Costing Analysis for FancyPants and GobStandard

VerifiedAdded on 2019/09/25

|12

|2280

|287

Report

AI Summary

The assignment content discusses Labour Variance, Efficiency Variance, Rate Variance, Sales Volume, Cost of FancyPants, Price Variance, Usage Variance, Reconciliation of Budgeted and actual gross margin for GobStandard and FancyPants. It also provides recommendations to generate gross margin similar to the budgeted one by applying marketing techniques. Additionally, it suggests producing a satchel utilizing waste material to manage costs efficiently and increase profit margin. Furthermore, it raises reservations regarding the appropriateness of linear allocation of non-unit-level activities to individual units, emphasizing the need for activity-based product costing.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

A4away

Performance Measurement and Management

Performance Measurement and Management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

a. How to change costing system.................................................................................................2

Aber plant.....................................................................................................................................2

Falmouth plants 3

b. Cost calculation........................................................................................................................3

Cost of Gobstandard.....................................................................................................................3

Cost of fancypants........................................................................................................................3

a. Cost of GobStandard.............................................................................................................4

b. Cost of fancypants................................................................................................................4

c. Cost of smartphone wallets...................................................................................................4

C. Calculation of profitability under each type of briefcase.........................................................5

Old system....................................................................................................................................5

Alternative system........................................................................................................................5

Recommendations........................................................................................................................5

D. Calculation of agenda item 1....................................................................................................6

Effect on actual performance.......................................................................................................6

Cost of GobStandard....................................................................................................................7

Cost of FancyPants.......................................................................................................................7

Reconciliation of Budgeted and actual gross margin...................................................................8

GobStandard.................................................................................................................................8

FancyPants...................................................................................................................................8

E. Recommendation on producing satchel...................................................................................8

F. Reservations regarding the appropriateness of linear allocation of non-unit-level activities to

individual units................................................................................................................................9

a. How to change costing system.................................................................................................2

Aber plant.....................................................................................................................................2

Falmouth plants 3

b. Cost calculation........................................................................................................................3

Cost of Gobstandard.....................................................................................................................3

Cost of fancypants........................................................................................................................3

a. Cost of GobStandard.............................................................................................................4

b. Cost of fancypants................................................................................................................4

c. Cost of smartphone wallets...................................................................................................4

C. Calculation of profitability under each type of briefcase.........................................................5

Old system....................................................................................................................................5

Alternative system........................................................................................................................5

Recommendations........................................................................................................................5

D. Calculation of agenda item 1....................................................................................................6

Effect on actual performance.......................................................................................................6

Cost of GobStandard....................................................................................................................7

Cost of FancyPants.......................................................................................................................7

Reconciliation of Budgeted and actual gross margin...................................................................8

GobStandard.................................................................................................................................8

FancyPants...................................................................................................................................8

E. Recommendation on producing satchel...................................................................................8

F. Reservations regarding the appropriateness of linear allocation of non-unit-level activities to

individual units................................................................................................................................9

a. How to change costing system

The existing costing system needs to be changed because the extra cost has occurred in both the

plants. The Aber plant produces two type of briefcase in which the structure is similar which can

be used under single setup to reduce the costing per unit. Similarly, Falmouth plant also requires

changing the existing cost system because extra cost is occurring in quality assurance and

employing a number of labors which impacts on the profitability.

Aber plant

There are two types of a briefcase which are produced by Aber plant, namely, GobStandard and

FancyPants. The GobStandard produced standard products, but the new setup is required at every

modification in the briefcase which increases the budget of costing and machine hours of

GobStandard are 4,500 which impacts on the profitability. The second product is FancyPants

which is a customized product which requires high costing due to change in setup for every new

briefcase.

The existing costing system can be changed through using the standard setup in which the

briefcase is prepared in a modified manner, and the modifications are inbuilt in the machine

which is set up by considering the consumers taste and preference which helps to build standard

setup. The standard setup eliminated the costs of new setup for every modification, and by using

single set up the machinery expense will also reduce which helps to increase the profit margin.

The standard modified setup helps to produce FancyPants by selecting the options according to

the consumer’s demand which removes the problem of extra costs in setting new setup. The

single setup will work because the structure of both the products is similar only the appearance is

changed which will be fulfilled by inbuilt the modification in the setup machines and it helps to

The existing costing system needs to be changed because the extra cost has occurred in both the

plants. The Aber plant produces two type of briefcase in which the structure is similar which can

be used under single setup to reduce the costing per unit. Similarly, Falmouth plant also requires

changing the existing cost system because extra cost is occurring in quality assurance and

employing a number of labors which impacts on the profitability.

Aber plant

There are two types of a briefcase which are produced by Aber plant, namely, GobStandard and

FancyPants. The GobStandard produced standard products, but the new setup is required at every

modification in the briefcase which increases the budget of costing and machine hours of

GobStandard are 4,500 which impacts on the profitability. The second product is FancyPants

which is a customized product which requires high costing due to change in setup for every new

briefcase.

The existing costing system can be changed through using the standard setup in which the

briefcase is prepared in a modified manner, and the modifications are inbuilt in the machine

which is set up by considering the consumers taste and preference which helps to build standard

setup. The standard setup eliminated the costs of new setup for every modification, and by using

single set up the machinery expense will also reduce which helps to increase the profit margin.

The standard modified setup helps to produce FancyPants by selecting the options according to

the consumer’s demand which removes the problem of extra costs in setting new setup. The

single setup will work because the structure of both the products is similar only the appearance is

changed which will be fulfilled by inbuilt the modification in the setup machines and it helps to

produce the FancyPants in a customized manner by reducing the costing per product. The unit

costing method is recommended because the method is suitable for the industry in which the

manufacturing is continued, and units are identical. In this case, the structures of both the

products are identified, so unit costing method is recommended which helps to reduce the non-

valuable cost by managing the cost per unit

Falmouth plant

Under this plant specialized product is produced, namely, Smartphone wallets which are

produced through labors without any setup. The quality is assured by assembly line workers

because the material is manufactured by local manufacturers. The existing costing system can be

changed by selecting the single manufacturer with the least cost and best quality among the

various manufacturers which helps to reduce the time and cost on checking the quality with the

production of specialized products. Single setup for assembling helps to reduce the cost and time

of labors by reducing the number of labors required which impacts on the profitability and helps

to provide standard quality products. The single setup helps to improve the quality of the product

which can't be achieved through handmade work.

b. Cost calculation

Particular Cost of Gobstandard Cost of fancypants Cost of smartphone

wallets

Production

(Units)

9,000 2,000 3,000

costing method is recommended because the method is suitable for the industry in which the

manufacturing is continued, and units are identical. In this case, the structures of both the

products are identified, so unit costing method is recommended which helps to reduce the non-

valuable cost by managing the cost per unit

Falmouth plant

Under this plant specialized product is produced, namely, Smartphone wallets which are

produced through labors without any setup. The quality is assured by assembly line workers

because the material is manufactured by local manufacturers. The existing costing system can be

changed by selecting the single manufacturer with the least cost and best quality among the

various manufacturers which helps to reduce the time and cost on checking the quality with the

production of specialized products. Single setup for assembling helps to reduce the cost and time

of labors by reducing the number of labors required which impacts on the profitability and helps

to provide standard quality products. The single setup helps to improve the quality of the product

which can't be achieved through handmade work.

b. Cost calculation

Particular Cost of Gobstandard Cost of fancypants Cost of smartphone

wallets

Production

(Units)

9,000 2,000 3,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

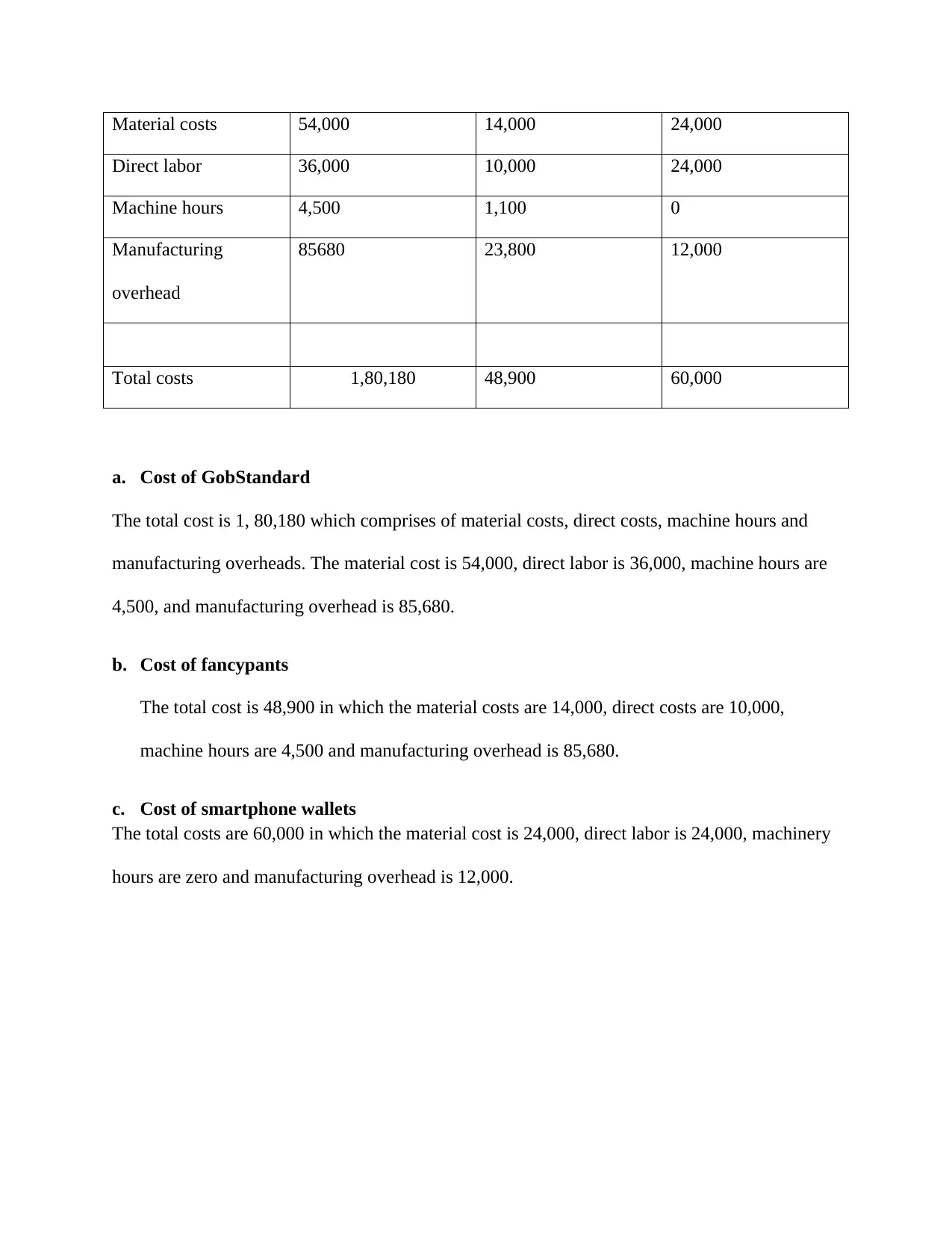

Material costs 54,000 14,000 24,000

Direct labor 36,000 10,000 24,000

Machine hours 4,500 1,100 0

Manufacturing

overhead

85680 23,800 12,000

Total costs 1,80,180 48,900 60,000

a. Cost of GobStandard

The total cost is 1, 80,180 which comprises of material costs, direct costs, machine hours and

manufacturing overheads. The material cost is 54,000, direct labor is 36,000, machine hours are

4,500, and manufacturing overhead is 85,680.

b. Cost of fancypants

The total cost is 48,900 in which the material costs are 14,000, direct costs are 10,000,

machine hours are 4,500 and manufacturing overhead is 85,680.

c. Cost of smartphone wallets

The total costs are 60,000 in which the material cost is 24,000, direct labor is 24,000, machinery

hours are zero and manufacturing overhead is 12,000.

Direct labor 36,000 10,000 24,000

Machine hours 4,500 1,100 0

Manufacturing

overhead

85680 23,800 12,000

Total costs 1,80,180 48,900 60,000

a. Cost of GobStandard

The total cost is 1, 80,180 which comprises of material costs, direct costs, machine hours and

manufacturing overheads. The material cost is 54,000, direct labor is 36,000, machine hours are

4,500, and manufacturing overhead is 85,680.

b. Cost of fancypants

The total cost is 48,900 in which the material costs are 14,000, direct costs are 10,000,

machine hours are 4,500 and manufacturing overhead is 85,680.

c. Cost of smartphone wallets

The total costs are 60,000 in which the material cost is 24,000, direct labor is 24,000, machinery

hours are zero and manufacturing overhead is 12,000.

C. Calculation of profitability under each type of briefcase

Old system

Under the old system, the FancyPants is having sales margin of 2,400 which is adverse price

variance whereas the GobStandard is having favorable sales margin volume of 496. The price

variance of GobStandard shows the favorable outcome of 4,250 and usage variance shows the

favorable outcome of 3,000 whereas the FancyPants shows the adverse price variance of 420 and

usage variance of 700 which shows that the profitability of GobStandard is better than the

FancyPants because the actual performance is higher than the estimated performance. So the

profitability of GobStandard is favorable than the profitability of FancyPants.

Alternative system

Under the alternative system, the profit margin of GobStandard is 11.3% in September 2016

which includes various expenses such as direct labor cost, direct material cost, and

manufacturing overhead. The profit margin of FancyPants is 40.25%, and the expenses include

direct labor cost, direct material cost, and manufacturing overhead. The profit margin of

Smartfone wallet is 20%, and the expenses include direct labor cost, direct material cost, and

manufacturing overhead. The FancyPants is having highest profit margin among the three

products because the selling price of the FancyPants is highest among all the products.

Recommendations

The company can improve its profitability by adopting the various marketing strategies which

help to promote the brand in the eyes of the consumers. The marketing activities include

advertisement, discounts, offers, promotional events and others. Another option is to improve the

Old system

Under the old system, the FancyPants is having sales margin of 2,400 which is adverse price

variance whereas the GobStandard is having favorable sales margin volume of 496. The price

variance of GobStandard shows the favorable outcome of 4,250 and usage variance shows the

favorable outcome of 3,000 whereas the FancyPants shows the adverse price variance of 420 and

usage variance of 700 which shows that the profitability of GobStandard is better than the

FancyPants because the actual performance is higher than the estimated performance. So the

profitability of GobStandard is favorable than the profitability of FancyPants.

Alternative system

Under the alternative system, the profit margin of GobStandard is 11.3% in September 2016

which includes various expenses such as direct labor cost, direct material cost, and

manufacturing overhead. The profit margin of FancyPants is 40.25%, and the expenses include

direct labor cost, direct material cost, and manufacturing overhead. The profit margin of

Smartfone wallet is 20%, and the expenses include direct labor cost, direct material cost, and

manufacturing overhead. The FancyPants is having highest profit margin among the three

products because the selling price of the FancyPants is highest among all the products.

Recommendations

The company can improve its profitability by adopting the various marketing strategies which

help to promote the brand in the eyes of the consumers. The marketing activities include

advertisement, discounts, offers, promotional events and others. Another option is to improve the

costing system which helps to reduce the cost per product, and it enables to increase the

profitability of the company. The effective costing system helps to eliminate the non-valuable

costs which help to utilize the funds in the most efficient and effective manner which is the aim

of every organization.

D. Calculation of agenda item 1

Effect on actual performance

The two items are discussed in the Agenda 1, namely, FancyPants and GobStandard. The

material variance includes price variance and usage variance. The material usage variance is

calculated by multiplying the actual quantity* standard priceless standard quantity*standard

price. The price variance is calculated by deducting the (selling price less actual price)* actual

quantity. The efficiency variance is calculated by deducting the actual unit from the standard unit

then multiplies with the standard cost. The rate variance is calculated by deducting the actual

price from the expected price then multiplies with the actual quantity. The effect of price

variance in GobStandard is positive because the actual performance is higher than the standard

performance which includes a purchase of lower quantity than the actual price, adequate price

negotiation by the procurement team; receive purchase discounts by the company which leads to

the overall cost effective procurement by the company. The Usage variance is also having the

positive impact on the actual performance because the performance is higher than the standard

performance (DRURY et al., 2013). The price variance of FancyPants is having adverse impact

because the actual price is less than the standard price which it includes the hike in the market

price of materials, purchase of material at higher quantity, increment in the bargaining power of

suppliers, inefficient purchase by the procurement department (Roberts et al., 2014). The Labour

profitability of the company. The effective costing system helps to eliminate the non-valuable

costs which help to utilize the funds in the most efficient and effective manner which is the aim

of every organization.

D. Calculation of agenda item 1

Effect on actual performance

The two items are discussed in the Agenda 1, namely, FancyPants and GobStandard. The

material variance includes price variance and usage variance. The material usage variance is

calculated by multiplying the actual quantity* standard priceless standard quantity*standard

price. The price variance is calculated by deducting the (selling price less actual price)* actual

quantity. The efficiency variance is calculated by deducting the actual unit from the standard unit

then multiplies with the standard cost. The rate variance is calculated by deducting the actual

price from the expected price then multiplies with the actual quantity. The effect of price

variance in GobStandard is positive because the actual performance is higher than the standard

performance which includes a purchase of lower quantity than the actual price, adequate price

negotiation by the procurement team; receive purchase discounts by the company which leads to

the overall cost effective procurement by the company. The Usage variance is also having the

positive impact on the actual performance because the performance is higher than the standard

performance (DRURY et al., 2013). The price variance of FancyPants is having adverse impact

because the actual price is less than the standard price which it includes the hike in the market

price of materials, purchase of material at higher quantity, increment in the bargaining power of

suppliers, inefficient purchase by the procurement department (Roberts et al., 2014). The Labour

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

variance of both the products shows the lower productivity of direct labor as compared to the

standard performance during the particular period of time which includes recruitment of low

skilled labors, decrease in the motivation and morale of labors and others (Peng et al., 2015).

Cost of GobStandard

Material variance

Price variance- (SP-AP)*AQ

£4,250

Usage variance- (AQ-SQ)*SP

£3,000

Labour variance

Efficiency variance- (AU-SU)*SC

£1,000

Rate variance- (AP-EP)*AQ

£750

Sales volume - £496

Cost of FancyPants

Price variance- £420

standard performance during the particular period of time which includes recruitment of low

skilled labors, decrease in the motivation and morale of labors and others (Peng et al., 2015).

Cost of GobStandard

Material variance

Price variance- (SP-AP)*AQ

£4,250

Usage variance- (AQ-SQ)*SP

£3,000

Labour variance

Efficiency variance- (AU-SU)*SC

£1,000

Rate variance- (AP-EP)*AQ

£750

Sales volume - £496

Cost of FancyPants

Price variance- £420

Usage variance-£700

Labour variance

Efficiency variance- £2,000

Rate variance-£600

Sales volume- £2,400

Reconciliation of Budgeted and actual gross margin

GobStandard

The actual margin of GobStandard is 496, and expected margin is 11.3%

FancyPants

The actual margin of FancyPants is 2400, and the budgeted margin is 40.25%

The recommendations in the c part help to generate the gross margin similar to the budgeted

gross margin by applying the various marketing techniques which help to generate high-profit

margin by promoting the brand in the eyes of the consumers. The actual margin is less than the

budgeted gross profit margin which can be achieved by applying the recommendations. The

marketing activities such as an advertisement, discount and others help to generate higher

revenue which enables to achieve the budgeted gross margin (Öker et al., 2016).

E. Recommendation on producing satchel

The company should produce satchel because the wasting twenty percent of material which leads

to manage the cost efficiently. The waste material can be used for making the Satchel which

helps to utilize the waste material in the most efficiency and effective manner which help to

Labour variance

Efficiency variance- £2,000

Rate variance-£600

Sales volume- £2,400

Reconciliation of Budgeted and actual gross margin

GobStandard

The actual margin of GobStandard is 496, and expected margin is 11.3%

FancyPants

The actual margin of FancyPants is 2400, and the budgeted margin is 40.25%

The recommendations in the c part help to generate the gross margin similar to the budgeted

gross margin by applying the various marketing techniques which help to generate high-profit

margin by promoting the brand in the eyes of the consumers. The actual margin is less than the

budgeted gross profit margin which can be achieved by applying the recommendations. The

marketing activities such as an advertisement, discount and others help to generate higher

revenue which enables to achieve the budgeted gross margin (Öker et al., 2016).

E. Recommendation on producing satchel

The company should produce satchel because the wasting twenty percent of material which leads

to manage the cost efficiently. The waste material can be used for making the Satchel which

helps to utilize the waste material in the most efficiency and effective manner which help to

increase the profit margin and increase new product in line which broadens the line of products

offered to the consumers. The wasting of twenty percent raw material impacts on the cost

management of resources which can be managed by utilizing the waste material to produce the

satchel. The material cost is zero because the scrap will be considered as the raw material and the

production will be done in the Aber plant, so the estimated sales per unit are equal to the cost

incurred in producing one product. It may not produce the higher profit margin in the beginning,

but once the product is correctly positioned then, it will help to contribute to the profit margin of

the company. The main reason for producing the satchel is proper utilization of waste material by

producing the new product which also helps in providing a new product to the consumers. The

production of satchel may attract the consumers with the low budget which helps to attract the

new consumers by utilizing the waste material in a most efficient and effective manner. The

waste management is necessary for the company because it helps to utilize the resources and

manage the costing system effectively (De Waal et al., 2013).

F. Reservations regarding the appropriateness of linear allocation of

non-unit-level activities to individual units

The non-unit level activities are defined as the activities which are not incurred at every stage,

but the cost related to these activities varies with the number of units produced. The reservation

regarding the packaging and dispatching is required because these are the non-unit level

activities but it takes more time, and it is considered as individual units. The activity based

product costing must be done which helps to assign the cost to the activities (Laonapaporn et al.,

2014). The reservation to the packaging and dispatch helps to calculate the cost of time required

in packaging and dispatching per product which help to allocate the cost of each product in a

offered to the consumers. The wasting of twenty percent raw material impacts on the cost

management of resources which can be managed by utilizing the waste material to produce the

satchel. The material cost is zero because the scrap will be considered as the raw material and the

production will be done in the Aber plant, so the estimated sales per unit are equal to the cost

incurred in producing one product. It may not produce the higher profit margin in the beginning,

but once the product is correctly positioned then, it will help to contribute to the profit margin of

the company. The main reason for producing the satchel is proper utilization of waste material by

producing the new product which also helps in providing a new product to the consumers. The

production of satchel may attract the consumers with the low budget which helps to attract the

new consumers by utilizing the waste material in a most efficient and effective manner. The

waste management is necessary for the company because it helps to utilize the resources and

manage the costing system effectively (De Waal et al., 2013).

F. Reservations regarding the appropriateness of linear allocation of

non-unit-level activities to individual units

The non-unit level activities are defined as the activities which are not incurred at every stage,

but the cost related to these activities varies with the number of units produced. The reservation

regarding the packaging and dispatching is required because these are the non-unit level

activities but it takes more time, and it is considered as individual units. The activity based

product costing must be done which helps to assign the cost to the activities (Laonapaporn et al.,

2014). The reservation to the packaging and dispatch helps to calculate the cost of time required

in packaging and dispatching per product which help to allocate the cost of each product in a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

most efficient and effective manner. When the packaging and dispatching are considered as an

individual unit it helps to apply the effective costing system. The effective costing system

impacts on the profitability of the company. The packaging and dispatching are the non-unit

activities because the variant time is required for every product which creates the improper

allocation of resources, so the assignment of packaging and dispatching as individual activities

helps to determine the cost of time used in the particular product.

individual unit it helps to apply the effective costing system. The effective costing system

impacts on the profitability of the company. The packaging and dispatching are the non-unit

activities because the variant time is required for every product which creates the improper

allocation of resources, so the assignment of packaging and dispatching as individual activities

helps to determine the cost of time used in the particular product.

References

De Waal, A. (2013). Strategic Performance Management: A managerial and behavioral

approach. Palgrave Macmillan.

Laonapaporn, B., & Phanthunane, P. (2014). Activity based costing system of continuous

ambulatory peritoneal dialysis under the Universal Coverage Scheme in Thailand. BMC Public

Health, 14(Suppl 1), P7.

Öker, F., & Adıgüzel, H. (2016). Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), 39-56.

Peng, Y. (2015). The application of activity based costing in cost accounting system of electric

power enterprises. Automation & Instrumentation, 11, 081.

Roberts, M., & Russo, R. (2014). A student's guide to analysis of variance. Routledge.

DRURY, C. M. (2013). Management and cost accounting. Springer.

De Waal, A. (2013). Strategic Performance Management: A managerial and behavioral

approach. Palgrave Macmillan.

Laonapaporn, B., & Phanthunane, P. (2014). Activity based costing system of continuous

ambulatory peritoneal dialysis under the Universal Coverage Scheme in Thailand. BMC Public

Health, 14(Suppl 1), P7.

Öker, F., & Adıgüzel, H. (2016). Time‐driven activity‐based costing: An implementation in a

manufacturing company. Journal of Corporate Accounting & Finance, 27(3), 39-56.

Peng, Y. (2015). The application of activity based costing in cost accounting system of electric

power enterprises. Automation & Instrumentation, 11, 081.

Roberts, M., & Russo, R. (2014). A student's guide to analysis of variance. Routledge.

DRURY, C. M. (2013). Management and cost accounting. Springer.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.