Taxation Law Assignment: Income, CGT, and Small Business Concessions

VerifiedAdded on 2022/08/29

|12

|2813

|24

Homework Assignment

AI Summary

This taxation law assignment, prepared for HI6028 at Holmes Institute, analyzes various tax scenarios under Australian law. The assignment addresses the taxability of different income sources, including employment income, tips, gifts, and fringe benefits, applying relevant case law such as Wainwrig...

Running Head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

Determining whether or not the receipts that is received by the taxpayer is taxable as

the ordinary income under “sec 6-5”.

Rule:

There is a rule given in “sec 995-1 (1)” that the taxable income represents the

assessable earnings subtracted by the total deductions. Under the “sec 6-1 (1)” the assessable

earnings of the taxpayer namely include the ordinary earnings plus the statutory earnings.

There is no such definition of ordinary earnings. Nevertheless, under the “sec 6-5 (1)” the

ordinary earnings are assessed for tax purpose (Atkinson and Leigh 2017). An employee is

normally held chargeable for the all the income that is earned from the employment. This

comprises of any kind of benefit that is received by the taxpayer on the virtue of employment.

In “Wainwright v Calvert (1947)”, it is not necessary that payments received from employer,

as the taxpayer here was employed as the taxi driver and received tips from the passengers.

The tips received by taxi driver was held to be the reward for service and taxable as profits

happening from employment.

As given in the “sec 6-5 (1)” when a taxpayer earns receipts from the employment

and service then it is included into the taxable earnings for tax purpose as either ordinary and

statutory earnings (Richardson and Lanis 2017). The facts given in “Hayes v FCT (1956)” a

receipts which is received by the taxpayer is not viewed as the product of employment if the

reward is for service.

The taxpayers are required to denote that a gain that is received by them as a simple

gift do not have the character of earnings. At the time of differentiating among the non-

Answer to question 1:

Issues:

Determining whether or not the receipts that is received by the taxpayer is taxable as

the ordinary income under “sec 6-5”.

Rule:

There is a rule given in “sec 995-1 (1)” that the taxable income represents the

assessable earnings subtracted by the total deductions. Under the “sec 6-1 (1)” the assessable

earnings of the taxpayer namely include the ordinary earnings plus the statutory earnings.

There is no such definition of ordinary earnings. Nevertheless, under the “sec 6-5 (1)” the

ordinary earnings are assessed for tax purpose (Atkinson and Leigh 2017). An employee is

normally held chargeable for the all the income that is earned from the employment. This

comprises of any kind of benefit that is received by the taxpayer on the virtue of employment.

In “Wainwright v Calvert (1947)”, it is not necessary that payments received from employer,

as the taxpayer here was employed as the taxi driver and received tips from the passengers.

The tips received by taxi driver was held to be the reward for service and taxable as profits

happening from employment.

As given in the “sec 6-5 (1)” when a taxpayer earns receipts from the employment

and service then it is included into the taxable earnings for tax purpose as either ordinary and

statutory earnings (Richardson and Lanis 2017). The facts given in “Hayes v FCT (1956)” a

receipts which is received by the taxpayer is not viewed as the product of employment if the

reward is for service.

The taxpayers are required to denote that a gain that is received by them as a simple

gift do not have the character of earnings. At the time of differentiating among the non-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

taxable personal gifts and the taxable voluntary payments related to service, greater emphasis

has been placed by the court regarding the nature of receipts in the hands of receiver instead

of the motive of the giver (Fayle, Chen and Pope 2015). In “Scott v FCT (1966)” the

taxpayer should understand that a receipt of unsolicited gift cannot be treated as ordinary

earnings simply due to the fact that gratitude was prompted for certain service since there is a

need for other types of factors as well.

The concept of fringe benefit is viewed as the kind of tax regime that essentially

imposes on large extent of benefits that is given by the employer to the employee. As given in

the “sec 136 (1)” the word benefit includes any sort of right, privilege, service or facility that

is given to the employee under the arrangement in respect of the performance of work. Most

importantly the benefit is held for tax under “sec 66 (1) of the FBTAA 1986” where the taxes

are levied on the employer on the basis of benefit given for fringe benefit and not on those

that receives the benefit (Tran-Nam et al. 2016). The court has mentioned its verdict in

“Esssenboourne v Pty Ltd (2002)” by stating that a fringe can only happen when the benefit

is related to or provided to a particular employee. There has to be a material relation among

the benefit that is given to the employee and the provision of employment.

As a general note, when a taxpayer receives any cash gift from the family member as

money that is not the source of taxable earnings then it is not regarded as the taxable

earnings. When a taxpayer receives gift by parents as money, then the gift is not regarded as

having any connection with the income generating activity (Findlay and Jones 2015). The

money received is not taxable as ordinary income under “sec 6-5”.

Application:

Accordingly, the case facts that is obtained from the study suggest that Emmi working on

the part-time basis has received a tips from its customer that amounted to $335. By referring

taxable personal gifts and the taxable voluntary payments related to service, greater emphasis

has been placed by the court regarding the nature of receipts in the hands of receiver instead

of the motive of the giver (Fayle, Chen and Pope 2015). In “Scott v FCT (1966)” the

taxpayer should understand that a receipt of unsolicited gift cannot be treated as ordinary

earnings simply due to the fact that gratitude was prompted for certain service since there is a

need for other types of factors as well.

The concept of fringe benefit is viewed as the kind of tax regime that essentially

imposes on large extent of benefits that is given by the employer to the employee. As given in

the “sec 136 (1)” the word benefit includes any sort of right, privilege, service or facility that

is given to the employee under the arrangement in respect of the performance of work. Most

importantly the benefit is held for tax under “sec 66 (1) of the FBTAA 1986” where the taxes

are levied on the employer on the basis of benefit given for fringe benefit and not on those

that receives the benefit (Tran-Nam et al. 2016). The court has mentioned its verdict in

“Esssenboourne v Pty Ltd (2002)” by stating that a fringe can only happen when the benefit

is related to or provided to a particular employee. There has to be a material relation among

the benefit that is given to the employee and the provision of employment.

As a general note, when a taxpayer receives any cash gift from the family member as

money that is not the source of taxable earnings then it is not regarded as the taxable

earnings. When a taxpayer receives gift by parents as money, then the gift is not regarded as

having any connection with the income generating activity (Findlay and Jones 2015). The

money received is not taxable as ordinary income under “sec 6-5”.

Application:

Accordingly, the case facts that is obtained from the study suggest that Emmi working on

the part-time basis has received a tips from its customer that amounted to $335. By referring

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

to the decision that is given in the “Wainwright v Calvert (1947)” the tips received by Emmi

is held to be the reward for service and taxable as profits happening from employment. The

amount will be included into the taxable income of Emmi under “sec 6-5 (1) ITA Act 97”.

The case of Emmi further reports that she has made an income of $25,000 from her

part-time employment with the Crown Melbourne Restaurant. Referring to the above stated

facts of Emmi, the decision of “Hayes v FCT (1956)” should be mentioned to explain that

Emmi will be held chargeable for the sum of $25,000 because it has the direct relation with

the employment and receipts (Fane and Richardson 2015). Therefore, the amount will be

treated as taxable income earned directly from employment and will be held for assessment

within “sec 6-5”.

She further reports that she has received a perfume from one of her customer during

the Christmas that had the worth of $250. Emmi is required to denote that the receipt of

perfume is a simple gift do not have the character of earnings. Mentioning the factual

evidences denoted in “Scott v FCT (1966)” the receipt of perfume by Emmi is a solicited gift

(Burman 2015). The gift of perfume having the worth of $250 cannot be treated as ordinary

earnings simply due to the fact that gratitude was prompted for certain service since there is a

need for other types of factors to treat the receipt of gift as a taxable income.

The instances that is denoted in the situation of Emmi suggest that she is paid with a

monthly entertainment. The employer has also spent money on Emmi for meals that was

consumed by her. The entertainment expenses and the food benefit given to Emmi is a fringe

benefit within the “sec 136 (1)”. By mentioning the verdict in “Esssenboourne v Pty Ltd

(2002)” it can be stated that the fringe benefit given to Emmi holds a material relation among

the benefit that is given to her and the provision of employment. Therefore, her employer will

be liable for the FBT under “sec 66 (1) of the FBTAA 1986”.

to the decision that is given in the “Wainwright v Calvert (1947)” the tips received by Emmi

is held to be the reward for service and taxable as profits happening from employment. The

amount will be included into the taxable income of Emmi under “sec 6-5 (1) ITA Act 97”.

The case of Emmi further reports that she has made an income of $25,000 from her

part-time employment with the Crown Melbourne Restaurant. Referring to the above stated

facts of Emmi, the decision of “Hayes v FCT (1956)” should be mentioned to explain that

Emmi will be held chargeable for the sum of $25,000 because it has the direct relation with

the employment and receipts (Fane and Richardson 2015). Therefore, the amount will be

treated as taxable income earned directly from employment and will be held for assessment

within “sec 6-5”.

She further reports that she has received a perfume from one of her customer during

the Christmas that had the worth of $250. Emmi is required to denote that the receipt of

perfume is a simple gift do not have the character of earnings. Mentioning the factual

evidences denoted in “Scott v FCT (1966)” the receipt of perfume by Emmi is a solicited gift

(Burman 2015). The gift of perfume having the worth of $250 cannot be treated as ordinary

earnings simply due to the fact that gratitude was prompted for certain service since there is a

need for other types of factors to treat the receipt of gift as a taxable income.

The instances that is denoted in the situation of Emmi suggest that she is paid with a

monthly entertainment. The employer has also spent money on Emmi for meals that was

consumed by her. The entertainment expenses and the food benefit given to Emmi is a fringe

benefit within the “sec 136 (1)”. By mentioning the verdict in “Esssenboourne v Pty Ltd

(2002)” it can be stated that the fringe benefit given to Emmi holds a material relation among

the benefit that is given to her and the provision of employment. Therefore, her employer will

be liable for the FBT under “sec 66 (1) of the FBTAA 1986”.

5TAXATION LAW

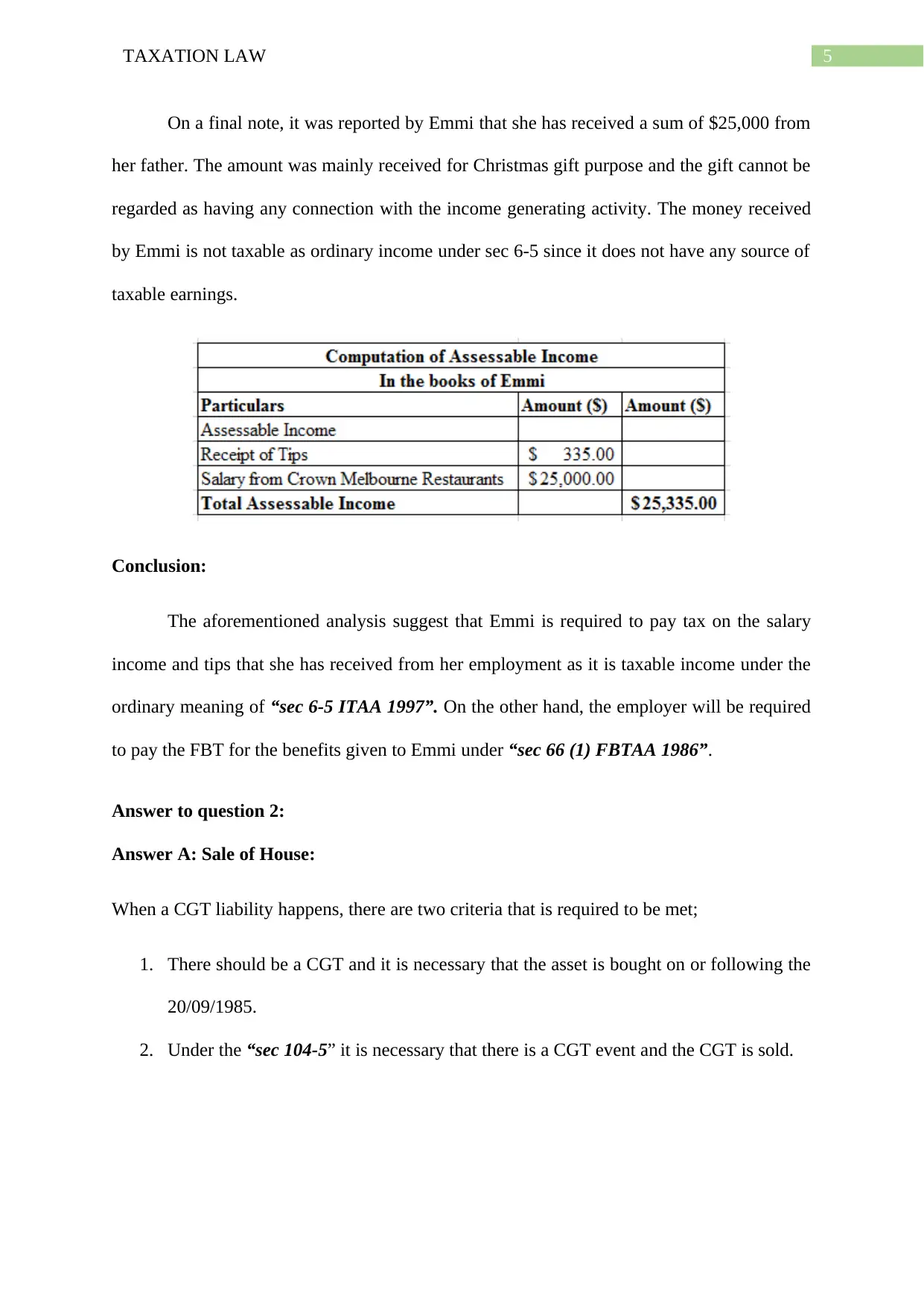

On a final note, it was reported by Emmi that she has received a sum of $25,000 from

her father. The amount was mainly received for Christmas gift purpose and the gift cannot be

regarded as having any connection with the income generating activity. The money received

by Emmi is not taxable as ordinary income under sec 6-5 since it does not have any source of

taxable earnings.

Conclusion:

The aforementioned analysis suggest that Emmi is required to pay tax on the salary

income and tips that she has received from her employment as it is taxable income under the

ordinary meaning of “sec 6-5 ITAA 1997”. On the other hand, the employer will be required

to pay the FBT for the benefits given to Emmi under “sec 66 (1) FBTAA 1986”.

Answer to question 2:

Answer A: Sale of House:

When a CGT liability happens, there are two criteria that is required to be met;

1. There should be a CGT and it is necessary that the asset is bought on or following the

20/09/1985.

2. Under the “sec 104-5” it is necessary that there is a CGT event and the CGT is sold.

On a final note, it was reported by Emmi that she has received a sum of $25,000 from

her father. The amount was mainly received for Christmas gift purpose and the gift cannot be

regarded as having any connection with the income generating activity. The money received

by Emmi is not taxable as ordinary income under sec 6-5 since it does not have any source of

taxable earnings.

Conclusion:

The aforementioned analysis suggest that Emmi is required to pay tax on the salary

income and tips that she has received from her employment as it is taxable income under the

ordinary meaning of “sec 6-5 ITAA 1997”. On the other hand, the employer will be required

to pay the FBT for the benefits given to Emmi under “sec 66 (1) FBTAA 1986”.

Answer to question 2:

Answer A: Sale of House:

When a CGT liability happens, there are two criteria that is required to be met;

1. There should be a CGT and it is necessary that the asset is bought on or following the

20/09/1985.

2. Under the “sec 104-5” it is necessary that there is a CGT event and the CGT is sold.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

An important information given in “sec 104-10 (5)(a)” which should be noted by the

taxpayer that a capital gains or loss should be simply overlooked or ignored when the asset is

acquired by the taxpayer before the 20/19/1985 (Hickman 2018).

The case facts of Liu provide suggestion that she has owned a house that she had

acquired in 1981 for a worth of $55,000. Now in the present tax year when Liu sold the house

she has derived a sum of $630,000. By referring to the explanation given in “sec 104-10 (5)

(a)”, the capital gains that is earned by Liu is required to be ignored because the house is a

pre-CGT asset since it is bought before the date of 20/09/1985.

Answer B: Sale of Car:

An important explanation is given to the taxpayer within the subdivision 108-C for

the “Personal use asset”. As mentioned in “sec 108-20 (2) & (3)”, assets when it is kept

under the possession of taxpayer for their personal enjoyment then it is treated as “Personal

use asset”. The common examples of this type of asset is boats, furniture, electric items,

motor vehicles etc. The special rule of “Personal use asset” given in the “sec 108-20 (1)”

says that a loss that happens from the personal use asset is required to be ignored by taxpayer.

The sale of car and any capital loss thereon, is normally required to be ignored. The

car which was kept under the possession of Liu is a Personal use asset within “sec 108-20 (2)

& (3)”. The disposal has resulted in “CGT event A1” under “sec 104-5 ITA Act 1997”

(Mishra and Anwar 2017). Consequently, the capital loss suffered from selling the car is

needed to be ignored under the special rules of “sec 108-20 (1)”.

Answer C: Sale of small business:

An instance was noted when Liu decided to sell her small business of photography

studio. The business was eventually taken over by a purchaser for $125,000. Therefore, Liu

An important information given in “sec 104-10 (5)(a)” which should be noted by the

taxpayer that a capital gains or loss should be simply overlooked or ignored when the asset is

acquired by the taxpayer before the 20/19/1985 (Hickman 2018).

The case facts of Liu provide suggestion that she has owned a house that she had

acquired in 1981 for a worth of $55,000. Now in the present tax year when Liu sold the house

she has derived a sum of $630,000. By referring to the explanation given in “sec 104-10 (5)

(a)”, the capital gains that is earned by Liu is required to be ignored because the house is a

pre-CGT asset since it is bought before the date of 20/09/1985.

Answer B: Sale of Car:

An important explanation is given to the taxpayer within the subdivision 108-C for

the “Personal use asset”. As mentioned in “sec 108-20 (2) & (3)”, assets when it is kept

under the possession of taxpayer for their personal enjoyment then it is treated as “Personal

use asset”. The common examples of this type of asset is boats, furniture, electric items,

motor vehicles etc. The special rule of “Personal use asset” given in the “sec 108-20 (1)”

says that a loss that happens from the personal use asset is required to be ignored by taxpayer.

The sale of car and any capital loss thereon, is normally required to be ignored. The

car which was kept under the possession of Liu is a Personal use asset within “sec 108-20 (2)

& (3)”. The disposal has resulted in “CGT event A1” under “sec 104-5 ITA Act 1997”

(Mishra and Anwar 2017). Consequently, the capital loss suffered from selling the car is

needed to be ignored under the special rules of “sec 108-20 (1)”.

Answer C: Sale of small business:

An instance was noted when Liu decided to sell her small business of photography

studio. The business was eventually taken over by a purchaser for $125,000. Therefore, Liu

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

can in this situation avail small business CGT concession under “division 152-B”. To

determine the eligibility of concession there are certain criteria that Liu is required to denote;

a. The business is defined under “Div 325 ITAA 1997” as the small business entity and

has the aggregated turnover of not greater than $2 million during the income year.

b. The net value of assets is not greater than $6 million.

c. The asset which is sold by the business is an active asset and has been used in

conducting the business.

When the above given four concessions is met, then a CGT concession is given to the

small business upon selling the business assets.

The 15-year exemption: This exemption is only given when the total amount of capital gains

which is owned by taxpayer for a greater than 15 years and the age of tax payer is not less

than 55 years.

50% reduction in capital gains: On noticing that the taxpayer qualifies for the concession,

the qualifying taxpayer are given the opportunity of reducing the capital gain by 50%, after

having applied the general 50% discount percent.

Retirement concession: The taxpayer that qualifies is allowed to disregard the capital gains

when the sale of CGT asset related to small business is restricted within $500,000 given the

proceeds obtained is used for retirement purpose.

Roll-over relief: The taxpayer is provided with the opportunity of deferring the capital gains

when the taxpayer purchases the replacement asset.

Accordingly, Liu will be considered eligible for small business CGT concession

because the value of her net asset is not greater than $2 million. As noticed here, the sales

proceeds that is earned by Liu from selling the business is $125,000. It is advised that Liu can

can in this situation avail small business CGT concession under “division 152-B”. To

determine the eligibility of concession there are certain criteria that Liu is required to denote;

a. The business is defined under “Div 325 ITAA 1997” as the small business entity and

has the aggregated turnover of not greater than $2 million during the income year.

b. The net value of assets is not greater than $6 million.

c. The asset which is sold by the business is an active asset and has been used in

conducting the business.

When the above given four concessions is met, then a CGT concession is given to the

small business upon selling the business assets.

The 15-year exemption: This exemption is only given when the total amount of capital gains

which is owned by taxpayer for a greater than 15 years and the age of tax payer is not less

than 55 years.

50% reduction in capital gains: On noticing that the taxpayer qualifies for the concession,

the qualifying taxpayer are given the opportunity of reducing the capital gain by 50%, after

having applied the general 50% discount percent.

Retirement concession: The taxpayer that qualifies is allowed to disregard the capital gains

when the sale of CGT asset related to small business is restricted within $500,000 given the

proceeds obtained is used for retirement purpose.

Roll-over relief: The taxpayer is provided with the opportunity of deferring the capital gains

when the taxpayer purchases the replacement asset.

Accordingly, Liu will be considered eligible for small business CGT concession

because the value of her net asset is not greater than $2 million. As noticed here, the sales

proceeds that is earned by Liu from selling the business is $125,000. It is advised that Liu can

8TAXATION LAW

avail the 15-year exemption because the asset has been owned by her for more than 15 years

and the age of Liu is greater than 55 years.

Answer to D: Sale of Furniture:

The special rules of personal use asset in “sec 118-10” says that capital gains upon

selling the asset is necessarily required to be ignored if the asset is having the purchase cost

of less than $10,000. Similarly, Liu reports the purchase of furniture that costs $2000 but was

sold for $4,800 (Mishra and Anwar 2017). Under the special rules of personal use asset in

“sec 118-10”, the capital gains need to be disregarded from selling the furniture.

Answer E Sale of Paintings:

The definition of collectable given in “sec 108-10 (2) & (3)” explains that it is kind of

asset that a taxpayer holds for their private use purpose. paintings, sculptures, coins, stamps

and antiques are some of the examples of collectables. Under the “sec 118-10 (1)”, the

capital gains or loss is ignored if the assets fail to meet the first element cost base.

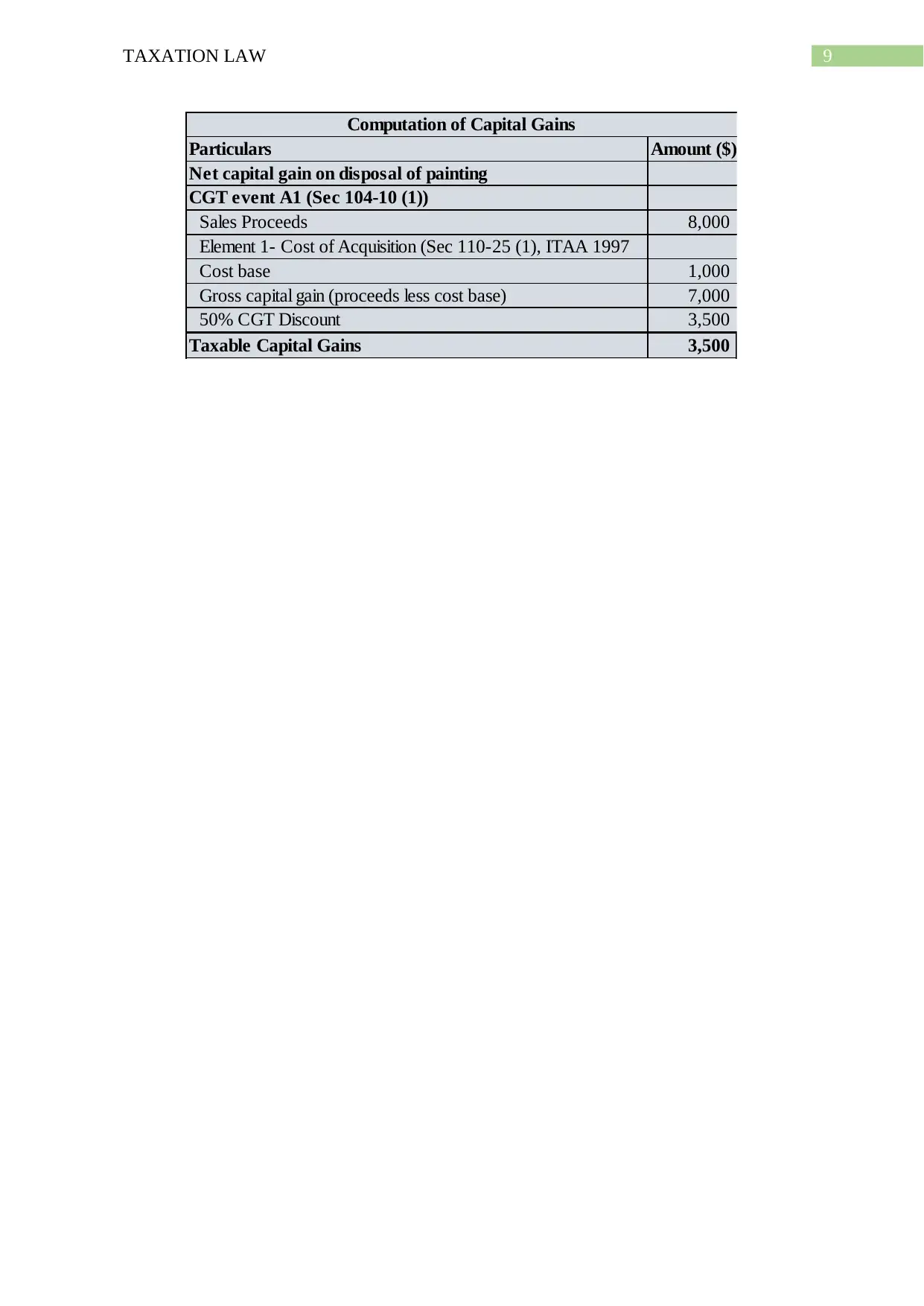

Liu here sells paintings and fetches $28,000 with none of the paintings has the cost

base of greater than $500. The paintings are categorized as collectable under “sec 108-10 (2)

& (3)” (Huizinga, Voget and Wagner 2018). The cost base of painting is less than $500, so

Liu should ignore the capital gains under “sec 108-10 (2) & (3)”. While she also sells one of

her painting having a cost base of $1000 for a sum of $8,000. The capital gains which is

made will be included into the taxable income of Liu as statutory income under “sec 102-5”.

avail the 15-year exemption because the asset has been owned by her for more than 15 years

and the age of Liu is greater than 55 years.

Answer to D: Sale of Furniture:

The special rules of personal use asset in “sec 118-10” says that capital gains upon

selling the asset is necessarily required to be ignored if the asset is having the purchase cost

of less than $10,000. Similarly, Liu reports the purchase of furniture that costs $2000 but was

sold for $4,800 (Mishra and Anwar 2017). Under the special rules of personal use asset in

“sec 118-10”, the capital gains need to be disregarded from selling the furniture.

Answer E Sale of Paintings:

The definition of collectable given in “sec 108-10 (2) & (3)” explains that it is kind of

asset that a taxpayer holds for their private use purpose. paintings, sculptures, coins, stamps

and antiques are some of the examples of collectables. Under the “sec 118-10 (1)”, the

capital gains or loss is ignored if the assets fail to meet the first element cost base.

Liu here sells paintings and fetches $28,000 with none of the paintings has the cost

base of greater than $500. The paintings are categorized as collectable under “sec 108-10 (2)

& (3)” (Huizinga, Voget and Wagner 2018). The cost base of painting is less than $500, so

Liu should ignore the capital gains under “sec 108-10 (2) & (3)”. While she also sells one of

her painting having a cost base of $1000 for a sum of $8,000. The capital gains which is

made will be included into the taxable income of Liu as statutory income under “sec 102-5”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Particulars Amount ($)

Net capital gain on disposal of painting

CGT event A1 (Sec 104-10 (1))

Sales Proceeds 8,000

Element 1- Cost of Acquisition (Sec 110-25 (1), ITAA 1997

Cost base 1,000

Gross capital gain (proceeds less cost base) 7,000

50% CGT Discount 3,500

Taxable Capital Gains 3,500

Computation of Capital Gains

Particulars Amount ($)

Net capital gain on disposal of painting

CGT event A1 (Sec 104-10 (1))

Sales Proceeds 8,000

Element 1- Cost of Acquisition (Sec 110-25 (1), ITAA 1997

Cost base 1,000

Gross capital gain (proceeds less cost base) 7,000

50% CGT Discount 3,500

Taxable Capital Gains 3,500

Computation of Capital Gains

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Atkinson, A.B. and Leigh, A., 2017. The distribution of top incomes in Australia. Economic

Record, 83(262), pp.247-261.

Burman, L., 2015. Taxing Capital Gains in Australia: Assessment and

Recommendations'. Australian Business Tax Reform in Retrospect and Prospect.

Fane, G. and Richardson, M., 2015. Negative gearing and the taxation of capital gains in

Australia. Economic Record, 81(254), pp.249-261.

Fayle, R., Chen, D.L. and Pope, J., 2015. Compliance costs of companies' income taxation in

Australia, The. Australian Tax Research Foundation Research Studies, p.110.

Findlay, C.C. and Jones, R.L., 2015. The marginal cost of Australian income

taxation. Economic Record, 58(3), pp.253-262.

Hickman, K., 2018. From capital gains to tax administration, and everything in between: in

honour of Professor Chris Evans. eJTR, 16, p.269.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Mishra, A.V. and Anwar, S., 2017. Foreign portfolio equity holdings and capital gains

taxation. International Review of Financial Analysis, 51, pp.54-68.

Richardson, G. and Lanis, R., 2017. Determinants of the variability in corporate effective tax

rates and tax reform: Evidence from Australia. Journal of accounting and public

policy, 26(6), pp.689-704.

References:

Atkinson, A.B. and Leigh, A., 2017. The distribution of top incomes in Australia. Economic

Record, 83(262), pp.247-261.

Burman, L., 2015. Taxing Capital Gains in Australia: Assessment and

Recommendations'. Australian Business Tax Reform in Retrospect and Prospect.

Fane, G. and Richardson, M., 2015. Negative gearing and the taxation of capital gains in

Australia. Economic Record, 81(254), pp.249-261.

Fayle, R., Chen, D.L. and Pope, J., 2015. Compliance costs of companies' income taxation in

Australia, The. Australian Tax Research Foundation Research Studies, p.110.

Findlay, C.C. and Jones, R.L., 2015. The marginal cost of Australian income

taxation. Economic Record, 58(3), pp.253-262.

Hickman, K., 2018. From capital gains to tax administration, and everything in between: in

honour of Professor Chris Evans. eJTR, 16, p.269.

Huizinga, H., Voget, J. and Wagner, W., 2018. Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial

Economics, 129(2), pp.306-328.

Mishra, A.V. and Anwar, S., 2017. Foreign portfolio equity holdings and capital gains

taxation. International Review of Financial Analysis, 51, pp.54-68.

Richardson, G. and Lanis, R., 2017. Determinants of the variability in corporate effective tax

rates and tax reform: Evidence from Australia. Journal of accounting and public

policy, 26(6), pp.689-704.

11TAXATION LAW

Tran-Nam, B., Evans, C., Walpole, M. and Ritchie, K., 2016. Tax compliance costs:

Research methodology and empirical evidence from Australia. National Tax Journal, pp.229-

252.

Tran-Nam, B., Evans, C., Walpole, M. and Ritchie, K., 2016. Tax compliance costs:

Research methodology and empirical evidence from Australia. National Tax Journal, pp.229-

252.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.