Microeconomics Assignment: Elasticity, Market Analysis, and Costs

VerifiedAdded on 2022/09/09

|9

|1154

|18

Homework Assignment

AI Summary

This microeconomics assignment explores core economic concepts through a series of questions and answers. The solution analyzes the effects of income changes on the demand for CFL tickets (normal goods) and the impact of price changes on substitute goods (TSN and RDS). It also examines the ...

Running head: MICROECONOMICS

Microeconomics

Name of Student:

Name of University:

Course ID:

Author Note:

Microeconomics

Name of Student:

Name of University:

Course ID:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MICROECONOMICS

Table of Contents

Answer to Question: 1.....................................................................................................................2

Answer to Question: 2.....................................................................................................................3

Answer to Question: 3.....................................................................................................................4

Answer to Question: 4.....................................................................................................................6

Reference List..................................................................................................................................8

Table of Contents

Answer to Question: 1.....................................................................................................................2

Answer to Question: 2.....................................................................................................................3

Answer to Question: 3.....................................................................................................................4

Answer to Question: 4.....................................................................................................................6

Reference List..................................................................................................................................8

2MICROECONOMICS

Quantity

Price

DB

DA

QA

A

QB

PA

PB

SA

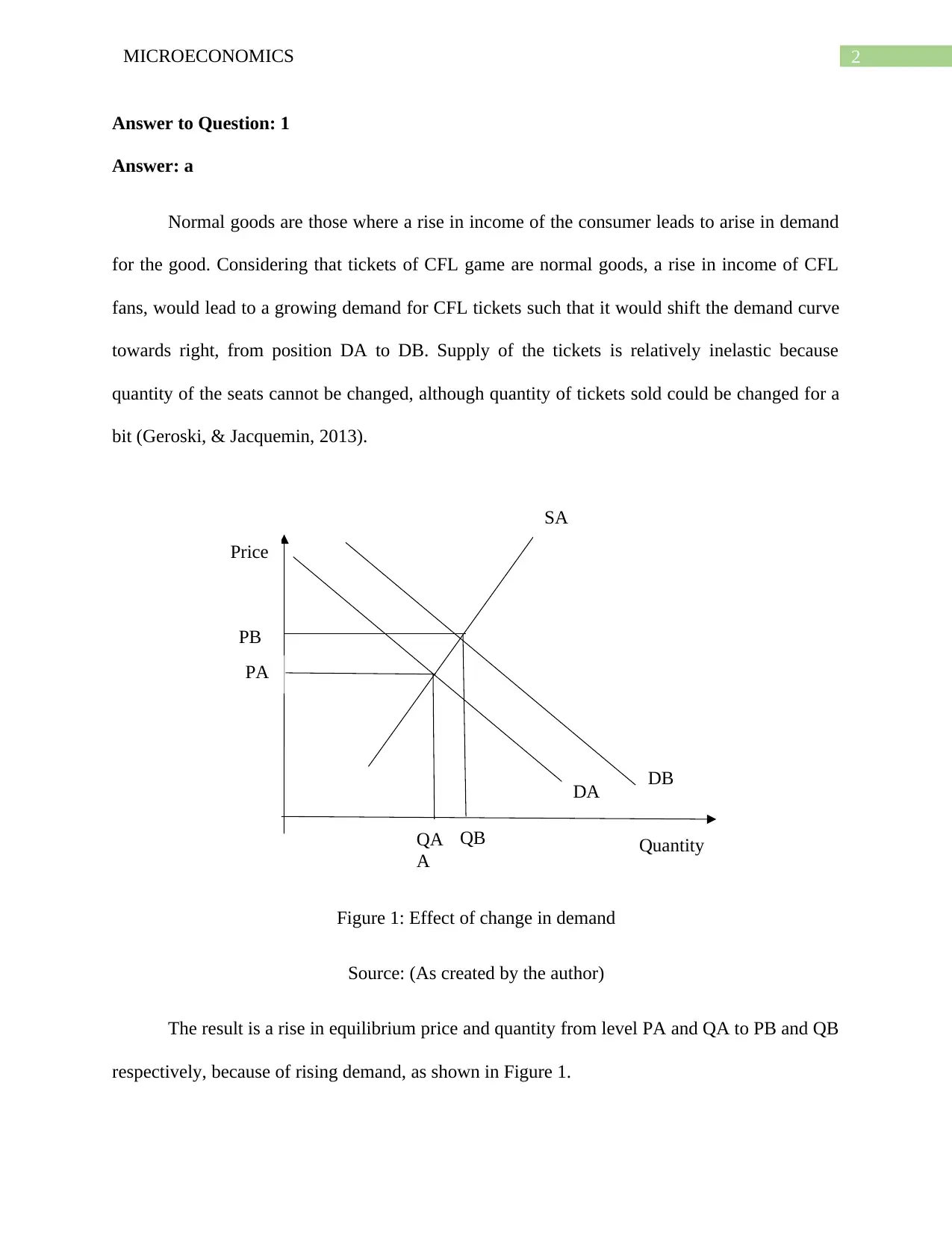

Answer to Question: 1

Answer: a

Normal goods are those where a rise in income of the consumer leads to arise in demand

for the good. Considering that tickets of CFL game are normal goods, a rise in income of CFL

fans, would lead to a growing demand for CFL tickets such that it would shift the demand curve

towards right, from position DA to DB. Supply of the tickets is relatively inelastic because

quantity of the seats cannot be changed, although quantity of tickets sold could be changed for a

bit (Geroski, & Jacquemin, 2013).

Figure 1: Effect of change in demand

Source: (As created by the author)

The result is a rise in equilibrium price and quantity from level PA and QA to PB and QB

respectively, because of rising demand, as shown in Figure 1.

Quantity

Price

DB

DA

QA

A

QB

PA

PB

SA

Answer to Question: 1

Answer: a

Normal goods are those where a rise in income of the consumer leads to arise in demand

for the good. Considering that tickets of CFL game are normal goods, a rise in income of CFL

fans, would lead to a growing demand for CFL tickets such that it would shift the demand curve

towards right, from position DA to DB. Supply of the tickets is relatively inelastic because

quantity of the seats cannot be changed, although quantity of tickets sold could be changed for a

bit (Geroski, & Jacquemin, 2013).

Figure 1: Effect of change in demand

Source: (As created by the author)

The result is a rise in equilibrium price and quantity from level PA and QA to PB and QB

respectively, because of rising demand, as shown in Figure 1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MICROECONOMICS

Answer b

Substitute goods are those goods which have mostly same features and satisfies the same

level of consumer demand. One good can be used in place of other good when there is rise in

price of one good (Scitovsky, 2013). Price and quantity demanded are inversely related such that

rise in subscription price of TSN would lead to a fall in demand for TSN. As TSN and RDS are

sports channels, therefore demand for RDS channel would go up as consumers would substitute

TSN for RDS.

Answer to Question: 2

In order to explain the relationship between number of diamonds purchased and the

average income of the consumers, the average income would be the dependent variable and the

number of diamonds purchased would be the independent variable. This is because the income of

the people determines the number of diamonds purchased (Dupraz, 2016).

Answer b

Substitute goods are those goods which have mostly same features and satisfies the same

level of consumer demand. One good can be used in place of other good when there is rise in

price of one good (Scitovsky, 2013). Price and quantity demanded are inversely related such that

rise in subscription price of TSN would lead to a fall in demand for TSN. As TSN and RDS are

sports channels, therefore demand for RDS channel would go up as consumers would substitute

TSN for RDS.

Answer to Question: 2

In order to explain the relationship between number of diamonds purchased and the

average income of the consumers, the average income would be the dependent variable and the

number of diamonds purchased would be the independent variable. This is because the income of

the people determines the number of diamonds purchased (Dupraz, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MICROECONOMICS

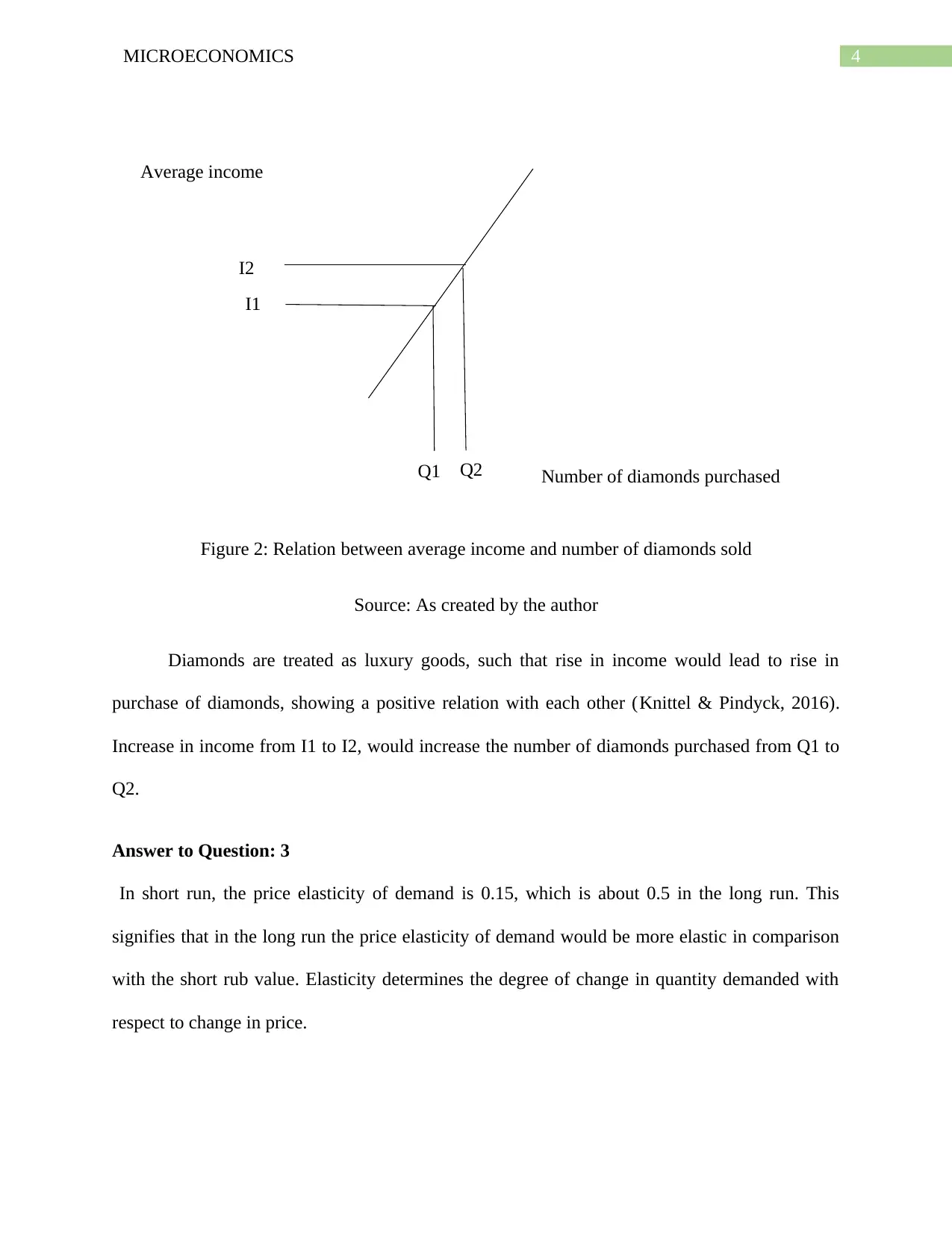

Number of diamonds purchasedQ1 Q2

I1

I2

Average income

Figure 2: Relation between average income and number of diamonds sold

Source: As created by the author

Diamonds are treated as luxury goods, such that rise in income would lead to rise in

purchase of diamonds, showing a positive relation with each other (Knittel & Pindyck, 2016).

Increase in income from I1 to I2, would increase the number of diamonds purchased from Q1 to

Q2.

Answer to Question: 3

In short run, the price elasticity of demand is 0.15, which is about 0.5 in the long run. This

signifies that in the long run the price elasticity of demand would be more elastic in comparison

with the short rub value. Elasticity determines the degree of change in quantity demanded with

respect to change in price.

Number of diamonds purchasedQ1 Q2

I1

I2

Average income

Figure 2: Relation between average income and number of diamonds sold

Source: As created by the author

Diamonds are treated as luxury goods, such that rise in income would lead to rise in

purchase of diamonds, showing a positive relation with each other (Knittel & Pindyck, 2016).

Increase in income from I1 to I2, would increase the number of diamonds purchased from Q1 to

Q2.

Answer to Question: 3

In short run, the price elasticity of demand is 0.15, which is about 0.5 in the long run. This

signifies that in the long run the price elasticity of demand would be more elastic in comparison

with the short rub value. Elasticity determines the degree of change in quantity demanded with

respect to change in price.

5MICROECONOMICS

Figure 3: Inelastic demand for electricity in short-run

In the short run, the demand is relatively less elastic or inelastic meaning that demand is

less responsive to price. Long run elasticity signifies that demand for goods would be more

elastic to price change such that the amount of fall in quantity demanded would be more than the

rise in place (Mankiw, 2016).

Figure 4: Long-run price elasticity of electricity

The long-run price elasticity of demand is flatter than the short run because in long run,

there are more number of firms who are able to produce substitute products. In short-run people

Figure 3: Inelastic demand for electricity in short-run

In the short run, the demand is relatively less elastic or inelastic meaning that demand is

less responsive to price. Long run elasticity signifies that demand for goods would be more

elastic to price change such that the amount of fall in quantity demanded would be more than the

rise in place (Mankiw, 2016).

Figure 4: Long-run price elasticity of electricity

The long-run price elasticity of demand is flatter than the short run because in long run,

there are more number of firms who are able to produce substitute products. In short-run people

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MICROECONOMICS

does not have much options and a price change would not change their demand in greater

proportions.

Answer to Question: 4

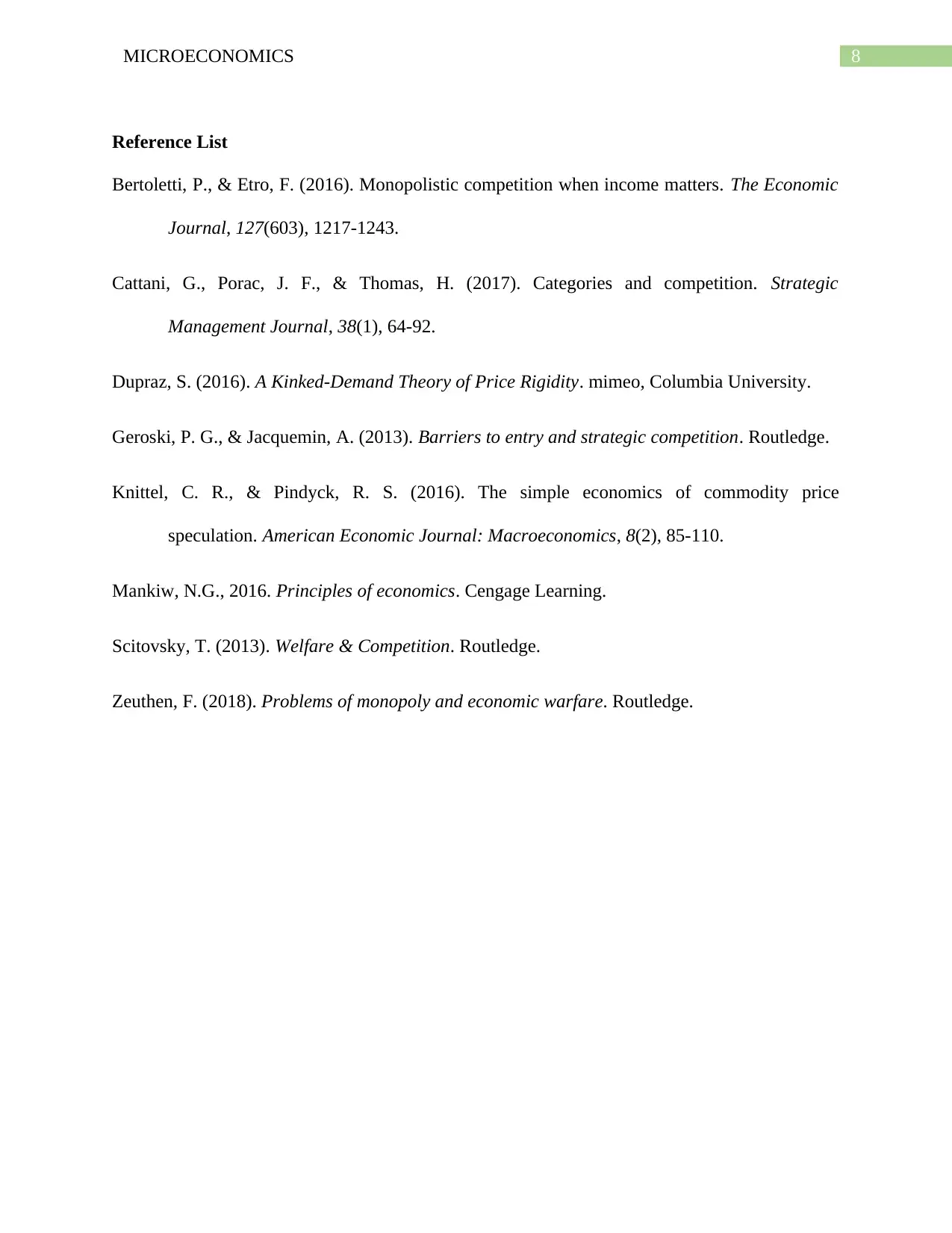

Table 1: Calculation of marginal cost and average cost of the firm

Answer a

In the short run, competitive firms would charge same price and still earn super normal

profits because there are fewer cherry firms in the industry. When the price is $8, the average

cost is lesser than the marginal cost, meaning that firm with gather super normal profit in the

short run as they would benefit from lower average cost (Zeuthen, 2018). With, passing time

news firms would enter in the market because of free entry and exit relationship between the

firms which would change the overall profit and output of firms. In long run, Hank and Helen

would have more rival firms producing the same good which would lower the demand for their

products and therefore, they need to set price below 8 dollars.

Answer b

When Hank and Helen are able to lower their price from 8 dollar to 3.75 dollar, the

demand for their cherries would go up in the market. However, the average cost exceeds the

does not have much options and a price change would not change their demand in greater

proportions.

Answer to Question: 4

Table 1: Calculation of marginal cost and average cost of the firm

Answer a

In the short run, competitive firms would charge same price and still earn super normal

profits because there are fewer cherry firms in the industry. When the price is $8, the average

cost is lesser than the marginal cost, meaning that firm with gather super normal profit in the

short run as they would benefit from lower average cost (Zeuthen, 2018). With, passing time

news firms would enter in the market because of free entry and exit relationship between the

firms which would change the overall profit and output of firms. In long run, Hank and Helen

would have more rival firms producing the same good which would lower the demand for their

products and therefore, they need to set price below 8 dollars.

Answer b

When Hank and Helen are able to lower their price from 8 dollar to 3.75 dollar, the

demand for their cherries would go up in the market. However, the average cost exceeds the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MICROECONOMICS

marginal cost, even in the short run where AC is $5.5 and MC is $4. Firms would run in loss as

their average cost exceeds the marginal cost. They would not be able to operate the firms for

longer time span as they won’t be able to generate profit which is used to buy inputs for further

productions. In the long run, firms of Hank and Helen would stop working as and shut down due

to repetitive losses in the short run (Dupraz, 2016).

marginal cost, even in the short run where AC is $5.5 and MC is $4. Firms would run in loss as

their average cost exceeds the marginal cost. They would not be able to operate the firms for

longer time span as they won’t be able to generate profit which is used to buy inputs for further

productions. In the long run, firms of Hank and Helen would stop working as and shut down due

to repetitive losses in the short run (Dupraz, 2016).

8MICROECONOMICS

Reference List

Bertoletti, P., & Etro, F. (2016). Monopolistic competition when income matters. The Economic

Journal, 127(603), 1217-1243.

Cattani, G., Porac, J. F., & Thomas, H. (2017). Categories and competition. Strategic

Management Journal, 38(1), 64-92.

Dupraz, S. (2016). A Kinked-Demand Theory of Price Rigidity. mimeo, Columbia University.

Geroski, P. G., & Jacquemin, A. (2013). Barriers to entry and strategic competition. Routledge.

Knittel, C. R., & Pindyck, R. S. (2016). The simple economics of commodity price

speculation. American Economic Journal: Macroeconomics, 8(2), 85-110.

Mankiw, N.G., 2016. Principles of economics. Cengage Learning.

Scitovsky, T. (2013). Welfare & Competition. Routledge.

Zeuthen, F. (2018). Problems of monopoly and economic warfare. Routledge.

Reference List

Bertoletti, P., & Etro, F. (2016). Monopolistic competition when income matters. The Economic

Journal, 127(603), 1217-1243.

Cattani, G., Porac, J. F., & Thomas, H. (2017). Categories and competition. Strategic

Management Journal, 38(1), 64-92.

Dupraz, S. (2016). A Kinked-Demand Theory of Price Rigidity. mimeo, Columbia University.

Geroski, P. G., & Jacquemin, A. (2013). Barriers to entry and strategic competition. Routledge.

Knittel, C. R., & Pindyck, R. S. (2016). The simple economics of commodity price

speculation. American Economic Journal: Macroeconomics, 8(2), 85-110.

Mankiw, N.G., 2016. Principles of economics. Cengage Learning.

Scitovsky, T. (2013). Welfare & Competition. Routledge.

Zeuthen, F. (2018). Problems of monopoly and economic warfare. Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.