Problems with Abandoning the Full-Deduction Rule

VerifiedAdded on 2022/08/25

|11

|2890

|20

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer A:..............................................................................................................................5

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................6

Answer D:..............................................................................................................................7

Answer E:...............................................................................................................................7

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Laws:......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................5

Answer to question 2:.................................................................................................................5

Answer A:..............................................................................................................................5

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................6

Answer D:..............................................................................................................................7

Answer E:...............................................................................................................................7

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Issues:

The issue involves ascertaining the taxability of receipts that is earned by the taxpayer

from part-time employment.

Laws:

Receipts which is linked with performance of contracts or provision of service is

characterized as payment to those that receives it. These receipts hold adequate link with

taxpayer’s income making activities (Graetz et al. 2015). As observed in “sec 6-5(1) ITA Act

97” the taxable income comprises the income which is in agreement with ordinary concepts.

When a taxpayer receives any income from revenue producing activities are held as ordinary

income. Voluntary payments which is linked to the professional activities of taxpayer is held

as ordinary income. In “Calvert v Waingwright (1947)” tips got by taxi driver were held as

taxable earnings despite the passenger did not had any obligation of paying it.

Where a person earns an income for personal service and employment it forms the

part of income from employment and service as well which may be taxable as ordinary and

statutory earnings. Receipts of salaries, wages, bonus, fees, commission that forms the

ordinary incidence of work is ordinary income (Tiley and Loutzenhiser 2014). In

“Moorhouse v Dooland (1955)” amounts that is earned by taxpayer directly or indirectly

from any personal service of taxpayer is held as ordinary earnings.

A gain which amounts to a mere gift is not held as ordinary income. Payments which

is given to employees or service givers are usually not held as income given it can be traced

to certain personal relationship which is existent among the payer and receiver rather than

any kind of provision for specific service which is given in past (Saad 2014). As noticed in

Answer to question 1:

Issues:

The issue involves ascertaining the taxability of receipts that is earned by the taxpayer

from part-time employment.

Laws:

Receipts which is linked with performance of contracts or provision of service is

characterized as payment to those that receives it. These receipts hold adequate link with

taxpayer’s income making activities (Graetz et al. 2015). As observed in “sec 6-5(1) ITA Act

97” the taxable income comprises the income which is in agreement with ordinary concepts.

When a taxpayer receives any income from revenue producing activities are held as ordinary

income. Voluntary payments which is linked to the professional activities of taxpayer is held

as ordinary income. In “Calvert v Waingwright (1947)” tips got by taxi driver were held as

taxable earnings despite the passenger did not had any obligation of paying it.

Where a person earns an income for personal service and employment it forms the

part of income from employment and service as well which may be taxable as ordinary and

statutory earnings. Receipts of salaries, wages, bonus, fees, commission that forms the

ordinary incidence of work is ordinary income (Tiley and Loutzenhiser 2014). In

“Moorhouse v Dooland (1955)” amounts that is earned by taxpayer directly or indirectly

from any personal service of taxpayer is held as ordinary earnings.

A gain which amounts to a mere gift is not held as ordinary income. Payments which

is given to employees or service givers are usually not held as income given it can be traced

to certain personal relationship which is existent among the payer and receiver rather than

any kind of provision for specific service which is given in past (Saad 2014). As noticed in

3TAXATION LAW

“Hayes v FCT (1947)” when a taxpayer receives any gift that relates to personal qualities

then it cannot be held as ordinary income. It is usually non-taxable to receiver.

As explained under “sec 66 (1) FBTAA” the FBT is commonly imposed on the

employer and not on the employee. This type of tax is normally imposed based on the

provision of fringe benefit and not upon the receipt of the benefit (Cooper, Krever and Vann

2016). “Sec 136 (1) FBTAA” says that fringe benefit involves the benefit that is given to

employee by employer when they are engaged in any employment activities. As noticed in

“Essenboourne Pty Ltd v FCT (2002)” a benefit will only be held as fringe benefit when

there is an adequate relation and material relation among the employment and provision of

benefit.

As stated by the ATO, cash gift or any other identical amounts that is received by a

taxpayer from their family members are not considered for assessment purpose while filing

tax return (Holland and Vann 2015). Usually money received as gift from a family person

that relates to personal reason and the gift does not have any connection to income producing

activities. These amounts are not taxable income and does not needs to be included in the tax

return.

Application:

Emmi in this case study is found to be student at Holmes Institute and works for part-

time only in Crown Melbourne restaurant. In the relevant income year a tips totalling $335 in

cash was received by a customer. The tips received must be treated as voluntary payments

which is linked to the professional activities of taxpayer. Referring to “Calvert v

Waingwright (1947)” tips got by Emmi should be held as ordinary income and will be

taxable under “sec 6-5 ITA Act 97”.

“Hayes v FCT (1947)” when a taxpayer receives any gift that relates to personal qualities

then it cannot be held as ordinary income. It is usually non-taxable to receiver.

As explained under “sec 66 (1) FBTAA” the FBT is commonly imposed on the

employer and not on the employee. This type of tax is normally imposed based on the

provision of fringe benefit and not upon the receipt of the benefit (Cooper, Krever and Vann

2016). “Sec 136 (1) FBTAA” says that fringe benefit involves the benefit that is given to

employee by employer when they are engaged in any employment activities. As noticed in

“Essenboourne Pty Ltd v FCT (2002)” a benefit will only be held as fringe benefit when

there is an adequate relation and material relation among the employment and provision of

benefit.

As stated by the ATO, cash gift or any other identical amounts that is received by a

taxpayer from their family members are not considered for assessment purpose while filing

tax return (Holland and Vann 2015). Usually money received as gift from a family person

that relates to personal reason and the gift does not have any connection to income producing

activities. These amounts are not taxable income and does not needs to be included in the tax

return.

Application:

Emmi in this case study is found to be student at Holmes Institute and works for part-

time only in Crown Melbourne restaurant. In the relevant income year a tips totalling $335 in

cash was received by a customer. The tips received must be treated as voluntary payments

which is linked to the professional activities of taxpayer. Referring to “Calvert v

Waingwright (1947)” tips got by Emmi should be held as ordinary income and will be

taxable under “sec 6-5 ITA Act 97”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

In the relevant income year Emmi made an income of $25,000 from her work in

Crown Melbourne Restaurants. The receipts by Emmi is related to her performance of

personal service. The income holds the adequate link with Emmi’s income making activities.

Referring to “Moorhouse v Dooland (1955)” the amount of $25,000 is characterised as

personal exertion income and holds nexus with the Emmi’s income producing activity

(Gordon et al. 2014). The amount will be included in Emmi’s taxable return and will be

chargeable under “sec 6-5 ITA Act 97” as “ordinary income”.

There was one occasion when one of Emmi’s regular customer gifted her with an

expensive perfume of $250 during the Christmas time. By citing the federal court’s

judgement in “Hayes v FCT (1947)” the gift of perfume to Emmi is related to her personal

qualities. This is because a personal relationship which is existent among the customer and

Emmi rather than any kind of provision for specific service which was given in past (Aaron

and Slemrod 2016). The gift of perfume is non-taxable to Emmi as ordinary income because

it is non-convertible to cash or money’s worth.

As Emmi was working in Crown Melbourne restaurant on part-time basis she was

given a monthly entertainment event which her employer paid. There was also a meal

expense of $380 was made by Emmi’s employer for the meal consumed by her. With respect

to “Sec 136 (1) FBTAA” the entertainment event and meal expenses paid by Crown

Melbourne restaurant for Emmi is a fringe benefit. Referring to “Essenboourne Pty Ltd v

FCT (2002)” the benefit will be held as fringe benefit for Emmi because there is an adequate

and substantial relation among the employment and provision of benefit (Lam and Whitney

2016). Under “sec 66 (1) FBTAA” Crown Melbourne restaurant, being Emmi’s employer

will be liable FBT relating to the value of benefit provided.

In the relevant income year Emmi made an income of $25,000 from her work in

Crown Melbourne Restaurants. The receipts by Emmi is related to her performance of

personal service. The income holds the adequate link with Emmi’s income making activities.

Referring to “Moorhouse v Dooland (1955)” the amount of $25,000 is characterised as

personal exertion income and holds nexus with the Emmi’s income producing activity

(Gordon et al. 2014). The amount will be included in Emmi’s taxable return and will be

chargeable under “sec 6-5 ITA Act 97” as “ordinary income”.

There was one occasion when one of Emmi’s regular customer gifted her with an

expensive perfume of $250 during the Christmas time. By citing the federal court’s

judgement in “Hayes v FCT (1947)” the gift of perfume to Emmi is related to her personal

qualities. This is because a personal relationship which is existent among the customer and

Emmi rather than any kind of provision for specific service which was given in past (Aaron

and Slemrod 2016). The gift of perfume is non-taxable to Emmi as ordinary income because

it is non-convertible to cash or money’s worth.

As Emmi was working in Crown Melbourne restaurant on part-time basis she was

given a monthly entertainment event which her employer paid. There was also a meal

expense of $380 was made by Emmi’s employer for the meal consumed by her. With respect

to “Sec 136 (1) FBTAA” the entertainment event and meal expenses paid by Crown

Melbourne restaurant for Emmi is a fringe benefit. Referring to “Essenboourne Pty Ltd v

FCT (2002)” the benefit will be held as fringe benefit for Emmi because there is an adequate

and substantial relation among the employment and provision of benefit (Lam and Whitney

2016). Under “sec 66 (1) FBTAA” Crown Melbourne restaurant, being Emmi’s employer

will be liable FBT relating to the value of benefit provided.

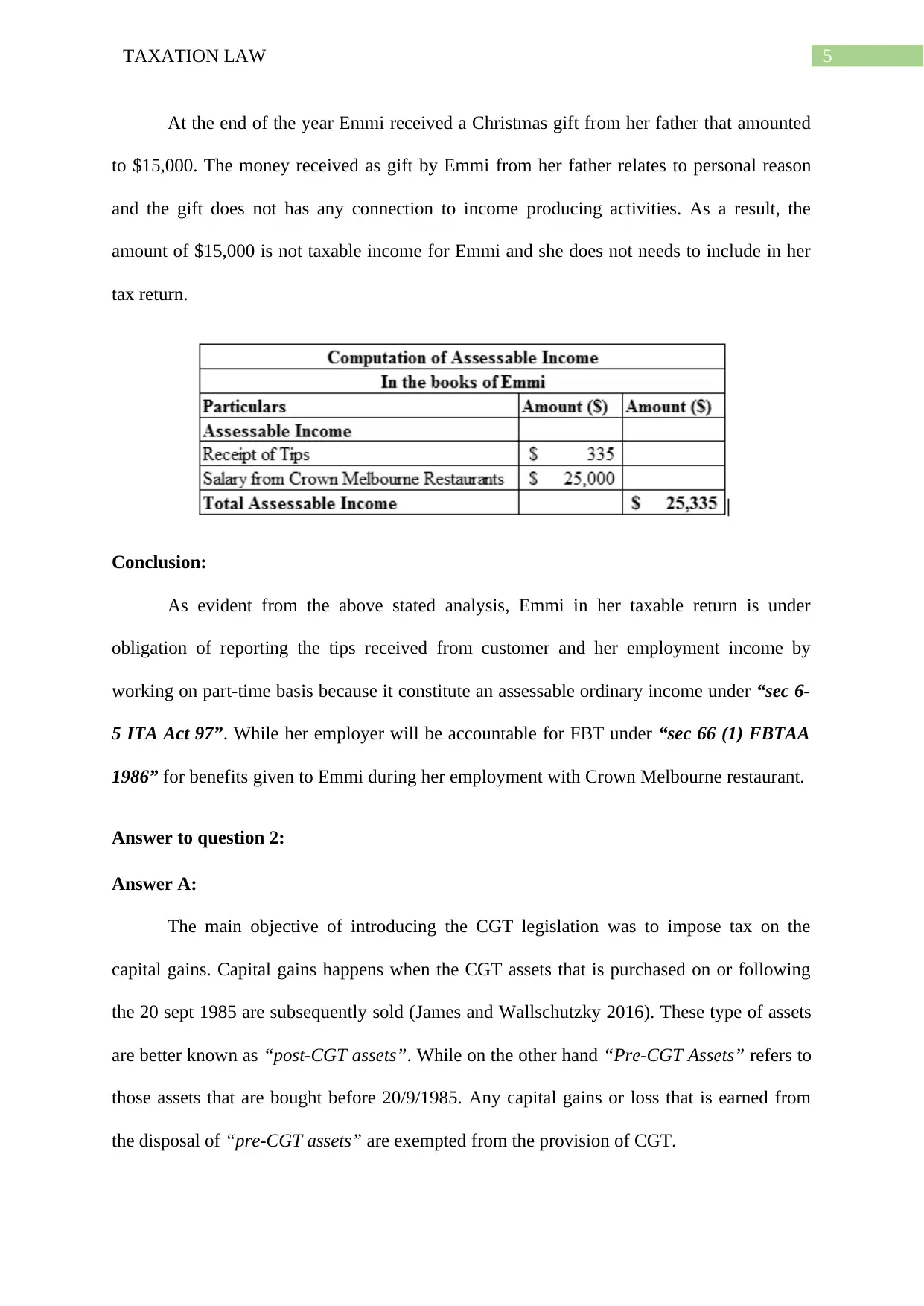

5TAXATION LAW

At the end of the year Emmi received a Christmas gift from her father that amounted

to $15,000. The money received as gift by Emmi from her father relates to personal reason

and the gift does not has any connection to income producing activities. As a result, the

amount of $15,000 is not taxable income for Emmi and she does not needs to include in her

tax return.

Conclusion:

As evident from the above stated analysis, Emmi in her taxable return is under

obligation of reporting the tips received from customer and her employment income by

working on part-time basis because it constitute an assessable ordinary income under “sec 6-

5 ITA Act 97”. While her employer will be accountable for FBT under “sec 66 (1) FBTAA

1986” for benefits given to Emmi during her employment with Crown Melbourne restaurant.

Answer to question 2:

Answer A:

The main objective of introducing the CGT legislation was to impose tax on the

capital gains. Capital gains happens when the CGT assets that is purchased on or following

the 20 sept 1985 are subsequently sold (James and Wallschutzky 2016). These type of assets

are better known as “post-CGT assets”. While on the other hand “Pre-CGT Assets” refers to

those assets that are bought before 20/9/1985. Any capital gains or loss that is earned from

the disposal of “pre-CGT assets” are exempted from the provision of CGT.

At the end of the year Emmi received a Christmas gift from her father that amounted

to $15,000. The money received as gift by Emmi from her father relates to personal reason

and the gift does not has any connection to income producing activities. As a result, the

amount of $15,000 is not taxable income for Emmi and she does not needs to include in her

tax return.

Conclusion:

As evident from the above stated analysis, Emmi in her taxable return is under

obligation of reporting the tips received from customer and her employment income by

working on part-time basis because it constitute an assessable ordinary income under “sec 6-

5 ITA Act 97”. While her employer will be accountable for FBT under “sec 66 (1) FBTAA

1986” for benefits given to Emmi during her employment with Crown Melbourne restaurant.

Answer to question 2:

Answer A:

The main objective of introducing the CGT legislation was to impose tax on the

capital gains. Capital gains happens when the CGT assets that is purchased on or following

the 20 sept 1985 are subsequently sold (James and Wallschutzky 2016). These type of assets

are better known as “post-CGT assets”. While on the other hand “Pre-CGT Assets” refers to

those assets that are bought before 20/9/1985. Any capital gains or loss that is earned from

the disposal of “pre-CGT assets” are exempted from the provision of CGT.

6TAXATION LAW

Liu in the relevant tax year disposes her main residence that she has held under her

ownership all through the period. Liu took the decision of selling the house for a market

value of $630,000 and the purchase value of the house in 1981 was $55,000. The main

residence of Liu must be classified as “pre-CGT asset”. Liu had bought the house in 1981

and this means that the property was purchased before the introduction of CGT regime.

Consequently, no taxes will be imposed on capital gains because it is an exempted property.

Answer B:

An explanation regarding the personal use asset is given in “subdivision 108C”.

Denoting the explanation given in “sec 108-20 (2) & (3)” personal use asset namely consists

of furniture, household items, electronic goods, motor vehicles, boats etc. that is kept under

the possession for private use of an individual (Aprill 2019). An important rule of “sec 108-

20 (1)” relating to personal use asset explains that any losses suffered from selling these type

of asset is basically ignored.

Liu in the relevant year has decided to sell a car. Liu sells the car for $8,000 but the

actual cost of car stood $37,000. Denoting the definition that is given in the “sec 108-20 (2)

& (3)” the car is referred as “personal use asset”. This is because Liu used the car primarily

for her private purpose. It is apparent that when Liu sold the car she suffered a capital loss

(Pu et al., 2019). Mentioning the special rules given in “sec 108-20 (1)” relating to personal

use asset, the capital loss suffered by Liu should be simply disregarded.

Answer C:

As given in the “Div 152” relief in the form of concession is given to small

businesses. There are certain important criteria for availing the concessions (Viswanathan

2019). This involves;

Liu in the relevant tax year disposes her main residence that she has held under her

ownership all through the period. Liu took the decision of selling the house for a market

value of $630,000 and the purchase value of the house in 1981 was $55,000. The main

residence of Liu must be classified as “pre-CGT asset”. Liu had bought the house in 1981

and this means that the property was purchased before the introduction of CGT regime.

Consequently, no taxes will be imposed on capital gains because it is an exempted property.

Answer B:

An explanation regarding the personal use asset is given in “subdivision 108C”.

Denoting the explanation given in “sec 108-20 (2) & (3)” personal use asset namely consists

of furniture, household items, electronic goods, motor vehicles, boats etc. that is kept under

the possession for private use of an individual (Aprill 2019). An important rule of “sec 108-

20 (1)” relating to personal use asset explains that any losses suffered from selling these type

of asset is basically ignored.

Liu in the relevant year has decided to sell a car. Liu sells the car for $8,000 but the

actual cost of car stood $37,000. Denoting the definition that is given in the “sec 108-20 (2)

& (3)” the car is referred as “personal use asset”. This is because Liu used the car primarily

for her private purpose. It is apparent that when Liu sold the car she suffered a capital loss

(Pu et al., 2019). Mentioning the special rules given in “sec 108-20 (1)” relating to personal

use asset, the capital loss suffered by Liu should be simply disregarded.

Answer C:

As given in the “Div 152” relief in the form of concession is given to small

businesses. There are certain important criteria for availing the concessions (Viswanathan

2019). This involves;

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

a. On finding that the business has the net value of asset is inside the $6 million or the

total business revenue is not greater than $10 million then it will be categorized as

“small business entity”.

b. The CGT asset that is possessed by the company must be categorized as active asset.

On meeting the above criteria there are four types of concession that is available to

the small businesses;

a. “15-year exemption” from the CGT when it is noticed that the asset has been owned

for 15-years and the age of taxpayer is 55 years or greater than that.

b. “50% reduction” is given to the taxpayer that qualifies the conditions following the

general application of 50% discount (Siebert 2019).

c. “Retirement concessions” is provided to the taxpayer when it is found that capital

gains made from sale of CGT asset is used for retirement purpose and the proceeds is

not more than $500,000.

d. “Roll-over relief” is given when a replacement asset is acquired by the taxpayer

The case of Liu highlights that she was carrying the photography business and as she

is moving to China she decides to retire from her business. She eventually sells the business

for $125,000 with photography equipment fetching her $53,000 and the goodwill fetching her

$50,000 (De Villiers 2019). Liu is eligible for availing small business entity concession

because the value of her net asset is not more than $6 million. As she has met the eligibility

criteria she can avail retirement concession because the value of her capital stands $125,000

which is under the limit of $500,000.

Answer D:

As per the special rule that is given for personal use asset in “sec 118-10”, any capital

gain that is made from selling the asset having a purchase cost of not more than $10,000 is

a. On finding that the business has the net value of asset is inside the $6 million or the

total business revenue is not greater than $10 million then it will be categorized as

“small business entity”.

b. The CGT asset that is possessed by the company must be categorized as active asset.

On meeting the above criteria there are four types of concession that is available to

the small businesses;

a. “15-year exemption” from the CGT when it is noticed that the asset has been owned

for 15-years and the age of taxpayer is 55 years or greater than that.

b. “50% reduction” is given to the taxpayer that qualifies the conditions following the

general application of 50% discount (Siebert 2019).

c. “Retirement concessions” is provided to the taxpayer when it is found that capital

gains made from sale of CGT asset is used for retirement purpose and the proceeds is

not more than $500,000.

d. “Roll-over relief” is given when a replacement asset is acquired by the taxpayer

The case of Liu highlights that she was carrying the photography business and as she

is moving to China she decides to retire from her business. She eventually sells the business

for $125,000 with photography equipment fetching her $53,000 and the goodwill fetching her

$50,000 (De Villiers 2019). Liu is eligible for availing small business entity concession

because the value of her net asset is not more than $6 million. As she has met the eligibility

criteria she can avail retirement concession because the value of her capital stands $125,000

which is under the limit of $500,000.

Answer D:

As per the special rule that is given for personal use asset in “sec 118-10”, any capital

gain that is made from selling the asset having a purchase cost of not more than $10,000 is

8TAXATION LAW

simply required to be ignored (Hoynes 2019). Accordingly, Liu in the relevant income year

reports the sale of painting for $4,800. The cost price of painting was not more than $2,000.

So the capital gains made by Liu from selling the painting must be simply ignored because

the cost of asset is not more than $10,000 and fails to meet the first element cost base given

under “sec 118-10”.

Answer E:

An explanation regarding the collectable is given in “subdivision 108B”. As noticed

in “sec 108-10 (2) & (3)” assets which the taxpayer has kept for private use is known as

collectable. Namely assets such as paintings, sculptures, jewellery, stamps, coins and antiques

is examples of collectables (Cohen and Viswanathan 2019). The special rule that is explained

in “sec 118-10 (1)” says that capital gain or loss for collectable purchased for $500 or less is

ignored.

In the relevant year, Liu sold all her paintings for a sales proceeds of $28,000. She has

purchased all the paintings with a cost base of $500 only. Referring to the special rules of

“sec 118-10 (1)” the capital gains from painting made by Liu must be ignored because the

cost of painting is not more than $500.

Apart from this, there was one painting which Liu had purchased from an artist

directly for $1,000 but sold it for $8,000. As a result the cost base of painting is more than

$500 and the sale of painting has resulted in capital gains for Liu. As there is a capital gains

earned from disposing the painting, Liu is required to denote that the gains will attract tax

liability within the legislative provision of “sec 102-5”.

simply required to be ignored (Hoynes 2019). Accordingly, Liu in the relevant income year

reports the sale of painting for $4,800. The cost price of painting was not more than $2,000.

So the capital gains made by Liu from selling the painting must be simply ignored because

the cost of asset is not more than $10,000 and fails to meet the first element cost base given

under “sec 118-10”.

Answer E:

An explanation regarding the collectable is given in “subdivision 108B”. As noticed

in “sec 108-10 (2) & (3)” assets which the taxpayer has kept for private use is known as

collectable. Namely assets such as paintings, sculptures, jewellery, stamps, coins and antiques

is examples of collectables (Cohen and Viswanathan 2019). The special rule that is explained

in “sec 118-10 (1)” says that capital gain or loss for collectable purchased for $500 or less is

ignored.

In the relevant year, Liu sold all her paintings for a sales proceeds of $28,000. She has

purchased all the paintings with a cost base of $500 only. Referring to the special rules of

“sec 118-10 (1)” the capital gains from painting made by Liu must be ignored because the

cost of painting is not more than $500.

Apart from this, there was one painting which Liu had purchased from an artist

directly for $1,000 but sold it for $8,000. As a result the cost base of painting is more than

$500 and the sale of painting has resulted in capital gains for Liu. As there is a capital gains

earned from disposing the painting, Liu is required to denote that the gains will attract tax

liability within the legislative provision of “sec 102-5”.

9TAXATION LAW

References:

Aaron, H. and Slemrod, J. eds., 2016. The crisis in tax administration. Brookings Institution

Press.

Aprill, E.P., 2019. A Tax Lesson for Election Law.

Cohen, N. and Viswanathan, M., 2019. Corporate Behavior and the Tax Cuts and Jobs

Act. Available at SSRN 3449860.

Cooper, G., Krever, R. and Vann, R., 2016. Income taxation commentary and materials.

Australian Tax Practice (ATP).

De Villiers, M., 2019. Tax avoidance eliminated by piercing the corporate veil: tax

law. Without Prejudice, 19(10), pp.39-40.

Gordon, R., Kalambokidis, L., Rohaly, J. and Slemrod, J., 2014. Toward a consumption tax,

and beyond. American Economic Review, 94(2), pp.161-165.

Graetz, M., Schenk, D., Freeland, J., Lathrope, D., Lind, S., Stephens, R., Burke, K., Brealey,

R., Myers, S., Allen, F. and Keyes, K., 2015. Federal Income Taxation, Principles and

Policies (University Casebook Series). Foundation Press/West Academic.

Holland, D. and Vann, R.J., 2015. Income tax incentives for investment. Tax law design and

drafting, 2, pp.2-9.

Hoynes, H., 2019. The Earned Income Tax Credit. The ANNALS of the American Academy of

Political and Social Science, 686(1), pp.180-203.

James, S. and Wallschutzky, I., 2016. Tax law improvement in Australia and the UK: the

need for a strategy for simplification. Fiscal Studies, 18(4), pp.445-460.

References:

Aaron, H. and Slemrod, J. eds., 2016. The crisis in tax administration. Brookings Institution

Press.

Aprill, E.P., 2019. A Tax Lesson for Election Law.

Cohen, N. and Viswanathan, M., 2019. Corporate Behavior and the Tax Cuts and Jobs

Act. Available at SSRN 3449860.

Cooper, G., Krever, R. and Vann, R., 2016. Income taxation commentary and materials.

Australian Tax Practice (ATP).

De Villiers, M., 2019. Tax avoidance eliminated by piercing the corporate veil: tax

law. Without Prejudice, 19(10), pp.39-40.

Gordon, R., Kalambokidis, L., Rohaly, J. and Slemrod, J., 2014. Toward a consumption tax,

and beyond. American Economic Review, 94(2), pp.161-165.

Graetz, M., Schenk, D., Freeland, J., Lathrope, D., Lind, S., Stephens, R., Burke, K., Brealey,

R., Myers, S., Allen, F. and Keyes, K., 2015. Federal Income Taxation, Principles and

Policies (University Casebook Series). Foundation Press/West Academic.

Holland, D. and Vann, R.J., 2015. Income tax incentives for investment. Tax law design and

drafting, 2, pp.2-9.

Hoynes, H., 2019. The Earned Income Tax Credit. The ANNALS of the American Academy of

Political and Social Science, 686(1), pp.180-203.

James, S. and Wallschutzky, I., 2016. Tax law improvement in Australia and the UK: the

need for a strategy for simplification. Fiscal Studies, 18(4), pp.445-460.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

Pu, Y., Liu, C., Chen, X., Cheng, Y. and Wang, J., 2019, December. Tax Treatment of

Employee Benefits. In 5th International Conference on Economics, Management, Law and

Education (EMLE 2019) (pp. 997-998). Atlantis Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Siebert, H., 2019. Reforming capital income taxation. Routledge.

Tiley, J. and Loutzenhiser, G., 2014. Revenue Law: Introduction to UK tax law; Income tax;

Capital gains tax; Inheritance tax. Bloomsbury Publishing.

Viswanathan, M., 2019. Tax Law: Problems with Abandoning the Full-Deduction Rule. The

Judges' Book, 3(1), p.16.

Pu, Y., Liu, C., Chen, X., Cheng, Y. and Wang, J., 2019, December. Tax Treatment of

Employee Benefits. In 5th International Conference on Economics, Management, Law and

Education (EMLE 2019) (pp. 997-998). Atlantis Press.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Siebert, H., 2019. Reforming capital income taxation. Routledge.

Tiley, J. and Loutzenhiser, G., 2014. Revenue Law: Introduction to UK tax law; Income tax;

Capital gains tax; Inheritance tax. Bloomsbury Publishing.

Viswanathan, M., 2019. Tax Law: Problems with Abandoning the Full-Deduction Rule. The

Judges' Book, 3(1), p.16.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.