Estimating Risk and Return: Assignment for Fundamentals of Finance

VerifiedAdded on 2022/08/22

|7

|995

|31

Homework Assignment

AI Summary

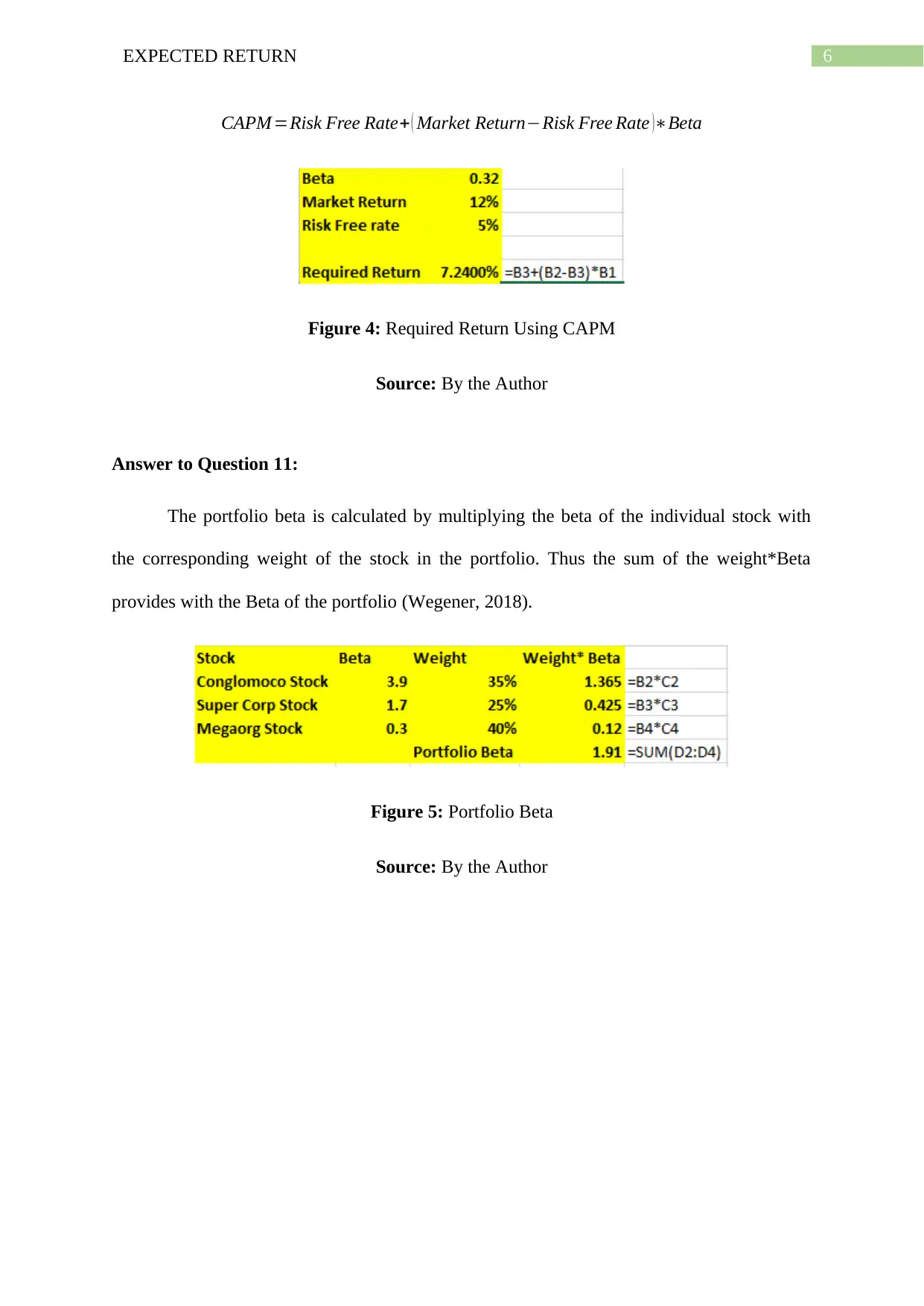

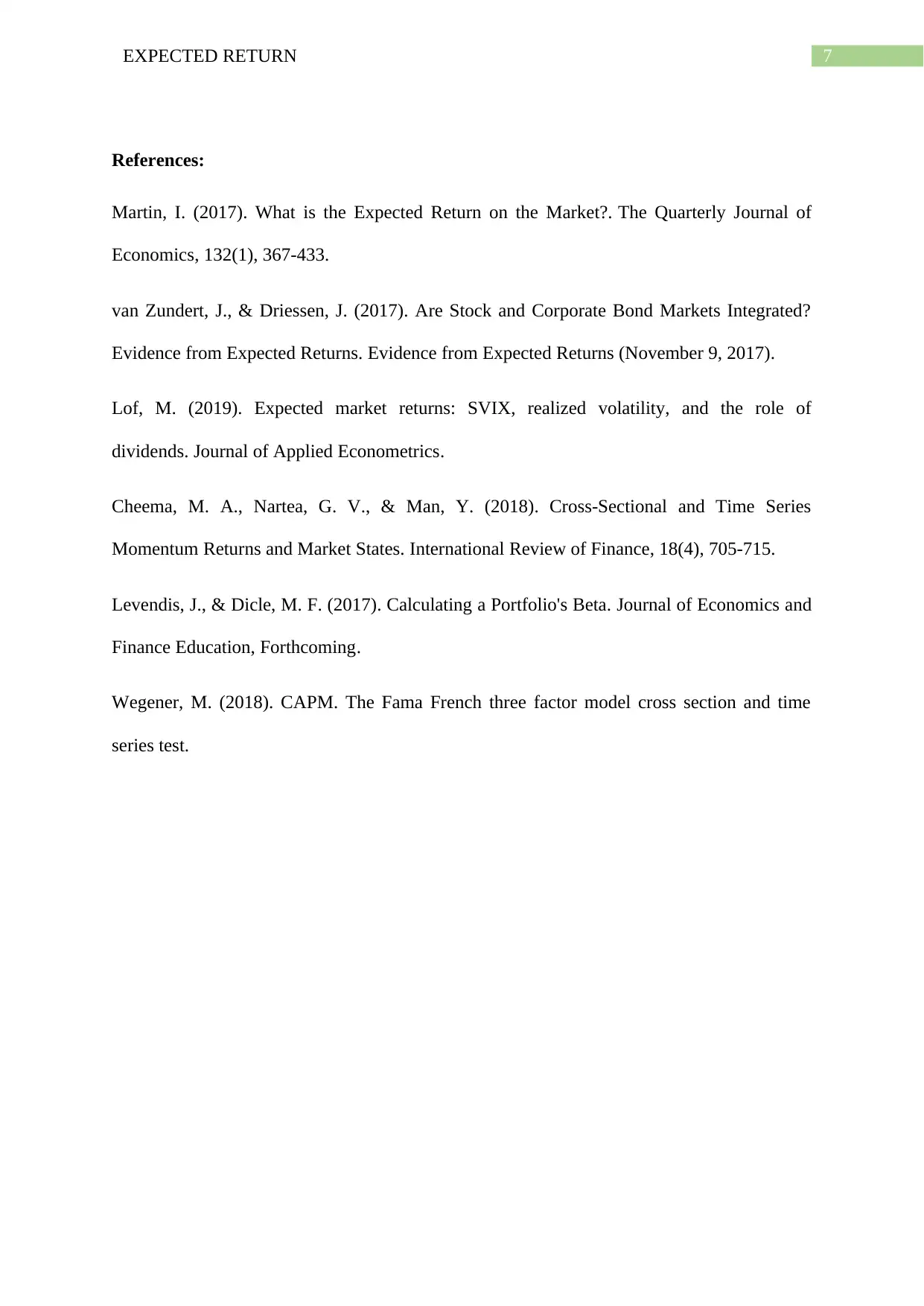

This assignment provides a comprehensive analysis of expected return and related financial concepts. It begins by defining expected return and its practical applications, followed by an exploration of the challenges associated with its use. The assignment then delves into portfolio construction, explaining how different allocations between risk-free securities and market portfolios can achieve desired risk levels. Furthermore, it covers the calculation of expected return under varying economic states, required return, and the market risk premium. The assignment culminates in the application of the Capital Asset Pricing Model (CAPM) and the calculation of portfolio beta, offering a complete understanding of risk and return estimation in finance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.