Case Study: Cash, Credit, and Float Management Analysis for Finance

VerifiedAdded on 2022/08/26

|12

|3236

|24

Case Study

AI Summary

This document provides comprehensive solutions to three case studies focused on financial management. The first case examines cash management challenges faced by Mind and Body, Inc., analyzing short-term financing needs and optimal cash reserve policies. The second case delves into credit policy management for Luvly Jubbly Inc., evaluating different credit terms, assessing their impact on financial ratios, and recommending the best credit policy. The third case study analyzes float management for Nathan Daniel, calculating operating and cash cycles, and assessing the efficiency of working capital management. The solutions include detailed calculations, financial ratio analysis, and strategic recommendations for improving financial performance and decision-making.

Case 1: Cash Management

Answer to Question 1:

The requirement for short term financing as computed in the attached excel reflects no definite

pattern and changed over months. This can be because of many reasons including general trend

of growth in the economy, seasonal variation in the business, and uncertainty associated with any

business in general. In order to manage a smooth fund flow, the company has to tide over the

short term financial needs as reflected by the projected cash deficit in the cash budget. Further, if

today we input the data for the estimated sales over next 13 months in the attached sheet, we will

witness that the company has surplus funds and need no additional funding. Short term funds are

raised to tide over short term deficits and thus company should have a flexible approach towards

raising funds and the policy should not be stringent or rigid.

Answer to Question 2:

The depreciation expense for a company is a non-cash expense, which does not involve any cash

flow (neither cash inflow nor cash outflow). The depreciation expenses are allowable expense

that reduces the value of assets of the company and do not involve any cash payment. Since cash

budgets include only transactions that affect cash position of the company, depreciation is not

included in the cash budget of the company.

Answer to Question 3:

If the company changes the minimum cash reserve policy from current $20,000 to $0 or $5,000

the company will run into cash shortage. in months of August, the company has a deficit and this

minimum cash reserve will not cover the shortage. This will affect the revenue of the company

negatively. Further, the cost of borrowing in emergency will rise and lead to higher interest costs.

In case of reserves for $50,000, the company would be in a better position to manage the

shortages in most of the months in next 13 projected months. At $5,00,000 the company would

suffer from loss of opportunity costs as they will have excess cash and in absence of such reserve

policy they could have used the cash for some other growth opportunities or investment leading

to generation of cash.

The company should not have a fixed cash reserve policy and adopt a compromise approach

where it plans for next 6 months and depending on the projection fixes minimum cash reserve

policy.

Answer to Question 4:

The EAR = (1 + 0.03) ^ 1/6 -1 = 0.494% per month.

Based on the above EAR at 6% interest from the bank, the company should invest with the bank

as they will receive 0.494% per month on the surplus that they maintain based on projections of

13 months. (as attached in excel)

1

Answer to Question 1:

The requirement for short term financing as computed in the attached excel reflects no definite

pattern and changed over months. This can be because of many reasons including general trend

of growth in the economy, seasonal variation in the business, and uncertainty associated with any

business in general. In order to manage a smooth fund flow, the company has to tide over the

short term financial needs as reflected by the projected cash deficit in the cash budget. Further, if

today we input the data for the estimated sales over next 13 months in the attached sheet, we will

witness that the company has surplus funds and need no additional funding. Short term funds are

raised to tide over short term deficits and thus company should have a flexible approach towards

raising funds and the policy should not be stringent or rigid.

Answer to Question 2:

The depreciation expense for a company is a non-cash expense, which does not involve any cash

flow (neither cash inflow nor cash outflow). The depreciation expenses are allowable expense

that reduces the value of assets of the company and do not involve any cash payment. Since cash

budgets include only transactions that affect cash position of the company, depreciation is not

included in the cash budget of the company.

Answer to Question 3:

If the company changes the minimum cash reserve policy from current $20,000 to $0 or $5,000

the company will run into cash shortage. in months of August, the company has a deficit and this

minimum cash reserve will not cover the shortage. This will affect the revenue of the company

negatively. Further, the cost of borrowing in emergency will rise and lead to higher interest costs.

In case of reserves for $50,000, the company would be in a better position to manage the

shortages in most of the months in next 13 projected months. At $5,00,000 the company would

suffer from loss of opportunity costs as they will have excess cash and in absence of such reserve

policy they could have used the cash for some other growth opportunities or investment leading

to generation of cash.

The company should not have a fixed cash reserve policy and adopt a compromise approach

where it plans for next 6 months and depending on the projection fixes minimum cash reserve

policy.

Answer to Question 4:

The EAR = (1 + 0.03) ^ 1/6 -1 = 0.494% per month.

Based on the above EAR at 6% interest from the bank, the company should invest with the bank

as they will receive 0.494% per month on the surplus that they maintain based on projections of

13 months. (as attached in excel)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Answer to Question 5:

The starting point for any budget is the estimation of sales over the next few periods, which is

provided by the sales department of a company. The department tries and manage the demand

and supply aspect of the product and set an estimated price for the offering against which they

predict some level of unit sales. The fact is that this estimation of price is dependent on various

assumptions, which are uncertain and may be inaccurate.

One of the many ways to reduce or minimize the uncertainty is use of sensitivity analysis by

which they can identify one or more variables that affect their estimation vastly and are of key

importance. This would enable to focus on that variable more and arrive at better projections.

2

The starting point for any budget is the estimation of sales over the next few periods, which is

provided by the sales department of a company. The department tries and manage the demand

and supply aspect of the product and set an estimated price for the offering against which they

predict some level of unit sales. The fact is that this estimation of price is dependent on various

assumptions, which are uncertain and may be inaccurate.

One of the many ways to reduce or minimize the uncertainty is use of sensitivity analysis by

which they can identify one or more variables that affect their estimation vastly and are of key

importance. This would enable to focus on that variable more and arrive at better projections.

2

Case 2: Credit Policy Management Case

Answer to Question 1:

The three components of a credit policy for any company are:

Terms of Sale - This includes the credit length and the discounts for early payments

Credit Extension – This includes offering credit to worthy customers after careful analysis of the

customer’s portfolio and goodwill

Collection Policy – This includes the follow up mechanism on credit extended.

Even though, the company satisfies all these 3 aspects of a credit policy, the policy is inefficient

in the sense that the credit policy mentions only the days in which the customers should pay but

do not mention any cash discount that it extends in case the customer is paying early or before

the stipulated time.

Answer to Question 2:

Alternative 1: 2/20 net 30 – Here, the company is extending 10 days credit. Considering the rate

per 10 days of .02∕.98 = 2.040%, there are 365∕10 = 36.5 such periods in a year, so the effective

annual rate is computed as:

EAR = (1.0204) ^36.5 − 1 = 109%; APR = .02040 × 36.5 = 74.46%

Alternative 1: 2/25 net 45 - Here, the company is extending 20 days credit. Considering the rate

per 20 days of .02∕.98 = 2.040%, there are 365∕20 = 18.25 such periods in a year, so the effective

annual rate is computed as:

EAR = (1.0204) ^18.25 − 1 = 44.56%; APR = .02040 × 18.25 = 37.24%

Buyer’s Point of View – Borrowing rate of 15%

Based on the above APR’s, both the alternatives are extremely expensive for them and thus they

wont benefit from early payments. The APR’s at which they should be able to accept the offers

are: APR = .15 x 36.5 = 5.48%; APR = .15 x 18.25 = 2.74%

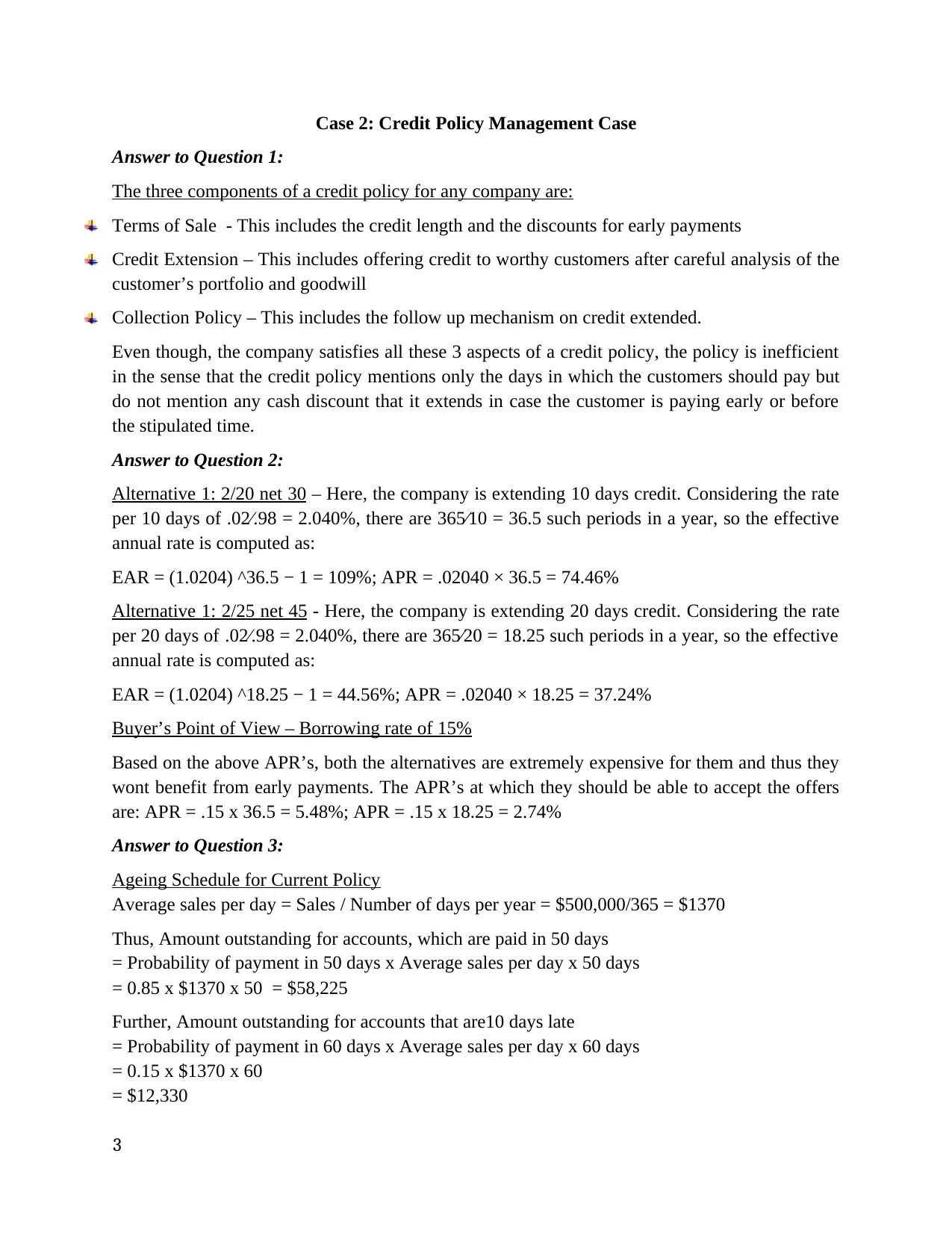

Answer to Question 3:

Ageing Schedule for Current Policy

Average sales per day = Sales / Number of days per year = $500,000/365 = $1370

Thus, Amount outstanding for accounts, which are paid in 50 days

= Probability of payment in 50 days x Average sales per day x 50 days

= 0.85 x $1370 x 50 = $58,225

Further, Amount outstanding for accounts that are10 days late

= Probability of payment in 60 days x Average sales per day x 60 days

= 0.15 x $1370 x 60

= $12,330

3

Answer to Question 1:

The three components of a credit policy for any company are:

Terms of Sale - This includes the credit length and the discounts for early payments

Credit Extension – This includes offering credit to worthy customers after careful analysis of the

customer’s portfolio and goodwill

Collection Policy – This includes the follow up mechanism on credit extended.

Even though, the company satisfies all these 3 aspects of a credit policy, the policy is inefficient

in the sense that the credit policy mentions only the days in which the customers should pay but

do not mention any cash discount that it extends in case the customer is paying early or before

the stipulated time.

Answer to Question 2:

Alternative 1: 2/20 net 30 – Here, the company is extending 10 days credit. Considering the rate

per 10 days of .02∕.98 = 2.040%, there are 365∕10 = 36.5 such periods in a year, so the effective

annual rate is computed as:

EAR = (1.0204) ^36.5 − 1 = 109%; APR = .02040 × 36.5 = 74.46%

Alternative 1: 2/25 net 45 - Here, the company is extending 20 days credit. Considering the rate

per 20 days of .02∕.98 = 2.040%, there are 365∕20 = 18.25 such periods in a year, so the effective

annual rate is computed as:

EAR = (1.0204) ^18.25 − 1 = 44.56%; APR = .02040 × 18.25 = 37.24%

Buyer’s Point of View – Borrowing rate of 15%

Based on the above APR’s, both the alternatives are extremely expensive for them and thus they

wont benefit from early payments. The APR’s at which they should be able to accept the offers

are: APR = .15 x 36.5 = 5.48%; APR = .15 x 18.25 = 2.74%

Answer to Question 3:

Ageing Schedule for Current Policy

Average sales per day = Sales / Number of days per year = $500,000/365 = $1370

Thus, Amount outstanding for accounts, which are paid in 50 days

= Probability of payment in 50 days x Average sales per day x 50 days

= 0.85 x $1370 x 50 = $58,225

Further, Amount outstanding for accounts that are10 days late

= Probability of payment in 60 days x Average sales per day x 60 days

= 0.15 x $1370 x 60

= $12,330

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

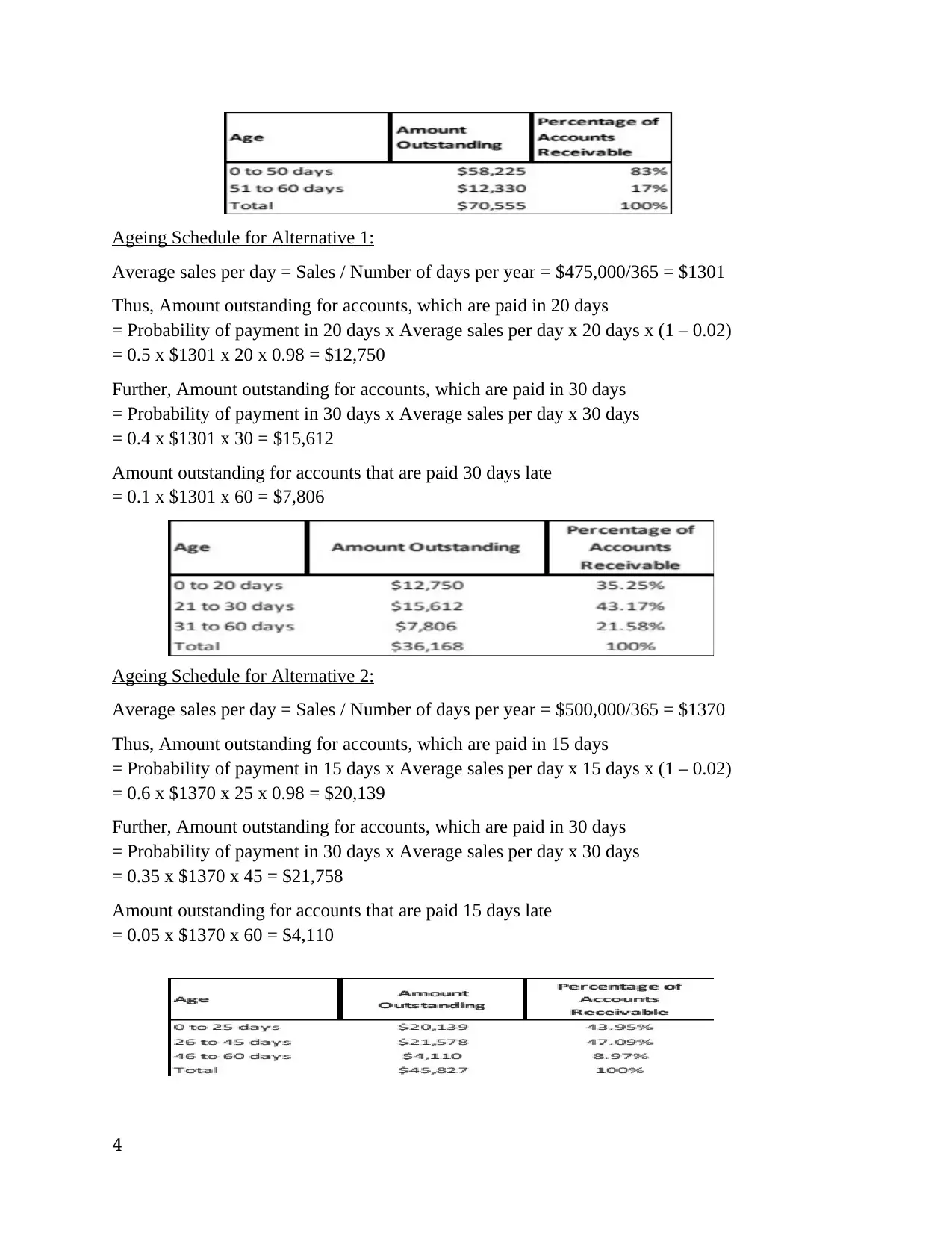

Ageing Schedule for Alternative 1:

Average sales per day = Sales / Number of days per year = $475,000/365 = $1301

Thus, Amount outstanding for accounts, which are paid in 20 days

= Probability of payment in 20 days x Average sales per day x 20 days x (1 – 0.02)

= 0.5 x $1301 x 20 x 0.98 = $12,750

Further, Amount outstanding for accounts, which are paid in 30 days

= Probability of payment in 30 days x Average sales per day x 30 days

= 0.4 x $1301 x 30 = $15,612

Amount outstanding for accounts that are paid 30 days late

= 0.1 x $1301 x 60 = $7,806

Ageing Schedule for Alternative 2:

Average sales per day = Sales / Number of days per year = $500,000/365 = $1370

Thus, Amount outstanding for accounts, which are paid in 15 days

= Probability of payment in 15 days x Average sales per day x 15 days x (1 – 0.02)

= 0.6 x $1370 x 25 x 0.98 = $20,139

Further, Amount outstanding for accounts, which are paid in 30 days

= Probability of payment in 30 days x Average sales per day x 30 days

= 0.35 x $1370 x 45 = $21,758

Amount outstanding for accounts that are paid 15 days late

= 0.05 x $1370 x 60 = $4,110

4

Average sales per day = Sales / Number of days per year = $475,000/365 = $1301

Thus, Amount outstanding for accounts, which are paid in 20 days

= Probability of payment in 20 days x Average sales per day x 20 days x (1 – 0.02)

= 0.5 x $1301 x 20 x 0.98 = $12,750

Further, Amount outstanding for accounts, which are paid in 30 days

= Probability of payment in 30 days x Average sales per day x 30 days

= 0.4 x $1301 x 30 = $15,612

Amount outstanding for accounts that are paid 30 days late

= 0.1 x $1301 x 60 = $7,806

Ageing Schedule for Alternative 2:

Average sales per day = Sales / Number of days per year = $500,000/365 = $1370

Thus, Amount outstanding for accounts, which are paid in 15 days

= Probability of payment in 15 days x Average sales per day x 15 days x (1 – 0.02)

= 0.6 x $1370 x 25 x 0.98 = $20,139

Further, Amount outstanding for accounts, which are paid in 30 days

= Probability of payment in 30 days x Average sales per day x 30 days

= 0.35 x $1370 x 45 = $21,758

Amount outstanding for accounts that are paid 15 days late

= 0.05 x $1370 x 60 = $4,110

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

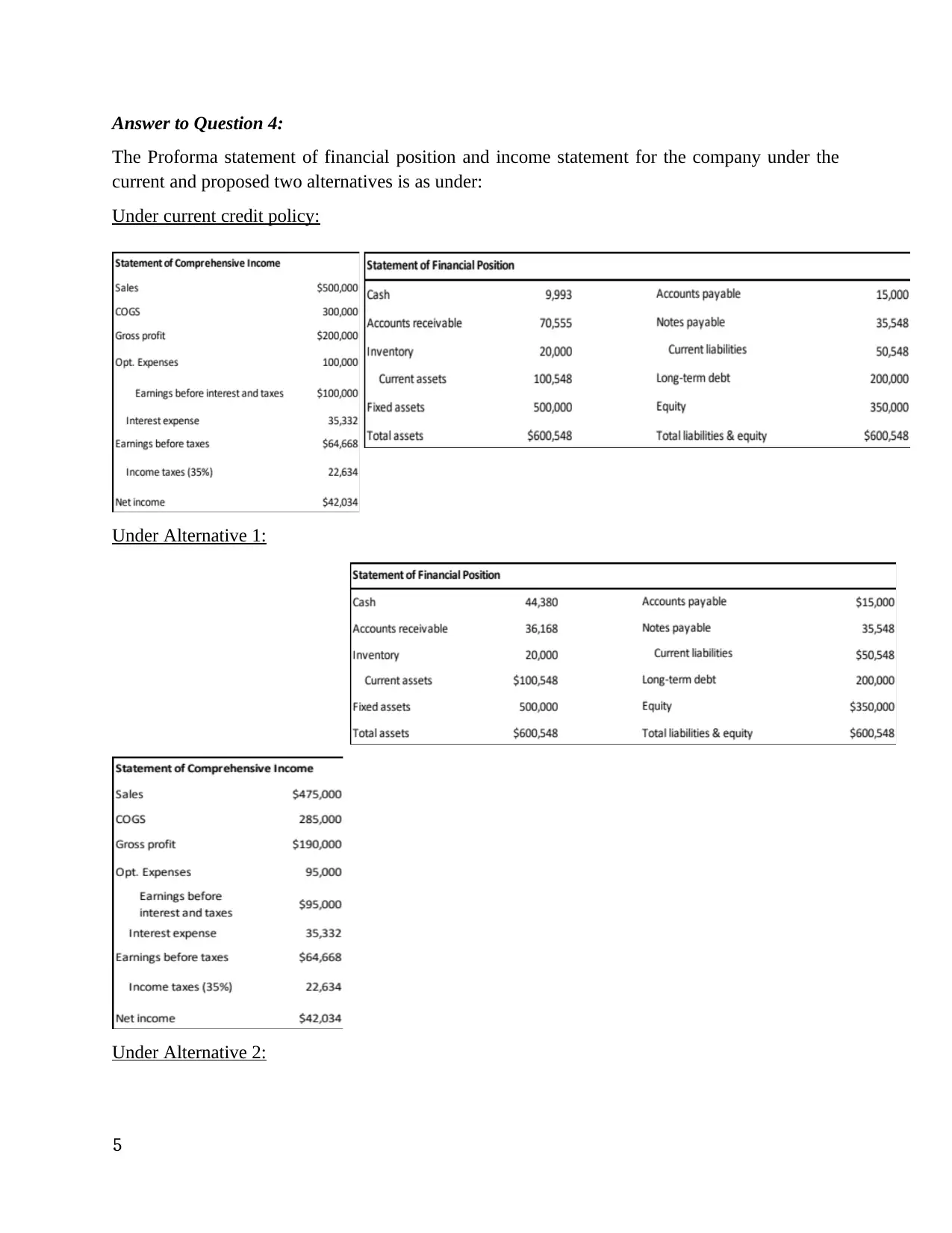

Answer to Question 4:

The Proforma statement of financial position and income statement for the company under the

current and proposed two alternatives is as under:

Under current credit policy:

Under Alternative 1:

Under Alternative 2:

5

The Proforma statement of financial position and income statement for the company under the

current and proposed two alternatives is as under:

Under current credit policy:

Under Alternative 1:

Under Alternative 2:

5

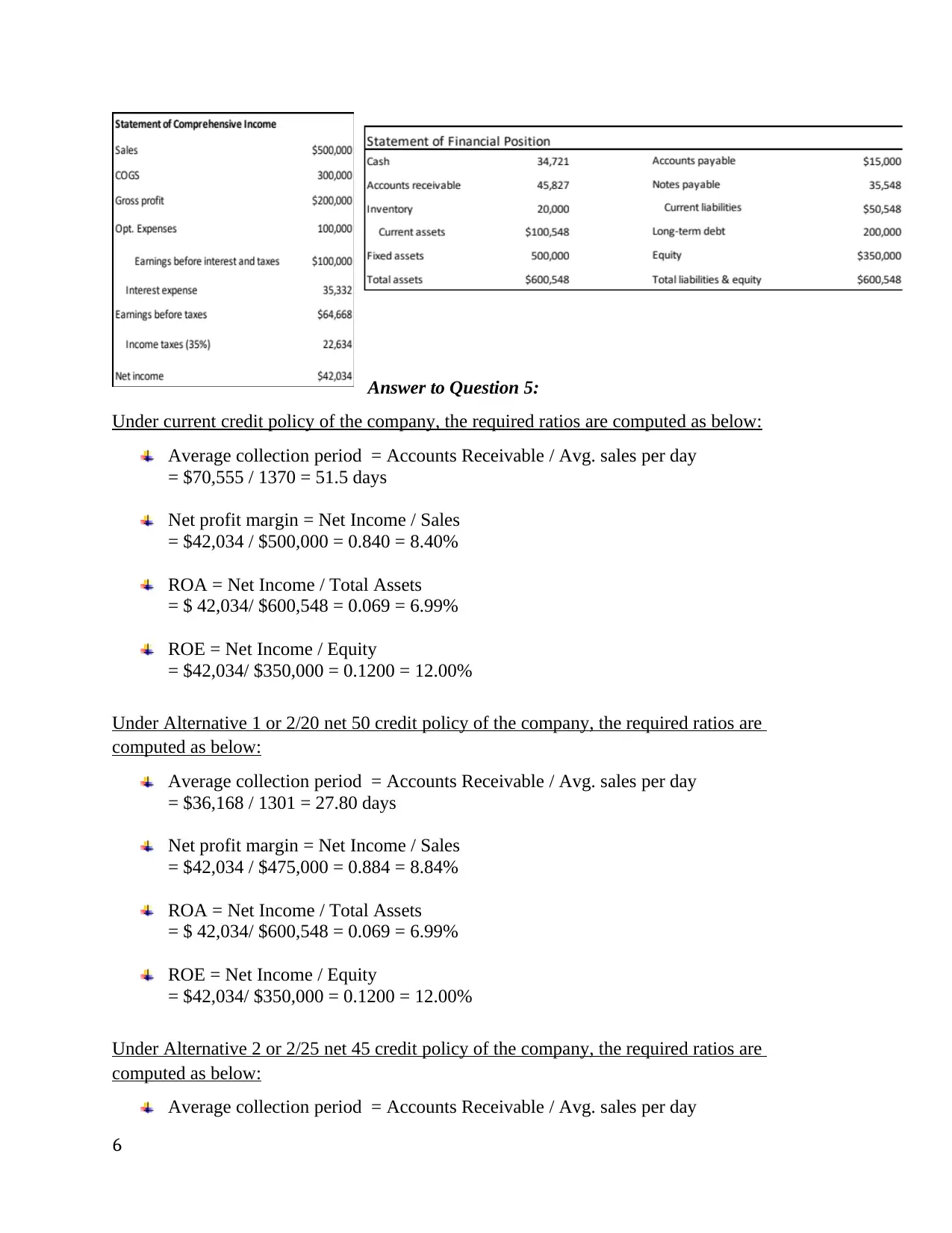

Answer to Question 5:

Under current credit policy of the company, the required ratios are computed as below:

Average collection period = Accounts Receivable / Avg. sales per day

= $70,555 / 1370 = 51.5 days

Net profit margin = Net Income / Sales

= $42,034 / $500,000 = 0.840 = 8.40%

ROA = Net Income / Total Assets

= $ 42,034/ $600,548 = 0.069 = 6.99%

ROE = Net Income / Equity

= $42,034/ $350,000 = 0.1200 = 12.00%

Under Alternative 1 or 2/20 net 50 credit policy of the company, the required ratios are

computed as below:

Average collection period = Accounts Receivable / Avg. sales per day

= $36,168 / 1301 = 27.80 days

Net profit margin = Net Income / Sales

= $42,034 / $475,000 = 0.884 = 8.84%

ROA = Net Income / Total Assets

= $ 42,034/ $600,548 = 0.069 = 6.99%

ROE = Net Income / Equity

= $42,034/ $350,000 = 0.1200 = 12.00%

Under Alternative 2 or 2/25 net 45 credit policy of the company, the required ratios are

computed as below:

Average collection period = Accounts Receivable / Avg. sales per day

6

Under current credit policy of the company, the required ratios are computed as below:

Average collection period = Accounts Receivable / Avg. sales per day

= $70,555 / 1370 = 51.5 days

Net profit margin = Net Income / Sales

= $42,034 / $500,000 = 0.840 = 8.40%

ROA = Net Income / Total Assets

= $ 42,034/ $600,548 = 0.069 = 6.99%

ROE = Net Income / Equity

= $42,034/ $350,000 = 0.1200 = 12.00%

Under Alternative 1 or 2/20 net 50 credit policy of the company, the required ratios are

computed as below:

Average collection period = Accounts Receivable / Avg. sales per day

= $36,168 / 1301 = 27.80 days

Net profit margin = Net Income / Sales

= $42,034 / $475,000 = 0.884 = 8.84%

ROA = Net Income / Total Assets

= $ 42,034/ $600,548 = 0.069 = 6.99%

ROE = Net Income / Equity

= $42,034/ $350,000 = 0.1200 = 12.00%

Under Alternative 2 or 2/25 net 45 credit policy of the company, the required ratios are

computed as below:

Average collection period = Accounts Receivable / Avg. sales per day

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

= $45,827 / 1370 = 33.45 days

Net profit margin = Net Income / Sales

= $42,034 / $500,000 = 0.840 = 8.40%

ROA = Net Income / Total Assets

= $ 42,034/ $600,548 = 0.069 = 6.99%

ROE = Net Income / Equity

= $42,034/ $350,000 = 0.1200 = 12.00%

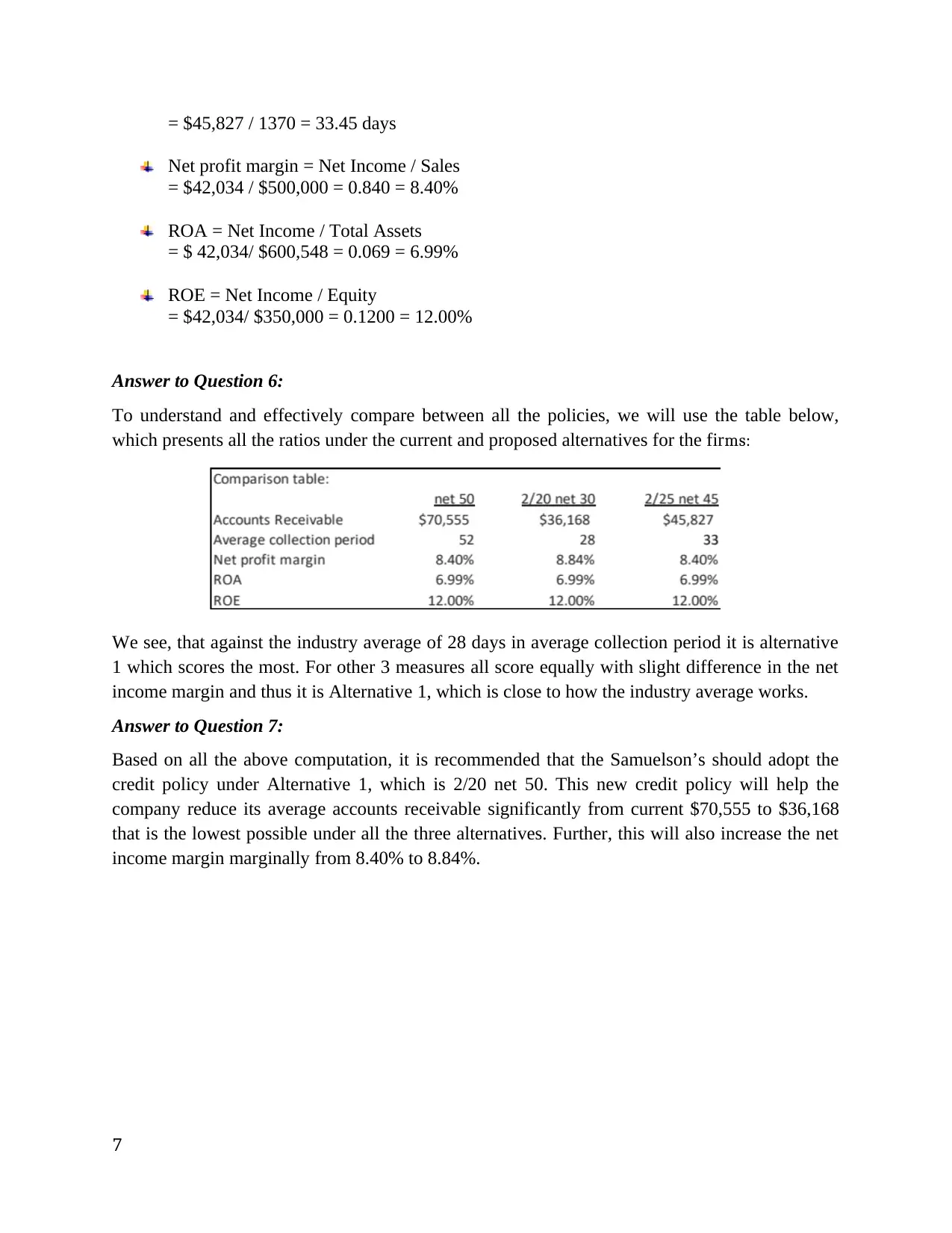

Answer to Question 6:

To understand and effectively compare between all the policies, we will use the table below,

which presents all the ratios under the current and proposed alternatives for the firms:

We see, that against the industry average of 28 days in average collection period it is alternative

1 which scores the most. For other 3 measures all score equally with slight difference in the net

income margin and thus it is Alternative 1, which is close to how the industry average works.

Answer to Question 7:

Based on all the above computation, it is recommended that the Samuelson’s should adopt the

credit policy under Alternative 1, which is 2/20 net 50. This new credit policy will help the

company reduce its average accounts receivable significantly from current $70,555 to $36,168

that is the lowest possible under all the three alternatives. Further, this will also increase the net

income margin marginally from 8.40% to 8.84%.

7

Net profit margin = Net Income / Sales

= $42,034 / $500,000 = 0.840 = 8.40%

ROA = Net Income / Total Assets

= $ 42,034/ $600,548 = 0.069 = 6.99%

ROE = Net Income / Equity

= $42,034/ $350,000 = 0.1200 = 12.00%

Answer to Question 6:

To understand and effectively compare between all the policies, we will use the table below,

which presents all the ratios under the current and proposed alternatives for the firms:

We see, that against the industry average of 28 days in average collection period it is alternative

1 which scores the most. For other 3 measures all score equally with slight difference in the net

income margin and thus it is Alternative 1, which is close to how the industry average works.

Answer to Question 7:

Based on all the above computation, it is recommended that the Samuelson’s should adopt the

credit policy under Alternative 1, which is 2/20 net 50. This new credit policy will help the

company reduce its average accounts receivable significantly from current $70,555 to $36,168

that is the lowest possible under all the three alternatives. Further, this will also increase the net

income margin marginally from 8.40% to 8.84%.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Case 3: Float Management Case

Answer to Question 1:

To compute the inventory, receivables and payables period, we will have to first compute the

average of these variables:

Inventory Period:

Average Inventory = (Beginning Inventory + Ending Inventory) / 2

= ($80,000 + $120,000) / 2 = $100,000

Inventory Turnover = Cost of Goods Sold / Average Inventory

= $2,625,000 / $100,000 = 26.25

Thus, Inventory Period = 365 / Inventory Turnover

= 365 / 26.25 = 13.90 days

Receivables Period:

Average Accounts Receivable = (Beginning AR + Ending AR) / 2

= ($175,000 + $145000) / 2 = $160,000

Accounts Receivable Turnover = Credit Sales / Average Accounts Receivable

= $2,450,000 / $160,0000 = 15.31

Accounts Receivable Period = 365 / Accounts Receivable Turnover

= 365 / 15.31 = 23.84 days

Payables Period:

Average Accounts Payable = (Beginning AP + Ending AP) / 2

= ($130,000 + $110,000) / 2 = $120,000

Accounts Payable Turnover = Cost of Goods Sold / Average Accounts Payable

= $2,625,000 / $120,000 = 21.88

Accounts Payable Period = 365 / Accounts Payable Turnover

= 365 / $21.88 = 16.68 days

8

Answer to Question 1:

To compute the inventory, receivables and payables period, we will have to first compute the

average of these variables:

Inventory Period:

Average Inventory = (Beginning Inventory + Ending Inventory) / 2

= ($80,000 + $120,000) / 2 = $100,000

Inventory Turnover = Cost of Goods Sold / Average Inventory

= $2,625,000 / $100,000 = 26.25

Thus, Inventory Period = 365 / Inventory Turnover

= 365 / 26.25 = 13.90 days

Receivables Period:

Average Accounts Receivable = (Beginning AR + Ending AR) / 2

= ($175,000 + $145000) / 2 = $160,000

Accounts Receivable Turnover = Credit Sales / Average Accounts Receivable

= $2,450,000 / $160,0000 = 15.31

Accounts Receivable Period = 365 / Accounts Receivable Turnover

= 365 / 15.31 = 23.84 days

Payables Period:

Average Accounts Payable = (Beginning AP + Ending AP) / 2

= ($130,000 + $110,000) / 2 = $120,000

Accounts Payable Turnover = Cost of Goods Sold / Average Accounts Payable

= $2,625,000 / $120,000 = 21.88

Accounts Payable Period = 365 / Accounts Payable Turnover

= 365 / $21.88 = 16.68 days

8

Answer to Question 2:

The computation of operating and cash cycle is as under:

Operating Cycle = Inventory Period + Accounts Receivable Period

= 13.90 + 23.84 = 37.74 days or 38 days

Cash Cycle = Operating Cycle – Accounts Payable Period

= 37.74 - 16.68 = 21.06 days or 21 days

Answer to Question 3:

38 days of operating cycle indicates that it takes 38 days for the company to buy the raw

material, make products, sell their inventory, and collect cash from the customers. Further, 21

days of cash cycle indicates that it takes 21 days to sell inventory and collect cash from

customers. Against the industry average of 30 days in operating cycle we see that the company is

taking 8 more days than average and thus needs to pay attention to shorten it and mange the

working capital more efficiently. As far as the cash cycle is concerned, the company is working

as per the industry standards.

Answer to Question 4:

Based on the customer’s cash cycle of 30 days and comparative cash cycle of 30 days for

company, we can say that both are aligned to each other and the customer pays to the company

as per their policy. Further, the company has been successful in enforcing their credit policy to

the customer and the collection team of the company is doing a good job by making customers

pay in the allowed 30 days time.

Answer to Question 5:

To compute the average daily collection and disbursement float, we will first have to compute

the total float for the company which is equal to the float for AB, BC and ON cheque.

Total Collection float = Float for AB cheque + Float for BC cheque + Float for ON cheque

= (AB x collection delay 1) + (BC x collection delay 2) + (ON x collection delay 4)

= ($1,750,000 x 1) + ($1,050,000 x 2) + ($700,000 x 4)

= $1,750,000 + $2,100,000 + $2,800,000

= $6,665,000

Based on the above total float, the average daily collection float can be computed as under:

Average daily float = Total float / Number of days per month

= $6,665,000 / 30

= $221,667

9

The computation of operating and cash cycle is as under:

Operating Cycle = Inventory Period + Accounts Receivable Period

= 13.90 + 23.84 = 37.74 days or 38 days

Cash Cycle = Operating Cycle – Accounts Payable Period

= 37.74 - 16.68 = 21.06 days or 21 days

Answer to Question 3:

38 days of operating cycle indicates that it takes 38 days for the company to buy the raw

material, make products, sell their inventory, and collect cash from the customers. Further, 21

days of cash cycle indicates that it takes 21 days to sell inventory and collect cash from

customers. Against the industry average of 30 days in operating cycle we see that the company is

taking 8 more days than average and thus needs to pay attention to shorten it and mange the

working capital more efficiently. As far as the cash cycle is concerned, the company is working

as per the industry standards.

Answer to Question 4:

Based on the customer’s cash cycle of 30 days and comparative cash cycle of 30 days for

company, we can say that both are aligned to each other and the customer pays to the company

as per their policy. Further, the company has been successful in enforcing their credit policy to

the customer and the collection team of the company is doing a good job by making customers

pay in the allowed 30 days time.

Answer to Question 5:

To compute the average daily collection and disbursement float, we will first have to compute

the total float for the company which is equal to the float for AB, BC and ON cheque.

Total Collection float = Float for AB cheque + Float for BC cheque + Float for ON cheque

= (AB x collection delay 1) + (BC x collection delay 2) + (ON x collection delay 4)

= ($1,750,000 x 1) + ($1,050,000 x 2) + ($700,000 x 4)

= $1,750,000 + $2,100,000 + $2,800,000

= $6,665,000

Based on the above total float, the average daily collection float can be computed as under:

Average daily float = Total float / Number of days per month

= $6,665,000 / 30

= $221,667

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Further, Disbursement float = Disbursement delay x Cheques written per day

= 4 x $2,625,000

= $10,500,000

Based on above total disbursement total, the average disbursement float can be computed as:

= Total disbursement float / Number of days per month

= $10,500,000 / 30

= $350,000

Answer to Question 6:

The net float of the company is the difference between the average disbursement float and

average collection float. It is computed as under:

Net float = Average disbursement float – Average collection float

= $350,000 - $221,667

= $128,333

Answer to Question 7:

The effective annual interest rate for the company can be computed using 15% annual interest

rate and 8 years of time as below:

Effective Annual Interest Rate (EAR) = [(1 + Annual Interest rate) ^ (1/ year)] – 1

= [(1.15) ^ (1/8)] – 1 = 1.76%

Thus, the annual total interest expense for the company is:

= Principal * EAR * time

= $530,000 x 0.0176 x 8

Or the total interest expense = $77,544.45

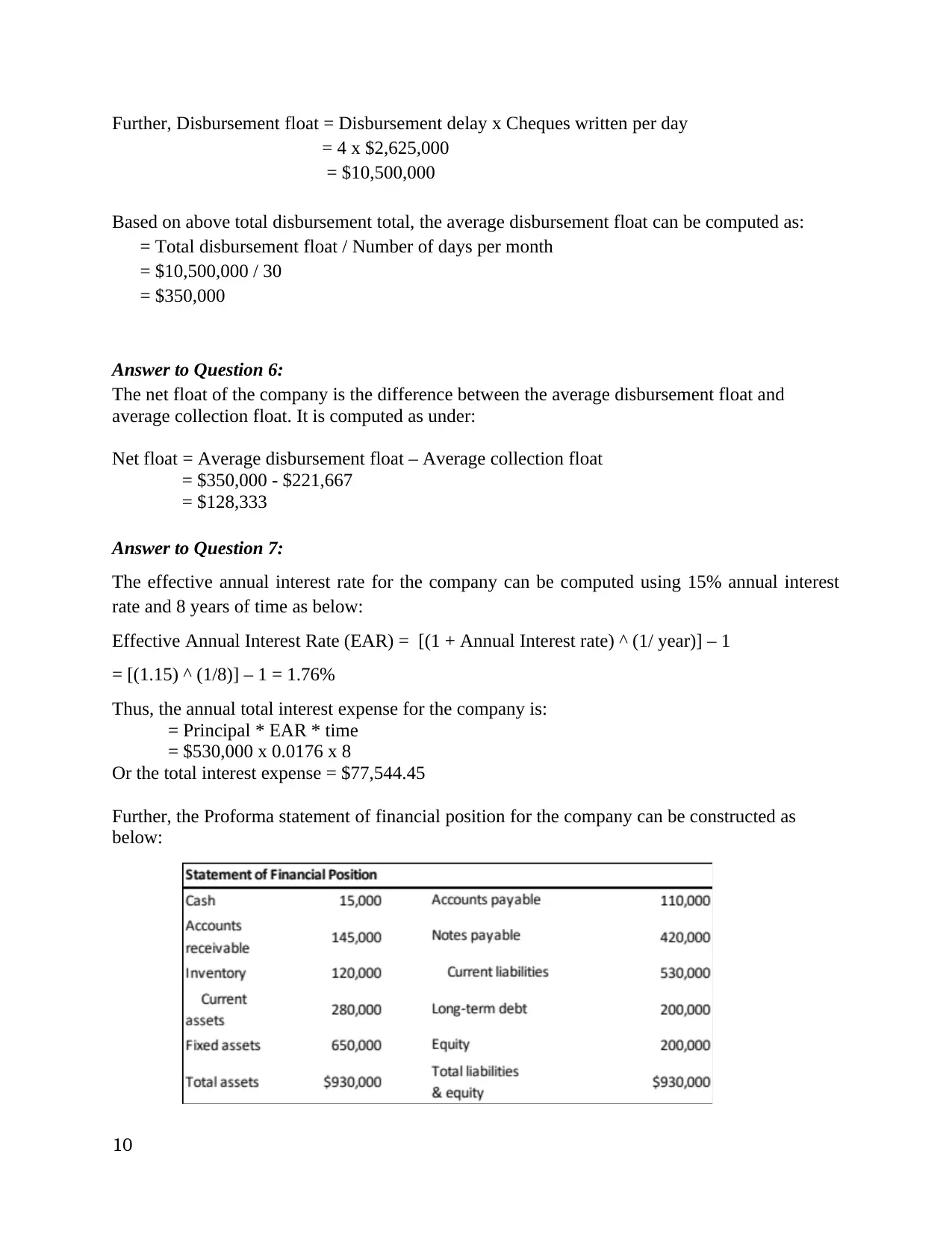

Further, the Proforma statement of financial position for the company can be constructed as

below:

10

= 4 x $2,625,000

= $10,500,000

Based on above total disbursement total, the average disbursement float can be computed as:

= Total disbursement float / Number of days per month

= $10,500,000 / 30

= $350,000

Answer to Question 6:

The net float of the company is the difference between the average disbursement float and

average collection float. It is computed as under:

Net float = Average disbursement float – Average collection float

= $350,000 - $221,667

= $128,333

Answer to Question 7:

The effective annual interest rate for the company can be computed using 15% annual interest

rate and 8 years of time as below:

Effective Annual Interest Rate (EAR) = [(1 + Annual Interest rate) ^ (1/ year)] – 1

= [(1.15) ^ (1/8)] – 1 = 1.76%

Thus, the annual total interest expense for the company is:

= Principal * EAR * time

= $530,000 x 0.0176 x 8

Or the total interest expense = $77,544.45

Further, the Proforma statement of financial position for the company can be constructed as

below:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Based on this, we see that the company will not require short term borrowing as the AR of

$145,000 is more than the AP of $110,000 indicating it can pay off its lender from the funds it

receive from the customer.

However, the firm will need to raise short term financing to the tune of $140,000 to be able to

pay off the notes payable in time.

The short-term interest expense for this will be $140,000 * 0.0176 * 8 = $19,172.

Answer to Question 8:

To compute the viability of the bank’s offering, we will first recompute the floats as below:

To compute the average daily collection and disbursement float, we will first have to compute

the total float for the company which is equal to the float for AB, BC and ON cheque.

Total Collection float = Float for AB cheque + Float for BC cheque + Float for ON cheque

= (AB x collection delay 1) + (BC x collection delay 1) + (ON x collection delay 1)

= ($1,750,000 x 1) + ($1,050,000 x 1) + ($700,000 x 1)

= $1,750,000 + $1,050,000 + $700,000

= $3,500,000 (NO COLLECTION DELAY)

Based on the above total float, the average daily collection float can be computed as under:

Average daily float = Total float / Number of days per month

= $3,500,000 / 30

= $116,667

Further, Disbursement float = Disbursement delay x Cheques written per day

= $2,625,000 (There will be no disbursement delay under this)

Based on above total disbursement total, the average disbursement float can be computed as:

= Total disbursement float / Number of days per month

= $2,625,000 / 30

= $87,500

Therefore Net Float = Disbursement float – Collection float – Fee charged by the bank

= $116,667 - $87,500 - $3,000

= $26,167

Thus, the net float for the company if they take up the Bank’s offer for same day collection and

deposit will be $26,167.

11

$145,000 is more than the AP of $110,000 indicating it can pay off its lender from the funds it

receive from the customer.

However, the firm will need to raise short term financing to the tune of $140,000 to be able to

pay off the notes payable in time.

The short-term interest expense for this will be $140,000 * 0.0176 * 8 = $19,172.

Answer to Question 8:

To compute the viability of the bank’s offering, we will first recompute the floats as below:

To compute the average daily collection and disbursement float, we will first have to compute

the total float for the company which is equal to the float for AB, BC and ON cheque.

Total Collection float = Float for AB cheque + Float for BC cheque + Float for ON cheque

= (AB x collection delay 1) + (BC x collection delay 1) + (ON x collection delay 1)

= ($1,750,000 x 1) + ($1,050,000 x 1) + ($700,000 x 1)

= $1,750,000 + $1,050,000 + $700,000

= $3,500,000 (NO COLLECTION DELAY)

Based on the above total float, the average daily collection float can be computed as under:

Average daily float = Total float / Number of days per month

= $3,500,000 / 30

= $116,667

Further, Disbursement float = Disbursement delay x Cheques written per day

= $2,625,000 (There will be no disbursement delay under this)

Based on above total disbursement total, the average disbursement float can be computed as:

= Total disbursement float / Number of days per month

= $2,625,000 / 30

= $87,500

Therefore Net Float = Disbursement float – Collection float – Fee charged by the bank

= $116,667 - $87,500 - $3,000

= $26,167

Thus, the net float for the company if they take up the Bank’s offer for same day collection and

deposit will be $26,167.

11

Answer to Question 9:

The additional cash that would made be available to the company in case they accept the Bank’s

proposal is the difference between the previous and proposed float which is equal to $3,165,000

($6,665,000 less $3,500,000).

Answer to Question 10:

The additional cash that the company will have to borrow in case they accept the Bank’s

proposal is the difference between the previous and proposed net floats which is equal to $99,166

($128,333 less $29,167 {26,167 + bank fee of $3,000).

Answer to Question 11:

Based on all the above computation, we recommend that the partners should accept the bank’s

same day deposit offer as it will generate additional funds for them which they can utilize for

other potential opportunities or invest for additional interest income.

12

The additional cash that would made be available to the company in case they accept the Bank’s

proposal is the difference between the previous and proposed float which is equal to $3,165,000

($6,665,000 less $3,500,000).

Answer to Question 10:

The additional cash that the company will have to borrow in case they accept the Bank’s

proposal is the difference between the previous and proposed net floats which is equal to $99,166

($128,333 less $29,167 {26,167 + bank fee of $3,000).

Answer to Question 11:

Based on all the above computation, we recommend that the partners should accept the bank’s

same day deposit offer as it will generate additional funds for them which they can utilize for

other potential opportunities or invest for additional interest income.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.