Financial Analysis and Proposal for Event Management Company Report

VerifiedAdded on 2023/04/17

|11

|3523

|442

Report

AI Summary

This report presents a comprehensive analysis of a proposal for an event management company, Fantastic Music Decorators. It begins with an executive summary and company introduction, including details on the venue and facilities. The report delves into market research, including market seg...

A report on the Proposal for Event Management

Company

Submitted by

Student’s Name:

Professor:

University:

1 | P a g e

Company

Submitted by

Student’s Name:

Professor:

University:

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Fantastic Music Decorators is a well known in the event management industry which is

specialised in retreating its corporate customer has asked its Assistant Finance manager to

identify and propose an event that seems to be financially viable. Hence the finance manager

is writing this proposal covering the broader aspects like the introduction of the company,

results of his market research, a critical analysis of the alternative sources of funds to fund the

event, a critical analysis of the pricing strategy to be adopted for pricing the products and

services for the vent etc, which have been presented in the following section.

2 | P a g e

Fantastic Music Decorators is a well known in the event management industry which is

specialised in retreating its corporate customer has asked its Assistant Finance manager to

identify and propose an event that seems to be financially viable. Hence the finance manager

is writing this proposal covering the broader aspects like the introduction of the company,

results of his market research, a critical analysis of the alternative sources of funds to fund the

event, a critical analysis of the pricing strategy to be adopted for pricing the products and

services for the vent etc, which have been presented in the following section.

2 | P a g e

Table of Contents

Executive Summary...............................................................................................................................2

Introduction...........................................................................................................................................4

Company Profile................................................................................................................................4

Description of the Venue and its facilities.........................................................................................4

Market research................................................................................................................................4

Market research and commercial viability of the events proposed......................................................4

Market Research...............................................................................................................................5

Market Segmentation........................................................................................................................5

Projected Statement of Profit and Loss.............................................................................................5

Critical analysis of the sources of funds.................................................................................................6

Critical analysis of the purpose of financial management.....................................................................6

Critical analysis of the pricing strategy..................................................................................................7

CVP analysis...........................................................................................................................................7

Recommendation..................................................................................................................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

3 | P a g e

Executive Summary...............................................................................................................................2

Introduction...........................................................................................................................................4

Company Profile................................................................................................................................4

Description of the Venue and its facilities.........................................................................................4

Market research................................................................................................................................4

Market research and commercial viability of the events proposed......................................................4

Market Research...............................................................................................................................5

Market Segmentation........................................................................................................................5

Projected Statement of Profit and Loss.............................................................................................5

Critical analysis of the sources of funds.................................................................................................6

Critical analysis of the purpose of financial management.....................................................................6

Critical analysis of the pricing strategy..................................................................................................7

CVP analysis...........................................................................................................................................7

Recommendation..................................................................................................................................8

Conclusion.............................................................................................................................................9

References...........................................................................................................................................10

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Company Profile

Fantastic Music Decorators is one of the renowned event company based out of London. The

company has been in profit for quite some time and employs 2 full time salaried people and 5

part time staff. The company mainly deals in decoration for events and parties, weddings and

other social functions. It is well known for its unique work in political manifestations, rallies

and music festivals and concerts as well. The company was formed in 1988 by 2 students

who were studying event management in the Greenwich University (Belton, 2017).

Description of the Venue and its facilities

The venue which will be chosen is Tottenham Hotspur stadium considering the huge capacity

of 50000 people which it can accommodate. The same has also been approved by the mayor

of London Boris Johnson in the month of February, 2016. The venue has been selected as it is

centrally located and easily accessible to local public. There are a number of transport means

which are available and people who use public transport like buses and trains can also reach

there quite easily. Furthermore, the stadium has got good security measures which will be an

added advantage considering the crowd.

Market research

As per the BBC news, a Bomb attack in Manchester Arena on 16th May, 2018 is suspected to

have killed over 22 lives and over 800 people were also injured who were present there to

celebrate one of the music events. The main reason for the selection of Tottenham Hotspur

stadium was the large capacity holding of 60000 people and ample security and safety for

people. It was also established that none of such event was organised in the stadium in the

past and that makes the venue more attractive for the fans of Tottenham club as well as the

local public.

Market research and commercial viability of the events

proposed

The Assistant Finance manager has proposed to organise a corporate retreat planning for the

Raymond Group of Industries considering it as one of the most profitable option to earn a

steady market gain (Alexander, 2016). The major reason for opting for this proposal is that

the Assistant Financial Manager strongly feels that though during the period of the economic

downturn companies prefer the trend to follow the cost cutting strategy, but this is not the

case for the large corporate groups like Raymond. These corporate groups may lay off its

employees, but shall always consider the expenses incurred on training their employees as a

worth making investment. Further recently one of the representative from the personnel

training and Administrative cell has visited the Fantastic Music Decorators with a view to

organising the Training session on the recently implemented tax mechanism of the

government naming goods and service taxes. Further the Assistant financial manager strongly

believes that the market for the corporate training and leadership retreats rarely shows a

diminishing trend rather demonstrates a steady rise always.

4 | P a g e

Company Profile

Fantastic Music Decorators is one of the renowned event company based out of London. The

company has been in profit for quite some time and employs 2 full time salaried people and 5

part time staff. The company mainly deals in decoration for events and parties, weddings and

other social functions. It is well known for its unique work in political manifestations, rallies

and music festivals and concerts as well. The company was formed in 1988 by 2 students

who were studying event management in the Greenwich University (Belton, 2017).

Description of the Venue and its facilities

The venue which will be chosen is Tottenham Hotspur stadium considering the huge capacity

of 50000 people which it can accommodate. The same has also been approved by the mayor

of London Boris Johnson in the month of February, 2016. The venue has been selected as it is

centrally located and easily accessible to local public. There are a number of transport means

which are available and people who use public transport like buses and trains can also reach

there quite easily. Furthermore, the stadium has got good security measures which will be an

added advantage considering the crowd.

Market research

As per the BBC news, a Bomb attack in Manchester Arena on 16th May, 2018 is suspected to

have killed over 22 lives and over 800 people were also injured who were present there to

celebrate one of the music events. The main reason for the selection of Tottenham Hotspur

stadium was the large capacity holding of 60000 people and ample security and safety for

people. It was also established that none of such event was organised in the stadium in the

past and that makes the venue more attractive for the fans of Tottenham club as well as the

local public.

Market research and commercial viability of the events

proposed

The Assistant Finance manager has proposed to organise a corporate retreat planning for the

Raymond Group of Industries considering it as one of the most profitable option to earn a

steady market gain (Alexander, 2016). The major reason for opting for this proposal is that

the Assistant Financial Manager strongly feels that though during the period of the economic

downturn companies prefer the trend to follow the cost cutting strategy, but this is not the

case for the large corporate groups like Raymond. These corporate groups may lay off its

employees, but shall always consider the expenses incurred on training their employees as a

worth making investment. Further recently one of the representative from the personnel

training and Administrative cell has visited the Fantastic Music Decorators with a view to

organising the Training session on the recently implemented tax mechanism of the

government naming goods and service taxes. Further the Assistant financial manager strongly

believes that the market for the corporate training and leadership retreats rarely shows a

diminishing trend rather demonstrates a steady rise always.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Market Research

Fantastic Music Decorators is serving the corporate customers in terms of their contribution

in event planning by way of contributing towards its teaming and skill development events in

which it has gained the specialisation. It is because the economy is showing the state of

gradual recovery from the economic downturn, but still the big corporates are continuously

making huge investment in their Huan capital to whom they consider their biggest asset and

expect that it shall always benefit them in the long run (Choy, 2018).

The company is presently enjoying the competitive advantage in the market too. First it is

focussing on the limited amount of services so that it can best serve the customer. Secondly

its quotation rates in comparison to its customers are much lower than its customers due to its

specialisation in the relevant area.

Further in order to ensure an effective marketing strategy it has launched its own website. At

the same time the participation in various trade shows too has been increased. Our customer

can do their booking s through online website platform. Further this website is highly

effective in spreading the major information about the services being provided along with the

prices to be charged. That has proved our transparency to a great extent (Werner, 2017).

Further due to the networking done trough the local chamber of commerce it is well

perceived that significant growth has been noticed during last few years that is again going to

contribute in terms of the growth of business.

Market Segmentation

Our company s primarily focussing on the corporate customers like Raymond without much

penetrating into the social market that is also a significant source of approaching to generate

revenue for the company (Fay & Negangard, 2017).

Actually there is specific reason for the same that is the corporate groups directly approach

the company for organising its various training or team building or product launching events.

Again it is because our company can manage it in a more cost effective way as our effort is

primarily focussed on event planning and the company too shall not have to engage its

employees to look after the arrangements in relation to the same as they might be highly busy

in their day to day work (Meroño-Cerdán, et al., 2017).

The projected amount of revenue to be generated through this event for the Raymond

Industry has been summarised hereunder:

Projected Statement of Profit and Loss

Particulars Amount

(Rs)

Sales 253000/-

Direct Cost of Sales 150000

Gross Profit 103000

Gross Margin 40.71%

5 | P a g e

Fantastic Music Decorators is serving the corporate customers in terms of their contribution

in event planning by way of contributing towards its teaming and skill development events in

which it has gained the specialisation. It is because the economy is showing the state of

gradual recovery from the economic downturn, but still the big corporates are continuously

making huge investment in their Huan capital to whom they consider their biggest asset and

expect that it shall always benefit them in the long run (Choy, 2018).

The company is presently enjoying the competitive advantage in the market too. First it is

focussing on the limited amount of services so that it can best serve the customer. Secondly

its quotation rates in comparison to its customers are much lower than its customers due to its

specialisation in the relevant area.

Further in order to ensure an effective marketing strategy it has launched its own website. At

the same time the participation in various trade shows too has been increased. Our customer

can do their booking s through online website platform. Further this website is highly

effective in spreading the major information about the services being provided along with the

prices to be charged. That has proved our transparency to a great extent (Werner, 2017).

Further due to the networking done trough the local chamber of commerce it is well

perceived that significant growth has been noticed during last few years that is again going to

contribute in terms of the growth of business.

Market Segmentation

Our company s primarily focussing on the corporate customers like Raymond without much

penetrating into the social market that is also a significant source of approaching to generate

revenue for the company (Fay & Negangard, 2017).

Actually there is specific reason for the same that is the corporate groups directly approach

the company for organising its various training or team building or product launching events.

Again it is because our company can manage it in a more cost effective way as our effort is

primarily focussed on event planning and the company too shall not have to engage its

employees to look after the arrangements in relation to the same as they might be highly busy

in their day to day work (Meroño-Cerdán, et al., 2017).

The projected amount of revenue to be generated through this event for the Raymond

Industry has been summarised hereunder:

Projected Statement of Profit and Loss

Particulars Amount

(Rs)

Sales 253000/-

Direct Cost of Sales 150000

Gross Profit 103000

Gross Margin 40.71%

5 | P a g e

Payroll 40000

Other 10000

Net Profit 53000

Net Profit Margin 20.75%

Critical analysis of the sources of funds

For the event management organisations there are several means of raising finance which are

available. Few of the major ones are government grant, sponsorship fees, participation fees,

sale of merchandise products, raffle and the spectator fees (Visinescu, et al., 2017).

The above means are discussed in brief hereunder:

Government grant: In case the government considers the organisation of some specific events

as in the public interest in such a case it provided grants as a measurement of encouragement

to promote such events.

Sponsorship this is one of the oldest way for raising finance by the event management group.

Like various charitable events are organised using this mode.

Participation fees: Under this method or source the events are identified as beneficial for

certain section of people. Hence by participating in such events such group of people are

interested in availing the benefits associated with the event. In such case they are also ready

to contribute something in terms of their participation fee (Sonu, et al., 2017).

Spectator fees: These events may be basically entertainment based. Hence the spectators are

asked to pay the spectator fees for them like visiting the exhibition ceremony.

The major sources of revenue for this event may be numerous. The first and the most easily

available means of finance is asking for the advance or just to recover the cost of organising

the event form the Raymond Industry itself so that the Company does not have to think over

its blocked fund.

The second option for this can be simply putting its own money to organise the event and

then finally get the amount back with the invoice raised in favour of the Raymond group. But

in such case it might so happen that its other professional commitments may be hampered.

The third source may be use of its surplus resources that might have been left with it or the

profit earned already from its previous activities. Similarly one more option may be getting

all the items required for the event on credit provided all the suppliers are ready for it and

then release their payment dues once the bill amount is realised from the Raymond group.

Critical analysis of the purpose of financial

management

Financial management in the event industry plays a very crucial role in its success it is

because it can not say that throughout the total financial year there shall be steady demand for

its service. Then in such case sometimes the demand may be at its peak, but other times there

may be the sign of downturn too (Dichev, 2017). In such case the proper forecast of the need

of fund becomes too crucial. Again it is not the case that all of its blocked funds with the

6 | P a g e

Other 10000

Net Profit 53000

Net Profit Margin 20.75%

Critical analysis of the sources of funds

For the event management organisations there are several means of raising finance which are

available. Few of the major ones are government grant, sponsorship fees, participation fees,

sale of merchandise products, raffle and the spectator fees (Visinescu, et al., 2017).

The above means are discussed in brief hereunder:

Government grant: In case the government considers the organisation of some specific events

as in the public interest in such a case it provided grants as a measurement of encouragement

to promote such events.

Sponsorship this is one of the oldest way for raising finance by the event management group.

Like various charitable events are organised using this mode.

Participation fees: Under this method or source the events are identified as beneficial for

certain section of people. Hence by participating in such events such group of people are

interested in availing the benefits associated with the event. In such case they are also ready

to contribute something in terms of their participation fee (Sonu, et al., 2017).

Spectator fees: These events may be basically entertainment based. Hence the spectators are

asked to pay the spectator fees for them like visiting the exhibition ceremony.

The major sources of revenue for this event may be numerous. The first and the most easily

available means of finance is asking for the advance or just to recover the cost of organising

the event form the Raymond Industry itself so that the Company does not have to think over

its blocked fund.

The second option for this can be simply putting its own money to organise the event and

then finally get the amount back with the invoice raised in favour of the Raymond group. But

in such case it might so happen that its other professional commitments may be hampered.

The third source may be use of its surplus resources that might have been left with it or the

profit earned already from its previous activities. Similarly one more option may be getting

all the items required for the event on credit provided all the suppliers are ready for it and

then release their payment dues once the bill amount is realised from the Raymond group.

Critical analysis of the purpose of financial

management

Financial management in the event industry plays a very crucial role in its success it is

because it can not say that throughout the total financial year there shall be steady demand for

its service. Then in such case sometimes the demand may be at its peak, but other times there

may be the sign of downturn too (Dichev, 2017). In such case the proper forecast of the need

of fund becomes too crucial. Again it is not the case that all of its blocked funds with the

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

customers shall be immediately released by them or all of its customers can pay them the

requisite advance to organise the event management programme. Hence due to this volatile

nature of the business it becomes important for it to draft a sound financial management plan

in advance so as to meet any urgent contingency. Otherwise its long term survival can be

troublesome due to lack of fund which may cause a big hit to serve its targeted customers at

the time of their need.

Further for the event management groups it seems quite difficult to procure the fund then any

other industry. It is because not many events gain the attention of either the government or

the sponsors to encourage them to contribute for organising the same. Moreover public often

fail to see the real benefit of organising such events. This is the reason why they are found

reluctant to contribute. Hence planning for the finance plays vital role in such a case

(Marques, 2018).

Critical analysis of the pricing strategy

The pricing for the event is again a very tricky decision to be taken by the Company. It is

because it is the pricing strategy that is going to decide whether the company shall succeed to

sell out its event or it shall fail. In such a case there are only two options left, i.e., the first

being to charge the optimum price for the event being organised or the second being ensuring

the cost cutting in terms of the services being provided (Heminway, 2017).

Further in this regard there are few major factors which serves as a guide on how to charge

the price. These are the own reputation in the market, Target customer group and finally the

market which is to be served. For example if the reputation is very high then it can be

expected that reasonable price may surely be charged. Similarly the category of customers

like in this case Corporate group in which case a relationship building too shall matter, hence

keeping this actor in mind the price to be charged. Finally the market too decides the price to

be charged as same price can not be charged from several markets.

Further the major pricing strategies followed by this industry are Flat pay charges, Hourly ay

charges, commission basis, a combination of hourly plus expenses and percentage based

commission (Jefferson, 2017).

As per the flat rate percentage method the pricing strategy seems to be highly transparent as

the customer is having the advance knowledge of the amount that is to be paid by him.

In case of the hourly rate charges it is the duration of the event that is gong to decide how

much to pay. That is higher the duration, higher shall be the charge and vice-versa.

A very few of the event organisers prefer to charge commission from the travel agents and

the hotels etc booked for the specific event.

Another strategy may be to charge hourly and additionally charge for the expenses

specifically incurred for the event (Goldmann, 2016).

Finally for those fund raising events it is the percentage of the amount raised through the fund

that is charged by the event managers.

In our case it is being suggested to charge on hourly basis, as it seems much justified in the

given case.

7 | P a g e

requisite advance to organise the event management programme. Hence due to this volatile

nature of the business it becomes important for it to draft a sound financial management plan

in advance so as to meet any urgent contingency. Otherwise its long term survival can be

troublesome due to lack of fund which may cause a big hit to serve its targeted customers at

the time of their need.

Further for the event management groups it seems quite difficult to procure the fund then any

other industry. It is because not many events gain the attention of either the government or

the sponsors to encourage them to contribute for organising the same. Moreover public often

fail to see the real benefit of organising such events. This is the reason why they are found

reluctant to contribute. Hence planning for the finance plays vital role in such a case

(Marques, 2018).

Critical analysis of the pricing strategy

The pricing for the event is again a very tricky decision to be taken by the Company. It is

because it is the pricing strategy that is going to decide whether the company shall succeed to

sell out its event or it shall fail. In such a case there are only two options left, i.e., the first

being to charge the optimum price for the event being organised or the second being ensuring

the cost cutting in terms of the services being provided (Heminway, 2017).

Further in this regard there are few major factors which serves as a guide on how to charge

the price. These are the own reputation in the market, Target customer group and finally the

market which is to be served. For example if the reputation is very high then it can be

expected that reasonable price may surely be charged. Similarly the category of customers

like in this case Corporate group in which case a relationship building too shall matter, hence

keeping this actor in mind the price to be charged. Finally the market too decides the price to

be charged as same price can not be charged from several markets.

Further the major pricing strategies followed by this industry are Flat pay charges, Hourly ay

charges, commission basis, a combination of hourly plus expenses and percentage based

commission (Jefferson, 2017).

As per the flat rate percentage method the pricing strategy seems to be highly transparent as

the customer is having the advance knowledge of the amount that is to be paid by him.

In case of the hourly rate charges it is the duration of the event that is gong to decide how

much to pay. That is higher the duration, higher shall be the charge and vice-versa.

A very few of the event organisers prefer to charge commission from the travel agents and

the hotels etc booked for the specific event.

Another strategy may be to charge hourly and additionally charge for the expenses

specifically incurred for the event (Goldmann, 2016).

Finally for those fund raising events it is the percentage of the amount raised through the fund

that is charged by the event managers.

In our case it is being suggested to charge on hourly basis, as it seems much justified in the

given case.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

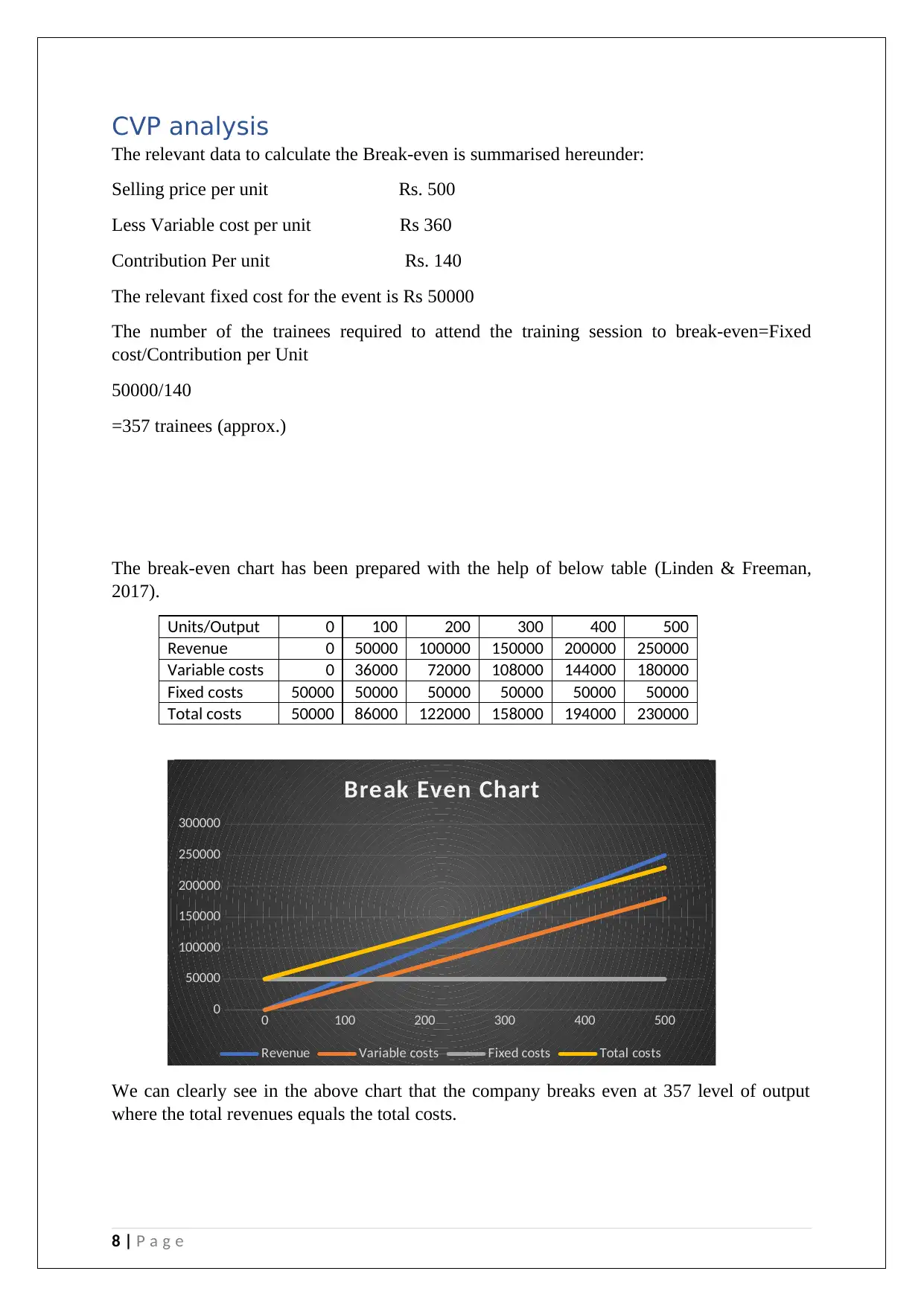

CVP analysis

The relevant data to calculate the Break-even is summarised hereunder:

Selling price per unit Rs. 500

Less Variable cost per unit Rs 360

Contribution Per unit Rs. 140

The relevant fixed cost for the event is Rs 50000

The number of the trainees required to attend the training session to break-even=Fixed

cost/Contribution per Unit

50000/140

=357 trainees (approx.)

The break-even chart has been prepared with the help of below table (Linden & Freeman,

2017).

Units/Output 0 100 200 300 400 500

Revenue 0 50000 100000 150000 200000 250000

Variable costs 0 36000 72000 108000 144000 180000

Fixed costs 50000 50000 50000 50000 50000 50000

Total costs 50000 86000 122000 158000 194000 230000

0 100 200 300 400 500

0

50000

100000

150000

200000

250000

300000

Break Even Chart

Revenue Variable costs Fixed costs Total costs

We can clearly see in the above chart that the company breaks even at 357 level of output

where the total revenues equals the total costs.

8 | P a g e

The relevant data to calculate the Break-even is summarised hereunder:

Selling price per unit Rs. 500

Less Variable cost per unit Rs 360

Contribution Per unit Rs. 140

The relevant fixed cost for the event is Rs 50000

The number of the trainees required to attend the training session to break-even=Fixed

cost/Contribution per Unit

50000/140

=357 trainees (approx.)

The break-even chart has been prepared with the help of below table (Linden & Freeman,

2017).

Units/Output 0 100 200 300 400 500

Revenue 0 50000 100000 150000 200000 250000

Variable costs 0 36000 72000 108000 144000 180000

Fixed costs 50000 50000 50000 50000 50000 50000

Total costs 50000 86000 122000 158000 194000 230000

0 100 200 300 400 500

0

50000

100000

150000

200000

250000

300000

Break Even Chart

Revenue Variable costs Fixed costs Total costs

We can clearly see in the above chart that the company breaks even at 357 level of output

where the total revenues equals the total costs.

8 | P a g e

Recommendation

After going through the above details it can be said that the best way to fund the event can be

to ask for the advance from the Raymond group. The major reason to be provided for this is

that as all of the various means of finance available for the event is not to made applicable

the in the given case other than the sponsorship fees. In other words, this event is going to be

sponsored by the Raymond group for the benefit of its own as it shall increase the working

efficiency of its valuable employees (Kim, et al., 2017). Such type of sponsorship from

Raymond group shall improve the business image of the group too. Actually sponsorship is

one of the most easily found and adopted practice by the large Corporate groups, as it is

somewhere being associated with their social image. One more mode that is to be suggested

is the participation fee. It’s not required that the participants have to bear the total cost of the

training session, but the same can be shared by the Raymond group and the participants

partially. Even the Raymond group can offer its employees that such participation fee is not

to be paid by them to the event management company, but the same shall get deducted from

their remuneration (Meroño-Cerdán, et al., 2017).

If this second strategy is followed then it shall ensure better scenario. The reason for the same

is given as the Raymond group shall be able to shift the expenses on training partially on its

employees. Employees too shall be able to give proper value to the training programme.

Moreover if some sort of certificates are provided for this type of training then also it shall

attract more number of participants for the training session (Trieu, 2017).

So far as the pricing strategy is concerned as the Raymond group is a major group in the

Textile industry which can significantly contribute towards the future growth of this business

of the vent management hence it is being advised that hourly rate pricing strategy may be

adopted in the given case (Vieira, et al., 2017). In the given case the flat rate does not seem to

be justified as because of the time factor. If we consider the flat rate then it shall cause

injustice to the company. Whereas hourly charge can encourage the event management

company to provide much better service too. Because there is no certainty as to the factor that

how long the Raymond group is going to utilise the services to be provided by the event

management company. The exploitation of the resources provided by the event management

group is to be justified with the return they are earning on the same (Dai & Vasarhelyi, 2017).

Conclusion

From the above analysis and discussion it is quite clear that the event organisation plan as

submitted by the Assistant finance Manager of Fantastic Music Decorators seems to be

highly justified having seen the proposal drafted by him especially keeping in mind the offer

made by Raymond group for providing the Goods and service tax training to its finance team.

Further not only in terms of organising this specific event but it is being expected that in near

future it shall ensure a long term business relationship with such a textile giant. That is

ultimately going to contribute towards the future growth of the business of the company.

Our analysis also reflects the critical evaluation of the factors that are to be kept in mind

while considering about the various options available to fund the event organising. Not only

this but what are the various influencers in determining the best pricing strategy for this

business have also been discussed above. One most important thing that can be perceived in

the given case is the company s primarily planning for focussing on very few of the services

9 | P a g e

After going through the above details it can be said that the best way to fund the event can be

to ask for the advance from the Raymond group. The major reason to be provided for this is

that as all of the various means of finance available for the event is not to made applicable

the in the given case other than the sponsorship fees. In other words, this event is going to be

sponsored by the Raymond group for the benefit of its own as it shall increase the working

efficiency of its valuable employees (Kim, et al., 2017). Such type of sponsorship from

Raymond group shall improve the business image of the group too. Actually sponsorship is

one of the most easily found and adopted practice by the large Corporate groups, as it is

somewhere being associated with their social image. One more mode that is to be suggested

is the participation fee. It’s not required that the participants have to bear the total cost of the

training session, but the same can be shared by the Raymond group and the participants

partially. Even the Raymond group can offer its employees that such participation fee is not

to be paid by them to the event management company, but the same shall get deducted from

their remuneration (Meroño-Cerdán, et al., 2017).

If this second strategy is followed then it shall ensure better scenario. The reason for the same

is given as the Raymond group shall be able to shift the expenses on training partially on its

employees. Employees too shall be able to give proper value to the training programme.

Moreover if some sort of certificates are provided for this type of training then also it shall

attract more number of participants for the training session (Trieu, 2017).

So far as the pricing strategy is concerned as the Raymond group is a major group in the

Textile industry which can significantly contribute towards the future growth of this business

of the vent management hence it is being advised that hourly rate pricing strategy may be

adopted in the given case (Vieira, et al., 2017). In the given case the flat rate does not seem to

be justified as because of the time factor. If we consider the flat rate then it shall cause

injustice to the company. Whereas hourly charge can encourage the event management

company to provide much better service too. Because there is no certainty as to the factor that

how long the Raymond group is going to utilise the services to be provided by the event

management company. The exploitation of the resources provided by the event management

group is to be justified with the return they are earning on the same (Dai & Vasarhelyi, 2017).

Conclusion

From the above analysis and discussion it is quite clear that the event organisation plan as

submitted by the Assistant finance Manager of Fantastic Music Decorators seems to be

highly justified having seen the proposal drafted by him especially keeping in mind the offer

made by Raymond group for providing the Goods and service tax training to its finance team.

Further not only in terms of organising this specific event but it is being expected that in near

future it shall ensure a long term business relationship with such a textile giant. That is

ultimately going to contribute towards the future growth of the business of the company.

Our analysis also reflects the critical evaluation of the factors that are to be kept in mind

while considering about the various options available to fund the event organising. Not only

this but what are the various influencers in determining the best pricing strategy for this

business have also been discussed above. One most important thing that can be perceived in

the given case is the company s primarily planning for focussing on very few of the services

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

it can provide to its customers. Generally one of the major reason for the failure of this type

of business is nothing but they can not make themselves specialised. But this company has

adopted the correct strategy in this regard. Further in terms of funding this type of event if the

partial contribution from those participants can be obtained then it shall make the

arrangement of such events in future too and that seems to be much justified. Hence it is

suggested to the company to give approval to this project as written by the Assistant finance

manager of the company as he has already undergone a broad market analysis along with the

market segment analysis done by him. Further he has made sufficient effort to justify his

proposal with the help of the various accounting tools like the projected profit and loss

account along with the cost volume profit technique. Hence we can not say that the proposal

is in vague status. That is the reason behind supporting the proposal and recommending its

acceptance.

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. 3 ed. London:

Macat International ltd.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 2(1), p. 145.

Dai, J. & Vasarhelyi, M. A., 2017. Towards blockchain-based accounting and assurance. Journal of

Information Systems.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, Volume 38, pp. 37-49.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 5(2), pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, 1(2), pp. 353-354.

10 | P a g e

of business is nothing but they can not make themselves specialised. But this company has

adopted the correct strategy in this regard. Further in terms of funding this type of event if the

partial contribution from those participants can be obtained then it shall make the

arrangement of such events in future too and that seems to be much justified. Hence it is

suggested to the company to give approval to this project as written by the Assistant finance

manager of the company as he has already undergone a broad market analysis along with the

market segment analysis done by him. Further he has made sufficient effort to justify his

proposal with the help of the various accounting tools like the projected profit and loss

account along with the cost volume profit technique. Hence we can not say that the proposal

is in vague status. That is the reason behind supporting the proposal and recommending its

acceptance.

References

Alexander, F., 2016. The Changing Face of Accountability. The Journal of Higher Education, 71(4), pp.

411-431.

Belton, P., 2017. Competitive Strategy: Creating and Sustaining Superior Performance. 3 ed. London:

Macat International ltd.

Choy, Y. K., 2018. Cost-benefit Analysis, Values, Wellbeing and Ethics: An Indigenous Worldview

Analysis. Ecological Economics, 2(1), p. 145.

Dai, J. & Vasarhelyi, M. A., 2017. Towards blockchain-based accounting and assurance. Journal of

Information Systems.

Dichev, I., 2017. On the conceptual foundations of financial reporting. Accounting and Business

Research, 47(6), pp. 617-632.

Fay, R. & Negangard, E., 2017. Manual journal entry testing : Data analytics and the risk of fraud.

Journal of Accounting Education, Volume 38, pp. 37-49.

Goldmann, K., 2016. Financial Liquidity and Profitability Management in Practice of Polish Business.

Financial Environment and Business Development, Volume 4, pp. 103-112.

Heminway, J., 2017. Shareholder Wealth Maximization as a Function of Statutes, Decisional Law, and

Organic Documents. SSRN, 5(2), pp. 1-35.

Jefferson, M., 2017. Energy, Complexity and Wealth Maximization, R. Ayres. Springer, Switzerland.

Technological Forecasting and Social Change, 1(2), pp. 353-354.

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Kim, M., Schmidgall, R. & Damitio, J., 2017. Key Managerial Accounting Skills for Lodging Industry

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of Hospitality

& Tourism Administration, , 18(1), pp. 23-40.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making.

Business Ethics Quarterly, 27(3), pp. 353-379.

Marques, R. P. F., 2018. Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, pp. 820-830.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, 7(1), pp. 1-15.

Sonu, C., Ahn, H. & Choi, A., 2017. Audit fee pressure and audit risk: evidence from the financial crisis

of 2008. Asia-Pacific Journal of Accounting & Economics , 24(1-2), pp. 127-144.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, Volume 93, pp. 111-124.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1), pp. 25-32.

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, Volume 25, pp. 57-80.

11 | P a g e

Managers: The Third Phase of a Repeated Cross-Sectional Study. International Journal of Hospitality

& Tourism Administration, , 18(1), pp. 23-40.

Linden, B. & Freeman, R., 2017. Profit and Other Values: Thick Evaluation in Decision Making.

Business Ethics Quarterly, 27(3), pp. 353-379.

Marques, R. P. F., 2018. Continuous Assurance and the Use of Technology for Business Compliance.

Encyclopedia of Information Science and Technology, pp. 820-830.

Meroño-Cerdán, A., Lopez-Nicolas, C. & Molina-Castillo, F., 2017. Risk aversion, innovation and

performance in family firms. Economics of Innovation and new technology, 7(1), pp. 1-15.

Sonu, C., Ahn, H. & Choi, A., 2017. Audit fee pressure and audit risk: evidence from the financial crisis

of 2008. Asia-Pacific Journal of Accounting & Economics , 24(1-2), pp. 127-144.

Trieu, V., 2017. Getting value from Business Intelligence systems: A review and research agenda.

Decision Support Systems, Volume 93, pp. 111-124.

Vieira, R., O’Dwyer, B. & Schneider, R., 2017. Aligning Strategy and Performance Management

Systems. SAGE Journals, 30(1), pp. 25-32.

Visinescu, L., Jones, M. & Sidorova, A., 2017. Improving Decision Quality: The Role of Business

Intelligence. Journal of Computer Information Systems, 57(1), pp. 58-66.

Werner, M., 2017. Financial process mining - Accounting data structure dependent control flow

inference. International Journal of Accounting Information Systems, Volume 25, pp. 57-80.

11 | P a g e

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.