Financial Planning Practice (Assessment 2)

VerifiedAdded on 2022/12/27

|7

|1898

|56

AI Summary

This document provides a practice assessment on financial planning, covering topics such as suitability report and risk profiling, income and expenditure analysis, life time cash flows, scenario analysis and recommendations. It offers expert guidance and suggestions for effective financial planning.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Planning

Practice (Assessment 2)

1

Practice (Assessment 2)

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents...........................................................................................................................................2

Suitability report and risk profiling:.......................................................................................3

Income and expenditure analysis:..........................................................................................3

Life time cash flows, Scenario Analysis and Recommendations:..........................................4

Conclusion and suggested action plan for the client:.............................................................6

REFERENCES................................................................................................................................7

2

Contents...........................................................................................................................................2

Suitability report and risk profiling:.......................................................................................3

Income and expenditure analysis:..........................................................................................3

Life time cash flows, Scenario Analysis and Recommendations:..........................................4

Conclusion and suggested action plan for the client:.............................................................6

REFERENCES................................................................................................................................7

2

Suitability report and risk profiling:

Risk is considering as essential element which every individual needs to colder before taking in

decision regarding their future planning. In case of David Ford, he is wanting to invest his capital

in exchange bonds, and gold security the rate of risk regarding taking portfolio of these securities

is very high as due to the trade war between gulf countries and impact of Brexit agreement, share

price of these securities has been impacted in upcoming future time period however, their price

may be raise and it is possibility that invest in these securities may give them future benefit and

higher rate of return. Moreover, he wants to spend his money in buying house as well as save his

money for retirement time period thus he need to invest in such type of portfolio through which

risk rate is minimal and return on invest rate is high (Topa, Lunceford and Boyatzis, 2018). Thus

he needs to take decision regarding investment in bond security rather than in gold.

Income and expenditure analysis:

Analysis of incomes of David Ford exhibits that there are four major sources of income

namely: Earned income, dividends, premium bond income and interest amount received. The

earned income is of £80000 which is major source of income of David. Earned income here is

salary which is taxable in the slab of 40% tax. While David’s dividend income is £1000 which is

tax free because of dividend as well as Premium bond income of 62.50 is also tax free in UK.

Further interest received income of £200 that is also exempt since interest up to £ 1000 is exempt

in UK.

On other hand, there are mutiuple expenses incurred by Davind which are of personal

nature (means Expenses not qualify for tax reliefs) like Food, cloths, council tax, Gym

membership, Phones, Socialising,, travel, Miscellaneous, Gifts, birthdays etc. Specifically in case

of car loan repayment, car is used by David for perosnal use thus he can not claim this money

against tax (França and Hershey, 2018). Also, same treatment would be in case of

Lloyds personal loan payment amounting 99 per month and Interest payment on HSBC credit

card amounting 100 per month. In this regard, following is summary of expenses and income:

Expenses:

Particulars Amount

Food 6000

Clothes 3600

3

Risk is considering as essential element which every individual needs to colder before taking in

decision regarding their future planning. In case of David Ford, he is wanting to invest his capital

in exchange bonds, and gold security the rate of risk regarding taking portfolio of these securities

is very high as due to the trade war between gulf countries and impact of Brexit agreement, share

price of these securities has been impacted in upcoming future time period however, their price

may be raise and it is possibility that invest in these securities may give them future benefit and

higher rate of return. Moreover, he wants to spend his money in buying house as well as save his

money for retirement time period thus he need to invest in such type of portfolio through which

risk rate is minimal and return on invest rate is high (Topa, Lunceford and Boyatzis, 2018). Thus

he needs to take decision regarding investment in bond security rather than in gold.

Income and expenditure analysis:

Analysis of incomes of David Ford exhibits that there are four major sources of income

namely: Earned income, dividends, premium bond income and interest amount received. The

earned income is of £80000 which is major source of income of David. Earned income here is

salary which is taxable in the slab of 40% tax. While David’s dividend income is £1000 which is

tax free because of dividend as well as Premium bond income of 62.50 is also tax free in UK.

Further interest received income of £200 that is also exempt since interest up to £ 1000 is exempt

in UK.

On other hand, there are mutiuple expenses incurred by Davind which are of personal

nature (means Expenses not qualify for tax reliefs) like Food, cloths, council tax, Gym

membership, Phones, Socialising,, travel, Miscellaneous, Gifts, birthdays etc. Specifically in case

of car loan repayment, car is used by David for perosnal use thus he can not claim this money

against tax (França and Hershey, 2018). Also, same treatment would be in case of

Lloyds personal loan payment amounting 99 per month and Interest payment on HSBC credit

card amounting 100 per month. In this regard, following is summary of expenses and income:

Expenses:

Particulars Amount

Food 6000

Clothes 3600

3

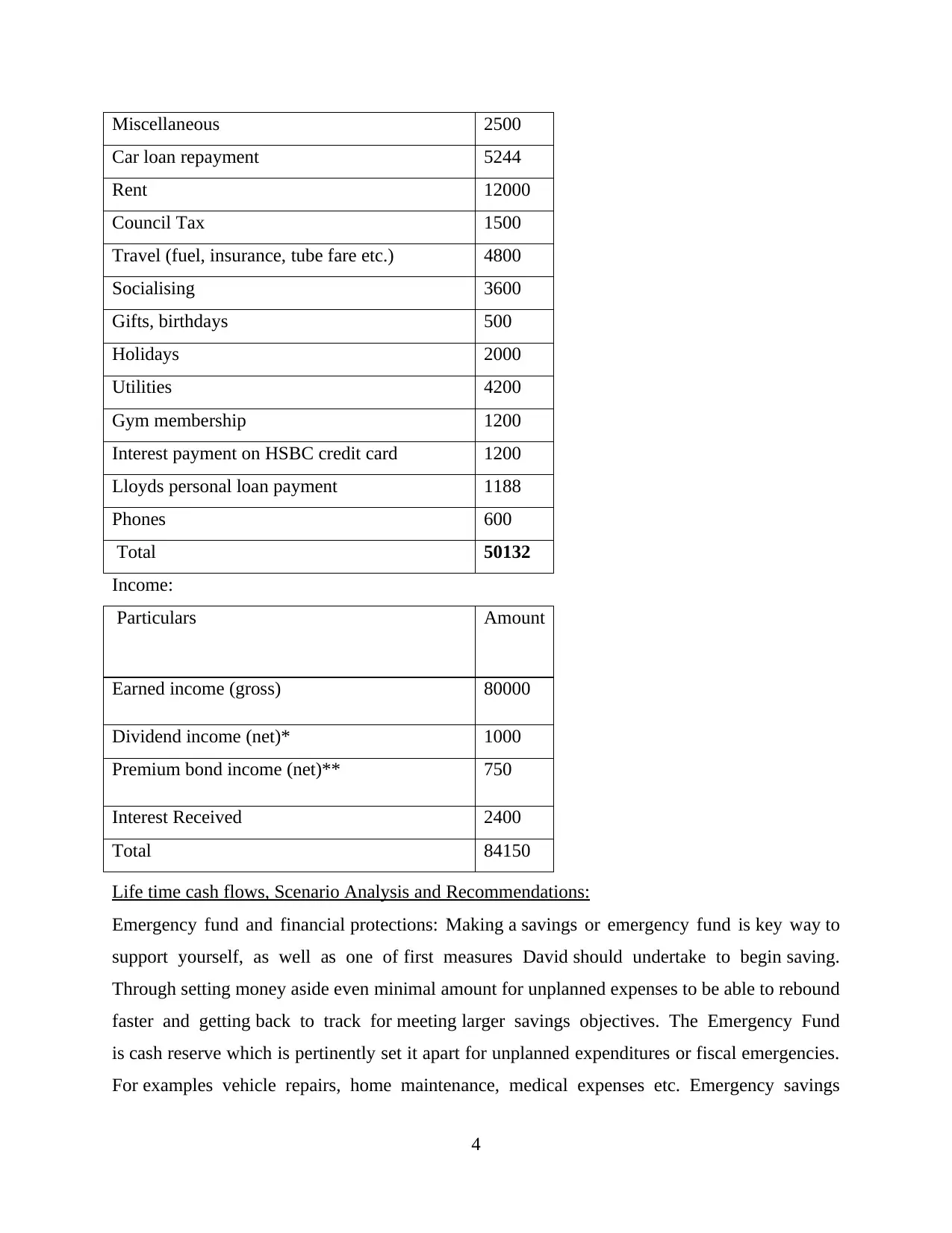

Miscellaneous 2500

Car loan repayment 5244

Rent 12000

Council Tax 1500

Travel (fuel, insurance, tube fare etc.) 4800

Socialising 3600

Gifts, birthdays 500

Holidays 2000

Utilities 4200

Gym membership 1200

Interest payment on HSBC credit card 1200

Lloyds personal loan payment 1188

Phones 600

Total 50132

Income:

Particulars Amount

Earned income (gross) 80000

Dividend income (net)* 1000

Premium bond income (net)** 750

Interest Received 2400

Total 84150

Life time cash flows, Scenario Analysis and Recommendations:

Emergency fund and financial protections: Making a savings or emergency fund is key way to

support yourself, as well as one of first measures David should undertake to begin saving.

Through setting money aside even minimal amount for unplanned expenses to be able to rebound

faster and getting back to track for meeting larger savings objectives. The Emergency Fund

is cash reserve which is pertinently set it apart for unplanned expenditures or fiscal emergencies.

For examples vehicle repairs, home maintenance, medical expenses etc. Emergency savings

4

Car loan repayment 5244

Rent 12000

Council Tax 1500

Travel (fuel, insurance, tube fare etc.) 4800

Socialising 3600

Gifts, birthdays 500

Holidays 2000

Utilities 4200

Gym membership 1200

Interest payment on HSBC credit card 1200

Lloyds personal loan payment 1188

Phones 600

Total 50132

Income:

Particulars Amount

Earned income (gross) 80000

Dividend income (net)* 1000

Premium bond income (net)** 750

Interest Received 2400

Total 84150

Life time cash flows, Scenario Analysis and Recommendations:

Emergency fund and financial protections: Making a savings or emergency fund is key way to

support yourself, as well as one of first measures David should undertake to begin saving.

Through setting money aside even minimal amount for unplanned expenses to be able to rebound

faster and getting back to track for meeting larger savings objectives. The Emergency Fund

is cash reserve which is pertinently set it apart for unplanned expenditures or fiscal emergencies.

For examples vehicle repairs, home maintenance, medical expenses etc. Emergency savings

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

should be used by David large or small unforeseen expenses or pay-outs which are not aspect of

his regular monthly expenses. One convenient approach for doing this is setting up recurring

payments through bank so that money is transferred directly from checking account to savings

account. David will be left to determine how many or how much, so once he get it set up, he will

make consistent contributions towards savings. It's a smart thing to be careful of accounts,

though, because one doesn’t pay overdraft penalties if he doesn’t have enough funds in account

at time of the automated transaction. To support you keep in mind, try putting up automatic alerts

or calendar updates to verify balance (Nam and Loibl, 2020).

Pensions (occupational pension & state pension): The term pension is defining as retirement

benefit which every employee entitled to get, if he is eligible to fulfil all the condition of entitled

of taking retirement benefits. For this purpose, person should be engaged in work as an employee

or employer in any business as well as he is entitled to be part of that organization they need to

contribute in employee scheme of organization. Person whose salary is less then £ 520 per month

is not entitled to take benefit of pension. In case of David Ford, he is working as an employee in

law firm and his salary is 80000 per annum, which means that he is entitled to take the benefit of

pension after his retirement as he is presently part of law fire where he works as an employee.

Moreover, besides that he is save his earning in bank and invested in various bond as well as

share through which he is able to take interest amount after his retirement and maturity of these

securities. This Will be part of cash inflow and source of income which help him to successfully

live his life after retirement. He is able to take pension as peer the norms of UK law (Fulda and

Lersch, 2018).

Buying a house: As given in case study, this has been ascertained that David wants to buy a

house and he is pre-occupied with saving for deposit of house. For buying a house David should

save minimum £4,000 per year as well as state with adding 25% bonus. David should make

investment in bonds or other saving scheme which may provide a saving of 4000 annually.

Further, David should optimise their expenses to increase earnings. Moreover, David can take

home loan as there is deduction on housing loan repayment which will help him to save more

taxes. David should also reduce unnecessary loans or credit card payments and contribute these

towards buying a house.

Early retirement at the age of 55: The retirement at the age of 55 years might lead to a range of

pros and cons in the context of above mentioned client. They key pros are that this can be helpful

5

his regular monthly expenses. One convenient approach for doing this is setting up recurring

payments through bank so that money is transferred directly from checking account to savings

account. David will be left to determine how many or how much, so once he get it set up, he will

make consistent contributions towards savings. It's a smart thing to be careful of accounts,

though, because one doesn’t pay overdraft penalties if he doesn’t have enough funds in account

at time of the automated transaction. To support you keep in mind, try putting up automatic alerts

or calendar updates to verify balance (Nam and Loibl, 2020).

Pensions (occupational pension & state pension): The term pension is defining as retirement

benefit which every employee entitled to get, if he is eligible to fulfil all the condition of entitled

of taking retirement benefits. For this purpose, person should be engaged in work as an employee

or employer in any business as well as he is entitled to be part of that organization they need to

contribute in employee scheme of organization. Person whose salary is less then £ 520 per month

is not entitled to take benefit of pension. In case of David Ford, he is working as an employee in

law firm and his salary is 80000 per annum, which means that he is entitled to take the benefit of

pension after his retirement as he is presently part of law fire where he works as an employee.

Moreover, besides that he is save his earning in bank and invested in various bond as well as

share through which he is able to take interest amount after his retirement and maturity of these

securities. This Will be part of cash inflow and source of income which help him to successfully

live his life after retirement. He is able to take pension as peer the norms of UK law (Fulda and

Lersch, 2018).

Buying a house: As given in case study, this has been ascertained that David wants to buy a

house and he is pre-occupied with saving for deposit of house. For buying a house David should

save minimum £4,000 per year as well as state with adding 25% bonus. David should make

investment in bonds or other saving scheme which may provide a saving of 4000 annually.

Further, David should optimise their expenses to increase earnings. Moreover, David can take

home loan as there is deduction on housing loan repayment which will help him to save more

taxes. David should also reduce unnecessary loans or credit card payments and contribute these

towards buying a house.

Early retirement at the age of 55: The retirement at the age of 55 years might lead to a range of

pros and cons in the context of above mentioned client. They key pros are that this can be helpful

5

in terms of health benefits, there can be an opportunity to start a new career or business venture.

Apart from the above pros there are some cons also which might hamper to above client after the

retirement in early age. One of the main issue is that if David will retire earlier than there can be

risk of less amount of savings, negative impact on mental health of client. The early retirement

can be effective only there is enough number of savings and secured plan for future. This is too

crucial because in the absence of proper financial plan there can be possibility to financial risk in

upcoming time period. From the given scenario this can be assessed that there is no future plan

created by David as well as there is no specific information about additional source of income

apart from the salary. So for above client this can be riskier to retire earlier at the age of 55 years

(Dalton, Gillice, Dalton and Langdon, 2019).

Conclusion and suggested action plan for the client:

Based on above discussion this has been analysed that David must change his financial planning

as per above analysis and recommendations. Setting up Emergency fund and financial protection

should be main priority of David, because without establishing an emergency funds this would

be hard for him to achieve other financial goals or targets. Further, this is also recommended here

to David that he should not take early retirement since income sources of David is limited and

expenses as well as loans are high. This is advisable to David to increase this income sources as

this will enable him to achieve his all the objectives as per planning. Further, loan should be

utilised towards purchase of home and make additional saving of £4,000 for this. Unnecessary

expenses like holidays and gifts should be minimise for increasing savings (Manly, Wells and

Bettencourt, 2017). Pensions (occupational pension & state pension) are also good way to

enhance savings and for fulfilling longer term goals. This is also recommended to choose

pension plan after retirement which provide more returns within short period. Cash flows

analysis indicate that there should be increment in cash flows by adding more dividend income,

for this David should make investment in shares of companies which provides regular dividends

and have a strong dividend history. This is also recommended here to buy adequate and

appropriate insurance plan to make safeguard against prospective pound losses. These involve

incapacity, obligations, catastrophic sudden medical expenditures, death as well as loss of

income sources.

6

Apart from the above pros there are some cons also which might hamper to above client after the

retirement in early age. One of the main issue is that if David will retire earlier than there can be

risk of less amount of savings, negative impact on mental health of client. The early retirement

can be effective only there is enough number of savings and secured plan for future. This is too

crucial because in the absence of proper financial plan there can be possibility to financial risk in

upcoming time period. From the given scenario this can be assessed that there is no future plan

created by David as well as there is no specific information about additional source of income

apart from the salary. So for above client this can be riskier to retire earlier at the age of 55 years

(Dalton, Gillice, Dalton and Langdon, 2019).

Conclusion and suggested action plan for the client:

Based on above discussion this has been analysed that David must change his financial planning

as per above analysis and recommendations. Setting up Emergency fund and financial protection

should be main priority of David, because without establishing an emergency funds this would

be hard for him to achieve other financial goals or targets. Further, this is also recommended here

to David that he should not take early retirement since income sources of David is limited and

expenses as well as loans are high. This is advisable to David to increase this income sources as

this will enable him to achieve his all the objectives as per planning. Further, loan should be

utilised towards purchase of home and make additional saving of £4,000 for this. Unnecessary

expenses like holidays and gifts should be minimise for increasing savings (Manly, Wells and

Bettencourt, 2017). Pensions (occupational pension & state pension) are also good way to

enhance savings and for fulfilling longer term goals. This is also recommended to choose

pension plan after retirement which provide more returns within short period. Cash flows

analysis indicate that there should be increment in cash flows by adding more dividend income,

for this David should make investment in shares of companies which provides regular dividends

and have a strong dividend history. This is also recommended here to buy adequate and

appropriate insurance plan to make safeguard against prospective pound losses. These involve

incapacity, obligations, catastrophic sudden medical expenditures, death as well as loss of

income sources.

6

REFERENCES

Books and Journals:

Topa, G., Lunceford, G. and Boyatzis, R.E., 2018. Financial planning for retirement: A

psychosocial perspective. Frontiers in psychology, 8, p.2338.

França, L.H. and Hershey, D.A., 2018. Financial preparation for retirement in Brazil: A cross-

cultural test of the interdisciplinary financial planning model. Journal of cross-cultural

gerontology, 33(1), pp.43-64.

Nam, Y. and Loibl, C., 2020. Financial capability and financial planning at the verge of

retirement age. Journal of Family and Economic Issues, pp.1-18.

Fulda, B.E. and Lersch, P.M., 2018. Planning until death do us part: Partnership status and

financial planning horizon. Journal of Marriage and Family, 80(2), pp.409-425.

Manly, C.A., Wells, R.S. and Bettencourt, G.M., 2017. Financial planning for college: Parental

preparation and capital conversion. Journal of Family and Economic Issues, 38(3),

pp.421-438.

Dalton, M.A., Gillice, J.M., Dalton, J.F. and Langdon, T.P., 2019. Fundamentals of Financial

Planning. Metairie, LA: Money Education.

7

Books and Journals:

Topa, G., Lunceford, G. and Boyatzis, R.E., 2018. Financial planning for retirement: A

psychosocial perspective. Frontiers in psychology, 8, p.2338.

França, L.H. and Hershey, D.A., 2018. Financial preparation for retirement in Brazil: A cross-

cultural test of the interdisciplinary financial planning model. Journal of cross-cultural

gerontology, 33(1), pp.43-64.

Nam, Y. and Loibl, C., 2020. Financial capability and financial planning at the verge of

retirement age. Journal of Family and Economic Issues, pp.1-18.

Fulda, B.E. and Lersch, P.M., 2018. Planning until death do us part: Partnership status and

financial planning horizon. Journal of Marriage and Family, 80(2), pp.409-425.

Manly, C.A., Wells, R.S. and Bettencourt, G.M., 2017. Financial planning for college: Parental

preparation and capital conversion. Journal of Family and Economic Issues, 38(3),

pp.421-438.

Dalton, M.A., Gillice, J.M., Dalton, J.F. and Langdon, T.P., 2019. Fundamentals of Financial

Planning. Metairie, LA: Money Education.

7

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.