Valuation Report: Bridgeford Street Enterprises Ltd - PLAN41031

VerifiedAdded on 2022/09/05

|15

|3917

|36

Report

AI Summary

This report provides a comprehensive valuation analysis for Bridgeford Street Enterprises Ltd, focusing on a property in Manchester City. The primary objective is to determine the market value of a building the company intends to purchase. The valuation utilizes the sales approach, examining comparable properties to establish a fair market value. The report explores factors affecting all-risk yields and market rents, including demographics, interest rates, and economic conditions. It also addresses the uncertainty associated with the valuation process, acknowledging the limitations of the market approach and the impact of economic instability and government policies. The analysis incorporates discussions on the G20 declaration on strengthening the financial system and the guidelines from the Basel Committee on Banking Supervision regarding the assessment of fair value, emphasizing the need to consider uncertainties and liquidity premiums in valuation methodologies.

Running head: VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 1

Valuation for Bridgeford Street Enterprises Ltd.

Student’s Name

Institutional Affiliation

Valuation for Bridgeford Street Enterprises Ltd.

Student’s Name

Institutional Affiliation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 2

Introduction

The office is situated in Manchester City. The property in which the office is located at

Bridgeford Street in Manchester City. The primary purpose of the valuation of this property is to

establish the market value of the property they propose to purchase to occupy for the business.

The office is situated in a large complex which contains five other similar offices. All the

partition categories of this building are identical in size and design. For example, all offices have

similar dimensions and plans. The building contains twelve offices, eight visitor rooms, five

executive rooms, and four rooms set for operations and maintenance.

The valuation method I would utilize in valuing the building is the sales approach. This

method is also referred to as the market approach. It relies heavily on the most updated sales data

from the comparable properties, for example, other office buildings within the Manchester City.

Bridgeford Street Enterprises Ltd would ascertain the fair market value of the premises situated

within the city to know the estimated market value of the entire building and not just an office.

The method is applicable because it does not have multiple drawbacks, unlike other methods.

The Factors Affecting the All Risk Yields and Market Rents for this Property

The All Risk Yield is a metric used to evaluate the capital value of an investment. It

comprises both net and gross yields. It is utilized when determining the probable risks of an

investment. The metric is also used to assess the market value of a property. ARY is computed

by dividing annual rental income by the value of the property and multiply the results by 100%

(Shapiro, Mackmin & Sams, 2019).

Demographics

Demographics refers to the composition of the population, such as gender, income, age,

race population growth as well as patterns of migration (Shapiro, Mackmin & Sams, 2019).

Introduction

The office is situated in Manchester City. The property in which the office is located at

Bridgeford Street in Manchester City. The primary purpose of the valuation of this property is to

establish the market value of the property they propose to purchase to occupy for the business.

The office is situated in a large complex which contains five other similar offices. All the

partition categories of this building are identical in size and design. For example, all offices have

similar dimensions and plans. The building contains twelve offices, eight visitor rooms, five

executive rooms, and four rooms set for operations and maintenance.

The valuation method I would utilize in valuing the building is the sales approach. This

method is also referred to as the market approach. It relies heavily on the most updated sales data

from the comparable properties, for example, other office buildings within the Manchester City.

Bridgeford Street Enterprises Ltd would ascertain the fair market value of the premises situated

within the city to know the estimated market value of the entire building and not just an office.

The method is applicable because it does not have multiple drawbacks, unlike other methods.

The Factors Affecting the All Risk Yields and Market Rents for this Property

The All Risk Yield is a metric used to evaluate the capital value of an investment. It

comprises both net and gross yields. It is utilized when determining the probable risks of an

investment. The metric is also used to assess the market value of a property. ARY is computed

by dividing annual rental income by the value of the property and multiply the results by 100%

(Shapiro, Mackmin & Sams, 2019).

Demographics

Demographics refers to the composition of the population, such as gender, income, age,

race population growth as well as patterns of migration (Shapiro, Mackmin & Sams, 2019).

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 3

These factors are vital when it comes to the determination of real estate or property. Significant

shifts in the demographic status of a country have a massive impact on the trend in the value of

the property located within a specific area.

Therefore, the market rent for the property would be affected by various factors affecting

the demand for properties in Manchester City. In the recent period, there has been a massive

influx of small and medium scale investors in the city. This situation has resulted in rising in

demand for properties, leading to an upward shift in prices. Therefore, the market prices for the

rental offices current is almost double the amount that was charged ten years ago. If demand

continues to rise, the price would probably rice higher in the future.

Interest Rate

The interest rates usually have a high impact on the value of the property. If Bridgeford

Street in Manchester wants to utilize a mortgage to purchase the office, it has to consider the cost

of the loan. The cost of the loan is highly dependent on the interest rate. If the interest rate is low,

then the cost of borrowing is small. A mortgage with a low price is desired because the firm

would service it quickly (Shapiro, Mackmin & Sams, 2019). However, the loan with a high-

interest rate is expensive. Therefore, the firm has to inquire about the current interest rates so that

it can come up with an informed decision on how to service the loan. Also, in case the cost of

building the complex was high because of high bank rates, the rental rates are likely to be

elevated to cover these costs.

The Economy

The overall health of the economy affects the value of a property to a great extent. This

factor can be measured using economic indicators like the gross domestic income of a country,

unemployment report, price of commodities, and the current manufacturing activities. Even

These factors are vital when it comes to the determination of real estate or property. Significant

shifts in the demographic status of a country have a massive impact on the trend in the value of

the property located within a specific area.

Therefore, the market rent for the property would be affected by various factors affecting

the demand for properties in Manchester City. In the recent period, there has been a massive

influx of small and medium scale investors in the city. This situation has resulted in rising in

demand for properties, leading to an upward shift in prices. Therefore, the market prices for the

rental offices current is almost double the amount that was charged ten years ago. If demand

continues to rise, the price would probably rice higher in the future.

Interest Rate

The interest rates usually have a high impact on the value of the property. If Bridgeford

Street in Manchester wants to utilize a mortgage to purchase the office, it has to consider the cost

of the loan. The cost of the loan is highly dependent on the interest rate. If the interest rate is low,

then the cost of borrowing is small. A mortgage with a low price is desired because the firm

would service it quickly (Shapiro, Mackmin & Sams, 2019). However, the loan with a high-

interest rate is expensive. Therefore, the firm has to inquire about the current interest rates so that

it can come up with an informed decision on how to service the loan. Also, in case the cost of

building the complex was high because of high bank rates, the rental rates are likely to be

elevated to cover these costs.

The Economy

The overall health of the economy affects the value of a property to a great extent. This

factor can be measured using economic indicators like the gross domestic income of a country,

unemployment report, price of commodities, and the current manufacturing activities. Even

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 4

though offices are not affected by the economic downturn because of the longer term of the

lease, purchasing a full building would be primarily affected by the financial status of the

country.

Government Policy or Subsidies

Government policies have a sizeable impact on property prices. Government with good

policies like tax credits, grants, and deductions can temporarily impact the value of the property

positively. The company would pay less to acquire the property if the government subsidies the

construction of such premises (Shapiro, Mackmin & Sams, 2019). Also, grants boost real estate

companies to construct more houses. The increase in the supply of buildings leads to a reduction

in demand, resulting in lower prices. Therefore, government policies would principally

determine the market value of the buildings situated in Manchester City.

The Uncertainty Associated With My Valuation

The market approach has various downsides or difficulties, just like any other approach.

Sometimes even though there are known and recent transactions in the market, the properties

may not be identical to the current building. Probably, the other transactions involved buildings

of different sizes, shapes, or different locations, which are valued based on land prices and cost

of construction in such areas. One may not be sure whether he would get a completely identical

property sold in the recent period to compare with. This situation makes the market approach

method complex.

In addition, the method can lead to a significantly large error in the amount of the value

of the object. The fact is that assessing the building's market value at the end of the forecast

period is much more difficult than assessing its building at the date of the assessment, since there

is no reliable basis for this. Therefore, the forecast of the reverse value of the object is very

though offices are not affected by the economic downturn because of the longer term of the

lease, purchasing a full building would be primarily affected by the financial status of the

country.

Government Policy or Subsidies

Government policies have a sizeable impact on property prices. Government with good

policies like tax credits, grants, and deductions can temporarily impact the value of the property

positively. The company would pay less to acquire the property if the government subsidies the

construction of such premises (Shapiro, Mackmin & Sams, 2019). Also, grants boost real estate

companies to construct more houses. The increase in the supply of buildings leads to a reduction

in demand, resulting in lower prices. Therefore, government policies would principally

determine the market value of the buildings situated in Manchester City.

The Uncertainty Associated With My Valuation

The market approach has various downsides or difficulties, just like any other approach.

Sometimes even though there are known and recent transactions in the market, the properties

may not be identical to the current building. Probably, the other transactions involved buildings

of different sizes, shapes, or different locations, which are valued based on land prices and cost

of construction in such areas. One may not be sure whether he would get a completely identical

property sold in the recent period to compare with. This situation makes the market approach

method complex.

In addition, the method can lead to a significantly large error in the amount of the value

of the object. The fact is that assessing the building's market value at the end of the forecast

period is much more difficult than assessing its building at the date of the assessment, since there

is no reliable basis for this. Therefore, the forecast of the reverse value of the object is very

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 5

inaccurate. With a short duration of the forecast period, the share of this component in the value

of the object reaches 75-95%, which can lead to serious errors in the assessment of the market

value of the property.

The G20 Declaration on Strengthening the Financial System, published in April 2009,

called for improved standards to reflect uncertainties in determining fair value. The reason for

the increased attention to this problem from the leading countries of the world was the report

presented by the Forum on Financial Stability in Markets, which noted that the result of any

methods of assessing market value is always accompanied by some inevitable uncertainty that

must be realized in order not to create market participants have the false impression that the cost

is determined exactly (Taub, 2009).

At the same Forum, which took place in the context of the crisis that began (2008), it was

noted that well-known approaches to valuation (primarily comparative) are based on data on

sales of objects in an active market comparable to the valuation object. However, during market

turmoil (we are talking about the 2008 crisis), due to the lack of demand and active trading

activity, the liquidity of many assets decreased. It became clear that even for facilities whose

quality was maintained the same, in a crisis, market participants demand a liquidity premium,

which has become significantly higher than in the years preceding the crisis. (Note that the

requirement of a premium for low liquidity reduces the cost of low liquid real estate.) In this

regard, according to the authors of this document, when markets cease to be active, Other

evaluation methods, in particular modeling methods, are required. The need to account for

liquidity premiums has become a serious problem in real estate valuation and a significant

additional factor in the uncertainty of the valuation result, therefore, the document emphasizes

the importance of finding ways to establish the degree of such uncertainty. This is important so

inaccurate. With a short duration of the forecast period, the share of this component in the value

of the object reaches 75-95%, which can lead to serious errors in the assessment of the market

value of the property.

The G20 Declaration on Strengthening the Financial System, published in April 2009,

called for improved standards to reflect uncertainties in determining fair value. The reason for

the increased attention to this problem from the leading countries of the world was the report

presented by the Forum on Financial Stability in Markets, which noted that the result of any

methods of assessing market value is always accompanied by some inevitable uncertainty that

must be realized in order not to create market participants have the false impression that the cost

is determined exactly (Taub, 2009).

At the same Forum, which took place in the context of the crisis that began (2008), it was

noted that well-known approaches to valuation (primarily comparative) are based on data on

sales of objects in an active market comparable to the valuation object. However, during market

turmoil (we are talking about the 2008 crisis), due to the lack of demand and active trading

activity, the liquidity of many assets decreased. It became clear that even for facilities whose

quality was maintained the same, in a crisis, market participants demand a liquidity premium,

which has become significantly higher than in the years preceding the crisis. (Note that the

requirement of a premium for low liquidity reduces the cost of low liquid real estate.) In this

regard, according to the authors of this document, when markets cease to be active, Other

evaluation methods, in particular modeling methods, are required. The need to account for

liquidity premiums has become a serious problem in real estate valuation and a significant

additional factor in the uncertainty of the valuation result, therefore, the document emphasizes

the importance of finding ways to establish the degree of such uncertainty. This is important so

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 6

as not to give a false impression of the accuracy of the evaluation result in order to protect

market participants from a false sense of security. At the same time, a correctly performed

modeling process does not remove uncertainty, but helps to understand and manage complex

risks, as well as analyze their consequences. therefore, the paper notes the importance of finding

ways to ascertain the degree of such uncertainty. This is important so as not to give a false

impression of the accuracy of the evaluation result in order to protect market participants from a

false sense of security. At the same time, a correctly performed modeling process does not

remove uncertainty, but helps to understand and manage complex risks, as well as analyze their

consequences. therefore, the paper notes the importance of finding ways to ascertain the degree

of such uncertainty. This is important so as not to give a false impression of the accuracy of the

evaluation result in order to protect market participants from a false sense of security. At the

same time, a correctly performed modeling process does not remove uncertainty, but helps to

understand and manage complex risks, as well as analyze their consequences.

The Guide prepared by the Basel Committee in 2009 indicates that the uncertainty

associated with determining the fair value of a financial instrument should be considered as an

integral characteristic of the valuation process (Basel Committee Banking Supervision, 2009).

Moreover, as the factors determining the existence of this uncertainty, the same document

indicates both the characteristics of the asset itself and the characteristics of the trading

environment, primarily the level of market activity that affects its liquidity. The document under

discussion noted that there is a close relationship between the level of uncertainty of the

valuation result and the financial risks associated with specific assets. In other words, the

uncertainty of the assessment result provokes the risk associated with the adoption of decisions

based on the assessment results.

as not to give a false impression of the accuracy of the evaluation result in order to protect

market participants from a false sense of security. At the same time, a correctly performed

modeling process does not remove uncertainty, but helps to understand and manage complex

risks, as well as analyze their consequences. therefore, the paper notes the importance of finding

ways to ascertain the degree of such uncertainty. This is important so as not to give a false

impression of the accuracy of the evaluation result in order to protect market participants from a

false sense of security. At the same time, a correctly performed modeling process does not

remove uncertainty, but helps to understand and manage complex risks, as well as analyze their

consequences. therefore, the paper notes the importance of finding ways to ascertain the degree

of such uncertainty. This is important so as not to give a false impression of the accuracy of the

evaluation result in order to protect market participants from a false sense of security. At the

same time, a correctly performed modeling process does not remove uncertainty, but helps to

understand and manage complex risks, as well as analyze their consequences.

The Guide prepared by the Basel Committee in 2009 indicates that the uncertainty

associated with determining the fair value of a financial instrument should be considered as an

integral characteristic of the valuation process (Basel Committee Banking Supervision, 2009).

Moreover, as the factors determining the existence of this uncertainty, the same document

indicates both the characteristics of the asset itself and the characteristics of the trading

environment, primarily the level of market activity that affects its liquidity. The document under

discussion noted that there is a close relationship between the level of uncertainty of the

valuation result and the financial risks associated with specific assets. In other words, the

uncertainty of the assessment result provokes the risk associated with the adoption of decisions

based on the assessment results.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 7

Given the importance of accounting for estimation uncertainties, this paper states that

further work is needed to describe the estimation uncertainty. It also states that the Basel

Committee plans to issue a Guide aimed at improving the reliability of estimates. In addition to

general recommendations for improving the reliability of estimates, this Guideline should

include recommendations for accounting for liquidity when establishing the level of uncertainty

in the results of estimates (IASB 2009). Particularly important is the recommendation to the

bodies that control the work of the bank, without fail to identify uncertainties for all assets. This

requires a methodology that could provide not only a qualitative analysis of the degree of

estimation uncertainty, but also a determination of its level in a quantitative form. Qualitative

and quantitative estimates of the level of uncertainty should be included in the assessment reports

, as well as in general reports containing risk analysis of the credit institution as a whole. It is

very important that this information is taken into account by the relevant structures that make

investment decisions and manage risks, including senior management and advice (Lefebvre,

Simonova and Scarlat, 2009).

The subject of measurement uncertainty has occupied an important place in the work of

the Council on International Financial Reporting Standards (IASB). In 2009, the Council began

work on draft ED / 2009/5, which outlined the conceptual framework for measuring fair value

(Johnson, 2009). According to this project, to determine the fair value of assets, it is assumed to

use valuation methods adopted in valuation practice to determine their market value, that is,

methods within one of three approaches - comparative (market), profitable or costly (property).

These and other refinements bring the concept of "fair value" closer to the concept of "market

value", therefore, when discussing the uncertainty of assessing market value, it is useful to

Given the importance of accounting for estimation uncertainties, this paper states that

further work is needed to describe the estimation uncertainty. It also states that the Basel

Committee plans to issue a Guide aimed at improving the reliability of estimates. In addition to

general recommendations for improving the reliability of estimates, this Guideline should

include recommendations for accounting for liquidity when establishing the level of uncertainty

in the results of estimates (IASB 2009). Particularly important is the recommendation to the

bodies that control the work of the bank, without fail to identify uncertainties for all assets. This

requires a methodology that could provide not only a qualitative analysis of the degree of

estimation uncertainty, but also a determination of its level in a quantitative form. Qualitative

and quantitative estimates of the level of uncertainty should be included in the assessment reports

, as well as in general reports containing risk analysis of the credit institution as a whole. It is

very important that this information is taken into account by the relevant structures that make

investment decisions and manage risks, including senior management and advice (Lefebvre,

Simonova and Scarlat, 2009).

The subject of measurement uncertainty has occupied an important place in the work of

the Council on International Financial Reporting Standards (IASB). In 2009, the Council began

work on draft ED / 2009/5, which outlined the conceptual framework for measuring fair value

(Johnson, 2009). According to this project, to determine the fair value of assets, it is assumed to

use valuation methods adopted in valuation practice to determine their market value, that is,

methods within one of three approaches - comparative (market), profitable or costly (property).

These and other refinements bring the concept of "fair value" closer to the concept of "market

value", therefore, when discussing the uncertainty of assessing market value, it is useful to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 8

familiarize yourself with the position of the International Council on Accounting Standards

(International Accounting Standards Board 2009).

Work on a document on the conceptual framework for measuring fair value was

completed by the development and entry into force in 2013 of the International Standard for

Financial Reporting (IFRS 13) “Measurement of Fair Value”.

The position of the International Council on Accounting Standards regarding the

disclosure of uncertainties in determining fair value is sufficiently clear in the draft standard

“Report on the analysis of the error in determining (measuring) fair value (ED / 2010/7), sent for

discussion to interested organizations.

As follows from this project, the International Accounting Standards Board and the

Financial Accounting Standards Board have made a preliminary decision to require companies to

conduct an uncertainty analysis for fair value measurements that are classified as part of level 3

of the fair value hierarchy, and apply valuation techniques based on unobserved market data.

Thus, in accordance with this project, the uncertainty analysis is primarily subject to fair value

measurements associated with a high level of uncertainty due to the lack of market data on actual

transactions.

In addition, this document states that when calculating the value of an asset, other issues

should be reflected that are directly related to the uncertainty of the valuation, in particular, the

liquidity of the valued asset, as well as expectations of possible changes in the amount or timing

of future cash flows that the company expects to receive from the asset (Financial Accounting

Standards Board 2009).

familiarize yourself with the position of the International Council on Accounting Standards

(International Accounting Standards Board 2009).

Work on a document on the conceptual framework for measuring fair value was

completed by the development and entry into force in 2013 of the International Standard for

Financial Reporting (IFRS 13) “Measurement of Fair Value”.

The position of the International Council on Accounting Standards regarding the

disclosure of uncertainties in determining fair value is sufficiently clear in the draft standard

“Report on the analysis of the error in determining (measuring) fair value (ED / 2010/7), sent for

discussion to interested organizations.

As follows from this project, the International Accounting Standards Board and the

Financial Accounting Standards Board have made a preliminary decision to require companies to

conduct an uncertainty analysis for fair value measurements that are classified as part of level 3

of the fair value hierarchy, and apply valuation techniques based on unobserved market data.

Thus, in accordance with this project, the uncertainty analysis is primarily subject to fair value

measurements associated with a high level of uncertainty due to the lack of market data on actual

transactions.

In addition, this document states that when calculating the value of an asset, other issues

should be reflected that are directly related to the uncertainty of the valuation, in particular, the

liquidity of the valued asset, as well as expectations of possible changes in the amount or timing

of future cash flows that the company expects to receive from the asset (Financial Accounting

Standards Board 2009).

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD 9

When discussing the uncertainty of determining fair value for accounting purposes, it is

necessary to mention the new concept of confidence (confidence), proposed in a joint document

of the Association of Chartered Certified Accountants (ACCA), Royal Institute securities,

investment and finance (the Chartered Institute for Securities & Investmentand Long Finance -

CISI) and the organization "Long Money" (Long Finance). By fiduciary accounting, the authors

of this concept understand the accounting method, according to which the numerical values

appearing in the balance sheet, profit and loss statement and cash flow statement, should be

expressed not by point (discrete) values, but by probability distributions. It should be noted that

the term confidence accounting, which we translated as "trust accounting" (similar to the term

confidence interval) was introduced in 2000 to replace, as we see it, the more understandable

term - "probabilistic accounting" (Jensen, 2009).

The proposed concept of fiduciary accounting reflects the position of the authors of the

concept that accounting based only on point (discrete) values of the value of assets and liabilities

is insufficient for an objective assessment of the financial condition of the company and the

associated uncertainties and risks (Platin et al 2007). The paper notes that there are many

potential sources of uncertainty in the value of assets and liabilities that make it impossible to

accurately determine “true value”. This problem resembles a similar measurement error problem.

In this regard, within the framework of the proposed accounting, all lines of the balance sheet

and the profit and loss statement are proposed to be kept in the form of probability distributions.

Histograms or confidence intervals can also be used (Novoa et al 2009).

To sum up, uncertainty is based on the probabilistic nature of the market. The fact is that

even transactions with identical and completely replaceable assets, carried out at the same time

and under the same conditions, can be carried out at different prices. In this case, price variability

When discussing the uncertainty of determining fair value for accounting purposes, it is

necessary to mention the new concept of confidence (confidence), proposed in a joint document

of the Association of Chartered Certified Accountants (ACCA), Royal Institute securities,

investment and finance (the Chartered Institute for Securities & Investmentand Long Finance -

CISI) and the organization "Long Money" (Long Finance). By fiduciary accounting, the authors

of this concept understand the accounting method, according to which the numerical values

appearing in the balance sheet, profit and loss statement and cash flow statement, should be

expressed not by point (discrete) values, but by probability distributions. It should be noted that

the term confidence accounting, which we translated as "trust accounting" (similar to the term

confidence interval) was introduced in 2000 to replace, as we see it, the more understandable

term - "probabilistic accounting" (Jensen, 2009).

The proposed concept of fiduciary accounting reflects the position of the authors of the

concept that accounting based only on point (discrete) values of the value of assets and liabilities

is insufficient for an objective assessment of the financial condition of the company and the

associated uncertainties and risks (Platin et al 2007). The paper notes that there are many

potential sources of uncertainty in the value of assets and liabilities that make it impossible to

accurately determine “true value”. This problem resembles a similar measurement error problem.

In this regard, within the framework of the proposed accounting, all lines of the balance sheet

and the profit and loss statement are proposed to be kept in the form of probability distributions.

Histograms or confidence intervals can also be used (Novoa et al 2009).

To sum up, uncertainty is based on the probabilistic nature of the market. The fact is that

even transactions with identical and completely replaceable assets, carried out at the same time

and under the same conditions, can be carried out at different prices. In this case, price variability

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD

10

may not be related to the features of the transaction and even to the market (Laux and Leuz,

2009). It may be due to the different goals of market participants, the difference in their

awareness, the motivation of the parties and other subjective factors. The most probable

transaction price determined during the valuation process generally does not coincide with the

actual transaction price; therefore, the estimation result always has some uncertainty to some

extent.

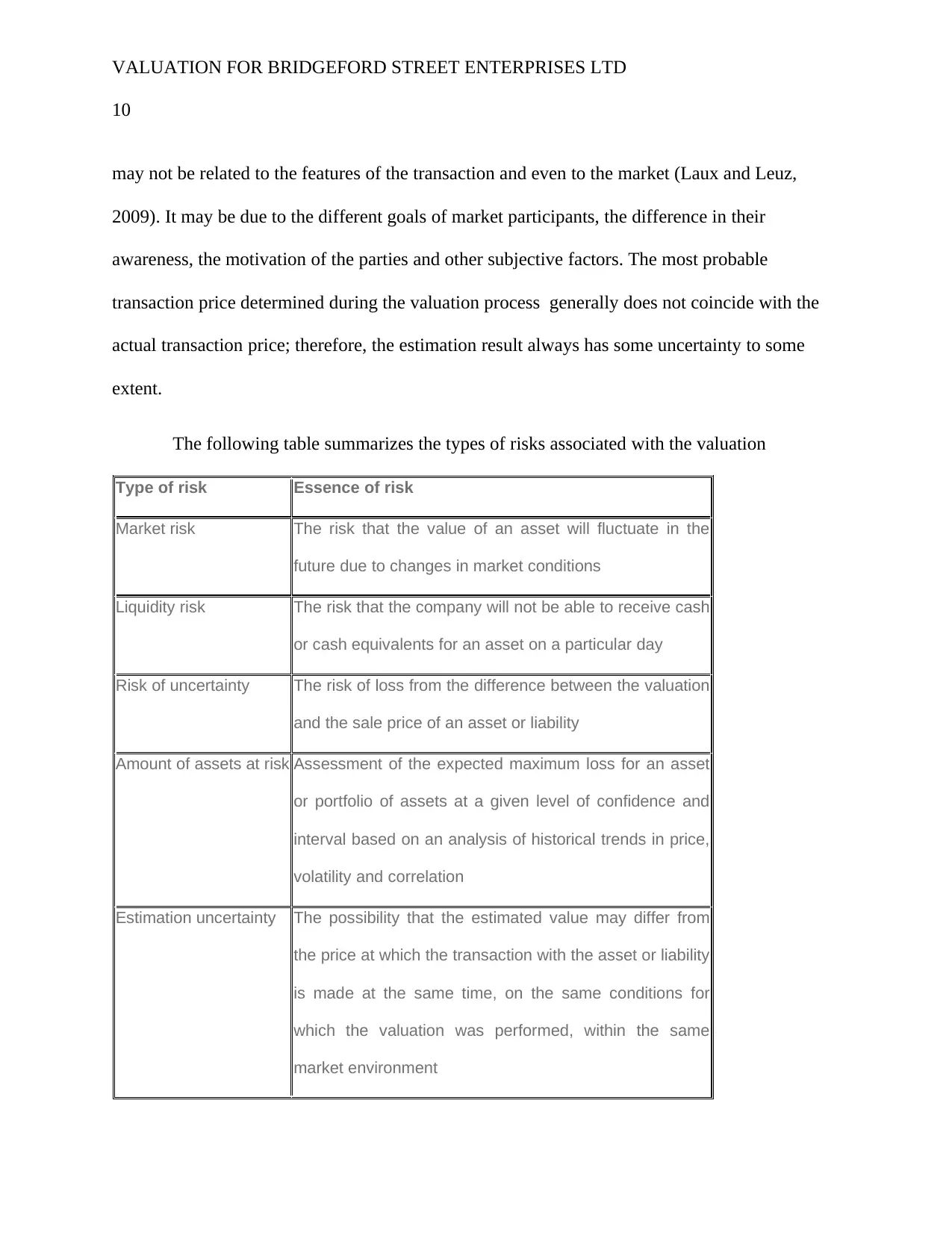

The following table summarizes the types of risks associated with the valuation

Type of risk Essence of risk

Market risk The risk that the value of an asset will fluctuate in the

future due to changes in market conditions

Liquidity risk The risk that the company will not be able to receive cash

or cash equivalents for an asset on a particular day

Risk of uncertainty The risk of loss from the difference between the valuation

and the sale price of an asset or liability

Amount of assets at risk Assessment of the expected maximum loss for an asset

or portfolio of assets at a given level of confidence and

interval based on an analysis of historical trends in price,

volatility and correlation

Estimation uncertainty The possibility that the estimated value may differ from

the price at which the transaction with the asset or liability

is made at the same time, on the same conditions for

which the valuation was performed, within the same

market environment

10

may not be related to the features of the transaction and even to the market (Laux and Leuz,

2009). It may be due to the different goals of market participants, the difference in their

awareness, the motivation of the parties and other subjective factors. The most probable

transaction price determined during the valuation process generally does not coincide with the

actual transaction price; therefore, the estimation result always has some uncertainty to some

extent.

The following table summarizes the types of risks associated with the valuation

Type of risk Essence of risk

Market risk The risk that the value of an asset will fluctuate in the

future due to changes in market conditions

Liquidity risk The risk that the company will not be able to receive cash

or cash equivalents for an asset on a particular day

Risk of uncertainty The risk of loss from the difference between the valuation

and the sale price of an asset or liability

Amount of assets at risk Assessment of the expected maximum loss for an asset

or portfolio of assets at a given level of confidence and

interval based on an analysis of historical trends in price,

volatility and correlation

Estimation uncertainty The possibility that the estimated value may differ from

the price at which the transaction with the asset or liability

is made at the same time, on the same conditions for

which the valuation was performed, within the same

market environment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD

11

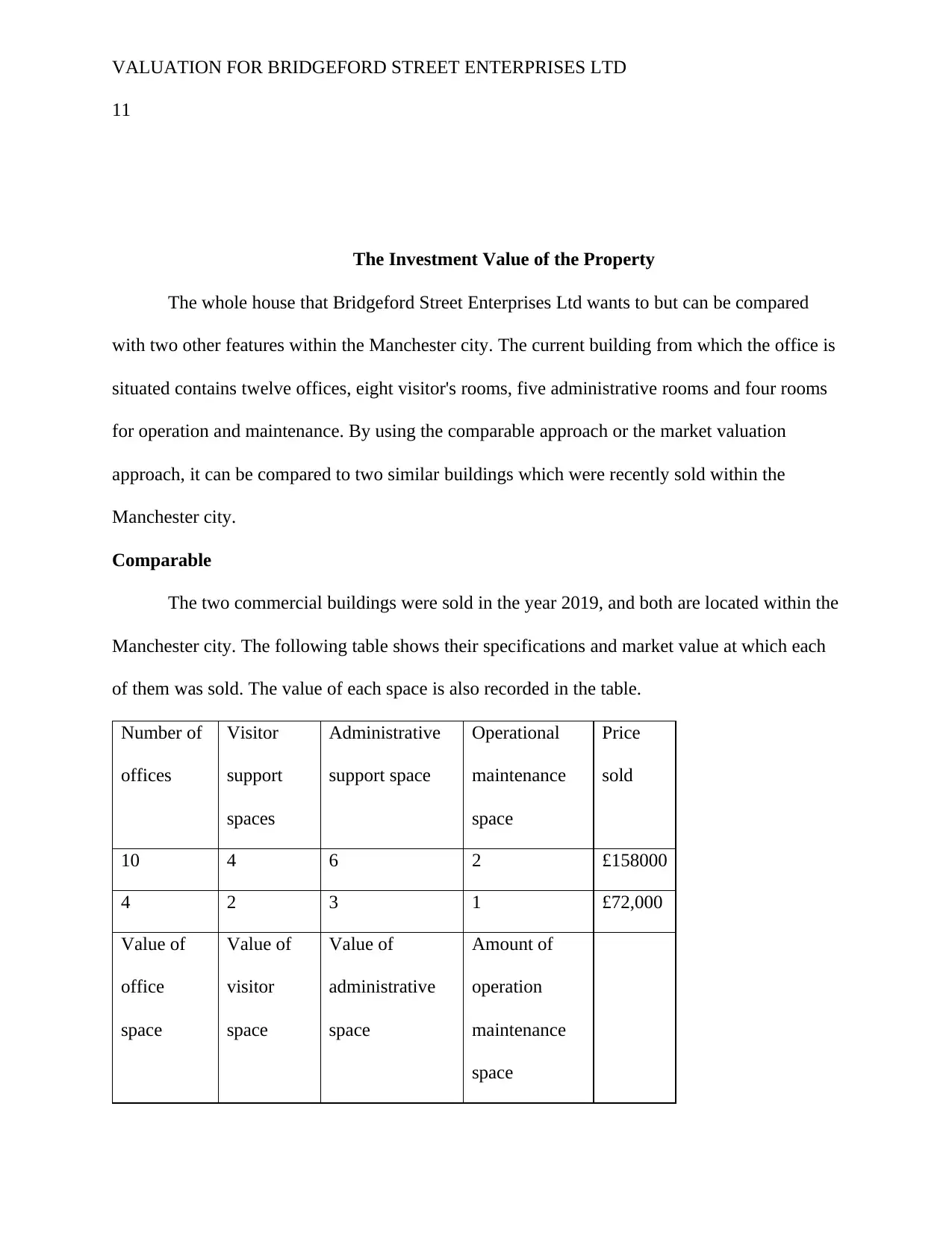

The Investment Value of the Property

The whole house that Bridgeford Street Enterprises Ltd wants to but can be compared

with two other features within the Manchester city. The current building from which the office is

situated contains twelve offices, eight visitor's rooms, five administrative rooms and four rooms

for operation and maintenance. By using the comparable approach or the market valuation

approach, it can be compared to two similar buildings which were recently sold within the

Manchester city.

Comparable

The two commercial buildings were sold in the year 2019, and both are located within the

Manchester city. The following table shows their specifications and market value at which each

of them was sold. The value of each space is also recorded in the table.

Number of

offices

Visitor

support

spaces

Administrative

support space

Operational

maintenance

space

Price

sold

10 4 6 2 £158000

4 2 3 1 £72,000

Value of

office

space

Value of

visitor

space

Value of

administrative

space

Amount of

operation

maintenance

space

11

The Investment Value of the Property

The whole house that Bridgeford Street Enterprises Ltd wants to but can be compared

with two other features within the Manchester city. The current building from which the office is

situated contains twelve offices, eight visitor's rooms, five administrative rooms and four rooms

for operation and maintenance. By using the comparable approach or the market valuation

approach, it can be compared to two similar buildings which were recently sold within the

Manchester city.

Comparable

The two commercial buildings were sold in the year 2019, and both are located within the

Manchester city. The following table shows their specifications and market value at which each

of them was sold. The value of each space is also recorded in the table.

Number of

offices

Visitor

support

spaces

Administrative

support space

Operational

maintenance

space

Price

sold

10 4 6 2 £158000

4 2 3 1 £72,000

Value of

office

space

Value of

visitor

space

Value of

administrative

space

Amount of

operation

maintenance

space

VALUATION FOR BRIDGEFORD STREET ENTERPRISES LTD

12

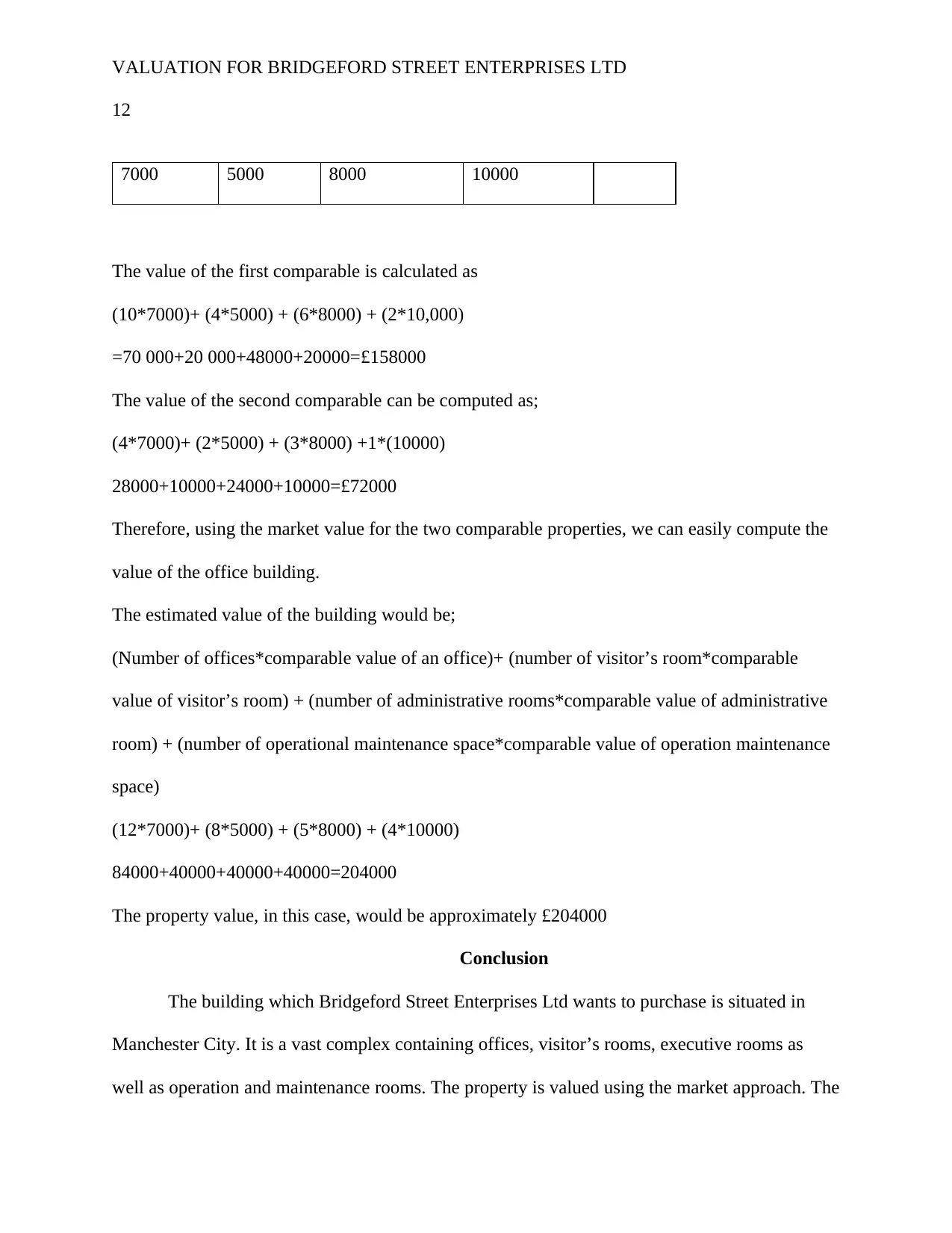

7000 5000 8000 10000

The value of the first comparable is calculated as

(10*7000)+ (4*5000) + (6*8000) + (2*10,000)

=70 000+20 000+48000+20000=£158000

The value of the second comparable can be computed as;

(4*7000)+ (2*5000) + (3*8000) +1*(10000)

28000+10000+24000+10000=£72000

Therefore, using the market value for the two comparable properties, we can easily compute the

value of the office building.

The estimated value of the building would be;

(Number of offices*comparable value of an office)+ (number of visitor’s room*comparable

value of visitor’s room) + (number of administrative rooms*comparable value of administrative

room) + (number of operational maintenance space*comparable value of operation maintenance

space)

(12*7000)+ (8*5000) + (5*8000) + (4*10000)

84000+40000+40000+40000=204000

The property value, in this case, would be approximately £204000

Conclusion

The building which Bridgeford Street Enterprises Ltd wants to purchase is situated in

Manchester City. It is a vast complex containing offices, visitor’s rooms, executive rooms as

well as operation and maintenance rooms. The property is valued using the market approach. The

12

7000 5000 8000 10000

The value of the first comparable is calculated as

(10*7000)+ (4*5000) + (6*8000) + (2*10,000)

=70 000+20 000+48000+20000=£158000

The value of the second comparable can be computed as;

(4*7000)+ (2*5000) + (3*8000) +1*(10000)

28000+10000+24000+10000=£72000

Therefore, using the market value for the two comparable properties, we can easily compute the

value of the office building.

The estimated value of the building would be;

(Number of offices*comparable value of an office)+ (number of visitor’s room*comparable

value of visitor’s room) + (number of administrative rooms*comparable value of administrative

room) + (number of operational maintenance space*comparable value of operation maintenance

space)

(12*7000)+ (8*5000) + (5*8000) + (4*10000)

84000+40000+40000+40000=204000

The property value, in this case, would be approximately £204000

Conclusion

The building which Bridgeford Street Enterprises Ltd wants to purchase is situated in

Manchester City. It is a vast complex containing offices, visitor’s rooms, executive rooms as

well as operation and maintenance rooms. The property is valued using the market approach. The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.