HI5017 Managerial Accounting: Financial Analysis of A2 Milk Company

VerifiedAdded on 2023/04/25

|19

|4260

|278

Report

AI Summary

This report evaluates the financial performance of A2 Milk Company Limited for 2018 and anticipates future performance based on company assumptions. It discusses top-down and bottom-up budgeting approaches and estimates the 2019 income statement. The analysis covers components of the master budget and their impact on financial performance. The report compares the actual 2018 income statement with the projected 2019 budget, emphasizing the importance of aligning budgeted figures with past performance for effective financial management. The report finds that with adequate marketing techniques, the A2 Milk Limited Company Limited has the ability of meeting the budgeted income target by increasing its product demand in the market.

Running head: MANAGERIAL ACCOUNTING

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Managerial Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGERIAL ACCOUNTING

Executive Summary:

The report has focused on evaluating the financial performance of the A2 Milk Company

Limited for 2018 along with anticipating future performance depending on a number of

assumptions made by the organisation. It is an ASX listed organisation producing milk and other

dairy products operating in Australia and New Zealand. By enforcing adequate marketing

techniques, the A2 Milk Limited Company Limited has the ability of meeting the budgeted

income target by increasing its product demand in the market. The increase in overall sales of

the firm is critical, since the management could generate the adequate cash flows to meet its

expenses and outflows. The projected income statement of the A2 Milk Limited Company

Limited is found to be suitable for the organisation in comparison to the financial performance

in 2018. However, it is to be noted that the generated budgeted figures are not in tandem with

the income statement prepared by the organisation in 2018. Therefore, it is crucial to develop

the budgeted income statement depending on relevant growth observed in the past accounting

year.

Executive Summary:

The report has focused on evaluating the financial performance of the A2 Milk Company

Limited for 2018 along with anticipating future performance depending on a number of

assumptions made by the organisation. It is an ASX listed organisation producing milk and other

dairy products operating in Australia and New Zealand. By enforcing adequate marketing

techniques, the A2 Milk Limited Company Limited has the ability of meeting the budgeted

income target by increasing its product demand in the market. The increase in overall sales of

the firm is critical, since the management could generate the adequate cash flows to meet its

expenses and outflows. The projected income statement of the A2 Milk Limited Company

Limited is found to be suitable for the organisation in comparison to the financial performance

in 2018. However, it is to be noted that the generated budgeted figures are not in tandem with

the income statement prepared by the organisation in 2018. Therefore, it is crucial to develop

the budgeted income statement depending on relevant growth observed in the past accounting

year.

2MANAGERIAL ACCOUNTING

Table of Contentss

Introduction:....................................................................................................................................3

Part a:...............................................................................................................................................4

Part b:...............................................................................................................................................8

Part c:.............................................................................................................................................11

Part d:............................................................................................................................................13

Conclusion:....................................................................................................................................14

References:....................................................................................................................................16

Table of Contentss

Introduction:....................................................................................................................................3

Part a:...............................................................................................................................................4

Part b:...............................................................................................................................................8

Part c:.............................................................................................................................................11

Part d:............................................................................................................................................13

Conclusion:....................................................................................................................................14

References:....................................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGERIAL ACCOUNTING

Introduction:

The report has focused on evaluating the financial performance of the A2 Milk Company

Limited for 2018 along with anticipating future performance depending on a number of

assumptions made by the organisation. It is an ASX listed organisation producing milk and other

dairy products operating in Australia and New Zealand (The a2 Milk Company 2019). In

addition, a detailed discussion of the top-down and bottom-up approaches to the budget

process is made in this paper. Furthermore, the income statement for 2019 has been

estimated, which could help in determining the future income of the firm. Adequate analysis of

the components of master budget is conducted for determining the impact on the overall

financial performance of the organisation. The analysis of the components of master budget

assists the management to identify income and expenses, which is anticipated to carry out the

business operations in future. By assessing the projected income statement, it would help in

adopting suitable measures for the organisation for generating the desired level of income.

Finally, the report covers comparison of the actual income statement of 2018 with the

budgeted income statement of 2019 for the A2 Milk Company Limited.

Introduction:

The report has focused on evaluating the financial performance of the A2 Milk Company

Limited for 2018 along with anticipating future performance depending on a number of

assumptions made by the organisation. It is an ASX listed organisation producing milk and other

dairy products operating in Australia and New Zealand (The a2 Milk Company 2019). In

addition, a detailed discussion of the top-down and bottom-up approaches to the budget

process is made in this paper. Furthermore, the income statement for 2019 has been

estimated, which could help in determining the future income of the firm. Adequate analysis of

the components of master budget is conducted for determining the impact on the overall

financial performance of the organisation. The analysis of the components of master budget

assists the management to identify income and expenses, which is anticipated to carry out the

business operations in future. By assessing the projected income statement, it would help in

adopting suitable measures for the organisation for generating the desired level of income.

Finally, the report covers comparison of the actual income statement of 2018 with the

budgeted income statement of 2019 for the A2 Milk Company Limited.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGERIAL ACCOUNTING

Part a:

Figure 1: Components of the master budget

(Source: Balakrishnan, Labro and Soderstrom 2014)

With the help of the above figure, the different components of the master budget are

represented, which a firm uses to prepare budgets for the respective periods. These

components primarily assist the management to acquire the required level of income from

operations and this has reduced the probability of occurrence of variance from the budgeted

sales figure to actual sales figure (Bandy 2014). Moreover, the components of budget direct

help the organisation in setting up relevant expenses and income, which would be derived from

business operations over the period. As pointed out by Banker and Byzalov (2014), master

budget would assist the organisation to derive high level of income from business operations,

which could enhance the overall efficiency of the management. The master budget would help

in obtaining the needed level of funds for supporting the master budget and due to this; there

Part a:

Figure 1: Components of the master budget

(Source: Balakrishnan, Labro and Soderstrom 2014)

With the help of the above figure, the different components of the master budget are

represented, which a firm uses to prepare budgets for the respective periods. These

components primarily assist the management to acquire the required level of income from

operations and this has reduced the probability of occurrence of variance from the budgeted

sales figure to actual sales figure (Bandy 2014). Moreover, the components of budget direct

help the organisation in setting up relevant expenses and income, which would be derived from

business operations over the period. As pointed out by Banker and Byzalov (2014), master

budget would assist the organisation to derive high level of income from business operations,

which could enhance the overall efficiency of the management. The master budget would help

in obtaining the needed level of funds for supporting the master budget and due to this; there

5MANAGERIAL ACCOUNTING

would be significant improvements in the entire business operations. The master budget

consists of a number of components, which are described as follows:

Sales budget:

This is the initial element of the master budget, which allows the organisation to detect

the level of selling units to be incurred from operations. The selling price per unit and number

of units sold are estimated for the upcoming quarters or periods in sales budget. Moreover, the

values included in the sales budget are identified from the previous growth in selling figures,

which are derived by the firm. The sales budget exercises direct impact on the components of

the master budget, as rise in selling units would have effect on the expenses and production

needs of the firm (Barr and McClellan 2018).

Production budget:

The main reason behind the use of production budget by the organisation is that they

could detect the estimated level of production, which is needed to be conducted by the

management so that they could support the overall product demand (Bhalla 2014). In addition,

the production budget provides enhanced value to the organisation to determine the

requirement of raw materials along with other purchases, which are needed for ensuring

smooth flow of business operations. The production budget ascertains the companies in

determining the activity levels, which would be needed for supporting sales demand from the

customers (Chenhall and Moers 2015).

Cash budget:

would be significant improvements in the entire business operations. The master budget

consists of a number of components, which are described as follows:

Sales budget:

This is the initial element of the master budget, which allows the organisation to detect

the level of selling units to be incurred from operations. The selling price per unit and number

of units sold are estimated for the upcoming quarters or periods in sales budget. Moreover, the

values included in the sales budget are identified from the previous growth in selling figures,

which are derived by the firm. The sales budget exercises direct impact on the components of

the master budget, as rise in selling units would have effect on the expenses and production

needs of the firm (Barr and McClellan 2018).

Production budget:

The main reason behind the use of production budget by the organisation is that they

could detect the estimated level of production, which is needed to be conducted by the

management so that they could support the overall product demand (Bhalla 2014). In addition,

the production budget provides enhanced value to the organisation to determine the

requirement of raw materials along with other purchases, which are needed for ensuring

smooth flow of business operations. The production budget ascertains the companies in

determining the activity levels, which would be needed for supporting sales demand from the

customers (Chenhall and Moers 2015).

Cash budget:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGERIAL ACCOUNTING

The cash budget is mainly prepared with the intent of determining the income and

expense levels expected to be derived from operations. The cash budget assists in representing

the cash position which the firm would derive in the accounting year. The cash budget is

prepared after the sales and production budget are prepared, which would assist the

management to determine the overall cash flows expected to occur from a particular

timeframe.

Direct labour budget:

The direct labour budget would be affected directly by the sales budget expected to be

derived from the firm. The rising level of output, which is needed by the sales budget, would

exercise direct influence on the direct labour requirements in the production system (Cokins

2014). Hence, direct labour budget assists the firms in determining the staff levels needed in

the production function for helping the production results along with compliance to the sales

budget. The direct labour budget is made after the preparation of production units and this

determines the level of labour input needed for the upcoming period (Finkler, Smith and

Calabrese 2019).

Direct materials budget:

After production budget and sales budget are prepared, an organisation prepares its

direct materials budget, which help in determining the level of materials needed in order to

support sales demand from the customers. In addition to this, the direct materials budget

would aid in determining the expense level adequately needed by the organisation in order to

enhance its production needs. Furthermore, the direct materials budget would help in

The cash budget is mainly prepared with the intent of determining the income and

expense levels expected to be derived from operations. The cash budget assists in representing

the cash position which the firm would derive in the accounting year. The cash budget is

prepared after the sales and production budget are prepared, which would assist the

management to determine the overall cash flows expected to occur from a particular

timeframe.

Direct labour budget:

The direct labour budget would be affected directly by the sales budget expected to be

derived from the firm. The rising level of output, which is needed by the sales budget, would

exercise direct influence on the direct labour requirements in the production system (Cokins

2014). Hence, direct labour budget assists the firms in determining the staff levels needed in

the production function for helping the production results along with compliance to the sales

budget. The direct labour budget is made after the preparation of production units and this

determines the level of labour input needed for the upcoming period (Finkler, Smith and

Calabrese 2019).

Direct materials budget:

After production budget and sales budget are prepared, an organisation prepares its

direct materials budget, which help in determining the level of materials needed in order to

support sales demand from the customers. In addition to this, the direct materials budget

would aid in determining the expense level adequately needed by the organisation in order to

enhance its production needs. Furthermore, the direct materials budget would help in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGERIAL ACCOUNTING

providing an overview of the material needs after the analysis of inventory currently held for

production (Karadag 2015).

Factory overhead budget:

By using this budget, the firm could obtain an insight of the factory expenses, which it

has to spend besides costs related to direct labour and direct materials. The information

included in the cost of budget has direct relationship with the cost of sales of the firm. This

would help in determining the level of expenses, which is necessary for the form to incur in

order to provide adequate support to the future selling units. The factory overhead budget is

considered to be beneficial in nature, as it takes into account a huge portion of expenses, which

the company has to incur so that it could accommodate the estimated sales (Kotas 2014).

Selling and administrative expense budget:

For evaluating the estimated operating expenses, the managers of any organisation use

this budget along with other manufacturing expenses incurred in the accounting year. In

addition, this evaluation helps the organisation to determine the selling and administrative

expenses needed to be understood by the organisation for providing its adequate support to its

future operations. By computing these expenses, the level of spending could be determined

and it is needed to be understood by the organisation so that its operations could be supported

in the accounting year through analysis of the outcomes (Lavia López and Hiebl 2014).

Budgeted financial statements:

providing an overview of the material needs after the analysis of inventory currently held for

production (Karadag 2015).

Factory overhead budget:

By using this budget, the firm could obtain an insight of the factory expenses, which it

has to spend besides costs related to direct labour and direct materials. The information

included in the cost of budget has direct relationship with the cost of sales of the firm. This

would help in determining the level of expenses, which is necessary for the form to incur in

order to provide adequate support to the future selling units. The factory overhead budget is

considered to be beneficial in nature, as it takes into account a huge portion of expenses, which

the company has to incur so that it could accommodate the estimated sales (Kotas 2014).

Selling and administrative expense budget:

For evaluating the estimated operating expenses, the managers of any organisation use

this budget along with other manufacturing expenses incurred in the accounting year. In

addition, this evaluation helps the organisation to determine the selling and administrative

expenses needed to be understood by the organisation for providing its adequate support to its

future operations. By computing these expenses, the level of spending could be determined

and it is needed to be understood by the organisation so that its operations could be supported

in the accounting year through analysis of the outcomes (Lavia López and Hiebl 2014).

Budgeted financial statements:

8MANAGERIAL ACCOUNTING

The budgeted financial statements are to be prepared by the firm after the

aforementioned components of the master budget are prepared effectively. The reason is that

they assist in preparing the balance sheet and income statement for the accounting year

(Melitski and Manoharan 2014). In addition, with the help of budgeted financial statements,

the company could determine the projected incomes expected to be earned over the upcoming

accounting periods. Due to this, the income and expense levels could be determined in the

accounting period.

Part b:

It is critical to engage various business units when there is preparation of a

comprehensive budget. This mandates the requirement of all unit representatives to participate

in the budget development process appropriately. Normally, a budget committee is present to

look after the process, which comprises of some top level executives of the organisation

(Menifield 2017). These personnel offer valuable judgements about the aspects having

association with sales, financing, production and other operating stages. Along with these, the

position of these individuals needs to be proper so that they could provide better information

to their concerned units along with advice on resource needs and opportunities.

There are a number of differences that could be noticed between top-down budget

approach and bottom-up budget approach that the firms could utilise for the preparation of

budgets. In addition, the comparison would help in detecting the suitable budgeting process,

which the organisations could utilise for preparing budget so that its business operations could

be supported adequately. The two above-stated approaches are mainly used in different

The budgeted financial statements are to be prepared by the firm after the

aforementioned components of the master budget are prepared effectively. The reason is that

they assist in preparing the balance sheet and income statement for the accounting year

(Melitski and Manoharan 2014). In addition, with the help of budgeted financial statements,

the company could determine the projected incomes expected to be earned over the upcoming

accounting periods. Due to this, the income and expense levels could be determined in the

accounting period.

Part b:

It is critical to engage various business units when there is preparation of a

comprehensive budget. This mandates the requirement of all unit representatives to participate

in the budget development process appropriately. Normally, a budget committee is present to

look after the process, which comprises of some top level executives of the organisation

(Menifield 2017). These personnel offer valuable judgements about the aspects having

association with sales, financing, production and other operating stages. Along with these, the

position of these individuals needs to be proper so that they could provide better information

to their concerned units along with advice on resource needs and opportunities.

There are a number of differences that could be noticed between top-down budget

approach and bottom-up budget approach that the firms could utilise for the preparation of

budgets. In addition, the comparison would help in detecting the suitable budgeting process,

which the organisations could utilise for preparing budget so that its business operations could

be supported adequately. The two above-stated approaches are mainly used in different

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGERIAL ACCOUNTING

business areas that aid the management in the process of decision making regarding its future

operational activities. By using the top-down approach to the budget process, both specific and

general perspectives could be used for evaluating a particular scenario. On the other hand, the

bottom-up approach to the budget process focuses on specific conditions after which it is

shifted to basic features. In addition to this, a particular variation is evident between top-down

budget approach and bottom-up approach of the process of budget, which signifies the

alternative measures undertaken on the part of each process (Miller 2018).

The management of an organisation mainly uses the top-down approach to the budget

process for preventing the budget holders in obtaining an opportunity to involve in the budget

process. Along with this, the top level management provides direct assistance in preparing the

budget. In this case, there has been adequate allocation of resources, which is conducted by

complying with the approval of the top officials. The firm is not engaged to utilise department

heads in this process for determining the budgeted values. With the help of top-down budget

approach, the managers could formulate the budget falling with the limits of the desired

budgeted values. This type of approach is highly advantageous that assists in reducing the lead

time in order to ensure completion of the manufacturing process. This is because the top level

management of an organisation bears the obligation of developing the required budgets. As a

result, it would lead to saving additional time, which could reduce the efforts of the individuals

accountable to conduct day-to-day business operations (Miller-Nobles, Mattison and

Matsumura 2016).

business areas that aid the management in the process of decision making regarding its future

operational activities. By using the top-down approach to the budget process, both specific and

general perspectives could be used for evaluating a particular scenario. On the other hand, the

bottom-up approach to the budget process focuses on specific conditions after which it is

shifted to basic features. In addition to this, a particular variation is evident between top-down

budget approach and bottom-up approach of the process of budget, which signifies the

alternative measures undertaken on the part of each process (Miller 2018).

The management of an organisation mainly uses the top-down approach to the budget

process for preventing the budget holders in obtaining an opportunity to involve in the budget

process. Along with this, the top level management provides direct assistance in preparing the

budget. In this case, there has been adequate allocation of resources, which is conducted by

complying with the approval of the top officials. The firm is not engaged to utilise department

heads in this process for determining the budgeted values. With the help of top-down budget

approach, the managers could formulate the budget falling with the limits of the desired

budgeted values. This type of approach is highly advantageous that assists in reducing the lead

time in order to ensure completion of the manufacturing process. This is because the top level

management of an organisation bears the obligation of developing the required budgets. As a

result, it would lead to saving additional time, which could reduce the efforts of the individuals

accountable to conduct day-to-day business operations (Miller-Nobles, Mattison and

Matsumura 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGERIAL ACCOUNTING

However, this budget approach suffers from a number of drawbacks. One of such

drawbacks includes the non-involvement of the persons detecting the specific expenses, which

could take place while carrying out daily business operations. Due to this, the budget would be

unable to cover up the expectations, as the top individuals would not take into consideration

the expenses to be incurred across the various departments (Noreen, Brewer and Garrison

2014).

The bottom-up approach to the budget process could be defined as a method where

there is chance for the budget holders to be involved in their own budgets. This procedure

seems to have direct involvement with the managers of the departments in order to prepare

the budget in tandem with the requirements and expenses. This approach is considered to be

highly valuable, as the estimated expenses could be accommodated appropriately within the

budget. On the other hand, the bottom-up approach to the budget process suffers from various

limitations, since the expenditures would be handled because of the increased spending target

of the departments. Therefore, the bottom-up approach to the budget process would help in

raising the level of expenses, which is needed for all the departments. The reason is that the

budget would take into account the expenditure requirements of all relevant managers

associated with the departments (Parker and Fleischman 2017).

For both the budgeting approaches, there have been different advantages and

drawbacks, which are observed to have adverse impact on the prepared budgets of the

business entities. By considering all these aspects, the A2 Milk Company Limited would become

beneficial by implementing the top-down approach to the budget process, as the budgets could

However, this budget approach suffers from a number of drawbacks. One of such

drawbacks includes the non-involvement of the persons detecting the specific expenses, which

could take place while carrying out daily business operations. Due to this, the budget would be

unable to cover up the expectations, as the top individuals would not take into consideration

the expenses to be incurred across the various departments (Noreen, Brewer and Garrison

2014).

The bottom-up approach to the budget process could be defined as a method where

there is chance for the budget holders to be involved in their own budgets. This procedure

seems to have direct involvement with the managers of the departments in order to prepare

the budget in tandem with the requirements and expenses. This approach is considered to be

highly valuable, as the estimated expenses could be accommodated appropriately within the

budget. On the other hand, the bottom-up approach to the budget process suffers from various

limitations, since the expenditures would be handled because of the increased spending target

of the departments. Therefore, the bottom-up approach to the budget process would help in

raising the level of expenses, which is needed for all the departments. The reason is that the

budget would take into account the expenditure requirements of all relevant managers

associated with the departments (Parker and Fleischman 2017).

For both the budgeting approaches, there have been different advantages and

drawbacks, which are observed to have adverse impact on the prepared budgets of the

business entities. By considering all these aspects, the A2 Milk Company Limited would become

beneficial by implementing the top-down approach to the budget process, as the budgets could

11MANAGERIAL ACCOUNTING

be developed by the organisation in order to support its future operations. Along with this, this

approach would assist the concerned firm in preparing the needed income and expense levels

to be earned and spent in a specific accounting period.

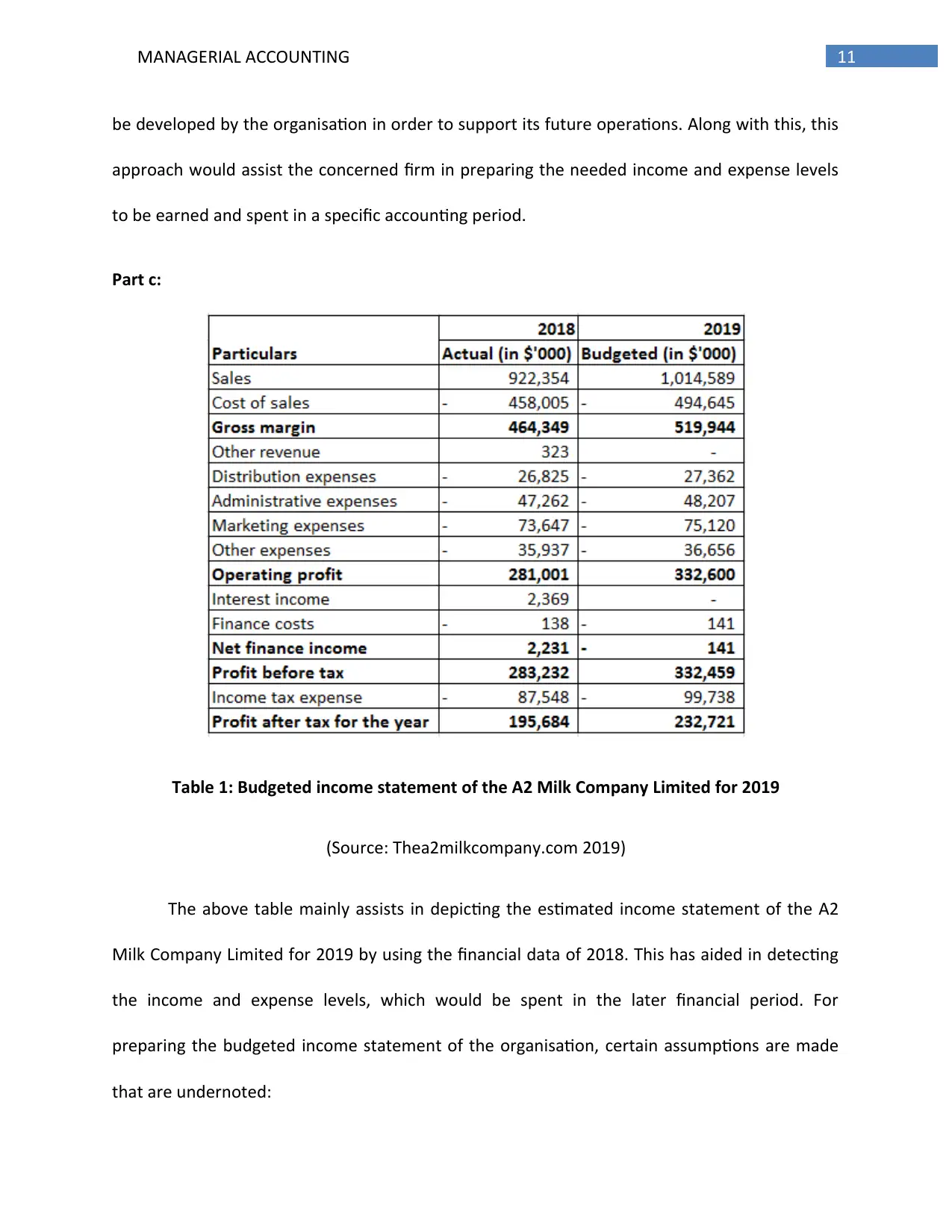

Part c:

Table 1: Budgeted income statement of the A2 Milk Company Limited for 2019

(Source: Thea2milkcompany.com 2019)

The above table mainly assists in depicting the estimated income statement of the A2

Milk Company Limited for 2019 by using the financial data of 2018. This has aided in detecting

the income and expense levels, which would be spent in the later financial period. For

preparing the budgeted income statement of the organisation, certain assumptions are made

that are undernoted:

be developed by the organisation in order to support its future operations. Along with this, this

approach would assist the concerned firm in preparing the needed income and expense levels

to be earned and spent in a specific accounting period.

Part c:

Table 1: Budgeted income statement of the A2 Milk Company Limited for 2019

(Source: Thea2milkcompany.com 2019)

The above table mainly assists in depicting the estimated income statement of the A2

Milk Company Limited for 2019 by using the financial data of 2018. This has aided in detecting

the income and expense levels, which would be spent in the later financial period. For

preparing the budgeted income statement of the organisation, certain assumptions are made

that are undernoted:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.