Intangible Assets Of The Microsoft’s Company

VerifiedAdded on 2022/09/08

|13

|2207

|19

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ACCOUNTING

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Accounting

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ACCOUNTING

Table of Contents

Part A...............................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................2

Question 3....................................................................................................................................3

Part B...............................................................................................................................................5

Question 1....................................................................................................................................5

Question 2....................................................................................................................................5

Question 3....................................................................................................................................5

Question 4....................................................................................................................................6

Part C...............................................................................................................................................7

Part D...............................................................................................................................................9

Part E.............................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Part A...............................................................................................................................................2

Question 1....................................................................................................................................2

Question 2....................................................................................................................................2

Question 3....................................................................................................................................3

Part B...............................................................................................................................................5

Question 1....................................................................................................................................5

Question 2....................................................................................................................................5

Question 3....................................................................................................................................5

Question 4....................................................................................................................................6

Part C...............................................................................................................................................7

Part D...............................................................................................................................................9

Part E.............................................................................................................................................10

References......................................................................................................................................11

2ACCOUNTING

Part A

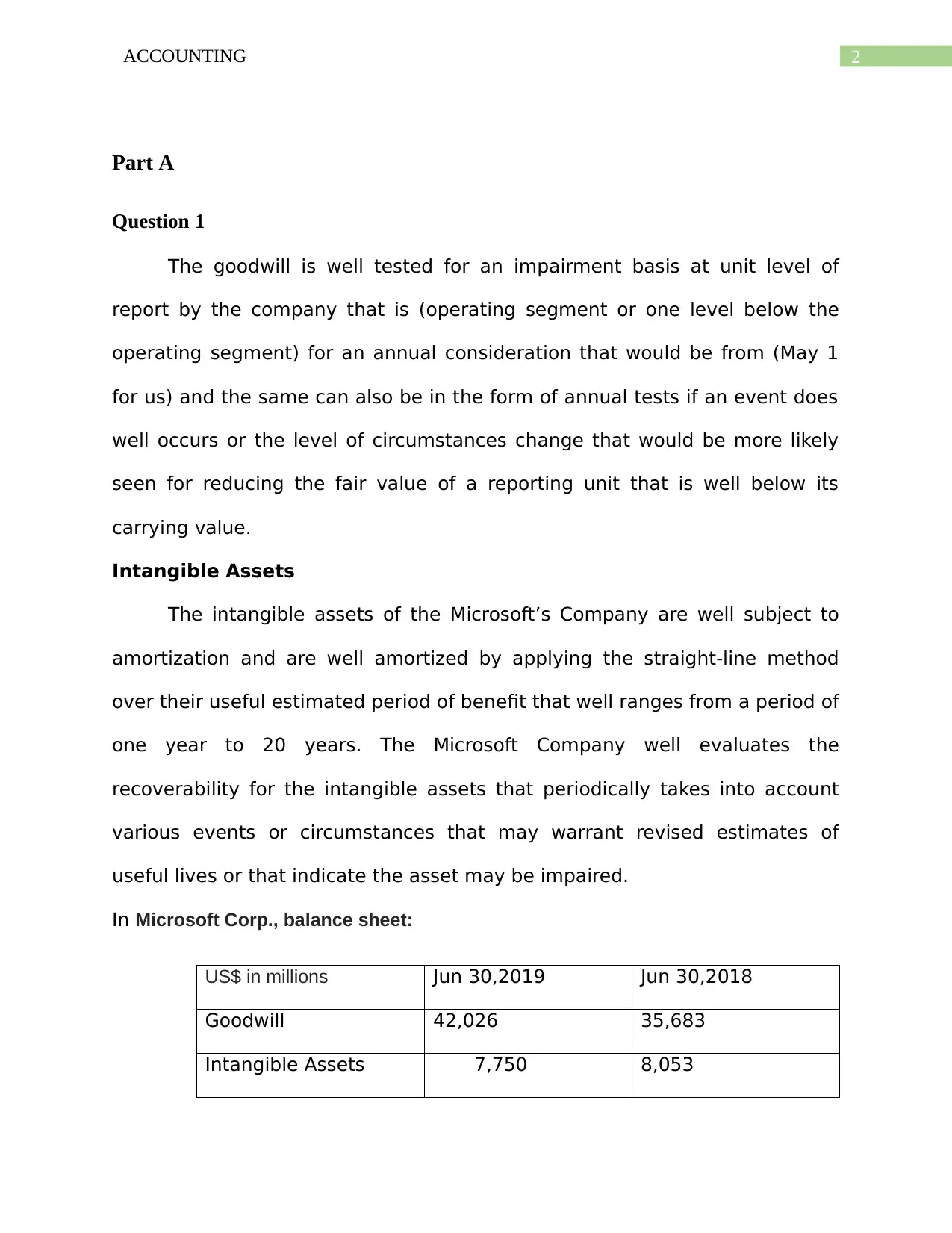

Question 1

The goodwill is well tested for an impairment basis at unit level of

report by the company that is (operating segment or one level below the

operating segment) for an annual consideration that would be from (May 1

for us) and the same can also be in the form of annual tests if an event does

well occurs or the level of circumstances change that would be more likely

seen for reducing the fair value of a reporting unit that is well below its

carrying value.

Intangible Assets

The intangible assets of the Microsoft’s Company are well subject to

amortization and are well amortized by applying the straight-line method

over their useful estimated period of benefit that well ranges from a period of

one year to 20 years. The Microsoft Company well evaluates the

recoverability for the intangible assets that periodically takes into account

various events or circumstances that may warrant revised estimates of

useful lives or that indicate the asset may be impaired.

In Microsoft Corp., balance sheet:

US$ in millions Jun 30,2019 Jun 30,2018

Goodwill 42,026 35,683

Intangible Assets 7,750 8,053

Part A

Question 1

The goodwill is well tested for an impairment basis at unit level of

report by the company that is (operating segment or one level below the

operating segment) for an annual consideration that would be from (May 1

for us) and the same can also be in the form of annual tests if an event does

well occurs or the level of circumstances change that would be more likely

seen for reducing the fair value of a reporting unit that is well below its

carrying value.

Intangible Assets

The intangible assets of the Microsoft’s Company are well subject to

amortization and are well amortized by applying the straight-line method

over their useful estimated period of benefit that well ranges from a period of

one year to 20 years. The Microsoft Company well evaluates the

recoverability for the intangible assets that periodically takes into account

various events or circumstances that may warrant revised estimates of

useful lives or that indicate the asset may be impaired.

In Microsoft Corp., balance sheet:

US$ in millions Jun 30,2019 Jun 30,2018

Goodwill 42,026 35,683

Intangible Assets 7,750 8,053

3ACCOUNTING

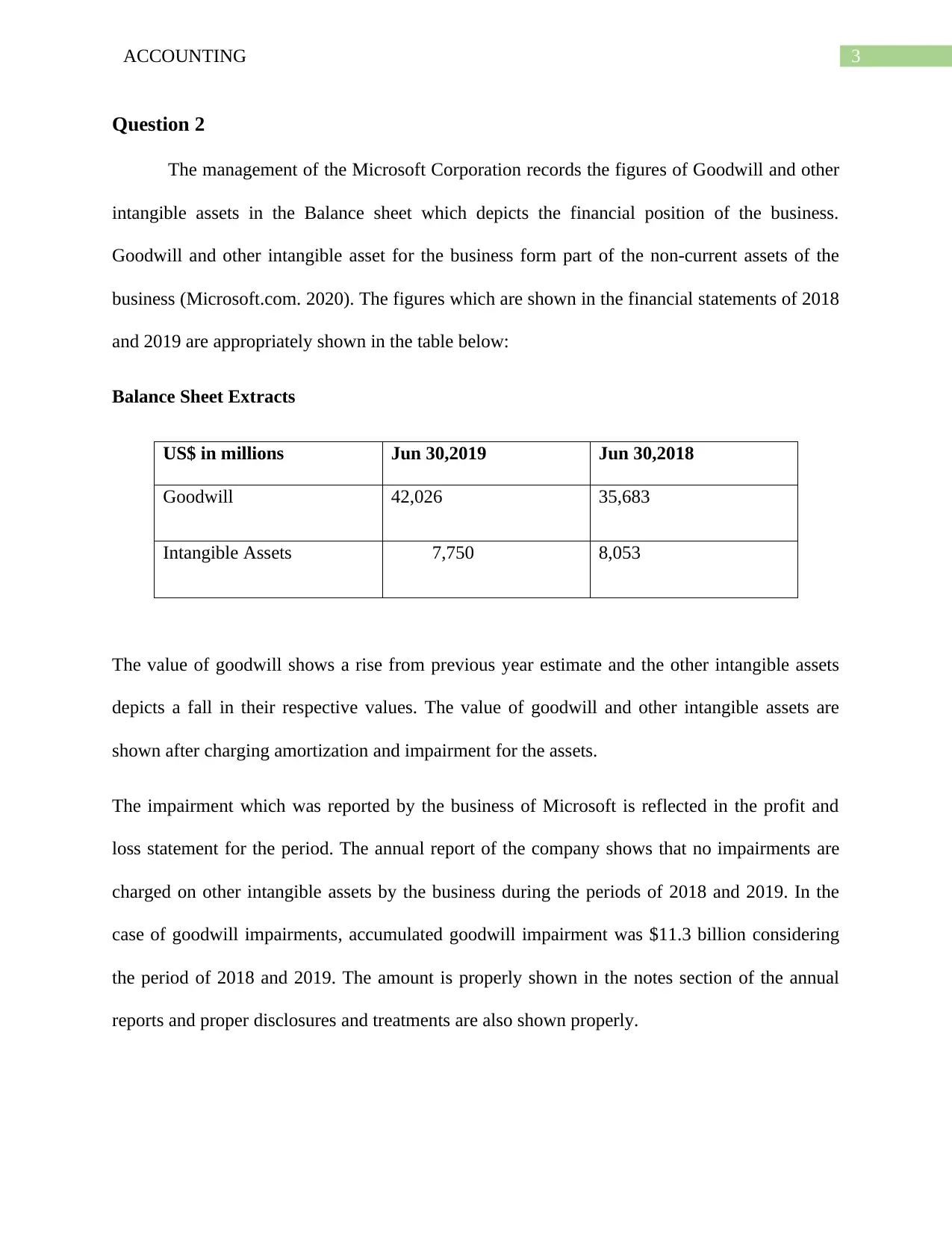

Question 2

The management of the Microsoft Corporation records the figures of Goodwill and other

intangible assets in the Balance sheet which depicts the financial position of the business.

Goodwill and other intangible asset for the business form part of the non-current assets of the

business (Microsoft.com. 2020). The figures which are shown in the financial statements of 2018

and 2019 are appropriately shown in the table below:

Balance Sheet Extracts

US$ in millions Jun 30,2019 Jun 30,2018

Goodwill 42,026 35,683

Intangible Assets 7,750 8,053

The value of goodwill shows a rise from previous year estimate and the other intangible assets

depicts a fall in their respective values. The value of goodwill and other intangible assets are

shown after charging amortization and impairment for the assets.

The impairment which was reported by the business of Microsoft is reflected in the profit and

loss statement for the period. The annual report of the company shows that no impairments are

charged on other intangible assets by the business during the periods of 2018 and 2019. In the

case of goodwill impairments, accumulated goodwill impairment was $11.3 billion considering

the period of 2018 and 2019. The amount is properly shown in the notes section of the annual

reports and proper disclosures and treatments are also shown properly.

Question 2

The management of the Microsoft Corporation records the figures of Goodwill and other

intangible assets in the Balance sheet which depicts the financial position of the business.

Goodwill and other intangible asset for the business form part of the non-current assets of the

business (Microsoft.com. 2020). The figures which are shown in the financial statements of 2018

and 2019 are appropriately shown in the table below:

Balance Sheet Extracts

US$ in millions Jun 30,2019 Jun 30,2018

Goodwill 42,026 35,683

Intangible Assets 7,750 8,053

The value of goodwill shows a rise from previous year estimate and the other intangible assets

depicts a fall in their respective values. The value of goodwill and other intangible assets are

shown after charging amortization and impairment for the assets.

The impairment which was reported by the business of Microsoft is reflected in the profit and

loss statement for the period. The annual report of the company shows that no impairments are

charged on other intangible assets by the business during the periods of 2018 and 2019. In the

case of goodwill impairments, accumulated goodwill impairment was $11.3 billion considering

the period of 2018 and 2019. The amount is properly shown in the notes section of the annual

reports and proper disclosures and treatments are also shown properly.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ACCOUNTING

The annual report for the company does not show any non-controlling interest for the

period as the same usually appears in the profit and loss statement or comprehensive income

statement. However, the business has recently acquired the company of GitHub and LinkedIn

which was done for enhancing the service and revenue of the business.

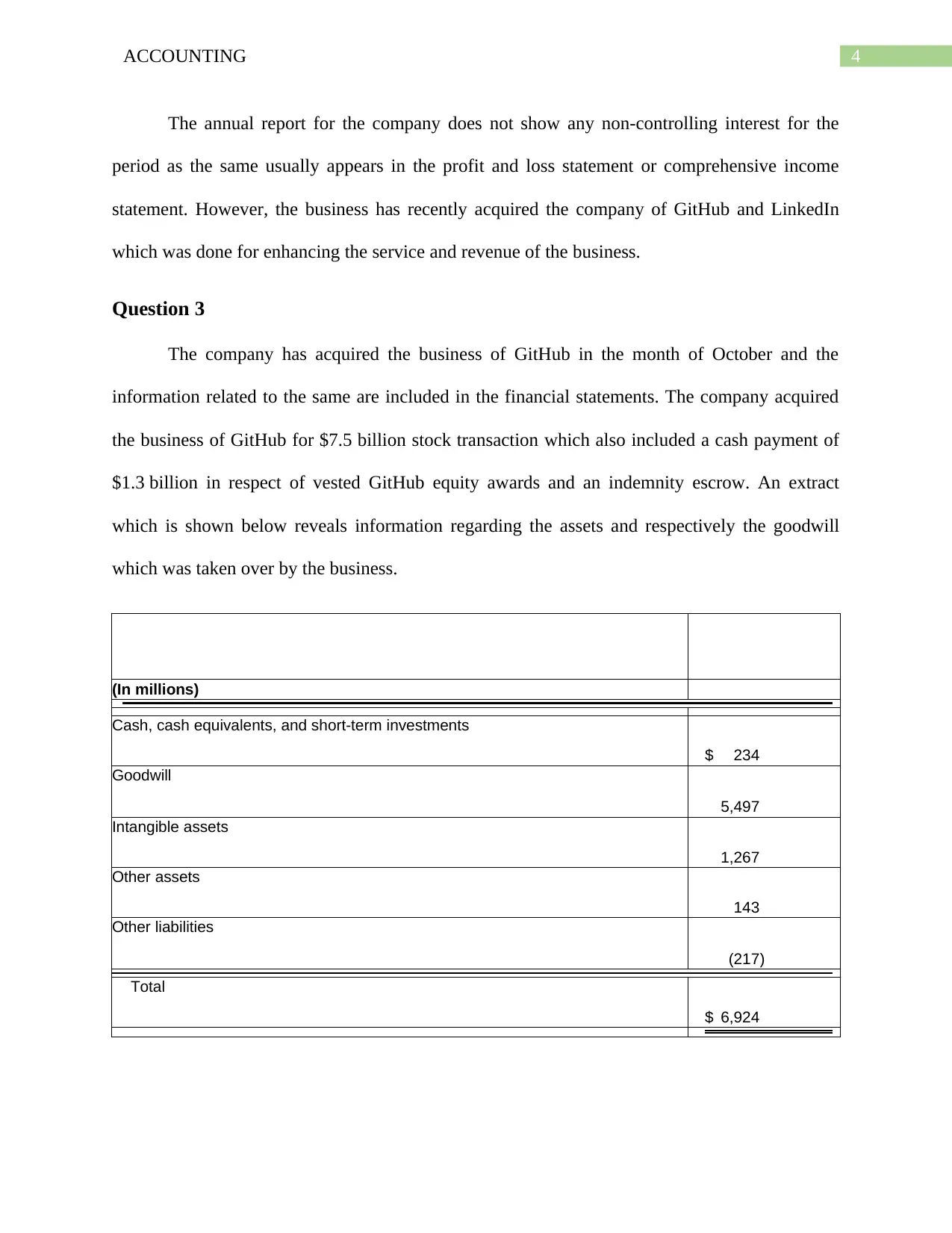

Question 3

The company has acquired the business of GitHub in the month of October and the

information related to the same are included in the financial statements. The company acquired

the business of GitHub for $7.5 billion stock transaction which also included a cash payment of

$1.3 billion in respect of vested GitHub equity awards and an indemnity escrow. An extract

which is shown below reveals information regarding the assets and respectively the goodwill

which was taken over by the business.

(In millions)

Cash, cash equivalents, and short-term investments

$ 234

Goodwill

5,497

Intangible assets

1,267

Other assets

143

Other liabilities

(217)

Total

$ 6,924

The annual report for the company does not show any non-controlling interest for the

period as the same usually appears in the profit and loss statement or comprehensive income

statement. However, the business has recently acquired the company of GitHub and LinkedIn

which was done for enhancing the service and revenue of the business.

Question 3

The company has acquired the business of GitHub in the month of October and the

information related to the same are included in the financial statements. The company acquired

the business of GitHub for $7.5 billion stock transaction which also included a cash payment of

$1.3 billion in respect of vested GitHub equity awards and an indemnity escrow. An extract

which is shown below reveals information regarding the assets and respectively the goodwill

which was taken over by the business.

(In millions)

Cash, cash equivalents, and short-term investments

$ 234

Goodwill

5,497

Intangible assets

1,267

Other assets

143

Other liabilities

(217)

Total

$ 6,924

5ACCOUNTING

The information relating to the acquisition was reported under the notes to account

section under the segment of business combinations. The other assets which are covered in the

financial statements and the same also shows disclosures.

Part B

Question 1

The investment which is made by the business during the period of 2015 is charged with

impairments considering the business model of the company. The impairment charges is

associated with the company of Phone Hardware. The same is appropriately shown in the notes

to accounts section of the financial reports of the business. The impairment charges which can be

identified from the annual report of the company is shown to be $7.5 billion for goodwill and

asset impairment charges and the same is related to Phone Hardware.

Question 2

The impairment charge which is reported by the company is done following the principles of

accounting which is followed in the company and forms part of generally accepted principles

(Hamberg and Beisland 2014). The business records impairments of goodwill in the income

statements and shows proper disclosures for the same in the notes to account section of the

business. The business conducts a goodwill tests and the results revealed that the carrying value

of Phone Hardware goodwill was in excess of its estimated fair value (Ey.com. 2020). The

impairment of goodwill is done so that the business is able to present accurate information

regarding the goodwill in the financial statements and there is no situation of inaccuracy in the

financial statements.

The information relating to the acquisition was reported under the notes to account

section under the segment of business combinations. The other assets which are covered in the

financial statements and the same also shows disclosures.

Part B

Question 1

The investment which is made by the business during the period of 2015 is charged with

impairments considering the business model of the company. The impairment charges is

associated with the company of Phone Hardware. The same is appropriately shown in the notes

to accounts section of the financial reports of the business. The impairment charges which can be

identified from the annual report of the company is shown to be $7.5 billion for goodwill and

asset impairment charges and the same is related to Phone Hardware.

Question 2

The impairment charge which is reported by the company is done following the principles of

accounting which is followed in the company and forms part of generally accepted principles

(Hamberg and Beisland 2014). The business records impairments of goodwill in the income

statements and shows proper disclosures for the same in the notes to account section of the

business. The business conducts a goodwill tests and the results revealed that the carrying value

of Phone Hardware goodwill was in excess of its estimated fair value (Ey.com. 2020). The

impairment of goodwill is done so that the business is able to present accurate information

regarding the goodwill in the financial statements and there is no situation of inaccuracy in the

financial statements.

6ACCOUNTING

Question 3

The impairment charges needs to be properly reported in the profit and loss statement and also

cash flow statement and proper disclosures also needs to be provided in the notes to account

section of the financial statements (André, Dionysiou and Tsalavoutas 2018). The profit and loss

statement for Microsoft Company shows that impairment charges are considered to be a charge

against the profits and the same is deducted from the revenue figure to arrive at the net profits for

the business during the period. It is to be noted that impairment charges form part of non-cash

expenses (Johansson, Hjelström and Hellman 2016). As per the 2015 annual report of the

company, the management utilizes indirect method of cash flow and therefore considers the

profits as the starting point. The non-cash expenses need to be added back to the profits so that

cash profits can be achieved. The cash flow statement for the company shows similar treatments

during the period. The business also adjusts other non-cash items which are required to be done

in order to achieve the cash profits of the business. The management of the company also needs

to consider such impairments with proper disclosures and the same should be presented in the

notes to accounts section of the business.

Question 4

The impairment of goodwill is done after proper testing for impairments is done for any

company. In the case of Microsoft also, the management of the company conducts impairments

tests by analysing the goodwill at reporting unit level. The first step which needs to be followed

while measuring impairment charges for goodwill is identification of reporting units in

association with the same. Then the fair value of the identified reporting unit is computed and the

method which is used for such a purpose is discounted cash flow. It is also to be noted that

number of assumptions needs to be made by the management of the company for accurately

Question 3

The impairment charges needs to be properly reported in the profit and loss statement and also

cash flow statement and proper disclosures also needs to be provided in the notes to account

section of the financial statements (André, Dionysiou and Tsalavoutas 2018). The profit and loss

statement for Microsoft Company shows that impairment charges are considered to be a charge

against the profits and the same is deducted from the revenue figure to arrive at the net profits for

the business during the period. It is to be noted that impairment charges form part of non-cash

expenses (Johansson, Hjelström and Hellman 2016). As per the 2015 annual report of the

company, the management utilizes indirect method of cash flow and therefore considers the

profits as the starting point. The non-cash expenses need to be added back to the profits so that

cash profits can be achieved. The cash flow statement for the company shows similar treatments

during the period. The business also adjusts other non-cash items which are required to be done

in order to achieve the cash profits of the business. The management of the company also needs

to consider such impairments with proper disclosures and the same should be presented in the

notes to accounts section of the business.

Question 4

The impairment of goodwill is done after proper testing for impairments is done for any

company. In the case of Microsoft also, the management of the company conducts impairments

tests by analysing the goodwill at reporting unit level. The first step which needs to be followed

while measuring impairment charges for goodwill is identification of reporting units in

association with the same. Then the fair value of the identified reporting unit is computed and the

method which is used for such a purpose is discounted cash flow. It is also to be noted that

number of assumptions needs to be made by the management of the company for accurately

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ACCOUNTING

ascertaining the impairment charges (Lange, Fornaro and Buttermilch 2014). Further, if any

changes takes place in the reporting unit or the assumptions which is considered than the whole

computation process for ascertaining the impairment charges would alter. The complexity of the

estimation of impairment charges for goodwill is the reason that the business needs to provide

proper disclosures in the financial statements so that a level of transparency is maintained in the

reporting framework of the entity.

Part C

IFRS GAAP

Assignment/allocation of Goodwill As per the provisions of

IAS 36, goodwill is

allocated to CGU or a

group for the purpose of

testing the same for

impairment charges. In

case the allocation of

Goodwill cannot be done

than the same is

measured at the lowest

level for the entity and

the same monitored

effectively.

In the case of GAAP,

goodwill is computed as a

difference between the

purchase price and total

value of assets and

liabilities. The goodwill is

appropriately measured

under this principle

considering thee assets

and liabilities of the

business which is being

considered.

Impairment of goodwill As per the provisions

which are covered in

IFRS framework, the

method compares the

total carrying value of

the CGU with the

recoverable amounts so

that it can be ascertained

if impairment charges is

applicable or not. In case

impairment is applicable,

Under GAAP framework,

the requirement is that

companies needs to

annually review their

goodwill for impairment

charges at a reporting unit

level. In case, the

carrying value of the

goodwill is higher than

the fair value of the

goodwill than impairment

ascertaining the impairment charges (Lange, Fornaro and Buttermilch 2014). Further, if any

changes takes place in the reporting unit or the assumptions which is considered than the whole

computation process for ascertaining the impairment charges would alter. The complexity of the

estimation of impairment charges for goodwill is the reason that the business needs to provide

proper disclosures in the financial statements so that a level of transparency is maintained in the

reporting framework of the entity.

Part C

IFRS GAAP

Assignment/allocation of Goodwill As per the provisions of

IAS 36, goodwill is

allocated to CGU or a

group for the purpose of

testing the same for

impairment charges. In

case the allocation of

Goodwill cannot be done

than the same is

measured at the lowest

level for the entity and

the same monitored

effectively.

In the case of GAAP,

goodwill is computed as a

difference between the

purchase price and total

value of assets and

liabilities. The goodwill is

appropriately measured

under this principle

considering thee assets

and liabilities of the

business which is being

considered.

Impairment of goodwill As per the provisions

which are covered in

IFRS framework, the

method compares the

total carrying value of

the CGU with the

recoverable amounts so

that it can be ascertained

if impairment charges is

applicable or not. In case

impairment is applicable,

Under GAAP framework,

the requirement is that

companies needs to

annually review their

goodwill for impairment

charges at a reporting unit

level. In case, the

carrying value of the

goodwill is higher than

the fair value of the

goodwill than impairment

8ACCOUNTING

the loss is first charges to

goodwill and then the

same is allocated to other

assets of the business. In

the case of IFRS

framework, reversal of

impairment charges is

prohibited considering

the provisions of IAS 36.

charges would be

applicable to the

business. The method is

more consistent with

considering the assets of

the business for analysis.

In the case of GAAP

principles as well,

reversal of impairment is

also prohibited so it can

be said that consistency is

maintained.

Amortization and impairment of

intangible assets other than goodwill

The criterion which is

followed for measuring

the intangible assets

needs to be followed. In

addition to this allocation

must be done to CBU for

identifying the carrying

value of the assets and

ensuring proper reporting

is maintained

The amortization and

impairment charges for

assets under this

framework need to be

properly measured. The

assets and liabilities of

the business also need to

be measured. The

amortization and

impairments charges for

GAAP are slightly

consistent with the

treatments which is

covered in IFRS

framework

Non-Controlling interest The non-controlling

interest for the business

is measured

appropriately. The

provisions of IAS 27

states that any position

that holds less than 50%

of the outstanding voting

rights is deemed to be

a non-controlling

interest.

The non-controlling

interest for the business

under IFRS framework

and the same is consistent

with the US GAAP

framework and the same

needs to be properly

reported in the financial

statements and

appropriate disclosures

are provided

the loss is first charges to

goodwill and then the

same is allocated to other

assets of the business. In

the case of IFRS

framework, reversal of

impairment charges is

prohibited considering

the provisions of IAS 36.

charges would be

applicable to the

business. The method is

more consistent with

considering the assets of

the business for analysis.

In the case of GAAP

principles as well,

reversal of impairment is

also prohibited so it can

be said that consistency is

maintained.

Amortization and impairment of

intangible assets other than goodwill

The criterion which is

followed for measuring

the intangible assets

needs to be followed. In

addition to this allocation

must be done to CBU for

identifying the carrying

value of the assets and

ensuring proper reporting

is maintained

The amortization and

impairment charges for

assets under this

framework need to be

properly measured. The

assets and liabilities of

the business also need to

be measured. The

amortization and

impairments charges for

GAAP are slightly

consistent with the

treatments which is

covered in IFRS

framework

Non-Controlling interest The non-controlling

interest for the business

is measured

appropriately. The

provisions of IAS 27

states that any position

that holds less than 50%

of the outstanding voting

rights is deemed to be

a non-controlling

interest.

The non-controlling

interest for the business

under IFRS framework

and the same is consistent

with the US GAAP

framework and the same

needs to be properly

reported in the financial

statements and

appropriate disclosures

are provided

9ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ACCOUNTING

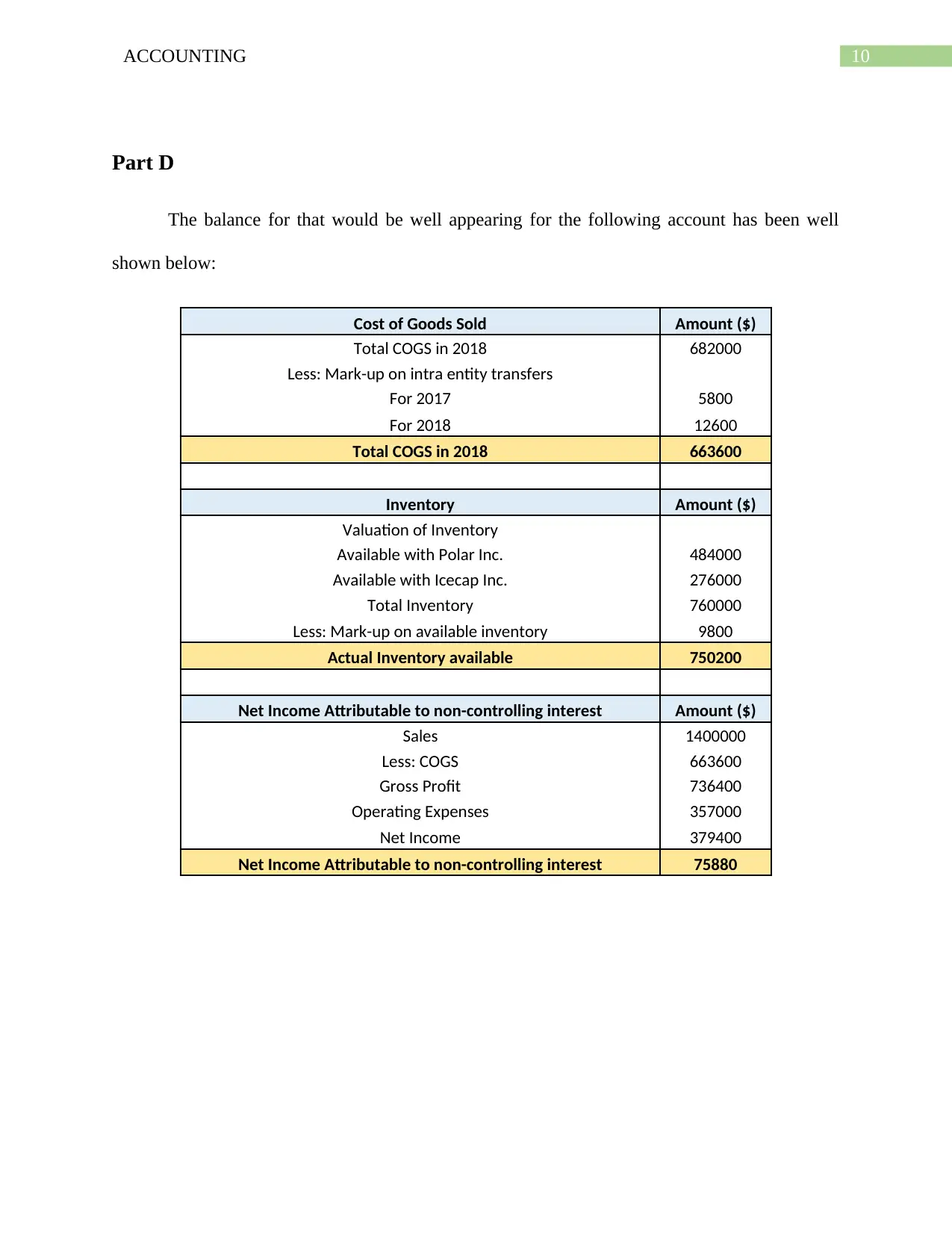

Part D

The balance for that would be well appearing for the following account has been well

shown below:

Cost of Goods Sold Amount ($)

Total COGS in 2018 682000

Less: Mark-up on intra entity transfers

For 2017 5800

For 2018 12600

Total COGS in 2018 663600

Inventory Amount ($)

Valuation of Inventory

Available with Polar Inc. 484000

Available with Icecap Inc. 276000

Total Inventory 760000

Less: Mark-up on available inventory 9800

Actual Inventory available 750200

Net Income Attributable to non-controlling interest Amount ($)

Sales 1400000

Less: COGS 663600

Gross Profit 736400

Operating Expenses 357000

Net Income 379400

Net Income Attributable to non-controlling interest 75880

Part D

The balance for that would be well appearing for the following account has been well

shown below:

Cost of Goods Sold Amount ($)

Total COGS in 2018 682000

Less: Mark-up on intra entity transfers

For 2017 5800

For 2018 12600

Total COGS in 2018 663600

Inventory Amount ($)

Valuation of Inventory

Available with Polar Inc. 484000

Available with Icecap Inc. 276000

Total Inventory 760000

Less: Mark-up on available inventory 9800

Actual Inventory available 750200

Net Income Attributable to non-controlling interest Amount ($)

Sales 1400000

Less: COGS 663600

Gross Profit 736400

Operating Expenses 357000

Net Income 379400

Net Income Attributable to non-controlling interest 75880

11ACCOUNTING

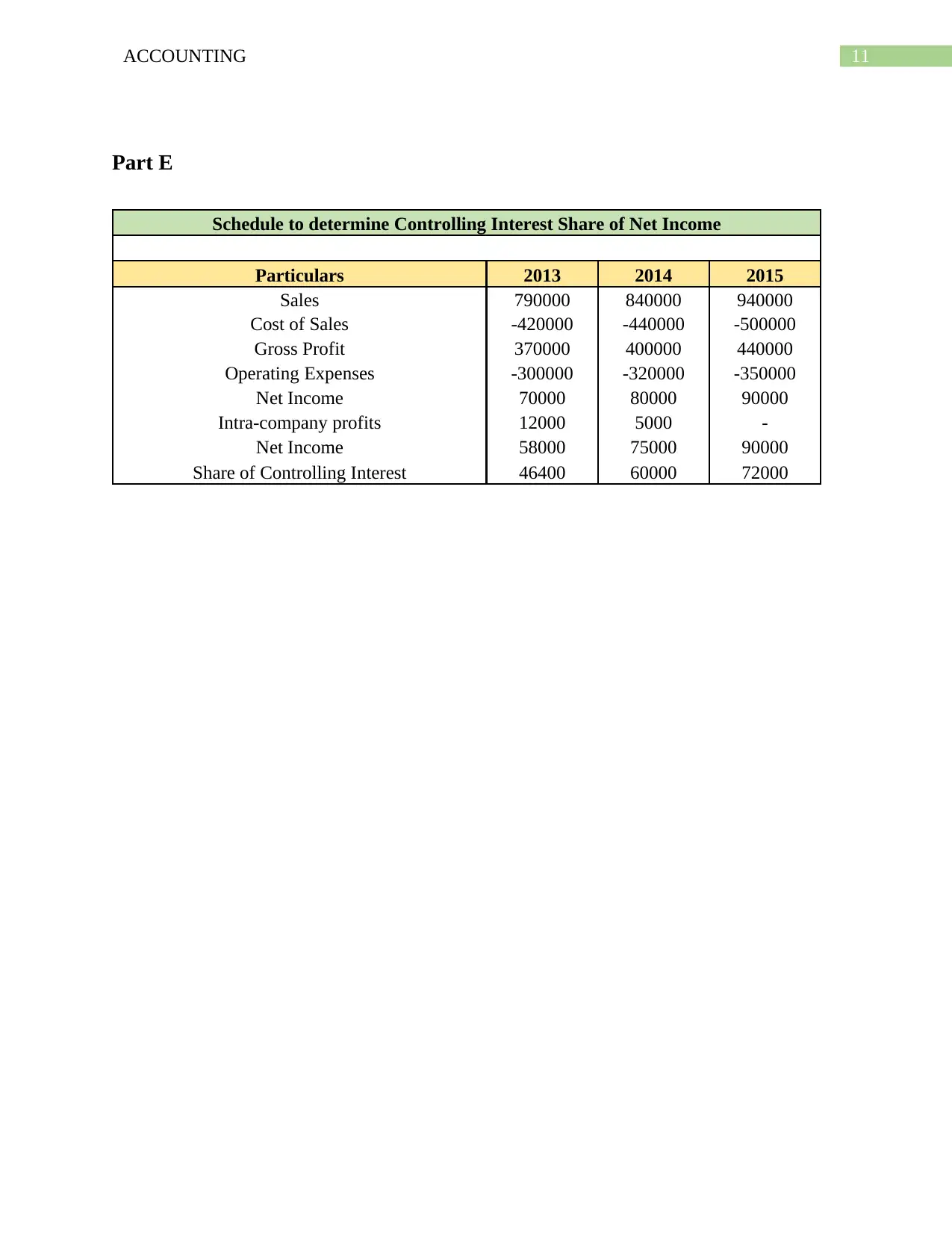

Part E

Schedule to determine Controlling Interest Share of Net Income

Particulars 2013 2014 2015

Sales 790000 840000 940000

Cost of Sales -420000 -440000 -500000

Gross Profit 370000 400000 440000

Operating Expenses -300000 -320000 -350000

Net Income 70000 80000 90000

Intra-company profits 12000 5000 -

Net Income 58000 75000 90000

Share of Controlling Interest 46400 60000 72000

Part E

Schedule to determine Controlling Interest Share of Net Income

Particulars 2013 2014 2015

Sales 790000 840000 940000

Cost of Sales -420000 -440000 -500000

Gross Profit 370000 400000 440000

Operating Expenses -300000 -320000 -350000

Net Income 70000 80000 90000

Intra-company profits 12000 5000 -

Net Income 58000 75000 90000

Share of Controlling Interest 46400 60000 72000

12ACCOUNTING

References

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts. Applied Economics, 50(7), pp.707-725.

Ey.com. (2020). [online] Available at:

https://www.ey.com/Publication/vwLUAssets/Impairment_accounting_the_basics_of_IAS_36_I

mpairment_of_Assets/$FILE/Impairment_accounting_IAS_36.pdf [Accessed 5 Apr. 2020].

Hamberg, M. and Beisland, L.A., 2014. Changes in the value relevance of goodwill accounting

following the adoption of IFRS 3. Journal of International Accounting, Auditing and

Taxation, 23(2), pp.59-73.

Johansson, S.E., Hjelström, T. and Hellman, N., 2016. Accounting for goodwill under IFRS: A

critical analysis. Journal of international accounting, auditing and taxation, 27, pp.13-25.

Lange, C., Fornaro, J. and Buttermilch, R., 2014. Qualitative assessment of impairment for

goodwill and other indefinite-lived intangibles. The CPA Journal, 2014, pp.22-29.

Microsoft.com. (2020). Download Center - Microsoft 2019 Annual Report. [online] Available at:

https://www.microsoft.com/investor/reports/ar19/download-center/ [Accessed 5 Apr. 2020].

References

André, P., Dionysiou, D. and Tsalavoutas, I., 2018. Mandated disclosures under IAS 36

Impairment of Assets and IAS 38 Intangible Assets: value relevance and impact on analysts’

forecasts. Applied Economics, 50(7), pp.707-725.

Ey.com. (2020). [online] Available at:

https://www.ey.com/Publication/vwLUAssets/Impairment_accounting_the_basics_of_IAS_36_I

mpairment_of_Assets/$FILE/Impairment_accounting_IAS_36.pdf [Accessed 5 Apr. 2020].

Hamberg, M. and Beisland, L.A., 2014. Changes in the value relevance of goodwill accounting

following the adoption of IFRS 3. Journal of International Accounting, Auditing and

Taxation, 23(2), pp.59-73.

Johansson, S.E., Hjelström, T. and Hellman, N., 2016. Accounting for goodwill under IFRS: A

critical analysis. Journal of international accounting, auditing and taxation, 27, pp.13-25.

Lange, C., Fornaro, J. and Buttermilch, R., 2014. Qualitative assessment of impairment for

goodwill and other indefinite-lived intangibles. The CPA Journal, 2014, pp.22-29.

Microsoft.com. (2020). Download Center - Microsoft 2019 Annual Report. [online] Available at:

https://www.microsoft.com/investor/reports/ar19/download-center/ [Accessed 5 Apr. 2020].

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.