of term CML is Capital market line whereas the SML presents the concept of

Security market line. The major difference between CML and SML is how the risk factor is

measured. Although, both of the approaches are used to measure the relationship between

risk and return but the difference is only in the process of calculating the risk factor in both

the approaches. Standard deviation is calculated to measure associated risk factors in CML

8

RISK MANAGEMENT OF SECURITIES

approach whereas beta co-efficient is used to measure the risk factor in SML approach

(between.net, 2020).

The graph which represent only Capital market line is only focuses over efficient portfolios

whereas the graph of SML defines both the efficient and non-efficient portfolios. The assets

which are risk free and return on the market portfolio are determined by the approach of

CML whereas security factors of all types are determined by SML approach. SML is

basically focuses over the risk and return relationship of individual stocks whereas CML

approach is focuses over the risk and relationship of return on the whole portfolio of assets, it

does not consider return on single or individual stock. Although, the major objectives of both

the approaches are same, both of the approaches used to measure return and risk on stocks

but the method of measuring is different in the approaches (between.net, 2020).

Conclusion

On the bases of above analysis of CML approach and CAPM model with SML approach with

Beta measurement, it can be said that CAPM model is very useful for the investors because it

provides guidelines to invest in profitable assets by protecting the investors with huge risk.

Beta measurement also guides the investors by providing the status of security with related to

its volatility with market fluctuations.

Recommendations for the investors

Investment management is a very crucial field because no model can predict exact return

related to the securities because of the presence of a large amount of non-diversifiable risk

present inside the market (O Wagdi, 2016). That is why an investor has to hedge its portfolio

properly by knowing the maximum risk in the assets in which he is going to invest. Investors

should take the help of CAPM model and CML approach by making sure about the

maximum return associated with minimum risk for the portfolio of assets (EG De Giorgi,

2019).

In portfolio management risk and return trade- off is very difficult and uncertain because of

the extremely volatility of the market but by taking the help of Beta measurement an investor

can be ensure about the sensitivity of the stock with respect to fluctuations in the market

(Kittipat Laisasikorn, 2019). There is always systematic and unsystematic risks are associated

RISK MANAGEMENT OF SECURITIES

approach whereas beta co-efficient is used to measure the risk factor in SML approach

(between.net, 2020).

The graph which represent only Capital market line is only focuses over efficient portfolios

whereas the graph of SML defines both the efficient and non-efficient portfolios. The assets

which are risk free and return on the market portfolio are determined by the approach of

CML whereas security factors of all types are determined by SML approach. SML is

basically focuses over the risk and return relationship of individual stocks whereas CML

approach is focuses over the risk and relationship of return on the whole portfolio of assets, it

does not consider return on single or individual stock. Although, the major objectives of both

the approaches are same, both of the approaches used to measure return and risk on stocks

but the method of measuring is different in the approaches (between.net, 2020).

Conclusion

On the bases of above analysis of CML approach and CAPM model with SML approach with

Beta measurement, it can be said that CAPM model is very useful for the investors because it

provides guidelines to invest in profitable assets by protecting the investors with huge risk.

Beta measurement also guides the investors by providing the status of security with related to

its volatility with market fluctuations.

Recommendations for the investors

Investment management is a very crucial field because no model can predict exact return

related to the securities because of the presence of a large amount of non-diversifiable risk

present inside the market (O Wagdi, 2016). That is why an investor has to hedge its portfolio

properly by knowing the maximum risk in the assets in which he is going to invest. Investors

should take the help of CAPM model and CML approach by making sure about the

maximum return associated with minimum risk for the portfolio of assets (EG De Giorgi,

2019).

In portfolio management risk and return trade- off is very difficult and uncertain because of

the extremely volatility of the market but by taking the help of Beta measurement an investor

can be ensure about the sensitivity of the stock with respect to fluctuations in the market

(Kittipat Laisasikorn, 2019). There is always systematic and unsystematic risks are associated

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

RISK MANAGEMENT OF SECURITIES

with the securities. However, systematic risk is a non-diversifiable risk because it is linked

with the fluctuations in the market whereas unsystematic risk can be diversifies by adding or

reducing particular securities from the portfolios. That is why it is very important for the

investors by using hedging tools for getting maximum profit from their portfolios (finweek,

2019).

RISK MANAGEMENT OF SECURITIES

with the securities. However, systematic risk is a non-diversifiable risk because it is linked

with the fluctuations in the market whereas unsystematic risk can be diversifies by adding or

reducing particular securities from the portfolios. That is why it is very important for the

investors by using hedging tools for getting maximum profit from their portfolios (finweek,

2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

RISK MANAGEMENT OF SECURITIES

References

between.net, D., 2020. Difference Between CML and SML. [Online]

Available at: http://www.differencebetween.net/business/difference-between-cml-and-sml/

[Accessed 15 January 2020].

C. Edward Chang, T. M. K. a. C. T. M., 2019. Intelligent Selection of Smart Beta Mutual

Funds. The Journal of Wealth Management , 22(1), pp. 10-23.

DR Mishra, T. O., 2019. Fama-French, CAPM, and implied cost of equity. Journal of

Economics and Business, Volume 101, pp. 73-85.

EG De Giorgi, T. P. A. Y., 2019. A concave security market line. Journal of Banking &

Finance, Volume 106, pp. 65-81.

finweek, S. L. -., 2019. How to make the right decisions-portfolio management. finweek, pp.

19-19.

Glabadanidis, P., 2019. Smart Beta and Statistical Significance. The Journal of Wealth

Management.

JY Campbell, S. G. C. P. R. T., 2018. An intertemporal CAPM with stochastic volatility.

Journal of Financial Economics, 128(2), pp. 207-233.

Kittipat Laisasikorn, N. R., 2019. A Study of the Relationship Between a Successful

Enterprise Risk Management System, a Performance Measurement System and the Financial

Performance of Thai Listed Companies. American Journal of Business, 10(2).

L Qoqiauri, N. Q., 2019. Main Regulations of CAPM Model and Its Modern Modification.

Management, 7(1), pp. 15-32.

RISK MANAGEMENT OF SECURITIES

References

between.net, D., 2020. Difference Between CML and SML. [Online]

Available at: http://www.differencebetween.net/business/difference-between-cml-and-sml/

[Accessed 15 January 2020].

C. Edward Chang, T. M. K. a. C. T. M., 2019. Intelligent Selection of Smart Beta Mutual

Funds. The Journal of Wealth Management , 22(1), pp. 10-23.

DR Mishra, T. O., 2019. Fama-French, CAPM, and implied cost of equity. Journal of

Economics and Business, Volume 101, pp. 73-85.

EG De Giorgi, T. P. A. Y., 2019. A concave security market line. Journal of Banking &

Finance, Volume 106, pp. 65-81.

finweek, S. L. -., 2019. How to make the right decisions-portfolio management. finweek, pp.

19-19.

Glabadanidis, P., 2019. Smart Beta and Statistical Significance. The Journal of Wealth

Management.

JY Campbell, S. G. C. P. R. T., 2018. An intertemporal CAPM with stochastic volatility.

Journal of Financial Economics, 128(2), pp. 207-233.

Kittipat Laisasikorn, N. R., 2019. A Study of the Relationship Between a Successful

Enterprise Risk Management System, a Performance Measurement System and the Financial

Performance of Thai Listed Companies. American Journal of Business, 10(2).

L Qoqiauri, N. Q., 2019. Main Regulations of CAPM Model and Its Modern Modification.

Management, 7(1), pp. 15-32.

11

RISK MANAGEMENT OF SECURITIES

mojo, W. s., 2020. Security Market Line (SML). [Online]

Available at: https://www.wallstreetmojo.com/security-market-line/

[Accessed 17 January 2020].

O Tilfani, P. F. M. E. B., 2020. Multiscale optimal portfolios using CAPM fractal regression:

estimation for emerging stock markets. Post-Communist Economies, 32(1), pp. 77-112.

O Wagdi, Y. T., 2016. The impact of financial risk on systematic risks: international

evidence. Journal of Applied Finance & Banking, 9(6).

S Hundal, A. E. D. T., 2019. Risk–return relationship in the Finnish stock market in the light

of Capital Asset Pricing Model (CAPM). Journal of Transnational Management , 24(4), pp.

305-322.

Sunderman, M., 2019. Housing'Beta'Common Risk Factor in Returns of Stocks. Journal of

Real Estate Finance and Economics .

TT Cai, J. H. Y. L. X. Z., 2019. High-dimensional minimum variance portfolio estimation

based on high-frequency data. Journal of Econometrics.

VI OSAYI, H. E. M. D., 2019. Risk Management Approach and Banks’ Portfolio Investment.

Risk management, 10(6).

RISK MANAGEMENT OF SECURITIES

mojo, W. s., 2020. Security Market Line (SML). [Online]

Available at: https://www.wallstreetmojo.com/security-market-line/

[Accessed 17 January 2020].

O Tilfani, P. F. M. E. B., 2020. Multiscale optimal portfolios using CAPM fractal regression:

estimation for emerging stock markets. Post-Communist Economies, 32(1), pp. 77-112.

O Wagdi, Y. T., 2016. The impact of financial risk on systematic risks: international

evidence. Journal of Applied Finance & Banking, 9(6).

S Hundal, A. E. D. T., 2019. Risk–return relationship in the Finnish stock market in the light

of Capital Asset Pricing Model (CAPM). Journal of Transnational Management , 24(4), pp.

305-322.

Sunderman, M., 2019. Housing'Beta'Common Risk Factor in Returns of Stocks. Journal of

Real Estate Finance and Economics .

TT Cai, J. H. Y. L. X. Z., 2019. High-dimensional minimum variance portfolio estimation

based on high-frequency data. Journal of Econometrics.

VI OSAYI, H. E. M. D., 2019. Risk Management Approach and Banks’ Portfolio Investment.

Risk management, 10(6).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.